Finding good mortgage lenders in Seattle requires more than comparing advertised rates on a website. The best lending partners combine competitive pricing with expert guidance, transparent communication, and proven execution in competitive markets. Whether you're buying your first home in Shoreline, refinancing in Lynnwood, or securing a jumbo loan for a property in Lake Forest Park, the lender you choose directly impacts your closing timeline, loan terms, and overall experience. This guide explains what separates truly good mortgage lenders from the rest, and how to identify the right partner for your Seattle-area home purchase or refinance.

What Makes Good Mortgage Lenders Stand Out

The mortgage industry includes banks, credit unions, online lenders, and local brokers-all offering different advantages. Good mortgage lenders distinguish themselves through consistent performance across several key areas that matter most to borrowers.

Transparency in Pricing and Fees

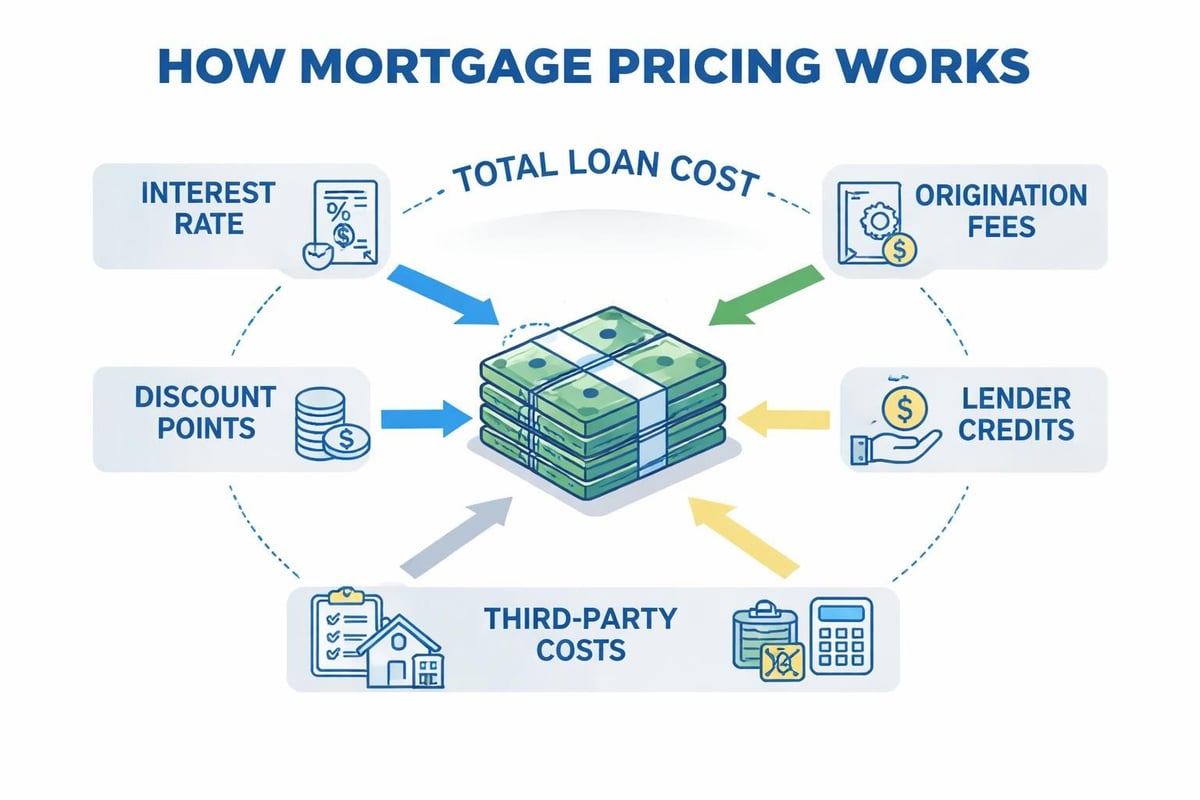

Upfront disclosure separates trustworthy lenders from those who hide costs until closing. The best lenders provide detailed Loan Estimates within three business days of application, clearly breaking down origination fees, discount points, third-party costs, and lender credits.

