Finding the best mortgage in Seattle's competitive 2026 housing market requires more than comparing interest rates. With median home prices exceeding $800,000 in neighborhoods from Capitol Hill to Bellevue and tech professionals leveraging RSUs and stock compensation for qualification, today's homebuyers need strategic guidance that accounts for loan type, closing speed, total cost, and qualification flexibility. Understanding which mortgage product aligns with your financial profile, timeline, and long-term goals can save tens of thousands of dollars while positioning you competitively against cash-heavy offers in Redmond, Kirkland, and surrounding communities.

Understanding What Makes the Best Mortgage for Your Situation

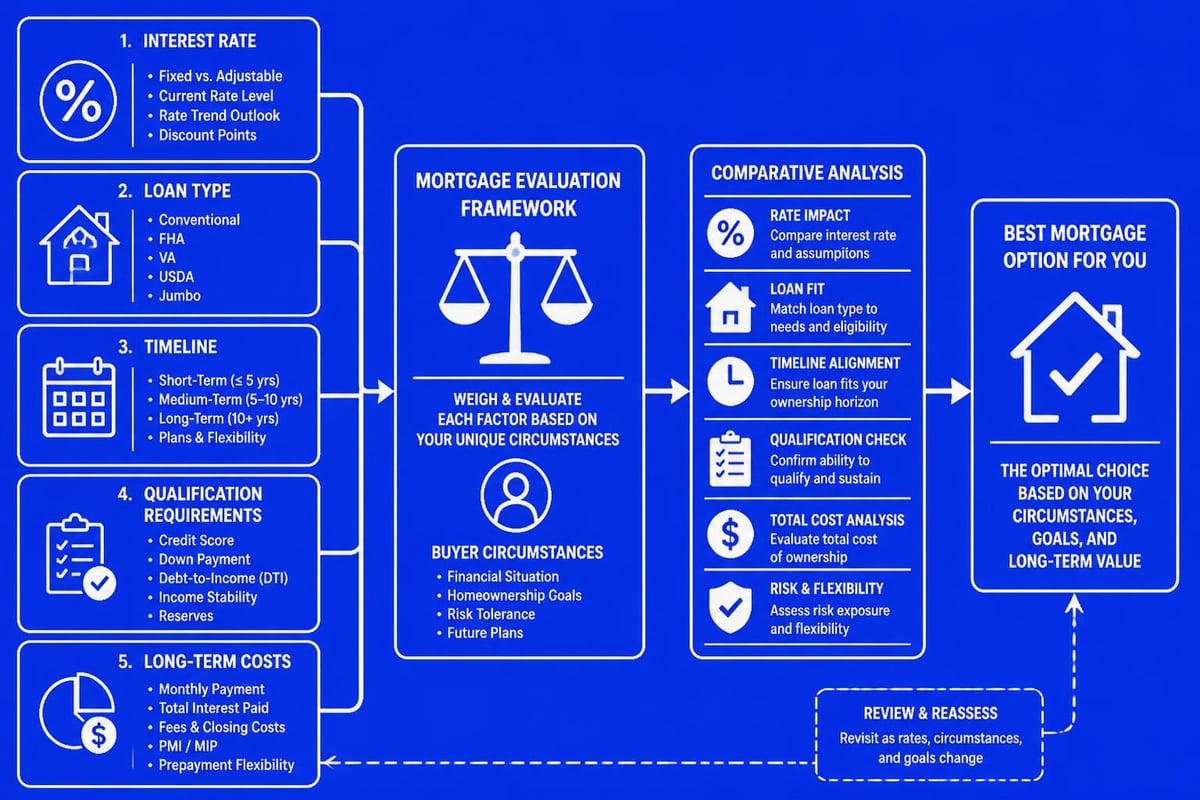

The best mortgage isn't determined by a single factor. Instead, it represents the optimal balance between interest rate, loan structure, qualification requirements, closing timeline, and total cost over the life of your loan.

