Securing a home mortgage loan represents one of the most significant financial decisions you'll make, particularly in competitive markets like Seattle, Bellevue, and Redmond. Whether you're a first-time buyer exploring neighborhoods in Shoreline or a tech professional at Microsoft looking to purchase in Kirkland, understanding the fundamentals of mortgage financing empowers you to make confident decisions. With mortgage rates fluctuating and lending guidelines evolving, working with an experienced broker who understands local market dynamics and diverse income structures-including stock compensation-can make the difference between securing your dream home and missing out in multiple-offer situations.

Understanding Home Mortgage Loan Fundamentals

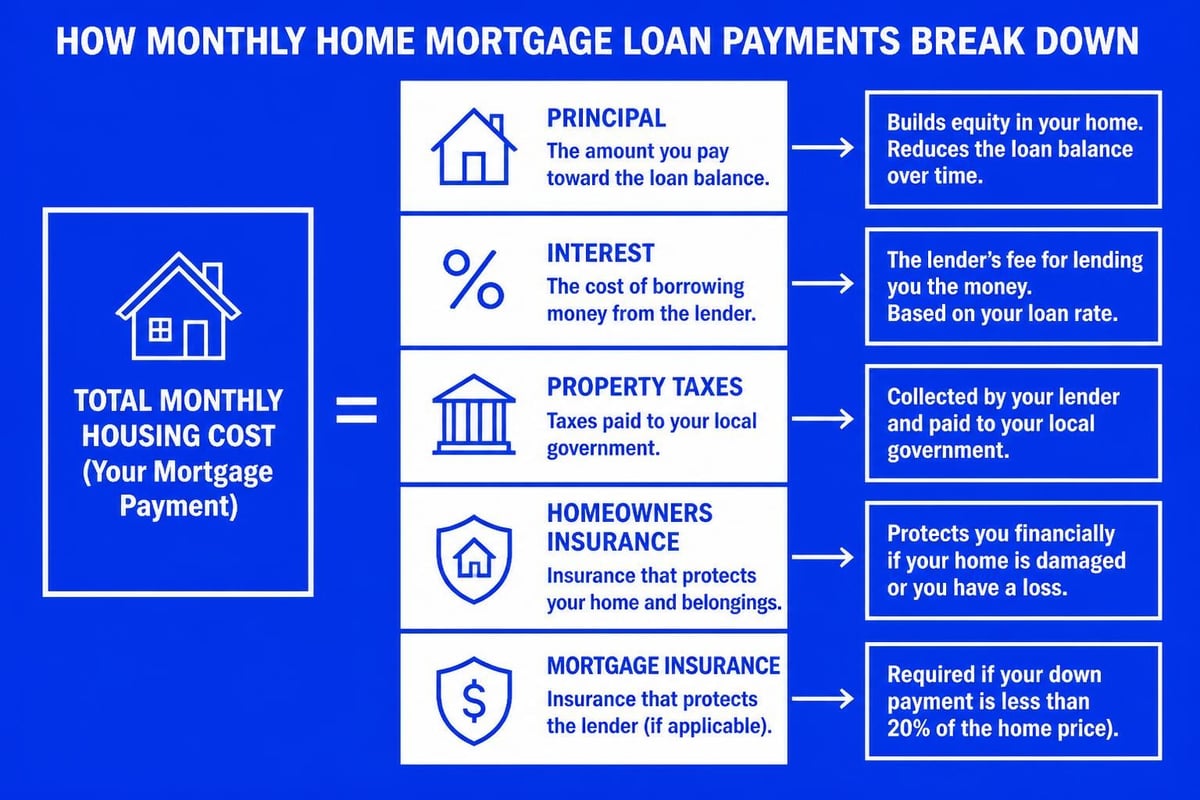

A home mortgage loan is a secured loan that allows you to purchase real estate by borrowing money from a lender, with the property itself serving as collateral. This arrangement enables homebuyers to acquire property without paying the full purchase price upfront, instead making monthly payments over a predetermined period, typically 15 to 30 years.

The mortgage structure includes several key components that directly impact your monthly payment and long-term costs. Principal refers to the amount you borrow, while interest represents the cost of borrowing that money. Your monthly payment also includes property taxes and homeowners insurance, often collected in an escrow account managed by your lender or servicer.

