Thinking about becoming a first time home buyer home in Seattle in 2026? You are part of a growing group as thousands prepare to navigate a market that stretches across Seattle, Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett.

Buying your first home brings both excitement and unique challenges, especially in today’s competitive market. From rising home prices to evolving loan options, the journey can feel overwhelming without the right guidance.

This guide is designed to provide first time home buyer home essentials for the Seattle area. You will find clear, actionable tips on eligibility, financial preparation, loan programs, credit strategies, the home search process, and local resources tailored for 2026.

Seattle’s housing landscape is always changing. With the right information and expert insights, you can approach your home buying journey with confidence and take the next step toward successful homeownership.

Understanding First-Time Homebuyer Eligibility in 2026

Buying your first time home buyer home in Seattle is an exciting milestone, but understanding eligibility is critical before you start the search. In 2026, both national and local requirements shape who qualifies. As a licensed mortgage broker serving Seattle, Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett, I guide clients through these definitions daily. Let’s break down what you need to know.

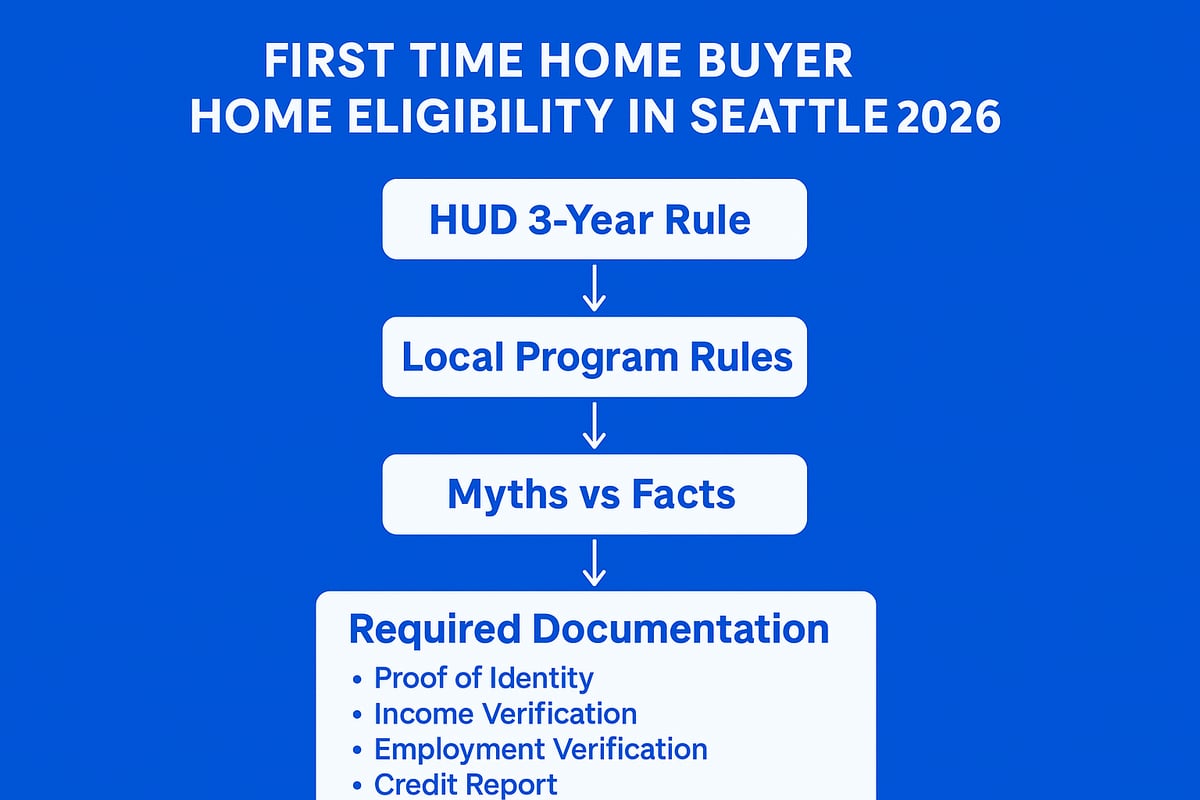

What Qualifies as a First-Time Homebuyer?

A first time home buyer home qualification starts with HUD’s definition: you must not have owned a principal residence in the past three years. This rule applies in Seattle and is commonly used by FHA and many local programs. Special cases exist, such as single parents or displaced homemakers who may qualify even if they owned a home with a former spouse.

Local programs might interpret eligibility differently. For example, a Lynnwood renter who sold their home in 2022 can qualify in 2026. Owners of non-permanent residences, like certain mobile homes, may also meet the criteria. Always verify with each lender or program since definitions can vary.

Remember, not all lenders use the same standard. Some may be stricter or more flexible, so checking early saves time. Most Seattle-area programs align with the three-year rule, but nuances matter for your first time home buyer home journey.

