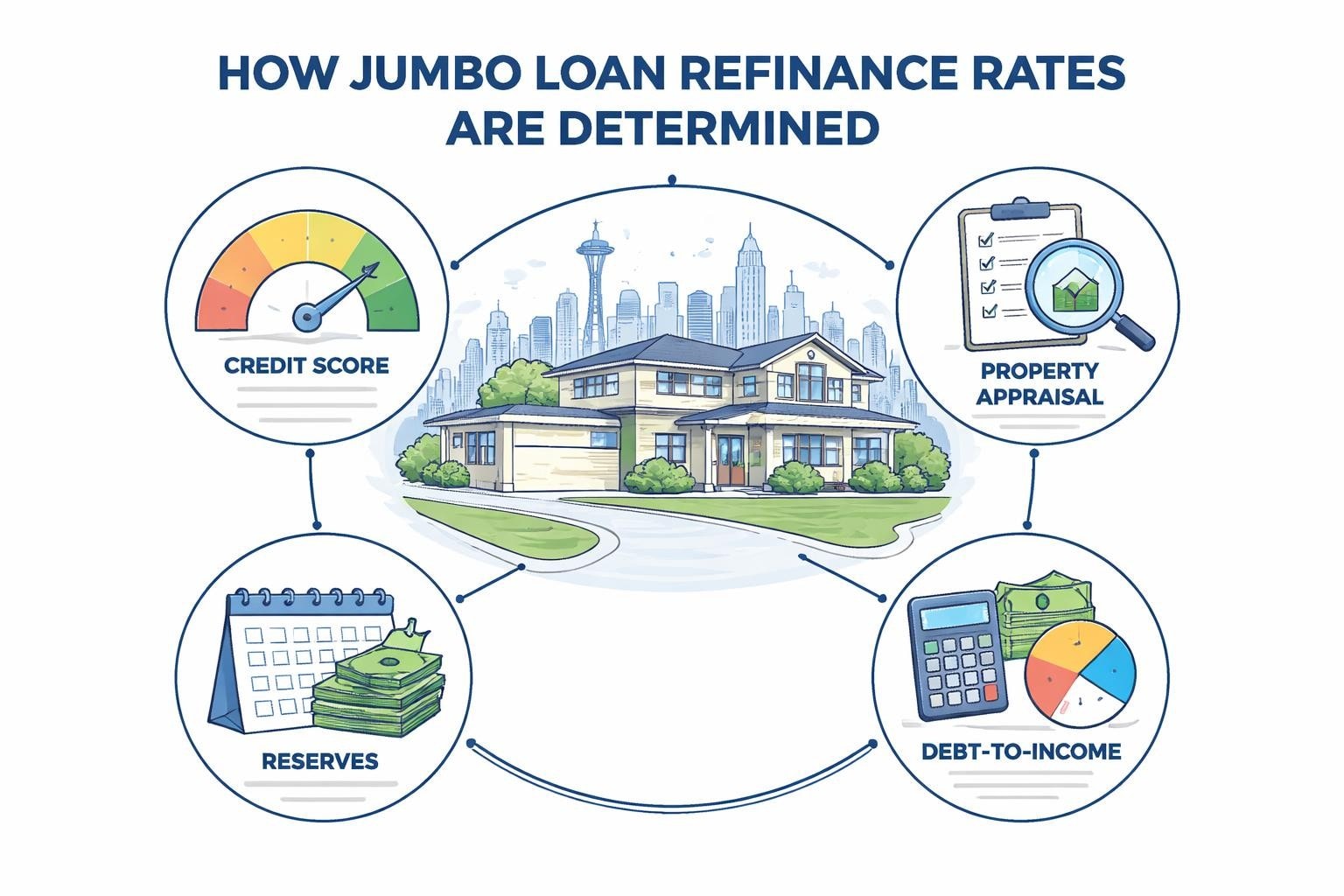

Refinancing a jumbo loan in Seattle's competitive real estate market requires strategic planning and a clear understanding of how lenders price high-balance mortgages. The jumbo loan refinance rate you receive depends on multiple factors including credit profile, property value, loan amount, and current market conditions. For homeowners in Seattle, Bellevue, Redmond, and Kirkland with properties exceeding conforming loan limits, understanding rate structures becomes essential to making informed refinance decisions. Tech professionals at Amazon, Microsoft, and Google frequently navigate jumbo refinancing as their compensation packages grow and property values appreciate in neighborhoods like Shoreline, Lynnwood, and Mill Creek.

