Thinking of buying a home in Seattle, Shoreline, or Everett in 2026? Navigating the local market starts with understanding your financing choices. The right conventional mortgage loan can open doors in a competitive landscape, but knowing the ins and outs is crucial for success.

This guide breaks down what a conventional mortgage loan is, how it works, and what you need to qualify. We cover loan types, down payment options, rates, the application process, and tips for approval in Seattle and nearby cities. Use this resource to make confident, informed decisions on your journey to homeownership.

What Is a Conventional Mortgage Loan?

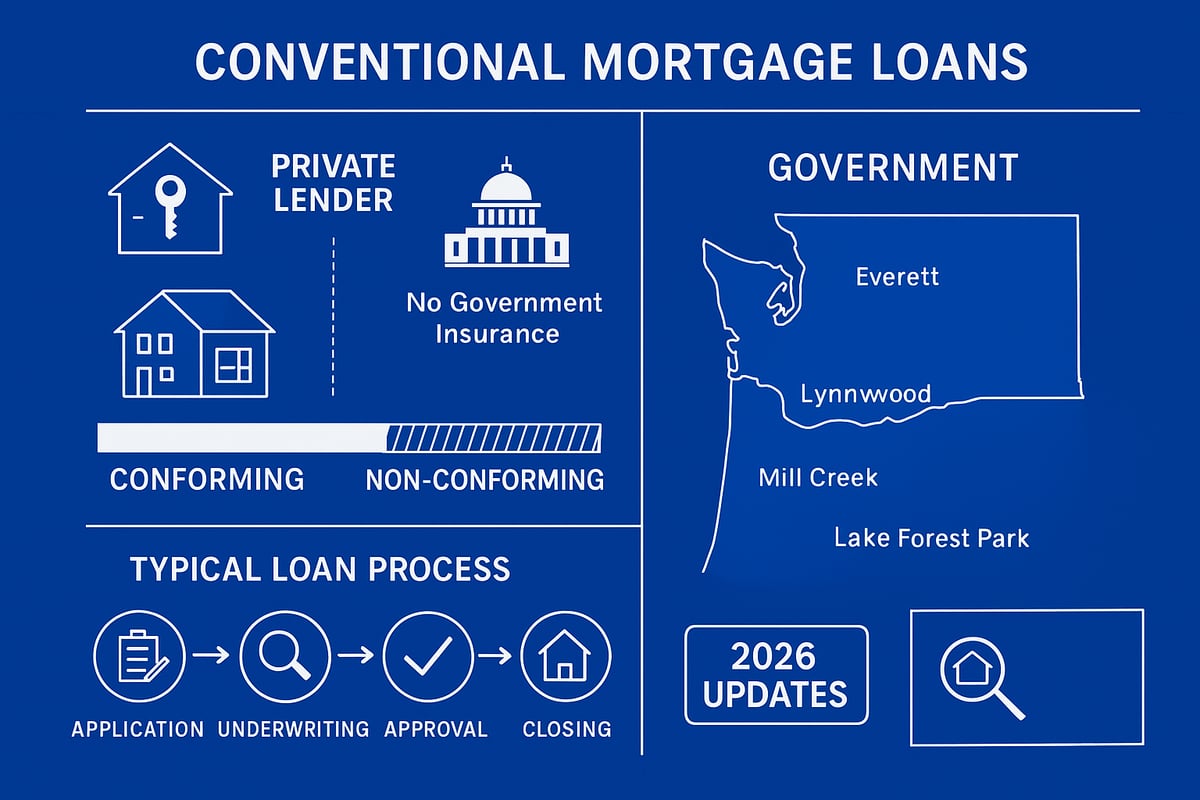

Thinking about buying a home in Seattle, Shoreline, or Everett? Understanding the conventional mortgage loan is essential to navigate the local real estate market with confidence. A conventional mortgage loan is a home loan not insured or guaranteed by government agencies like FHA, VA, or USDA. Instead, these loans are offered by private lenders and are typically backed by Fannie Mae or Freddie Mac when they meet certain criteria. Unlike government-backed loans, a conventional mortgage loan often requires a stronger credit profile and a higher down payment. In Seattle and surrounding areas, most buyers choose this route for its flexibility and competitive rates. As of 2026, updated guidelines and loan limits make it even more accessible for buyers. For a full breakdown of the latest requirements, you can review the Conventional Loan Requirements for 2026.