Key Mortgage Components Explained

Understanding how these elements work together helps you evaluate loan offers effectively:

- Down payment: The upfront cash you contribute, typically ranging from 3% to 20% or more

- Loan-to-value ratio (LTV): The percentage of the home's value you're financing

- Private mortgage insurance (PMI): Required on conventional loans with less than 20% down

- Annual percentage rate (APR): The true cost of borrowing, including interest and fees

- Closing costs: Various fees paid at closing, typically 2% to 5% of the loan amount

For Seattle-area buyers, especially those purchasing in higher-priced markets like Bellevue or Redmond, understanding these components becomes critical when comparing loan options from different lenders. A slightly lower interest rate might seem attractive, but higher fees could make that loan more expensive over time.

Types of Home Mortgage Loans Available

Selecting the right mortgage product depends on your financial situation, down payment capacity, and long-term homeownership goals. The mortgage industry offers several distinct loan types, each with specific qualification requirements and benefits.

Conventional Loans

Conventional loans represent the most common financing option and are not backed by government agencies. These loans typically require credit scores of 620 or higher, though stronger credit profiles (740+) secure the best rates.

Benefits of conventional financing:

- Competitive interest rates for qualified borrowers

- Flexibility in property types and loan amounts

- PMI can be removed once you reach 20% equity

- Available for primary residences, second homes, and investment properties

For those wondering about conventional loan down payment requirements, qualified buyers can secure financing with as little as 3% down, though 5% to 20% down payments are more common in competitive Seattle markets.

FHA Loans

Federal Housing Administration (FHA) loans serve buyers who may not qualify for conventional financing due to lower credit scores or limited down payment funds. These government-backed loans require as little as 3.5% down for borrowers with credit scores of 580 or higher.

FHA loans charge both upfront and annual mortgage insurance premiums, which remain for the life of the loan if you put down less than 10%. For Seattle first-time buyers exploring neighborhoods in Lake Forest Park or Lynnwood, FHA financing can provide an accessible path to homeownership.

VA Loans

Veterans, active-duty service members, and eligible spouses can access VA loans, which offer exceptional benefits including zero down payment requirements and no PMI. These loans, backed by the Department of Veterans Affairs, typically feature competitive interest rates and more flexible credit guidelines.

USDA Loans

For buyers considering properties in qualifying rural and suburban areas, USDA loans offer 100% financing with no down payment required. While Seattle proper doesn't qualify, some areas in Snohomish County and beyond may be eligible under this program.

Jumbo Loans

When purchasing homes exceeding conforming loan limits ($806,500 for single-family homes in King County in 2026), you'll need a jumbo loan. These non-conforming loans typically require larger down payments (10% to 20%), excellent credit (700+), and substantial reserves.

For tech professionals with significant stock compensation at Amazon, Google, or Microsoft, jumbo financing enables purchases in premium Seattle neighborhoods. Specialized underwriting can qualify RSUs, stock options, and bonus income to maximize buying power.

| Loan Type | Min. Down Payment | Credit Score | Mortgage Insurance | Best For |

|---|---|---|---|---|

| Conventional | 3% – 20% | 620+ | PMI if <20% down | Strong credit, stable income |

| FHA | 3.5% | 580+ | Required (MIP) | Lower credit, smaller down payment |

| VA | 0% | No minimum* | None | Veterans and military |

| USDA | 0% | 640+ | Annual fee | Rural/suburban areas |

| Jumbo | 10% – 20% | 700+ | Varies by lender | High-balance purchases |

*VA loans don't have minimum credit requirements, but most lenders require 580-620.

