Choosing the right home loan company represents one of the most important financial decisions Seattle homebuyers will make in 2026. Whether you're a first-time buyer navigating Lake Forest Park neighborhoods or a tech professional at Amazon or Microsoft looking to leverage RSU income for a jumbo loan in Bellevue, understanding how different lenders operate can save you thousands of dollars and weeks of stress. A home loan company encompasses various types of mortgage providers, from national banks and credit unions to mortgage brokers and direct lenders, each offering distinct advantages depending on your financial profile, timeline, and property goals. In the competitive Seattle market, where bidding wars remain common and closing speed matters, selecting a lender who understands local conditions and regulatory requirements becomes critical to success.

Understanding Different Types of Home Loan Companies

Not all mortgage lenders operate the same way, and the distinctions between them directly impact your experience, available loan products, and overall costs.

Banks and Credit Unions

Traditional financial institutions offer mortgage products as part of a broader suite of banking services. Large national banks often provide competitive rates for borrowers with excellent credit and straightforward income profiles. Credit unions, which serve members rather than shareholders, may offer relationship-based pricing and lower fees. However, both types of institutions typically maintain stricter underwriting standards and offer limited flexibility for complex income situations.

Key characteristics include:

- Portfolio products that may offer unique features

- Relationship discounts for existing customers

- Standardized underwriting with less customization

- Limited loan officer availability during evenings and weekends

- Slower response times in competitive markets

For tech professionals with stock compensation or bonus income, traditional banks may struggle to qualify these income sources efficiently, potentially reducing your buying power in markets like Redmond or Kirkland.

