Homeowners across Seattle, Bellevue, Redmond, and Kirkland are constantly evaluating their mortgage options as market conditions shift. Whether you purchased during a high-rate period or simply want to access your home's equity, understanding when and how to refinance home loans can unlock substantial financial benefits. With property values in the Greater Seattle area continuing to appreciate, many homeowners now have significant equity that makes refinancing a strategic opportunity worth exploring. This comprehensive guide breaks down everything you need to know about the refinancing process, from timing considerations to qualifying with stock compensation.

Understanding When to Refinance Home Loans

The decision to refinance home mortgages hinges on multiple factors beyond just interest rates. While securing a lower rate remains the most common motivation, homeowners should evaluate their complete financial picture before proceeding.

Key timing indicators include:

- Interest rates have dropped at least 0.75% below your current rate

- Your credit score has improved by 50+ points since origination

- You need to eliminate private mortgage insurance (PMI)

- Cash flow requirements have changed significantly

- You want to consolidate high-interest debt

Market conditions in 2026 present unique opportunities for Seattle homeowners. Tech professionals at companies like Amazon, Microsoft, and Google often receive substantial stock compensation that wasn't available when they first purchased. This additional documented income can qualify you for better terms when you refinance your existing loan.

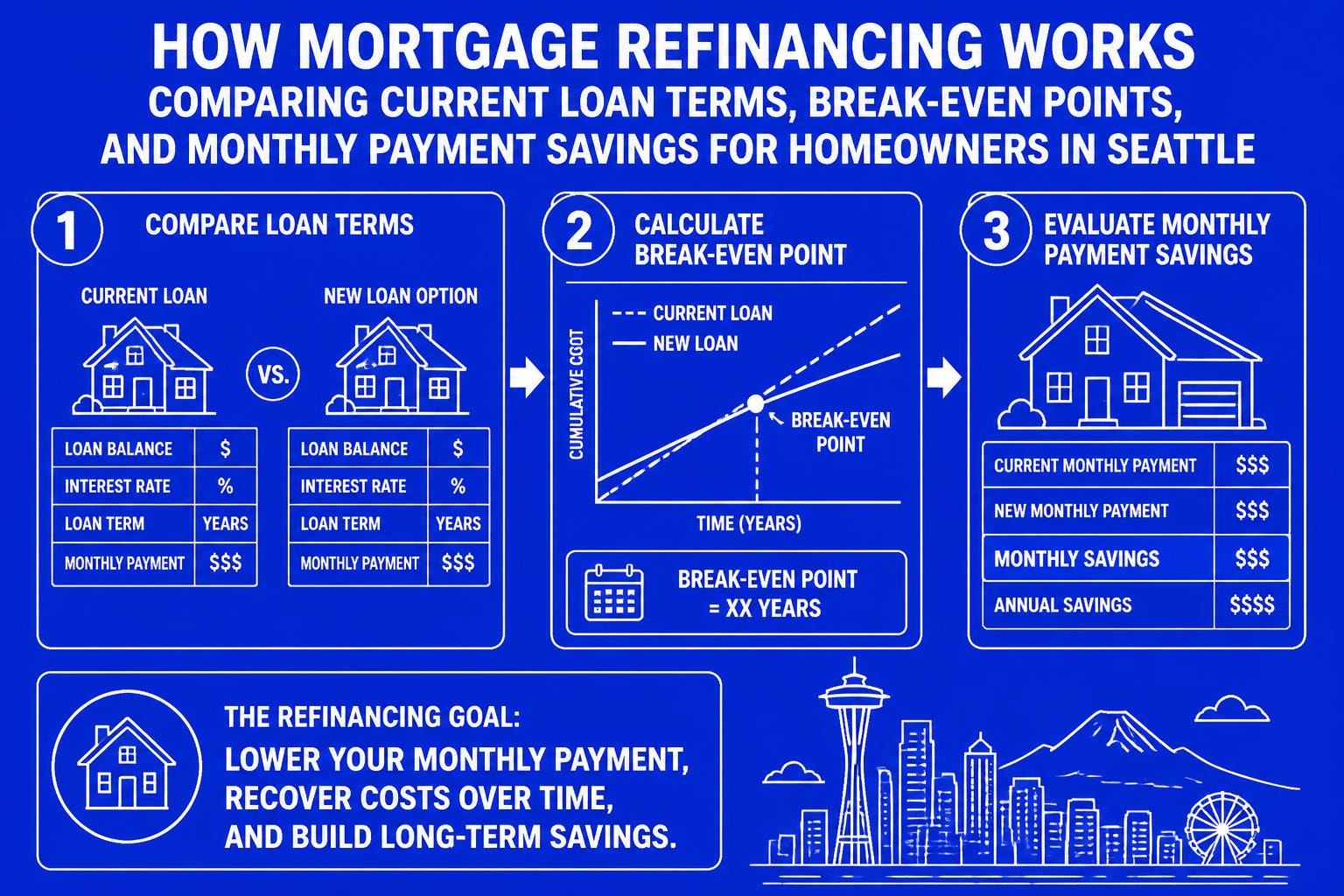

Calculating Your Break-Even Point

Every refinance involves closing costs, typically ranging from 2% to 5% of the loan amount. Understanding your break-even point determines whether refinancing makes financial sense.

| Loan Amount | Closing Costs (3%) | Monthly Savings | Break-Even (Months) |

|---|---|---|---|

| $500,000 | $15,000 | $250 | 60 |

| $750,000 | $22,500 | $400 | 56 |

| $1,000,000 | $30,000 | $575 | 52 |

