Buying your first home in the Seattle area represents one of the most significant financial decisions you'll ever make. With median home prices consistently above the national average and a competitive market driven by tech industry growth, first time buyers face unique challenges-but also powerful opportunities. Understanding your financing options, qualification strategies, and local programs can transform what feels overwhelming into an achievable milestone. Whether you're targeting neighborhoods in Seattle, Shoreline, or Lake Forest Park, a strategic approach to your home loan makes all the difference in securing the right property at the right price.

Understanding What First Time Buyers Actually Need

The definition of a first-time homebuyer extends beyond someone who has never owned property. According to federal guidelines, you qualify as a first time buyer if you haven't owned a primary residence in the past three years. This means even if you previously owned a home, you may still access programs designed for new buyers.

Key qualifications that define first time buyer status:

- No primary residence ownership in the previous 36 months

- Divorced individuals who owned jointly but not individually

- Single parents who owned only with a former spouse

- Previous ownership of a property not permanently affixed to a foundation

For Seattle-area buyers, this distinction matters significantly when accessing Washington State first-time buyer programs that offer down payment assistance, reduced interest rates, or tax credits. Many tech professionals relocating to Bellevue or Redmond from other states where they owned property can still qualify under these guidelines.

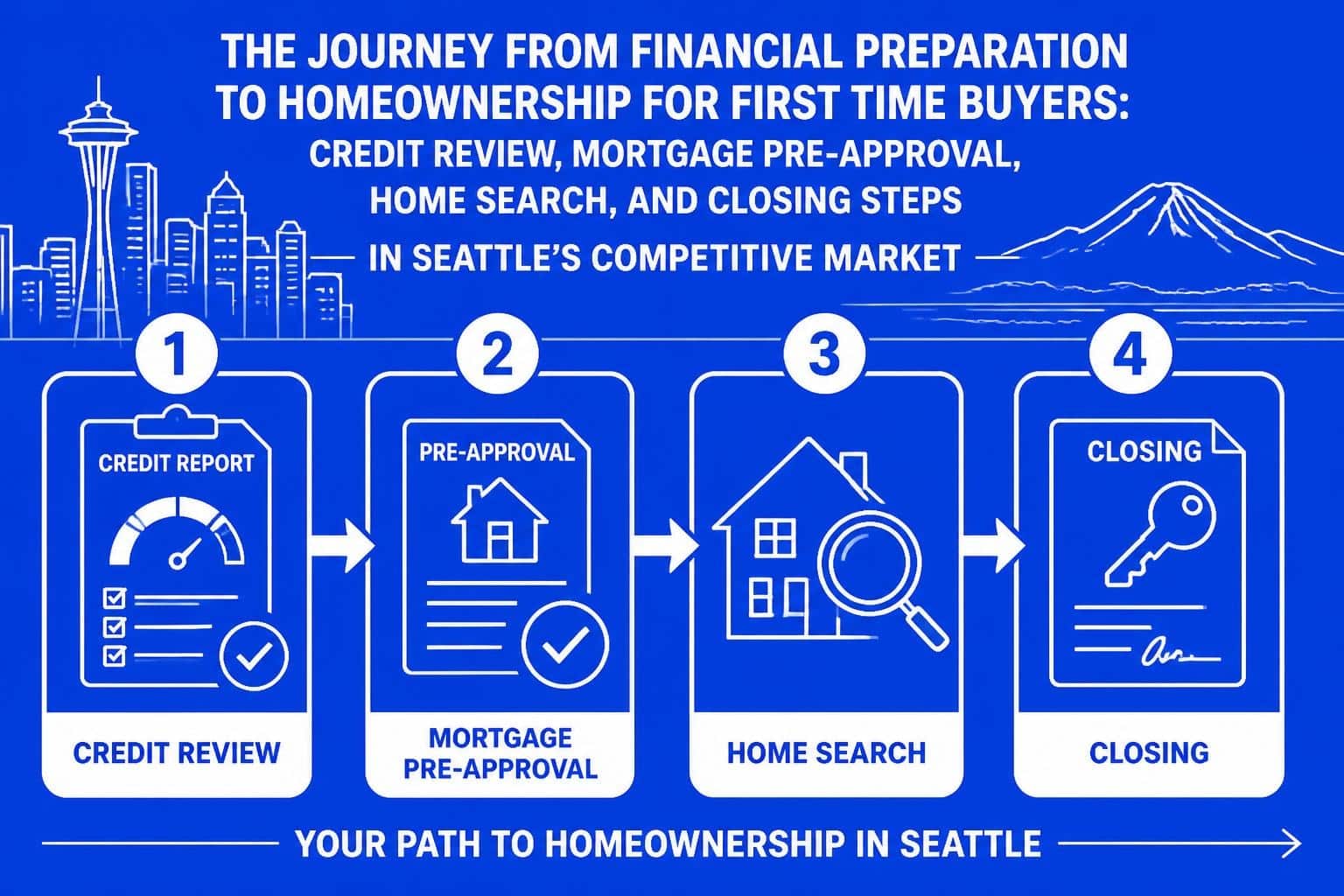

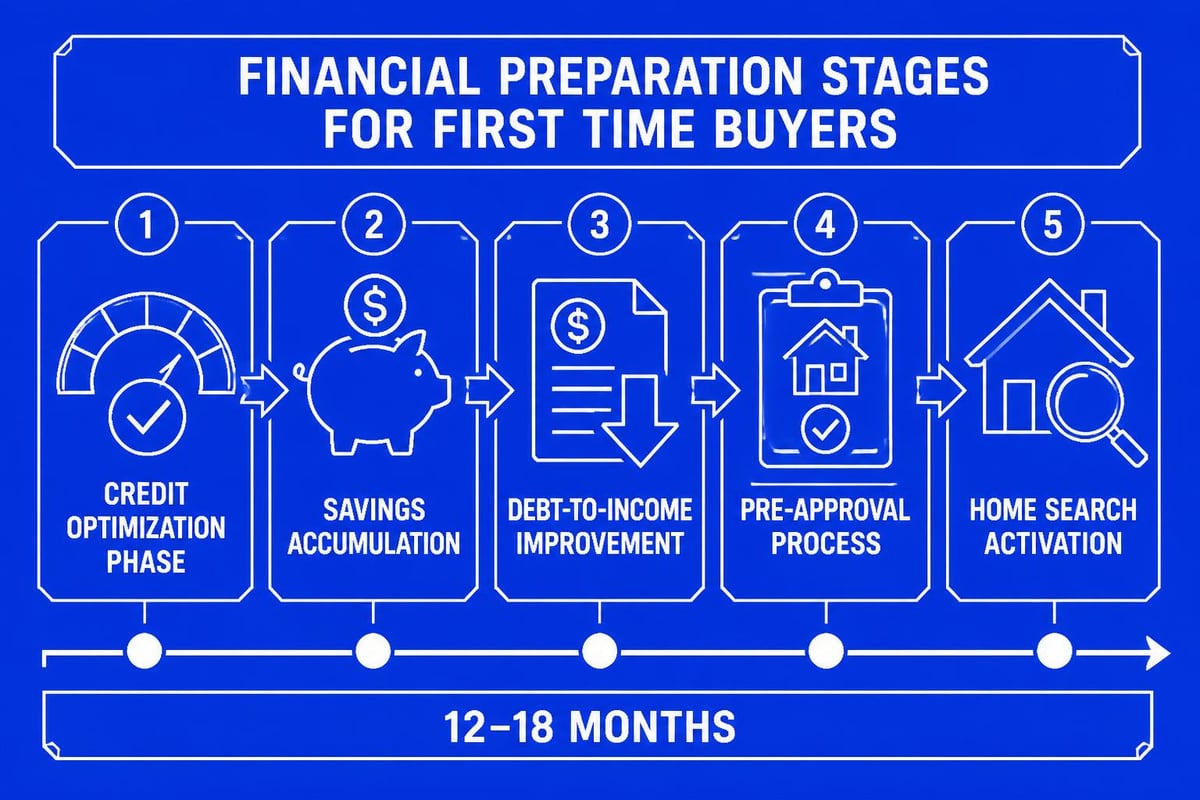

Financial Preparation Timeline for New Homebuyers

Successful first time buyers typically begin their financial preparation 12 to 18 months before seriously house hunting. This timeline allows for credit score improvement, savings accumulation, and strategic debt reduction.

| Preparation Phase | Timeline | Key Actions |

|---|---|---|

| Credit Building | 12-18 months out | Pay down balances, dispute errors, avoid new credit |

| Savings Acceleration | 9-12 months out | Automate transfers, reduce expenses, explore assistance programs |

| Pre-Approval Readiness | 3-6 months out | Gather documentation, compare lenders, understand options |

| Active House Hunting | 1-3 months out | Work with agent, submit offers, lock rate |

The Seattle housing market moves quickly, particularly in desirable neighborhoods like Montlake, Capitol Hill, and Shoreline. Having your finances prepared before you find your dream home prevents missed opportunities and strengthens your offer in competitive situations.

Loan Programs Designed for First Time Buyers

First time buyers have access to several specialized loan programs, each with distinct advantages depending on your financial situation, employment type, and long-term housing goals.