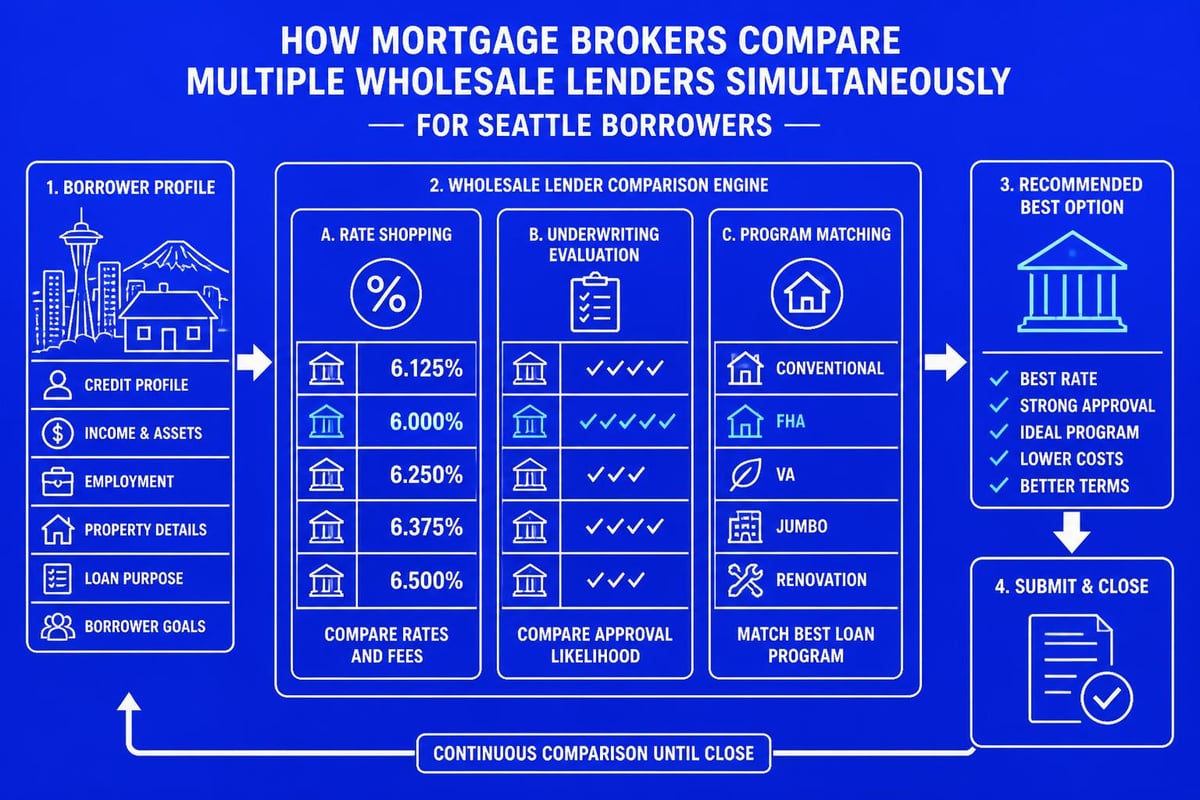

Mortgage Brokers as Home Loan Companies

Mortgage brokers operate differently from direct lenders. Rather than funding loans from their own capital, brokers access multiple wholesale lenders, comparing products, rates, and underwriting standards to match borrowers with optimal solutions. This model creates competition among lenders for your business, often resulting in better pricing and terms.

A good mortgage broker in Seattle brings market expertise, relationship equity with underwriters, and the ability to navigate complex scenarios. When qualifying RSU income or structuring a 10% down jumbo loan for a $1.5 million home in Mill Creek, broker expertise becomes invaluable.

Advantages of working with mortgage brokers:

- Access to 20-50+ lenders through one application

- Competitive rate shopping without multiple credit pulls

- Specialized knowledge of niche programs

- Dedicated support throughout the transaction

- Flexibility for self-employed, commissioned, or equity-compensated borrowers

Direct Mortgage Lenders

Direct lenders fund loans using their own capital or warehouse lines of credit. Online-only lenders have grown significantly since 2020, offering streamlined digital experiences and competitive rates. However, direct lenders vary widely in service quality, local market knowledge, and ability to close complex transactions quickly.

According to data from Polygon Research’s 2025 HMDA analysis, the top mortgage lenders in 2026 continue to evolve their technology platforms while maintaining personalized service for high-value clients.

How to Evaluate a Home Loan Company

Selecting a lender requires more than comparing interest rates. The lowest rate means nothing if the lender cannot close on time or misqualifies your income during underwriting.

Licensing and Compliance Standards

Every legitimate home loan company must maintain proper state and federal licensing. In Washington State, lenders must comply with the Department of Financial Institutions regulations and adhere to consumer financial protection laws that govern mortgage lending practices.

Verify your lender's credentials through the Nationwide Multistate Licensing System (NMLS) database. Each loan officer should have an active NMLS number and clean disciplinary history.

Review History and Reputation

Online reviews provide valuable insight into lender performance, but context matters. Look for patterns across multiple platforms rather than focusing on isolated complaints.

| Review Platform | What to Assess | Red Flags |

|---|---|---|

| Google Reviews | Overall satisfaction, communication quality | Repeated closing delays, rate lock issues |

| Zillow | Transaction complexity handled | Inability to close complex deals |

| Yelp | Customer service responsiveness | Poor communication, missed deadlines |

Lenders with 500+ reviews and consistent 4.5+ star ratings demonstrate proven track records. In Seattle's competitive market, understanding why local expertise matters can differentiate between winning and losing in multiple-offer situations.

Rate Competitiveness and Fee Transparency

Interest rates fluctuate daily, but fee structures remain relatively stable. Request a detailed Loan Estimate within three business days of application to compare:

- Origination charges

- Discount points (if applicable)

- Third-party fees (appraisal, title, escrow)

- Lender credits or rate buydown options

A home loan company offering a rate 0.125% lower but charging $3,000 in unnecessary fees may cost more over the loan's life than a slightly higher rate with minimal costs.

Closing Timeline and Execution Capability

Seattle's real estate market demands speed. The median home in Bellevue or Redmond receives multiple offers, often with escalation clauses and appraisal gap coverage. Sellers and listing agents favor buyers with lenders who can close in 14-21 days with confidence.