If you plan to stay in your Seattle home beyond the break-even period, refinancing typically provides long-term value. For homeowners in rapidly appreciating neighborhoods like Shoreline or Mill Creek, the combination of lower rates and increased equity creates compelling refinance scenarios.

Building a network of trusted advisors helps ensure you're making informed decisions throughout the refinancing process.

Types of Refinance Options Available

Different refinancing strategies serve distinct financial goals. Choosing the right type depends on your current situation and long-term objectives.

Rate-and-Term Refinance

This straightforward option focuses on securing better loan terms without changing your principal balance. Homeowners use rate-and-term refinancing to:

- Lower their monthly payment through reduced interest rates

- Shorten loan terms from 30 to 15 years

- Switch from adjustable-rate to fixed-rate mortgages

- Remove FHA mortgage insurance requirements

Rate-and-term refinancing works exceptionally well for Seattle tech professionals who've seen income growth through RSUs and want to accelerate their mortgage payoff timeline without changing their monthly budget significantly.

Cash-Out Refinance

When you need to access home equity for renovations, investments, or debt consolidation, cash-out refinancing offers a strategic solution. This option replaces your current mortgage with a larger loan, providing the difference in cash.

Common uses for cash-out proceeds:

- Major home improvements that increase property value

- Eliminating high-interest credit card debt

- Funding investment property down payments

- Covering education expenses

- Starting or expanding a business

Lenders typically allow you to borrow up to 80% of your home's value, though requirements vary based on property type and credit profile. In appreciating markets like Lynnwood and Lake Forest Park, homeowners often discover they have substantial equity available even after just a few years of ownership.

Streamline Refinance Programs

FHA and VA streamline refinances offer simplified processes for existing borrowers with these loan types. Benefits include reduced documentation requirements, no appraisal in many cases, and faster processing times.