Common Myths and Misconceptions

Many first time home buyer home applicants in the Seattle region are held back by myths. One common misconception is that owning a home in the past makes you ineligible. In reality, if you have not owned a principal residence in three years, you may still qualify.

Another myth is that both spouses must be first-time buyers. In fact, only one spouse needs to meet the requirement for most programs. For example, an Everett buyer who previously owned a mobile home, not classified as a permanent residence, may still be eligible.

A third misconception is assuming you are disqualified due to past ownership regardless of circumstances. Misunderstandings like these cause many to miss out on valuable assistance. Always confirm your status with a trusted professional to maximize your first time home buyer home options.

Local Eligibility Factors in Seattle and Surrounding Cities

Seattle, Shoreline, Mill Creek, and Everett have unique program guidelines that can affect your first time home buyer home eligibility. Some city programs require you to live or work within city limits. Income limits and purchase price caps also vary by location.

For instance, Lake Forest Park down payment assistance programs may set stricter income requirements compared to Seattle. Household size and composition can influence eligibility, with larger households sometimes qualifying for higher income thresholds.

Every local housing authority and nonprofit may use different standards. To stay current, check city and county websites for updated 2026 criteria, or explore Seattle first-time buyer programs for detailed local guidance on what’s available for your first time home buyer home search.

Documentation and Proof Needed

Gathering the right documents is essential for a smooth first time home buyer home purchase. Standard paperwork includes tax returns, pay stubs, and rental history. You’ll need to provide proof you have not owned a principal residence, such as deeds, closing statements, or affidavits.

For single parents or displaced homemakers, divorce decrees or separation agreements may be needed. For example, a Lynnwood buyer might use rental agreements from the past three years to verify non-ownership. Lenders will also verify your status through their own processes.

Start organizing documents early, as incomplete files cause 80 percent of delays. A well-prepared paper trail speeds up approval and helps you become a first time home buyer home owner in a competitive market.

Preparing Your Finances for a First Home Purchase

Getting your finances in order is the foundation for a successful first time home buyer home journey in Seattle. With high competition in Seattle, Shoreline, Everett, and surrounding cities, understanding your budget, credit, and documentation requirements is essential. Here is how to prepare for your first purchase with confidence.