Definition and Overview

A conventional mortgage loan is a home financing option that is not insured by a federal agency. The main difference between a conventional mortgage loan and a government-backed loan is who provides the guarantee. FHA, VA, and USDA loans are backed by government agencies, while a conventional mortgage loan relies on private lenders and investors for funding. In Seattle and nearby cities, the conventional mortgage loan is the most common choice for buyers seeking flexibility and control over their financing. For example, a typical Seattle homebuyer with a solid credit score and stable income might choose a conventional mortgage loan for a primary residence. Regulatory changes in 2026 have slightly increased loan limits and clarified credit standards, making this loan type even more attractive for a variety of buyers.

How Conventional Loans Work

The process for obtaining a conventional mortgage loan begins with an application and moves through pre-approval, property selection, underwriting, and closing. Loans are categorized as conforming if they meet Fannie Mae or Freddie Mac guidelines, or non-conforming if they exceed set limits or have unique features. For example, a fixed-rate conventional mortgage loan in Lake Forest Park offers predictable monthly payments, while an adjustable-rate option may start with a lower interest rate. Key terms you will encounter include principal (the loan amount), interest (the cost to borrow), and escrow (an account for taxes and insurance). Loan servicing is typically managed by the original lender or transferred to a specialized company.

Key Features and Benefits

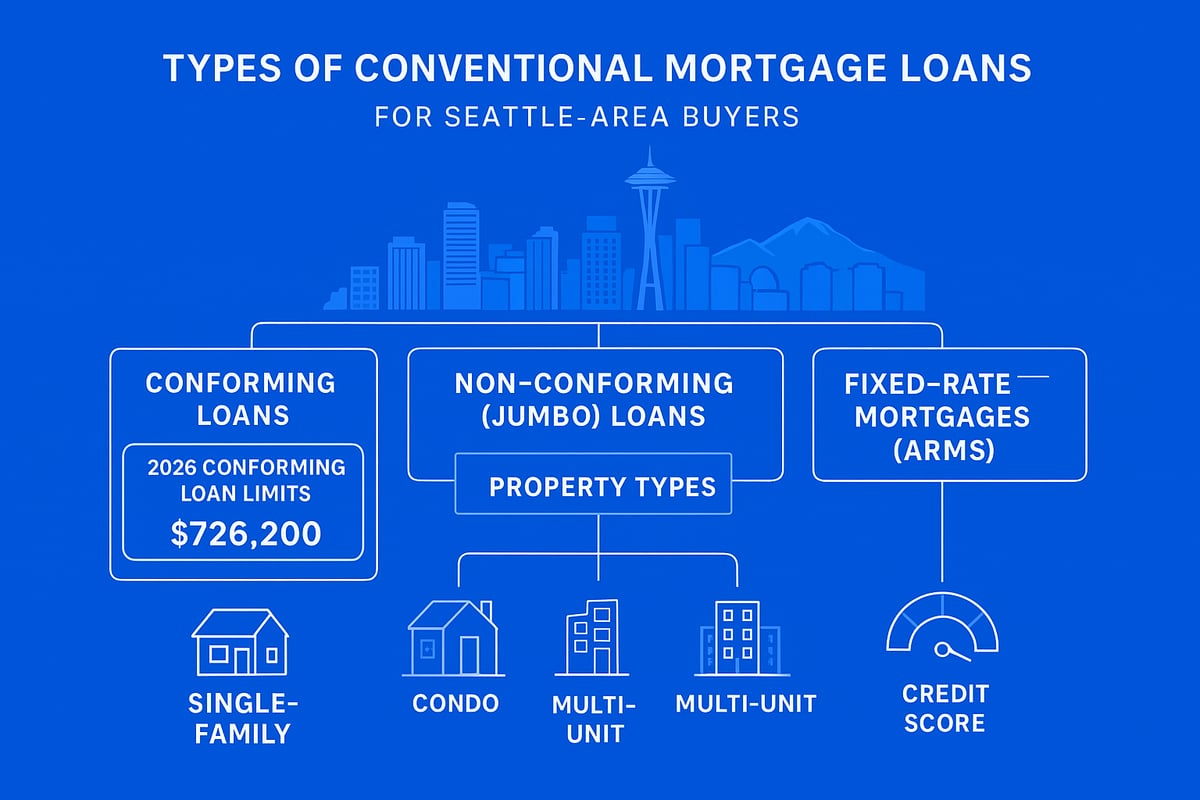

A conventional mortgage loan provides broad flexibility in property types, including single-family homes, condos, and multi-unit properties. For 2026, the conforming loan limit in King and Snohomish counties has increased, allowing buyers in Seattle, Mill Creek, or Shoreline to finance more expensive homes without needing a jumbo loan. Unlike FHA or VA loans, a conventional mortgage loan does not require upfront mortgage insurance, which can save qualified borrowers money. Interest rates are highly competitive for those with strong credit and low debt. For example, a Mill Creek buyer with excellent credit may benefit from lower monthly payments thanks to these features.

Conventional Loans in the Seattle Market

