Purchasing your first home in Washington State represents a significant milestone, particularly in competitive markets like Seattle, Bellevue, and surrounding communities. As a first time home buyer washington resident, you have access to numerous state-sponsored programs, specialized loan products, and strategic advantages designed specifically to help you transition from renter to homeowner. Understanding these resources and navigating the mortgage landscape with expert guidance can mean the difference between waiting years to buy and securing your dream home in 2026.

The Washington housing market presents unique challenges and opportunities for first-time buyers. With median home prices in King County exceeding $750,000 and neighboring areas like Shoreline and Lynnwood offering more affordable entry points, your strategy must align with both your financial capacity and long-term goals. Whether you're a tech professional at Amazon or Microsoft looking to leverage stock compensation, or a young family seeking a starter home in Everett, the right mortgage approach opens doors that might otherwise seem closed.

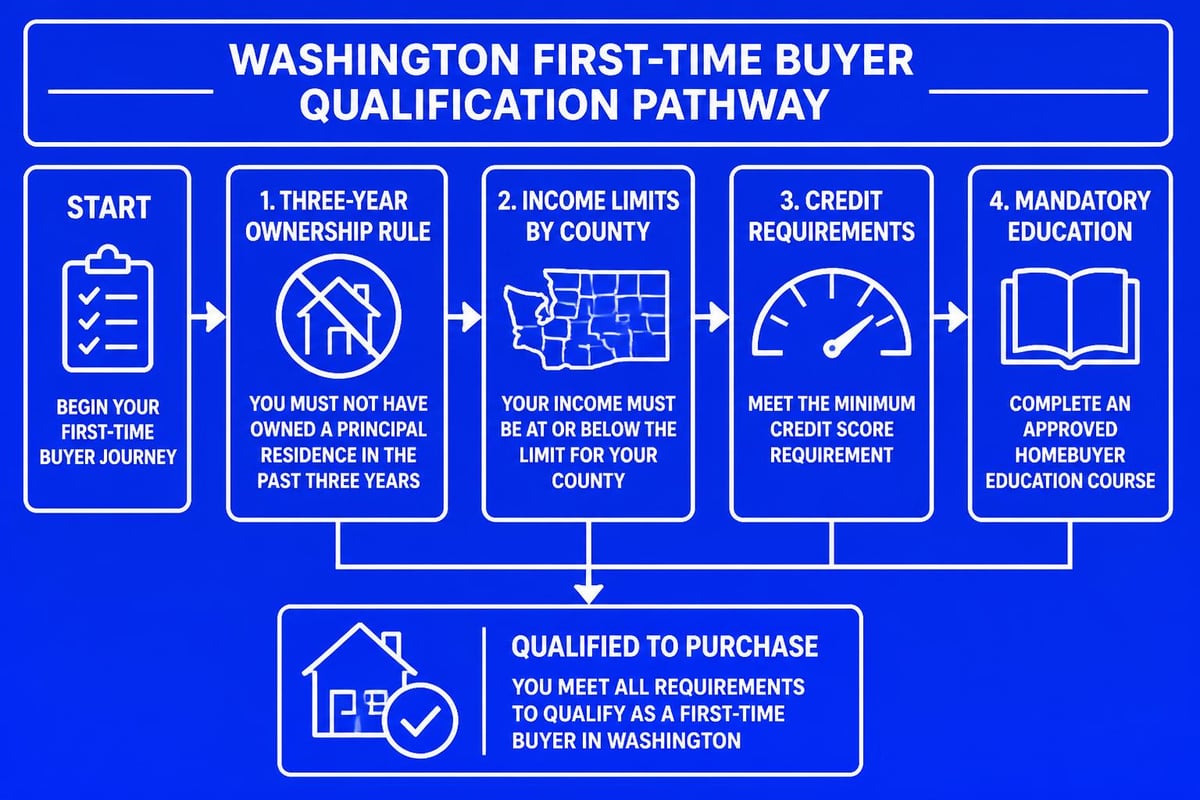

Understanding First Time Home Buyer Status in Washington

Washington State defines first-time homebuyers more broadly than many people realize. You qualify as a first time home buyer washington candidate if you haven't owned a principal residence in the past three years. This means even if you previously owned a home, you may still access first-time buyer programs and benefits.

The three-year lookback period creates opportunities for individuals who sold a home during relocation, divorce, or other life transitions. Additionally, single parents who only owned a home with a former spouse while married may qualify immediately, regardless of the three-year window.

