Understanding the mortgage lending process is essential for anyone preparing to purchase a home in Seattle, Shoreline, or the surrounding communities. Whether you're a tech professional at Amazon or Microsoft looking to leverage stock compensation, a first-time buyer navigating Lynnwood's housing market, or a seasoned investor expanding your portfolio in Bellevue, knowing what to expect at each stage creates confidence and reduces stress. The mortgage lending process involves multiple steps, regulatory requirements, and decision points that directly impact your timeline and buying power. This comprehensive guide breaks down each phase so you can approach your home purchase or refinance with clarity and preparation.

Pre-Approval: Establishing Your Buying Power

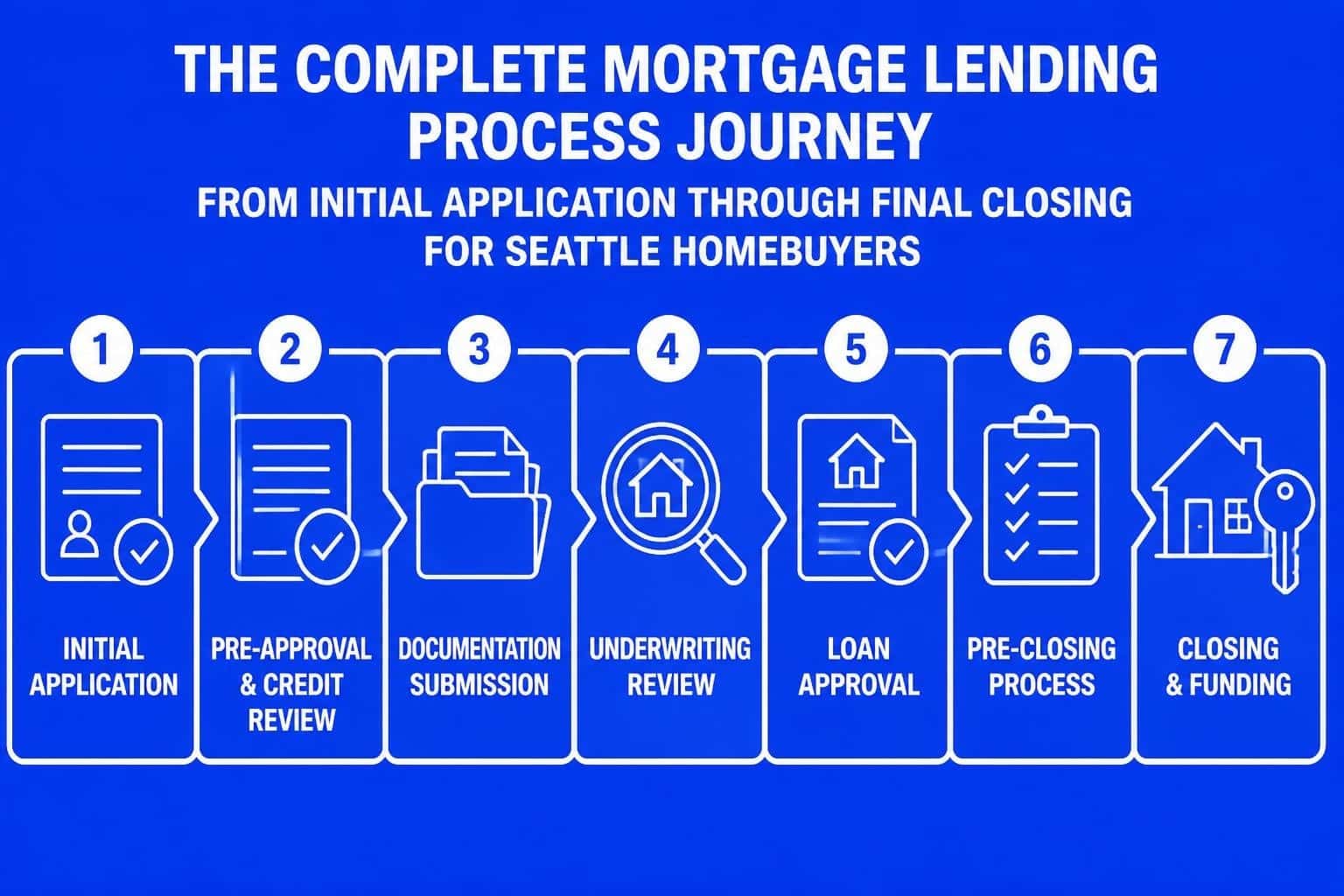

The mortgage lending process begins well before you submit a formal application. Pre-approval represents the critical first step that defines your budget and strengthens your position in competitive markets like Redmond and Kirkland.

