Purchasing your first home in Seattle or the surrounding areas represents a significant financial milestone, and choosing the right lender makes all the difference. First time home buyer lenders specialize in guiding new buyers through loan qualification, program selection, and closing timelines while addressing the unique challenges of competitive markets like Seattle, Bellevue, Shoreline, and Lynnwood. Understanding which lenders offer the best programs, rates, and support can save you thousands of dollars and eliminate unnecessary stress during your homebuying journey.

What Makes First Time Home Buyer Lenders Different

First time home buyer lenders distinguish themselves by offering specialized loan programs, educational resources, and flexible qualification criteria designed for buyers without previous homeownership experience. Unlike standard mortgage lenders, these specialists understand the challenges new buyers face-limited down payment savings, uncertainty about credit requirements, and confusion about documentation.

These lenders typically offer access to programs that accept down payments as low as 3% on conventional loans or 3.5% on FHA loans. They also provide detailed guidance on debt-to-income ratios, credit score improvement strategies, and how to structure employment income for maximum qualification potential.

Specialized Support and Education

Working with lenders who focus on first-time buyers means receiving comprehensive education about the mortgage process. This includes one-on-one consultations explaining different loan types, pre-approval timelines, and what to expect during underwriting.

Many first time home buyer lenders also connect clients with down payment assistance programs, which can be particularly valuable in higher-cost markets like Seattle and Redmond. According to NerdWallet’s guide on programs for first-time homebuyers, understanding these options early in the process helps buyers maximize their purchasing power and avoid common pitfalls.

Key Loan Programs for First-Time Buyers in Seattle

Several loan programs cater specifically to buyers making their initial real estate purchase, each with distinct advantages depending on your financial situation and property goals.

