First time buying a house represents one of the most significant financial decisions you'll ever make, particularly in competitive markets like Seattle, Bellevue, and Redmond. The process involves more than just finding the right property-it requires understanding mortgage programs, qualifying with various income types, and navigating a fast-paced real estate environment where preparation determines success. For tech professionals working at Amazon, Microsoft, and Google, the challenge often involves maximizing buying power through strategic use of stock compensation and bonus income. This comprehensive guide walks you through every critical step, from financial readiness to closing day, with insights specific to the Greater Seattle area's unique market conditions.

Understanding Your Financial Foundation

The journey of first time buying a house begins with a thorough assessment of your financial situation. Your credit score, savings, debt-to-income ratio, and employment history all play crucial roles in determining what you can afford and which loan programs you qualify for.

Credit Score Requirements

Most conventional loan programs require a minimum credit score of 620, though achieving 740 or higher unlocks the best interest rates. FHA loans offer more flexibility, accepting scores as low as 580 with a 3.5% down payment, or even 500 with 10% down.

Key actions to improve your credit position:

- Review your credit reports from all three bureaus for errors

- Pay down credit card balances below 30% utilization

- Avoid opening new credit accounts during the mortgage process

- Maintain consistent on-time payments for at least 12 months

- Keep older credit accounts open to preserve credit history length

Your debt-to-income (DTI) ratio matters just as much as your credit score. Most lenders prefer a DTI below 43%, though some programs allow up to 50% with compensating factors like substantial reserves or high credit scores.

Building Your Down Payment Strategy

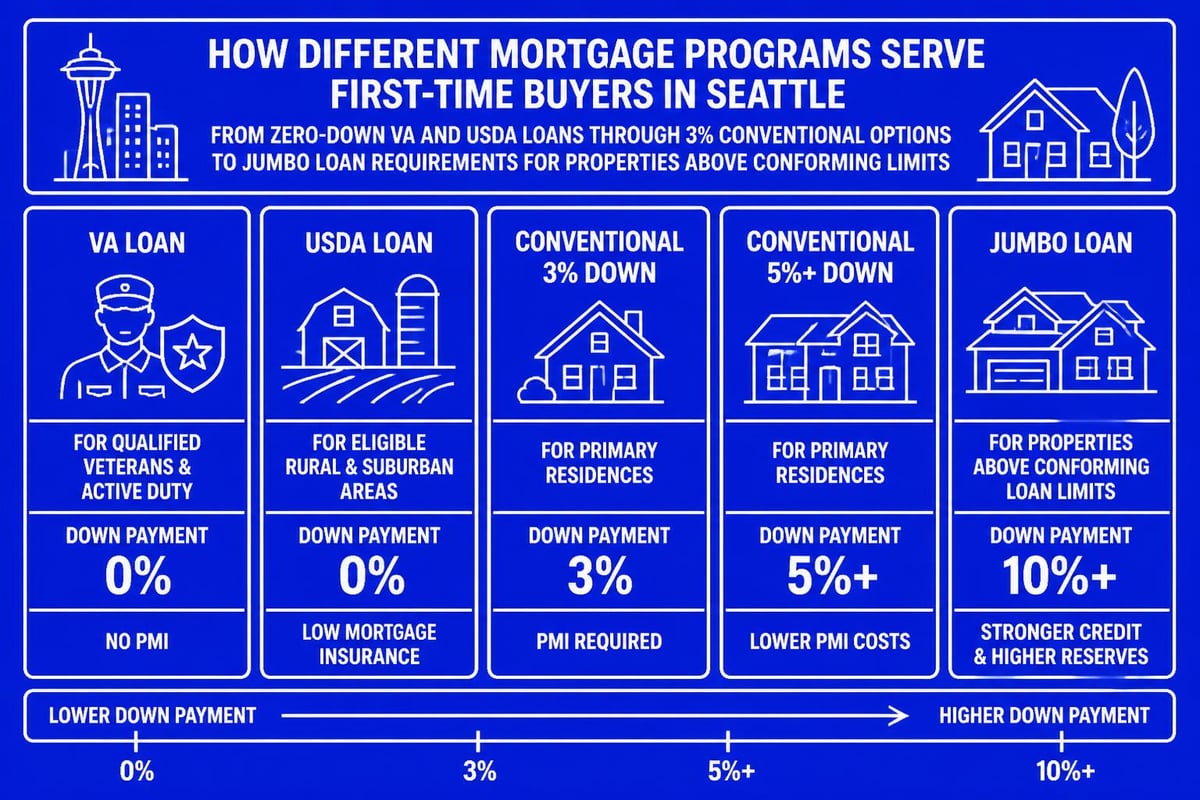

The down payment guide for Seattle homebuyers in 2026 explains how different loan programs offer flexibility based on your financial situation. Contrary to popular belief, 20% down is not always required when first time buying a house.

