When you're ready to buy a home in Seattle, Shoreline, or Bellevue, understanding who handles your mortgage can make the difference between a smooth closing and a frustrating experience. The mortgage industry has several key players, and one term you'll frequently encounter is "mortgage banker." While many homebuyers use this term interchangeably with mortgage broker or loan officer, these roles serve distinctly different functions in the lending ecosystem. A mortgage banker works directly for a lending institution, originating and funding loans using the bank's own capital, while other professionals may shop your loan across multiple lenders. For Seattle-area homebuyers-especially tech professionals navigating stock compensation or jumbo loan scenarios-knowing which type of mortgage professional suits your needs can significantly impact your interest rate, closing timeline, and overall experience.

What Is a Mortgage Banker and How Do They Operate

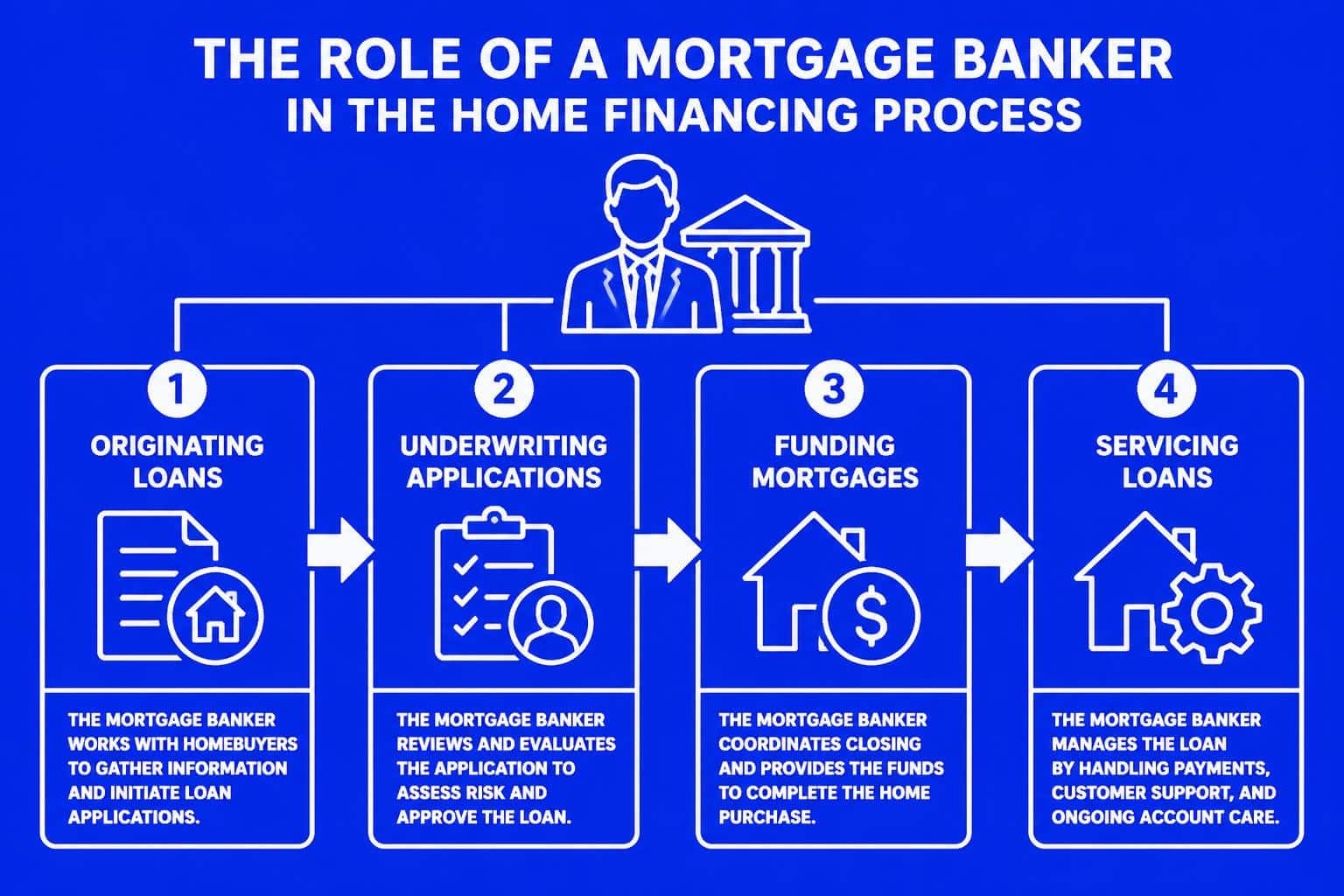