Key Eligibility Criteria

Beyond the ownership timeline, Washington first-time buyer programs typically require:

- Primary residence commitment (the home must be your main dwelling)

- Income limitations that vary by county and program

- Credit score minimums ranging from 580 to 640 depending on the loan type

- Debt-to-income ratio generally below 43-50%

- Homebuyer education completion through approved providers

Most programs administered by the Washington State Housing Finance Commission require an eight-hour homebuyer education course. This investment pays significant dividends by preparing you for the responsibilities and financial realities of homeownership.

Washington State First-Time Buyer Programs and Assistance

Washington offers some of the most comprehensive first-time homebuyer programs in the nation. These initiatives address the primary barrier most first-time buyers face: accumulating sufficient down payment and closing costs while maintaining emergency reserves.

Home Advantage Program

The Home Advantage program through the Washington State Housing Finance Commission provides low down payment options with competitive interest rates. As a first time home buyer washington participant, you can access:

- Down payment assistance ranging from $15,000 to $45,000

- 30-year fixed-rate mortgages with no private mortgage insurance in some configurations

- Flexible credit requirements starting at 640 FICO

- Statewide availability including Seattle, Mill Creek, and Lake Forest Park

The program operates through approved lenders who understand the specific documentation and underwriting requirements. Working with an experienced mortgage broker ensures your application highlights qualifying income sources, including bonuses, overtime, and stock compensation for tech professionals.

House Key Program Options

The House Key family of loan products includes several variations designed for different buyer profiles:

| Program Name | Down Payment | Income Limit (King County) | Key Benefit |

|---|---|---|---|

| House Key Standard | 3% minimum | $178,100 (1-2 person) | Low rates, flexible terms |

| House Key Plus | 3.5% minimum | $178,100 (1-2 person) | DPA up to 4% of loan amount |

| House Key Opportunity | 3% minimum | $214,920 (1-2 person) | Higher income limits for targeted areas |

These programs work alongside conventional, FHA, and VA loan structures, providing flexibility for military veterans and those seeking home loans for first-time buyers in competitive neighborhoods.