| Loan Type | Minimum Down Payment | PMI Requirement | Best For |

|---|---|---|---|

| Conventional 97 | 3% | Yes, until 20% equity | Strong credit, stable income |

| FHA | 3.5% | Yes, for loan life | Lower credit scores |

| VA | 0% | No PMI | Eligible veterans and service members |

| USDA | 0% | Yes, annual fee | Rural/suburban eligible areas |

| Jumbo | 10-20% | Varies by lender | High-value properties over $802,650 |

Seattle tech professionals often have unique advantages when building their down payment. Restricted stock units (RSUs), employee stock purchase plans (ESPPs), and annual bonuses can all contribute to your purchasing power when properly documented and structured.

Qualifying Income for Seattle Tech Workers

First time buying a house in the Seattle metro area often involves navigating complex compensation packages. Traditional mortgage guidelines were built around W-2 wage earners, but experienced brokers understand how to qualify non-traditional income sources.

RSU and Stock Compensation Strategies

Amazon, Microsoft, and Google employees frequently receive substantial portions of their compensation through equity. Lenders can use RSU income when calculating your qualifying income, but the approach varies based on vesting schedules and documentation.

Requirements for qualifying RSU income:

- Two-year history of receiving stock compensation

- Continued expectation of future vesting

- Average of past two years, minus a haircut (typically 15-30%)

- Recent pay stubs showing actual vesting events

- Offer letter or compensation statement confirming ongoing grants

Bonus income follows similar guidelines. Lenders typically average your bonus income over two years and apply it to your qualifying income. A consistent or increasing bonus pattern strengthens your application significantly.

Self-Employment and 1099 Income

Freelancers, consultants, and entrepreneurs face different documentation requirements. Most programs require two years of tax returns, though some lenders offer one-year self-employed programs for strong borrowers with substantial reserves.

The challenge with self-employment lies in tax deductions. While writing off business expenses reduces your tax liability, it also reduces your qualifying income for mortgage purposes. Planning 12-24 months ahead of your home purchase allows you to balance tax strategy with mortgage qualification needs.

