Understanding the home buyers process can feel overwhelming, especially in competitive markets like Seattle, Bellevue, Redmond, and Kirkland. Whether you're a first-time buyer evaluating first-time mortgage loans or a tech professional leveraging stock compensation for a jumbo purchase, knowing what to expect at each stage transforms uncertainty into confidence. This comprehensive guide walks through every phase of the home buyers process, providing practical insights and strategic advice to help you navigate one of the most significant financial decisions you'll ever make.

Financial Preparation and Assessment

The home buyers process begins long before you tour your first property. Evaluating your financial readiness establishes the foundation for everything that follows.

Reviewing Your Credit Profile

Your credit score directly impacts mortgage rates and loan approval. Most conventional loans require a minimum score of 620, while FHA loans may accept scores as low as 580. Review your credit reports from all three bureaus, dispute any errors, and address outstanding collections or late payments.

Key credit improvement strategies:

- Pay down credit card balances below 30% utilization

- Avoid opening new credit accounts within six months of applying

- Keep existing accounts open to maintain credit history length

- Set up automatic payments to prevent future late payments

For Seattle-area tech professionals with RSUs and stock compensation, maintaining strong credit becomes even more important when qualifying for jumbo home loans that exceed conventional loan limits.

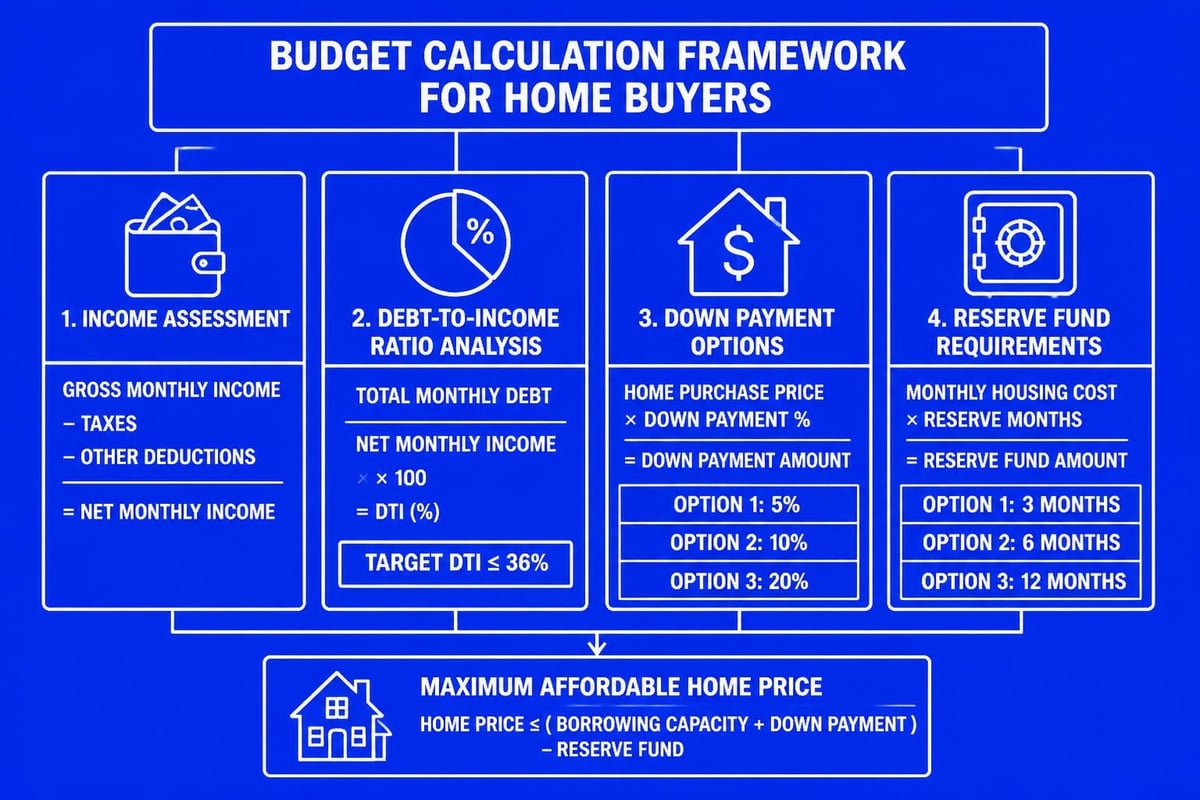

Calculating Your Budget

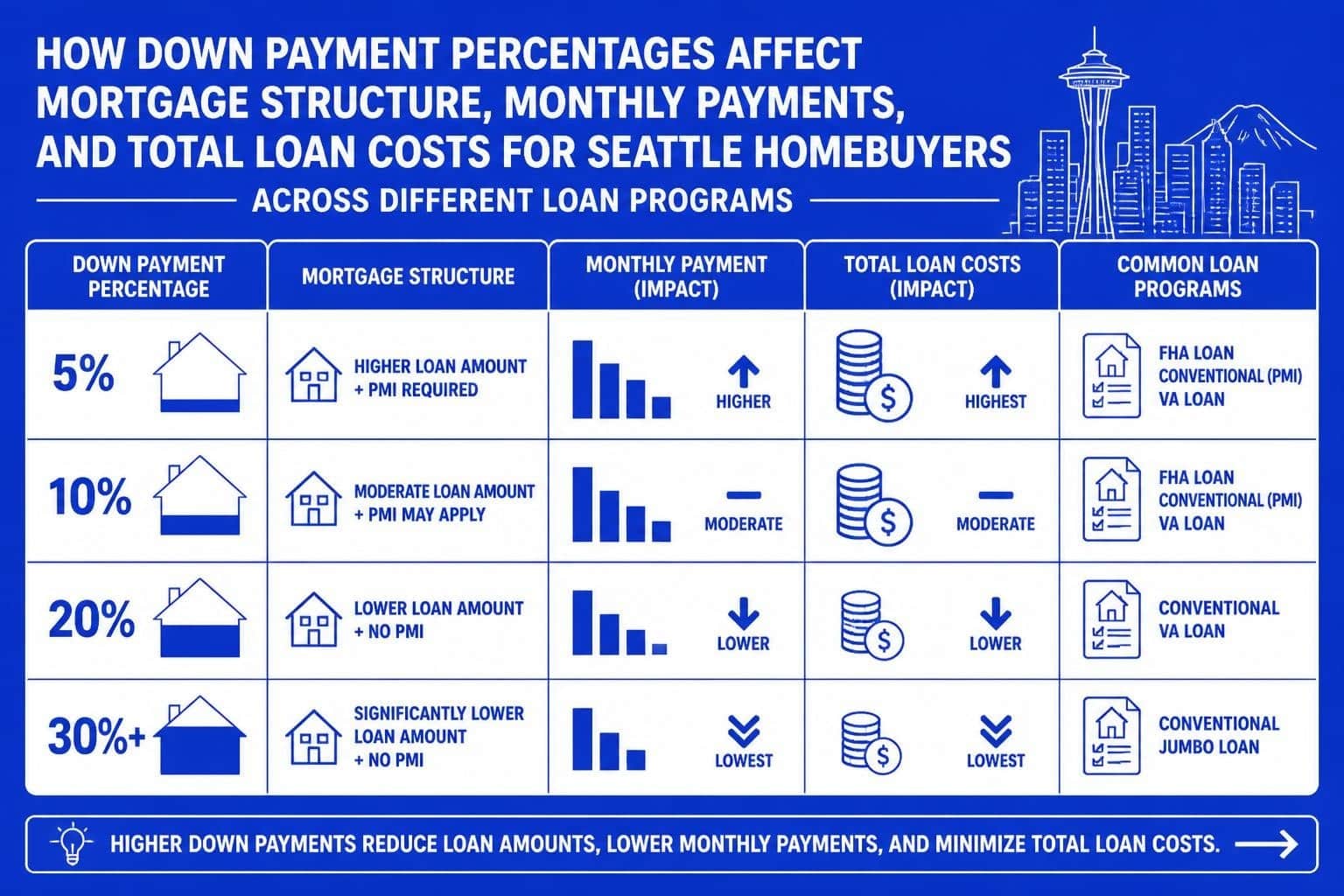

Determining how much house you can afford requires more than just looking at your salary. The home buyers process demands a realistic assessment of your complete financial picture, including down payment capacity, monthly payment comfort level, and reserve funds.

| Budget Component | Recommended Amount | Purpose |

|---|---|---|

| Down Payment | 3% to 20%+ | Initial equity, affects PMI |

| Closing Costs | 2% to 5% of purchase price | Fees, taxes, insurance |

| Emergency Reserve | 3 to 6 months expenses | Financial cushion |

| Monthly Payment | Max 28% of gross income | Principal, interest, taxes, insurance |

Seattle's median home prices often exceed $800,000, making down payment planning particularly critical. Understanding conventional loans down payment requirements helps you set realistic savings goals.