Ask potential lenders:

- What is your average closing timeline for purchase transactions?

- How quickly can you provide pre-approval letters?

- What percentage of your loans close on the original estimated date?

- Do you underwrite loans in-house or outsource to third parties?

Advanced lenders can close conventional and jumbo loans in as few as 9-12 business days when borrowers provide documentation promptly and properties appraise at value.

Mortgage Products Available Through Home Loan Companies

The right lender offers program diversity to match your specific situation, property type, and down payment capacity.

Conventional Conforming Loans

Conventional home loans remain the most common mortgage product for Seattle buyers with strong credit and stable income. These loans conform to Fannie Mae and Freddie Mac guidelines, offering:

- Down payments as low as 3% for first-time buyers

- Competitive rates for borrowers with 740+ credit scores

- Private mortgage insurance (PMI) that can be removed at 20% equity

- Loan amounts up to $806,500 in King County (2026 conforming limit)

Jumbo Loan Programs

Seattle's housing market regularly requires jumbo financing, particularly in neighborhoods like Madison Park, Laurelhurst, and Queen Anne where median prices exceed conforming limits. Jumbo loans require stronger credit profiles but offer flexibility for high-earning professionals.

Jumbo loan considerations:

- Loan amounts exceeding $806,500

- Typically require 10-20% down payment

- Slightly higher rates than conforming loans

- More stringent income documentation

- Debt-to-income ratios up to 43% (sometimes 50% with compensating factors)

Tech professionals frequently leverage RSU income for mortgage qualification on jumbo purchases, requiring lenders familiar with equity compensation documentation.

Government-Backed Loan Programs

FHA, VA, and USDA loans each serve specific borrower segments with unique advantages.

| Loan Type | Minimum Down Payment | Credit Score Minimum | Key Benefit |

|---|---|---|---|

| FHA | 3.5% | 580 (580+ for 3.5% down) | Flexible credit standards |

| VA | 0% | No minimum | No PMI, competitive rates |

| USDA | 0% | 640 typically | Rural/suburban property eligibility |

FHA home loans work well for first-time buyers in Shoreline or Lynnwood who have limited down payment funds but stable employment. VA loans provide exceptional value for veterans and active military personnel, eliminating down payment requirements and monthly mortgage insurance.

Portfolio and Non-QM Products

Some home loan companies maintain portfolio lending divisions for borrowers who fall outside conventional guidelines. Self-employed professionals, real estate investors, and borrowers with recent credit events may qualify through alternative documentation programs.

Non-QM (Non-Qualified Mortgage) loans use bank statements, asset depletion, or debt service coverage ratios rather than traditional income verification, expanding homeownership opportunities for non-traditional earners.

The Mortgage Application Process With a Home Loan Company

Understanding the timeline and requirements streamlines your experience and prevents delays.

Pre-Approval vs. Pre-Qualification

Pre-qualification provides a rough estimate based on self-reported information without verification. It carries minimal weight with sellers.

Pre-approval involves a comprehensive review of credit, income, assets, and employment with conditional approval from underwriting. In competitive Seattle markets, pre-approval letters from reputable lenders significantly strengthen offers.

Request pre-approval before touring homes seriously. The process typically requires:

- Completed loan application (1003 form)

- Two years of W-2s and tax returns

- Recent pay stubs (30 days)