Key Components of an Optimal Mortgage Decision

When evaluating mortgage options, Seattle homebuyers should assess multiple dimensions simultaneously:

- Interest rate competitiveness relative to current market conditions

- Loan-to-value ratio and down payment flexibility

- Closing timeline capabilities in fast-moving markets

- Qualification guidelines for unique income sources like RSUs, bonuses, and stock compensation

- Total interest paid over the projected ownership period

- Prepayment flexibility and refinance potential

The comparison of mortgage rates reveals that even a 0.25% rate difference on a $750,000 loan amounts to approximately $35,000 in additional interest over a 30-year term. However, focusing exclusively on rate while ignoring qualification strength or closing speed can result in lost opportunities in competitive Seattle neighborhoods.

Tech Industry Income and Mortgage Qualification

For Amazon, Microsoft, and Google employees throughout Seattle, Bellevue, and Redmond, understanding how lenders qualify stock-based compensation dramatically affects buying power. Many loan officers treat RSUs and bonuses conservatively, averaging historical income or excluding certain components entirely.

The best mortgage strategy for tech professionals involves working with specialists who can maximize qualification by properly documenting and underwriting:

- Restricted stock units with vesting schedules

- Performance bonuses with consistent payment history

- Stock options and equity compensation

- Sign-on bonuses with recurrence documentation

This specialized approach to jumbo home loans enables qualification at higher purchase prices without requiring disproportionately large down payments from liquid assets.