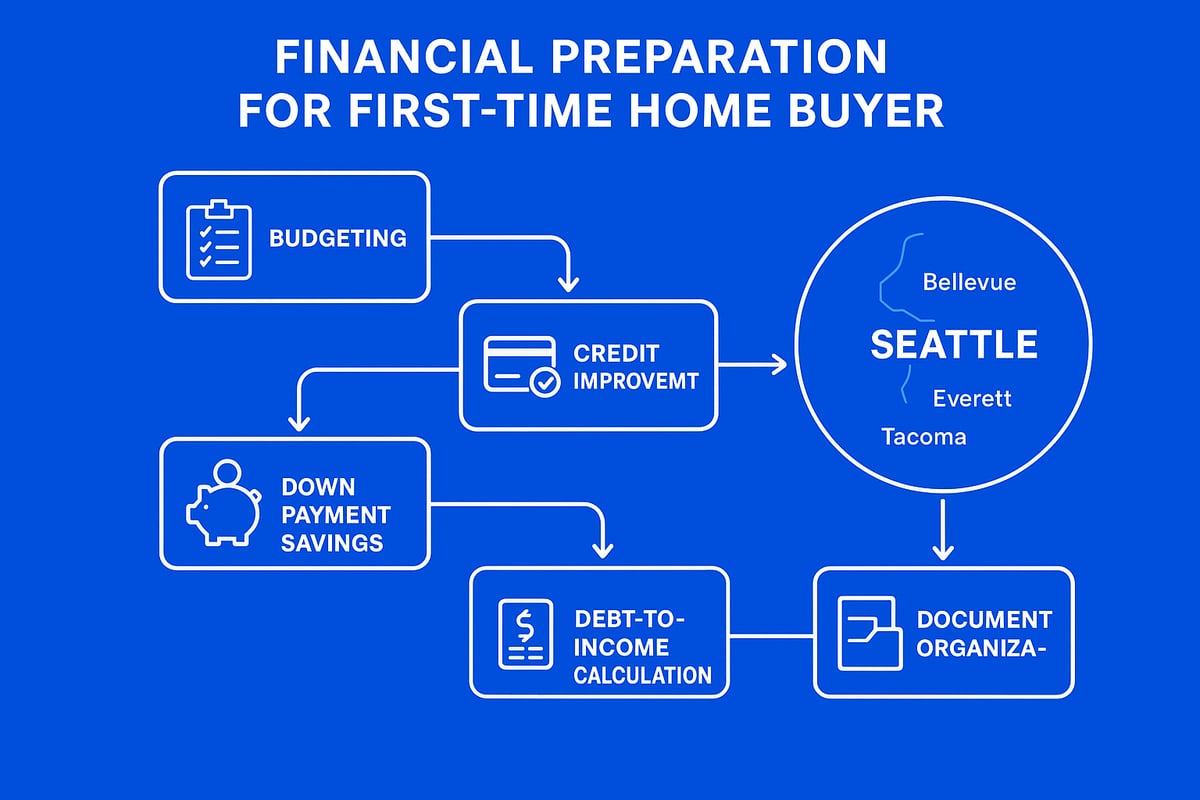

Assessing Your Budget and Affordability

Start by calculating your total monthly housing costs for a first time home buyer home in Seattle. This includes your mortgage payment, property taxes, homeowner’s insurance, utilities, and any HOA dues. In 2026, the median home price in Seattle means monthly payments may be higher than in Everett or Shoreline, so use a local mortgage calculator for accuracy.

Break down your budget like an Everett buyer might, comparing principal, interest, taxes, and insurance. Always include an emergency savings cushion to handle unexpected costs. As a rule of thumb, keep your total housing costs below 30 percent of your gross income. This strategy ensures your first time home buyer home purchase is both comfortable and sustainable.

Understanding and Improving Your Credit Score

Your credit score plays a pivotal role in qualifying for a first time home buyer home loan. FHA loans generally require a minimum score of 580 for 3.5 percent down, while conventional loans often need 620 or higher. The higher your score, the better your rate and approval odds.

To boost your score, pay down revolving debt, dispute any errors, and avoid opening new credit accounts before applying. For example, a Lynnwood resident who raised their score from 600 to 680 saw significant savings over the life of their first time home buyer home mortgage. Use free credit monitoring tools, and check your score at least six months before starting your home search.

Saving for Down Payment and Closing Costs

Saving for a first time home buyer home in Seattle means preparing for both down payment and closing costs. Most conventional loans require 3 to 5 percent down, FHA loans need 3.5 percent, and VA loans offer zero down for eligible buyers. Closing costs typically range from 2 to 5 percent of the purchase price across Seattle, Mill Creek, and Everett.

Local down payment assistance programs can make a big difference. For example, a Mill Creek buyer reduced upfront costs by combining savings with city grants. Gift funds from family are allowed, but must be properly documented. For more strategies, see this guide to down payment options for conventional loans. Automate your savings and review discretionary spending to reach your goal faster.

Debt-to-Income Ratio (DTI) and Other Qualifying Factors

Lenders in Seattle and surrounding areas closely examine your debt-to-income ratio when approving a first time home buyer home loan. Most prefer a DTI below 43 percent, though some programs allow up to 50 percent. Factor in car loans, student loans, and credit cards.

If your DTI is high, consider paying off smaller debts, as a Lake Forest Park buyer did by eliminating a car payment. Stable employment history—ideally two years—is preferred, but exceptions exist for those with non-traditional income like bonuses or RSUs. Lower DTI gives you access to more loan options and helps you secure better terms on your first time home buyer home.

Building a Strong Financial Paper Trail

Organizing your documentation is critical for a smooth first time home buyer home transaction. Start by collecting clean bank statements, pay stubs, tax returns, and rental history. Avoid large unexplained deposits, as lenders will require sources for all funds.

For example, an Everett buyer who kept 12 months of rent checks and organized tax documents closed their first time home buyer home 20 percent faster. Respond promptly to lender requests and keep financial records updated. A well-prepared file streamlines approval and positions you as a strong buyer in Seattle’s competitive market.

Exploring First-Time Homebuyer Loan Programs and Assistance

Navigating the first time home buyer home journey in Seattle and surrounding cities requires a clear understanding of mortgage options and assistance programs. With 2026 bringing new opportunities and programs, buyers in Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett need tailored guidance. Let’s break down the essential loan programs and resources every first time home buyer home in the region should know.

Overview of 2026 Loan Program Options

For a first time home buyer home in Seattle, understanding loan options is crucial. FHA loans remain a popular choice, requiring just 3.5% down and offering flexibility for buyers with lower credit. Conventional loans can be secured with as little as 3% down for first timers, but often require a higher credit score.

VA loans provide 0% down for eligible veterans in Everett and Lynnwood. USDA loans are limited in the metro area but are available in some outlying communities. Washington State Housing Finance Commission (WSHFC) and city-based programs add further options. For example, a Shoreline buyer might compare FHA and WSHFC programs to find the best fit for their first time home buyer home needs.

Down Payment and Closing Cost Assistance Programs

Seattle-area buyers can access several down payment and closing cost assistance programs. The Seattle Home Advantage DPA, House Key Opportunity, and city grants help bridge the affordability gap for a first time home buyer home. Local programs in Everett and Lynnwood provide additional support, with eligibility based on income and purchase price.

