Securing a home purchase loan represents one of the most significant financial decisions you'll make in your lifetime. Whether you're a first-time buyer in Shoreline or a tech professional relocating to Bellevue, understanding how these loans work can mean the difference between a smooth transaction and costly delays. The Seattle metropolitan area's competitive housing market demands that buyers approach their financing strategically, armed with knowledge about loan options, qualification requirements, and the approval timeline. With median home prices exceeding $800,000 in many Seattle neighborhoods, choosing the right home purchase loan structure becomes even more critical for long-term financial success.

Understanding Home Purchase Loan Fundamentals

A home purchase loan is financing specifically designed to help buyers acquire residential property. Unlike refinance loans that replace existing mortgages, purchase loans create new debt secured by the property you're buying. Lenders evaluate your financial profile, the property's value, and market conditions to determine how much they'll lend and at what interest rate.

The anatomy of a home purchase loan includes several key components that directly impact your monthly payment and long-term costs. Principal represents the actual loan amount, while interest compensates the lender for risk and opportunity cost. Most borrowers also pay property taxes and homeowners insurance through their monthly payment, held in escrow by the lender.

Primary Loan Types Available to Seattle Buyers

Different loan programs serve different buyer profiles and property types. Understanding these distinctions helps you match your financial situation with the most advantageous financing.

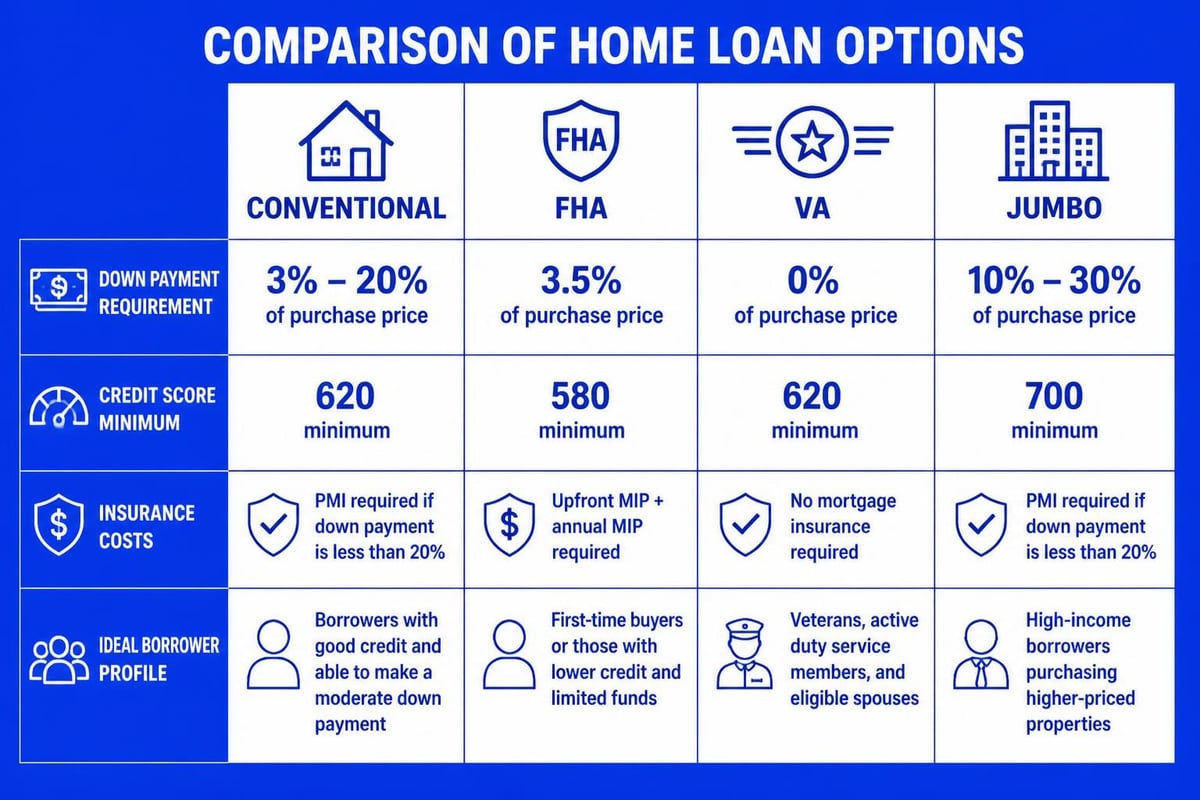

Conventional loans dominate the Seattle market, requiring as little as 3% down for qualified buyers. These loans follow guidelines set by Fannie Mae and Freddie Mac, with conforming limits reaching $1,149,825 in King County for 2026. They offer competitive rates and flexible terms, though borrowers with less than 20% down pay private mortgage insurance (PMI) until reaching sufficient equity. For buyers with strong credit and stable income, conventional loans offer predictable qualification standards and streamlined approval processes.