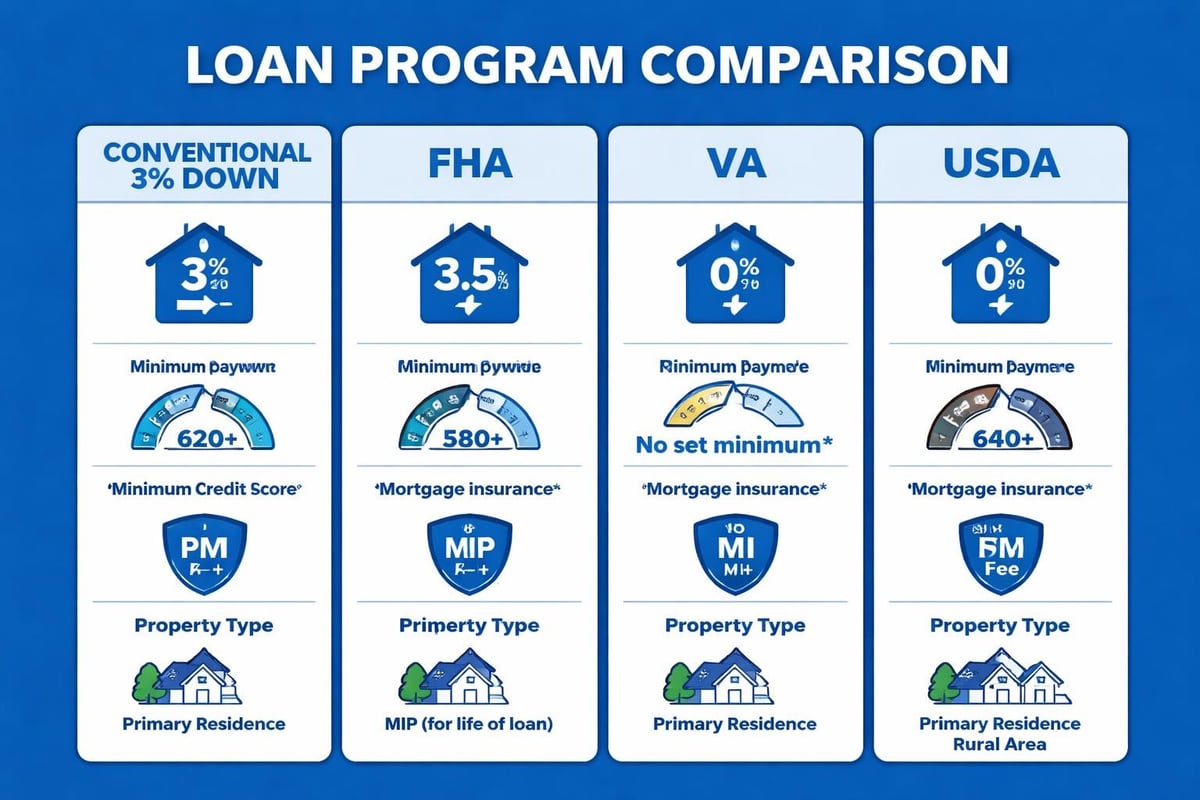

Conventional 97 and HomeReady Loans

Conventional loans with just 3% down payment represent one of the most popular choices for first-time buyers with solid credit scores. The HomeReady program, backed by Fannie Mae, allows for even greater flexibility by permitting income from non-borrowing household members to qualify.

Key benefits include:

- Down payments as low as 3%

- Competitive interest rates for borrowers with 620+ credit scores

- No upfront mortgage insurance premium

- Mortgage insurance cancellation once you reach 20% equity

These programs work exceptionally well for tech professionals in Seattle, Bellevue, and Redmond who have strong incomes from employers like Amazon and Microsoft but may not have accumulated large down payment savings yet.

FHA Loans for Flexible Qualification

Federal Housing Administration (FHA) loans provide accessible financing for buyers with credit scores as low as 580 and down payments of just 3.5%. This program particularly benefits buyers in Mill Creek and Everett who may have excellent income stability but limited credit history.

| Feature | Conventional 3% Down | FHA 3.5% Down |

|---|---|---|

| Minimum Credit Score | 620 | 580 |

| Down Payment | 3% | 3.5% |

| Upfront Insurance | None | 1.75% of loan amount |

| Monthly Insurance | Cancellable at 20% equity | Permanent (if less than 10% down) |

| Debt-to-Income Ratio | Up to 50% | Up to 56.99% |

VA Loans for Military Service Members

Veterans and active-duty service members gain access to VA loans offering zero down payment, no private mortgage insurance, and competitive interest rates. These benefits make homeownership immediately accessible without years of savings accumulation.

USDA Loans in Suburban Markets

For properties in qualifying suburban and rural areas outside Seattle's core, USDA loans provide 100% financing with no down payment required. Certain areas near Lynnwood and Lake Forest Park may qualify, making this an excellent option for buyers seeking more space and lower property prices.

How to Choose the Right First Time Home Buyer Lender

Selecting a lender involves evaluating multiple factors beyond advertised interest rates. The right partnership ensures smooth processing, timely closings, and expert guidance throughout your transaction.

Experience with Local Markets

First time home buyer lenders with deep Seattle-area expertise understand local appraisal challenges, property tax structures, and competitive offer dynamics. This knowledge proves invaluable when crafting financing contingencies and meeting seller timelines in neighborhoods throughout Shoreline and Bellevue.

Lenders familiar with Washington State's specific requirements can also guide you through homebuyer education requirements and local down payment assistance programs that many national lenders overlook.

Technology and Communication Standards

Modern first-time buyers expect digital convenience alongside personal service. Top lenders provide online application portals, mobile document upload, and real-time loan status updates while maintaining accessibility through phone and email.

Evaluate lenders based on:

- Average response time to inquiries

- Availability of dedicated loan officer vs. call center

- Online application and document submission capabilities

- Client review ratings across multiple platforms

- Clear explanation of fees and costs upfront

Closing Speed and Reliability

In competitive markets like Seattle and Redmond, closing speed often determines whether your offer gets accepted. First time home buyer lenders who can close in 14-21 days (or faster with advanced underwriting) provide significant advantages when competing against cash offers or well-qualified buyers.