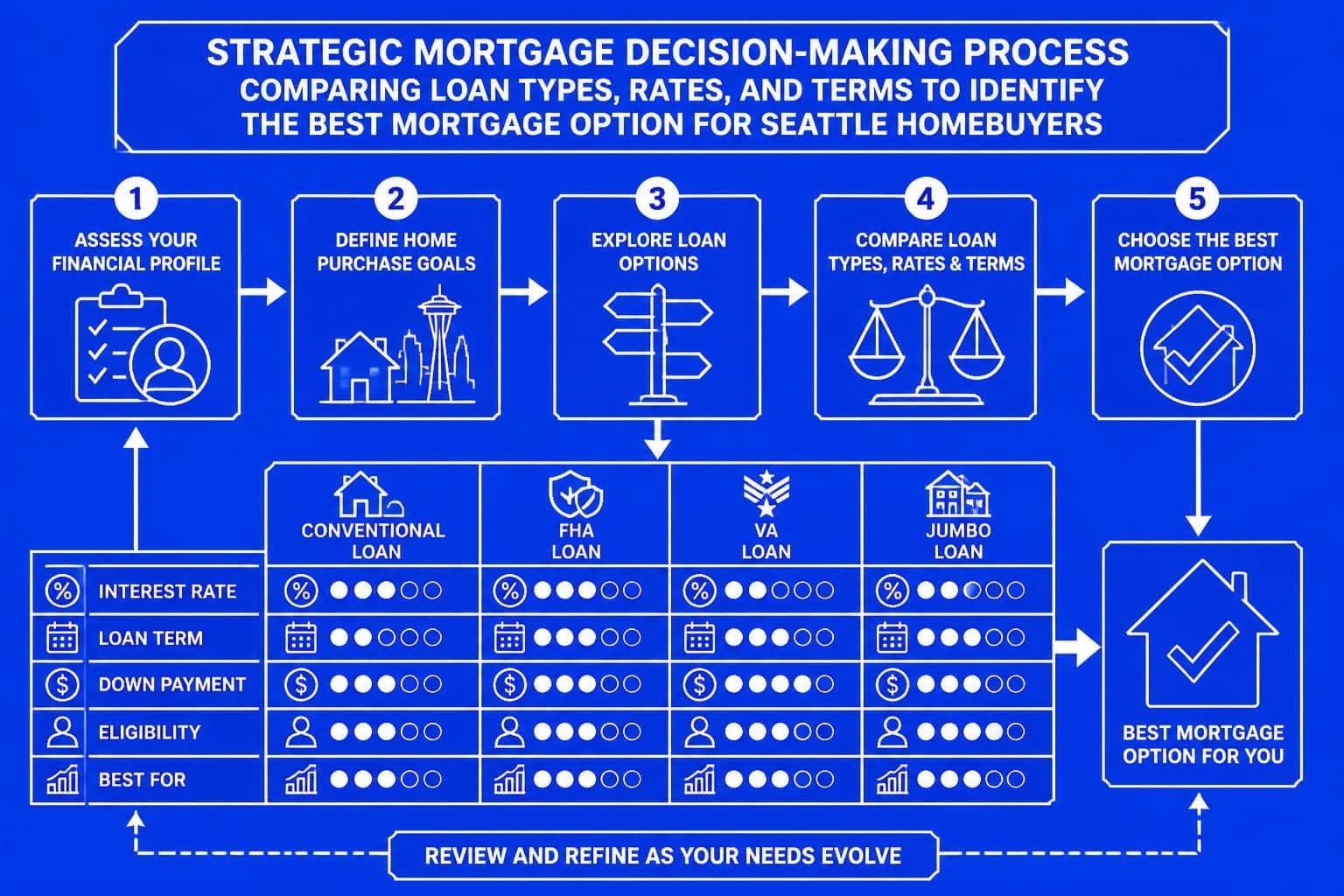

Comparing Primary Mortgage Types Available in 2026

Seattle homebuyers typically choose from four primary mortgage categories, each offering distinct advantages depending on down payment capacity, property type, and financial profile.

| Loan Type | Minimum Down Payment | Property Limit | Best For |

|---|---|---|---|

| Conventional | 3-5% (owner-occupied) | $806,500 (conforming) | Strong credit, standard income |

| FHA | 3.5% | $806,500 | Lower credit scores, minimal down payment |

| VA | 0% | No limit | Veterans, active military |

| Jumbo | 10-20% | Above conforming limits | High-value properties |

Conventional Loans: Flexibility and Competitive Pricing

Conventional mortgages remain the best mortgage choice for buyers with strong credit (680+), stable income documentation, and at least 5% down payment. These loans offer flexible qualification guidelines without government insurance premiums once you reach 20% equity.

For buyers in Shoreline, Lynnwood, and Mill Creek where median prices hover near conforming limits, conventional financing provides the straightest path to competitive offers with minimal ongoing costs. The ability to remove private mortgage insurance through appreciation or principal paydown creates long-term savings unavailable with FHA products.

Jumbo Loans for Seattle's Premium Markets

Properties exceeding $806,500 require jumbo financing, making loan officer expertise particularly valuable. The best jumbo mortgage programs in 2026 feature:

- Competitive rates within 0.125-0.375% of conforming pricing

- Down payment options as low as 10% for exceptional borrowers

- Sophisticated income qualification accommodating stock compensation

- Faster underwriting through specialized processing teams

Buyers targeting waterfront homes in Kirkland, executive properties in Bellevue, or luxury condos in downtown Seattle find that jumbo loan expertise directly impacts qualification amounts and negotiating strength.