Conventional Loans with Low Down Payments

Contrary to popular belief, you don't need 20% down to buy a home. Conventional loans through qualified mortgage financing allow down payments as low as 3% for first time buyers. These programs require private mortgage insurance (PMI) when you put down less than 20%, but PMI automatically cancels once you reach 22% equity.

Benefits of conventional loans for new buyers:

- Flexible property types including condos and townhomes

- Competitive interest rates for strong credit profiles

- PMI removal once equity threshold is reached

- Lower overall costs compared to government-backed alternatives

- Gift funds allowed from family members for down payment

For Seattle tech professionals earning substantial compensation through RSUs and stock options, conventional loans often provide the most efficient path to homeownership, particularly when a skilled broker can properly document and qualify equity-based income.

FHA Loans for Buyers with Limited Savings

Federal Housing Administration (FHA) loans require just 3.5% down and accept credit scores as low as 580, making them accessible for first time buyers who haven't had years to build perfect credit. The tradeoff involves mortgage insurance that remains for the life of the loan on most FHA mortgages originated today.

In competitive Seattle neighborhoods, FHA financing can occasionally face resistance from sellers who prefer conventional financing or cash offers. However, in areas like Everett, Lynnwood, and Mill Creek, FHA loans remain widely accepted and represent excellent options for buyers prioritizing affordability over speed.

State and Local Down Payment Assistance

Washington State offers several programs specifically supporting first time buyers, including the Home Advantage program that provides competitive interest rates and down payment assistance. These programs often feature income limits that vary by county and household size.

First time buyers in King County can access grants and forgivable loans covering 3-5% of the purchase price, significantly reducing the cash needed at closing. Similar programs exist in Snohomish County, making homeownership more accessible across the greater Seattle region.

Maximizing Your Buying Power with Tech Income

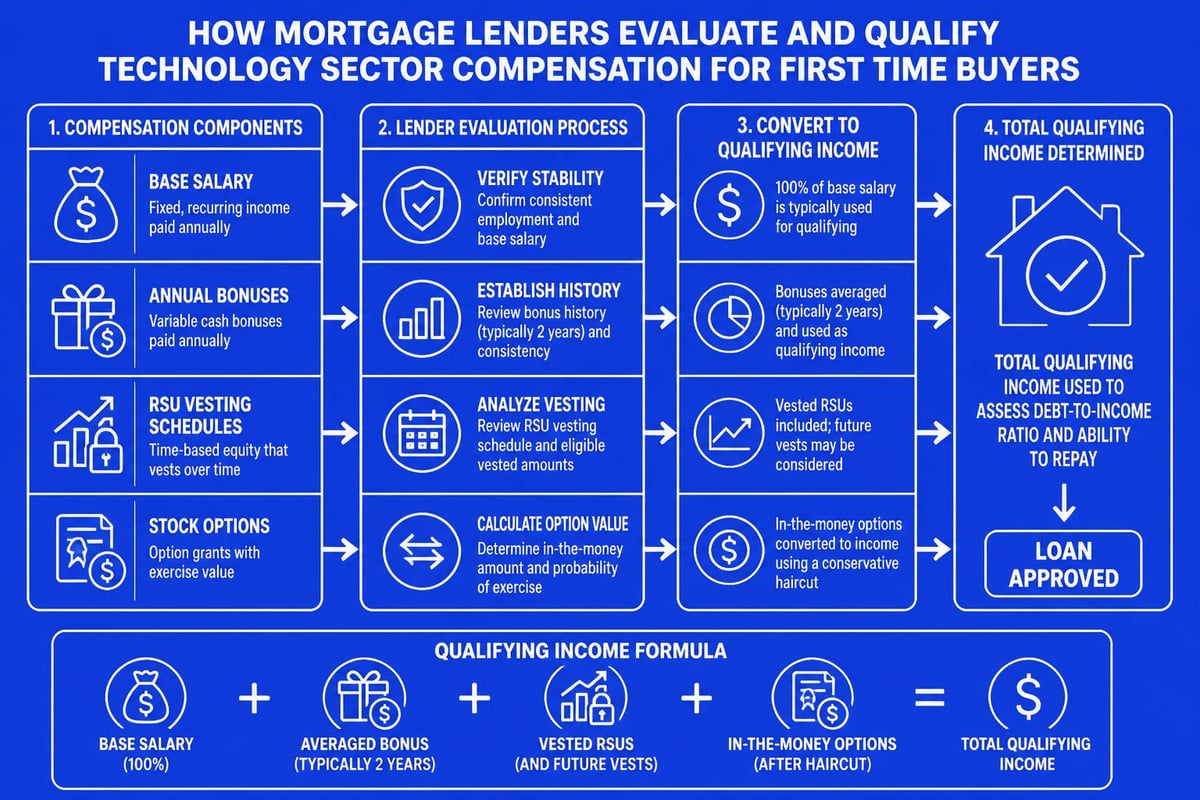

Seattle's concentration of high-paying technology employers creates unique opportunities and challenges for first time buyers. Understanding how lenders qualify stock compensation, bonuses, and restricted stock units (RSUs) can dramatically increase your purchasing power.