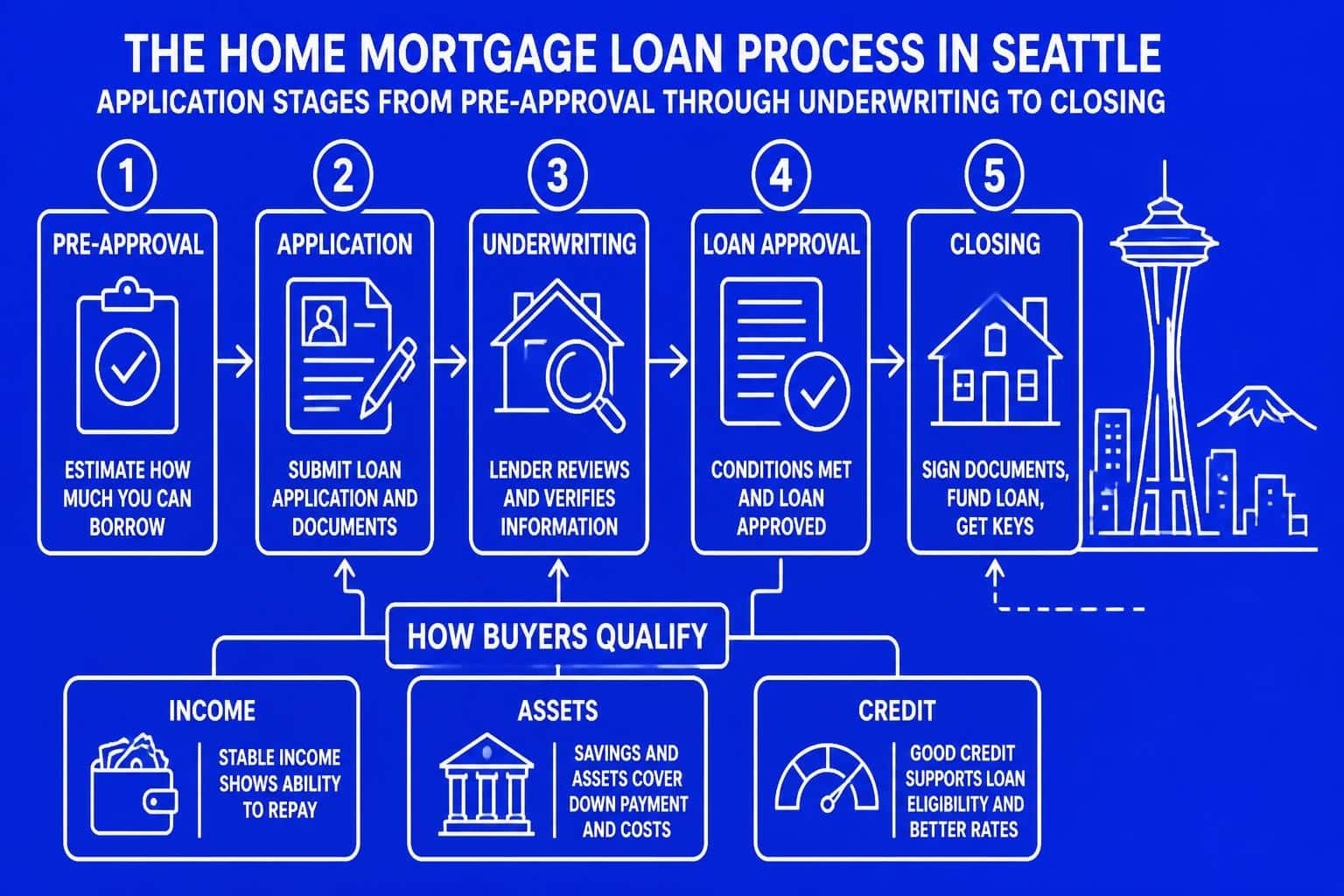

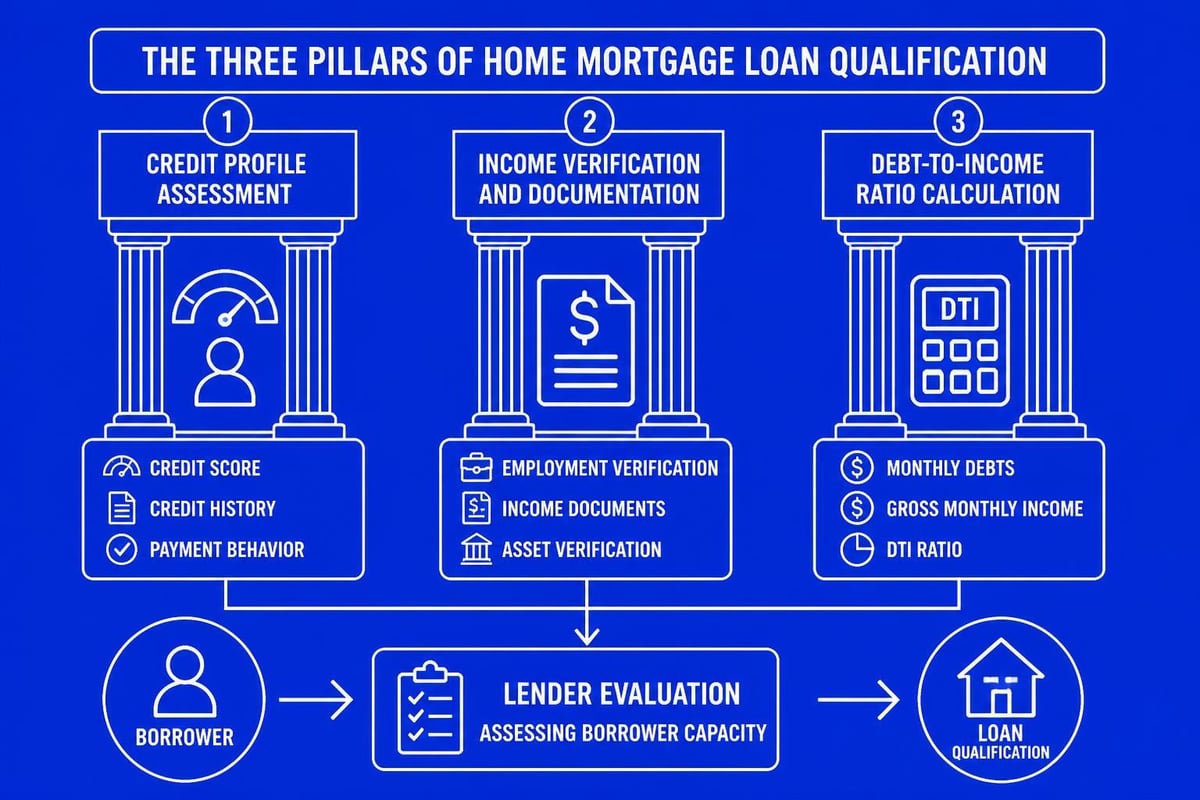

Qualifying for a Home Mortgage Loan

Lenders evaluate your ability to repay a home mortgage loan through a comprehensive review of your financial profile. Understanding these qualification factors helps you prepare effectively and identify potential issues before applying.

The Three Pillars of Mortgage Qualification

Credit History and Scores: Your credit score influences both loan approval and interest rate. Lenders review your payment history, credit utilization, length of credit history, and recent credit inquiries. For conventional loans, scores above 740 typically secure the best rates, while FHA loans accommodate scores as low as 580.

Income and Employment Verification: Lenders verify stable, sufficient income to support your mortgage payment. W-2 employees typically provide two years of tax returns, recent pay stubs, and employment verification. For Seattle tech workers with stock compensation, specialized documentation of RSUs, options, and bonuses can significantly increase qualifying income.

Debt-to-Income Ratios: Lenders calculate two critical ratios:

- Front-end ratio: Monthly housing payment divided by gross monthly income (typically max 28%)

- Back-end ratio: Total monthly debt payments divided by gross monthly income (typically max 43% for conventional, up to 50% for FHA)

Documentation Requirements

Organizing your documentation streamlines the approval process. Standard requirements include:

- Two years of federal tax returns (personal and business if self-employed)

- Two recent pay stubs showing year-to-date earnings

- Two months of bank statements for all accounts

- Documentation of additional income sources (bonuses, commissions, rental income)