For instance, a Mill Creek buyer may secure a $10,000 grant to reduce upfront costs. To learn more about eligibility, application process, and available funds, visit the Seattle Office of Housing Down Payment Assistance page. Remember, grants and loans have different repayment terms, so review each program closely before applying.

Understanding FHA, Conventional, and Other Loan Types

Selecting the right mortgage type is a key decision for a first time home buyer home. FHA loans are ideal for buyers with lower credit, though they include higher mortgage insurance. Conventional loans typically have stricter qualifications but offer lower long-term costs.

VA loans, available to veterans and active-duty military in areas like Lynnwood and Everett, require no down payment and do not carry private mortgage insurance. Jumbo loans are necessary for high-value homes in Seattle or Bellevue, with loan limits above $1,037,300. For example, a tech worker in Bellevue might use a jumbo loan to purchase a $1.5M property. Matching the loan type to your financial profile ensures you maximize affordability and security.

| Loan Type | Min Down Payment | Credit Score | Key Features | Ideal For |

|---|---|---|---|---|

| FHA | 3.5% | 580+ | Flexible credit, higher insurance | Lower-credit buyers |

| Conventional | 3% (first timers) | 620+ | Lower insurance, stricter guidelines | Buyers with strong credit |

| VA | 0% | 620+ | No PMI, for veterans/active-duty | Eligible military/veterans |

| Jumbo | 10–20% | 700+ | For homes above $1,037,300 | High-value Seattle/Bellevue buys |