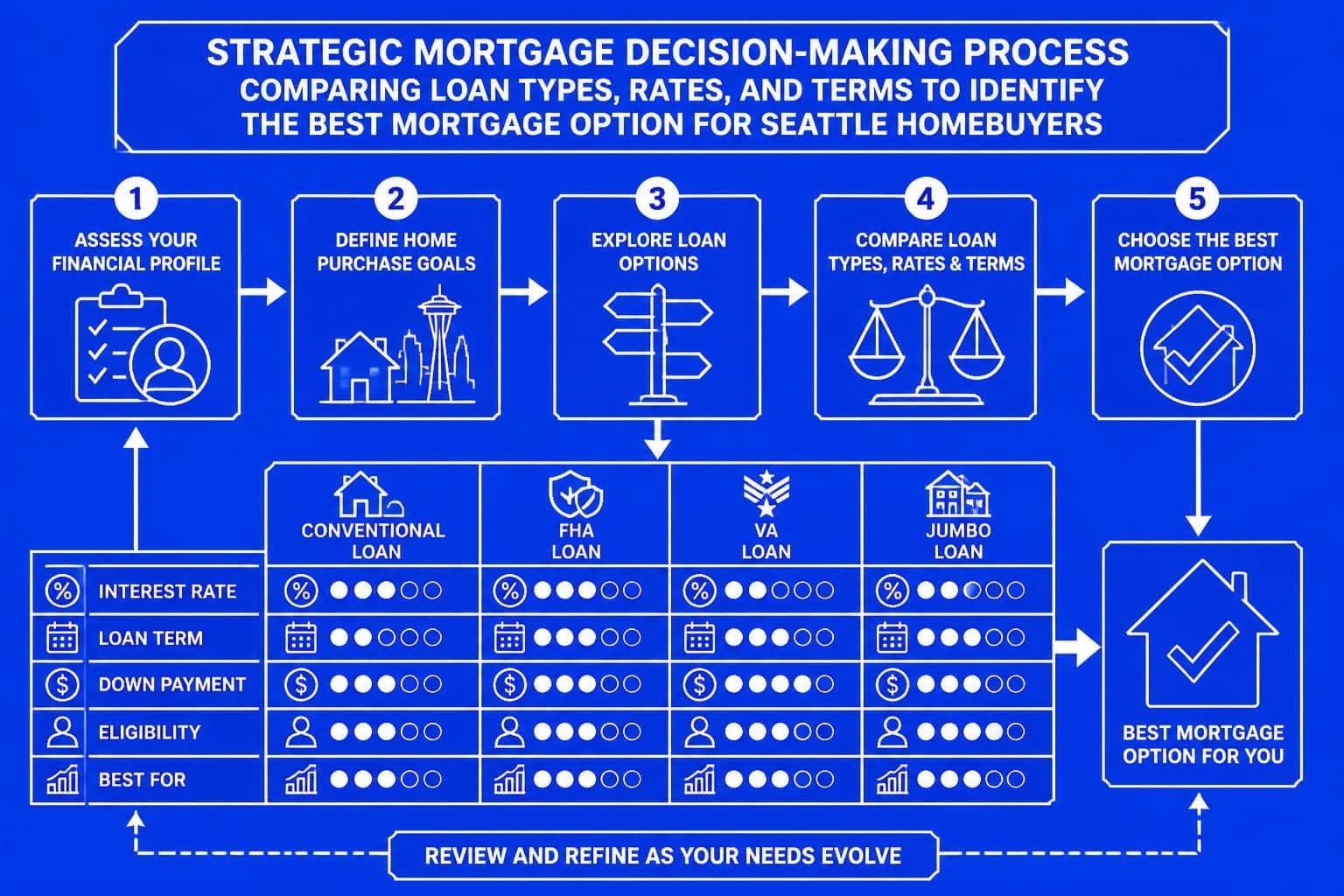

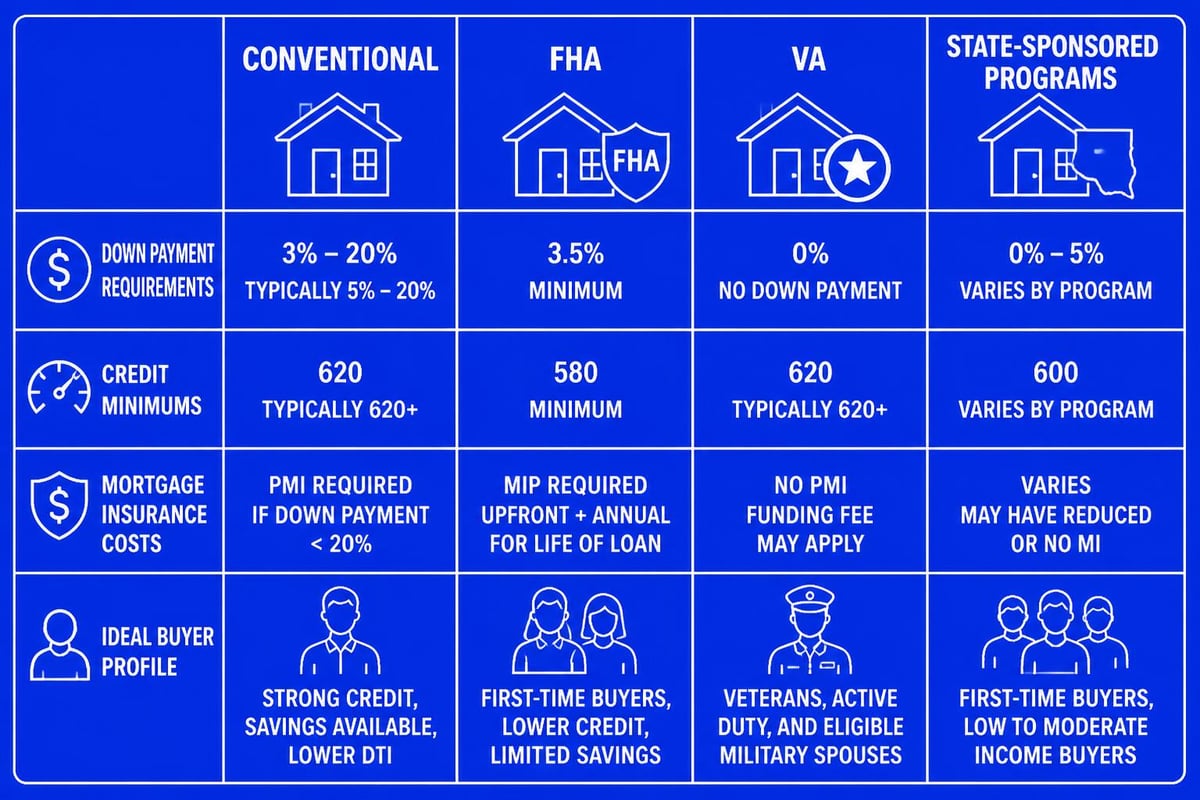

Financing Options for First-Time Buyers

Beyond state-specific programs, first time home buyer washington candidates should evaluate the full spectrum of mortgage products available in 2026. Each loan type carries distinct advantages depending on your down payment capacity, credit profile, and property selection.