Mortgage Pre-Approval Process

Securing pre-approval represents one of the most critical steps in the home buyers process. Unlike pre-qualification, which provides a rough estimate, pre-approval involves complete financial verification.

Gathering Required Documentation

Lenders need comprehensive documentation to verify your ability to repay the mortgage. Organized paperwork accelerates the process and demonstrates financial responsibility.

Standard documentation includes:

- Two years of W-2 forms and tax returns

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Documentation of additional income sources

- Explanations for large deposits or withdrawals

Tech professionals should also provide RSU vesting schedules, stock option agreements, and bonus history. Lenders typically average variable compensation over two years, so complete documentation of stock compensation for maximum buying power becomes essential in competitive markets.

Understanding Loan Options

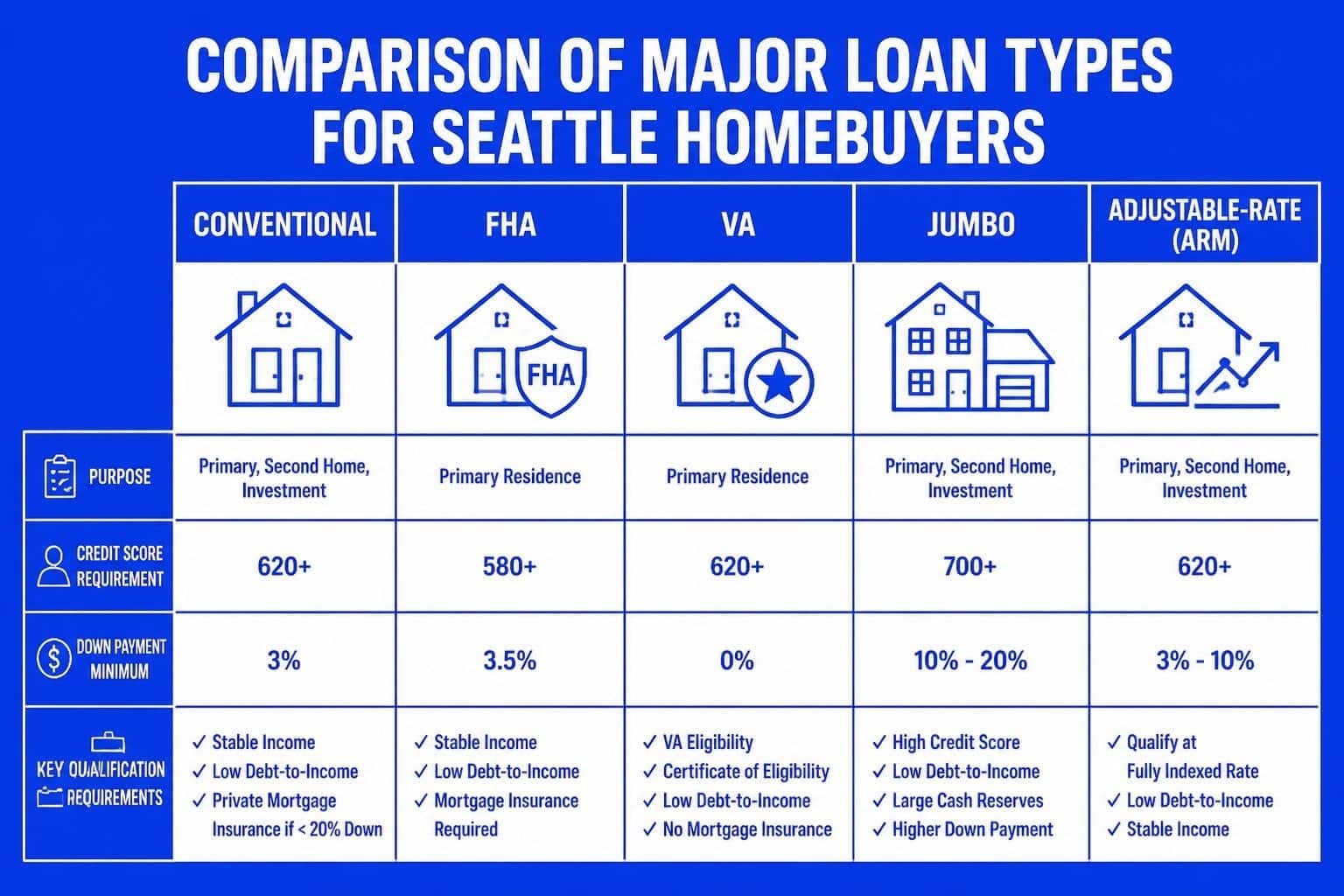

The home buyers process requires selecting the right mortgage product for your situation. Each loan type offers distinct advantages depending on your down payment, credit profile, and property type.