FHA loans provide accessible financing for buyers who may not qualify conventionally. With down payments as low as 3.5% and more flexible credit requirements, these government-backed loans help many first-time buyers enter the market. However, they require both upfront and ongoing mortgage insurance premiums, which can increase long-term costs compared to conventional financing.

VA loans offer incredible benefits for eligible military service members, veterans, and qualifying spouses. These loans require no down payment, no mortgage insurance, and typically feature lower interest rates than conventional options. In expensive markets like Seattle and Redmond, VA loans can be particularly powerful, though they do have funding fees that can be rolled into the loan amount.

| Loan Type | Minimum Down Payment | Credit Score Minimum | Mortgage Insurance | Best For |

|---|---|---|---|---|

| Conventional | 3% | 620 | Required if < 20% down | Strong credit, stable income |

| FHA | 3.5% | 580 | Always required | Lower credit scores, limited savings |

| VA | 0% | No set minimum | None | Eligible veterans and service members |

| Jumbo | 10-20% | 680-700 | Usually not required | High-value properties exceeding conforming limits |

Jumbo loans become necessary when your home purchase exceeds conforming loan limits. In Seattle's luxury neighborhoods like Medina or Madison Park, jumbo financing is common for properties above $1.15 million. These loans typically require larger down payments, stronger credit profiles, and more substantial cash reserves, but they enable purchases that conventional financing can't accommodate.