Understanding Jumbo Loan Refinance Rates in 2026

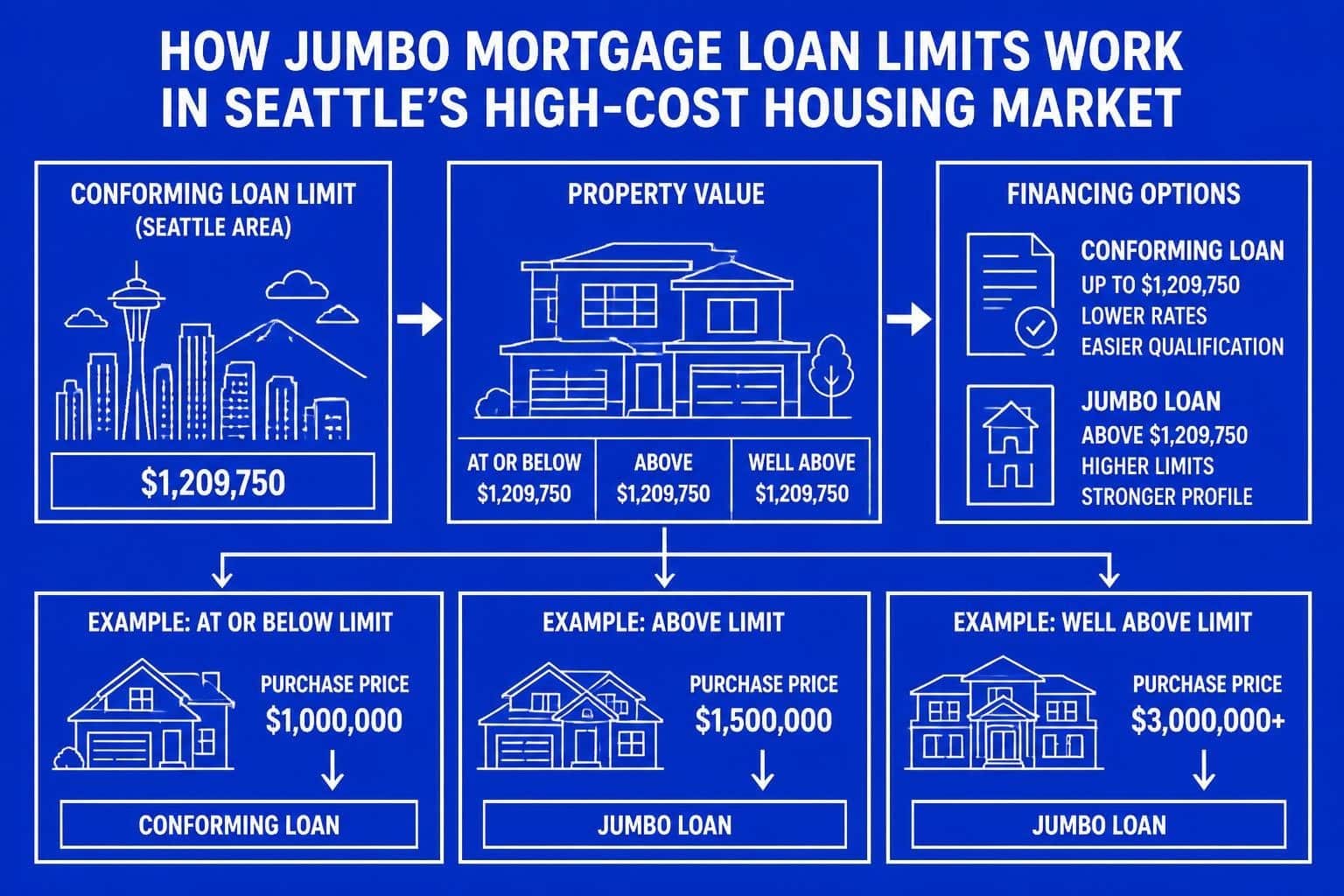

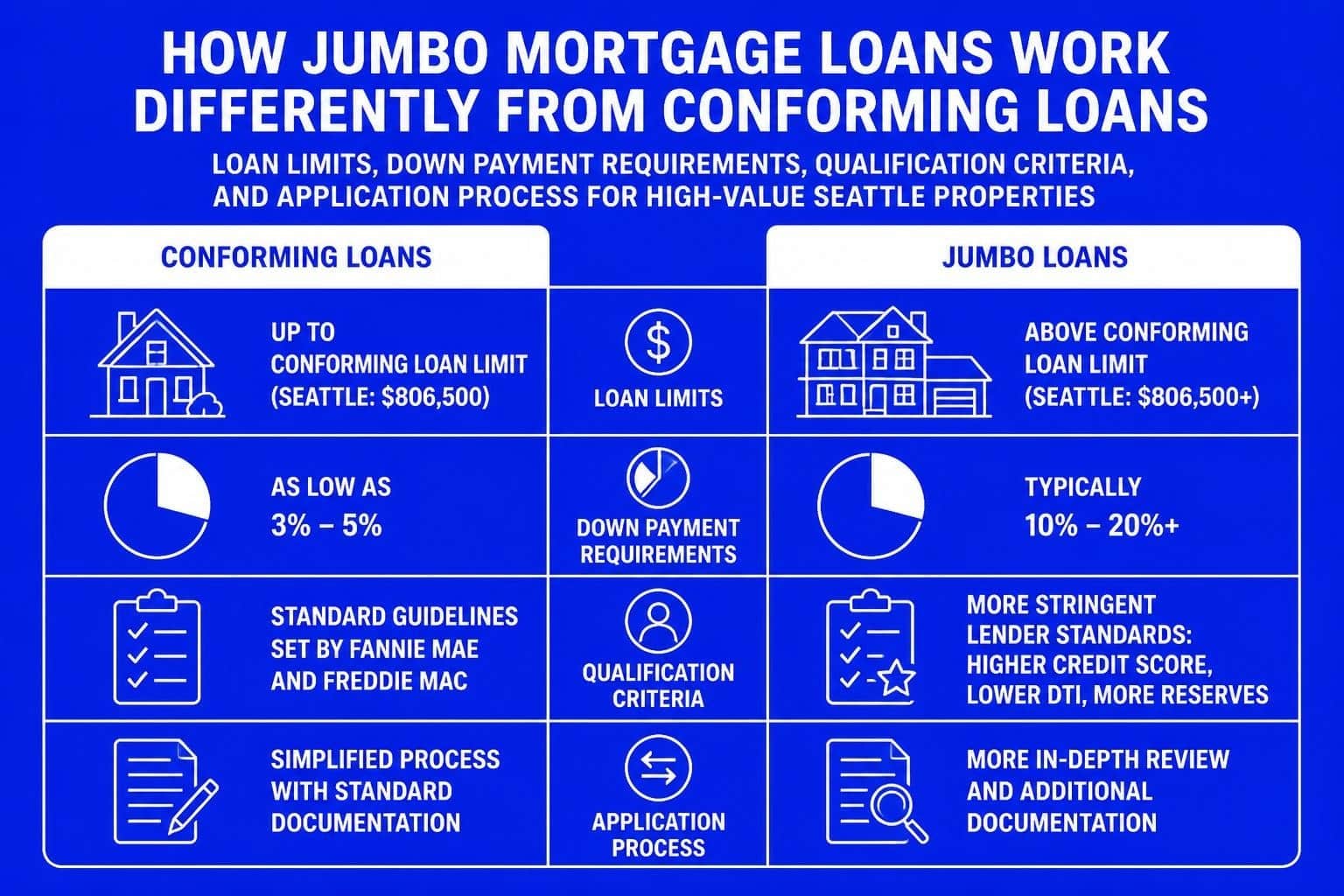

A jumbo loan refinance rate typically runs higher than conforming loan rates because lenders assume greater risk with larger loan amounts. In King County and Snohomish County, the 2026 conforming loan limit sits at $806,500 for single-family homes, meaning any mortgage above this threshold requires jumbo financing.

Current Rate Environment

Bankrate provides current jumbo refinance rates that reflect national trends, though Seattle-area rates may vary based on local market dynamics. Several factors influence the jumbo loan refinance rate landscape:

- Federal Reserve monetary policy and benchmark interest rate adjustments

- Bond market performance and investor demand for mortgage-backed securities

- Regional economic conditions specific to the Pacific Northwest

- Property type and location within the greater Seattle metropolitan area

- Loan-to-value ratios determined by current property appraisals

The spread between jumbo and conforming rates has narrowed considerably since 2020, with some lenders offering competitive jumbo programs that approach conventional pricing for well-qualified borrowers.