Conventional loans suit buyers with strong credit and at least 3% down. FHA loans accommodate lower credit scores with as little as 3.5% down. VA loans provide zero-down financing for eligible veterans and service members. Jumbo loans finance properties exceeding conventional limits, common in Seattle, Bellevue, and Kirkland.

Working with an experienced broker ensures you understand which options maximize your purchasing power while minimizing long-term costs. The right guidance during this phase of the home buyers process can save tens of thousands over the life of your loan.

Property Search and Selection

With financing secured, the home buyers process shifts to finding the right property. This phase combines practical considerations with emotional decision-making.

Defining Your Priorities

Create a clear list of must-haves versus nice-to-haves. Consider commute times to major employers like Amazon, Microsoft, and Google when evaluating neighborhoods in Shoreline, Lynnwood, or Mill Creek.

Common priority categories:

- Location and school districts

- Property size and layout

- Condition and age

- Future appreciation potential

- Proximity to amenities and transportation

Working with Real Estate Professionals

Experienced real estate agents provide market knowledge, negotiation expertise, and access to listings before they hit major platforms. They understand important steps when buying a home specific to the Greater Seattle area.

Your agent should communicate regularly with your lender to ensure offer terms align with your financing capabilities. This coordination prevents complications during the home buyers process and strengthens your position in multiple-offer situations.

Making an Offer and Negotiation

Once you identify the right property, the home buyers process accelerates quickly. Competitive Seattle markets often require strategic approaches to stand out.

Crafting a Competitive Offer

Your offer includes the purchase price, earnest money deposit, contingencies, proposed closing timeline, and any special terms. In hot markets, buyers sometimes waive contingencies or offer escalation clauses.

| Offer Component | Purpose | Typical Terms |

|---|---|---|

| Purchase Price | Amount offered | Based on comps, condition |

| Earnest Money | Shows commitment | 1% to 3% of price |

| Inspection Contingency | Property condition review | 10 to 17 days |

| Financing Contingency | Loan approval protection | 21 to 30 days |

| Appraisal Contingency | Value verification | Included with financing |

Strong pre-approval letters from reputable lenders increase seller confidence. Some buyers in Redmond and Bellevue include proof of funds for down payment or appraisal gap coverage to strengthen their position.

Navigating Counteroffers

Sellers may counter your initial offer with different terms. The negotiation phase of the home buyers process requires balancing your budget limits with market realities. Your real estate agent and mortgage broker should collaborate to ensure any agreed terms remain financially feasible.