Seattle’s housing market is known for its high prices and fierce competition. In this environment, the conventional mortgage loan stands out for its acceptance among sellers and agents. Local data shows that a significant share of home purchases in Seattle, Lynnwood, and Everett use a conventional mortgage loan, often due to higher loan limits and flexible terms. Inventory remains tight, so having a conventional mortgage loan pre-approval can strengthen your offer. In Everett, typical down payments range from 5 to 20 percent, with loan sizes reflecting the area’s median home prices. This approach allows buyers to compete effectively in a dynamic market.

Types of Conventional Mortgage Loans

Navigating the world of conventional mortgage loan options in Seattle and surrounding cities can seem overwhelming, but understanding the main types is key to making an informed decision. Whether you are buying in Shoreline, Lynnwood, or Mill Creek, knowing the differences between loan types will help you secure the right fit for your financial goals in 2026.

Conforming vs. Non-Conforming Loans

A conventional mortgage loan can be classified as either conforming or non-conforming, depending on whether it meets the guidelines set by Fannie Mae and Freddie Mac. Conforming loans must stay within set loan limits, which for 2026 in Seattle and nearby cities are expected to reflect rising home prices. For example, a Shoreline home priced above these limits would require a non-conforming, or "jumbo," loan.

Non-conforming loans also include portfolio and niche products that don't fit standard guidelines. While conforming loans typically offer better rates and easier qualification, non-conforming loans provide flexibility for unique or high-value properties. Understanding which category your loan falls into will shape your path to homeownership in the Seattle area.

| Loan Type | Meets Fannie/Freddie Guidelines | Max Loan Amount (2026, Seattle) | Typical Use Case |

|---|---|---|---|

| Conforming | Yes | ~$1,000,000+ | Most single-family homes |

| Non-Conforming | No | Above local limits | Luxury, unique properties |

Fixed-Rate Mortgages

The fixed-rate conventional mortgage loan remains the most popular choice for Seattle-area buyers seeking stability. With fixed-rate loans, your interest rate and monthly payment stay the same throughout the term—whether you choose 15, 20, or 30 years. This predictability is especially attractive in fluctuating markets like Lynnwood, where budgeting for the long term is a priority.