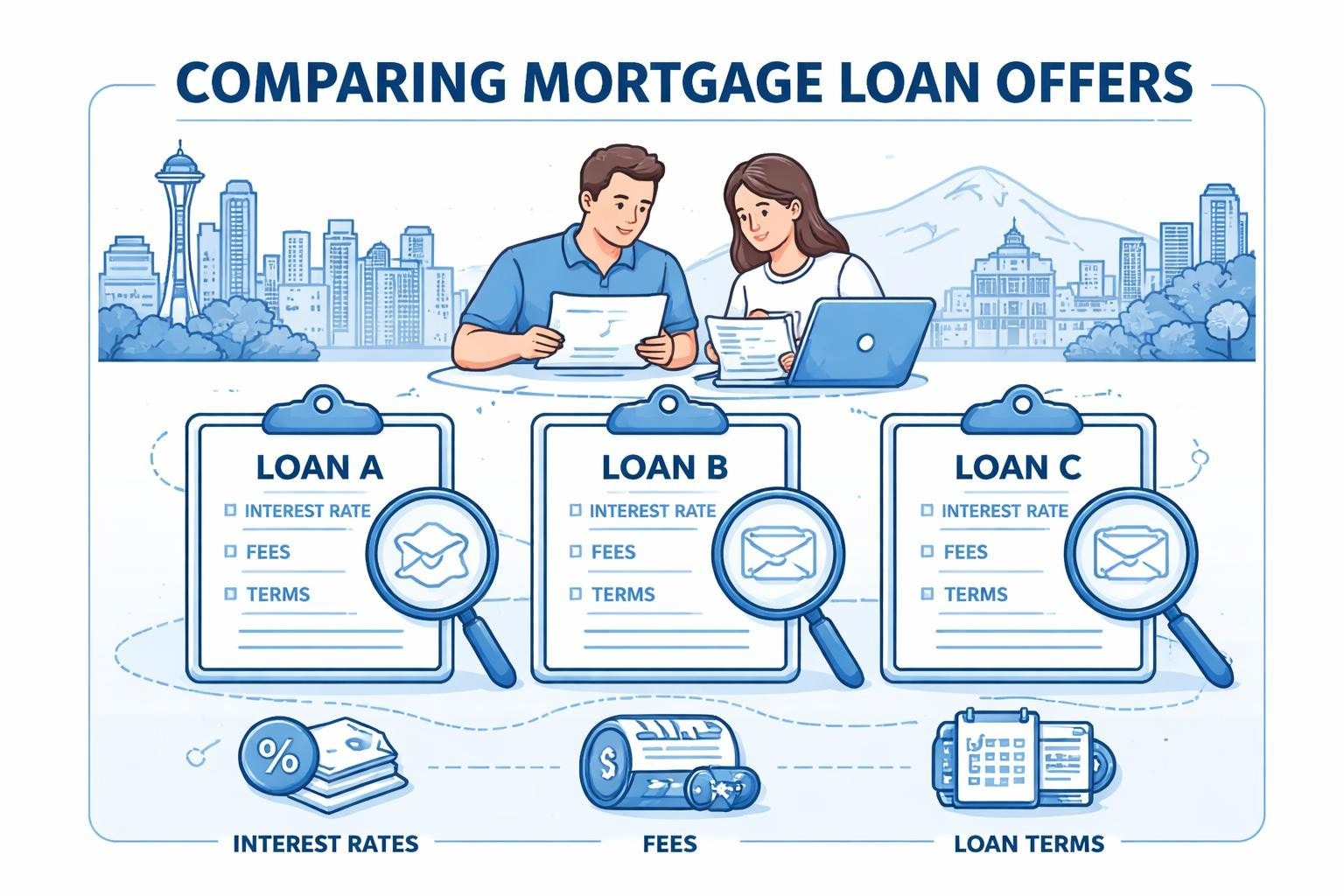

Comparing Interest Rates, Terms, and Fees

Interest rates and loan terms can vary significantly for a first time home buyer home in Seattle. FHA loans may offer slightly higher rates compared to conventional, but can be more accessible. In 2026, Seattle buyers can expect rates to be a bit higher than in previous years, so shopping for the best option is essential.

Always compare the APR, not just the base interest rate, to understand total loan costs. Typical lender fees in Seattle include origination, underwriting, and appraisal costs. For example, an Everett buyer who compares multiple lenders might save $5,000 over the life of the loan. Even a 0.25% difference in rate can change your monthly payment by $50 or more, so review terms carefully.

Navigating Pre-Approval and Lender Selection

Securing pre-approval is a necessary step for a first time home buyer home in Seattle’s competitive market. Pre-approval not only clarifies your budget, it also strengthens your offer. Gather documents such as income statements, asset records, and identification early.

Local lenders often provide better service and understand unique Seattle-area needs compared to national banks. For example, a Shoreline buyer who gets pre-approved before touring homes is more likely to secure their desired property. Remember to ask about lender closing timelines, as a 9-21 day close is considered competitive in this region.

Working with a Trusted Seattle Mortgage Broker

A trusted local mortgage broker can be a valuable partner for a first time home buyer home, especially in Seattle, Bellevue, and surrounding cities. Brokers offer education, strategic advice, and access to a wide range of loan programs, including WSHFC and city grants.

If you have complex compensation, such as RSUs or stock options from Amazon or Microsoft, a broker can help structure your application for maximum approval potential. For instance, a Redmond buyer may use RSUs as part of their down payment with broker guidance. Brokers also streamline the process, offering transparent explanations of terms, fees, and helping many buyers close in as little as nine business days. This support ensures you get the most from your first time home buyer home experience.