How Lenders Qualify RSUs and Stock Compensation

Traditional mortgage underwriting focuses on W-2 income, but tech professionals often receive substantial compensation through equity. Experienced mortgage brokers can document this income properly, typically requiring:

- Two years of vesting history showing consistent RSU grants

- Recent paystubs reflecting stock sales and withholdings

- Employment verification confirming future vesting schedules

- Calculation methodology averaging historical vesting amounts

For Amazon, Microsoft, and Google employees in the Seattle area, properly qualifying stock income can increase purchasing power by $100,000 to $300,000 or more, opening access to neighborhoods and property types that seemed financially out of reach.

Jumbo Loan Strategies for High Earners

When home prices exceed conforming loan limits ($806,500 in 2026 for most areas), first time buyers need jumbo loan financing. These loans require stronger financial profiles but offer competitive rates for qualified borrowers.

Jumbo loan qualification factors:

- Credit scores typically 700 or higher

- Debt-to-income ratios below 43%

- Reserves covering 6-12 months of housing payments

- Larger down payments, often 10-20%

- Comprehensive documentation of all income sources

First time buyers in Bellevue, Kirkland, and Seattle neighborhoods with higher price points benefit from working with brokers experienced in jumbo financing who understand how to structure loans optimally and present files to underwriters effectively.

Navigating Seattle's Competitive Housing Market

The greater Seattle area consistently ranks among the nation's most competitive housing markets. First time buyers need strategic approaches to stand out among multiple offers while protecting their financial interests.