While fixed-rate loans may start with a slightly higher rate than adjustable options, they protect you from future rate increases. Many families in Seattle and Lake Forest Park prefer this option for peace of mind and straightforward financial planning. If you want steady payments and plan to stay in your home for many years, a fixed-rate loan could be your best fit.

Adjustable-Rate Mortgages (ARMs)

An adjustable-rate mortgage, or ARM, is a conventional mortgage loan with a variable interest rate. Typically, ARMs start with a lower fixed rate for an initial period—such as five or seven years—then adjust periodically based on market conditions. This structure can offer significant savings early on, making ARMs appealing to buyers in fast-growing areas like Mill Creek and Everett.

However, after the initial fixed period, your payments may increase if rates rise. ARMs are often chosen by buyers who expect to move or refinance within a few years, thus taking advantage of the initial lower payments. Understanding the terms and adjustment schedules is essential before committing to an ARM in Seattle's dynamic market.

Jumbo Loans

A jumbo conventional mortgage loan is designed for properties that exceed the conforming loan limits set for Seattle and surrounding cities. With home prices climbing in Bellevue, Kirkland, and central Seattle, jumbo loans have become increasingly common for buyers targeting high-value real estate.

Jumbo loans require higher credit scores, larger down payments, and more rigorous documentation compared to conforming loans. For example, a tech professional purchasing a luxury home in Seattle may need a jumbo loan to finance the property. While jumbo loans offer flexibility for expensive homes, be prepared for stricter qualification standards and potentially higher rates.

Specialty and Niche Conventional Loans

Specialty and niche conventional mortgage loan products cater to unique borrower needs. Portfolio loans are offered by local banks that keep the loans in-house, allowing for customized underwriting. Other options include interest-only loans, physician loans for medical professionals, and investor-specific products.

Self-employed borrowers in Everett may benefit from bank statement loans, which use alternative documentation for income. Investors looking to purchase duplexes or multi-unit properties in Mill Creek can explore conventional loan for investment property options to maximize flexibility and returns. These specialized loans expand access for buyers whose profiles or goals fall outside standard guidelines.

Eligibility and Qualification Requirements

Navigating the eligibility requirements for a conventional mortgage loan in Seattle and surrounding areas is crucial for a smooth homebuying experience. Understanding these standards not only prepares you for the application process, but also helps you position your finances for the best possible terms. Whether you are buying in Shoreline, Lynnwood, Everett, or Mill Creek, knowing what lenders look for can make all the difference.