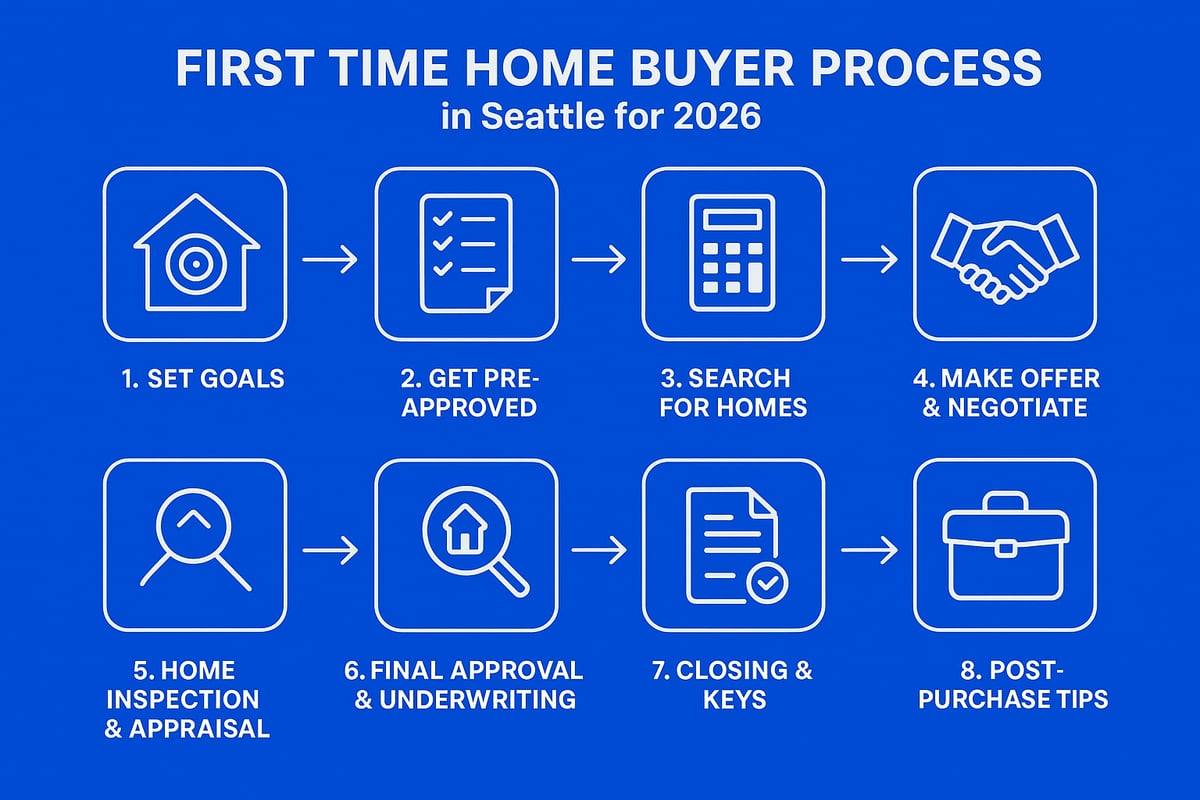

Step-by-Step Guide: The First-Time Home Buying Process in Seattle

Navigating the first time home buyer home process in Seattle in 2026 can feel overwhelming, but having a clear roadmap makes all the difference. As a local mortgage broker, I have seen buyers in Seattle, Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett succeed by following a structured, step-by-step approach. This guide will walk you through each critical stage to help you secure your first time home buyer home with confidence.

Step 1: Set Your Homebuying Goals and Timeline

Start your first time home buyer home journey by clarifying your must-haves and nice-to-haves. Consider the size, number of bedrooms, commute times, school districts, and neighborhood amenities in Seattle and nearby cities like Shoreline or Mill Creek.

Write down your timeline. Are you aiming for a summer 2026 move-in, or do you have more flexibility? Setting a clear timeline helps you stay focused and align your search with the Seattle market realities.

Buyers with written goals are twice as likely to close on time. Take time to discuss your needs with any co-buyers. Staying organized at this stage can prevent costly setbacks later on.

Step 2: Get Pre-Approved for a Mortgage

Pre-approval is essential for a first time home buyer home in Seattle’s fast-paced market. Pre-approval shows sellers you are a serious, qualified buyer and gives you a clear budget.

Gather documents early, including pay stubs, W-2s, tax returns, and bank statements. Your lender will review your credit, employment, and assets. In Everett and Lynnwood, buyers with strong pre-approval letters often win in multiple-offer situations.

Remember, pre-qualification is not the same as pre-approval. Update your pre-approval if your financial situation or interest rates change. This step gives you a competitive edge from the start.

Step 3: Search for Homes in Seattle and Surrounding Cities

With pre-approval in hand, begin your first time home buyer home search using local MLS, Redfin, or Zillow. Expand your horizons by touring homes in Shoreline, Mill Creek, Lake Forest Park, and Everett for more options and potential savings.

Tour open houses, schedule private showings, or use virtual tours if needed. Evaluate each neighborhood for safety, schools, walkability, and future growth potential.

Being flexible about location can help you find better value. For instance, a Mill Creek buyer may discover larger homes or newer construction compared to Seattle’s core neighborhoods.

Step 4: Make an Offer and Negotiate

Making a strong, competitive offer is crucial in Seattle’s 2026 market. Consider key elements like earnest money, contingencies, and escalation clauses. In Lake Forest Park, buyers may win with flexible closing dates or seller credits.

Seattle often sees multiple offers and appraisal gaps, so work closely with your agent and lender to craft a winning strategy. For actionable strategies, check out this home buying strategies guide.

Negotiation doesn’t end with price. You can negotiate repairs, closing costs, or even appliances. Preparation and speed are your best allies when making an offer.

Step 5: Home Inspection and Appraisal

A thorough inspection is vital for any first time home buyer home, especially in older Seattle properties. Common issues include foundation cracks, aging roofs, and older plumbing, which are often found in Everett and Lynnwood homes.

Schedule your inspection quickly to allow time for negotiation if issues arise. The appraisal confirms the home’s market value and can impact your loan approval.

If the appraisal comes in low, discuss options with your lender and agent. Never skip the inspection, even in a highly competitive market, to avoid costly surprises later.

Step 6: Final Loan Approval and Underwriting

During underwriting, your lender reviews all documentation for your first time home buyer home purchase. They will verify your income, assets, and property details.

Respond promptly to any requests for additional paperwork. Delays often occur due to missing documents or last-minute financial changes. For example, an Everett buyer who pre-submits all documentation can close early.

Avoid opening new credit accounts or making large purchases until after closing. Staying in close contact with your lender ensures a smoother approval process.

Step 7: Closing and Getting the Keys

At closing, you will review and sign final documents, pay closing costs, and transfer funds. In Seattle and surrounding areas, you may have the option of remote or in-person signings.

Review your settlement statement to ensure accuracy. Once everything is complete, you will receive the keys to your first time home buyer home, often within a day of closing.

The average closing time in Seattle in 2026 is 21 to 30 days, but organized buyers can sometimes close even faster, especially with early document preparation.

Step 8: Post-Purchase Tips for New Homeowners

After moving into your first time home buyer home, set up utilities, update your insurance, and change your address. Create a maintenance schedule to protect your investment and plan for property tax and insurance payments.