When evaluating pricing transparency, look for these qualities:

- Willingness to explain every line item on the Loan Estimate

- Clear communication about how rate and fees trade off

- No surprise charges appearing at closing

- Written documentation of all verbal promises

- Honest discussion of all-in costs versus advertised rates

The Better Business Bureau emphasizes the importance of comparing multiple lenders and understanding all associated fees before committing to a mortgage partner.

Communication and Responsiveness

In Seattle's competitive housing market, where buyers in Mill Creek and Everett often face multiple-offer situations, a lender's communication speed can determine whether your offer succeeds. Good mortgage lenders respond to questions within hours, not days, and proactively update you throughout the process.

Communication quality includes several measurable factors:

| Communication Factor | What to Expect | Red Flag |

|---|---|---|

| Initial response time | Within 4 hours on business days | Next-day or slower response |

| Preapproval turnaround | 24-48 hours with complete docs | 5+ days without explanation |

| Update frequency | Proactive weekly check-ins minimum | Only responds when contacted |

| Availability | Evenings/weekends during transaction | Strictly business hours only |

| Technology options | Text, email, phone, video options | Phone-only communication |

Your lender should feel like a partner, not a vendor. That means anticipating your questions, explaining complex guidelines in plain language, and keeping all parties informed throughout the transaction.

Types of Mortgage Lenders and Their Strengths

Understanding the different types of mortgage lenders helps you choose the right fit for your specific situation and priorities.

Banks and Credit Unions

Traditional banks offer the security of established institutions and sometimes relationship pricing for existing customers. Credit unions typically provide competitive rates for members and personalized service in their local communities.

Banks work best when you value name recognition, have existing banking relationships, and your loan fits standard guidelines. They excel with straightforward W-2 income and conventional financing.

Credit unions shine for borrowers seeking relationship-based lending, those with membership eligibility, and buyers who prefer local decision-making. They often show flexibility for members with long banking histories.

Online Mortgage Lenders

Digital-first lenders streamline the application process with automated underwriting, online document uploads, and 24/7 account access. CNBC Select reviews highlight several online lenders known for competitive rates and user-friendly platforms.

Advantages include:

- Lower overhead translating to competitive rates

- Convenient digital application and document submission

- Automated status updates and milestone tracking

- Quick preapprovals for standard scenarios

Limitations to consider:

- Less personal guidance for complex income situations

- Limited local market knowledge for Seattle-specific strategies

- Potential challenges with non-standard scenarios like stock compensation

- Customer service may not match local broker accessibility

Mortgage Brokers

Brokers access multiple wholesale lenders, allowing them to shop rates and programs on your behalf. A Seattle mortgage broker with local market expertise brings particular value in competitive neighborhoods where timing and strategy matter.

Broker advantages include program diversity, personalized guidance, and the ability to match complex income situations with appropriate lenders. They excel with jumbo loans, self-employed borrowers, and buyers using stock compensation or bonuses for qualifying income.

For tech professionals in Seattle working at Amazon, Microsoft, or Google, brokers who specialize in qualifying RSUs and equity compensation provide significant advantages. They understand how different lenders underwrite vesting schedules, exercise strategies, and bonus income-often unlocking higher purchasing power than traditional banks.

Key Factors to Evaluate When Choosing Lenders

Selecting good mortgage lenders requires systematic evaluation across multiple criteria that impact both your immediate transaction and long-term satisfaction.

Rate and Fee Comparison

Interest rates fluctuate daily, but the pattern of a lender's pricing relative to market averages reveals their competitiveness. Good mortgage lenders price within a reasonable range of wholesale rates while maintaining service quality.

Compare the Annual Percentage Rate (APR) rather than just the note rate. APR incorporates fees, giving you a more accurate cost comparison. A slightly higher rate with lower fees often costs less over time than a low rate buried in expensive origination charges.