Credit Score Standards

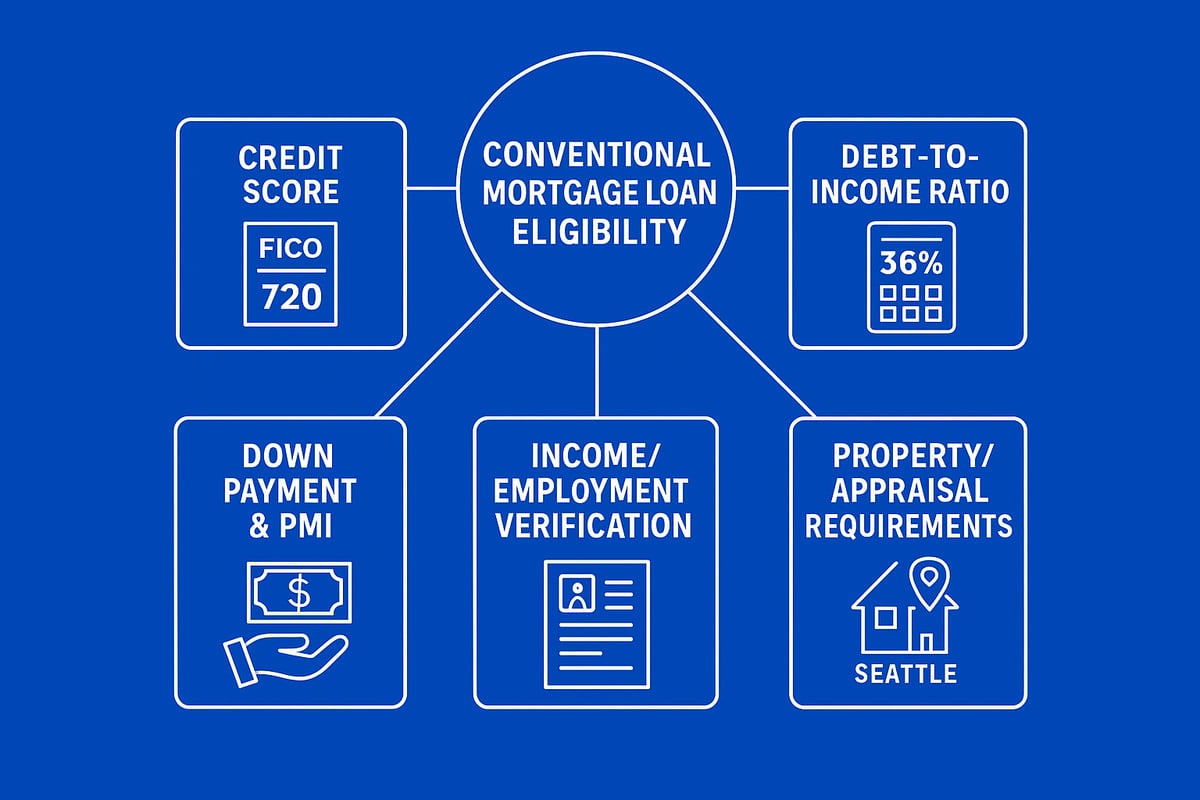

Lenders in Seattle typically require a minimum FICO score of 620 to qualify for a conventional mortgage loan, but higher scores open the door to better rates and smoother approvals. For example, a Lynnwood homebuyer with a 760 credit score may secure a notably lower interest rate than one with a 680 score. In 2026, the average FICO for approved borrowers in the region often exceeds national averages, reflecting the competitive local market. Your credit score acts as a key indicator of risk, so monitoring and improving it before applying for a conventional mortgage loan can save you thousands over the life of your loan.

Debt-to-Income (DTI) Ratios

A central factor in conventional mortgage loan approval is your debt-to-income (DTI) ratio. Most Seattle-area lenders set maximum DTI limits between 43 and 50 percent, but lower ratios are always preferred. DTI is calculated by dividing your total monthly debt payments by your gross monthly income. Both front-end (housing costs only) and back-end (all debts) ratios matter. For instance, a Seattle couple with student loans may need to pay down debts or increase income to qualify. Maintaining a healthy DTI signals to lenders that you can comfortably manage a conventional mortgage loan alongside other obligations.

Down Payment Options and PMI

One of the most flexible features of a conventional mortgage loan is the range of down payment options. Buyers in Mill Creek or Everett can put down as little as 3 to 5 percent, though a 20 percent down payment eliminates private mortgage insurance (PMI) entirely. PMI is required for down payments under 20 percent and can be removed once you reach sufficient equity. First-time buyers often choose lower down payment routes, balancing savings with monthly costs. For a detailed breakdown of down payment choices, see this Conventional loan with 5% down guide.

Income and Employment Verification

To qualify for a conventional mortgage loan in Seattle, lenders require thorough documentation of your income and employment history. This often includes recent pay stubs, W-2s, and federal tax returns. For tech professionals in Everett or Amazon employees in Seattle, lenders can also count RSUs and bonus income, provided there is a consistent history. Stability—typically two years or more in the same field—is highly valued. Self-employed applicants or those with variable income may need to provide additional paperwork to verify their ability to repay a conventional mortgage loan.