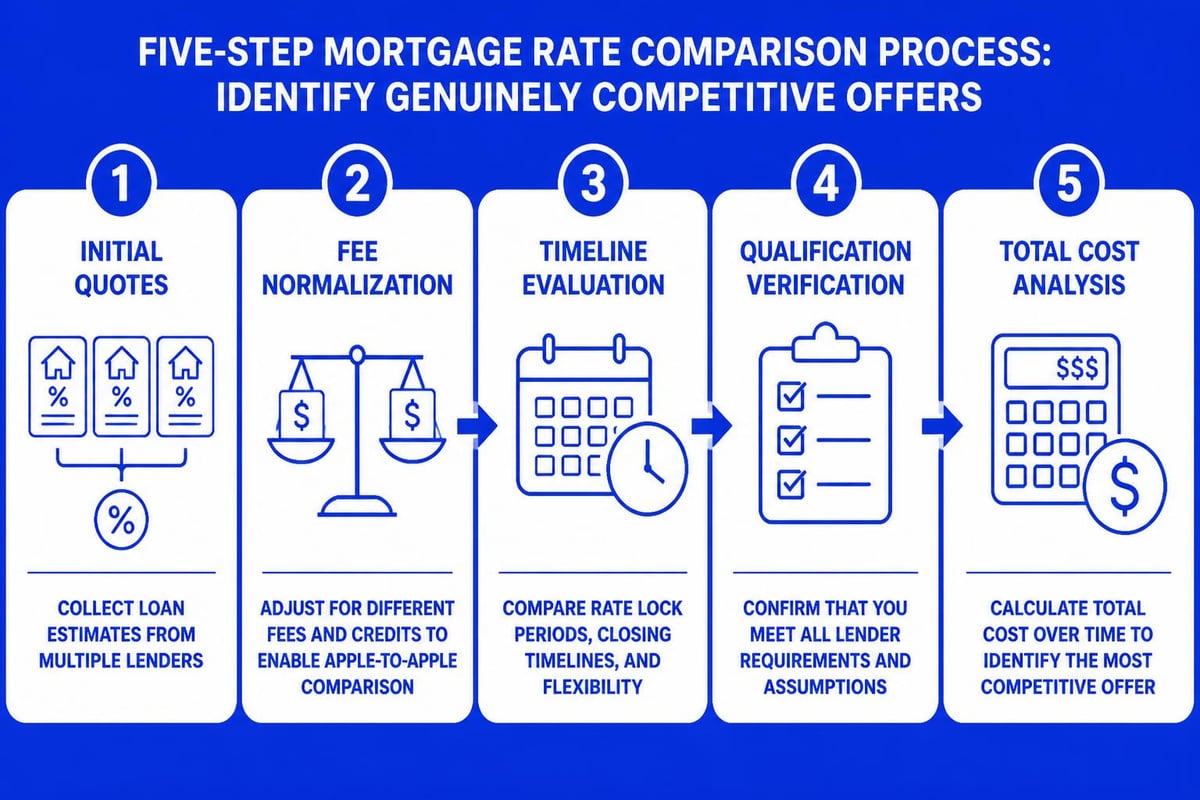

Strategic Rate Shopping Without Compromising Timeline

Shopping for mortgage rates effectively requires understanding the relationship between rate, points, and total closing costs. The best mortgage rate isn't always the lowest advertised number.

Understanding Rate Lock Strategy

In 2026's fluctuating rate environment, timing your rate lock represents a critical decision. Rate locks typically extend 30, 45, or 60 days, with longer periods carrying slightly higher costs.

Seattle's competitive market necessitates balancing rate protection with closing speed. Properties in Everett and Lake Forest Park often see multiple offers within 48 hours, making 9-business-day closing capabilities a differentiating factor that can justify accepting a marginally higher rate for execution certainty.

Rate Comparison Considerations

- Points and fees: One point equals 1% of loan amount and typically reduces rate by 0.25%

- Break-even timeline: Calculate months until rate reduction recoups upfront point costs

- Appraisal contingencies: Low rates mean nothing if valuation challenges delay closing

- Lock extension costs: Missing closing dates can add 0.125-0.25% in extension fees

The mortgage comparison tools available online provide starting points, but local market expertise ensures you're comparing apples-to-apples when evaluating lender quotes.

Preparation Steps That Secure the Best Mortgage Terms

Borrowers who prepare systematically before beginning their mortgage search consistently secure better terms and experience smoother transactions.

Credit Optimization Timeline

Six months before home shopping:

- Pull credit reports from all three bureaus

- Dispute any inaccuracies or outdated information

- Pay down revolving balances below 30% utilization

- Avoid opening new credit accounts

Three months before:

- Document all income sources with pay stubs and W-2s

- Organize two years of tax returns if self-employed

- Accumulate bank statements showing reserve requirements

- Gather RSU vesting schedules and bonus history for tech income

One month before:

- Obtain pre-approval with full documentation review

- Verify employment and income stability

- Finalize down payment and reserve fund sourcing

- Secure gift letters if receiving family assistance

This preparation enables competitive pre-approval letters that sellers and listing agents in Seattle's multiple-offer environment take seriously.