During pre-approval, lenders evaluate your financial profile including income, assets, credit history, and existing debts. For Seattle-area tech professionals, this stage offers an opportunity to discuss how equity compensation factors into your qualification. Restricted Stock Units (RSUs), stock options, and performance bonuses can significantly increase your purchasing power when properly documented and presented to underwriting.

Documentation Requirements for Pre-Approval

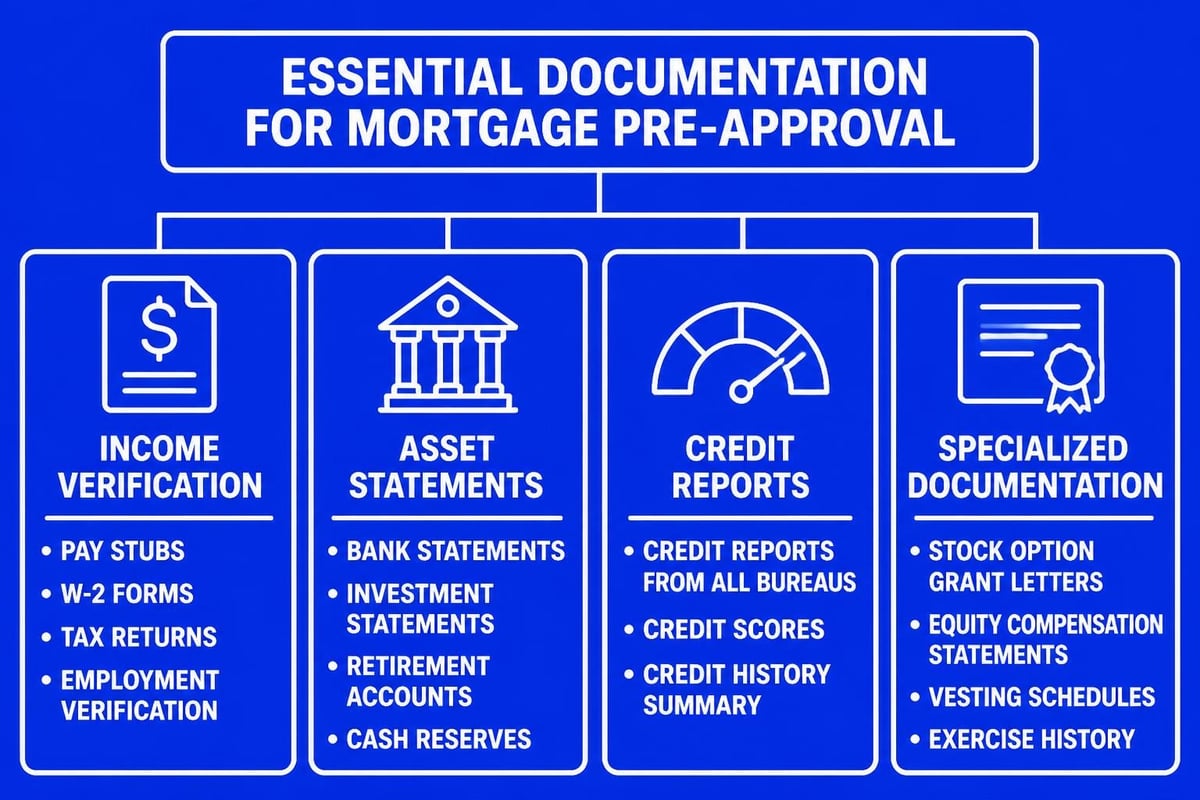

Gathering documentation early accelerates the entire mortgage lending process. Essential documents include:

- Two years of W-2 forms and recent pay stubs showing year-to-date earnings

- Two months of bank statements for all accounts (checking, savings, investment)

- Tax returns for the past two years if you're self-employed or have rental income

- Stock compensation statements detailing vesting schedules and grant dates

- Credit authorization allowing the lender to pull your credit report

The Consumer Financial Protection Bureau provides detailed guidance on mortgage basics and what documentation you'll need throughout the process.