A mortgage banker is a lending professional who represents a specific financial institution and originates mortgage loans using that institution's funds. Unlike brokers who act as intermediaries, mortgage bankers work directly for lenders, handling the entire loan process from application through closing and often servicing the loan after funding.

Key responsibilities of a mortgage banker include:

- Evaluating borrower qualifications and financial documentation

- Originating loans according to their institution's specific guidelines

- Submitting applications to their in-house underwriting department

- Funding loans using the bank's capital reserves

- Often servicing the loan or selling it on the secondary market

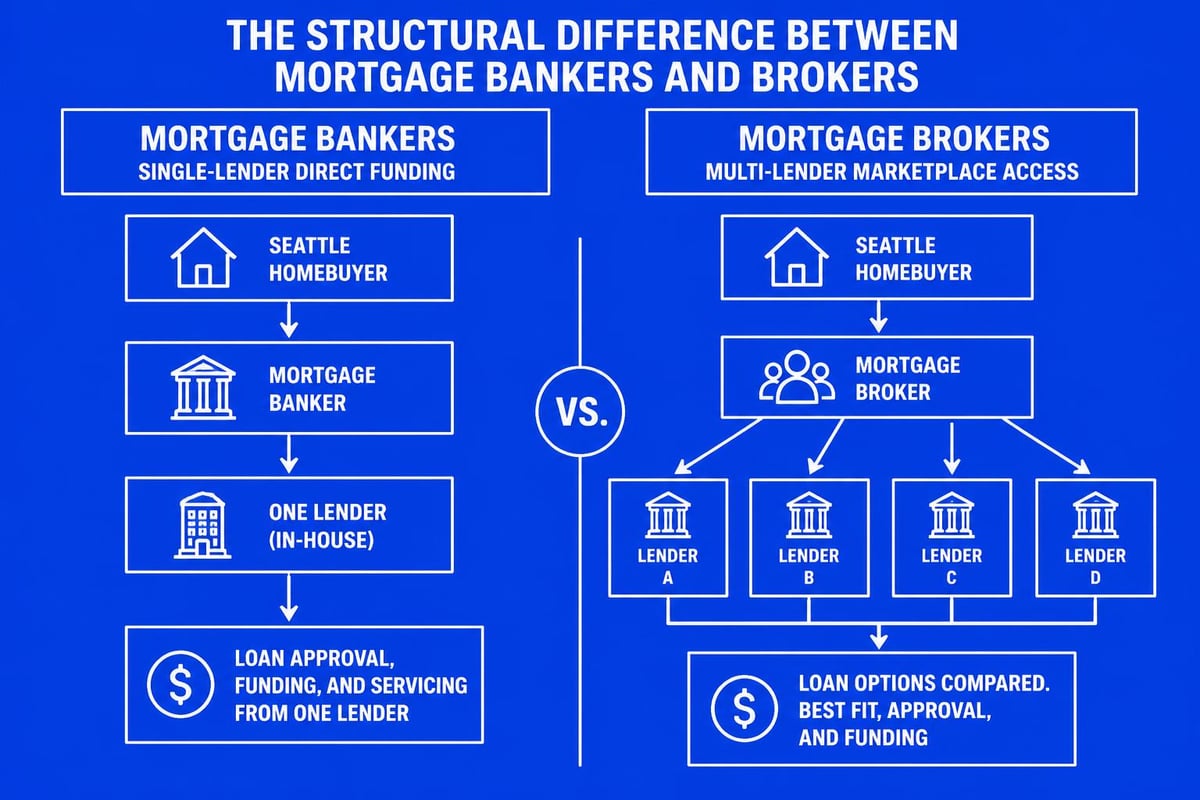

The fundamental difference lies in the source of funding. A mortgage banker has direct access to their institution's lending capital and decision-making authority. When you work with a mortgage banker at Wells Fargo or Chase, for example, you're working with someone who can only offer that specific bank's products and rates.