- Two months of bank/investment statements

- Authorization for credit report

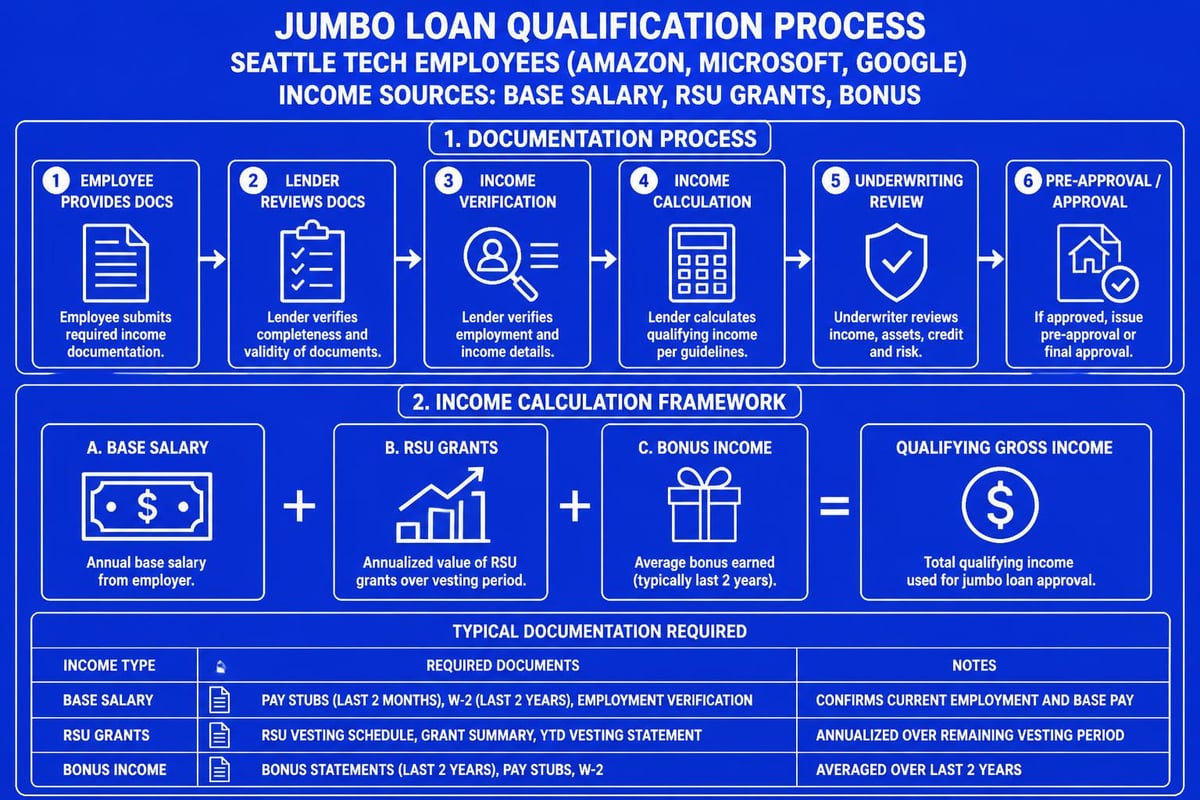

Documentation Requirements for Tech Professionals

Amazon, Microsoft, and Google employees often receive total compensation packages that include base salary, RSUs, bonuses, and sometimes stock options. Properly documenting and qualifying this income maximizes buying power but requires lender expertise.

RSU qualification typically requires:

- Two-year history of RSU vesting (shown on W-2s)

- Current vesting schedule from employer

- Evidence of continued employment

- Average of two years of vesting, discounted for volatility

Some home loan companies discount RSU income by 25-30% for qualification purposes, while others with advanced underwriting platforms use more favorable calculations, potentially adding $100,000+ to your qualified loan amount.

Underwriting and Closing Timeline

After submitting your application and documentation, the loan enters underwriting review where a licensed underwriter evaluates risk and compliance with lending guidelines.

Typical timeline breakdown:

- Days 1-3: Initial application submission and documentation review

- Days 4-7: Order appraisal, title search, and verification of employment

- Days 8-14: Underwriting review and conditional approval

- Days 15-21: Clear conditions, final approval, and closing disclosure sent

- Days 22-30: Funding and recording

Lenders with in-house processing, underwriting, and closing departments control the timeline more effectively than those outsourcing these functions. For Seattle homebuyers navigating down payment strategies, understanding gift fund documentation requirements and reserve expectations prevents last-minute scrambling.