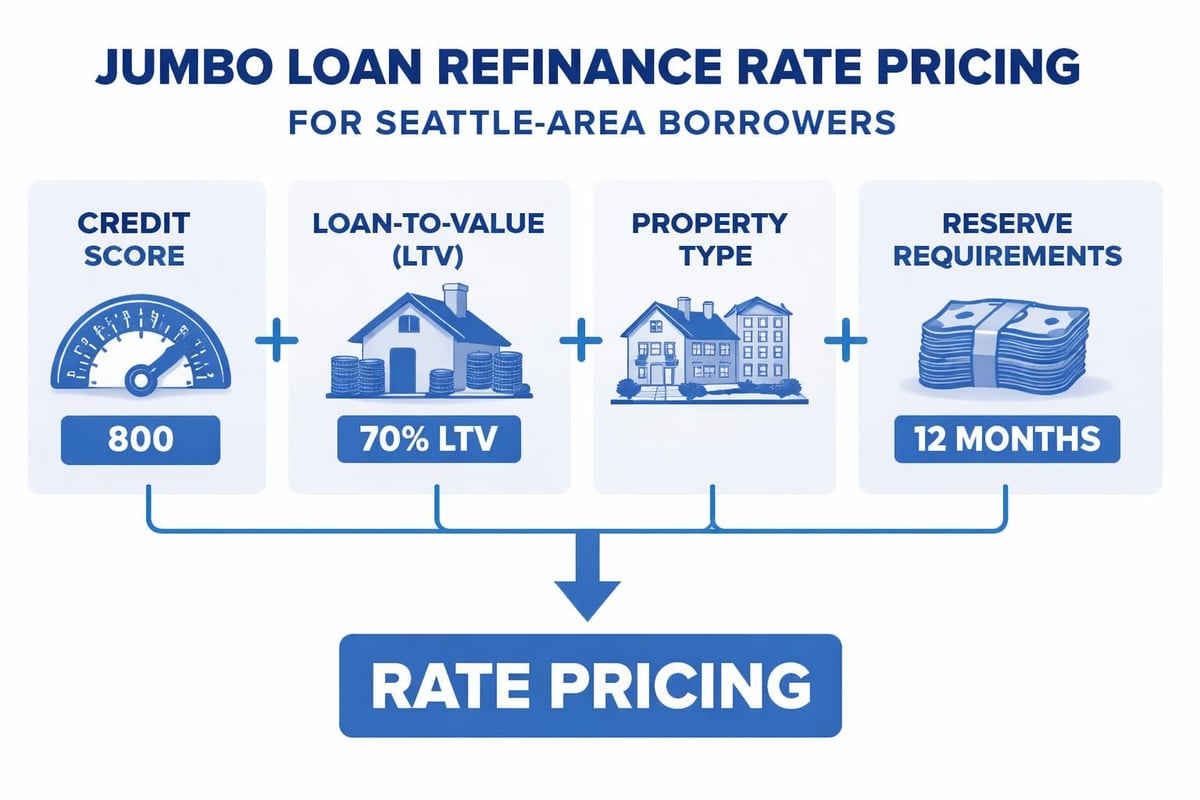

Rate Tiers and Pricing Adjustments

Lenders structure jumbo loan refinance rate pricing through a tiered system that rewards strong borrower profiles. Your rate gets determined by examining multiple risk factors simultaneously.

| Credit Score Range | Typical Rate Adjustment | LTV Impact |

|---|---|---|

| 740+ | Best available rates | Up to 80% LTV |

| 700-739 | +0.125% to +0.25% | Up to 75% LTV |

| 680-699 | +0.25% to +0.50% | Up to 70% LTV |

| Below 680 | Limited options | Below 70% LTV |

Property type also influences pricing. Single-family residences in Everett or Lake Forest Park receive more favorable rates than condos or investment properties. Cash-out refinances typically carry higher rates than rate-and-term refinances.

Qualifying for Competitive Jumbo Refinance Rates

Seattle-area homeowners seeking the best jumbo loan refinance rate must meet stricter qualification standards than conventional borrowers. Lenders examine your complete financial profile with heightened scrutiny.

Credit Requirements

Most jumbo lenders require minimum credit scores between 680 and 700, though rates improve significantly at 740 and above. For tech professionals with stock compensation, maintaining excellent credit becomes crucial when refinancing properties in Bellevue or Redmond that often exceed $1.5 million.

Review your credit reports from all three bureaus at least 90 days before applying. Address any errors, pay down revolving balances below 30% utilization, and avoid opening new credit accounts during the refinance process.

Documentation Standards

Jumbo refinances demand comprehensive documentation:

- Two years of personal tax returns with all schedules

- Two years of W-2s or 1099s showing consistent income

- Two months of bank statements for all accounts

- Investment account statements proving liquid reserves

- Current mortgage statement and property insurance declarations

- RSU vesting schedules for equity compensation (tech sector)

NerdWallet discusses the pros and cons of jumbo loans including these enhanced documentation requirements that separate jumbo products from conventional financing.

Income Verification for Stock Compensation

Amazon and Microsoft employees refinancing homes in Seattle face unique challenges when lenders evaluate RSU income. Your jumbo loan refinance rate depends partly on how effectively your mortgage broker structures and documents equity compensation.