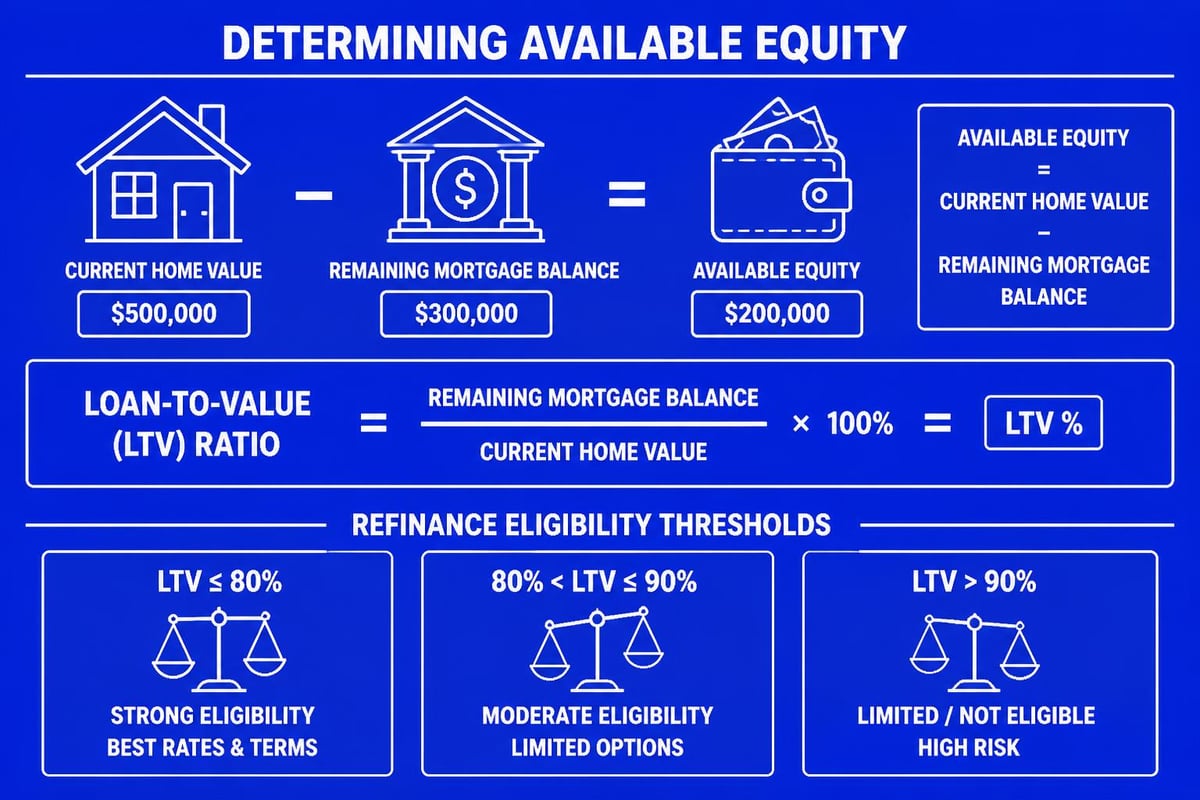

Equity Requirements and Loan-to-Value Ratios

Understanding how much equity you need to refinance determines your available options and potential terms.

Most conventional refinances require at least 20% equity (80% LTV) to avoid PMI. However, several programs accommodate lower equity positions:

| Refinance Type | Minimum Equity | Maximum LTV |

|---|---|---|

| Conventional Rate-and-Term | 5% | 95% |

| Conventional Cash-Out | 20% | 80% |

| FHA Streamline | Varies | 97.75% |

| VA IRRRL | 0% | 100%+ |

Seattle's strong appreciation rates mean many homeowners reach 20% equity faster than national averages. Properties in desirable neighborhoods like Everett or Bellevue often appreciate 5-8% annually, accelerating equity growth beyond principal paydown.

Qualifying with Stock Compensation and Bonus Income

Tech professionals throughout the Seattle area face unique challenges when documenting income for mortgage refinancing. RSUs, stock options, and performance bonuses require specialized underwriting approaches that many lenders don't offer.

Documentation Requirements for Complex Income

To refinance home loans using equity compensation, you'll need:

- Two years of W-2s showing consistent bonus/stock income

- Recent pay stubs reflecting year-to-date equity compensation

- Award letters or vesting schedules for unvested RSUs

- Employer verification of ongoing compensation structure

Advanced underwriting can qualify restricted stock units before they vest, significantly increasing your borrowing power. For conventional loans with competitive terms, documenting all income sources properly makes the difference between approval and denial.

