Dreaming of owning your first home in Seattle or the surrounding areas? You’re not alone. 2026 is shaping up to be a pivotal year for those seeking assistance for first time homebuyers.

Navigating the path to homeownership can feel overwhelming, especially in a competitive market like Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. This guide is designed to simplify the process and provide you with a clear, step-by-step roadmap.

Inside, you’ll find everything you need to know about eligibility requirements, financial assistance programs, application steps, local market tips, and answers to frequently asked questions. Our aim is to equip you with the knowledge and confidence to make your first home purchase a reality in 2026.

Whether you’re a recent graduate, a growing family, or a long-time renter, follow this guide to start your journey toward homeownership.

Understanding First-Time Homebuyer Assistance in 2026

Navigating assistance for first time homebuyers in Seattle and the surrounding region can feel complex, but understanding the basics is the first step. Whether you are a renter in Shoreline, a recent graduate in Lynnwood, or relocating to Everett, knowing your options puts you in control of your homeownership journey.

What Qualifies as a First-Time Homebuyer?

The definition of a first-time homebuyer is broader than many realize. According to HUD and Washington State guidelines, you qualify if you have not owned a principal residence in the past three years. This means many Seattle renters, recent college graduates in Lynnwood, or families relocating to Mill Creek may all be considered first-time buyers.

There are exceptions to keep in mind. For example, if you owned a home but sold it over three years ago, you likely qualify again. Special rules may also apply for single parents or displaced homemakers. Understanding these nuances is essential when seeking assistance for first time homebuyers.

Types of Assistance Available

There are several forms of assistance for first time homebuyers in Seattle and the surrounding cities. These include:

- Down payment grants and forgivable loans that help reduce your upfront costs.

- Closing cost assistance to cover fees at settlement.

- Tax credits like the Mortgage Credit Certificate program to lower your annual tax bill.

- Low-interest and government-backed loans through state and federal programs.

Each city, from Everett to Lake Forest Park, may offer unique local programs. For a detailed look at Seattle-specific options, review the Seattle first-time buyer programs.

Key Eligibility Criteria in Seattle and Surrounding Areas

Eligibility for assistance for first time homebuyers depends on several factors:

- Income limits: King and Snohomish counties set annual income caps based on household size.

- Credit score: Most programs require a minimum 620 credit score, but higher scores can unlock better rates.

- Home price caps: Each city, including Shoreline and Lynnwood, has maximum allowable purchase prices.

- Residency and occupancy: Buyers must plan to live in the home as their primary residence.

Check program guidelines for each location to confirm current requirements, as these can shift annually.

2026 Updates and Trends

The landscape of assistance for first time homebuyers is evolving in 2026. New programs have launched or expanded, especially those supporting BIPOC and low-income buyers across Seattle, Everett, and Mill Creek. Funding levels for grants and forgivable loans have increased, making it possible for more buyers to qualify.

Loan limits and grant amounts have also been adjusted to reflect rising median home prices. For example, Seattle’s median home price continues to climb, with Shoreline and Lake Forest Park following suit. Staying informed on these trends ensures you can maximize your eligibility and take advantage of the newest resources.