How Mortgage Bankers Differ From Brokers

Understanding the distinction between mortgage brokers and lenders becomes critical when choosing your financing partner in competitive Seattle neighborhoods like Capitol Hill or Kirkland. These differences extend beyond simple terminology to affect your rate, product options, and closing experience.

| Feature | Mortgage Banker | Mortgage Broker |

|---|---|---|

| Funding Source | Institution's own capital | Multiple lender partners |

| Product Options | Single lender's products | Multiple lenders' products |

| Rate Control | Sets rates per bank policy | Negotiates with lenders |

| Underwriting | In-house department | Third-party lenders |

| Compensation | Salary plus commission | Commission from lenders |

A mortgage banker represents one lending institution exclusively. They cannot shop your application to competing lenders or negotiate between multiple underwriting teams. This limitation can be advantageous when that specific lender offers the best product for your situation-such as a tech professional needing RSU income qualification-but restrictive when you'd benefit from comparing multiple options.

In contrast, mortgage brokers work with multiple wholesale lenders, accessing a broader range of products and potentially securing better rates through lender competition. For Seattle homebuyers with complex income situations-like Microsoft employees with significant stock compensation or real estate investors seeking portfolio loans-the broker model often provides more flexibility.

Advantages of Working With a Mortgage Banker

Choosing a mortgage banker offers specific benefits that appeal to certain borrower profiles and transaction scenarios. These advantages become particularly relevant in fast-moving markets like Bellevue and Redmond, where execution speed matters.

Streamlined communication represents the primary benefit. When your loan officer, underwriter, and funding source all work for the same institution, information flows directly without third-party intermediaries. This structure eliminates the coordination challenges that can delay underwriting decisions or create miscommunication between parties.

Speed and Direct Decision-Making Authority

Mortgage bankers often deliver faster closing timelines because they control the entire process internally. Without waiting for third-party lender approvals or coordinating between separate institutions, decisions happen more quickly. For Seattle buyers competing in multiple-offer situations, this speed advantage can prove decisive.

Additional advantages include:

- Single point of contact throughout the loan process

- Potential relationship benefits for existing bank customers

- In-house underwriting reduces approval uncertainty

- Direct access to senior underwriters for complex scenarios

- Simplified documentation requirements when banking relationship exists

For Mill Creek or Lynnwood buyers with straightforward financial profiles-W-2 income, strong credit, conventional down payments-a mortgage banker's streamlined approach often provides the fastest path to closing. The efficiency gains become measurable when you're trying to close in competitive timeframes.

However, this efficiency comes with trade-offs. Because mortgage bankers represent a single institution, they cannot offer rate comparisons or product alternatives from competing lenders. If their bank's guidelines exclude your income type or property situation, they cannot pivot to alternative lenders with more flexible criteria.

When a Mortgage Banker May Not Be Your Best Option

Despite their advantages, mortgage bankers face inherent limitations that can disadvantage certain borrower situations. Understanding these constraints helps Seattle-area homebuyers make informed decisions about their lending partner.

The most significant limitation involves product selection. A mortgage banker can only offer their institution's specific loan programs, rates, and underwriting guidelines. When comparing mortgage brokers to banks, this restriction becomes apparent-bankers sacrifice breadth for depth.

Scenarios where mortgage bankers face challenges:

- Complex income documentation: Self-employed borrowers, commission-based income, or multiple income streams may not fit rigid bank guidelines

- Non-traditional properties: Investment properties, condos with litigation, or unique structures often require specialized lenders

- Credit challenges: Past credit events may fall outside a specific bank's acceptable risk parameters

- Jumbo loan scenarios: Not all banks offer competitive jumbo products or understand Seattle's high-cost market nuances

- VA or specialized government loans: Some banks limit or don't offer certain government-backed programs

For Lake Forest Park or Everett buyers working with complex compensation structures-think Amazon employees with substantial RSU income or real estate investors juggling multiple properties-a mortgage banker's single-lender limitation can become problematic. These situations often benefit from working with a broker who can navigate multiple lenders to find the optimal fit.