Maximizing Qualifying Income

Lenders calculate qualifying income differently based on compensation type. Bonuses and RSUs typically require two-year averages, while base salary qualifies dollar-for-dollar. Strategic timing of your refinance application around vesting dates and bonus payments can optimize your debt-to-income ratio.

The Refinance Process Timeline

Understanding the complete refinance process helps you prepare appropriately and avoid delays. While some lenders advertise quick closings, realistic timelines account for appraisals, title work, and underwriting.

Standard refinance timeline:

- Application and Initial Review (Days 1-3): Submit application with income documentation, credit authorization, and property information

- Appraisal Ordered (Days 3-5): Lender orders property valuation to confirm current value

- Processing and Underwriting (Days 7-20): Documentation review, income verification, title search

- Clear to Close (Days 18-25): Final underwriting approval and closing disclosure issued

- Closing (Days 21-30): Sign loan documents and await funding

With experienced guidance and advanced underwriting capabilities, some refinances close in as few as 9 business days. However, typical home loan approval timeframes depend on documentation complexity and appraisal scheduling.

Avoiding Common Processing Delays

Delays often stem from preventable issues. Homeowners can expedite their refinance by:

- Providing complete documentation upfront

- Responding quickly to underwriter requests

- Avoiding major credit changes during processing

- Maintaining employment consistency

- Keeping adequate funds in verified accounts

Working with a trusted mortgage broker in Seattle who understands local market conditions and appraisal challenges helps navigate potential obstacles before they cause delays.

Cost Analysis and Fee Structures

Refinancing involves multiple costs that homeowners should understand before committing. Transparency around fees enables accurate comparison between lenders and loan programs.

Typical Refinance Closing Costs

| Fee Category | Typical Range | Description |

|---|---|---|

| Origination/Points | 0-2% | Lender compensation and rate buydown |

| Appraisal | $500-$800 | Professional property valuation |

| Title/Escrow | $1,000-$2,500 | Title search, insurance, closing services |

| Recording Fees | $200-$400 | County recording charges |

| Credit Report | $30-$100 | Credit bureau inquiry fees |

Some lenders offer "no-closing-cost" refinances, but these typically involve slightly higher interest rates that recoup costs over time. When evaluating offers, calculate both immediate out-of-pocket expenses and long-term interest paid.

What to watch for when refinancing includes understanding how different fee structures impact your total cost of borrowing over your expected ownership period.

How Often You Can Refinance

There's no legal limit on refinancing frequency, though practical and financial considerations create natural constraints. Lender-imposed waiting periods vary by loan type and situation.

Standard waiting periods:

- Conventional rate-and-term: No waiting period after closing

- Conventional cash-out: 6 months from most recent closing

- FHA refinance: 210 days from previous closing plus 6 payments made

- VA refinance: 210 days from previous closing

Frequent refinancing rarely makes financial sense due to closing costs and break-even calculations. However, in rapidly changing rate environments or when property values surge, strategic refinancing every 2-3 years can optimize your loan structure.

Seattle homeowners in appreciating neighborhoods may refinance to access growing equity or eliminate PMI sooner than originally anticipated. Each scenario requires individual analysis of costs versus benefits.