Step-by-Step: How to Access First-Time Homebuyer Assistance

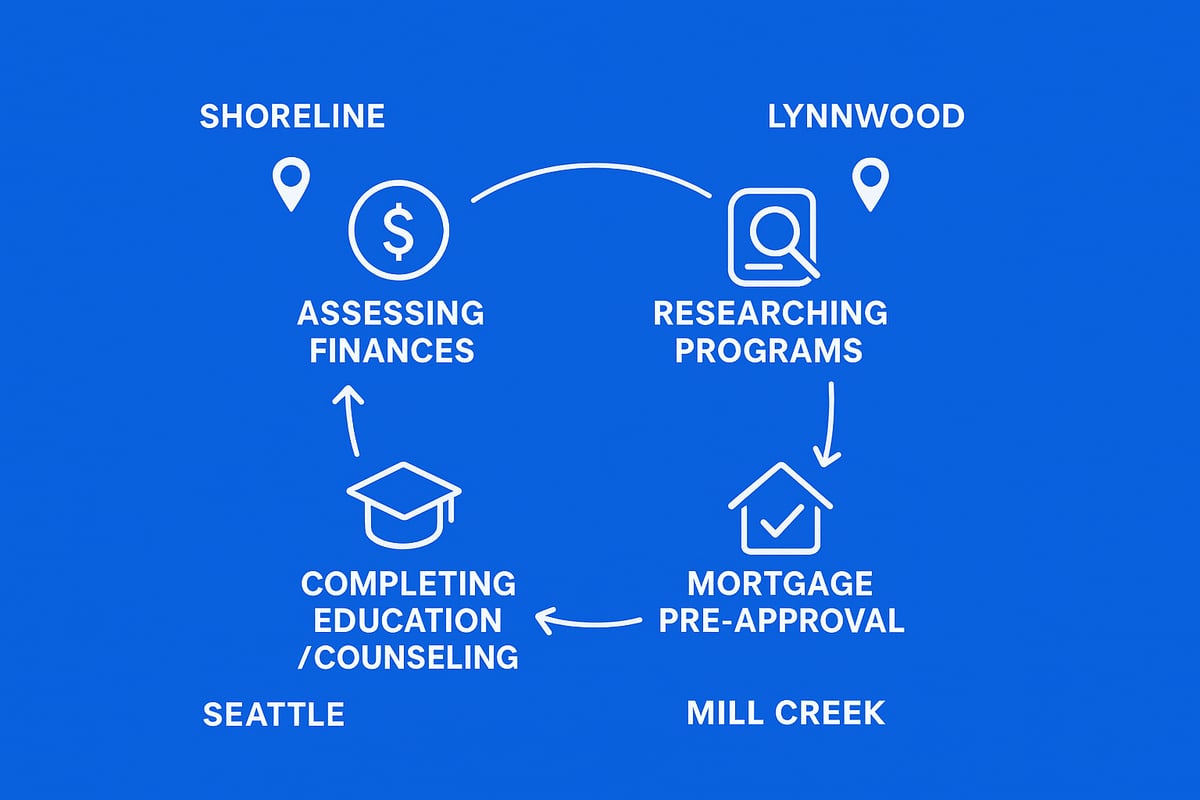

Navigating assistance for first time homebuyers in Seattle and nearby cities can feel overwhelming, but breaking it down into clear, manageable steps makes the process much smoother. Whether you’re searching in Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett, following a proven path helps you move from dreamer to homeowner with confidence.

Step 1: Assess Your Financial Readiness

The first step in securing assistance for first time homebuyers is understanding your financial position. Start by reviewing your income, monthly expenses, and savings to create a realistic homeownership budget.

Calculate your debt-to-income (DTI) ratio, which lenders use to determine eligibility for programs in Seattle and surrounding areas. Most assistance for first time homebuyers requires a DTI below 45 percent.

Check your credit report for accuracy and aim for a score of at least 620, though higher scores may unlock better rates or more options. If your score needs improvement, focus on paying down credit card balances and making all payments on time.

Preparing your finances early sets a solid foundation for the next steps.

Step 2: Research and Choose the Right Program

Once you know your budget, it’s time to explore the variety of programs offering assistance for first time homebuyers in Seattle, Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett.

Compare down payment grants, forgivable loans, and tax credits from the WA State Housing Finance Commission, the City of Seattle, and local nonprofit organizations. Each program has unique eligibility rules and benefits.

For a comprehensive overview of statewide loan and grant programs, homebuyer education, and eligibility requirements, visit the Washington State Housing Finance Commission Homebuyer Programs.

Make a list of programs that match your profile, and note application deadlines and documentation required.

Step 3: Get Pre-Approved for a Mortgage

In Seattle’s competitive market, pre-approval is essential for any assistance for first time homebuyers. This step shows sellers you’re serious and ready to move quickly.

Gather recent pay stubs, tax returns, bank statements, and proof of assets. Lenders in Everett or Mill Creek may have slightly different timelines, but most can provide pre-approval within days if paperwork is in order.

Compare offers from multiple lenders to find the best combination of rates and program compatibility. Remember, some assistance for first time homebuyers is only available through specific lenders or mortgage brokers.

Pre-approval also helps you define your price range and strengthens your offer when you find the right home.

Step 4: Complete Required Education and Counseling

Most assistance for first time homebuyers in the Seattle area requires completion of an approved homebuyer education course. These classes—offered by WSHFC, city programs, and local nonprofits—cover budgeting, mortgage basics, and the buying process.

Choose between online and in-person options in the Puget Sound region. Some cities, like Lynnwood or Shoreline, may offer special workshops tailored to local buyers.