Request detailed quotes from at least three lenders for the same:

- Loan amount and program type

- Lock period (typically 30-45 days)

- Down payment percentage

- Credit score range

- Property type and use

The American Bankers Association recommends reviewing loan basics and comparing multiple quotes to ensure you understand the full cost structure.

Closing Speed and Reliability

In hot markets like Shoreline and Lake Forest Park, the ability to close quickly strengthens your offer. Standard closing timelines run 30-45 days, but good mortgage lenders with efficient processing can close purchase transactions in as few as 14-21 days when needed.

Ask specific questions about their track record:

- What percentage of loans close on the original timeline?

- What's their average time from application to clear-to-close?

- Do they have in-house processing and underwriting?

- Can they accommodate accelerated timelines when necessary?

- What's their process for handling last-minute issues?

Lenders who consistently deliver on promised timelines demonstrate operational competence and appropriate staffing levels. Those who frequently request extensions or surprise borrowers with last-minute conditions signal process problems.

Loan Program Variety

Your financial situation may not fit the standard conventional loan mold. Good mortgage lenders offer diverse programs to serve different borrower profiles and property types.

Essential program options include:

- Conventional loans (conforming and jumbo)

- FHA financing for lower down payments

- VA loans for eligible veterans and service members

- USDA loans for qualifying suburban and rural properties

- Portfolio products for unique situations

- Construction-to-permanent financing

- Investment property programs

First-time home buyer lenders particularly benefit from working with lenders who offer FHA, conventional low-down-payment options, and down payment assistance programs specific to Washington State.

Technology and Tools That Signal Quality Lenders

Modern mortgage lending combines personal service with technological efficiency. The tools a lender provides reveal their investment in client experience and operational excellence.

Digital Application and Document Management

Good mortgage lenders offer secure online portals where you can complete applications, upload documents, and track your loan progress in real time. This technology saves time and reduces the back-and-forth of email document exchanges.

Look for platforms that provide:

- Mobile-friendly application access

- Automatic document recognition and categorization

- Real-time task lists showing outstanding requirements

- Secure messaging with your loan team

- Electronic signature capabilities

- Automated status updates via text or email

Security matters tremendously when sharing sensitive financial information. Verify that lenders use bank-level encryption, multi-factor authentication, and comply with data protection regulations.

Online Calculators and Education Resources

Lenders confident in their expertise provide educational tools that empower borrowers to make informed decisions. Quality resources include mortgage calculators, buying power estimators, and educational content about different loan programs.

These tools demonstrate a lender's commitment to borrower education rather than just transaction volume. NerdWallet’s mortgage reviews often highlight lender educational resources as a key differentiator in their evaluations.

Verifying Lender Credentials and Reputation

Professional credentials and third-party validation help you distinguish legitimate, competent lenders from those cutting corners or lacking proper oversight.

Licensing and Regulatory Compliance

All mortgage lenders must be licensed and comply with state and federal regulations. In Washington State, verify that individual loan officers hold active Mortgage Loan Originator (MLO) licenses through the Nationwide Multistate Licensing System (NMLS).

Check these verification points:

- Active NMLS license number

- No disciplinary actions or complaints

- Years of licensing history

- Company licensing in Washington State

- Membership in professional organizations

Compliance with regulations like TRID (TILA-RESPA Integrated Disclosure) and qualified mortgage rules ensures lenders follow consumer protection standards designed to prevent predatory lending practices.

Reviews and References

Third-party reviews on Google, Zillow, Yelp, and the Better Business Bureau provide unfiltered feedback from past clients. Good mortgage lenders accumulate hundreds of verified reviews demonstrating consistent service quality.

When reading reviews, look for patterns rather than individual comments:

| Review Pattern | Positive Signal | Concern |

|---|---|---|

| Volume | 100+ reviews | Fewer than 20 reviews |

| Recency | Regular new reviews monthly | Old reviews only |

| Response rate | Lender responds to concerns | No engagement with feedback |

| Specific details | Names, dates, specific scenarios | Generic or vague praise |

| Common themes | Consistency across reviews | Wildly varying experiences |

Ask for references from recent clients with situations similar to yours. A lender confident in their service readily provides contact information for satisfied customers. Speaking with someone who recently purchased in Everett or Lynnwood gives you market-specific insights.