Understanding Income Qualification for Tech Professionals

Seattle's concentration of technology employers creates unique opportunities for first-time buyers with stock-based compensation. However, not all first time home buyer lenders understand how to properly qualify restricted stock units (RSUs), stock options, and performance bonuses.

Qualifying RSUs and Stock Compensation

Lenders experienced with tech industry compensation can include vested RSUs as qualifying income, significantly increasing your purchasing power. This typically requires two years of documented stock awards and a calculation methodology that accounts for vesting schedules.

For buyers working at Amazon, Microsoft, or Google in Seattle and Bellevue, this expertise can mean the difference between qualifying for a $600,000 home versus a $800,000 home-critical in a market where median home prices frequently exceed $700,000.

Bonus and Variable Income Strategies

Commission-based income, annual bonuses, and profit-sharing distributions require careful documentation and averaging methodologies. Experienced lenders calculate two-year averages while accounting for upward trends that may allow higher qualification amounts.

Down Payment Assistance and Grant Programs

Numerous down payment assistance programs exist specifically for first-time buyers, though many remain underutilized due to lack of awareness. Working with knowledgeable first time home buyer lenders ensures you explore all available options.

Washington State Housing Finance Commission Programs

The Washington State Housing Finance Commission offers down payment assistance through Home Advantage and House Key programs. These provide grants and low-interest second mortgages to qualified buyers throughout Seattle, Lynnwood, and Lake Forest Park.

Eligibility typically depends on income limits relative to area median income and purchase price caps. CNBC Select’s guide to the best mortgage lenders highlights how working with lenders familiar with these state-specific programs streamlines the application process.

Employer-Sponsored Assistance

Major Seattle employers increasingly offer homebuyer assistance programs as recruitment and retention benefits. Amazon, Microsoft, and other technology companies may provide down payment grants, favorable loan terms, or homebuying counseling as part of comprehensive benefits packages.