Property and Appraisal Requirements

The property you purchase with a conventional mortgage loan must meet certain standards. An independent appraisal confirms the home’s value and condition, protecting both you and the lender. In Seattle, this is critical given the range of property types, from condos to multi-unit homes. Occupancy rules apply, whether you are buying a primary residence in Lynnwood, a second home in Lake Forest Park, or an investment property in Everett. Condos and multi-family properties have added requirements, so be sure to consult with your lender early in the process to ensure your desired property fits conventional mortgage loan guidelines.

The Conventional Loan Process in Seattle: Step-by-Step

Navigating the conventional mortgage loan process in Seattle requires a clear plan, especially with the area’s competitive real estate market. Whether you are buying in Shoreline, Lynnwood, Mill Creek, or Everett, understanding each step can help you secure your ideal home with confidence. Here’s a breakdown of the process, tailored for Seattle-area buyers.

Step 1: Pre-Approval and Preparation

The first step in your conventional mortgage loan journey is pre-approval. In Seattle’s fast-paced market, pre-approval gives you a competitive edge. Lenders will review your credit, income, debts, and assets to determine how much you can borrow.

Gather these documents for pre-approval:

- Recent pay stubs

- W-2s or tax returns

- Bank statements

- Photo ID

A well-prepared application can help you stand out, especially in Shoreline or when multiple offers are expected. For example, a buyer in Shoreline recently won a bidding war by presenting a solid pre-approval letter, which reassured the seller of their financial readiness.

Step 2: House Hunting and Making Offers

With pre-approval in hand, you can start house hunting in Seattle, Lynnwood, or Mill Creek. Your real estate agent will help you target homes that fit your budget and loan criteria. Using a conventional mortgage loan often strengthens your offer, as sellers view these as reliable and less likely to face financing delays.

In high-demand areas like Mill Creek during spring, you might encounter appraisal gaps or multiple-offer situations. Learning strategies to structure a winning offer is critical. For more in-depth tips, explore this Home buying strategies guide designed for Seattle buyers.

Remember, a strong offer is more than price; it includes your financing terms, contingencies, and the confidence you bring with your conventional mortgage loan approval.

Step 3: Loan Application and Processing

Once your offer is accepted, you’ll complete a full conventional mortgage loan application. This stage requires additional documentation and detailed information about your finances and the property.

Expect your lender to request:

- Updated income documents

- Proof of assets for your down payment

- Details about debts and obligations

The underwriting team will verify your information and assess the risk. In Lynnwood, it’s common for lenders to request clarification on recent bank deposits or employment history, so be prepared to respond quickly.

Keep communication open with your mortgage broker to ensure a smooth process and avoid delays.

Step 4: Appraisal, Title, and Final Approval

The lender will order an appraisal to confirm the home’s value matches the purchase price. In Lake Forest Park, unique property features can sometimes trigger appraisal questions, so be ready for potential follow-ups.

Meanwhile, a title company will conduct a search to ensure there are no legal issues with the property. You will also secure title insurance for added protection.

The underwriter will review the appraisal and title results, then issue final approval if all requirements are satisfied. Meeting these conditions is essential for your conventional mortgage loan to proceed to closing.

Step 5: Closing and Funding

In the final stage, you’ll review the Closing Disclosure, which details all costs and terms of your conventional mortgage loan. Schedule a final walk-through of the property to ensure everything is as agreed.

On closing day, you’ll sign documents at the escrow office. Once funds are transferred and the transaction is recorded, the home is officially yours.

In Seattle, the typical closing timeline ranges from 9 to 30 days, depending on the complexity of the transaction. Buyers in Everett often find that being organized and responsive helps ensure a smooth and timely closing.

Conventional Loan Rates, Costs, and Fees in 2026

Navigating the costs of a conventional mortgage loan in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett starts with understanding rates, fees, and insurance. In 2026, local buyers face a dynamic market, so careful planning is essential to maximize value and avoid surprises.