Conventional Loans with Low Down Payment

Conventional mortgages now accommodate down payments as low as 3% for qualified first-time buyers. These loans, backed by Fannie Mae and Freddie Mac through programs like HomeReady and Home Possible, offer:

- Competitive interest rates for strong credit profiles (720+ FICO)

- The ability to cancel PMI once you reach 20% equity

- Higher loan limits suitable for Seattle and Bellevue markets

- Flexibility in property type including condos and townhomes

For buyers with stable employment, minimal debt, and strong credit, conventional financing often provides the most cost-effective path to homeownership. Understanding conventional loan options helps you compare true costs beyond just the interest rate.

FHA Loans: Lower Credit Requirements

Federal Housing Administration loans remain popular among first-time Washington buyers due to their accessible qualification standards. With down payments starting at 3.5% and credit scores accepted as low as 580, FHA financing opens doors for buyers still building credit history.

The trade-off involves mandatory mortgage insurance premiums both upfront (1.75% of the loan amount) and monthly. However, for buyers purchasing in areas like Lynnwood or Shoreline where home prices remain more moderate, the total cost may be lower than saving for a larger down payment on a conventional loan.

VA Loans for Military Service Members

Veterans and active-duty service members buying in Washington gain substantial advantages through VA financing. Zero down payment requirements combined with no private mortgage insurance create powerful purchasing leverage in expensive markets.

VA loans also feature:

- More lenient credit requirements (typically 620 minimum)

- Limits on closing costs sellers can require buyers to pay

- No prepayment penalties

- Assumability by future buyers (subject to lender approval)

The Seattle metro area has significant military presence with Joint Base Lewis-McChord nearby, making VA loans a common choice for first time home buyer washington veterans transitioning to civilian homeownership.

Maximizing Your Down Payment and Closing Cost Strategy

The perception that you need 20% down prevents many qualified renters from pursuing homeownership. In reality, strategic down payment planning combined with available assistance programs enables first time home buyer washington purchases with significantly less upfront capital.

Calculating Total Cash Requirements

Beyond the down payment percentage, first-time buyers must budget for:

- Earnest money deposit (typically 1-3% of purchase price, applied toward down payment)

- Closing costs (2-5% of loan amount including title, escrow, and lender fees)

- Inspection and appraisal fees ($500-$1,500 combined)

- Homeowners insurance (first year often due at closing)

- Property tax reserves (2-6 months depending on closing date)

- HOA fees (if applicable, often prepaid for several months)

For a $600,000 home in Seattle with 5% down, total cash required at closing typically ranges from $45,000 to $55,000 depending on the specific loan program and negotiated seller concessions.