Pre-approval letters typically remain valid for 60-90 days, giving you time to search for homes confidently. In fast-moving markets like Mill Creek and Lake Forest Park, a strong pre-approval from an experienced Seattle mortgage broker can differentiate your offer from competing bids.

Loan Application and Property Selection

Once you've identified a property and had your offer accepted, the formal mortgage lending process transitions to the application phase. This stage involves completing a comprehensive loan application-officially known as the Uniform Residential Loan Application (URLA) or Form 1003.

The application captures detailed information about the property you're purchasing, your employment history, income sources, assets, liabilities, and the loan amount you're requesting. Accuracy matters tremendously during this phase. Inconsistencies or omissions can delay processing or trigger additional documentation requests.

Loan Estimate Disclosure

Within three business days of receiving your complete application, federal law requires lenders to provide a Loan Estimate. This standardized document outlines:

| Section | Information Provided |

|---|---|

| Loan Terms | Interest rate, monthly payment, loan amount, loan type |

| Projected Payments | Principal, interest, taxes, insurance, HOA fees |

| Costs at Closing | Lender fees, third-party services, prepaid items |

| Cash to Close | Total funds needed at settlement |

| Comparisons | APR, total interest percentage, total payments |

The Loan Estimate allows you to compare offers from different lenders objectively. For those exploring jumbo home loans in Everett or Bellevue, these disclosures become particularly important given the larger loan amounts and potential rate variations.

Understanding the Real Estate Settlement Procedures Act helps borrowers recognize their rights during this stage of the mortgage lending process.

Processing and Underwriting

After you submit your application, the loan enters processing-a phase where documentation is verified, ordered, and prepared for underwriting review. Your loan processor coordinates with third parties to obtain:

- Appraisal to determine the property's market value

- Title search and insurance to verify clear ownership

- Homeowners insurance to protect the collateral

- Employment verification to confirm current income

- Asset verification to validate down payment and reserves

Processing typically takes one to two weeks, though timelines vary based on property type, loan program, and documentation complexity. For those pursuing first-time mortgage loans, additional education requirements may extend this phase slightly.