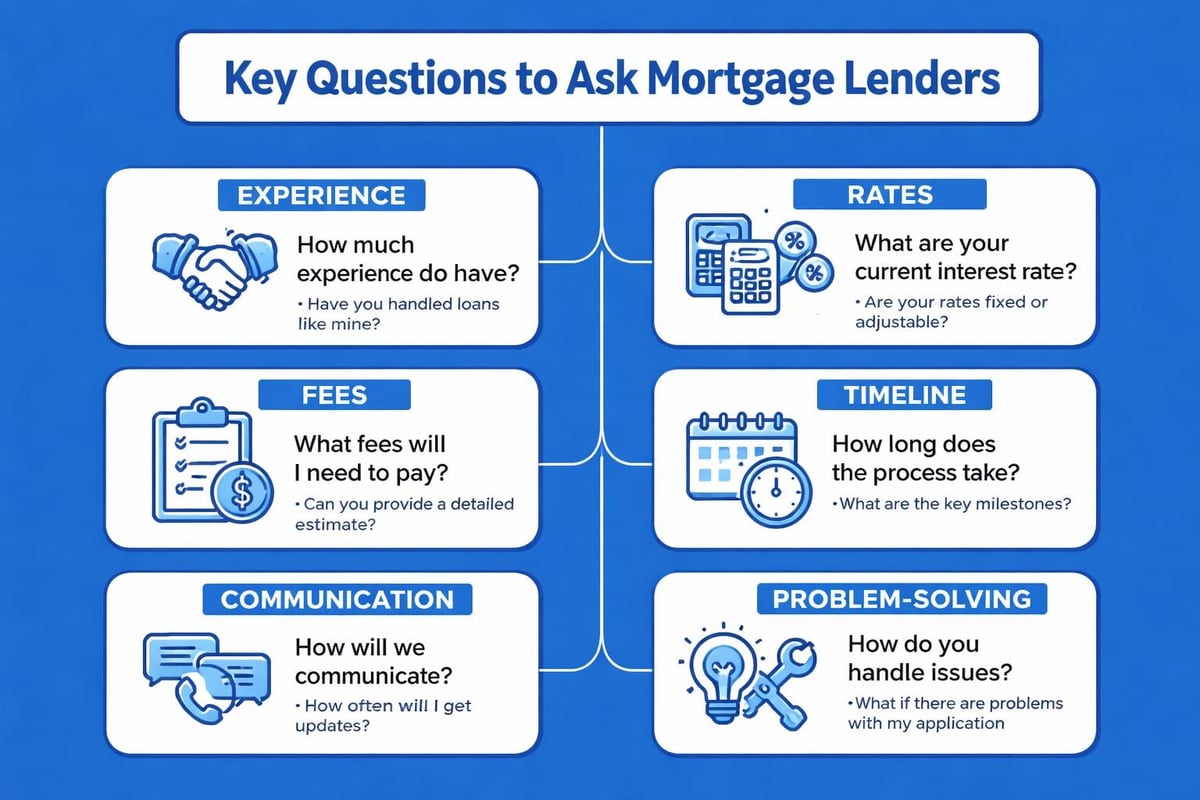

Questions to Ask Potential Lenders

The right questions during your initial lender conversations reveal their expertise, transparency, and fit for your needs.

About Their Experience and Specialization

Start by understanding their background and areas of focus:

- How long have you been originating mortgages?

- What percentage of your business comes from the Seattle area?

- Do you specialize in any particular loan types or borrower situations?

- How many loans do you close monthly?

- What's your experience with buyers in my price range?

Specialists in your specific situation-whether that's FHA financing options, jumbo loans, or self-employment income-bring valuable expertise that generalists may lack.

About Their Process and Timeline

Understanding their workflow helps set realistic expectations:

- What documents do you need to issue a preapproval?