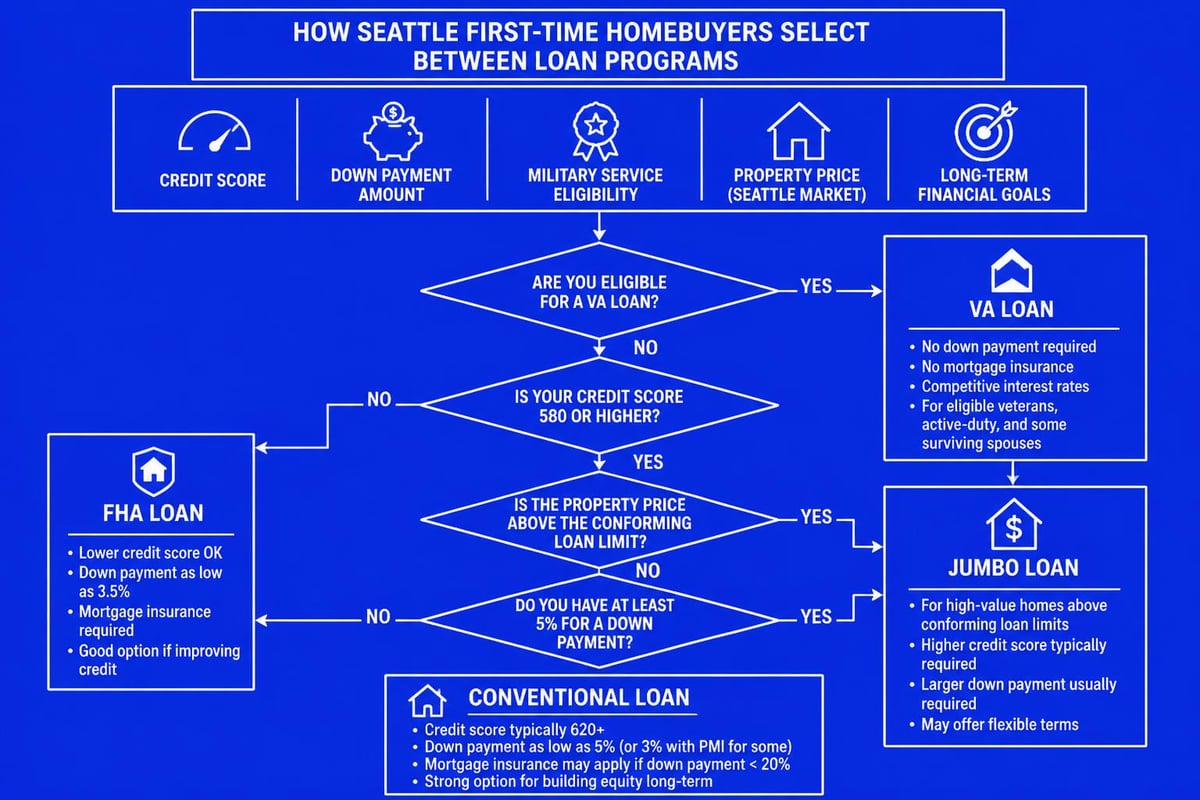

Choosing the Right Mortgage Program

Understanding which mortgage program aligns with your financial profile makes the difference between stretching uncomfortably and buying confidently. Mortgage financing options in Seattle vary based on property type, price point, and borrower qualifications.

Conventional Loans

Conventional loans dominate the Seattle market for buyers with strong credit and stable income. These loans offer competitive rates, flexible property types, and the ability to cancel PMI once you reach 20% equity.

Conventional loan advantages:

- Lowest rates for high credit scores (740+)

- Investment property and second home eligibility

- PMI removal at 20% equity through appreciation or principal paydown

- Higher loan limits ($802,650 in King County for 2026)

- Streamlined refinance options in the future

For properties exceeding conforming loan limits, jumbo home loans provide financing for Seattle's higher-priced neighborhoods like Capitol Hill, Queen Anne, and Bellevue's downtown corridor.

Government-Backed Programs

FHA, VA, and USDA loans each serve specific borrower segments with unique advantages. FHA loans work well for first time buying a house with less-than-perfect credit, while VA loans offer unmatched benefits for military service members and veterans.

The home loans for first-time buyers resource explains how these programs differ and which situations benefit most from each option. VA loans stand out with zero down payment, no PMI, and competitive rates regardless of credit score variations within acceptable ranges.

USDA loans serve buyers in eligible areas outside Seattle's urban core, including parts of Snohomish County and areas east of Lake Washington. These zero-down loans require no down payment but include income limits and property location restrictions.

Navigating Seattle's Competitive Market

First time buying a house in Seattle requires speed and strategy. The median days on market in desirable neighborhoods like Fremont, Ballard, and Wallingford often measures in single digits for well-priced properties.

The Pre-Approval Advantage

Generic pre-qualification letters carry little weight in multiple-offer situations. A comprehensive pre-approval from a trusted Seattle mortgage broker demonstrates serious intent backed by verified income, assets, and credit.

Elements of a strong pre-approval:

- Full credit report review and score verification

- Documented income through pay stubs, W-2s, or tax returns

- Asset verification showing funds for down payment and reserves

- Conditional approval through underwriting when possible

- Lender reputation known to listing agents and sellers

Seattle listing agents recognize brokers with track records for reliable closings. A pre-approval from an experienced local broker often outweighs higher offers from buyers with uncertain financing.

Understanding Appraisal Challenges

Properties in hot neighborhoods sometimes sell above appraised value, creating an appraisal gap. This means you'll need additional cash beyond your planned down payment to cover the difference between the appraised value and purchase price.

| Scenario | Purchase Price | Appraised Value | Down Payment (10%) | Cash Needed |

|---|---|---|---|---|

| At Value | $800,000 | $800,000 | $80,000 | $80,000 |

| Gap Scenario | $800,000 | $775,000 | $80,000 | $105,000 |

The gap scenario requires an additional $25,000 because lenders calculate your loan based on the lower of purchase price or appraised value. Strong buyers maintain extra reserves specifically for this possibility.

Closing Process and Timeline Expectations

The path from offer acceptance to keys in hand typically spans 30-45 days, though experienced lenders can close qualified buyers in as few as 9 business days when all documentation is prepared upfront.