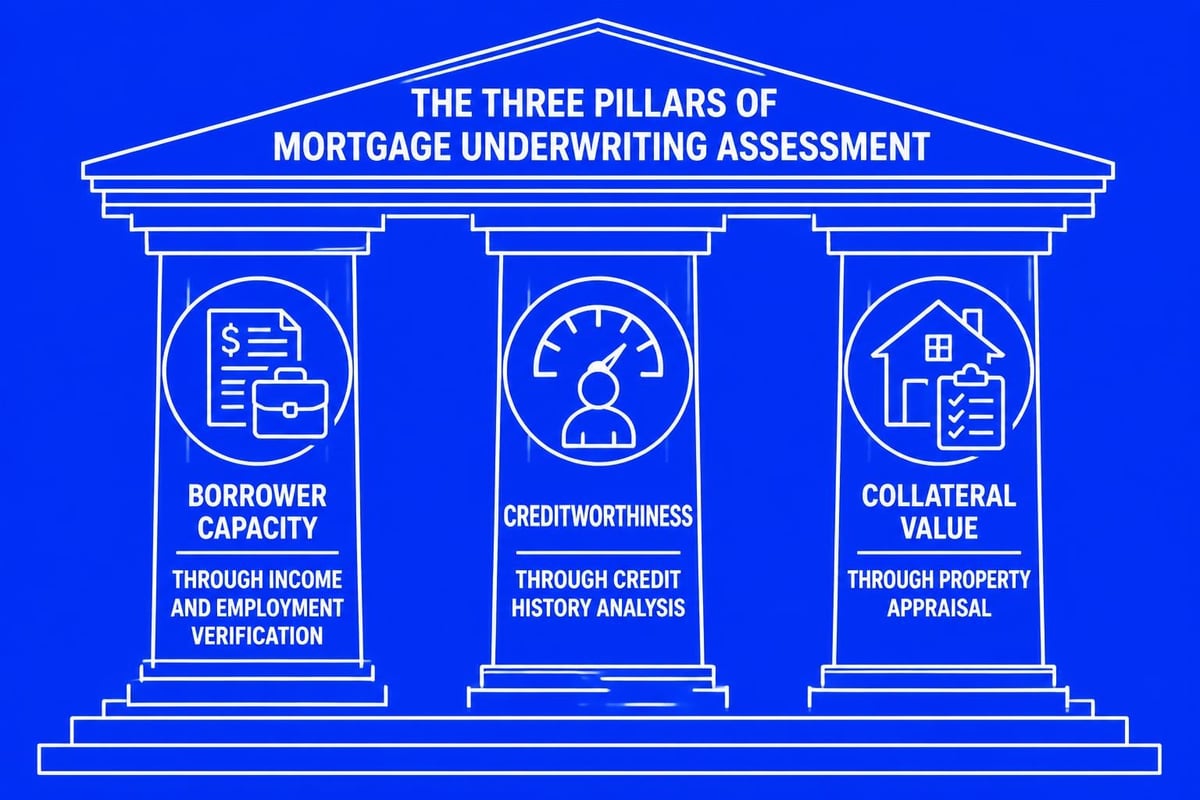

The Underwriting Review

Underwriting represents the heart of the mortgage lending process. An underwriter-a trained specialist who evaluates loan risk-reviews your complete file against lending guidelines. They assess three primary areas:

Capacity: Can you afford the monthly payments based on stable, documented income? Underwriters calculate debt-to-income ratios, typically requiring that total monthly debts (including the proposed mortgage) remain below 43-50% of gross monthly income.

Credit: Does your credit history demonstrate responsible debt management? Credit scores, payment patterns, recent inquiries, and debt levels all factor into this evaluation.

Collateral: Does the property value support the loan amount? The appraisal must meet or exceed the purchase price, and the property must meet minimum condition standards.

For Seattle tech professionals, underwriters often require additional documentation to validate stock compensation. This might include grant letters, vesting schedules, and historical evidence of equity awards. Understanding how to properly qualify this income separates experienced mortgage professionals from generalists.

Conditional Approval and Clear to Close

Most initial underwriting reviews result in conditional approval. The underwriter has reviewed your file and is willing to approve the loan, provided you satisfy specific conditions. Common conditions include:

- Explanation letters for recent large deposits or credit inquiries

- Updated pay stubs or bank statements

- Documentation of transferred funds between accounts

- Homeowners insurance declaration page

- Final inspection reports for new construction

- Subordination agreements for existing liens

Addressing conditions promptly keeps the mortgage lending process on schedule. Delays often stem from borrowers who don't respond quickly to condition requests or who make financial changes during the pending loan period.

What to Avoid During Processing

Maintaining financial stability throughout the mortgage lending process is critical. Avoid these common mistakes that can derail your approval:

- Changing jobs or employment status without discussing it with your lender first

- Making large purchases that increase your debt or deplete your assets

- Opening new credit accounts or closing existing ones

- Making unusual deposits without clear documentation of the source

- Co-signing loans for others, which increases your debt obligations

Once all conditions are satisfied and the underwriter provides final approval, your loan receives "clear to close" status. This milestone means you're ready to schedule your closing appointment and finalize the transaction.

Closing Preparation and Settlement

The final stage of the mortgage lending process involves preparing settlement documents and coordinating the closing appointment. Federal regulations require that you receive a Closing Disclosure at least three business days before closing.

The Closing Disclosure mirrors the format of your initial Loan Estimate but reflects actual final figures. Compare these documents carefully to ensure fees and terms align with your expectations. The Consumer Financial Protection Bureau explains what to expect in the mortgage closing process, including your right to review changes.

The Closing Appointment

Closing typically occurs at a title company office, where you'll meet with a closing agent or settlement attorney. The appointment usually takes 30-60 minutes and involves signing numerous documents:

| Document Type | Purpose |

|---|---|

| Promissory Note | Your promise to repay the loan with interest |

| Deed of Trust/Mortgage | Grants the lender security interest in the property |

| Closing Disclosure | Final accounting of all transaction costs |

| Initial Escrow Disclosure | Details of property tax and insurance reserves |

| Transfer Documents | Title and deed transferring property ownership |

You'll bring your cashier's check or arrange a wire transfer for your down payment and closing costs. The closing agent will record the transaction with the county, and you'll receive keys to your new home.