The Home Purchase Loan Approval Process

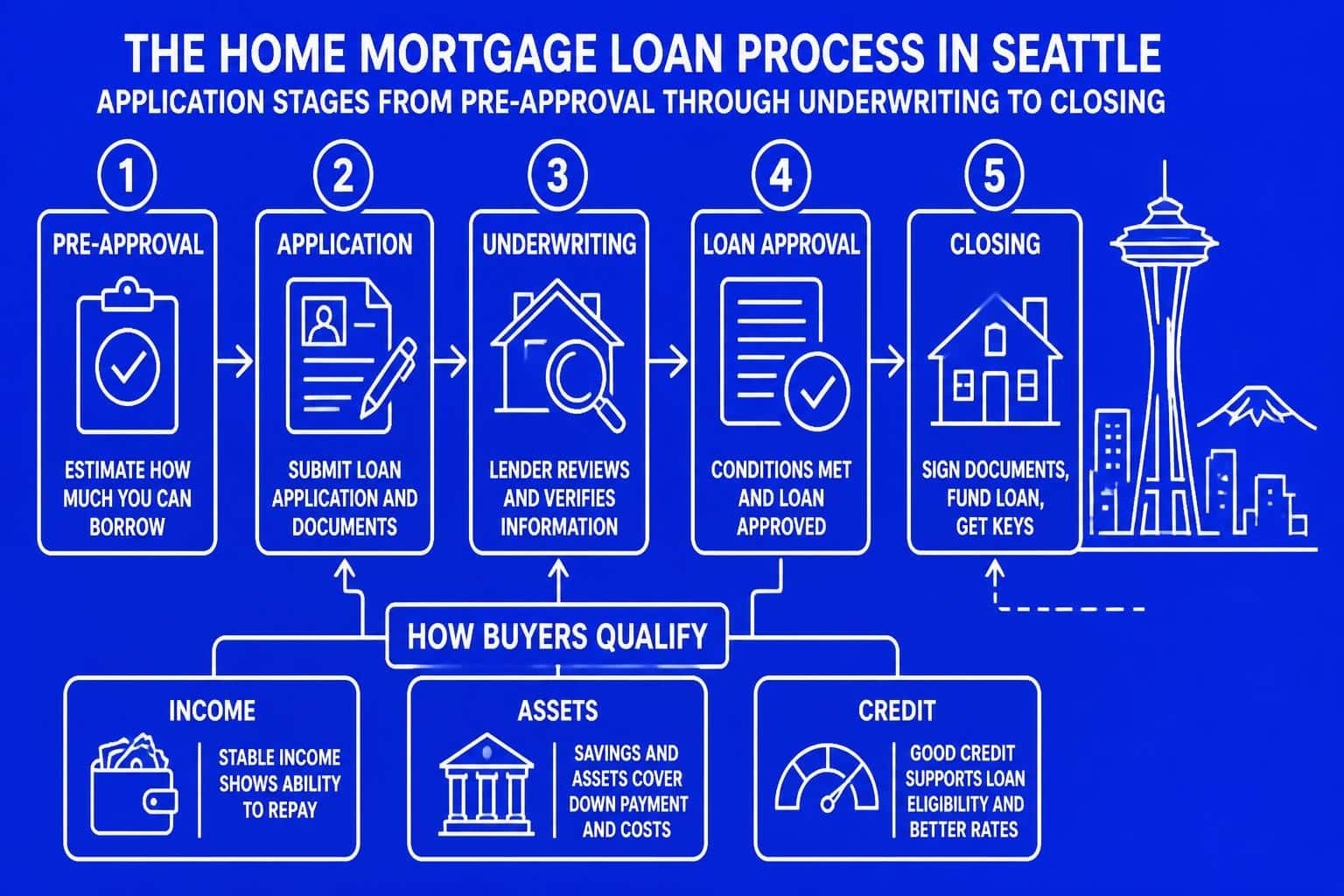

Getting approved for a home purchase loan involves multiple stages, each with specific requirements and timelines. Understanding this process helps you prepare documentation, set realistic expectations, and avoid surprises that could derail your purchase.

Pre-Qualification and Pre-Approval

The journey begins with pre-qualification, an informal estimate of how much you might borrow based on basic financial information you provide. While helpful for initial planning, pre-qualification letters carry limited weight with sellers in competitive markets like Kirkland or Lake Forest Park.

Pre-approval represents a significantly stronger position. During pre-approval, lenders verify your income, assets, credit, and employment through documentation review. They run your credit report, analyze tax returns, and validate bank statements. In Seattle's fast-paced market, sellers often won't seriously consider offers without pre-approval letters from reputable lenders.

Pre-approval typically remains valid for 60-90 days, though credit scores are re-pulled before closing. For tech professionals with complex compensation including RSUs and stock options, working with a broker who understands how to qualify this income becomes essential. Many mortgage brokers in Seattle specialize in technology sector compensation, ensuring you maximize your borrowing power.