Restricted stock units require specific treatment:

- Two-year average of vested RSUs typically counts toward qualifying income

- Recent grants may receive partial credit based on vesting schedule

- Stock price volatility gets factored into income calculations

- Tax withholding must be properly documented

Working with a Seattle mortgage broker experienced in tech compensation ensures maximum income consideration, potentially qualifying you for larger loan amounts at better rates.

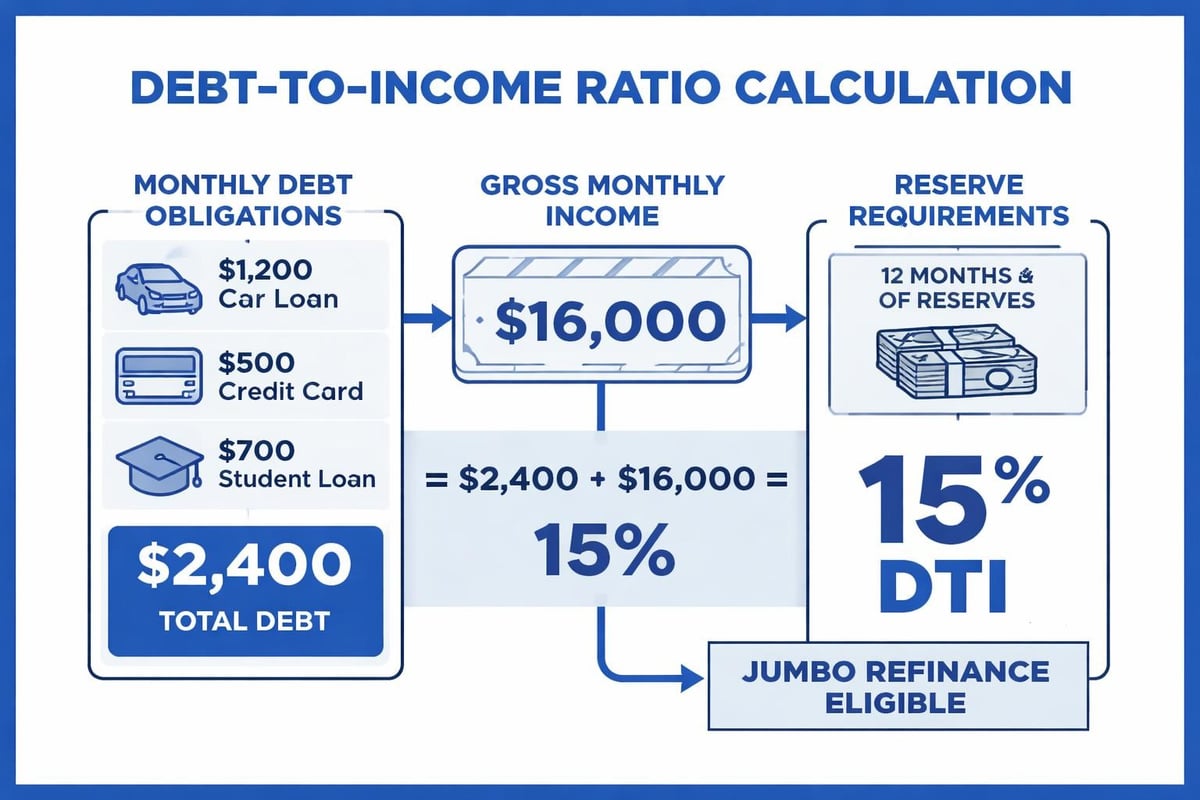

Debt-to-Income Ratios and Reserve Requirements

Your debt-to-income ratio (DTI) significantly impacts the jumbo loan refinance rate lenders offer. While conventional loans allow DTIs up to 50% in some cases, jumbo products typically cap at 43% to 45%.

Calculating Your DTI

Lenders divide your total monthly debt payments by gross monthly income. For a Seattle homeowner earning $20,000 monthly:

- Maximum housing payment at 43% DTI: $8,600

- Minus property taxes ($1,200), insurance ($300), HOA ($400)

- Maximum principal and interest payment: $6,700

This calculation determines borrowing capacity and influences rate pricing. Lower DTIs frequently unlock better rates.

Liquid Reserve Standards

Jumbo lenders require substantial cash reserves after closing. Expect requirements between 6 and 24 months of principal, interest, taxes, and insurance (PITI) payments, depending on loan amount and property type.

For a $1.2 million refinance in Shoreline with $7,500 monthly PITI:

- 12-month reserve requirement: $90,000 in liquid assets

- Acceptable sources include checking, savings, investment accounts, and vested retirement funds

- Pending RSU vesting may count with proper documentation

Strong reserves demonstrate financial stability and can improve your jumbo loan refinance rate by reducing perceived lender risk.