Essential Closing Steps

Understanding the closing timeline helps you coordinate with your employer, current landlord, and moving plans. Most delays stem from incomplete documentation or appraisal scheduling challenges.

Standard closing timeline breakdown:

- Days 1-3: Initial disclosures, lock interest rate, order appraisal

- Days 4-7: Submit full documentation package to underwriting

- Days 8-14: Appraisal completed and reviewed

- Days 15-21: Underwriting review and conditional approval

- Days 22-28: Clear conditions, final walkthrough scheduled

- Days 29-30: Clear to close, final closing disclosure review

- Day 30-35: Closing appointment, funding, recording

Home inspections typically occur within the first 10 days, giving you time to negotiate repairs or credits before significant closing costs become non-refundable. According to The Week’s home inspection tips, attending your inspection provides invaluable education about your future home's systems and maintenance needs.

Title and Escrow Coordination

Washington State uses escrow companies rather than attorney closings. Your escrow officer coordinates between all parties, handles earnest money, orders title insurance, and facilitates the final closing.

Title insurance protects against ownership disputes, liens, or errors in public records. Lenders require a lender's policy, while an owner's policy (strongly recommended) protects your equity interest in the property.

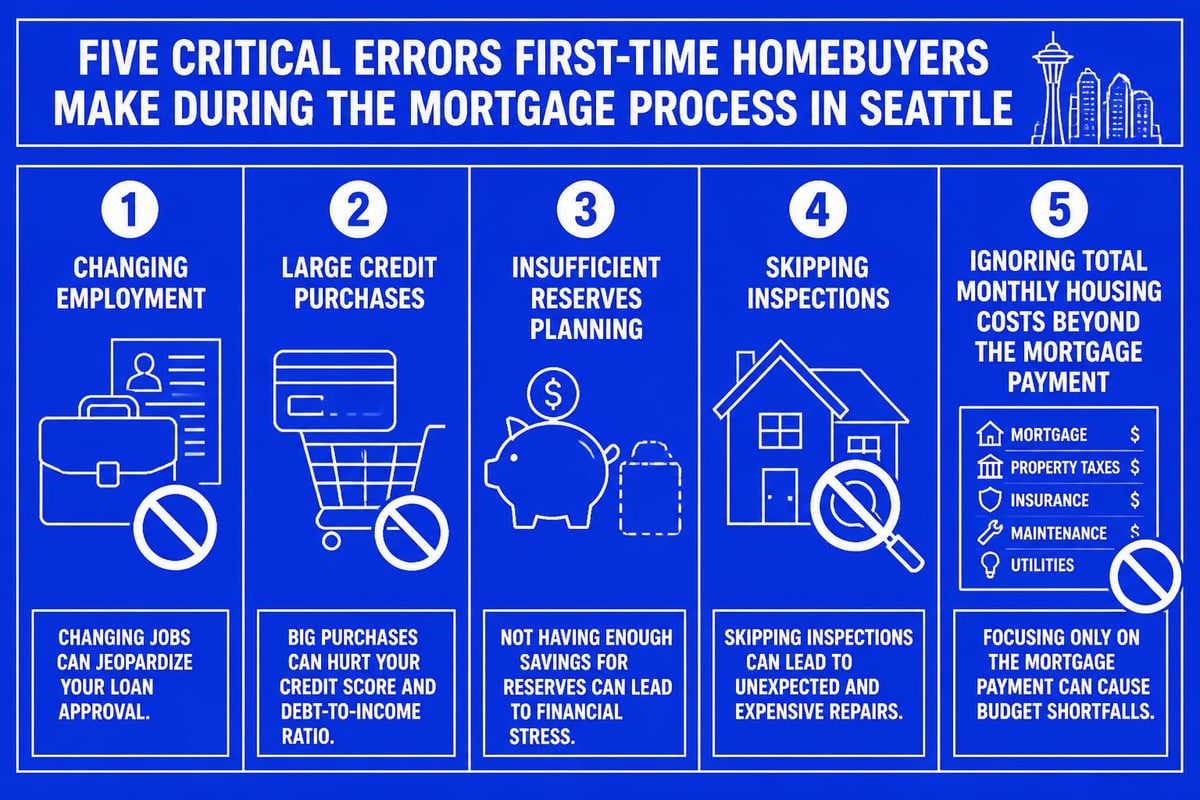

Common Mistakes to Avoid

Learning from others' experiences helps you sidestep costly errors. Kiplinger’s home buying lessons highlight how small oversights create significant complications when first time buying a house.