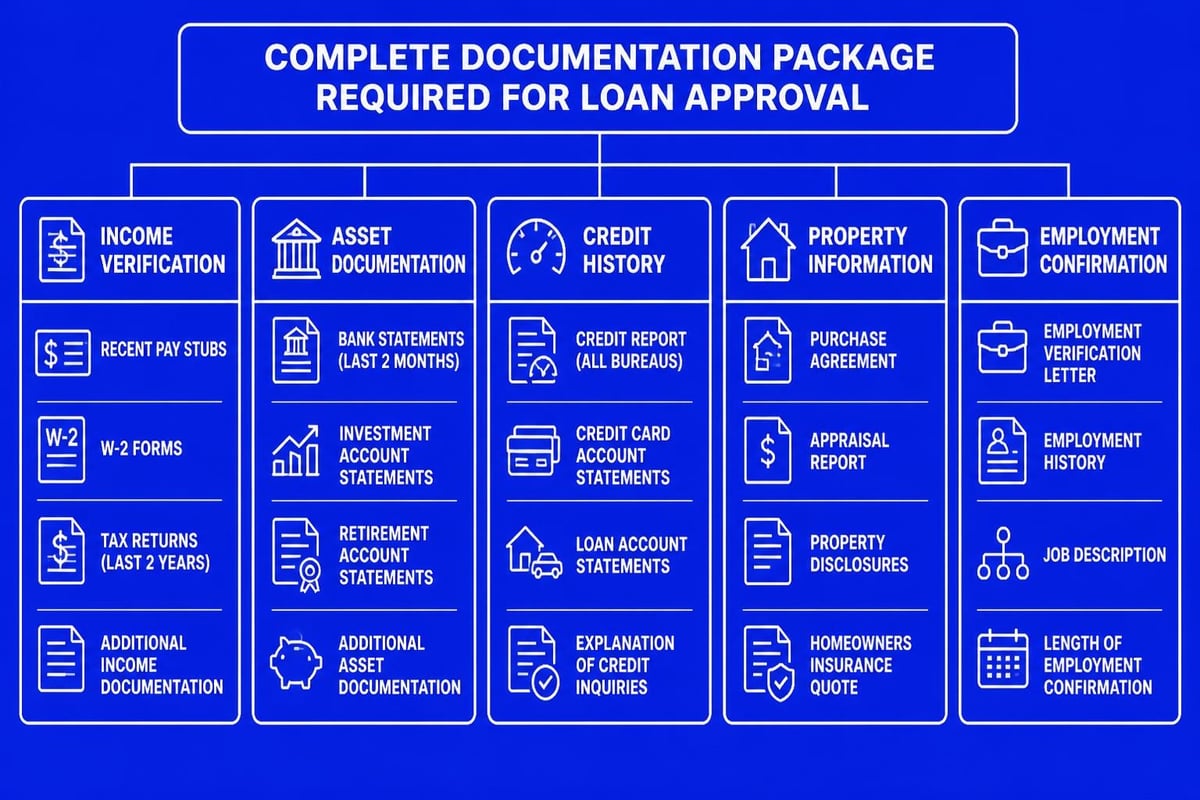

Documentation Requirements

Lenders require comprehensive documentation to verify your financial profile and reduce their risk. Standard requirements include:

- Two years of W-2s demonstrating employment history and income stability

- Recent pay stubs (typically 30 days) showing current earnings

- Two months of bank statements for all accounts used for down payment and reserves

- Tax returns (often two years) particularly for self-employed buyers or those with investment income