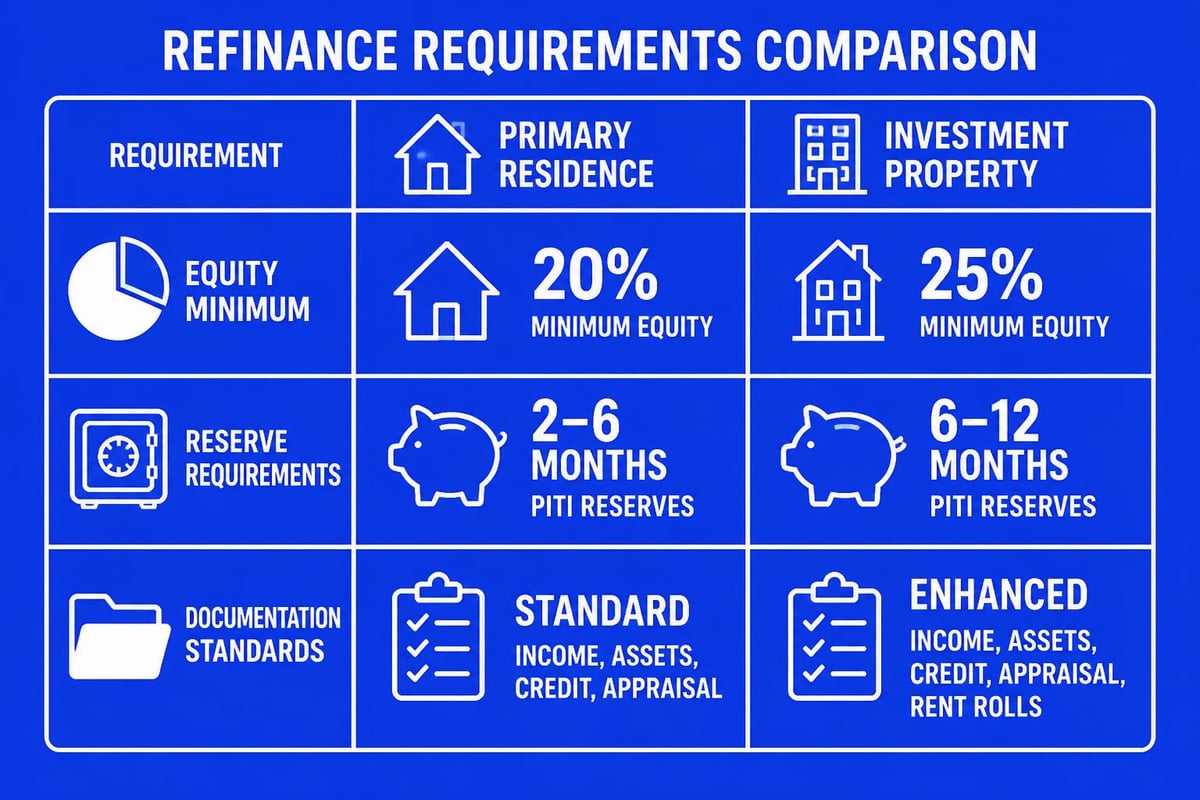

Special Considerations for Investment Properties

Refinancing investment properties follows stricter guidelines than primary residences. Lenders view rental properties as higher risk, resulting in different requirements.

Investment property refinance typically requires:

- 25% minimum equity (75% maximum LTV)

- Higher credit scores (typically 680-700 minimum)

- Larger cash reserves (6-12 months PITI)

- Property income documentation if used for qualifying

For Seattle-area investors managing multiple properties, conventional loans for investment properties offer the flexibility to optimize each property's financing independently. Rate differences between owner-occupied and investment properties typically range from 0.5% to 0.75%.

Credit Score Impact and Optimization

Your credit profile significantly influences refinance approval and rate pricing. Understanding how refinancing affects credit helps you time applications strategically.

Short-Term Credit Effects

Refinancing temporarily impacts credit scores through:

- Hard inquiry (5-10 point decrease)

- Reduced average account age

- Temporary utilization changes

These effects typically resolve within 3-6 months. The long-term benefits of lower monthly payments and faster principal reduction outweigh temporary score fluctuations.

Rate pricing tiers (conventional loans):

| Credit Score | Rate Adjustment |

|---|---|

| 780+ | Best available rates |

| 760-779 | +0.125% |

| 740-759 | +0.25% |

| 720-739 | +0.375% |

| 700-719 | +0.50% |

| 680-699 | +0.75% |

Improving your credit score by even 20 points before applying can save thousands over your loan term. For homeowners near threshold scores, delaying refinancing 2-3 months to improve credit often produces better overall results.