- Explanation letters for credit issues, employment gaps, or large deposits

- Documentation of stock compensation for tech professionals

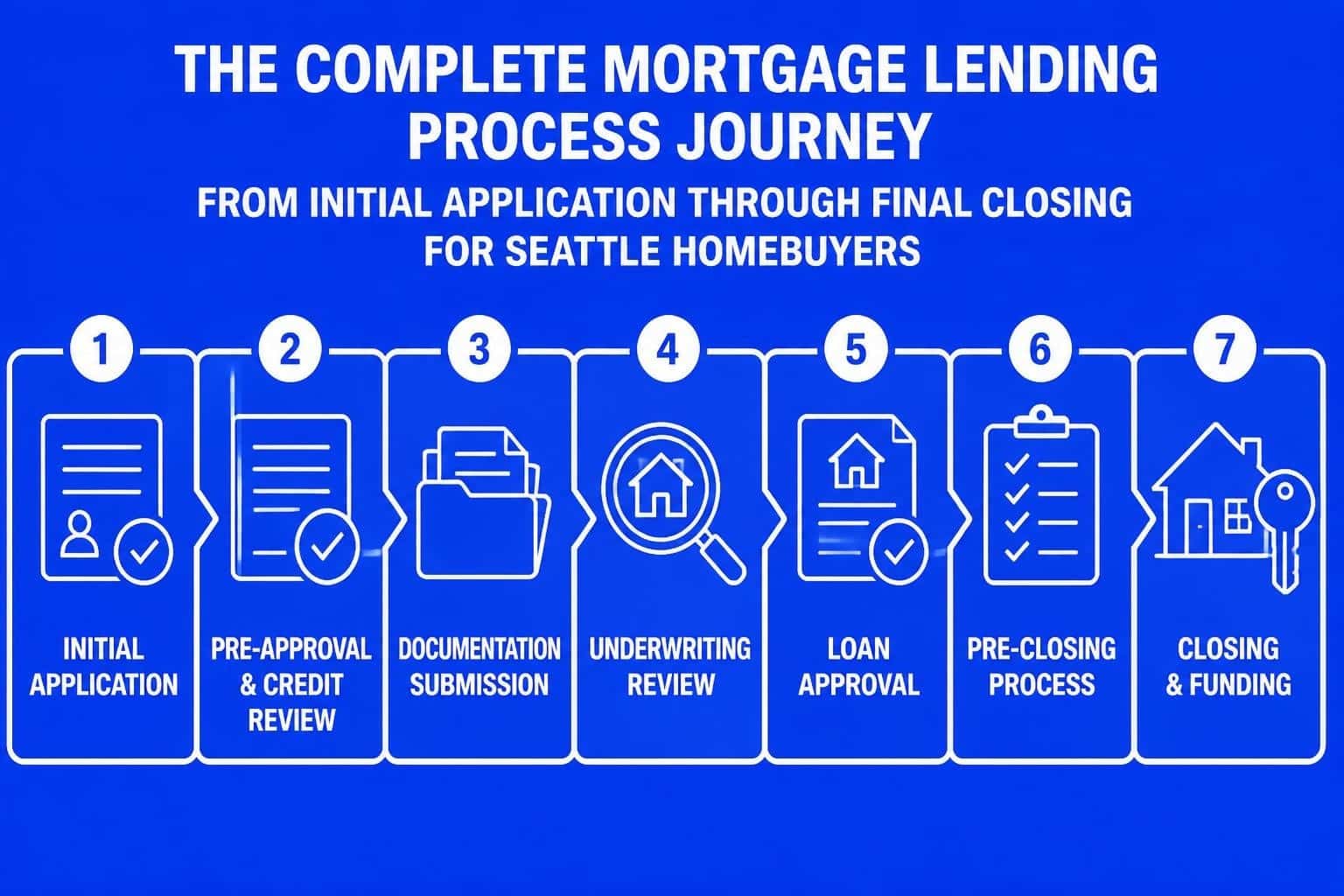

The mortgage lending process typically takes 30 to 45 days, though experienced brokers with direct underwriting access can close qualified transactions in as few as 9 business days-critical in competitive Seattle markets with multiple offers.

Strategic Considerations for Seattle-Area Buyers

Seattle's unique housing market presents specific challenges and opportunities that influence your home mortgage loan strategy. With median home prices significantly above national averages and inventory constraints creating competitive bidding situations, preparation and strategy matter.

Market-Specific Factors

Property values in greater Seattle: Home prices vary significantly across the region. While Seattle proper commands premium prices, neighboring areas like Shoreline, Mill Creek, and Everett offer relative affordability. Understanding these variations helps you align your budget with realistic options.

Competitive offer situations: Multiple offers remain common in desirable neighborhoods. Pre-approval from a reputable broker signals serious intent and financial capability to sellers. Strong pre-approvals can differentiate your offer when competing against cash buyers or other financed offers.