Strategic Timing for Jumbo Refinancing

Market timing significantly affects the jumbo loan refinance rate available to Seattle homeowners. Understanding economic indicators helps identify optimal refinancing windows.

Rate Monitoring and Lock Strategies

Daily rate volatility requires active monitoring during your refinance process. Rates can shift based on:

- Federal Reserve announcements and economic projections

- Employment data releases (first Friday monthly)

- Inflation reports and consumer price index data

- Treasury yield movements in bond markets

Consider current refinance rate trends when deciding whether to lock immediately or float. Most lenders offer lock periods between 30 and 60 days, with longer locks sometimes carrying pricing adjustments.

Break-Even Analysis

Calculate your break-even point before refinancing. Divide total closing costs by monthly payment savings to determine months until you recover expenses.

Example for a Lynnwood homeowner:

- Current payment (P&I): $6,800 at 4.5%

- New payment (P&I): $6,200 at 3.75%

- Monthly savings: $600

- Total closing costs: $18,000

- Break-even period: 30 months

If you plan to keep the property beyond 30 months, refinancing makes financial sense even if the jumbo loan refinance rate seems only marginally better.

Comparing Lender Options and Programs

Not all lenders price jumbo loans identically. Seattle homeowners should compare multiple options to secure the most competitive jumbo loan refinance rate.

Portfolio Lenders vs. Agency Lenders

Portfolio lenders hold loans on their balance sheets rather than selling to investors. This structure allows greater flexibility in underwriting but may result in higher rates. Agency-adjacent lenders follow Fannie Mae and Freddie Mac guidelines closely, even for jumbo products, offering more predictable pricing.

U.S. Bank outlines their jumbo refinance options as an example of traditional bank portfolio lending, while mortgage brokers access multiple wholesale lenders simultaneously.

Broker Advantages in Rate Shopping

Working with an experienced broker provides access to numerous lender programs without multiple credit inquiries. A top Seattle mortgage broker can:

- Compare 20+ lender rate sheets daily for optimal pricing

- Match your profile to lenders offering the best jumbo loan refinance rate

- Negotiate pricing adjustments based on your credit strength

- Expedite underwriting through established lender relationships

- Close quickly (potentially in 9 business days with select lenders)

Tech professionals in Mill Creek or Everett benefit particularly from brokers who understand RSU qualification, as specialized knowledge directly impacts approval odds and rate competitiveness.