- Explanation letters for any credit issues, employment gaps, or large deposits

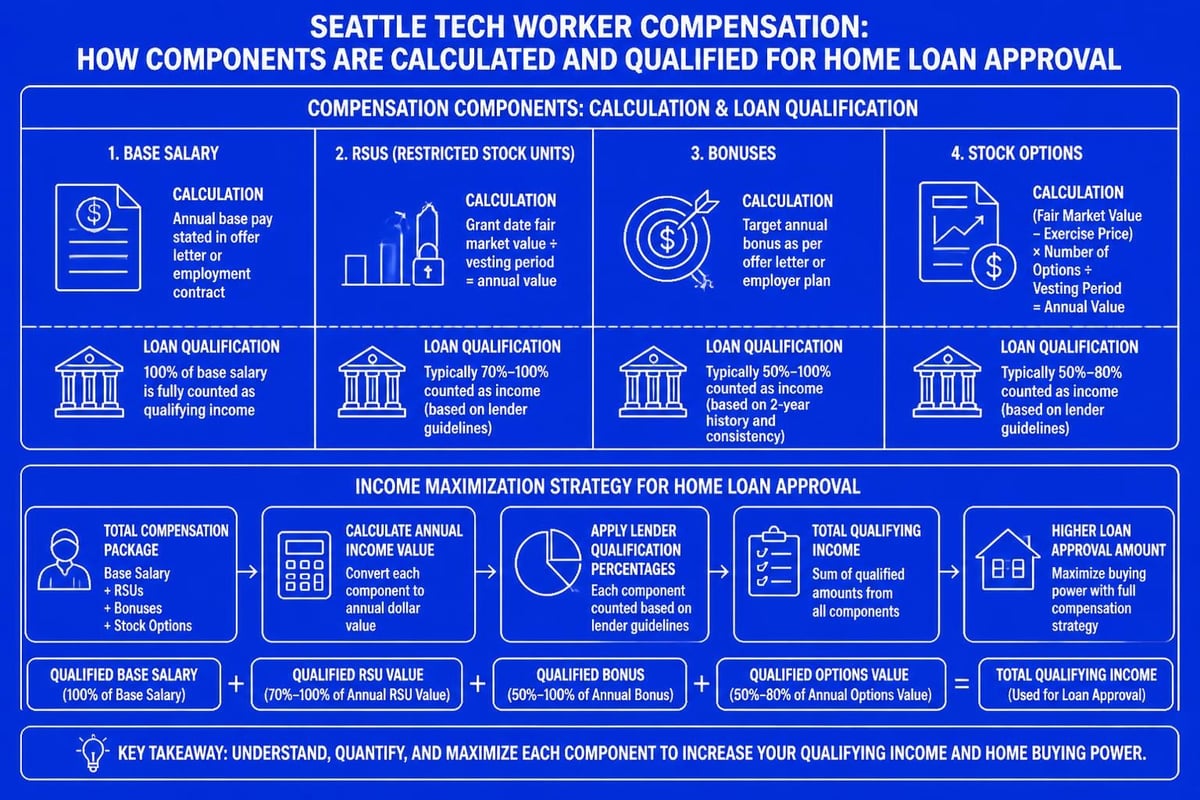

For Seattle tech workers receiving stock compensation, additional documentation proves essential. RSU vesting schedules, stock option agreements, and historical grant patterns help lenders establish qualifying income. Some lenders average stock compensation over two years, while others use more conservative calculations, significantly impacting your approved loan amount.

Calculating Your Home Purchase Loan Capacity

Determining how much home you can afford involves more than just your income. Lenders evaluate your complete financial picture through specific ratios and requirements designed to ensure you can sustain the mortgage long-term.

Debt-to-Income Ratio Standards

Your debt-to-income ratio (DTI) compares your monthly debt obligations to your gross monthly income. Lenders calculate two DTI figures:

- Front-end ratio divides your proposed housing payment by gross monthly income

- Back-end ratio includes all monthly debt (housing, car loans, credit cards, student loans) divided by gross income

Conventional loans typically allow back-end DTI up to 45-50%, though some programs permit higher ratios with compensating factors like substantial cash reserves or excellent credit. FHA loans may allow DTI approaching 56.99% in certain scenarios, particularly valuable for buyers with student debt or other obligations.

For a household earning $200,000 annually in Everett, lenders would generally cap total monthly debt around $7,500-8,300, depending on the specific loan program and credit profile. If you already have $1,500 in monthly debt payments, your maximum housing payment would range from $6,000-6,800.

Down Payment and Reserve Requirements

Every home purchase loan requires some combination of down payment and cash reserves, though amounts vary significantly by loan type.

- Conventional loans: 3-20% down, with 2-6 months reserves often required

- FHA loans: 3.5% down, minimal reserve requirements

- VA loans: 0% down for eligible borrowers

- Jumbo loans: 10-20% down, 6-12 months reserves typically required

Down payment sources must be documented and verified. Acceptable sources include:

- Personal savings demonstrated through bank statements

- Gift funds from immediate family members with proper documentation

- Retirement account withdrawals (subject to tax implications)

- Sale proceeds from existing property

- Employer assistance programs (common at Seattle tech companies)

Larger down payments reduce your loan amount, eliminate or reduce mortgage insurance costs, and often secure better interest rates. However, maintaining liquidity for reserves, moving costs, and furnishings should also factor into your down payment decision.

Navigating Property Appraisal and Underwriting

Once you've found a property and have an accepted offer, your home purchase loan enters the underwriting phase where lenders verify all information and ensure the property meets their standards.

The Appraisal Process

Lenders order appraisals to confirm the property's value supports the loan amount. An independent appraiser inspects the home, evaluates its condition, and compares it to recent sales of similar properties in the area. Understanding how home appraisals work helps you prepare for potential valuation issues that could affect your financing.

In Seattle's competitive market, appraisal gaps occasionally occur when the appraised value comes in below the purchase price. This creates several scenarios:

- You increase your down payment to cover the gap

- The seller reduces the purchase price

- You negotiate a compromise splitting the difference

- The deal falls through if neither party can accommodate the gap

Tech professionals with substantial stock compensation often have flexibility to increase down payments if appraisal gaps arise, providing a competitive advantage in multiple-offer situations.

Underwriting Timeline and Conditions

Underwriters review every aspect of your loan file, verifying information and identifying any issues requiring resolution. This process typically takes 7-15 days but can extend longer with complex income structures or property issues.