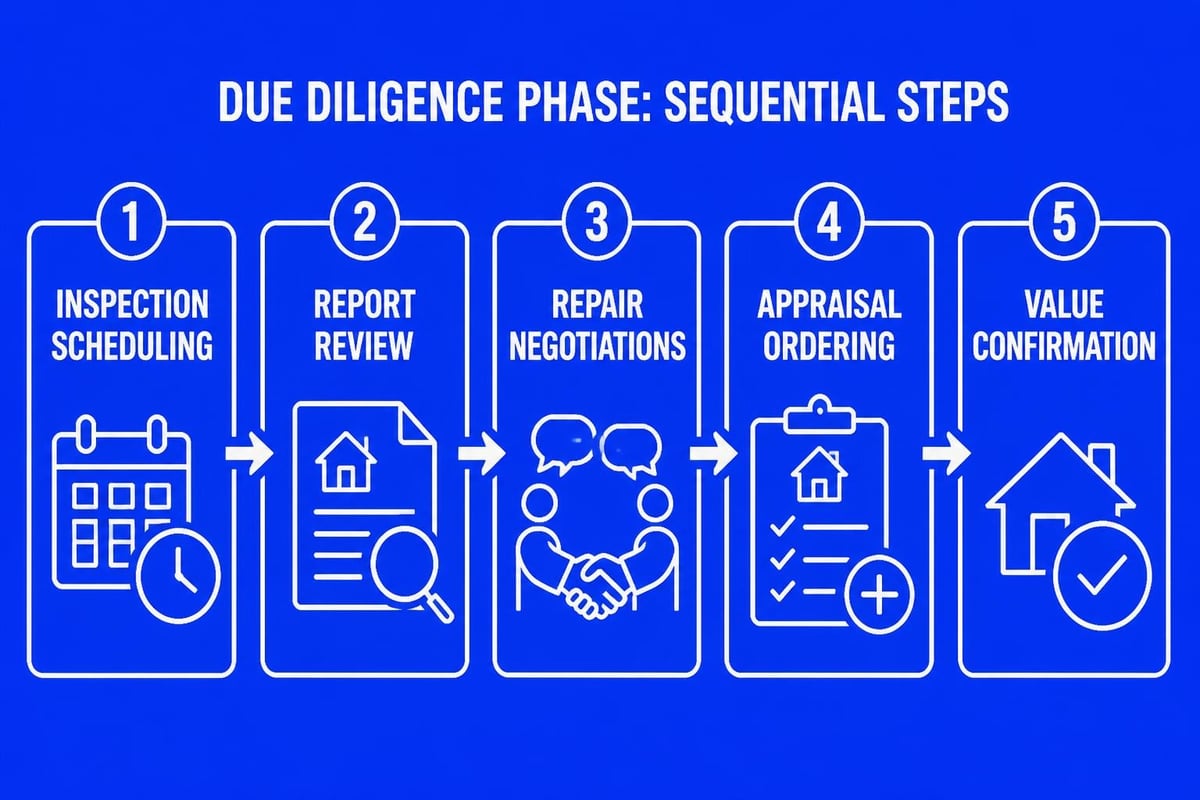

Home Inspection and Due Diligence

After offer acceptance, the home buyers process enters a critical verification period. This phase protects your investment by uncovering potential issues before finalizing the purchase.

Professional Inspection

Hire a qualified inspector to evaluate the property's condition. They examine structural elements, systems, safety concerns, and code violations. Inspection reports typically run 30 to 50 pages with detailed findings and photographs.

Key inspection areas:

- Foundation and structural integrity

- Roof condition and remaining lifespan

- Electrical, plumbing, and HVAC systems

- Windows, doors, and insulation

- Evidence of water damage or mold

In Lake Forest Park and Everett, where many homes were built decades ago, thorough inspections become especially important. Findings may lead to repair negotiations, price adjustments, or in severe cases, contract termination.

Additional Assessments

Depending on property type and location, you may need specialized inspections for septic systems, wells, pest damage, or environmental hazards. These assessments add time and cost but provide essential protection during the home buyers process.

Appraisal and Final Loan Processing

While you complete due diligence, your lender continues processing your loan application. The appraisal represents a critical milestone in the home buyers process.

Understanding the Appraisal

Lenders order independent appraisals to verify the property's value supports the loan amount. Appraisers analyze recent comparable sales, property condition, and market trends to determine fair market value.

If the appraisal comes in below the purchase price, you face several options: negotiate with the seller, increase your down payment to cover the gap, or terminate the contract if you included an appraisal contingency.

Finalizing Loan Approval

Your lender reviews title reports, completes final employment verification, and confirms no significant financial changes occurred since pre-approval. Maintaining financial stability throughout the home buyers process is crucial. Avoid large purchases, job changes, or new debt before closing.

The home buying checklist steps emphasize maintaining consistency in your financial profile from application through closing.

Closing Preparation

The final stage of the home buyers process involves coordinating multiple parties, reviewing extensive documentation, and preparing for ownership transfer.

Reviewing Closing Disclosure

Lenders must provide your Closing Disclosure at least three business days before closing. This document details your final loan terms, monthly payment, closing costs, and cash needed to close.

Compare the Closing Disclosure against your Loan Estimate to identify any significant changes. Your lender should explain any differences and ensure you understand every fee and charge.

Final Walkthrough

Conduct a final walkthrough within 24 hours of closing to verify the property's condition matches your expectations. Confirm agreed-upon repairs were completed and no new damage occurred since inspection.

Final walkthrough checklist:

- All included appliances and fixtures remain

- Agreed repairs were completed properly

- Utilities are functional

- No new damage or missing items

- Property is clean and debris-free

The Closing Day Experience

Closing day represents the culmination of the home buyers process. Understanding what happens ensures a smooth transaction.

Signing Session

You'll sign numerous documents including the mortgage note, deed of trust, initial escrow disclosure, and various acknowledgments. The closing agent explains each document, but review everything carefully before signing.