Property Appraisal Considerations

The appraisal determines your available refinance options by establishing current market value. Seattle's competitive market creates unique appraisal dynamics that homeowners should understand.

Appraisers evaluate:

- Recent comparable sales within 0.5 miles

- Property condition and improvements

- Neighborhood trends and desirability

- Market conditions and absorption rates

In rapidly appreciating areas like Mill Creek or Shoreline, appraisals sometimes lag market reality. Providing appraisers with recent comparable sales and documentation of improvements helps ensure accurate valuations.

If your appraisal comes in lower than expected, options include:

- Challenging the appraisal with additional comparables

- Making a larger down payment to achieve target LTV

- Waiting 3-6 months for additional appreciation

- Seeking alternative valuation methods when available

Debt-to-Income Requirements and Strategies

Lenders evaluate your ability to repay through debt-to-income (DTI) ratio calculations. Understanding these requirements helps you prepare effectively.

Maximum DTI ratios for refinancing:

- Conventional loans: 50% (some investors allow higher with compensating factors)

- FHA loans: 56.9% with qualifying credit/reserves

- VA loans: No explicit maximum (residual income method)

- Jumbo loans: 43-45% typically

DTI calculation formula:

Total monthly debt obligations ÷ gross monthly income = DTI percentage

Seattle tech professionals often have excellent DTI ratios due to strong base salaries, but large stock vesting events can temporarily inflate income calculations. Consistent documentation across multiple years provides the most reliable qualifying approach.