Down Payment Strategies

While 20% down payments eliminate PMI on conventional loans, many Seattle buyers successfully purchase with less. Consider these approaches:

- 3% to 5% down conventional loans: Access homeownership sooner while building equity

- 10% to 15% down: Balance lower monthly PMI with preserved liquidity for reserves

- 20% or more: Eliminate PMI and secure better rates, but ensure adequate reserves remain

For first-time buyers, exploring available programs and assistance can provide down payment support and favorable terms.

Leveraging Stock Compensation

Tech employees represent a significant portion of Seattle-area homebuyers. Traditional underwriting often underutilizes stock compensation, but experienced brokers can maximize buying power by:

- Qualifying vested RSUs at current market value with appropriate discounts

- Including documented bonus history to increase qualifying income

- Structuring asset-based qualification when income fluctuates

- Coordinating vesting schedules with purchase timing for optimal qualification

This specialized approach helps tech professionals access jumbo financing that matches their true earning capacity, not just base salary.

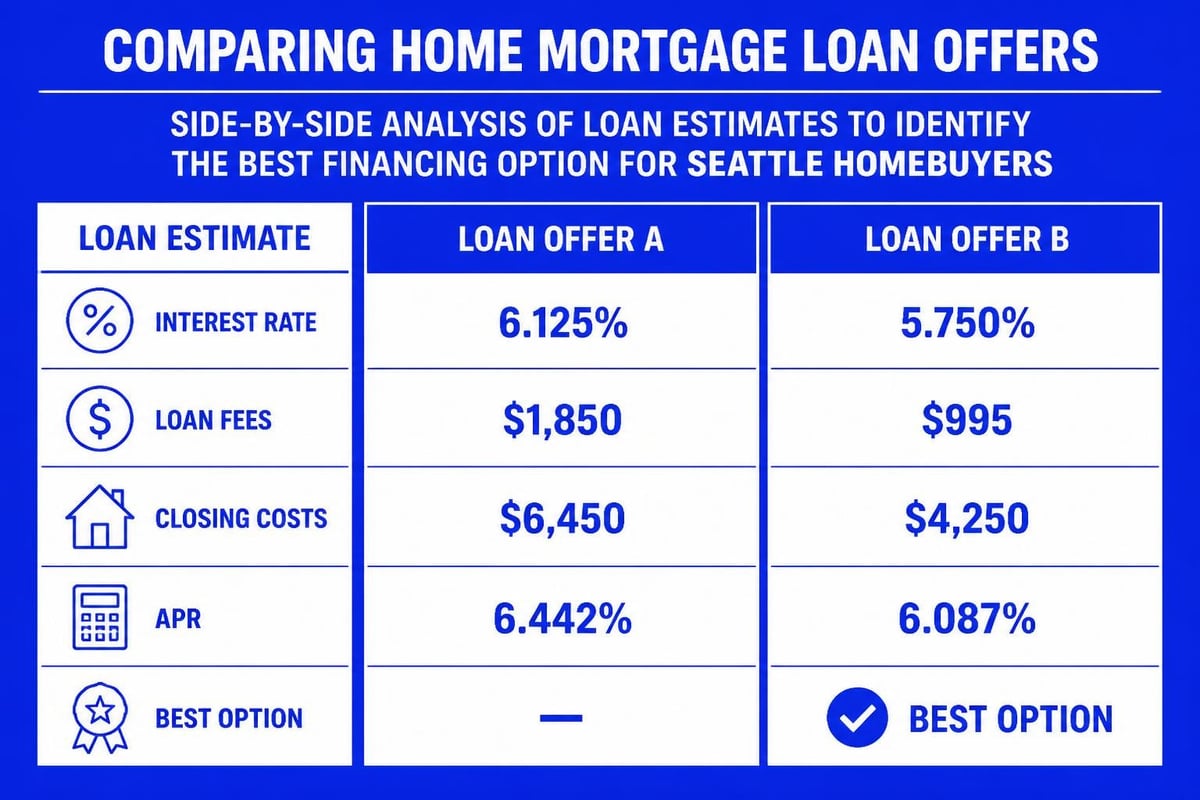

Comparing Mortgage Offers and Choosing Lenders

Shopping multiple lenders ensures you secure competitive terms and understand your options. The Consumer Financial Protection Bureau recommends comparing offers from at least three different lenders, reviewing Loan Estimates carefully to identify the true cost of each option.