Finishing this step not only fulfills eligibility requirements but also prepares you for the realities of homeownership. It’s a smart move even if not mandatory for your chosen program.

Step 5: Apply for Assistance and Submit Offers

With your documents ready and education complete, you can apply for assistance for first time homebuyers and begin making offers on homes in Seattle, Everett, or Lake Forest Park.

Coordinate closely with your lender and real estate agent. Submit completed applications for grants or loans before making an offer, as some programs require pre-approval of assistance.

Expect processing times to vary by city and program, ranging from a few days to several weeks. For example, a first-time buyer in Lynnwood might secure down payment assistance within two weeks, while Seattle programs could take longer due to demand.

Stay organized, follow up regularly, and be ready to act fast when your application is approved.

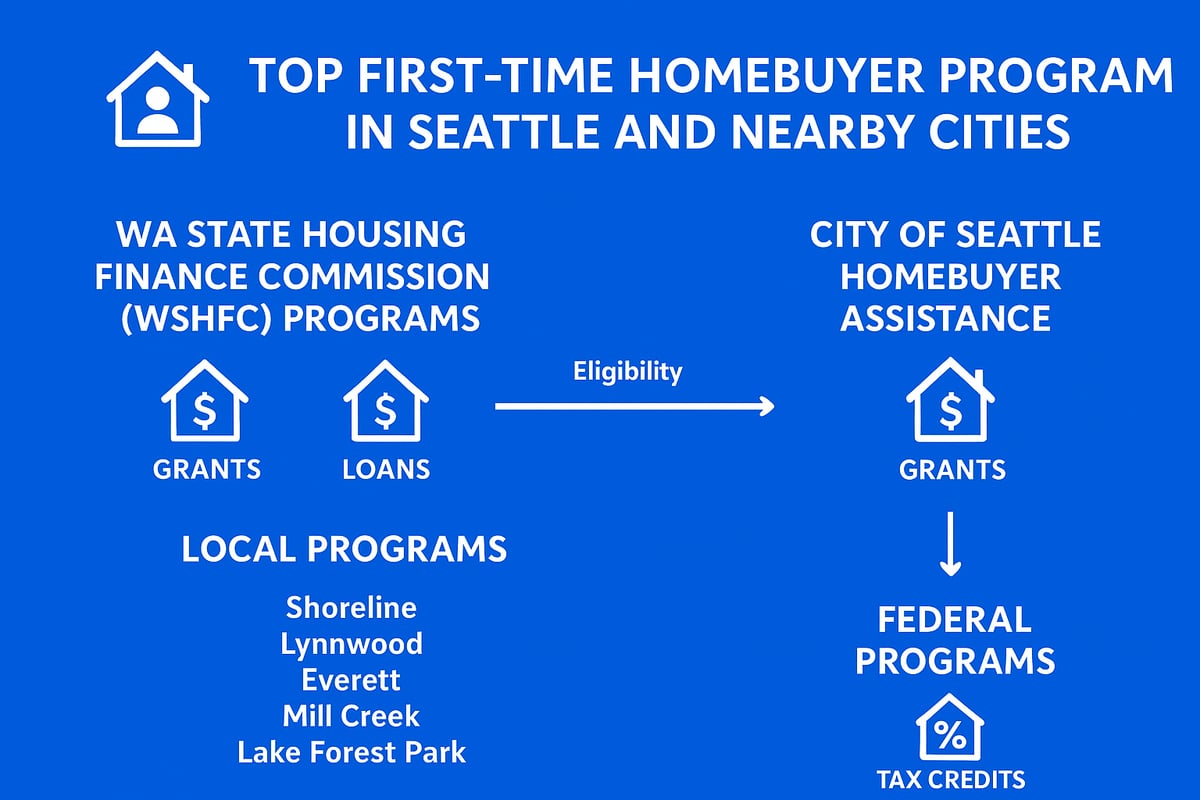

Exploring the Top First-Time Homebuyer Programs in Seattle & Nearby Cities

For those seeking assistance for first time homebuyers in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett, the right program can make all the difference. Understanding the options available in 2026 is crucial for a smooth path to homeownership. Below, I’ll walk you through the leading programs, their benefits, and how to choose the best fit for your needs.

WA State Housing Finance Commission (WSHFC) Programs

The WA State Housing Finance Commission (WSHFC) is a cornerstone for assistance for first time homebuyers across the region. Their Home Advantage and House Key Opportunity programs offer low-interest mortgages and access to down payment assistance.