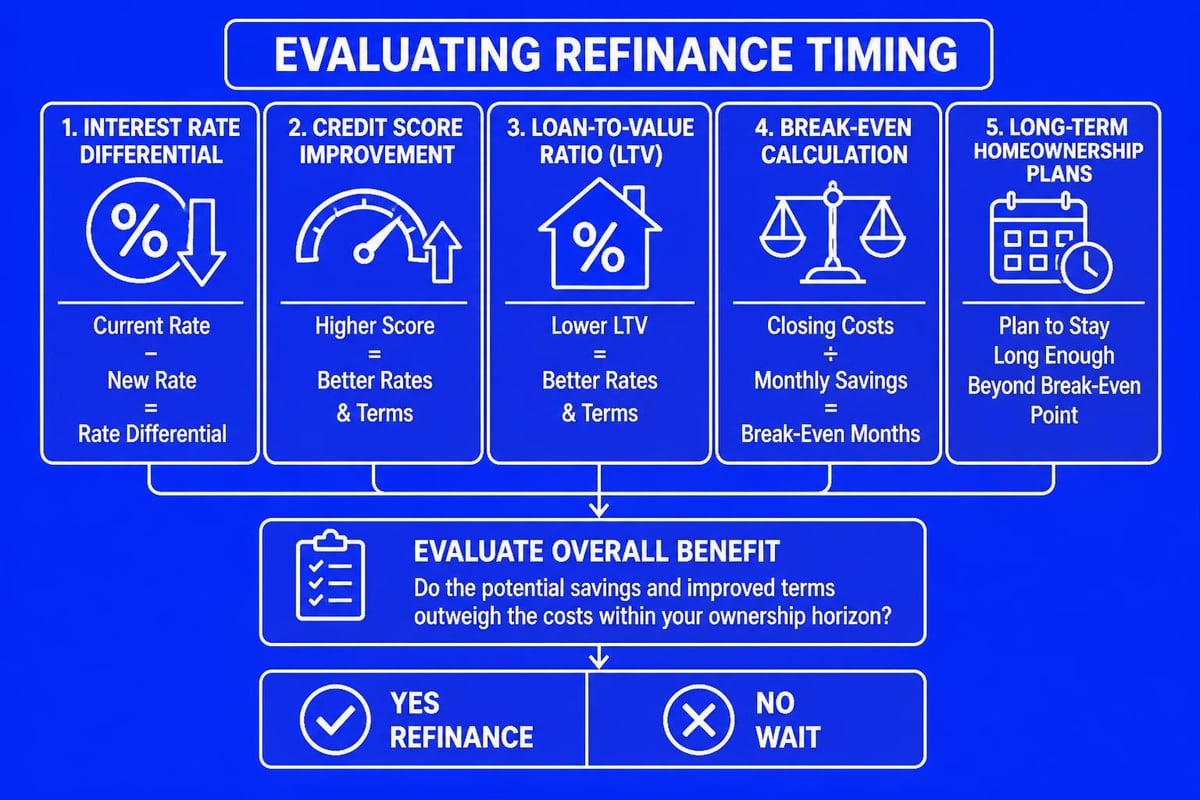

Rate Lock Strategies and Market Timing

Interest rate volatility requires strategic rate lock decisions. Understanding when and how to lock your rate protects against unfavorable market movements.

Rate locks typically range from 15 to 60 days, with longer locks carrying higher costs. For standard refinances, 30-day locks balance protection and pricing. Complex transactions requiring extended processing may warrant 45-60 day locks despite premium pricing.

Rate lock considerations:

- Lock when you have loan approval and appraisal ordered

- Consider float-down options in declining rate environments

- Understand extension fees if closing delays occur

- Monitor market trends but avoid excessive speculation

Market timing for refinancing depends more on personal circumstances than attempting to predict rate bottoms. When refinancing makes financial sense based on your break-even analysis, proceeding promptly reduces exposure to rate increases.

Jumbo Loan Refinancing in Seattle

Seattle's high property values mean many homeowners require jumbo financing when they refinance home mortgages above conforming loan limits ($806,500 in 2026 for most counties).

Jumbo refinancing requires:

- Stronger credit profiles (typically 700+ minimum, 740+ for best pricing)

- Lower maximum DTI ratios (43-45%)

- Larger reserves (6-12 months PITI)

- More stringent income documentation

However, jumbo rates have become increasingly competitive. For well-qualified borrowers, jumbo refinance rates often match or barely exceed conforming rates. Seattle's competitive lending market benefits homeowners seeking jumbo refinancing for properties in Bellevue, Kirkland, and other high-value areas.

Escrow and Tax Considerations

Refinancing creates new escrow accounts and may affect your property tax payment timing. Understanding these transitions prevents payment confusion.

When you refinance:

- Your old escrow account closes (refund issued 20-30 days after closing)

- New escrow account establishes with initial deposit at closing

- Property tax and insurance payment responsibility transfers

- First new payment typically due 30-45 days after closing

The overlap period sometimes creates cash flow considerations, particularly for homeowners with large annual tax bills. Planning for these transitions ensures smooth financial management during the refinance process.

Mortgage interest deduction changes under tax law mean refinancing for debt consolidation may affect your tax situation differently than traditional refinancing. Consulting with tax professionals about refinance implications provides comprehensive financial planning.

ARM to Fixed-Rate Conversions

Homeowners with adjustable-rate mortgages often refinance into fixed-rate products as adjustment periods approach. This strategy provides payment stability and protection against future rate increases.

Converting from ARM to fixed makes sense when:

- Your initial fixed period nears expiration

- You plan extended homeownership (5+ years)

- Current fixed rates approximate your ARM rate

- You value payment predictability over potential savings

Seattle homeowners who purchased with 5/1 or 7/1 ARMs in 2019-2021 may find current fixed rates attractive compared to potential ARM adjustments. Evaluating your adjustment caps and index margins helps determine optimal conversion timing.

Refinancing your home strategically unlocks equity, reduces monthly payments, and optimizes your overall financial position in Seattle's dynamic real estate market. Whether you're looking to lower your rate, access cash for improvements, or adjust your loan term, understanding the complete refinance landscape empowers confident decisions. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle-area homeowners navigate refinancing with clarity and expertise, specializing in complex income scenarios for tech professionals and offering closing timelines as fast as 9 business days. Reach out today to explore your refinance options with a trusted local expert.