What to Compare Across Loan Estimates

When evaluating home mortgage loan offers, focus on these critical elements:

Interest rate vs. APR: The interest rate determines your monthly payment, while the APR reflects total borrowing costs including fees. A lower rate with higher fees might cost more over time than a slightly higher rate with minimal fees.

Loan fees and origination charges: These vary significantly between lenders. Compare origination fees, processing fees, underwriting fees, and any discount points. Some lenders advertise low rates but compensate with excessive fees.

Closing cost allocation: Understanding which fees the lender charges versus third-party services helps identify where costs originate and potential negotiation opportunities.

| Cost Category | Typical Range | What It Covers |

|---|---|---|

| Origination fee | 0% – 1% of loan | Lender's processing and underwriting |

| Discount points | 0% – 3% of loan | Optional rate buy-down |

| Appraisal | $500 – $800 | Property valuation |

| Title/escrow | $1,500 – $3,000 | Title insurance and closing services |

| Prepaid items | Varies | Property taxes, insurance, interest |

Working with Mortgage Brokers vs. Direct Lenders

Mortgage brokers access multiple lenders, providing options and competitive pricing that single-source lenders cannot match. Benefits include:

- Access to wholesale rates not available directly to consumers

- Expertise navigating complex income situations and credit challenges

- Personalized service throughout the process

- Local market knowledge and relationship-based guidance

For Seattle buyers, particularly those with unique income structures or purchasing in competitive markets, experienced mortgage brokers provide strategic advantages that extend beyond rate shopping.

Understanding Mortgage Regulations and Consumer Protections

Federal regulations govern mortgage lending to ensure fair treatment and transparency. Understanding these protections helps you recognize legitimate practices and identify potential issues.

Key Federal Regulations

The Truth in Lending Act (TILA) requires lenders to disclose loan terms clearly, enabling borrowers to compare offers accurately. The standardized Loan Estimate and Closing Disclosure forms stem from TILA requirements, ensuring consistency across lenders.

The Real Estate Settlement Procedures Act (RESPA) prohibits kickbacks and requires disclosure of settlement costs. This regulation ensures you receive a Loan Estimate within three business days of application and a Closing Disclosure at least three business days before closing.

Ability-to-Repay and Qualified Mortgage standards, detailed in federal regulations, require lenders to verify your ability to repay the loan based on documented income, assets, employment, credit history, and debt-to-income ratio. These standards protect both borrowers and the broader housing market.

Understanding your rights under these regulations empowers you to recognize proper lending practices. The FDIC provides comprehensive consumer resources explaining mortgage basics and protections.

Red Flags to Avoid

While most lenders operate ethically, awareness of predatory practices protects your interests:

- Pressure to overstate income or assets on applications

- Encouragement to purchase more home than you can afford

- Unexplained fee increases between application and closing

- Requests to sign blank documents or forms with incomplete information

- Reluctance to provide clear explanations of loan terms

Rate Locks, Float Strategies, and Timing Considerations

Interest rates fluctuate daily based on economic indicators, Federal Reserve policy, and bond market activity. Strategic timing of your rate lock can save thousands over the life of your home mortgage loan.

Understanding Rate Lock Mechanics

A rate lock guarantees your interest rate for a specified period, typically 30, 45, or 60 days. This protection shields you from rate increases during processing but also prevents you from benefiting if rates decline.

When to lock your rate:

- Lock when you're satisfied with the rate relative to recent trends

- Consider longer lock periods (45-60 days) in volatile markets or for complex transactions

- Lock immediately if you're at your affordability threshold and cannot absorb rate increases

- Evaluate float-down options that allow one-time rate adjustment if rates drop significantly

Rate Float Strategies

Floating means not locking your rate, betting that rates will decline before closing. This strategy works when:

- Economic indicators suggest declining rates

- You have financial cushion to absorb potential increases

- You're early in the process with ample time to monitor markets

For Seattle buyers navigating multiple-offer situations, coordinating your rate lock with offer acceptance timing optimizes both rate and closing timeline alignment.

Refinancing Your Home Mortgage Loan

Market conditions, equity accumulation, or changed financial circumstances may make refinancing advantageous. Understanding when refinancing makes sense helps you maximize long-term savings.