Rate Competition and Market Positioning

Mortgage bankers set rates based on their institution's funding costs, overhead structure, and market positioning strategy. Without competition from other lenders on your specific application, you may not receive the most aggressive pricing available in the market.

| Consideration | Mortgage Banker Impact | Alternative Approach |

|---|---|---|

| Rate Shopping | Limited to one lender's rates | Broker compares multiple lenders |

| Fee Structures | Bank's standard fee schedule | Potential negotiation across lenders |

| Underwriting Flexibility | Single guideline interpretation | Multiple underwriting perspectives |

| Program Availability | Bank's product menu only | Access to niche or specialized products |

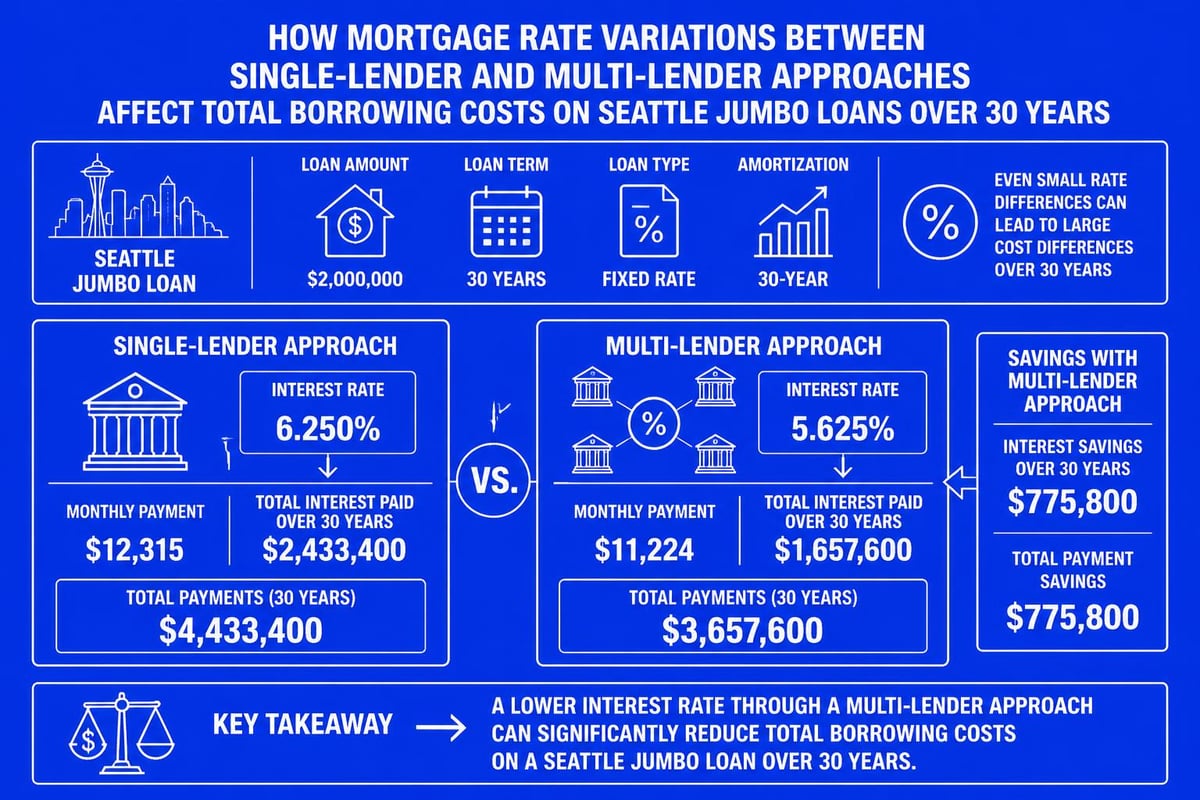

The rate difference may seem minor-perhaps 0.125% to 0.25%-but on a Seattle jumbo loan of $1.2 million, that translates to $1,500 to $3,000 in annual interest. Over a 30-year mortgage, these seemingly small differences compound significantly.

Understanding the Mortgage Banker Role in Your Transaction

When you choose to work with a mortgage banker, understanding their specific responsibilities and limitations helps set realistic expectations for your home financing journey. This knowledge proves especially valuable during time-sensitive decisions or when unexpected challenges arise.