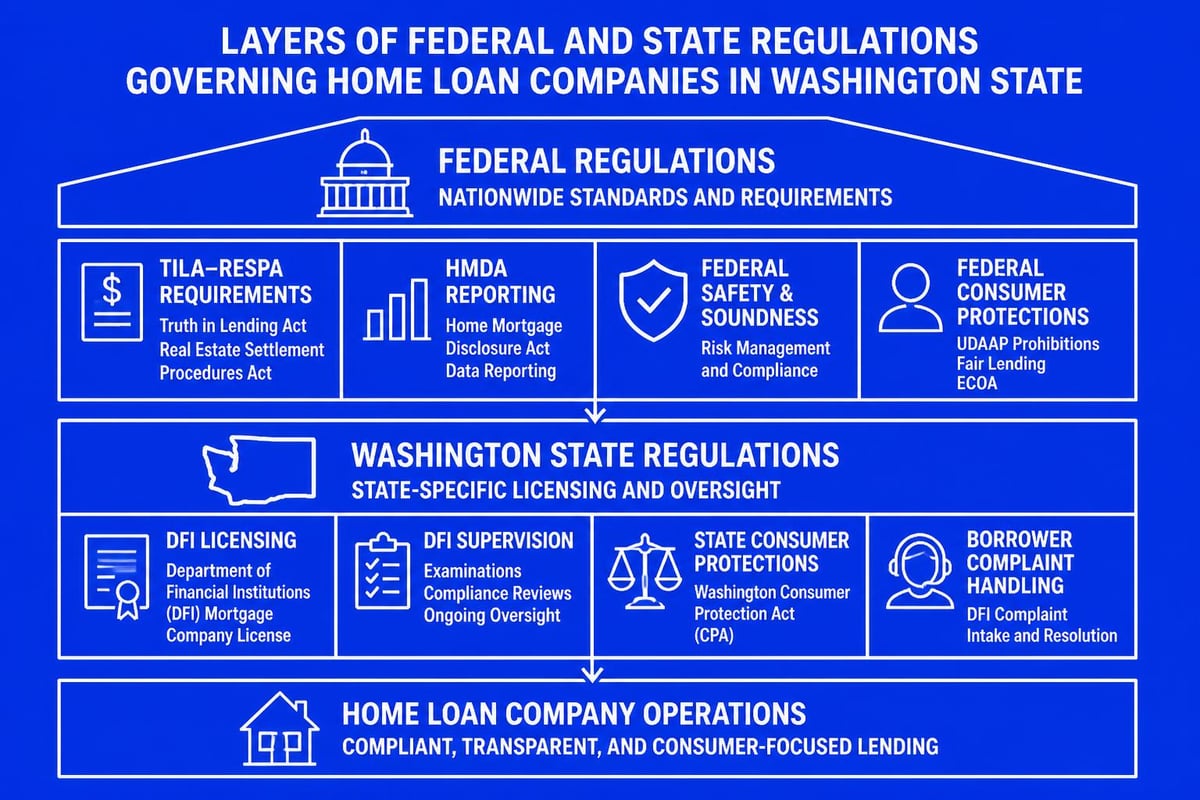

Regulatory Oversight of Home Loan Companies

Federal and state regulations protect consumers while ensuring lender accountability and fair lending practices.

Federal Lending Standards

The FDIC provides comprehensive mortgage lending guidelines that govern product offerings, disclosure requirements, and fair lending practices. The Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA) mandate specific disclosures at application and closing.

Home Mortgage Disclosure Act (HMDA) requires lenders to report detailed loan data annually, creating transparency around lending patterns. The Federal Reserve’s Regulation C implementation guide outlines reporting requirements that help identify discriminatory lending practices.