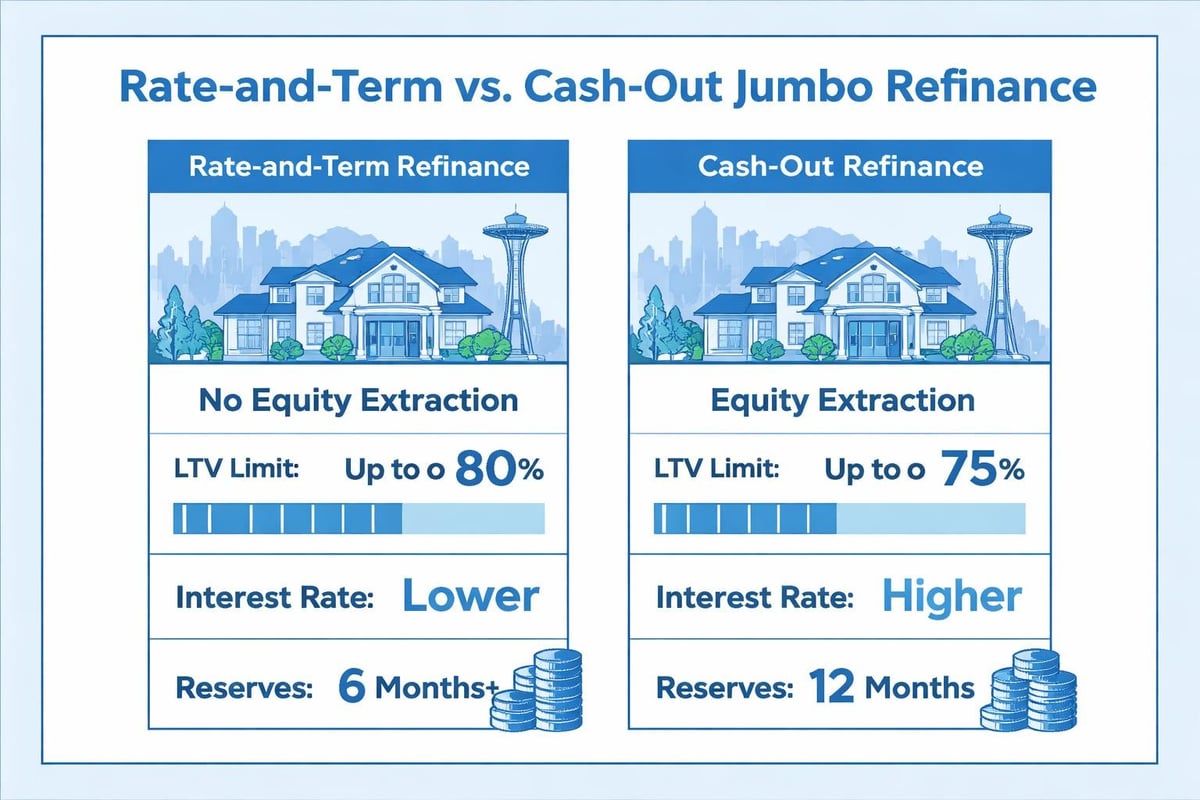

Rate-and-Term vs. Cash-Out Refinancing

Your refinance objective influences both qualification requirements and the jumbo loan refinance rate you receive. Understanding these distinctions helps set realistic expectations.

Rate-and-Term Refinancing

This straightforward refinance pays off your existing mortgage with a new loan at better terms. Lenders view rate-and-term refinances favorably because you're not extracting equity.

Benefits include:

- Lower rates compared to cash-out options

- Simplified underwriting in some cases

- More flexible LTV allowances (up to 80% in many programs)

- Reduced closing costs due to smaller loan amounts

Seattle homeowners looking to reduce monthly payments or shorten loan terms find rate-and-term refinancing most cost-effective.

Cash-Out Refinancing

Extracting equity for home improvements, debt consolidation, or investment opportunities requires cash-out refinancing. Lower.com explains how refinancing a jumbo loan works, including cash-out scenarios where borrowers access accumulated home equity.

Key differences:

| Feature | Rate-and-Term | Cash-Out |

|---|---|---|

| Maximum LTV | 80% | 70-75% |

| Rate pricing | Best available | +0.25% to +0.50% |

| Reserve requirements | 6-12 months | 12-18 months |

| Documentation | Standard | Enhanced |

A Bellevue homeowner with $500,000 in equity might refinance at 70% LTV, receiving $150,000 cash while maintaining a $1.05 million mortgage on a $1.5 million property.

Closing Costs and Fee Structures

Jumbo loan refinances carry substantial closing costs due to higher loan amounts and enhanced underwriting. Understanding fee structures helps you evaluate total refinancing costs beyond just the jumbo loan refinance rate.

Typical Cost Breakdown

For a $1.2 million jumbo refinance in Redmond:

- Origination fee: 0.5% to 1% ($6,000 to $12,000)

- Appraisal fee: $600 to $1,200 (complex properties higher)

- Title insurance: $3,500 to $5,000 (based on loan amount)

- Escrow and recording fees: $1,500 to $2,500

- Credit report and miscellaneous: $500 to $800

- Prepaid property taxes and insurance: Varies by timing

Total costs typically range from $15,000 to $25,000, or 1.25% to 2% of the loan amount.

No-Closing-Cost Options

Some lenders offer no-closing-cost refinances where fees get built into the rate or loan amount. Your jumbo loan refinance rate increases approximately 0.25% to 0.50%, but you avoid upfront expenses.

This strategy works best when:

- You have limited liquidity despite strong income

- You plan to refinance again within 3-5 years

- Current rates are significantly lower than your existing mortgage

- You want to preserve cash for other investments

Property Appraisal Considerations

Accurate property valuation directly impacts your loan-to-value ratio and the jumbo loan refinance rate offered. Seattle's unique real estate market presents specific appraisal challenges.

Market Volatility Factors

King County home values fluctuate based on tech sector employment, interest rates, inventory levels, and broader economic conditions. An appraisal conducted during a market downturn might show less equity than expected, affecting your:

- Available loan amount

- Rate tier qualification

- Cash-out proceeds (if applicable)

- PMI requirements (rare but possible on high LTV jumbos)

Properties in Lake Forest Park or Shoreline with significant custom features require appraisers experienced in luxury home valuation to accurately capture property worth.

Preparing for Appraisal Success

Maximize your appraised value through strategic preparation:

- Complete deferred maintenance and cosmetic updates

- Provide comparable sales data from your neighborhood

- Document recent renovations with permits and receipts

- Ensure property access for thorough interior inspection

- Highlight unique features that justify premium pricing

A higher appraisal strengthens your LTV ratio, potentially moving you into a better rate tier and reducing your jumbo loan refinance rate by 0.125% to 0.25%.