How Interest Rates Are Determined

Interest rates on a conventional mortgage loan in Seattle are shaped by both national and personal factors. Market influences include Federal Reserve policy, inflation, and bond market trends. In 2026, Seattle-area rates have responded to ongoing economic shifts, impacting monthly payments for buyers in Shoreline and Mill Creek.

Personal factors also play a big role. Your credit score, down payment amount, and loan type can all affect your offered rate. For example, a buyer in Lynnwood with excellent credit may secure a lower fixed rate than someone with a moderate score.

It is smart to consider rate lock strategies, especially in a competitive market. Locking your rate early can protect you from increases during your home search. For a detailed look at current local trends, check out this Seattle mortgage rates overview.

Closing Costs and Typical Fees

When closing on a conventional mortgage loan, expect a range of fees, often totaling 2 to 5 percent of the home's price. These costs include:

- Lender origination fees

- Appraisal and credit report charges

- Title insurance and escrow services

- Prepaid taxes and homeowners insurance

Average closing costs in Seattle and Everett tend to be higher than in Lynnwood, reflecting local property values. Buyers in Shoreline often compare lenders to negotiate better terms or request seller credits, which can help offset expenses. Always review your Loan Estimate to understand each fee and explore lender-paid closing options if available.

Private Mortgage Insurance (PMI)

A conventional mortgage loan usually requires PMI if your down payment is less than 20 percent. PMI protects the lender and is calculated based on loan size, credit score, and down payment percentage.

Buyers in Mill Creek who put 5 percent down will see PMI added to their monthly payment. Some lenders offer upfront or split-premium PMI options, giving flexibility in how you pay. The good news is that PMI can be removed once you reach 20 percent equity, either through payments or property appreciation—a common milestone for Seattle buyers as home values rise.

Tips for Minimizing Loan Costs

Smart borrowers take steps to lower the total expense of a conventional mortgage loan. Consider these strategies:

- Improve your credit score before applying

- Reduce your debt-to-income ratio for better terms

- Compare loan estimates from multiple Seattle-area lenders

- Choose the right loan term (shorter terms often mean lower rates)

- Negotiate for lender credits or seller-paid closing costs

For example, an Everett buyer saved thousands by improving their credit and selecting a lender offering competitive rates and credits. Careful planning and local expertise can make your home purchase more affordable.

Pros and Cons of Conventional Loans for Seattle-Area Buyers

Buying a home in Seattle, Shoreline, or Everett? Understanding the pros and cons of a conventional mortgage loan is crucial for making the right decision in today’s fast-moving market. Let’s break down the benefits, potential drawbacks, and how these loans stack up against other popular options in the region.

Advantages of Conventional Loans

A conventional mortgage loan offers several advantages for Seattle-area buyers, especially those with solid credit and stable income. Here’s why many choose this route:

- Lower overall costs for borrowers with strong financials

- Flexible property options including single-family, condos, and multi-units

- No upfront mortgage insurance unlike FHA or VA loans

- Ability to remove PMI once you reach 20% equity

For example, a Bellevue investor can purchase a condo or multi-unit property without the restrictions found in government-backed loans. These features make a conventional mortgage loan especially attractive in competitive markets like Mill Creek and Lynnwood. For more local insight on these advantages and 2026 loan limits, visit the Seattle Mortgage Guide 2026.

Potential Drawbacks and Limitations

Despite the benefits, a conventional mortgage loan does come with some challenges that buyers should consider:

- Stricter credit and DTI requirements compared to FHA or VA loans

- Larger down payment (often 5 to 20 percent) for the best rates

- PMI costs apply if your down payment is under 20 percent

For instance, a first-time buyer in Lake Forest Park with a lower credit score may find it harder to qualify for a conventional mortgage loan or face higher rates and PMI costs. It’s important to weigh these factors if your financial profile is still growing.