Build an emergency fund for unexpected repairs. Connect with local resources, such as neighborhood associations or Seattle-area homeownership classes, for ongoing support.

For example, Shoreline homeowners benefit from joining community groups, which provide valuable connections and advice. Staying engaged helps you make the most of your new home.

Navigating Seattle’s 2026 Housing Market: Trends, Challenges, and Opportunities

For any first-time home buyer home search in Seattle, understanding the market landscape is essential. The region, including Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett, is experiencing evolving trends, unique challenges, and new opportunities that shape the path to homeownership.

Seattle Market Overview and 2026 Projections

Seattle’s 2026 housing market remains competitive, with the median home price projected to rise about 4%, outpacing national averages. Inventory is expected to improve slightly, particularly in Mill Creek and Lake Forest Park, offering more options for buyers. Interest rates are forecasted to remain steady but higher than in previous years.

According to Seattle Housing Market Trends 2026, the median price for a first time home buyer home in Seattle is now about 5% higher than in 2023, while Everett and Shoreline offer more affordable alternatives. Tech sector growth continues to drive demand, making quick decision-making vital for buyers.

Competitive Offer Strategies for First-Time Buyers

Navigating the first time home buyer home process in Seattle’s fast-paced market calls for well-planned strategies. Pre-inspections, escalation clauses, and flexible closing timelines can give buyers an edge, especially when multiple offers are common.

Consider these tips:

- Prepare a strong pre-approval letter

- Offer higher earnest money deposits

- Use local market data to inform your offer price

Waiving certain contingencies can strengthen your offer, but always balance risk with professional advice. As shown in recent Seattle Housing Market Forecast 2026, preparation and speed are crucial, especially in Shoreline, Lynnwood, and Everett, where bidding wars still occur.

Affordable Neighborhoods and Hidden Gems Near Seattle

Finding an affordable first time home buyer home near Seattle takes local insight. Lynnwood, Mill Creek, and Lake Forest Park have emerged as up-and-coming areas, offering more value per square foot than the Seattle core.

A quick comparison:

| Area | Median Price (2026) | Value per Sq. Ft. |

|---|---|---|

| Seattle | $850,000 | High |

| Everett | $600,000 | Moderate |

| Shoreline | $700,000 | Moderate |

| Mill Creek | $650,000 | Moderate/Low |

Transit-friendly communities like Shoreline and Everett appeal to commuters, while Mill Creek offers newer homes and strong amenities. Expanding your search radius can increase affordability and help you find the right fit.

Leveraging Local Homebuyer Resources and Counseling

Maximizing your success as a first time home buyer home in the Seattle area means tapping into local resources. Nonprofits like HomeSight and Urban League, along with the Washington State Housing Finance Commission (WSHFC), provide free education, workshops, and down payment assistance.

Many city programs, including those in Everett and Shoreline, offer grants or special financing for qualified buyers. Completing a WSHFC class can unlock valuable benefits, such as below-market rates or additional support. Start early, as these resources can streamline your journey and boost your confidence throughout the process.

Frequently Asked Questions for Seattle First-Time Home Buyers

Seattle’s real estate market brings unique questions for those starting the journey as a first time home buyer home purchaser. Below, I address the most common FAQs I encounter as a Seattle-area mortgage broker, with examples from Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett.

What Credit Score Do I Need to Buy a Home in Seattle?

For a first time home buyer home purchase in Seattle, most lenders require a minimum credit score of 580 for FHA loans and 620 for conventional loans. However, the best rates typically go to buyers with scores above 740. Some Seattle-area lenders may be flexible, especially for buyers in Everett or Lynnwood.

If you are just short of the threshold, focus on paying down debts and correcting credit report errors. For example, an Everett first time home buyer home applicant improved their score from 610 to 670 in six months, unlocking better loan terms. Always review your credit early so you have time to boost your score before applying.

How Much Down Payment Is Required in Seattle?

A first time home buyer home in Seattle can often be purchased with as little as 3 percent down for conventional loans or 3.5 percent for FHA. VA loans require no down payment for eligible buyers in cities like Shoreline or Mill Creek.

Many first time home buyer home purchasers use down payment assistance or gift funds to lower upfront costs. For instance, a Shoreline client recently bought a home with just $8,000 down thanks to local grant programs. More than 40 percent of Seattle first time home buyer home purchases close with less than 5 percent down.

Can I Use RSUs, Bonuses, or Stock as Income?

Yes, in the Seattle area, using RSUs, bonuses, or stock as qualifying income is common for a first time home buyer home, especially for tech employees at Amazon, Microsoft, or Google. Lenders require a documented history of receiving these assets, and each has specific guidelines.

A Redmond buyer recently used RSUs to qualify for a first time home buyer home loan, but needed detailed statements and employer verification. It is crucial to work with a lender or first-time home buyer broker guide experienced with tech compensation to ensure your income is counted correctly.