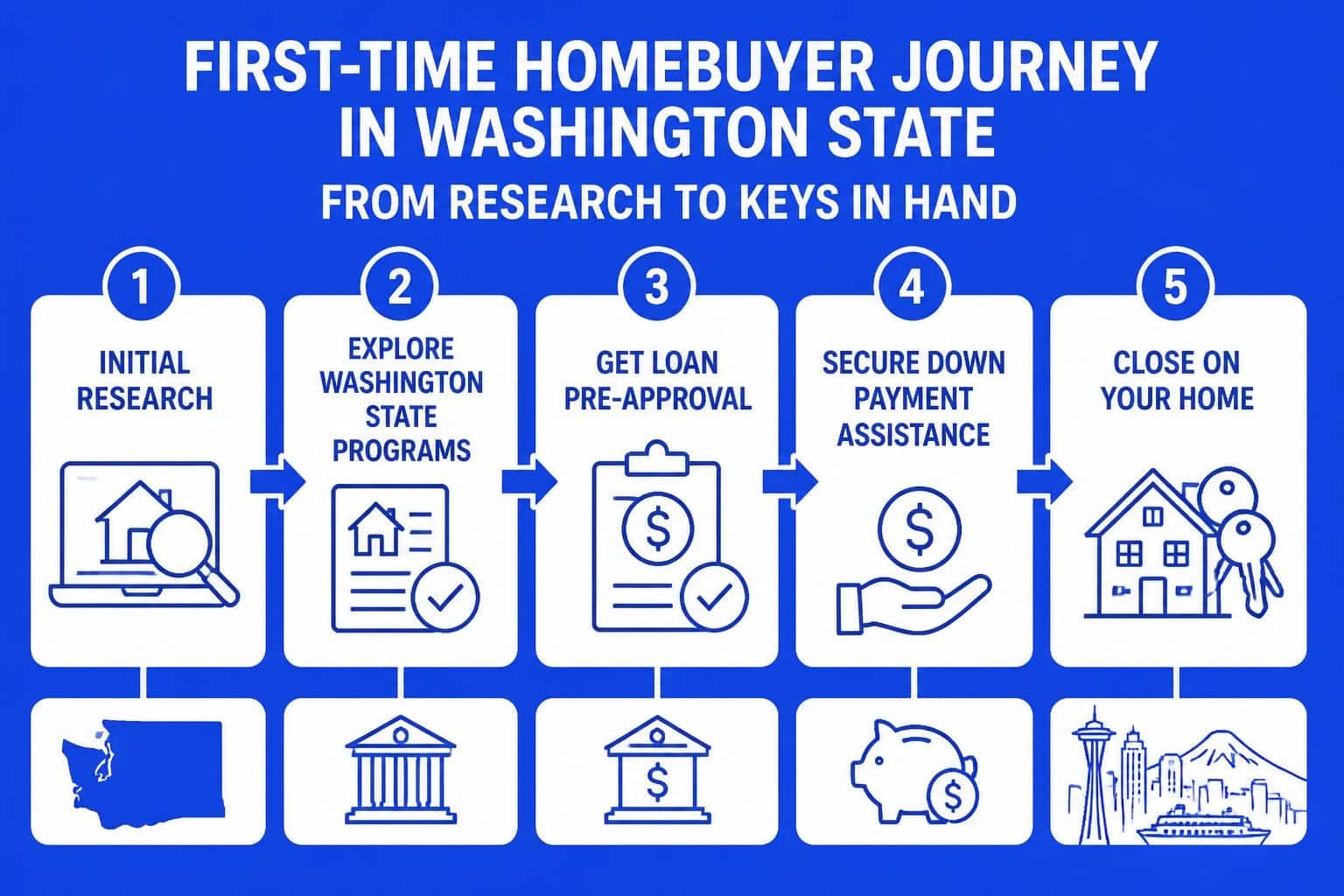

Leveraging Down Payment Assistance

Washington provides multiple pathways to reduce your upfront cash requirement. The Consumer Financial Protection Bureau’s homeownership resources help buyers understand how these programs integrate with primary financing.

Down payment assistance in Washington typically comes as:

- Deferred second mortgages with no monthly payment, forgiven after remaining in the home for a specified period

- Zero-interest loans repayable only when you sell or refinance

- Grants requiring no repayment if you meet residency requirements

Combining state assistance with employer programs common among Seattle tech companies creates powerful purchasing capability. Many Amazon and Microsoft employees can access additional down payment support through benefits programs while simultaneously qualifying for state assistance.

Navigating the Seattle-Area Housing Market

The greater Seattle region presents distinct submarkets with varying price points and competition levels. As a first time home buyer washington candidate, understanding where your budget aligns with available inventory determines your search strategy.

Price Points Across King and Snohomish Counties

The 2026 housing market continues showing geographic price differentiation:

| Area | Median Home Price | Typical Starter Home | Competition Level |

|---|---|---|---|

| Seattle (Central) | $875,000 | $650,000+ | Extremely High |

| Bellevue | $1,150,000 | $750,000+ | Extremely High |

| Shoreline | $725,000 | $550,000 | High |

| Lake Forest Park | $695,000 | $575,000 | Moderate-High |

| Lynnwood | $625,000 | $500,000 | Moderate |

| Everett | $565,000 | $425,000 | Moderate |

These figures reflect single-family homes; condos and townhomes in each area typically price 15-25% lower, providing alternative entry points for budget-conscious first-time buyers.

Timing Your Purchase in 2026

Market conditions in Washington favor prepared buyers who can act decisively. Inventory remains constrained in desirable neighborhoods, though gradual improvement from 2025 levels provides more selection than the previous three years.

Spring and early summer traditionally bring peak competition, while late fall and winter offer reduced buyer pools but also limited inventory. Your timeline should prioritize financial readiness over seasonal timing, as the right property at favorable terms can appear any month.

Working with an experienced mortgage professional who provides quick closings helps you compete effectively when your ideal home hits the market. Pre-approval with full underwriting creates seller confidence that your financing won't delay or jeopardize the transaction.