For Shoreline and Lynnwood buyers closing on tight timelines, working with lenders who offer expedited processing can mean closing in as few as nine business days when circumstances require speed.

Loan Programs and Guideline Variations

The mortgage lending process varies somewhat depending on your chosen loan program. Each has specific requirements that affect documentation, approval criteria, and timelines.

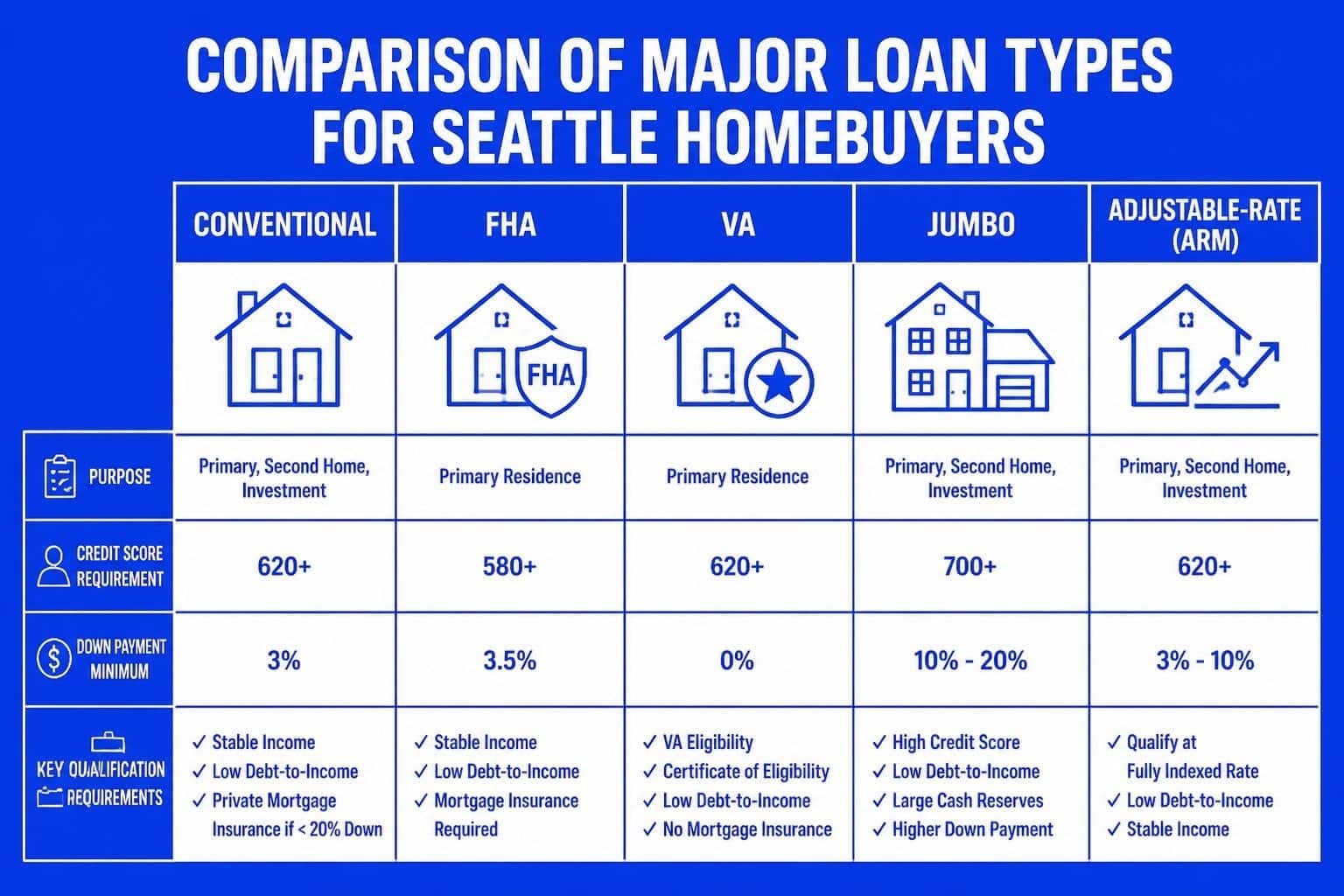

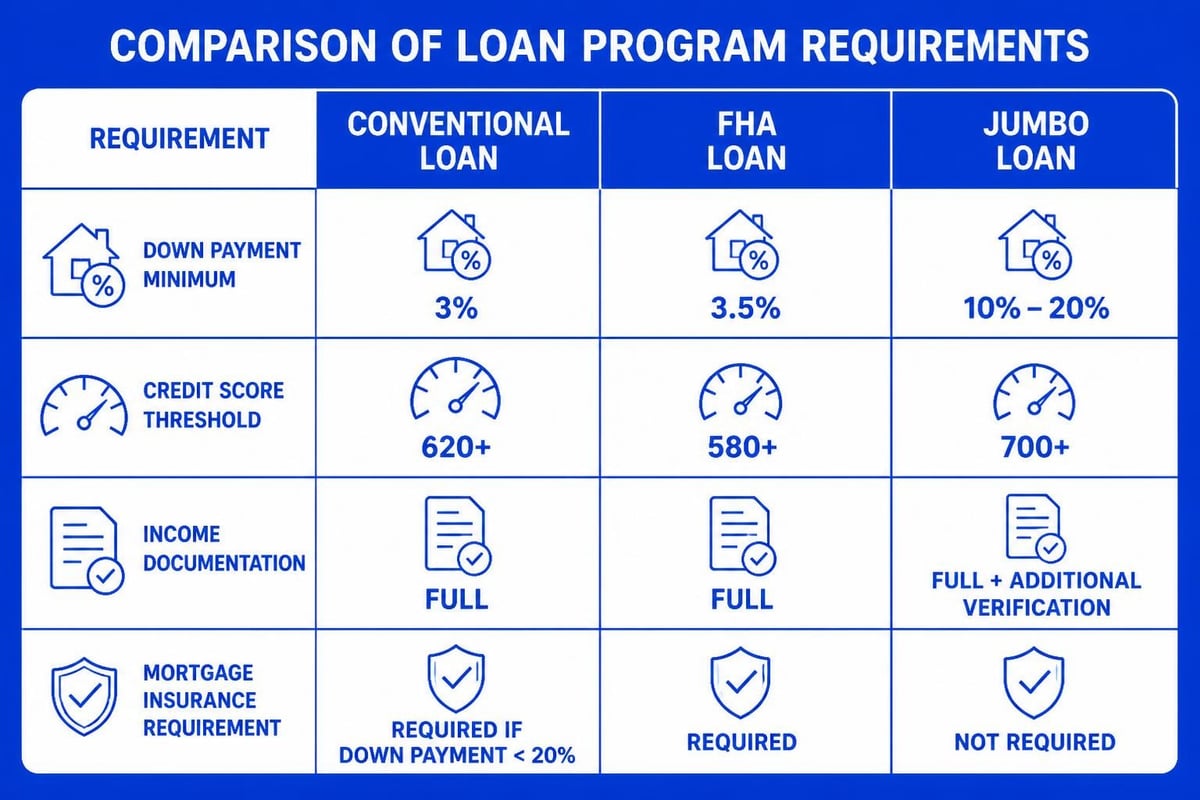

Conventional Loans

Conventional mortgages follow guidelines established by Fannie Mae and Freddie Mac. These loans typically require:

- Minimum credit scores of 620-640

- Down payments as low as 3% for first-time buyers

- Private mortgage insurance (PMI) when down payment is less than 20%

- Maximum debt-to-income ratios around 45-50%

Those exploring conventional loan options benefit from flexible property type eligibility and the ability to finance investment properties with appropriate down payments.

FHA Loans

The Federal Housing Administration insures loans that serve borrowers who may not qualify conventionally. The HUD Single Family Housing Policy Handbook details FHA's comprehensive guidelines. Key features include:

- Credit scores as low as 580 with 3.5% down

- More lenient qualification for recent credit events

- Upfront and annual mortgage insurance premiums

- Limits on maximum loan amounts by county

FHA financing often appeals to first-time buyers in Lake Forest Park and Mill Creek who have limited down payment funds but stable income.

Jumbo Loans

Properties exceeding conforming loan limits ($806,500 in most of Washington state for 2026) require jumbo financing. The mortgage lending process for jumbo home mortgages involves:

- Higher credit score requirements (typically 700-720 minimum)

- Larger down payments (usually 10-20%)

- More substantial cash reserves (6-12 months)

- Additional income documentation and verification

Seattle's competitive housing market frequently requires jumbo financing, particularly in neighborhoods like Bellevue, Redmond, and Kirkland where median home prices exceed conforming limits.