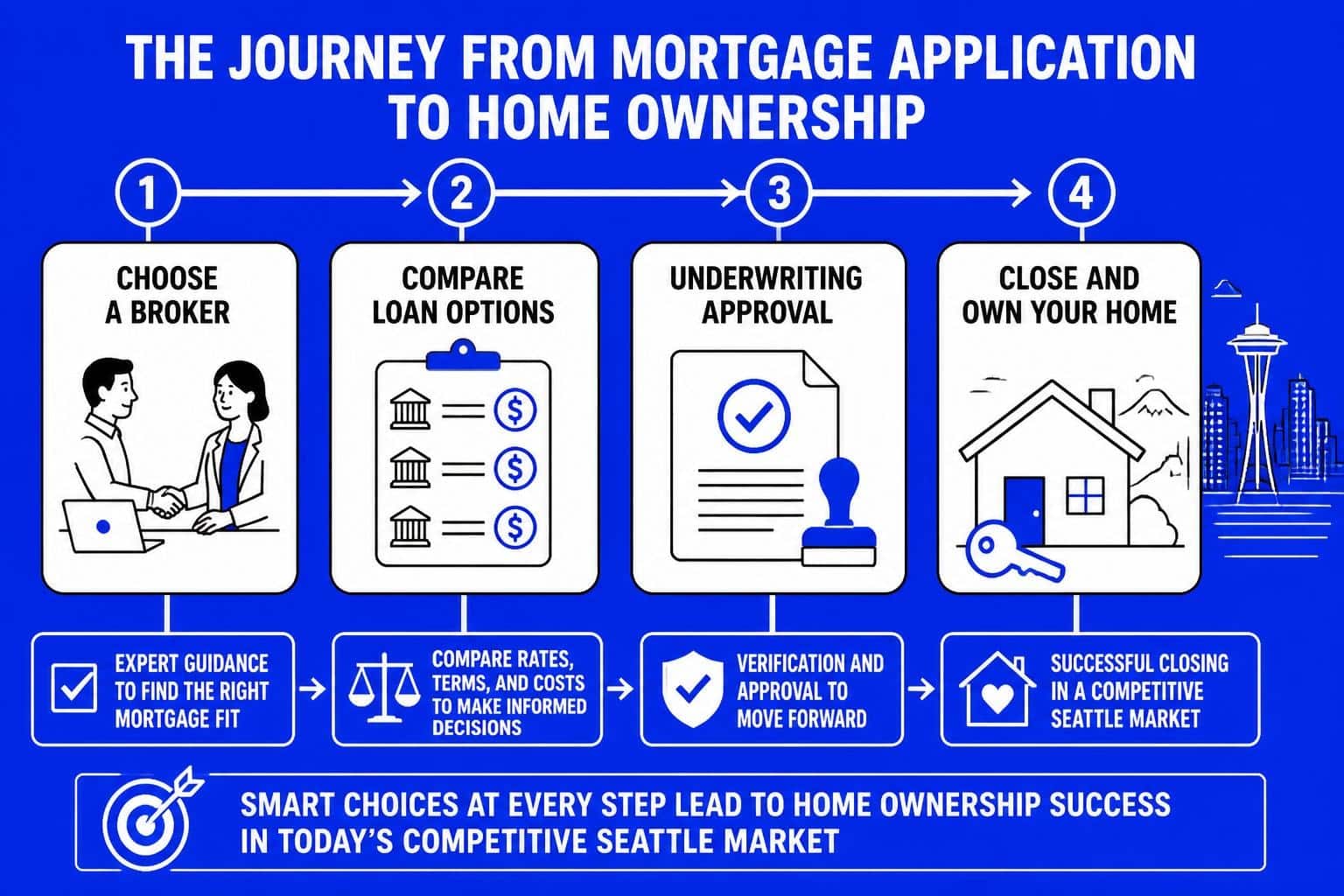

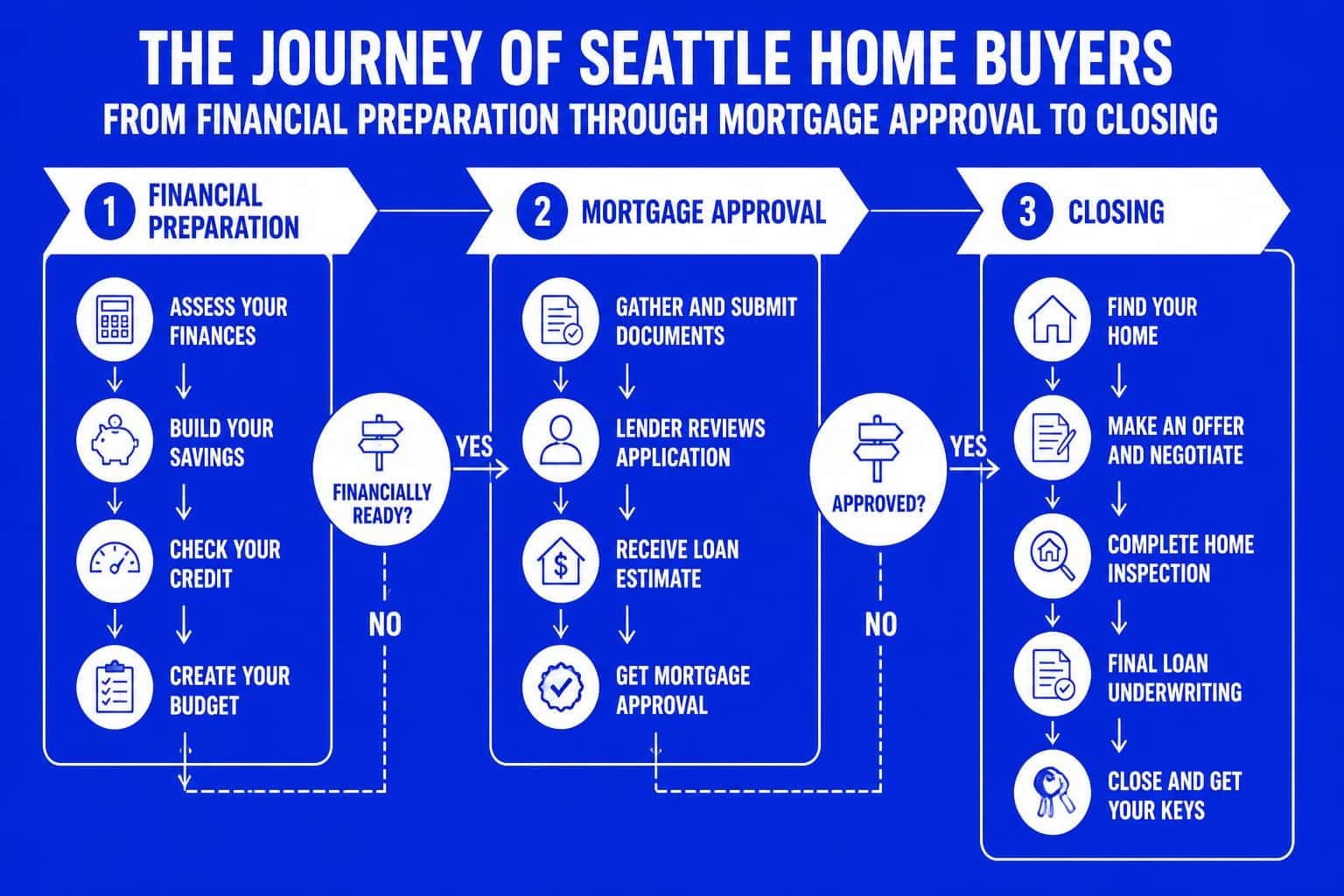

Pre-Approval Process and Timeline Expectations

Understanding the pre-approval process helps first-time buyers prepare appropriately and avoid delays when they find their ideal property.

Documentation Requirements

First time home buyer lenders require comprehensive financial documentation to verify income, assets, and creditworthiness. Gathering these materials before beginning your home search accelerates pre-approval.

Standard documentation includes:

- Two years of W-2 statements

- Two years of federal tax returns (if self-employed)

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Documentation of any gift funds for down payment

- Explanations for any credit issues or gaps in employment

Credit Review and Score Optimization

Lenders evaluate credit reports from all three bureaus, using the middle score for qualification purposes. First-time buyers with scores between 620-680 may benefit from delaying their purchase by 3-6 months to improve scores and secure better rates.

Simple strategies like paying down credit card balances below 30% utilization and avoiding new credit applications can increase scores by 20-40 points relatively quickly.

Common Mistakes First-Time Buyers Make with Lenders

Avoiding these frequent errors saves time, money, and frustration during your homebuying journey.

Shopping Based Solely on Rate

While interest rates matter, focusing exclusively on the lowest advertised rate often backfires. These rates typically require perfect credit, significant down payments, and may come with high closing costs or poor service quality.

Compare total costs including origination fees, discount points, and lender credits across multiple first time home buyer lenders. A rate that's 0.125% higher but saves $3,000 in closing costs often provides better value.