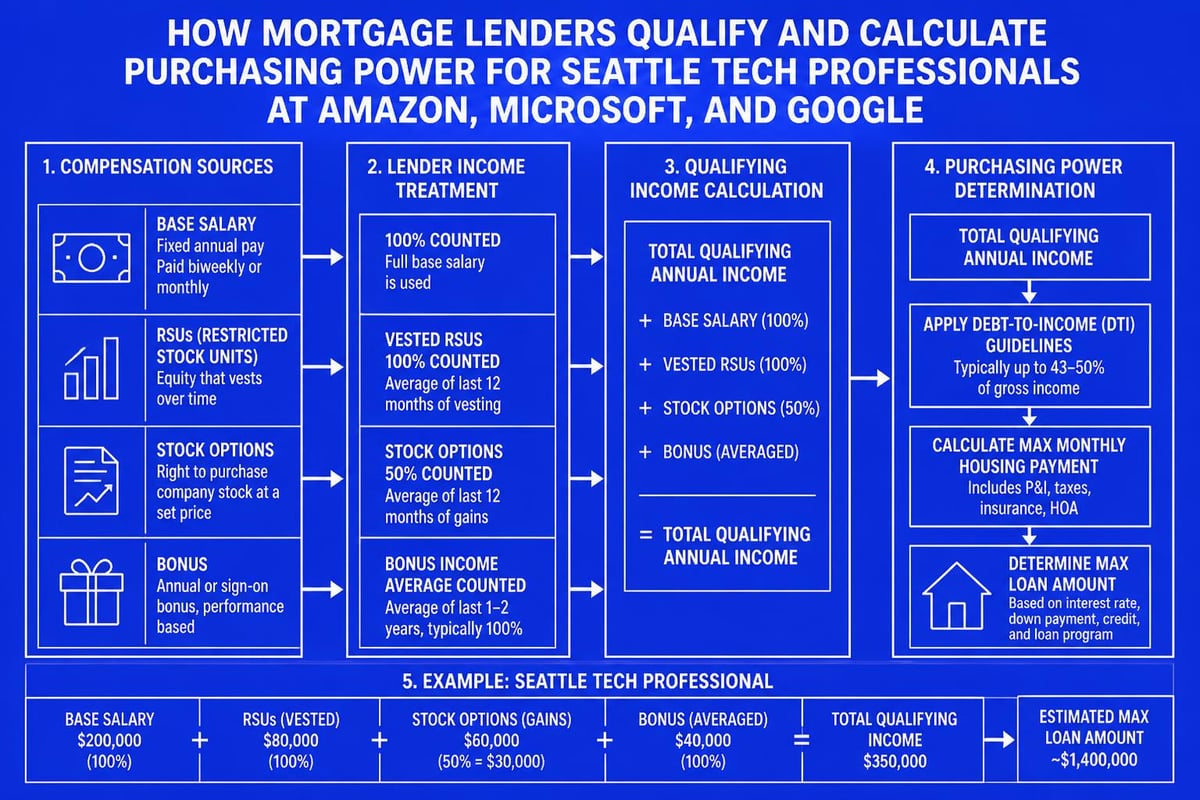

Qualifying Income for Tech Professionals

Seattle's economy centers on technology companies offering substantial compensation through salary, bonuses, and equity. As a first time home buyer washington tech employee, understanding how mortgage underwriting evaluates these income sources maximizes your purchasing power.

Stock Compensation and RSU Qualification

Restricted Stock Units and stock options create mortgage-qualifying income when properly documented and analyzed. Lenders typically require:

- Two years of vesting history showing consistent equity compensation

- Evidence of continued grants through offer letters or HR documentation

- Discount for volatility (often 25-30% of the income amount)

- Tax returns reflecting the income over multiple years

For Amazon, Microsoft, and Google employees, this specialized underwriting often adds $100,000 to $300,000 in purchasing power compared to qualifying on base salary alone. This expertise proves particularly valuable when pursuing jumbo home loans for properties exceeding conforming loan limits.

Bonus and Overtime Income

Variable income requires two-year history for full consideration in most mortgage programs. However, certain exceptions apply for recent promotions or job changes within the same field. Documentation requirements include:

- Pay stubs showing year-to-date bonuses or overtime

- W-2 forms from previous two years

- Employer letter confirming bonus structure is likely to continue

- Written explanation of any significant income fluctuations

Strategic timing of your home purchase relative to bonus payment schedules affects both qualification and available down payment funds. Planning these elements six months ahead of your intended purchase date creates optimal positioning.

Pre-Approval Process and Timeline

Securing legitimate pre-approval represents your first major step as a first time home buyer washington candidate. This process differs substantially from informal pre-qualification, providing sellers and listing agents confidence in your ability to close.