Financial Missteps

Critical mistakes that jeopardize your mortgage approval:

- Changing jobs during the mortgage process without discussing with your lender

- Making large purchases on credit before closing

- Moving money between accounts without maintaining clear paper trails

- Accepting deposits into your account that appear as undocumented income

- Co-signing loans for family or friends

- Opening new credit cards to earn rewards points

Even seemingly innocent actions can derail your closing. Lenders verify employment and re-pull credit immediately before funding. A new car loan or job change discovered at this stage can delay or cancel your closing entirely.

Market Timing Considerations

Attempting to time the market perfectly often backfires. Kiplinger’s advice on navigating tough housing markets emphasizes making decisions based on personal readiness rather than market predictions.

Interest rates fluctuate based on economic conditions beyond individual control. If you're financially prepared, have stable employment, and plan to stay in the property for at least five years, current market conditions matter less than your personal circumstances.

Calculating True Homeownership Costs

The mortgage payment represents just one component of homeownership expenses. Property taxes, insurance, utilities, maintenance, and HOA fees all impact your monthly budget.

Seattle Area Cost Breakdown

King County property taxes average 0.92% of assessed value annually, while Snohomish County averages slightly lower at 0.89%. A $700,000 home in Seattle generates approximately $6,440 in annual property taxes, or $537 monthly.

Monthly cost estimation for a $700,000 Seattle home:

| Expense Category | Monthly Cost | Annual Cost |

|---|---|---|

| Principal & Interest (6.5%, 10% down) | $3,980 | $47,760 |

| Property Taxes | $537 | $6,440 |

| Homeowners Insurance | $150 | $1,800 |

| PMI (until 20% equity) | $263 | $3,156 |

| HOA Fees (if applicable) | $350 | $4,200 |

| Utilities & Maintenance | $400 | $4,800 |

| Total Monthly | $5,680 | $68,156 |

This calculation assumes 10% down on a conventional loan. Larger down payments reduce or eliminate PMI, significantly lowering monthly obligations.

Building Reserve Funds

Beyond closing costs and down payment, maintaining 3-6 months of housing expenses in reserves provides financial cushion for unexpected repairs or income disruptions. Lenders often require 2-6 months of reserves for jumbo loans or investment properties.

Financial experts at Charles Schwab recommend maintaining separate reserves beyond your emergency fund specifically for home repairs and improvements. HVAC systems, roofs, and appliances all have finite lifespans requiring eventual replacement.

Maximizing Your Buying Power

Strategic planning before first time buying a house expands your options and negotiating position. Small adjustments to timing, documentation, and loan structure can increase your buying power by tens of thousands of dollars.

Documentation Optimization

For tech workers with stock compensation, the timing of your mortgage application relative to vesting schedules matters significantly. Applying after major vesting events provides the most recent evidence of continued equity compensation.

Optimal documentation timing strategies:

- Apply within 30 days of RSU vesting for current pay stub evidence

- Wait until after year-end bonuses hit your account for W-2 inclusion

- Gather two years of tax returns before changing employment

- Document side income through 1099s filed on your tax returns

- Maintain consistent employment with your primary employer

Chase Bank’s comprehensive guide emphasizes the importance of organizing financial documents months before you start house hunting. This preparation accelerates the approval process and identifies potential issues while you still have time to address them.

Rate Lock Strategies

Interest rate locks protect you from rate increases during your closing process but typically cost more for extended periods. Standard locks run 30-45 days, with options to extend for a fee.

Floating your rate means risking increases but potentially benefiting from decreases. Most borrowers lock once they have a signed purchase agreement, balancing protection with cost efficiency. Your broker should explain how rate lock timing impacts your specific situation based on market conditions and closing timeline.

Location-Specific Considerations Across Greater Seattle

First time buying a house varies significantly depending on which Seattle-area community you target. Each city offers distinct advantages, price points, and neighborhood characteristics.

Seattle Proper

Seattle neighborhoods range from affordable South Seattle options to premium Capitol Hill, Queen Anne, and Magnolia properties. The city's strong job market, walkability, and cultural amenities command premium prices, with median home values exceeding $850,000 in 2026.

Buyers working downtown often prioritize proximity to employers, light rail access, and urban amenities. First-time mortgage loans in Seattle frequently involve jumbo financing due to price points exceeding conforming limits.