Washington State Regulations

Washington's Department of Financial Institutions regulates mortgage lenders, brokers, and loan originators through licensing requirements and regular examinations. State law requires:

- Surety bonds for mortgage brokers

- Continuing education for loan officers

- Disclosure of compensation structures

- Compliance with state-specific consumer protections

These regulations ensure that every home loan company operating in Seattle, Everett, or Lynnwood meets minimum competency and financial stability standards.

Market Trends Shaping Home Loan Companies in 2026

The mortgage industry continues evolving rapidly, with technology, regulation, and economic factors driving change.

Digital Transformation and Hybrid Models

Pure online lenders gained market share during the pandemic but many borrowers still value personalized guidance for complex transactions. The most successful home loan companies in 2026 blend digital efficiency with human expertise, offering:

- Digital document upload portals and e-signatures

- Real-time loan status tracking

- Automated income and asset verification (when possible)

- Direct access to experienced loan officers for questions

- Mobile apps for managing the application

According to Mordor Intelligence’s home loan market analysis, the global mortgage industry continues consolidating while simultaneously fragmenting into specialized niches serving specific borrower segments.

Interest Rate Environment and Refinance Activity

Interest rates in 2026 remain influenced by Federal Reserve policy, inflation trends, and bond market dynamics. When rates drop 0.75-1.00% below current levels, refinance activity surges, creating capacity constraints at many lenders.

Working with a home loan company that maintains consistent service quality during both purchase and refinance markets ensures reliability regardless of economic cycles.

Specialized Lending for Tech Compensation

Seattle's concentration of high-paying tech employers creates demand for lenders who understand equity compensation structures. As companies shift compensation mixes toward RSUs and away from cash bonuses, mortgage qualification strategies must adapt.

Forward-thinking lenders develop underwriting expertise for:

- Amazon RSU vesting schedules and L4-L7 compensation bands

- Microsoft stock awards and performance bonuses

- Google equity packages and refresh grants

- Startup equity with liquidity constraints

This specialization directly impacts qualified loan amounts for jumbo home loans with 10% down in high-cost Seattle neighborhoods.

Common Mistakes When Choosing a Home Loan Company

Avoiding these errors saves money, stress, and potential deal failures.

Focusing Exclusively on Interest Rates

A 0.125% rate difference on a $600,000 loan equals approximately $42 per month or $15,000 over 30 years. While significant, it matters little if the lender:

- Fails to close on time, costing you the home

- Misqualifies your income, forcing last-minute loan changes

- Provides poor communication, creating unnecessary stress

- Charges excessive fees that eliminate rate savings

Evaluate the total cost of borrowing, service quality, and execution capability alongside rate competitiveness.

Neglecting to Compare Loan Estimates

Federal law requires lenders to provide a standardized Loan Estimate within three business days of application. This three-page document details all costs and allows direct comparison between lenders.

Pay attention to:

- Section A: Origination charges (what the lender earns)

- Section B: Services you cannot shop for (controlled by lender)

- Section C: Services you can shop for (title, escrow, insurance)

- Page 3: Cash to close breakdown

Ignoring Local Market Expertise

A home loan company based in another state may offer competitive rates but lack understanding of Seattle's competitive dynamics, appraisal challenges, or local closing attorney preferences. Understanding the difference between mortgage brokers and banks in the context of local market knowledge becomes essential.

Lake Forest Park, for example, has specific appraisal considerations due to lot sizes and waterfront properties. Everett's diverse housing stock requires different underwriting approaches than downtown Seattle condos. Local expertise matters.

Making Major Financial Changes During the Process

Between pre-approval and closing, avoid:

- Changing jobs or income structure

- Opening new credit accounts

- Making large purchases on credit

- Transferring money between accounts without documentation

- Co-signing loans for others

Lenders re-verify employment and pull credit immediately before closing. Unexplained changes can delay or derail your loan even days before scheduled closing.

Questions to Ask Every Home Loan Company

Before committing to a lender, request clear answers to these essential questions.

About Experience and Expertise

- How many loans do you personally close per year?