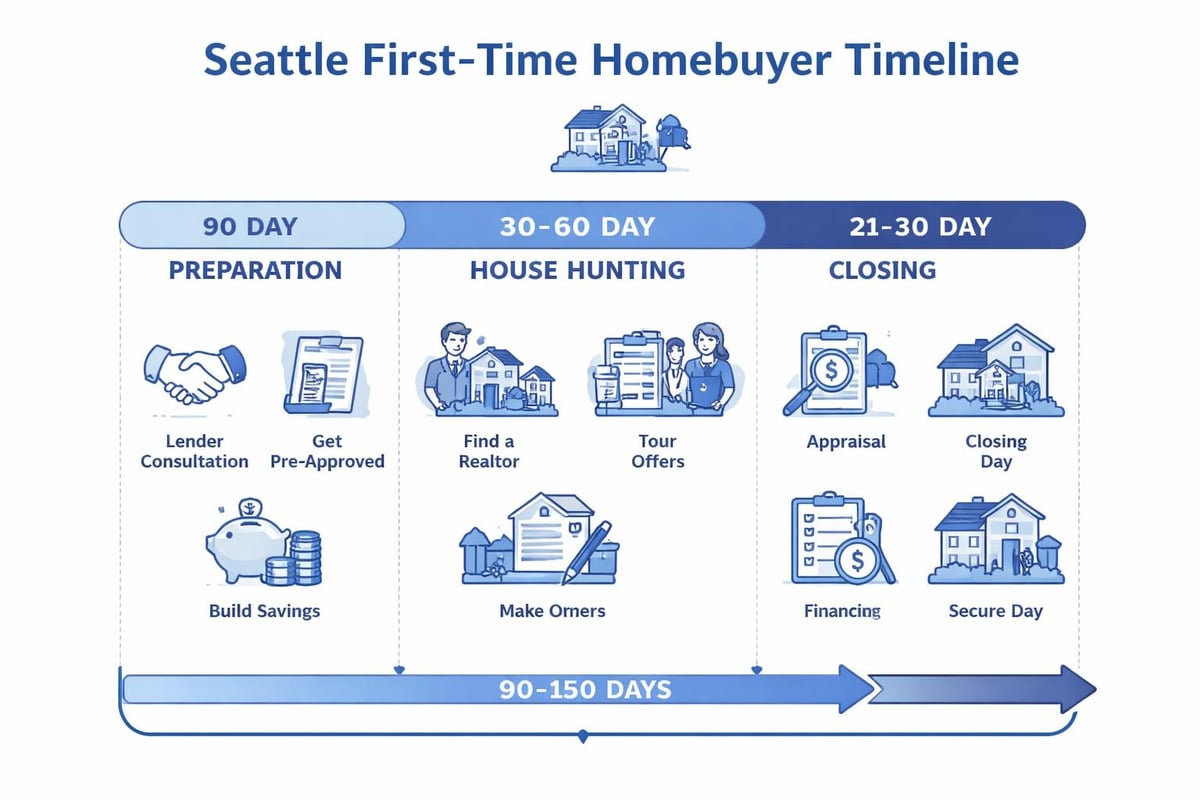

Waiting Too Long for Pre-Approval

Many first-time buyers wait until they've found a property before getting pre-approved. In competitive Seattle neighborhoods, this delay means losing homes to better-prepared buyers with financing already arranged.

Securing pre-approval 60-90 days before beginning your search demonstrates seriousness to sellers and their agents, particularly in markets like Bellevue and Redmond where multiple offers are common.

Changing Financial Status During Underwriting

First time home buyer lenders monitor your financial situation throughout the loan process. Opening new credit accounts, making large purchases, or changing jobs after pre-approval can delay closing or even cause loan denial.

Questions to Ask Potential Lenders

Interviewing multiple lenders helps identify the best fit for your specific situation and goals.

-

What loan programs do you recommend for my financial profile, and why? This reveals whether the lender conducts personalized analysis or pushes a single product to everyone.

-

What are your total closing costs, and can you provide an itemized estimate? Transparency about fees indicates trustworthiness and helps you compare actual costs.

-

How do you handle income qualification for stock compensation? Critical for Seattle tech workers whose RSUs represent significant portions of total compensation.

-

What is your average closing timeline, and can you accommodate accelerated closings if needed? Understanding realistic timelines prevents disappointment in competitive situations.

-

How many first-time buyers did you help last year, and what percentage of your business do they represent? Higher specialization often correlates with better service and expertise.

Interest Rate Locks and Market Timing

First time home buyer lenders offer rate lock options that protect you from increases during your closing period. Understanding these mechanisms helps you make strategic decisions.

Standard Lock Periods

Most lenders provide 30, 45, or 60-day rate locks at no additional cost. Extended locks of 90 days or longer typically incur fees ranging from 0.125% to 0.375% of the loan amount.

For buyers in Lake Forest Park or Mill Creek who anticipate longer closing timelines due to property conditions or seller requirements, these extended locks provide valuable protection.