A mortgage banker serves as your primary contact from application through closing, but they operate within their institution's established framework. They cannot override underwriting guidelines, offer products their bank doesn't provide, or negotiate rates outside their authorized parameters.

Throughout your transaction, your mortgage banker will:

- Collect and review all financial documentation

- Enter your application into their lending system

- Submit your file to their underwriting department

- Coordinate with their processor and closer

- Clear underwriting conditions using bank-approved documentation

- Schedule closing with their title and escrow partners

This vertical integration creates efficiency but also constrains flexibility. When an underwriter requests additional documentation or questions income calculation, your mortgage banker advocates within their system but cannot simply move your file to a more flexible lender.

The Pre-Approval Process With a Mortgage Banker

Obtaining pre-approval from a mortgage banker follows a structured process governed by their specific institution's requirements. For Shoreline or Bellevue buyers entering competitive markets, understanding this process helps you gauge timeline expectations and documentation needs.

The typical mortgage banker pre-approval workflow includes:

- Initial consultation and needs assessment

- Credit report authorization and review

- Income and asset documentation submission

- Debt-to-income ratio calculation

- Underwriter review of submitted documentation

- Pre-approval letter issuance with specific conditions

Because mortgage bankers work within a single underwriting framework, their pre-approval letters often carry weight with sellers who recognize established brand names. A pre-approval from a major bank signals financial stability and lending commitment, though experienced brokers can provide equally strong pre-approvals when backed by reputable wholesale lenders.

The critical question becomes whether the mortgage banker's single-lender approach aligns with your specific financial situation and property goals. For straightforward transactions, this streamlined model works efficiently. For complex scenarios involving significant stock compensation, multiple properties, or unique underwriting needs, the limitations may outweigh the benefits.

Mortgage Bankers, Loan Officers, and Brokers: Clarifying the Roles

The mortgage industry uses various titles that often confuse homebuyers, especially when comparing different types of mortgage professionals. Clarifying these distinctions helps you understand exactly who you're working with and what they can offer.

Loan officer is a general term describing anyone licensed to originate mortgage loans. Both mortgage bankers and mortgage brokers employ loan officers, but the structure differs significantly. A loan officer working for a mortgage banker represents that specific institution. A loan officer working for a mortgage brokerage represents multiple lending partners.