Tax Implications of Jumbo Refinancing

Understanding tax treatment of mortgage interest helps Seattle homeowners calculate true refinancing costs and benefits.

Mortgage Interest Deduction Limits

The Tax Cuts and Jobs Act limits mortgage interest deductions to interest on $750,000 of acquisition debt for married couples filing jointly ($375,000 for single filers). This cap affects many jumbo borrowers in Seattle's high-value market.

Important considerations:

- Only interest on debt used to buy, build, or substantially improve your home qualifies

- Refinancing to pay off credit cards or fund college doesn't create deductible interest

- Washington State has no income tax, but federal deductions still matter

- Consult a CPA about your specific situation before refinancing

Points and Origination Fee Deductibility

Discount points paid to reduce your jumbo loan refinance rate may be tax-deductible, though different rules apply to refinances versus purchases:

- Purchase points are fully deductible in the tax year paid

- Refinance points must be amortized over the loan term

- One point on a $1 million 30-year refinance creates $33 annual deduction

Track these expenses carefully and work with tax professionals familiar with high-net-worth mortgage financing.

Alternative Refinancing Strategies

Beyond traditional refinancing, Seattle homeowners have additional options worth exploring depending on goals and circumstances.

ARM to Fixed Rate Conversions

If your jumbo loan uses an adjustable-rate mortgage (ARM) structure, converting to fixed-rate financing locks in predictable payments. This strategy makes sense when:

- Your ARM adjustment period is approaching

- Fixed rates remain historically low

- You plan long-term ownership (10+ years)

- Payment stability outweighs potential rate decreases

Refi.com provides an overview of jumbo mortgage rates including ARM and fixed-rate comparisons that help inform conversion decisions.

Portfolio Restructuring with Multiple Properties

Tech professionals in Kirkland or Bellevue often own multiple properties including primary residences, vacation homes, and investment properties. Strategic refinancing across your portfolio might involve:

- Refinancing the primary residence at the lowest jumbo loan refinance rate available

- Extracting equity for investment property down payments

- Consolidating multiple property mortgages with a single lender for relationship pricing

- Timing refinances to maximize tax benefits across properties

This advanced approach requires careful coordination with mortgage, tax, and investment advisors.

Hybrid Refinancing Approaches

Some borrowers benefit from splitting large mortgages into conforming and jumbo pieces. For a $1.2 million refinance:

- First mortgage: $806,500 (conforming limit)

- Second mortgage: $393,500 (jumbo)

This structure potentially provides:

- Lower blended rate compared to single jumbo mortgage

- Conforming loan advantages on the larger first mortgage

- Flexibility to pay off the smaller second mortgage early

However, two separate loans mean two sets of closing costs and monthly payments, requiring careful cost-benefit analysis.

Making Your Refinance Decision

Refinancing a jumbo loan requires balancing multiple factors beyond simply securing the lowest jumbo loan refinance rate. Seattle homeowners should evaluate:

Personal Financial Goals Alignment

Your refinance should support broader financial objectives. Consider whether you're trying to:

- Reduce monthly obligations to improve cash flow for other investments

- Shorten the loan term to build equity faster and save interest long-term

- Access equity for home improvements that increase property value

- Consolidate debt at lower interest rates than credit cards or personal loans

- Eliminate PMI if your original loan included mortgage insurance

Each goal suggests different refinance structuring. A Mill Creek homeowner focused on cash flow prioritizes the lowest possible payment, while an Everett investor building a rental portfolio might optimize for equity access despite higher rates.

Life Stage and Property Plans

How long you plan to keep the property fundamentally affects refinancing wisdom. Seattle's competitive market means properties often appreciate significantly, but career changes, family growth, or retirement plans might alter your timeline.

Run scenarios comparing:

- Current mortgage maintained through expected ownership period

- Refinanced mortgage with lower rate but closing costs factored

- Alternative investments if you kept current mortgage and invested the cash saved

The analysis frequently reveals that even small rate improvements justify refinancing when you're staying 5+ years.

Understanding jumbo loan refinance rates empowers Seattle-area homeowners to make strategic financing decisions that align with both immediate needs and long-term wealth building. Whether you're a tech professional leveraging stock compensation or a seasoned investor optimizing your real estate portfolio, securing competitive rates requires expertise in complex underwriting, local market knowledge, and lender relationship management. Keith Akada at Mortgage Reel brings 25+ years of experience helping clients across Seattle, Bellevue, Redmond, Kirkland, Shoreline, Lynnwood, and surrounding communities navigate jumbo refinancing with transparency, strategy, and the ability to close in as few as 9 business days through Fairway's advanced underwriting platform.