Regulatory Framework and Consumer Protections

The mortgage lending process operates within a comprehensive regulatory framework designed to protect consumers and ensure fair lending practices. Understanding these protections empowers you to recognize your rights and advocate for fair treatment.

The Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA) establish key consumer protections including:

- Right to receive good faith estimates of closing costs within specific timeframes

- Protection against kickbacks and unearned fees among settlement service providers

- Ability to review settlement statements before closing

- Limits on escrow account requirements and regulations governing escrow management

Additional protections emerged from the Dodd-Frank Wall Street Reform and Consumer Protection Act. Title XIV of Dodd-Frank introduced the Ability-to-Repay rule, which requires lenders to make reasonable determinations that borrowers can repay their mortgages.

Fair Lending and Equal Credit Opportunity

The Equal Credit Opportunity Act (ECOA) and Fair Housing Act prohibit discrimination in lending based on race, color, religion, national origin, sex, marital status, age, or source of income. These protections ensure the mortgage lending process remains accessible and equitable.

Working with a reputable home lending professional ensures compliance with these regulations while maximizing your qualification opportunities through legitimate means.

Strategic Considerations for Seattle Homebuyers

The mortgage lending process requires strategic thinking beyond simply qualifying for financing. Seattle-area buyers face unique market conditions that influence timing, property selection, and loan structuring.

Stock Compensation Strategies

Tech professionals throughout Seattle, Bellevville, and Redmond often hold significant wealth in equity compensation. Maximizing this income for mortgage qualification requires understanding how underwriters evaluate different compensation types:

- Vested RSUs: Typically counted at 100% of value with two-year history

- Unvested RSUs: May count at 70-100% with consistent vesting patterns

- Stock options: Generally not counted until exercised and sold

- Bonuses: Require two-year history with consistency and likelihood of continuance

Documenting these income sources properly can increase buying power by tens or hundreds of thousands of dollars in high-earning households.

Down Payment Planning

While low down payment programs exist, larger down payments offer strategic advantages in the mortgage lending process:

- Elimination of mortgage insurance at 20% down, reducing monthly payments

- Stronger offers in competitive multiple-offer situations

- Better interest rates on jumbo financing with larger equity positions

- Lower monthly obligations creating more financial flexibility

Balancing down payment size against investment opportunities and emergency reserves requires personalized financial analysis based on your specific circumstances.

Rate Lock Timing

Interest rates fluctuate daily based on economic conditions, Federal Reserve policy, and bond market activity. The mortgage lending process typically allows you to lock your interest rate once you have a ratified purchase contract.

Rate lock periods commonly range from 15 to 60 days, with longer locks sometimes carrying fees. Consider these factors when timing your lock:

- Current rate trends and economic forecasts

- Expected closing timeline based on contract terms

- Property type and potential appraisal delays

- Seller's timeline and flexibility on closing dates

The Office of the Comptroller of the Currency provides context on mortgage banking practices including rate lock policies and secondary market operations.

Common Obstacles and Solutions

Even well-prepared borrowers encounter challenges during the mortgage lending process. Recognizing common obstacles and their solutions helps you navigate issues efficiently.

Appraisal Issues

When the appraisal comes in below the purchase price, several options exist:

- Negotiate price reduction with the seller to match the appraised value

- Bring additional cash to cover the difference between price and appraised value

- Request appraisal reconsideration with supporting comparable sales data

- Order a second appraisal if the first appears flawed (with lender approval)

- Include appraisal contingencies in your offer to protect your earnest money

Seattle's competitive market sometimes leads to prices that exceed appraisal values, particularly in hot neighborhoods throughout Shoreline and Everett.