- How long does your underwriting process typically take?

- What's your average time from application to closing?

- How do you communicate updates during the process?

- Who will I work with throughout the transaction?

- What happens if issues arise during underwriting?

Vague answers or reluctance to commit to timelines suggests disorganization or insufficient staffing. Good mortgage lenders confidently explain their process with specific timeframes and clear accountability.

About Rates and Costs

Financial transparency begins with direct questions:

- What rate can you offer for my scenario today?

- How do your rates compare to current market averages?

- What fees do you charge, and which are negotiable?

- How much will I pay in total closing costs?

- Can you provide a written Loan Estimate for this conversation?

- How long can you lock this rate?

- What happens if rates drop after I lock?

Good mortgage lenders welcome these questions and provide detailed answers with written documentation. Those who hedge, deflect, or pressure you to commit before providing clear pricing warrant caution.

Working with Lenders on Complex Income Situations

Standard W-2 employment represents the simplest income scenario for mortgage qualification. Tech professionals, business owners, and commissioned salespeople require lenders with deeper underwriting expertise.

Stock Compensation and Equity Income

Amazon, Microsoft, Google, and Seattle's other major tech employers compensate employees significantly through Restricted Stock Units (RSUs), stock options, and Employee Stock Purchase Plans (ESPPs). Not all lenders understand how to maximize qualifying income from these sources.

RSU qualification depends on several factors:

- Vesting schedule and frequency

- Historical vesting pattern (typically 2 years)

- Current stock price versus grant price

- Tax withholding methodology

- Documentation from employer HR

Good mortgage lenders experienced with tech compensation know which documentation satisfies underwriters, how to calculate averaged income from variable vesting amounts, and which programs allow the highest percentage of RSU income for qualifying.

Self-Employment and Business Ownership

Self-employed borrowers and business owners face additional documentation requirements and income calculation methods. Lenders must analyze tax returns, profit-and-loss statements, and business structures to determine qualifying income.

The complexity increases with:

- Schedule C sole proprietors versus S-Corp or partnership structures

- Industry-specific deductions and depreciation

- Multiple businesses or income streams

- Recent business start dates (less than 2 years)

- Declining versus increasing income trends

Specialized lenders understand how to present self-employment income favorably within underwriting guidelines, potentially qualifying you for larger loan amounts than less experienced lenders.

Local Market Knowledge Matters in Seattle

National online lenders and major banks offer competitive rates, but local Seattle market expertise provides strategic advantages that impact your success in multiple-offer scenarios.

Understanding Seattle's Competitive Landscape

Good mortgage lenders familiar with Seattle, Shoreline, Lynnwood, and surrounding markets understand what makes offers competitive beyond just price. They know which appraisal management companies work efficiently, which title companies close quickly, and how to structure offers that appeal to sellers.

Local expertise includes:

- Typical days-on-market for different price ranges and neighborhoods

- Common contingency periods that remain competitive

- Appraisal challenges in specific areas

- HOA approval timelines for condominiums

- Title issue frequency in older neighborhoods

- Tax considerations specific to Washington State

A lender closing dozens of Seattle-area loans monthly recognizes patterns and potential issues before they derail your transaction. They provide realistic guidance about timelines, offer strategy, and local market conditions.

Relationships with Local Real Estate Professionals

Real estate agents, title companies, and escrow officers form the transaction team alongside your lender. Good mortgage lenders maintain strong professional relationships built through reliable execution and clear communication.

These relationships benefit you through:

- Smoother coordination between transaction parties

- Faster issue resolution when challenges arise

- Professional referrals and recommendations

- Collaborative problem-solving approach

- Enhanced credibility of your preapproval letter

Top agents in Mill Creek, Everett, and Lake Forest Park know which lenders consistently close on time and which create last-minute problems. Their willingness to work with your lender signals market reputation earned through proven performance.

Red Flags That Indicate Poor Lenders

Recognizing warning signs early protects you from frustrating experiences, missed opportunities, and potentially predatory lending practices.