Common Refinance Scenarios

Rate-and-term refinancing replaces your existing mortgage with a new loan at a lower rate or different term. This strategy makes sense when rates have dropped significantly since your original purchase or you want to adjust your loan term.

Cash-out refinancing accesses accumulated equity while refinancing your existing mortgage. Seattle homeowners often use this strategy to fund renovations, consolidate higher-interest debt, or make investment purchases.

Streamline refinancing through FHA or VA programs offers simplified processing with reduced documentation when you already have that loan type.

Calculating Refinance Value

Determine your break-even point by dividing closing costs by monthly savings. If refinancing costs $6,000 and saves $250 monthly, you break even in 24 months. Plan to stay in the home beyond this period to realize value.

Additional considerations for Seattle homeowners:

- How much equity you've accumulated (typically need 20% to avoid PMI)

- Whether removing PMI from your original loan justifies refinancing

- Potential tax implications of cash-out refinancing

- Impact on retirement or other financial goals

Preparing for the Home Mortgage Loan Process

Preparation significantly impacts your experience and outcomes. Taking strategic steps before applying positions you for approval and competitive advantage in offer situations.

Pre-Approval vs. Pre-Qualification

Pre-qualification provides a rough estimate based on information you provide without verification. This preliminary assessment offers minimal value to sellers.

Pre-approval involves full documentation review, credit check, and underwriter evaluation. This comprehensive assessment carries weight in competitive markets, signaling to sellers that you're a qualified, serious buyer.

For Seattle-area purchases, particularly in Bellevue, Redmond, or Kirkland where competition remains strong, robust pre-approval from a reputable broker distinguishes your offer.

Financial Preparation Steps

Strengthen your mortgage application through these actions:

- Review credit reports from all three bureaus, disputing errors and addressing issues

- Reduce credit card balances below 30% of limits to improve scores

- Avoid new credit inquiries in the months before applying

- Accumulate cash reserves beyond your down payment and closing costs

- Document irregular income thoroughly if you're self-employed or have variable compensation

- Stabilize employment by avoiding job changes during the process if possible

Timeline Expectations

Understanding the typical home mortgage loan timeline helps you plan effectively:

- Pre-approval: 1-3 days with complete documentation

- Home shopping: Varies by market conditions and buyer criteria

- Offer acceptance to closing: 30-45 days standard, 9-21 days for expedited closings

- Underwriting review: 1-2 weeks for initial decision

- Appraisal: 1-2 weeks depending on property type and location

- Final approval and clear to close: 3-5 days before closing date

Working with brokers who have direct underwriting access and strong processor relationships accelerates these timelines, particularly valuable in competitive Seattle markets where sellers favor quick closes.

Making Your Home Mortgage Loan Decision

Your mortgage choice impacts your financial health for years or decades. Balancing immediate affordability with long-term goals requires careful consideration of multiple factors.

Evaluating Loan Terms and Monthly Payment Comfort

While lenders qualify you based on debt-to-income ratios, personal comfort matters more than maximum qualification. Consider:

- Monthly payment sustainability across income fluctuations

- Reserve funds for maintenance, repairs, and emergencies

- Other financial goals (retirement savings, education funding, investments)

- Lifestyle priorities beyond housing

Seattle's higher cost of living makes this evaluation particularly important. Tech professionals with stock-heavy compensation should account for market volatility when determining sustainable payment levels.

Balancing Down Payment and Reserves

Larger down payments reduce monthly costs and eliminate PMI, but depleting savings creates risk. Maintain adequate reserves for:

- Emergency funds (3-6 months of expenses)

- Home maintenance and unexpected repairs

- Property taxes and insurance increases

- Career transitions or income interruptions

Finding the optimal balance depends on your risk tolerance, income stability, and long-term plans.

Securing the right home mortgage loan requires understanding your options, preparing thoroughly, and working with experienced professionals who navigate complex markets effectively. Whether you're a first-time buyer in Mill Creek or a tech professional purchasing a luxury home in Bellevue, strategic financing positions you for long-term success. Keith Akada and the team at Mortgage Reel bring 25+ years of Seattle market expertise, specializing in stock compensation qualification, jumbo loans, and rapid closings that give you competitive advantage. Connect with Mortgage Reel today to explore your financing options and move forward with confidence.