Documentation Requirements

Comprehensive pre-approval requires submitting:

- Two years of tax returns with all schedules

- Recent pay stubs (last 30 days)

- Two months of bank statements for all accounts

- Photo identification (driver's license or passport)

- Authorization for credit report (signed consent form)

- Employment verification (signed VOE or HR contact)

- Documentation of debts (student loans, auto loans, credit cards)

For self-employed buyers or those with complex income structures, additional documentation including profit and loss statements, business tax returns, and CPA-prepared financials become necessary.

Underwriting Timeline and Conditions

Full underwriting review during pre-approval identifies potential issues before you're under contract, reducing stress and surprise denials. The process typically requires:

- Initial submission and credit review (1-2 business days)

- Income and asset verification (2-3 business days)

- Underwriter analysis and conditions (1-2 business days)

- Condition clearing and final approval (1-3 business days)

Total timeline from application to full underwritten pre-approval ranges from 5-10 business days depending on documentation completeness and lender capacity. This investment pays significant returns when competing against other buyers with less rigorous approval letters.

Understanding Closing Costs and Fees

Beyond down payment considerations, first time home buyer washington purchasers must budget for various closing costs and fees. These expenses, while negotiable in some cases, require cash reserves separate from your down payment.

Typical Cost Breakdown

Washington closing costs generally include:

- Loan origination fees (0.5-1.0% of loan amount)

- Appraisal fee ($600-$850 for standard properties)

- Credit report ($50-$100)

- Title insurance (varies by purchase price, roughly $1,000-$2,500)

- Escrow fees (split with seller, approximately $500-$1,200 buyer portion)

- Recording fees ($200-$400)

- Home inspection (optional but recommended, $400-$700)

- Survey (if required, $400-$800)

For a $600,000 purchase with $30,000 down, total closing costs typically range from $12,000 to $18,000. Some programs allow rolling certain costs into the loan amount, while others require cash payment.

Negotiating Seller Concessions

Market conditions and property circumstances determine seller willingness to contribute toward buyer closing costs. In balanced or buyer-favorable markets, requesting 2-3% seller concessions creates realistic expectations.

These contributions reduce your cash requirement at closing but increase the purchase price proportionally. The strategy makes particular sense when you're cash-constrained but can qualify for a slightly larger loan amount. Your mortgage advisor and real estate agent should coordinate this negotiation to optimize your financial position.

Credit Score Optimization Strategies

Your credit profile directly impacts both mortgage approval odds and the interest rate you'll receive. As a first time home buyer washington candidate, dedicating three to six months to credit improvement can save tens of thousands of dollars over your loan's lifetime.

Score Ranges and Rate Impact

Mortgage pricing tiers create meaningful cost differences based on credit score bands:

- 740+ FICO: Best available rates, maximum program eligibility

- 700-739 FICO: Slightly higher rates (typically 0.25-0.50% increase)

- 660-699 FICO: Moderate rate premiums (0.50-1.00% increase)

- 620-659 FICO: Higher rates and limited program options

- Below 620 FICO: FHA or state programs only, substantial rate premiums

For a $500,000 loan amount, the difference between 740 and 680 credit scores might mean $150-$250 in additional monthly payment due to higher interest rates and mortgage insurance adjustments.

Rapid Improvement Techniques

If your credit score falls below ideal ranges, focus on these high-impact actions:

- Pay down credit card balances below 30% of limits (under 10% provides maximum benefit)

- Dispute any inaccurate information on your credit reports

- Avoid opening new credit accounts during the mortgage process

- Become an authorized user on a family member's established, positive account

- Request goodwill adjustments from creditors for isolated late payments

Timeline matters significantly here. Most credit improvements require 30-60 days to reflect in updated scores, so beginning this process well before home shopping creates optimal results.

Property Types and First-Time Buyer Considerations

First time home buyer washington candidates often debate between single-family homes, condos, and townhomes. Each property type carries distinct advantages, costs, and lifestyle implications.

Single-Family Home Benefits

Detached homes provide maximum privacy, control, and typically better long-term appreciation potential. In markets like Mill Creek or Lake Forest Park, single-family inventory at entry-level prices remains available, offering:

- No shared walls or HOA governance over property use

- Land ownership with potential for additions or modifications

- Generally easier financing and higher desirability for resale

- More space for growing families or remote work arrangements

The trade-off involves higher maintenance responsibilities and typically higher purchase prices compared to attached housing options.

Condo and Townhome Advantages

Attached housing provides lower entry costs and reduced maintenance burdens, appealing to busy professionals or those prioritizing location over square footage. Seattle's urban neighborhoods offer numerous condo options within walking distance of employment centers.