Initial underwriting produces a conditional approval listing items required before final clearance. Common conditions include:

- Updated pay stubs closer to closing

- Explanation for recent credit inquiries

- Insurance binder for the property

- HOA documentation for condominiums

- Title work clearing any liens or ownership issues

Final underwriting occurs after all conditions are satisfied. The underwriter issues a "clear to close," signaling the loan is approved and ready for funding. For buyers needing rapid closings in competitive Seattle neighborhoods, working with lenders offering expedited underwriting can provide significant advantages.

Strategic Considerations for Seattle Market Success

The Greater Seattle housing market presents unique challenges that require strategic thinking about your home purchase loan approach. Understanding these dynamics helps you structure financing that supports your offer competitiveness while maintaining financial prudence.

Rate Lock Timing and Strategy

Interest rates fluctuate daily based on economic conditions, Federal Reserve policy, and bond market activity. When you lock your rate determines your actual borrowing cost, making timing a critical strategic decision.

Rate locks guarantee a specific interest rate for a defined period, typically 30-60 days. In volatile rate environments, locking early provides certainty but removes the possibility of benefiting from rate decreases. Conversely, floating your rate maintains flexibility but exposes you to potential increases.

Consider these rate lock strategies:

- Lock immediately when rates are rising or if you've found your rate floor

- Float with a lock option allowing you to secure rates if they spike

- Short-term lock for fast closings, often with slightly better pricing

- Extended lock when building new construction with delayed closing dates

Leveraging Technology Sector Compensation

Seattle's concentration of major tech employers creates unique opportunities for home purchase loan qualification. Many lenders undercalculate or entirely exclude valuable compensation components, artificially limiting buying power.

RSUs (Restricted Stock Units) typically vest over several years following grants. Forward-thinking lenders average historical vesting amounts over two years, treating this income as stable and recurring. Conservative lenders may exclude unvested RSUs entirely or apply significant discounts.

Stock options require even more nuanced analysis. The spread between strike price and current value, combined with vesting schedules and exercise timelines, determines qualifying income. Lenders experienced with technology compensation can often qualify substantially more income than conventional approaches.

Bonuses and commissions gain full qualification when you can demonstrate two-year history and likelihood of continuance. Many Amazon, Microsoft, and Google employees significantly underestimate their qualifying income by working with lenders unfamiliar with tech compensation structures.

Common Challenges and Solutions

Even well-prepared buyers encounter obstacles during the home purchase loan process. Anticipating common challenges and knowing solutions keeps your transaction moving forward.

Credit Score Optimization

Your credit score directly impacts both loan approval and interest rate. For home purchase loans in 2026, scoring thresholds include:

| Credit Score Range | Loan Options | Typical Impact |

|---|---|---|

| 760+ | All programs, best rates | Optimal pricing |

| 700-759 | All programs, good rates | Slight rate increase |

| 640-699 | Most programs, higher rates | Moderate rate increase |

| 580-639 | FHA, some conventional | Significant rate increase |

| Below 580 | Very limited options | Challenging to qualify |

Improving credit before applying for your home purchase loan can save thousands over the loan's life. Focus on:

- Paying down credit card balances below 30% utilization

- Correcting any errors on credit reports

- Avoiding new credit applications during the home buying process

- Maintaining on-time payment history across all accounts

Employment and Income Verification Issues

Lenders require stable, verifiable income to approve home purchase loans. Complications arise when:

- You've recently changed jobs, particularly if switching industries or moving from W-2 to contract work

- Income varies significantly year to year without clear upward trend

- You're self-employed requiring two years of tax returns and business stability documentation

- Your employment is contract-based, requiring proof of ongoing work availability

For buyers in Lynnwood or Mill Creek planning job transitions, timing your purchase relative to employment changes can prevent qualification issues. Generally, completing your home purchase before changing jobs simplifies approval, though changing to higher-paying positions with similar responsibilities can work with proper documentation.