Documentation Requirements for Stock Compensation

Tech professionals seeking the best mortgage qualification should compile:

- Two years of W-2s showing base salary plus RSU income

- Detailed pay stubs reflecting current vesting schedule

- Stock account statements documenting recent sales and values

- Offer letters specifying ongoing equity compensation structure

- Vesting schedules for all outstanding grants

Lenders specializing in Seattle's tech market can often qualify 100% of vested RSUs and establish patterns for unvested compensation, dramatically increasing purchasing power compared to traditional underwriting approaches.

First-Time Buyer Considerations in the Seattle Market

First-time homebuyers in Seattle face unique challenges combining high property values with limited down payment funds. The best mortgage strategy often involves creative structuring rather than simply accepting starter loan programs.

Down Payment Assistance Programs

Washington State and King County offer several programs supporting first-time purchases:

- House Key Opportunity Loan: Second mortgage covering up to 4% of purchase price

- Home Advantage: Down payment assistance combined with competitive first mortgages

- County-specific programs: Income-qualified assistance in targeted neighborhoods

These programs work best when combined with conventional or FHA first mortgages, creating layered financing that minimizes upfront cash requirements while maintaining competitive offer strength.

FHA Loans: Benefits and Limitations

FHA financing allows 3.5% down payments with credit scores as low as 580, making homeownership accessible for buyers in Lynnwood, Mill Creek, and Shoreline who haven't accumulated substantial savings. However, the mortgage insurance structure requires careful evaluation.

| Feature | FHA Requirement | Impact |

|---|---|---|

| Upfront MIP | 1.75% of loan amount | Added to loan balance |

| Annual MIP | 0.55-0.85% ongoing | Permanent for <10% down |

| Removal | Refinance required | Cannot cancel via appreciation |

For buyers planning long-term ownership in appreciating Seattle markets, conventional loans with removable PMI often prove more economical despite higher credit requirements.