To qualify, buyers must meet income and purchase price limits, which are adjusted for King and Snohomish counties. Typically, you’ll need a minimum credit score of 620. WSHFC’s down payment loans can be combined with other programs, making them ideal for Seattle and neighboring cities. These resources are especially valuable for those with moderate incomes or who are new to the process.

City of Seattle Homebuyer Assistance

The City of Seattle’s homebuyer support stands out for its robust down payment loan program, designed specifically as assistance for first time homebuyers. Eligible buyers who plan to occupy their home in Seattle can access forgivable loans, which are repaid only if you sell or refinance within the loan’s term.

Income limits and residency rules apply, and the city updates maximum assistance amounts annually. For those interested in the details, Seattle’s Down Payment Assistance Programs provides comprehensive, up-to-date information on eligibility and application steps.

Local Programs in Shoreline, Lynnwood, Everett, Mill Creek, and Lake Forest Park

Outside Seattle, assistance for first time homebuyers is available through targeted city and county programs. Shoreline, Lynnwood, Everett, Mill Creek, and Lake Forest Park often partner with local nonprofits and credit unions to offer grants or deferred loans.

These programs may have unique income caps and property price limits based on local market data. For example, Lynnwood’s offerings often prioritize families and essential workers, while Everett and Mill Creek focus on affordability for new residents. Average assistance amounts vary, but many buyers receive several thousand dollars toward their purchase.

Federal Programs for First-Time Buyers

Federal options remain a vital component of assistance for first time homebuyers in the Seattle area. FHA loans require lower down payments and flexible credit scores, while VA and USDA loans cater to veterans and rural buyers.

Additionally, Fannie Mae and Freddie Mac provide conventional loan options with competitive rates for qualified buyers. In 2026, the National Homebuyer Assistance Fund, if available, will further expand opportunities for eligible applicants. These federal choices offer flexibility, especially when combined with local or state programs.

Comparing Program Benefits and Drawbacks

Understanding how each program stacks up is key for anyone seeking assistance for first time homebuyers. Consider the following comparison:

| Program Type | Max Assistance | Repayment Terms | Can Combine With Others | Ideal For |

|---|---|---|---|---|

| WSHFC | Up to $15,000 | Deferred/forgivable | Yes | Moderate-income buyers |

| Seattle City | Up to $55,000 | Forgivable/deferred | Yes | Seattle residents |

| Local Programs | $5,000–$25,000 | Deferred/forgivable | Sometimes | Buyers in Shoreline, Everett, etc. |

| Federal Programs | Varies | Standard mortgage | Yes | Wide range, including veterans |

Many buyers successfully stack programs, such as combining WSHFC with a city loan, to maximize their buying power.

Keith Akada – Trusted Mortgage Guidance for Seattle First-Time Buyers

For those seeking assistance for first time homebuyers in Seattle and nearby cities, Keith Akada brings over 25 years of local mortgage expertise. Keith specializes in guiding first-time buyers through every step, from understanding down payment grants to securing fast-track mortgage approvals.

Keith’s approach is tailored for the Seattle area, including Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. With deep knowledge of local and state assistance programs, he helps clients with complex income—especially tech professionals—navigate unique challenges like RSUs and bonus structures.

Education and transparency are at the heart of Keith’s process. He’s earned more than 750 five-star reviews by ensuring buyers are informed and confident. For a closer look at how a dedicated broker can simplify your journey, see these first-time home buyer broker insights.

Clients from Lynnwood to Everett have achieved homeownership thanks to Keith’s strategic guidance, turning the dream of a first home into reality.

Navigating the Seattle-Area Real Estate Market as a First-Time Buyer

Entering the Seattle housing market as a first-time buyer in 2026 brings opportunity and challenge. Understanding local trends and leveraging assistance for first time homebuyers is essential for success. Let’s break down what to expect and how to navigate each step, whether you’re searching in Seattle, Shoreline, Lynnwood, Mill Creek, Lake Forest Park, or Everett.

Current Market Conditions in Seattle and Surrounding Cities

In 2026, the Seattle-area real estate market remains highly competitive, especially for those seeking assistance for first time homebuyers. Median home prices have stabilized compared to previous years but still reflect strong demand. In Seattle, entry-level homes average $675,000. Shoreline and Lynnwood sit slightly lower, around $600,000, while Mill Creek, Lake Forest Park, and Everett offer more affordable options closer to $550,000.