Timeline and Closing Preparation

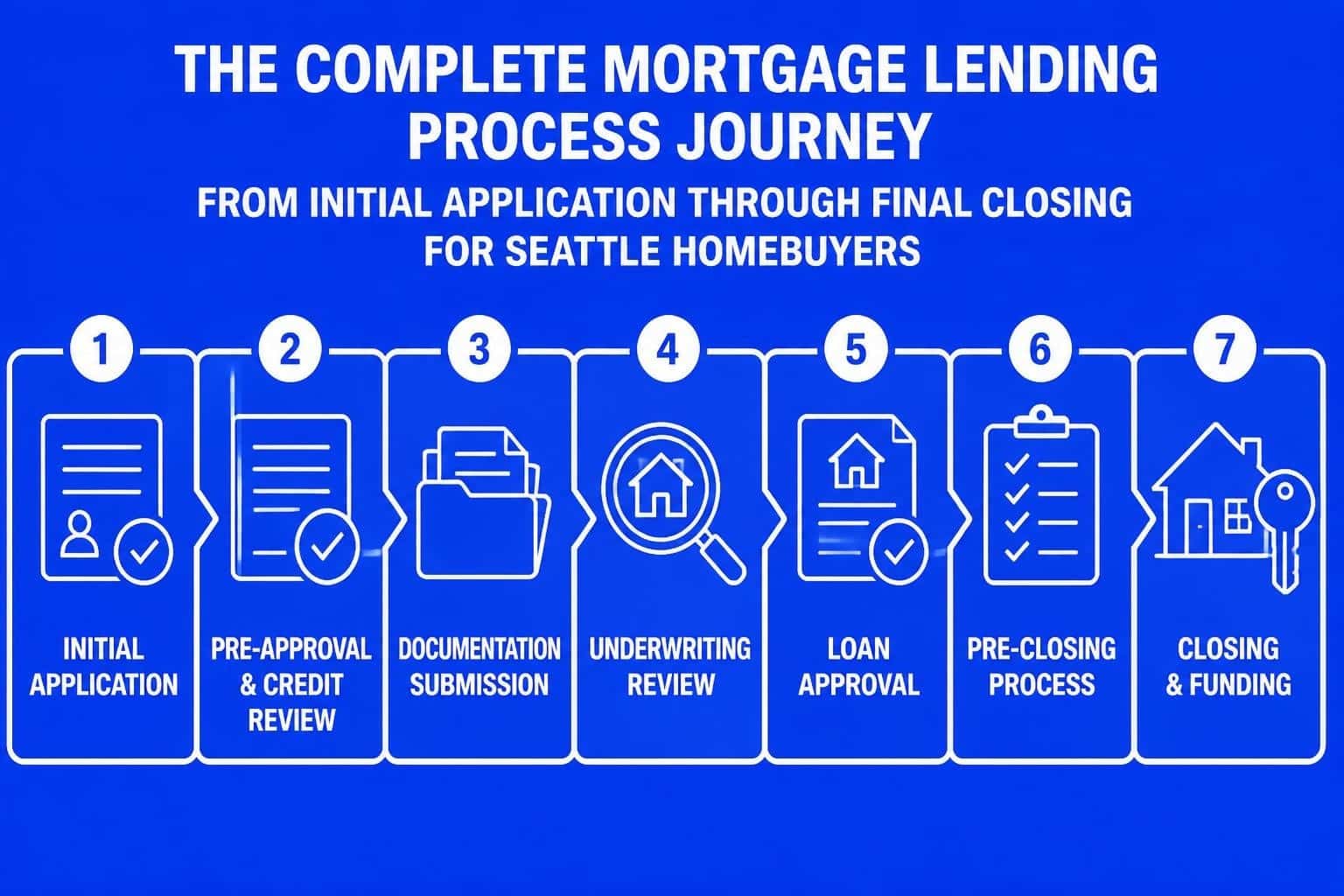

Understanding the complete home buying and mortgage loan process timeline helps you coordinate all parties and meet critical deadlines. From accepted offer to closing typically requires 30-45 days, though experienced lenders can compress this timeline significantly when needed.

Key Milestones in the Loan Process

The home purchase loan journey follows a predictable sequence:

Days 1-3: Loan application submitted, initial disclosures provided, and appraisal ordered. You'll receive a Loan Estimate detailing all costs, rates, and terms within three business days of application.

Days 4-10: Appraisal conducted and documentation submitted to underwriting. This period involves gathering any additional paperwork requested by your loan officer.

Days 11-20: Initial underwriting review completed, conditional approval issued, and conditions addressed. Quick response to underwriter requests keeps your timeline on track.

Days 21-28: Final underwriting, title work completed, and closing disclosure prepared. You'll receive the Closing Disclosure at least three business days before closing, detailing final numbers.