What Are Typical Closing Costs in Seattle?

For a first time home buyer home purchase in Seattle, closing costs generally range from 2 percent to 5 percent of the purchase price. These costs include lender fees, title insurance, escrow, and taxes. In Mill Creek and Lake Forest Park, buyers often negotiate for seller credits to help cover these expenses.

For more detailed breakdowns and current data, the Seattle Housing Market Update 2026 provides recent examples of closing costs and market trends. Always request a Loan Estimate early so you can budget for your first time home buyer home closing with confidence.

As you take your first steps toward buying a home in Seattle, it’s normal to have questions about eligibility, loan programs, and how to make your offer stand out in a fast-paced market. I’m here to help you navigate each stage with clarity and confidence, whether you’re exploring neighborhoods or sorting through financial details. If you’d like personalized guidance tailored to your unique situation—even if you’re just starting your research—let’s connect for a friendly, no pressure conversation about your homebuying goals and next steps.

Let’s have a conversation

Key Takeaways

- The First Time Home Buyer Home Guide Tips for 2026 offers essential advice for navigating Seattle’s competitive real estate market.

- Homeownership eligibility depends on local and national rules; understanding these definitions is critical before beginning your search.

- Preparing your finances, understanding loan options, and utilizing local resources can enhance your chances of success in 2026.

- Prospective buyers should know myths and misconceptions about first-time homeownership, such as previous ownership affecting eligibility.

- Seattle’s housing market is evolving, and buyers need to stay informed about trends, potential challenges, and opportunities.

Estimated reading time: 23 minutes

In Seattle, a first-time home buyer is typically someone who hasn’t owned a primary residence in the past three years, though some programs allow exceptions. Eligibility varies by loan and assistance program, so confirming early helps avoid surprises.

Many Seattle first-time home buyers can purchase with 3% down on conventional loans, 3.5% down on FHA loans, or 0% down with VA loans if eligible. Down payment assistance programs can further reduce required cash.

Yes, Seattle and King County offer down payment assistance programs that provide low-interest loans or deferred payments for qualified buyers. These are often layered with Washington State Housing Finance Commission programs.

Common options include FHA loans, low-down-payment conventional loans, VA loans for eligible veterans, and Washington State Housing Finance Commission programs. The best choice depends on income, credit profile, and long-term plans.

Many Seattle-area first-time buyer assistance programs require a certified homebuyer education course. Even when not required, these classes help buyers understand financing, inspections, and the competitive local market.

Most FHA loans allow credit scores as low as 580, while conventional loans often require 620 or higher. In Seattle’s competitive market, stronger credit can improve rates and offer strength.

Mortgage pre-approval typically takes one to three weeks once documents are submitted. A solid pre-approval is essential for Seattle first-time buyers competing in fast-moving neighborhoods.

Closing costs in Seattle generally range from 2% to 5% of the purchase price and include lender fees, title, escrow, and prepaid items. Some buyers negotiate seller credits to reduce upfront costs.

Yes, many Seattle lenders allow documented RSUs, bonuses, or variable income to qualify, especially for tech employees. Specific guidelines apply, so early review with a lender is important.

Seattle’s higher home prices and competition can be challenging, but preparation, smart loan strategy, and local assistance programs help first-time buyers compete successfully and avoid overextending financially.

Many Seattle first-time home buyers can purchase with 3% down on conventional loans, 3.5% down on FHA loans, or 0% down with VA loans if eligible. Down payment assistance programs can further reduce required cash.

Yes, Seattle and King County offer down payment assistance programs that provide low-interest loans or deferred payments for qualified buyers. These are often layered with Washington State Housing Finance Commission programs.

Common options include FHA loans, low-down-payment conventional loans, VA loans for eligible veterans, and Washington State Housing Finance Commission programs. The best choice depends on income, credit profile, and long-term plans.

Many Seattle-area first-time buyer assistance programs require a certified homebuyer education course. Even when not required, these classes help buyers understand financing, inspections, and the competitive local market.

Most FHA loans allow credit scores as low as 580, while conventional loans often require 620 or higher. In Seattle’s competitive market, stronger credit can improve rates and offer strength.

Mortgage pre-approval typically takes one to three weeks once documents are submitted. A solid pre-approval is essential for Seattle first-time buyers competing in fast-moving neighborhoods.

Closing costs in Seattle generally range from 2% to 5% of the purchase price and include lender fees, title, escrow, and prepaid items. Some buyers negotiate seller credits to reduce upfront costs.

Yes, many Seattle lenders allow documented RSUs, bonuses, or variable income to qualify, especially for tech employees. Specific guidelines apply, so early review with a lender is important.

Seattle’s higher home prices and competition can be challenging, but preparation, smart loan strategy, and local assistance programs help first-time buyers compete successfully and avoid overextending financially.