Inventory has improved, with more listings available in Everett and Lynnwood than central Seattle. However, homes in all these cities often receive multiple offers and sell within two weeks. Buyers benefiting from assistance for first time homebuyers may find increased opportunity as new listings hit the market, but competition remains fierce throughout the region.

Strategies for Competing in a Hot Market

Success in Seattle’s 2026 market depends on preparation and smart use of assistance for first time homebuyers. Start by securing fast-track mortgage pre-approval, which shows sellers you’re serious and ready. Work with a local agent who knows first-time buyer programs in Shoreline, Mill Creek, and Everett.

Craft compelling offers by including flexible contingencies and understanding seller motivations. Consider using escalation clauses to stay competitive. For more actionable tips, consult the Home buying strategies guide to maximize your advantage.

By leveraging both financial assistance and informed strategies, first-time buyers can compete confidently, even in Seattle’s fast-paced market.

Common Challenges and Solutions

Assistance for first time homebuyers is valuable, but navigating hurdles is part of the journey. Appraisal gaps are common when offer prices rise above appraised value, especially in Seattle and Lynnwood. Discuss options with your lender, such as appraisal gap coverage or adjusting your offer structure.

Bidding wars are frequent, particularly for move-in ready homes in Everett and Lake Forest Park. Stay flexible on closing dates or minor repairs to make your offer more appealing. Balancing affordability with location may require broadening your search to areas like Mill Creek or Shoreline, where assistance for first time homebuyers can stretch further.

Persistence, education, and a strong support team are key to overcoming these obstacles.

Timing Your Purchase for Maximum Assistance

Knowing when to buy can help maximize assistance for first time homebuyers in the Seattle area. Home prices typically dip in late fall and winter, while spring brings more listings but increased competition. Many programs refresh funding at the start of the year, so early applicants in Mill Creek, Lynnwood, and Shoreline may have better access to grants and loans.

Monitor program deadlines and market slowdowns. Coordinating your purchase with funding cycles and less crowded market periods can boost your chances of success. Stay informed about local trends and program updates to make the most of your homebuying journey.

Frequently Asked Questions: First-Time Homebuyer Assistance in Seattle

Navigating assistance for first time homebuyers in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett can feel overwhelming. Here are answers to the most common questions I receive as a licensed mortgage broker serving these communities.

Who qualifies as a first-time homebuyer in 2026?

For assistance for first time homebuyers, eligibility in Seattle and neighboring cities follows federal and state standards. You are considered a first-time homebuyer if you have not owned a primary residence in the past three years. This rule applies to all household members on the loan.

There are exceptions. For example, if you are a recent graduate renting in Everett, or a family relocating to Mill Creek after selling a home more than three years ago, you qualify. Married couples where only one spouse has owned before may still be eligible, depending on the specific program.

Always verify with your lender or program administrator, as some local initiatives in Shoreline and Lynnwood offer added flexibility for unique situations.

How much can I get in down payment or closing cost assistance?

Assistance for first time homebuyers varies based on income, purchase price, and location. In Seattle and surrounding areas, typical down payment assistance ranges from $10,000 to $55,000. Some city and nonprofit programs in Everett and Lake Forest Park may offer forgivable loans or grants.

For example, HomeSight Purchase Assistance Programs provide targeted support, including deferred loans and special products for eligible buyers. Maximum grant or loan amounts depend on the program and your household size.

Here's a quick comparison table:

| City | Typical Assistance Range |

|---|---|

| Seattle | $20,000 – $55,000 |

| Lynnwood | $10,000 – $30,000 |

| Everett | $15,000 – $40,000 |

| Mill Creek | $10,000 – $25,000 |

Check with your mortgage broker for current limits, as program funding and eligibility can change annually.

What are the most common mistakes first-time buyers make?

When seeking assistance for first time homebuyers, avoid these frequent errors:

- Skipping required homebuyer education classes, which are often mandatory for eligibility.

- Not researching multiple programs, missing out on grants or better loan terms.

- Underestimating closing costs, leading to last-minute surprises.

- Failing to check credit reports early, which can delay pre-approval.

- Overlooking local resources in Shoreline and Lake Forest Park.

Completing a home ownership education course is vital. It prepares you for the process, improves your eligibility, and helps you avoid costly pitfalls.