Considerations include:

- HOA fees ranging from $200 to $800+ monthly depending on amenities

- Reserve fund health (review HOA financials before purchasing)

- Special assessments potential for major building repairs

- Rental restrictions that may limit future flexibility

- FHA approval status (some condos don't meet FHA requirements)

For first-time buyers prioritizing Bellevue or Seattle proper, condos and townhomes often represent the only sub-$600,000 options in desirable neighborhoods.

Common Mistakes to Avoid

First-time buyers frequently encounter preventable setbacks that delay or derail their homeownership goals. Learning from others' experiences helps you navigate the process more successfully as a first time home buyer washington participant.

Financial Missteps

- Making large purchases or opening new credit during the mortgage process

- Changing employment before closing without discussing implications with your lender

- Depleting all savings for down payment without maintaining emergency reserves

- Overlooking property tax implications in different municipalities

- Failing to budget for maintenance, utilities, and homeownership costs beyond the mortgage

Process Errors

- Skipping home inspection to make offers more competitive

- Waiving financing contingencies without fully underwritten approval

- Failing to research neighborhoods thoroughly before committing

- Underestimating commute times to employment centers

- Overlooking school quality if children are in your future plans

Professional guidance from an experienced mortgage broker and qualified real estate agent prevents most of these issues. Choosing experienced local professionals who understand Washington's specific requirements and market dynamics provides invaluable protection during your transaction.

Tax Benefits and Long-Term Financial Planning

Homeownership creates several tax advantages that improve your overall financial position compared to renting. As a first time home buyer washington taxpayer, understanding these benefits helps you calculate the true cost of ownership.

Mortgage Interest Deduction

You can deduct mortgage interest paid on loans up to $750,000 (the limit for mortgages originated after December 15, 2017). For most first-time buyers in Washington, this represents your entire loan amount, creating substantial tax savings.

In the early years of your mortgage, interest comprises the majority of each payment. A $500,000 loan at 6.5% interest generates roughly $32,000 in deductible interest during year one, potentially reducing your federal tax liability by $7,000-$10,000 depending on your bracket.

Property Tax Deduction

Washington property taxes, while lower than many states, remain deductible up to $10,000 annually when combined with state and local taxes. This cap, part of the Tax Cuts and Jobs Act, affects high-income earners more significantly but still provides benefit for most first-time buyers.

Building Equity Versus Renting

The financial comparison between renting and owning extends beyond monthly payments. Each mortgage payment builds equity in an appreciating asset, creating forced savings and wealth accumulation. Historical Seattle appreciation rates averaging 4-6% annually compound this benefit.

| Scenario | After 5 Years | After 10 Years |

|---|---|---|

| Renting ($2,500/month) | $0 equity | $0 equity |

| Owning ($3,000/month) | $75,000-$100,000 equity | $175,000-$225,000 equity |

These projections assume 3% down payment, 4% annual appreciation, and principal paydown through normal amortization. Individual results vary based on market performance and specific loan terms.

Resources and Next Steps

Taking action as a first time home buyer washington candidate requires assembling the right team and resources. Success depends on preparation, education, and strategic execution.

Essential Educational Resources

- Complete the required homebuyer education through approved Washington providers

- Review Bankrate’s comprehensive first-time homebuyer guide for national perspective

- Explore Zillow’s home buying resources for market data and tools

- Attend first-time buyer seminars offered by housing counseling agencies

- Meet with mortgage professionals to understand your specific qualification picture

Building Your Professional Team

Successful home purchases require coordination among:

- Mortgage broker or loan officer with Washington expertise and strong communication

- Real estate agent specializing in first-time buyers and your target neighborhoods

- Home inspector providing thorough property evaluation

- Real estate attorney (optional in Washington but valuable for complex transactions)

- Insurance agent offering competitive homeowners coverage

Starting with mortgage pre-approval before engaging a real estate agent ensures you're searching within realistic price parameters and can act quickly when you find the right property.

Becoming a homeowner in Washington State requires understanding available programs, optimizing your financial profile, and working with professionals who prioritize your success. Whether you're targeting Seattle's urban core or considering more affordable communities like Lynnwood and Everett, the right mortgage strategy transforms homeownership from aspiration to reality. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping first-time buyers navigate Washington's housing market, from qualifying complex tech compensation to securing approvals in as few as 9 business days. With 750+ five-star reviews and deep expertise in state programs, stock-based income, and competitive markets, we're ready to guide you from pre-approval through closing.