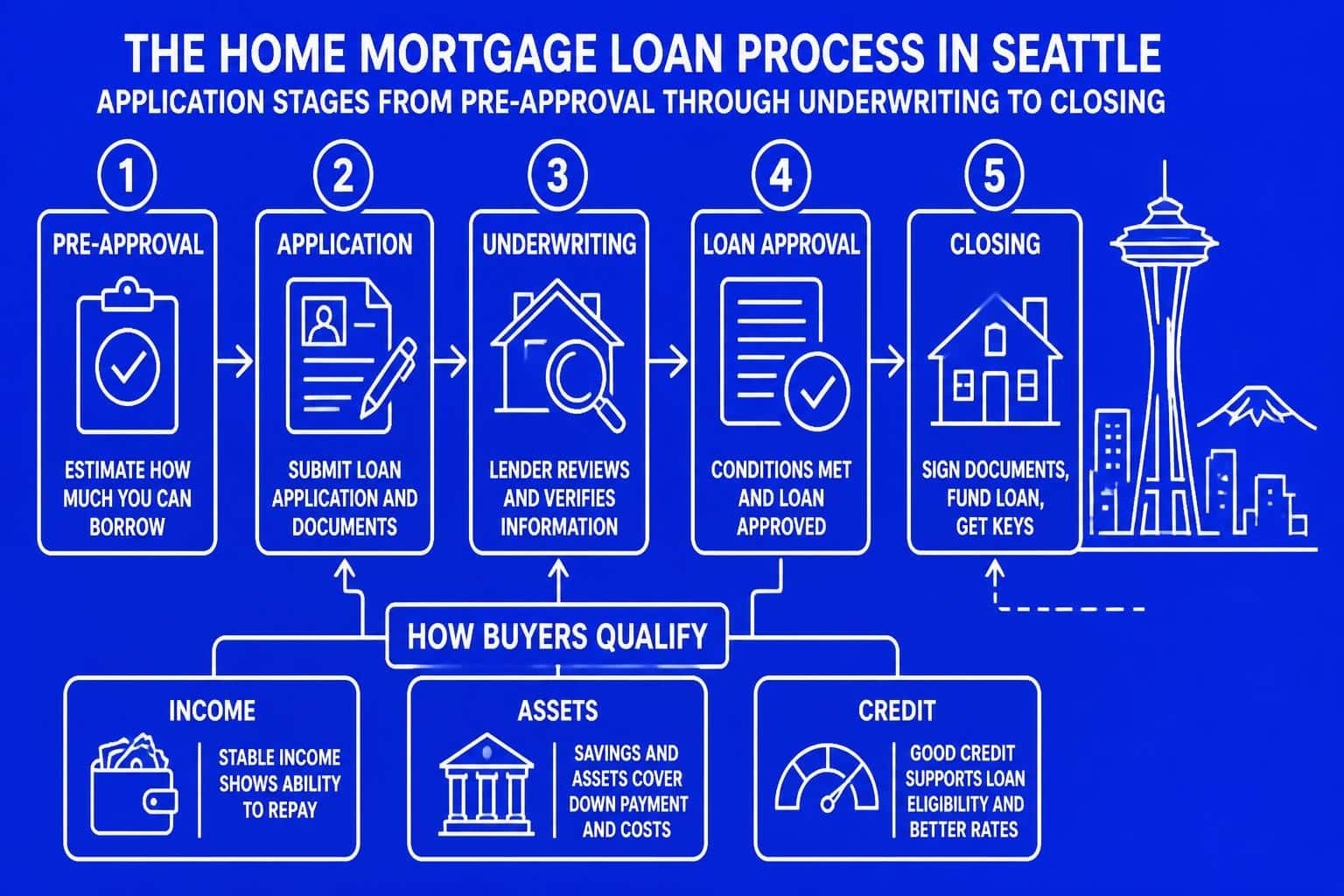

Pre-Approval Versus Pre-Qualification

Many first time buyers mistakenly believe pre-qualification letters carry the same weight as pre-approval. The distinction matters significantly in competitive scenarios.

| Feature | Pre-Qualification | Pre-Approval |

|---|---|---|

| Credit Check | Optional or soft pull | Hard credit inquiry required |

| Documentation | Self-reported information | Full verification of income, assets, employment |

| Underwriter Review | No underwriter involvement | File reviewed by underwriting team |

| Seller Perception | Weak, often ignored | Strong, competitive positioning |

| Commitment Level | Informational only | Conditional loan commitment |

Working with a trusted Seattle mortgage broker who can deliver genuine pre-approval with underwriter review gives first time buyers credibility that matches cash offers in many situations.

Appraisal Gaps and Escalation Clauses

In markets where homes regularly sell above asking price, first time buyers face the challenge of appraisal gaps-when the appraised value comes in below the purchase price. Your lender will only finance based on the lower of the purchase price or appraised value.

Smart strategies include:

- Keeping reserves specifically for potential appraisal gaps

- Including appraisal gap coverage in your offer up to a specific amount

- Requesting comparable sales data before making offers

- Working with experienced real estate agents familiar with neighborhood values

First time buyers in hot neighborhoods like Capitol Hill, Fremont, and Queen Anne should budget an additional 5-10% beyond their offer price to cover potential gaps, inspection repairs, and closing cost variations.

Common Mistakes First Time Buyers Make

Learning from others' experiences helps you avoid costly missteps that can derail your home purchase or create long-term financial strain.

Overextending on Purchase Price

The single most common mistake involves buying more house than you can comfortably afford. Lenders qualify you based on debt-to-income ratios that reach 50% in some cases, but that doesn't mean you should use your entire approved amount.

Recommended affordability guidelines for first time buyers:

- Keep housing costs below 28% of gross monthly income

- Maintain total debt payments under 36% of gross income

- Reserve 1-2% of home value annually for maintenance

- Build 3-6 months emergency fund before closing

Remember that homeownership includes property taxes, insurance, HOA fees, utilities, and maintenance-costs that can add 30-50% to your monthly mortgage payment. Reviewing comprehensive tips for first-time home buyers helps you understand the full financial picture.

Neglecting the Inspection Process

In competitive markets, some first time buyers waive inspections to strengthen offers. This approach carries substantial risk, particularly with Seattle's older housing stock and potential issues like drainage problems from heavy rainfall.

Consider a pre-inspection strategy where you hire an inspector before making an offer, allowing you to submit a clean offer with confidence while maintaining informed decision-making. This approach works particularly well in Shoreline, Lake Forest Park, and Lynnwood where inventory levels allow slightly more deliberate timelines.

Ignoring Neighborhood Research and Future Needs

First time buyers often focus exclusively on the home itself while underestimating the importance of location. Schools, commute times, walkability, and neighborhood trajectory significantly impact both quality of life and future resale value.

Research considerations include:

- School district ratings and boundaries

- Proximity to employment centers

- Public transportation access

- Planned development and zoning changes

- Crime statistics and community engagement

- Retail, dining, and recreational amenities

For those considering areas like Mill Creek or Everett, understanding the Snohomish County market dynamics and growth patterns helps ensure your investment appreciates appropriately over time.