- What percentage of your business comes from repeat clients and referrals?

- Do you specialize in any particular loan types or borrower profiles?

- How do you stay current with guideline changes and market conditions?

- Can you provide references from recent clients with similar scenarios?

About Process and Communication

- Who will I communicate with during the process (loan officer, processor, assistant)?

- What are your typical response times for emails and calls?

- How do you handle issues that arise during underwriting?

- What technology platforms do you use for document collection and status updates?

- Do you provide after-hours or weekend availability for time-sensitive situations?

About Pricing and Programs

- What is your current rate for [my specific loan scenario]?

- Are you quoting par pricing, or does this include lender credits or discount points?

- What are all of your lender fees (origination, processing, underwriting, admin)?

- Do you offer rate locks, and what is your policy on float-down options?

- What loan programs do you have access to beyond conventional, FHA, and VA?

For first-time buyers in Washington, asking about down payment assistance programs and closing cost credit options reveals lender knowledge and commitment to finding optimal solutions.

The Role of Technology in Modern Home Loan Companies

Technology reshapes mortgage lending but cannot replace human expertise for complex transactions.

Automated Underwriting Systems

Fannie Mae's Desktop Underwriter and Freddie Mac's Loan Product Advisor analyze borrower data against thousands of data points, providing instant credit decisions for straightforward scenarios. These systems accelerate approvals but require skilled interpretation for non-standard situations.

When qualifying stock compensation or structuring debt-to-income ratios creatively, experienced underwriters add value beyond automated systems.

Digital Verification Services

Rather than manually reviewing bank statements and pay stubs, many home loan companies use automated verification services that connect directly to financial institutions and payroll providers. These services:

- Reduce documentation requirements

- Accelerate verification timelines

- Minimize fraud risk

- Improve borrower experience

However, self-employed borrowers, those with complex income sources, or clients with privacy concerns may prefer traditional documentation methods.

Customer Relationship Management

Leading lenders use sophisticated CRM platforms to track communication, manage deadlines, and ensure nothing falls through the cracks. These systems generate automatic reminders for rate lock expirations, appraisal deadlines, and condition clearance dates.

For borrowers, this translates to proactive communication and fewer surprises during the transaction.

Building Long-Term Relationships With Your Home Loan Company

Mortgage lending should not be transactional. The right lender becomes a trusted advisor for multiple life stages.

Beyond the Initial Purchase

Homeownership spans decades, creating multiple opportunities to leverage lender relationships:

- Refinancing when rates drop or income increases

- Home equity lines of credit for renovations or investment

- Streamlined processing for move-up purchases

- Portfolio reviews to optimize debt structure

- Investment property financing as wealth grows

A home loan company that prioritizes education and long-term relationship building provides value far beyond the initial transaction. Understanding options like mortgage recasting versus refinancing helps homeowners make informed decisions as circumstances change.

Market Updates and Education

Quality lenders provide ongoing market commentary, rate updates, and strategic advice even when you are not actively borrowing. This education helps you:

- Time refinance decisions optimally

- Understand how economic trends affect home values

- Plan major purchases around mortgage qualification

- Prepare for future real estate investments

The U.S. home loan market continues evolving with new products, changing regulations, and shifting competitive dynamics. Staying informed through a trusted advisor prevents costly mistakes.

Selecting the right home loan company determines more than your interest rate-it shapes your entire homebuying experience, closing timeline, and long-term financial strategy. Whether you're purchasing in Seattle, Bellevue, Shoreline, or Lake Forest Park, working with experienced professionals who understand local markets, complex income qualification, and competitive closing timelines makes the difference between offers accepted and opportunities lost. Keith Akada at Mortgage Reel brings over 25 years of experience helping Seattle-area homebuyers navigate complex scenarios with transparency, strategy, and execution. With 750+ five-star reviews and expertise in qualifying RSU income for tech professionals, Keith provides the guidance and reliability you need to make confident home financing decisions.