Pressure Tactics and Rushed Decisions

Good mortgage lenders educate and guide without pressuring. Be wary of lenders who:

- Push you to submit an application before answering your questions

- Claim their rate is only available if you commit immediately

- Discourage you from shopping other lenders

- Make guarantees that sound unrealistic

- Rush you through disclosures without explanation

Legitimate urgency exists when rate markets move dramatically or lock periods expire, but good lenders explain the context clearly without manipulation.

Lack of Transparency or Documentation

Professional lenders document conversations, provide written rate quotes, and issue required disclosures on time. Warning signs include:

- Refusing to provide written rate quotes

- Delaying Loan Estimate delivery beyond 3 business days

- Verbal promises that don't match written documents

- Unwillingness to explain fees or rate factors

- Missing or incomplete disclosures

Banks.com’s guide to choosing lenders emphasizes the importance of understanding fee structures and getting all promises in writing before proceeding.

Poor Communication or Availability

Once you've submitted your application, communication quality becomes critical. Red flags include:

- Days passing without responses to urgent questions

- Being passed between multiple team members who lack context

- Missed deadlines without proactive communication

- Discovering problems at the last minute

- Inability to reach your loan officer during business hours

These patterns indicate either inadequate staffing or poor internal processes-both creating risk for your transaction timeline.

Maximizing Your Lender Relationship

Choosing good mortgage lenders is only the first step. Your actions throughout the process significantly impact the outcome.

Providing Complete Documentation Promptly

Underwriting moves only as quickly as you provide requested documentation. Good mortgage lenders give you a complete list upfront, but additional requests often arise during underwriting review.

Best practices for documentation:

- Respond to requests within 24 hours when possible

- Provide complete documents (all pages) in readable quality

- Ask clarifying questions if you don't understand what's needed

- Notify your lender immediately of any financial changes

- Keep copies of everything you submit

The step-by-step guide from NerdWallet emphasizes proactive document submission as a key factor in smooth mortgage processes.

Maintaining Financial Stability During the Process

Your financial picture must remain stable from application through closing. Major changes can delay or derail your approval even after initial underwriting approval.

Avoid these actions during your mortgage process:

- Changing jobs or income sources

- Making large purchases or opening new credit accounts

- Moving money between accounts without explanation

- Co-signing loans for others

- Making large deposits without documentation

Good mortgage lenders explain these requirements during your initial conversation and send reminders as closing approaches. If unavoidable changes occur, notify your lender immediately rather than hoping underwriters won't notice.

The Value of Expert Guidance for Seattle Homebuyers

Seattle's dynamic real estate market combines high home prices, competitive inventory, and diverse buyer profiles ranging from first-time purchasers to seasoned investors and tech professionals with complex compensation structures.

Good mortgage lenders serve as strategic advisors throughout your homebuying journey, not just transaction processors. They help you understand how much home you can afford, which loan programs best fit your situation, and how to structure competitive offers that appeal to sellers while protecting your interests.

For first-time buyers in Seattle, this guidance proves particularly valuable. Navigating down payment requirements, understanding PMI, comparing FHA versus conventional options, and learning about Washington State down payment assistance programs requires expertise that goes beyond simple loan origination.

Tech professionals leveraging stock compensation benefit from lenders who understand both the technical aspects of RSU qualification and the strategic timing of purchases relative to vesting schedules. This specialized knowledge can mean the difference between qualifying for your target home or settling for a lower price range.

Finding good mortgage lenders in Seattle requires evaluating transparency, communication, local expertise, and proven execution alongside competitive pricing. The right lender becomes a trusted advisor who guides you through complex decisions and delivers reliable results in competitive markets. Keith Akada brings over 25 years of experience helping Seattle-area homebuyers and homeowners navigate purchases and refinances with clarity and confidence. With 750+ five-star reviews and specialized expertise in tech compensation, he serves clients throughout Seattle, Shoreline, Lynnwood, and surrounding communities. Connect with Mortgage Reel to discuss your home financing goals and experience the difference that expert guidance makes.