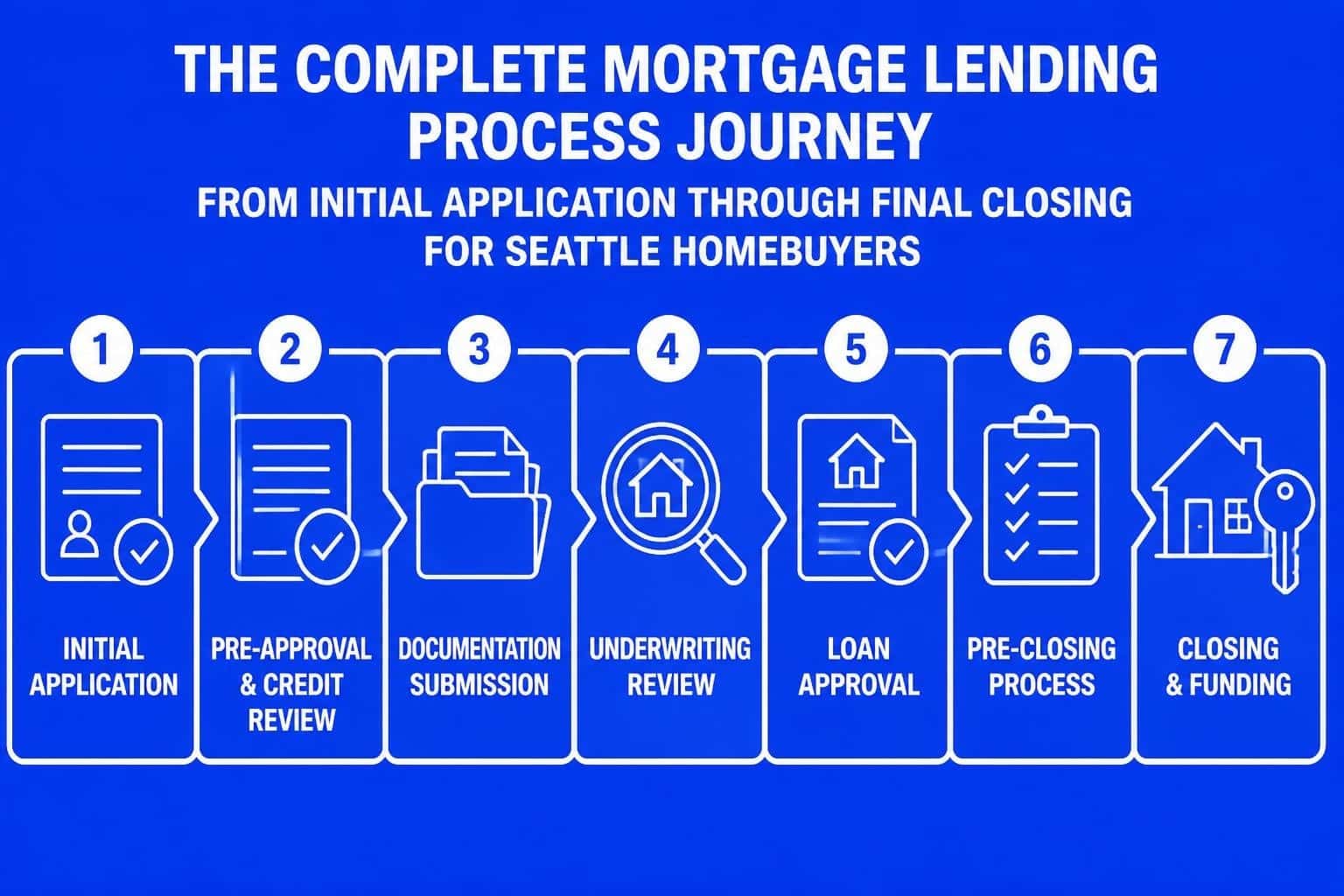

The Pre-Approval and Application Process

Understanding what happens from initial consultation through closing eliminates anxiety and helps you prepare appropriately for each stage of your home loan.