Shoreline and Lake Forest Park

Moving north offers more space and often better school districts while maintaining reasonable Seattle commutes. Shoreline and Lake Forest Park provide excellent value propositions for families prioritizing yards, parks, and highly-rated schools.

These communities appeal to buyers seeking suburban amenities without sacrificing urban accessibility. Homes here typically range $650,000-$900,000, with larger properties and lots compared to Seattle proper.

Lynnwood, Mill Creek, and Everett

Snohomish County communities deliver maximum space per dollar, attracting buyers willing to commute for better housing value. Snohomish County home loans serve buyers targeting these growth areas with strong schools and family-friendly environments.

Mill Creek's planned community design, Lynnwood's retail corridor, and Everett's waterfront access each offer unique lifestyle advantages. First time buying a house in these areas often means newer construction, larger lots, and stronger appreciation potential as Seattle's growth continues northward.

Bellevue, Redmond, and Kirkland

Eastside communities compete with Seattle for tech workers prioritizing proximity to Microsoft, Google, Meta, and other major employers. These cities offer excellent schools, lower crime rates, and substantial retail amenities.

Premium pricing reflects these advantages, with median values in Bellevue exceeding $1.2 million and Redmond approaching $1 million. Buyers here frequently utilize jumbo financing and rely heavily on stock compensation for qualification.

Working with the Right Mortgage Professional

Your lender choice impacts your experience as much as the loan program itself. Finding a great mortgage broker means prioritizing experience, responsiveness, and local market knowledge over the lowest advertised rate.

Questions to Ask Potential Lenders

Evaluate mortgage professionals with these essential questions:

- How many first-time buyers have you closed in Seattle during the past 12 months?

- What percentage of your loans close on time without last-minute delays?

- Do you offer in-house underwriting or send files to remote processing centers?

- How do you qualify RSU, stock compensation, and bonus income?

- What is your average response time for client questions during the process?

- Can you provide references from recent clients with similar financial profiles?

According to NerdWallet’s guide for first-time homebuyers, working with professionals who specialize in your specific situation dramatically improves outcomes. A broker experienced with tech compensation understands how to position your file for optimal results.

Understanding Broker Value Versus Online Lenders

Online lenders advertise low rates but often lack flexibility for complex income situations. When first time buying a house with stock compensation, self-employment income, or unique property types, experienced local brokers provide solutions that automated systems cannot accommodate.

Brokers access multiple lenders, comparing programs to find optimal fits for your situation. This wholesale access often yields better rates than retail banks while providing personalized service throughout the closing process.

Long-Term Planning Beyond Your First Purchase

First time buying a house should align with a broader financial strategy encompassing career growth, family planning, and wealth building. The decisions you make now impact your flexibility and financial health for years to come.

Considering Future Flexibility

Life circumstances change. Job relocations, growing families, and evolving preferences may mean moving within 5-7 years. Choose loan programs and properties that maintain options rather than locking you into long-term constraints.

Adjustable-rate mortgages (ARMs) offer lower initial rates for buyers planning shorter holding periods. A 7/1 ARM provides seven years of fixed rates before adjusting, potentially saving thousands compared to 30-year fixed rates if you sell or refinance before adjustment.

Building Equity Strategically

Equity building accelerates through multiple channels:

- Principal paydown through regular mortgage payments

- Market appreciation in strong Seattle-area neighborhoods

- Strategic improvements that enhance property value

- Refinancing to eliminate PMI once reaching 20% equity

- Extra principal payments when cash flow allows

Fidelity’s step-by-step guide explains how homeownership fits within comprehensive financial planning, balancing mortgage paydown against retirement contributions, emergency funds, and investment diversification.

Your first home likely won't be your forever home. Viewing it as a stepping stone rather than a permanent solution reduces pressure to find perfection and helps you focus on building equity and establishing ownership.

Successfully navigating first time buying a house requires preparation, expert guidance, and strategic decision-making tailored to Seattle's competitive market conditions. Whether you're a tech professional leveraging stock compensation or a traditional W-2 employee building your down payment, working with an experienced local mortgage broker ensures you maximize buying power while avoiding common pitfalls. Keith Akada at Mortgage Reel brings 25+ years of experience helping Seattle-area buyers make confident purchase decisions, with expertise in qualifying complex income types and closing loans in as few as 9 business days-reach out today to start your homeownership journey with a trusted advisor who prioritizes education, transparency, and results.