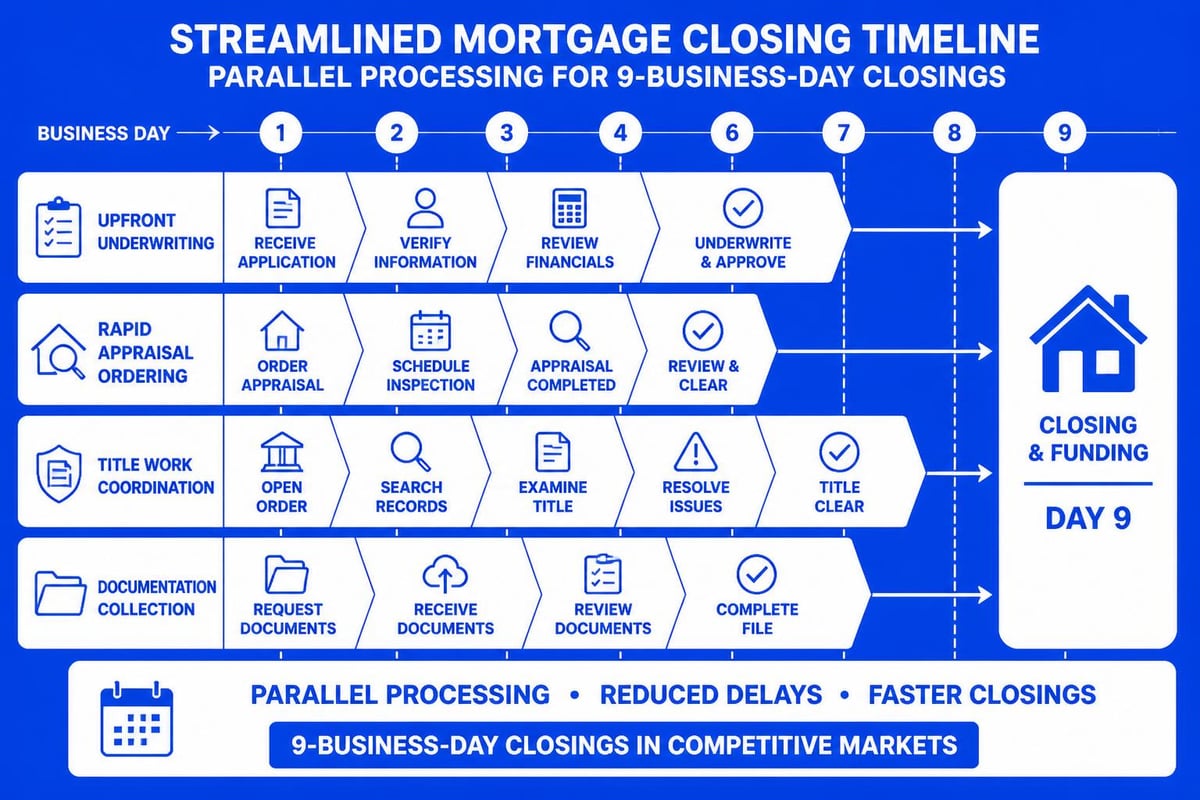

Closing Speed as a Competitive Advantage

In Seattle's inventory-constrained market, the ability to close in 9-15 business days transforms offer competitiveness. The best mortgage process combines thorough upfront underwriting with streamlined execution.

Pre-Underwriting Advantages

Full pre-underwriting before house hunting means:

- Complete file review including income, assets, and credit

- Preliminary title work reducing closing timeline surprises

- Appraisal management preparation for rapid ordering

- Conditions cleared before ratification when possible

This approach enables faster closings that appeal to sellers who have already purchased their next home or face timing pressures. In competitive neighborhoods from Capitol Hill to Bellevue, closing speed can compensate for offers $10,000-$20,000 below competing bids.

Relationship-Based Processing Benefits

Working with experienced mortgage brokers who maintain direct relationships with underwriters, processors, and appraisers creates efficiency unavailable through online-only platforms. When complications arise, direct communication resolves issues in hours rather than days.

This human element proves particularly valuable for complex scenarios involving:

- Non-traditional income documentation

- Multi-property portfolios

- Self-employment or variable compensation

- Properties requiring specialized appraisal approaches

Refinancing Strategy for Existing Seattle Homeowners

The best mortgage decision for current homeowners often involves strategic refinancing rather than maintaining original loans. With substantial equity appreciation across Seattle, Kirkland, Redmond, and Bellevue since 2020, refinance opportunities extend beyond simple rate reduction.

Cash-Out Refinance Applications

Homeowners with 20%+ equity can access appreciation through cash-out refinancing for:

- Investment property down payments in emerging neighborhoods

- Home renovations that further increase property value

- High-interest debt consolidation at mortgage rates

- Educational expenses or business investments

The key is ensuring the new rate and terms justify closing costs, typically 2-3% of the loan amount. Break-even calculations should account for planned ownership duration and alternative financing costs.

Rate-and-Term Refinance Timing

Pure rate-reduction refinances make sense when you can:

- Lower rate by at least 0.75% (covering costs within 24-36 months)

- Eliminate mortgage insurance by reaching 20% equity

- Shorten loan term to 15 years without excessive payment increases

- Switch from adjustable to fixed rates before adjustment periods

2026's rate environment favors homeowners who financed in late 2025 or maintain older loans originated above 6%. The current rate landscape creates opportunities for substantial long-term savings.

Working With Specialized Seattle Mortgage Professionals

The complexity of Seattle's market, particularly for tech professionals with equity compensation and buyers pursuing properties above conforming limits, makes specialized expertise valuable. The best mortgage outcomes typically involve collaboration with professionals who understand local market dynamics.

What to Look for in a Mortgage Broker

Evaluate potential mortgage advisors based on:

- Years of local market experience spanning multiple rate cycles

- Verified client reviews across multiple platforms demonstrating consistent performance

- Lender relationships enabling access to specialized programs

- Technology capabilities supporting rapid processing and communication

- Educational approach ensuring you understand all options and trade-offs

Professional mortgage guidance proves particularly valuable when navigating scenarios involving investment properties, self-employment income, or unique property types that require specialized underwriting knowledge.

Questions to Ask Potential Lenders

Before committing to a mortgage professional, clarify:

- How do you qualify RSUs and stock compensation?

- What's your average closing timeline for conventional and jumbo loans?