Income Documentation Challenges

Self-employed borrowers, commission-based earners, and those with complex income structures often face additional documentation requirements. Solutions include:

- Providing detailed profit and loss statements prepared by accountants

- Obtaining CPA letters verifying business income and stability

- Demonstrating increasing income trends over multiple years

- Maintaining clear separation between business and personal accounts

- Working with underwriters experienced in complex income scenarios

Credit Score Concerns

If your credit score falls below program minimums or you have recent derogatory items, consider:

- Rapid rescore to quickly update credit reports with documented corrections

- Authorized user tradelines to build credit history (with caution)

- Debt paydown to improve credit utilization ratios

- Waiting periods after bankruptcies, foreclosures, or short sales

- Manual underwriting for borderline situations with compensating factors

Timeline Expectations and Acceleration Strategies

Understanding realistic timelines for the mortgage lending process helps you plan accordingly and identify opportunities for acceleration when needed.

Standard Timeline Breakdown

| Phase | Typical Duration | Acceleration Potential |

|---|---|---|

| Pre-approval | 1-3 days | Same day with complete documentation |

| Application to processing | 3-5 days | 1-2 days with digital submission |

| Processing to underwriting | 5-10 days | 3-5 days with prompt third-party responses |

| Underwriting review | 3-5 days | 1-2 days with complete documentation |

| Conditional approval to clear | 3-7 days | 1-3 days with immediate condition response |

| Clear to close to closing | 3-4 days | Minimum 3 days by federal regulation |

| Total Timeline | 18-34 days | 9-15 days with optimal conditions |

Acceleration requires exceptional preparation, responsive communication, and experienced coordination. Lenders with dedicated processing teams and strong third-party relationships can compress timelines significantly when circumstances demand speed.

Factors That Extend Timelines

Be aware of circumstances that commonly extend the mortgage lending process:

- Complex property types (condos requiring HOA certification, new construction, rural properties)

- Self-employment or non-traditional income requiring additional documentation

- Multiple borrowers with complicated financial situations

- Properties requiring repairs or additional inspections

- Purchase contracts with extended due diligence periods

- High loan volume periods creating processing backlogs

Working with an experienced mortgage professional who understands these variables helps set appropriate expectations and mitigate delays proactively.

Post-Closing Considerations

The mortgage lending process doesn't end at closing. Understanding post-closing elements ensures you manage your mortgage effectively over time.

Loan Servicing Transfer

Your lender may sell servicing rights to your loan, meaning another company collects your payments and manages your escrow account. The federal regulations require notification at least 15 days before the transfer, and your loan terms cannot change.

Escrow Account Management

If you established an escrow account for property taxes and insurance, you'll receive annual escrow analyses. These statements project your upcoming tax and insurance costs and adjust your monthly payment accordingly to maintain proper reserves.

Refinancing Opportunities

Monitor interest rate trends and your financial situation for refinancing opportunities. Refinancing essentially repeats the mortgage lending process to replace your current loan with new terms. Consider refinancing when:

- Interest rates drop 0.75% or more below your current rate

- You want to eliminate mortgage insurance after reaching 20% equity

- You need to access equity for improvements or debt consolidation

- You want to shorten your loan term to build equity faster

For those interested in mortgage financing strategies, understanding when refinancing makes financial sense optimizes your long-term housing costs.

Leveraging Professional Expertise

Navigating the mortgage lending process successfully requires knowledge, experience, and strategic thinking. While this guide provides comprehensive information, individual circumstances vary significantly based on income type, credit profile, property characteristics, and financial goals.

Professional mortgage brokers bring value through:

- Access to multiple lenders and loan programs rather than a single bank's products

- Expertise in complex income including stock compensation, bonuses, and self-employment

- Relationship leverage for expedited processing and underwriting flexibility

- Market knowledge specific to Seattle-area lending and real estate dynamics

- Problem-solving experience when obstacles arise during processing

The difference between a smooth, efficient mortgage lending process and a stressful, complicated experience often comes down to the expertise guiding you through each phase.

Successfully navigating the mortgage lending process requires preparation, documentation, and strategic decision-making at each phase from pre-approval through closing. Understanding federal regulations, loan program requirements, and local market dynamics positions Seattle-area homebuyers to make confident financing decisions. Whether you're a tech professional leveraging equity compensation, a first-time buyer exploring low down payment options, or an investor expanding your portfolio throughout Seattle, Bellevue, Redmond, Kirkland, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett, working with an experienced professional makes all the difference. Keith Akada at Mortgage Reel brings 25+ years of expertise, 750+ five-star reviews, and the ability to close loans in as few as 9 business days, providing the education, transparency, and execution you need for successful homeownership.