Comparing Conventional to FHA, VA, and USDA Loans

How does a conventional mortgage loan stack up against other common options? Here’s a quick comparison:

| Feature | Conventional | FHA | VA | USDA |

|---|---|---|---|---|

| Min. Down Payment | 3% | 3.5% | 0% | 0% |

| Credit Score Needed | 620+ | 580+ | 620+ | 640+ |

| PMI/MIP | Yes, if <20% | Yes | No | Yes |

| Flexibility | High | Medium | Veteran Only | Rural Only |

For example, an Everett buyer might qualify for both an FHA and a conventional mortgage loan. The best fit depends on credit, down payment, and property type. Always compare total costs, not just rates.

Who Should Consider a Conventional Loan?

A conventional mortgage loan is ideal for buyers who have:

- Good to excellent credit (typically 680 or higher)

- Stable employment and income

- Down payment savings (at least 5 to 20 percent)

- Interest in a wider range of property types

Scenarios where a conventional mortgage loan shines include Seattle families upgrading from a condo to a single-family home, tech professionals in Kirkland using RSUs as income, or investors purchasing duplexes in Everett. If you fit these profiles, conventional financing gives you more flexibility and long-term savings.

FAQs: Conventional Mortgage Loans in Seattle, Shoreline, Lynnwood, and Beyond

Thinking about a conventional mortgage loan in Seattle or surrounding areas? Below, I answer the most common questions I get from buyers in Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. Whether you are a first-time buyer or upgrading, these insights will help you make informed decisions in 2026.

Common Questions Answered

What is the minimum down payment for a conventional mortgage loan in Seattle? Most lenders allow as little as 3 percent down for qualified buyers, although putting 20 percent down eliminates PMI. You can use gift funds or local down payment assistance programs in Everett or Mill Creek, subject to lender approval. For credit, a FICO score of 620 is typically required, but higher scores unlock better rates. Duplexes and investment properties are allowed with stricter requirements. In the Seattle area, closing on a home with a conventional mortgage loan generally takes between 9 and 30 days, depending on your situation.

Local Market Insights and Examples

Seattle’s median home price in 2026 means many buyers approach or exceed conforming loan limits, especially in Shoreline and Lynnwood. The Federal Housing Finance Agency updates these limits yearly; for the latest, see the FHFA Announces Conforming Loan Limit Values for 2026. For example, a Mill Creek buyer using a 3 percent down payment may still stay within the conforming range, but higher-priced homes in Lake Forest Park could require a jumbo loan. Everett’s market moves quickly, so typical approval timelines stay near the 2-week mark for well-prepared buyers.

Tips for First-Time Buyers and Tech Professionals

If you are using RSUs, bonuses, or stock income to qualify for a conventional mortgage loan, work with a local lender who understands Seattle tech compensation. In multiple-offer situations, getting pre-approved and understanding updated loan requirements is crucial. For a visual breakdown of the new rules, watch the NEW Conventional Loan Requirements 2026. Take advantage of local down payment assistance if needed. For example, an Amazon or Microsoft employee can maximize buying power by documenting all income sources and collaborating with an experienced loan officer.

Preparing for Success in 2026

To boost your chances of qualifying for a conventional mortgage loan, start early. Monitor your credit, pay down debts, and gather key documents like pay stubs, W-2s, and tax returns. Partner with Seattle-area experts who know how to navigate local markets. Here is a quick checklist for success:

- Review your credit report and correct errors

- Calculate your debt-to-income ratio

- Save for down payment and closing costs

- Get pre-approved before house hunting

- Stay in close contact with your lender and agent

With preparation, your Seattle homebuying journey can be both smooth and successful.

Now that you’ve explored the ins and outs of conventional mortgage loans, from eligibility and local strategies to tips for tech professionals, you might be wondering how these details apply to your unique goals in Seattle’s competitive market. Whether you’re a first time buyer or looking to refine your financing options, I’m here to help you make sense of it all. Together, we can lay out a plan that fits your needs and maximizes your buying power with confidence and clarity. If you’re ready to start the conversation, let’s have a conversation.