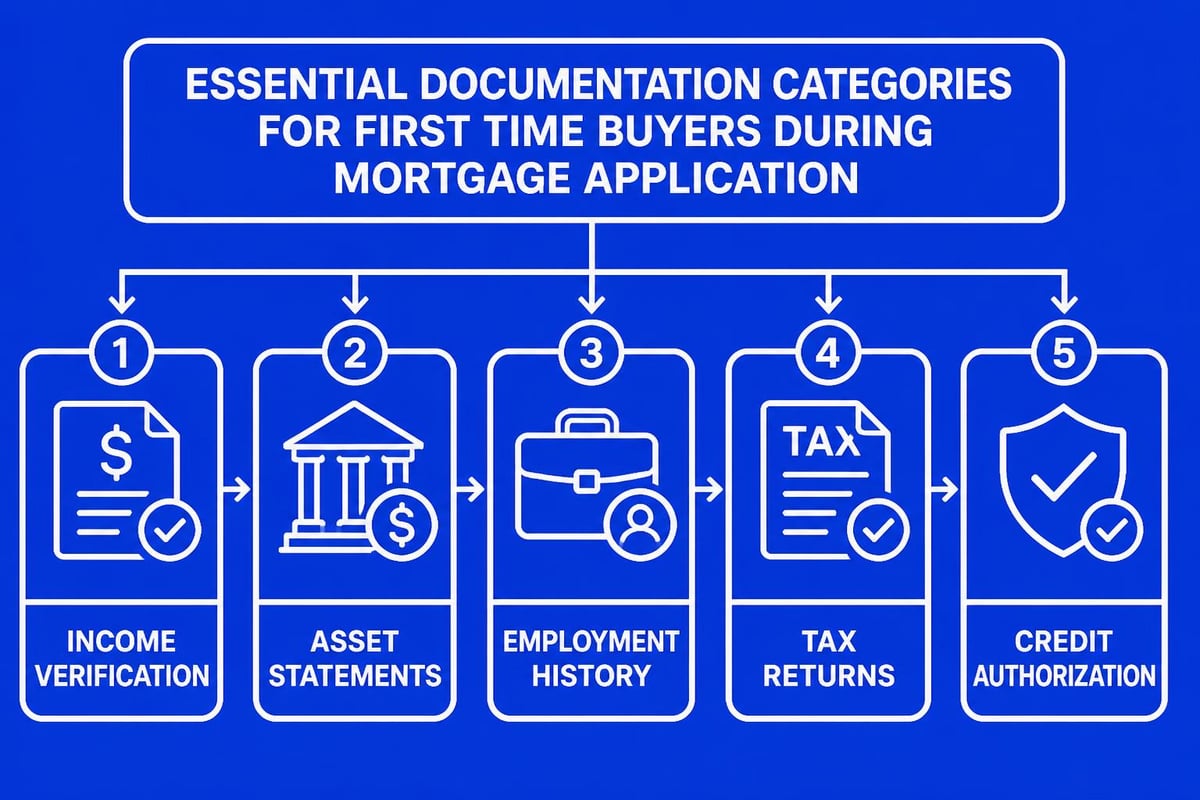

Documents You'll Need for Full Approval

First time buyers should gather comprehensive documentation before starting the mortgage process. Complete preparation accelerates approval timelines and prevents delays that could jeopardize your purchase contract.

Standard documentation requirements:

- Two years of W-2 forms and tax returns

- 60 days of bank statements for all accounts

- Recent paystubs covering one month

- Employment verification letters

- Explanation letters for any credit issues

- Gift letters if receiving down payment assistance

- Investment account statements showing vested RSUs

Tech professionals should also provide RSU vesting schedules, option grant documents, and detailed compensation statements. Proper documentation of these income sources separates experienced brokers from those unfamiliar with technology sector compensation structures.

Understanding Loan Estimates and Closing Disclosures

Within three business days of your application, lenders must provide a Loan Estimate detailing your interest rate, monthly payment, and closing costs. This standardized form allows comparison shopping between lenders.

The Closing Disclosure arrives at least three business days before closing and shows the final numbers. Review both documents carefully, comparing the Closing Disclosure against your Loan Estimate to identify any significant changes.

First time buyers working with experienced Seattle mortgage brokers benefit from detailed explanations of each fee, negotiation of lender charges where possible, and advocacy throughout the process to ensure fair treatment.

Rate Lock Strategies and Timing Decisions

Interest rates fluctuate daily based on economic indicators, Federal Reserve policy, and bond market movements. First time buyers must decide when to lock their rate and for how long.

When to Lock Your Interest Rate

Most brokers recommend locking once you have an accepted offer and clear closing timeline. Lock periods typically range from 15 to 60 days, with longer locks carrying slightly higher costs.

| Lock Period | Best For | Considerations |

|---|---|---|

| 15-day lock | Purchase contracts with quick close, usually cash-heavy deals | Very tight timeline, little buffer for delays |

| 30-day lock | Standard purchase contracts | Most common option, balances cost and timeline |

| 45-60 day lock | New construction, complex financing, or delayed closings | Higher cost but necessary protection for extended timelines |

In Seattle's market, where some closings can be expedited to 9 business days with proper preparation, experienced buyers often benefit from shorter locks that minimize costs while still providing rate protection.