Days 29-30: Final walkthrough, closing appointment, and funding. After signing, the transaction funds and you receive keys to your new home.

Lenders with advanced technology and streamlined processes can compress this timeline substantially. In competitive Seattle neighborhoods where sellers prefer quick closings, demonstrating you can close in 15-20 days provides significant negotiating leverage.

Preparing for Closing Day

The final steps before closing require attention to several details:

- Wire transfer arrangements for your down payment and closing costs

- Homeowners insurance binder proving coverage effective at closing

- Final walkthrough confirming the property condition matches your agreement

- Closing disclosure review verifying all numbers match your expectations

- Valid identification (typically driver's license or passport)

Bring a cashier's check for any amounts not wired and be prepared to sign numerous documents during your closing appointment. Your lender provides a closing checklist outlining exactly what you need to bring and what to expect during the signing.

Cost Analysis Beyond the Purchase Price

Your home purchase loan creates both immediate and ongoing costs that extend well beyond the property's price. Understanding total ownership costs prevents budget surprises and supports sustainable homeownership.

Upfront Closing Costs

Closing costs typically range from 2-5% of the purchase price, including:

- Origination fees charged by your lender for processing the loan

- Appraisal fees covering property valuation ($600-1,000 in Seattle)

- Title insurance protecting against ownership defects

- Escrow fees for third-party transaction management

- Recording fees paid to county offices for deed registration

- Prepaid items including initial property tax and insurance escrow deposits

For a $750,000 home purchase in Seattle, expect closing costs between $15,000-37,500. Some costs are negotiable with sellers, particularly in buyer-friendly markets, while others remain fixed regardless of negotiation.

Ongoing Monthly Obligations

Your monthly housing payment includes several components beyond principal and interest:

- Property taxes (approximately 1% of assessed value annually in King County)

- Homeowners insurance ($1,200-2,500 annually for typical Seattle homes)

- HOA fees if purchasing a condominium or townhome

- Mortgage insurance if required by your loan type

- Maintenance reserves (recommended 1% of home value annually)

A $750,000 purchase with 10% down and a 6.5% interest rate creates approximately:

- Principal and interest: $4,270

- Property taxes: $625

- Insurance: $150

- PMI (if applicable): $280

- Total monthly payment: $5,325

These numbers vary based on your specific situation, but understanding complete costs prevents budget strain after closing.

Maximizing Long-Term Value

Your home purchase loan structure impacts not just immediate affordability but long-term wealth building. Strategic decisions during loan selection create financial advantages that compound over decades.

Term Selection Considerations

While 30-year mortgages dominate the market, alternative terms offer different advantages:

15-year mortgages build equity rapidly and save substantial interest over the loan life but require significantly higher monthly payments. These work well for high-income buyers who prioritize rapid equity building over monthly payment minimization.

Adjustable-rate mortgages (ARMs) offer lower initial rates that adjust after a fixed period. Common structures include 5/1, 7/1, and 10/1 ARMs. These benefit buyers planning to sell or refinance before adjustment periods, particularly in Seattle's mobile tech workforce.

Refinance Opportunities

Your home purchase loan need not remain permanent. Many buyers refinance within 3-5 years to:

- Secure lower interest rates as market conditions change

- Remove mortgage insurance after reaching 20% equity

- Convert from adjustable to fixed-rate financing

- Access home equity for renovations or other investments

- Shorten loan terms to build equity faster

Keeping good credit, maintaining employment stability, and tracking rate environments positions you to capitalize on refinance opportunities when they arise. Working with experienced mortgage professionals who proactively monitor refinance opportunities ensures you don't miss beneficial timing.

Successfully securing a home purchase loan requires understanding program options, preparing comprehensive documentation, and navigating approval processes strategically. Whether you're buying your first home in Lake Forest Park or upgrading to a luxury property in Bellevue, the right financing structure and professional guidance make all the difference. Keith Akada at Mortgage Reel brings 25+ years of experience helping Seattle-area buyers navigate complex loan scenarios, from qualifying technology sector compensation to closing transactions in as few as 9 business days. With 750+ five-star reviews and deep expertise in the Greater Seattle market, Keith provides the education, transparency, and execution you need to purchase with confidence.