Bring a government-issued ID, cashier's check or wire confirmation for closing costs, and proof of homeowner's insurance. The entire process typically takes one to two hours.

Receiving the Keys

After all documents are signed and funds are transferred, you receive the keys to your new home. Some areas record documents electronically, providing immediate ownership transfer. Others may take several days for county recording.

Post-Closing Responsibilities

The home buyers process doesn't end at closing. New homeowners face immediate responsibilities and opportunities.

Setting Up Utilities and Services

Transfer or establish accounts for electricity, gas, water, sewer, garbage, internet, and security systems. Many providers require deposits or advance payments for new customers.

Understanding Your Mortgage

Your first payment typically occurs 30 to 45 days after closing. Set up automatic payments to avoid late fees and protect your credit. Review your escrow account annually to ensure property taxes and insurance premiums are covered.

| Post-Closing Task | Timing | Importance |

|---|---|---|

| Change locks | Immediately | Security |

| Forward mail | Within 1 week | Continuity |

| File homestead exemption | Within 1 year | Tax savings |

| Review title insurance | Within 30 days | Protection verification |

| Schedule maintenance | Ongoing | Property preservation |

Leveraging Equity and Refinancing

Understanding how the home buyers process connects to long-term wealth building helps maximize your investment.

Building Equity Strategically

Equity grows through principal paydown and appreciation. Making extra principal payments accelerates equity building, while home improvements may increase property value.

Seattle-area properties have historically appreciated well, though market conditions vary. Monitor local market trends in your specific neighborhood to understand your home's value trajectory.

Refinancing Considerations

Market changes may create refinancing opportunities to lower your rate, eliminate PMI, or access equity. The home buying process timeline you followed initially prepares you for streamlined refinancing when beneficial.

Special Considerations for Tech Professionals

Seattle's concentration of major tech employers creates unique opportunities and challenges within the home buyers process.

Qualifying Stock Compensation

Lenders can include RSUs, stock options, and bonuses in qualifying income after establishing two-year history. Providing complete vesting schedules and historical documentation of variable compensation strengthens your application.

Some lenders average the most recent year with the previous year, while others use a two-year average. Understanding these calculation methods helps you maximize qualifying income for jumbo home mortgage applications.

Fast-Track Closing Options

Competitive markets sometimes require rapid closing capabilities. Advanced underwriting systems can compress the home buyers process timeline to as few as nine business days when documentation is complete and property conditions allow.

This speed advantage proves valuable in multiple-offer situations where sellers prioritize certainty and quick closings alongside purchase price.

Common Mistakes to Avoid

Learning from others' experiences helps you navigate the home buyers process more smoothly.

Frequent pitfalls include:

- Skipping pre-approval and house hunting beyond budget

- Making large purchases or changing jobs during processing

- Waiving inspections in competitive markets without expert guidance

- Failing to budget for ongoing maintenance and repairs

- Overlooking total monthly costs including HOA fees and utilities

- Not reading all documents thoroughly before signing

Working with experienced professionals throughout the 10-step home buying process helps you avoid these costly mistakes and make informed decisions at every stage.

Market-Specific Strategies for Greater Seattle

Understanding regional dynamics improves outcomes during the home buyers process in different neighborhoods.

Seattle and Bellevue

These markets feature high prices, limited inventory, and intense competition. Strong pre-approval, competitive down payments, and flexible terms often determine success. Consider properties in adjacent neighborhoods like Shoreline or Lake Forest Park for better value.

Redmond and Kirkland

Proximity to Microsoft and other tech employers drives demand. Properties move quickly, and buyer competition remains fierce. Understanding how to buy a home with local market expertise becomes essential.

Lynnwood, Mill Creek, and Everett

These areas offer relatively better affordability while maintaining reasonable commute access. Inventory levels typically exceed core Seattle neighborhoods, providing more negotiating leverage during the home buyers process.

Successfully navigating the home buyers process requires careful preparation, expert guidance, and strategic decision-making at every phase. Whether you're a first-time buyer establishing homeownership or a tech professional leveraging stock compensation for a jumbo purchase, understanding each step positions you for confident, informed decisions. Keith Akada brings over 25 years of experience helping buyers throughout Seattle, Bellevue, Redmond, Kirkland, and surrounding communities achieve their homeownership goals with transparency, education, and reliable execution. Ready to start your home buyers process with expert support? Connect with Mortgage Reel today for personalized guidance tailored to your unique situation.