Float-Down Options and Rate Improvement

Some lenders offer float-down provisions allowing you to capture lower rates if market conditions improve after locking. These options typically cost 0.125% to 0.25% of your loan amount and include specific restrictions on timing and rate improvement thresholds.

First time buyers should carefully evaluate whether float-down protection makes financial sense based on current rate trends, economic forecasts, and your specific timeline. Working through comprehensive home buying guides helps you understand market context for these decisions.

Post-Closing Considerations for New Homeowners

Your responsibilities as a homeowner begin the moment you receive your keys. First time buyers often underestimate the ongoing financial and maintenance commitments involved.

Building Your Home Maintenance Fund

Financial experts recommend saving 1-2% of your home's value annually for maintenance and repairs. For a $700,000 home in Seattle, that means setting aside $7,000 to $14,000 each year for:

- HVAC system servicing and eventual replacement

- Roof maintenance and repairs

- Plumbing and electrical updates

- Exterior painting and siding maintenance

- Appliance replacements

- Landscape care and drainage management

Create a separate savings account dedicated to home maintenance, automatically transferring funds monthly to ensure you're prepared when major systems need attention.

Understanding Property Tax Appeals

King County and Snohomish County assess property values annually, sometimes resulting in significant increases that impact your monthly payment if you escrow taxes. First time buyers have the right to appeal assessments they believe exceed fair market value.

The appeal process requires:

- Comparable sales data supporting a lower valuation

- Evidence of property condition issues affecting value

- Submission during the appeal window (typically April through July)

- Detailed documentation and sometimes professional appraisals

Successful appeals can reduce your annual property tax burden by hundreds or thousands of dollars, making the effort worthwhile when assessments seem unreasonable relative to market conditions.

Leveraging Professional Guidance Throughout Your Journey

First time buyers who attempt to navigate the home-buying process alone often encounter preventable problems, missed opportunities, and increased stress. Building the right professional team dramatically improves outcomes.

The Value of Experienced Mortgage Brokers

Working with brokers who specialize in first time buyers provides several advantages over retail bank loan officers. Brokers access multiple lending sources, compare programs across different institutions, and advocate for your interests throughout underwriting.

Quality brokers invest time in education, ensuring you understand your options, the implications of different loan structures, and strategies for building long-term wealth through homeownership. This educational approach particularly benefits those purchasing their first home in Seattle’s competitive market.

Coordinating with Real Estate Agents and Other Professionals

Your real estate agent, mortgage broker, escrow officer, and home inspector should work as a coordinated team. First time buyers benefit from professionals who communicate proactively, anticipate potential issues, and solve problems collaboratively.

Ask for referrals from your mortgage broker to real estate agents familiar with your target neighborhoods and price range. Agents who regularly work with first time buyers understand the additional education and patience required, making the experience smoother for everyone involved.

Exploring Specific Seattle-Area Neighborhoods

Different Seattle neighborhoods offer distinct advantages for first time buyers depending on priorities like commute distance, school quality, walkability, and lifestyle preferences.

Shoreline and Lake Forest Park Opportunities

These northern Seattle suburbs offer more affordable entry points compared to central Seattle while maintaining excellent schools and community amenities. The Shoreline School District consistently ranks among the region's best, making these areas attractive for families.

First time buyers can find condos and townhomes starting in the mid-$400,000s, with single-family homes ranging from $600,000 to over $1 million depending on size and location. The Lake Forest Park market offers slightly lower prices with a small-town feel and quick access to Seattle employment centers.

Everett and Lynnwood Value Propositions

For first time buyers willing to extend their commute, Everett and Lynnwood provide substantially lower entry prices while still offering convenient access to Seattle via I-5 or transit. These markets feature new construction opportunities, larger lots, and growing commercial development.

Average home prices run 20-30% below comparable properties in Seattle, Bellevue, or Redmond, making them attractive for buyers prioritizing space and value over proximity to urban amenities.

Successfully navigating your first home purchase in the Seattle area requires strategic planning, comprehensive financial preparation, and expert guidance through each stage of the process. From understanding loan programs and qualifying complex tech compensation to competing effectively in multiple-offer situations, first time buyers face numerous decisions that impact both immediate affordability and long-term financial success. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping first time buyers throughout Seattle, Bellevue, Redmond, and surrounding communities make confident financing decisions. With specialized expertise in tech compensation, access to diverse loan programs, and a proven track record of reliable execution, Keith helps you maximize buying power and secure the right home at the right price. Start your homeownership journey with a trusted partner who prioritizes education, transparency, and your long-term success-connect with Mortgage Reel today.