- Can you provide recent client references with similar financial profiles?

- Which wholesale lenders do you access for rate competitiveness?

- How do you handle appraisal challenges in competitive markets?

Transparent answers to these questions separate experienced professionals from transactional originators who may struggle with complex scenarios common in Seattle's tech-heavy market.

Investment Property Mortgage Strategies

Seattle real estate investors pursuing properties in Everett, Lake Forest Park, or emerging neighborhoods require different mortgage strategies than primary residence buyers. The best mortgage for investment properties balances qualification requirements with cash flow optimization.

Conventional Investment Loans

Non-owner-occupied financing typically requires:

- 15-20% down payment depending on credit strength and property count

- Six months reserves covering PITI on all financed properties

- Debt-to-income calculation including estimated rental income at 75% of market rent

- Property count limits affecting rates and qualification (1-4 properties vs. 5-10)

Experienced investors leverage portfolio loan options that accommodate higher property counts while maintaining competitive pricing through relationship-based underwriting.

DSCR Loans for Maximum Flexibility

Debt Service Coverage Ratio loans qualify based solely on rental income relative to mortgage payment, eliminating traditional income documentation requirements. These programs benefit:

- Self-employed investors with complex tax returns

- Buyers accumulating multiple properties rapidly

- High-income professionals reaching conventional loan limits

DSCR loans typically carry rates 0.50-1.00% above conventional investment loans but provide qualification flexibility unavailable through traditional channels.

Long-Term Cost Analysis Beyond Interest Rate

The best mortgage decision requires evaluating total cost of ownership over your expected holding period, not just monthly payment or interest rate.

Comprehensive Cost Components

| Cost Element | Impact Over 7 Years | Evaluation Priority |

|---|---|---|

| Interest paid | $150,000-$200,000 on $750K loan | High |

| Mortgage insurance | $35,000-$50,000 (if applicable) | Medium-High |

| Closing costs | $15,000-$22,500 (2-3%) | Medium |

| Prepayment penalties | $0-$15,000 (rare in 2026) | Low |

| Opportunity cost | Variable by alternative investments | High for investors |

This analysis becomes particularly important when deciding between buying down rates with points versus maintaining liquidity for renovations, reserves, or alternative investments in Seattle's appreciating market.

Tax Implications and Deductibility

For 2026, mortgage interest remains deductible on loans up to $750,000 for most Seattle homeowners. However, tax benefits vary significantly based on:

- Total itemized deductions relative to standard deduction ($30,000 married filing jointly)

- State and local tax deduction limits ($10,000 cap)

- Alternative Minimum Tax considerations for high earners

Sophisticated buyers coordinate with tax advisors to understand actual after-tax cost when comparing mortgage options, particularly for jumbo financing above deductibility limits.

Market-Specific Considerations Across Seattle Communities

The best mortgage strategy varies by target neighborhood based on price ranges, property types, and typical buyer profiles across Seattle's diverse communities.

Urban Core vs. Suburban Strategies

Downtown Seattle, Capitol Hill, Bellevue:

- Higher conforming and jumbo loan prevalence

- Condo financing requiring project certification

- HOA documentation and reserve study reviews

- Faster appreciation justifying lower down payments

Shoreline, Lynnwood, Mill Creek, Lake Forest Park, Everett:

- Stronger conventional loan presence

- Single-family homes with standard financing

- More first-time buyer activity

- Opportunity for investment property acquisition

Understanding these patterns helps buyers structure offers that align with seller expectations and competitive norms in specific neighborhoods.

Finding the best mortgage in 2026 requires balancing rate competitiveness with qualification strength, closing speed, and long-term cost optimization tailored to Seattle's unique market dynamics. Whether you're a tech professional leveraging stock compensation, a first-time buyer navigating high prices in Kirkland or Redmond, or an investor building a portfolio across greater Seattle, expert guidance transforms complex decisions into confident action. Keith Akada and the team at Mortgage Reel bring 25+ years of experience and 750+ five-star reviews helping Seattle-area buyers secure optimal financing with education, transparency, and execution that closes in as few as 9 business days.