How do I start the process if I live in Shoreline, Lynnwood, or Everett?

To access assistance for first time homebuyers in Shoreline, Lynnwood, or Everett, begin by gathering financial documents and checking your credit. Next, research city and county programs online, then register for a homebuyer education class.

The typical step-by-step looks like this:

- Assess budget and credit.

- Complete homebuyer education.

- Get pre-approved by a lender familiar with local assistance.

- Apply for grants or loans through city programs.

- Work with a real estate agent to find eligible properties.

Local nonprofits and city housing offices often have dedicated staff to guide you. For Mill Creek residents, starting the application online and attending a local workshop ensures you do not miss critical deadlines.

Pro Tips for a Smooth First-Time Homebuying Journey in 2026

Embarking on the path to homeownership in Seattle or nearby cities is a significant milestone. With the right assistance for first time homebuyers, you can navigate the process confidently and avoid common pitfalls. These pro tips are designed to help you build a strong foundation, maximize your purchasing power, and ensure a seamless experience from start to finish.

Build a Strong Homebuying Team

Success in Seattle’s competitive market often starts with assembling the right team. Your mortgage broker and real estate agent should be local experts who understand the nuances of neighborhoods like Shoreline, Lynnwood, and Mill Creek.

- Look for professionals with experience helping first-time buyers.

- Choose a mortgage broker who can explain assistance for first time homebuyers and tailor loan options to your situation.

- Prioritize open, proactive communication throughout the process.

Having a knowledgeable team by your side will help you navigate negotiations, paperwork, and deadlines with greater confidence.

Maximize Your Buying Power

To make the most of assistance for first time homebuyers, focus on strengthening your financial profile. Improving your credit score, reducing debt, and considering all sources of income will expand your options.

- Review your credit report and address any errors early.

- Pay down credit cards and avoid taking on new debt before applying.

- Tech professionals in Redmond or Everett can often leverage RSUs or bonuses to qualify for higher loan amounts.

By preparing your finances, you can access better mortgage rates and qualify for more robust assistance programs.

Understand Long-Term Costs and Benefits

Owning a home in Seattle, Lake Forest Park, or Everett involves more than just your monthly mortgage payment. Be sure to factor in additional expenses and compare them to renting.

- Account for property taxes, homeowner’s insurance, and potential HOA fees.

- Set aside savings for maintenance and unexpected repairs.

- Track how building equity over time can benefit your financial future.

A clear understanding of long-term costs ensures your home remains a sustainable investment.

Stay Informed on Changing Programs and Market Trends

Eligibility and funding for assistance for first time homebuyers can shift each year. Stay current with program updates, loan limits, and market conditions in cities like Lynnwood and Mill Creek.

- Monitor local market reports and new program launches.

- Visit resources such as the Washington State Department of Commerce Homeownership Capital Programs to discover state-funded opportunities for first-time buyers.

- Connect with your mortgage broker regularly for alerts on policy changes.

Staying informed puts you in the best position to capitalize on new or expanded assistance offerings.

Leverage Education and Counseling Resources

Homebuyer education is not just a requirement for many assistance for first time homebuyers programs—it is also invaluable for building confidence.

- Attend free or low-cost classes offered by the WA State Housing Finance Commission or local nonprofits.

- Choose between in-person workshops in Seattle or online courses for flexibility.

- Seek ongoing support from counselors even after closing.

Education helps you anticipate challenges and make informed decisions throughout your journey.

Final Checklist Before Closing

In the final stage, double-check every requirement to ensure a smooth closing. This is especially important when using assistance for first time homebuyers in fast-moving markets like Everett or Shoreline.

- Confirm that all funding and documentation are in place.

- Schedule a pre-closing walk-through to spot any last-minute issues.

- Review all closing documents with your agent and mortgage broker.

Careful attention to these final steps will help you transition from buyer to homeowner with confidence.

You’ve just explored the ins and outs of first time homebuyer assistance in Seattle and nearby cities, from understanding eligibility to making your strongest offer in a competitive market. Navigating this journey can feel overwhelming, but you don’t have to do it alone. With more than 25 years of experience and a genuine focus on education and strategy, I’m here to help you make confident decisions every step of the way—whether you’re a tech professional with RSUs or simply ready to stop renting. If you’re ready to talk through your goals or have questions about your next steps, Let’s have a conversation.