Float-Down Options

Some first time home buyer lenders offer float-down provisions allowing you to capture lower rates if market conditions improve before closing. These options usually require rates to drop by at least 0.25% and may involve additional fees.

Working with Real Estate Agents and Lenders Together

Successful first-time purchases involve coordination between your real estate agent and lender, creating a unified team advocating for your interests.

Pre-Approval Letter Strength

Lenders who provide detailed, verified pre-approval letters carry more weight with listing agents and sellers than generic qualification letters. In competitive Seattle markets, this credibility can be the deciding factor when sellers choose between similar offers.

Top first time home buyer lenders communicate directly with listing agents to confirm financing strength and realistic closing timelines, removing uncertainty that might otherwise favor competing buyers.

Appraisal Contingency Navigation

When properties appraise below purchase price-common in rapidly appreciating areas like Shoreline and Everett-experienced lenders can suggest solutions like challenging the appraisal, restructuring loan terms, or helping you understand when to walk away.

The Role of Mortgage Insurance in First-Time Buyer Loans

Understanding mortgage insurance costs and structures helps you evaluate total monthly payments and long-term affordability.

Private Mortgage Insurance (PMI) on Conventional Loans

Conventional loans with less than 20% down require PMI, typically costing 0.3% to 1.5% of the original loan amount annually. This insurance protects the lender if you default but provides no benefit to you as the borrower.

The advantage is that PMI automatically cancels once you reach 22% equity through payments and appreciation, or you can request cancellation at 20% equity. In Seattle's appreciating market, this often occurs within 3-5 years.

FHA Mortgage Insurance Premium (MIP)

FHA loans require both upfront MIP (1.75% of loan amount) and annual MIP (0.45% to 1.05% depending on loan size and term). For loans with less than 10% down, this insurance remains for the life of the loan unless you refinance to conventional.

Refinancing Considerations for Future Planning

First time home buyer lenders should also discuss your long-term financial strategy, including potential refinancing opportunities as your situation evolves.

When Refinancing Makes Sense

As your income increases and you build equity, refinancing from FHA to conventional eliminates mortgage insurance. Similarly, if rates drop significantly or your credit score improves by 40+ points, refinancing can reduce monthly payments substantially.

Many Seattle buyers who purchased homes with 3% down in markets like Lynnwood find that appreciation creates refinancing opportunities within 2-3 years, allowing them to eliminate PMI and reduce rates simultaneously.

Digital Tools and Resources from Modern Lenders

Technology-forward first time home buyer lenders provide tools that simplify the complex mortgage process and keep you informed throughout your transaction.

Online Application Portals

Modern platforms allow document upload via smartphone, electronic signature on disclosures, and real-time status updates. These conveniences prove especially valuable for busy tech professionals in Seattle and Bellevue who may struggle to visit physical offices during business hours.

Mortgage Calculators and Affordability Tools

Sophisticated calculators help you model different scenarios including varying down payment amounts, interest rates, and property tax estimates specific to Washington State. These tools empower informed decision-making before you commit to specific properties or loan structures.

Alternative Documentation Programs for Self-Employed Buyers

First-time buyers who are self-employed, freelancers, or gig economy workers face additional documentation challenges that specialized first time home buyer lenders can navigate.

Bank Statement Programs

Rather than tax returns, these programs analyze 12-24 months of business bank statements to determine qualifying income. This approach often reveals higher income than tax returns show for self-employed buyers who maximize business deductions.

Profit and Loss Statement Options

Some lenders accept year-to-date profit and loss statements prepared by CPAs alongside tax returns, capturing more recent income growth that may not yet appear on filed returns.

Navigating the complexities of first-time homebuying requires expert guidance from lenders who understand both your financial situation and the unique dynamics of the Greater Seattle market. Whether you're exploring conventional programs, need help qualifying stock compensation, or want to close quickly in a competitive situation, working with a specialized mortgage professional makes all the difference. Mortgage Reel serves first-time buyers throughout Seattle, Shoreline, Lynnwood, and surrounding communities with transparent guidance, advanced financing options, and the local expertise needed to turn your homeownership goals into reality.