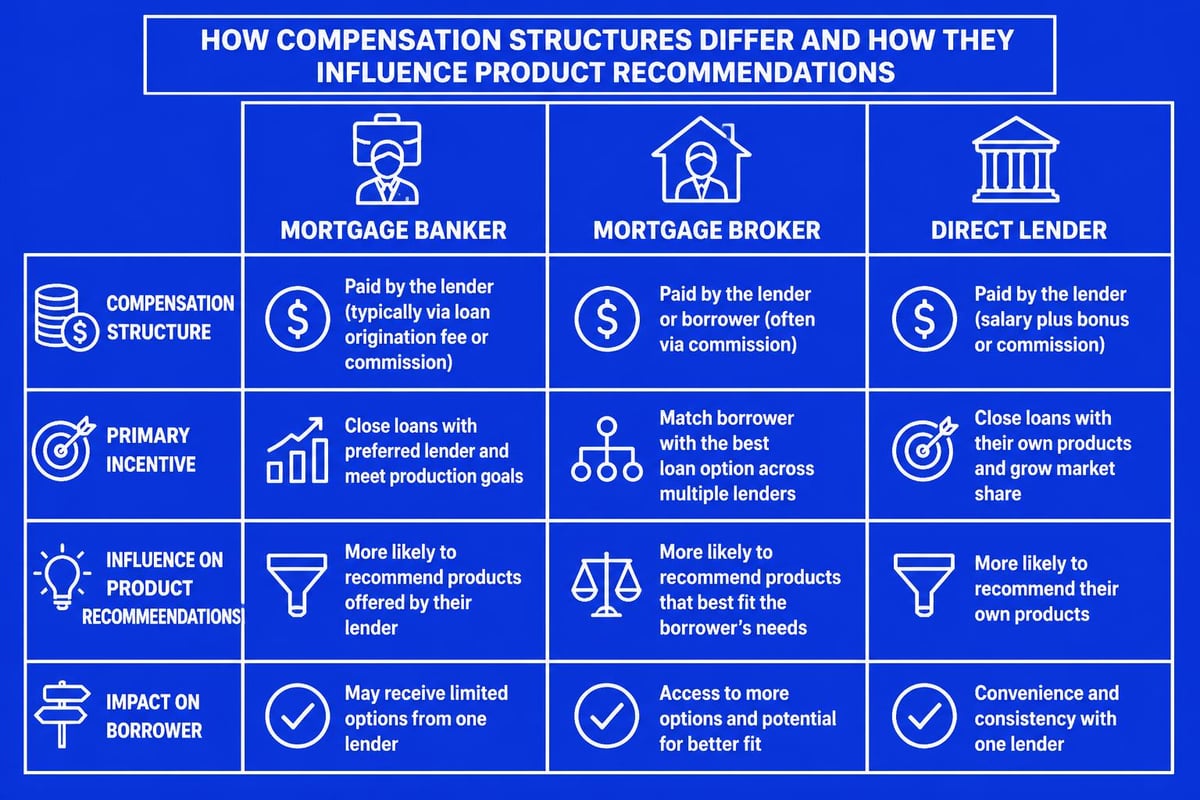

Compensation Structures and Potential Conflicts

Understanding how different mortgage professionals get paid reveals potential motivations and conflicts of interest that might affect your experience. Transparency around compensation builds trust and helps you evaluate advice objectively.

| Professional Type | Primary Compensation | Potential Conflicts |

|---|---|---|

| Mortgage Banker | Salary + commission on funded loans | May push higher-rate products for commission tiers |

| Mortgage Broker | Lender-paid commission on closed loans | May favor lenders offering higher compensation |

| Direct Lender Rep | Salary-based with performance bonuses | Incentivized to close deals regardless of fit |

Mortgage bankers typically receive base salaries plus production-based commissions tied to loan volume and sometimes product mix. This structure incentivizes closing loans but may also encourage recommending higher-margin products when multiple options exist within their portfolio.

Federal regulations require mortgage professionals to disclose compensation arrangements, but understanding the underlying incentive structures helps you evaluate recommendations critically. Whether working with a mortgage banker or broker in Seattle, asking direct questions about compensation and rate options ensures you're making informed decisions.

For tech professionals in Redmond or Kirkland navigating jumbo loan scenarios with stock compensation, compensation structures matter less than competency with complex income documentation. The right professional understands RSU vesting schedules, ISO versus NSO tax treatment, and how underwriters evaluate equity compensation for qualifying purposes.

Choosing the Right Mortgage Professional for Seattle Real Estate

The Seattle metropolitan area presents unique lending challenges that require specialized knowledge and experience. High property values, competitive bidding environments, and a concentration of tech professionals with complex compensation packages create specific demands for mortgage professionals.

Seattle-specific considerations when choosing your lender include:

- Understanding jumbo loan requirements in high-cost markets

- Experience qualifying stock compensation and RSUs

- Familiarity with Seattle-area condo approval processes

- Knowledge of competitive offer strategies and appraisal challenges

- Relationships with local title companies and real estate agents

Whether you choose a mortgage banker or broker matters less than their specific expertise with your transaction type. A mortgage banker with deep experience in Seattle's jumbo loan market may serve you better than a broker unfamiliar with equity compensation qualifying. Conversely, a broker with strong wholesale lender relationships might access better rates than a mortgage banker whose institution prices conservatively.

Evaluating Credentials and Track Record

Beyond job title, evaluate potential mortgage professionals based on verifiable credentials and proven track record. In competitive Seattle neighborhoods, execution matters as much as initial rate quotes.

Key evaluation criteria include:

- Licensing and compliance: Verify NMLS license and complaint history

- Market experience: Years actively lending in Seattle-area markets

- Review history: Pattern of verified client feedback across platforms

- Closing speed: Average timeline from application to funding

- Communication style: Responsiveness and transparency during initial interactions

- Specialized knowledge: Expertise with your specific loan scenario

For first-time homebuyers in Seattle, educational approach and patience matter significantly. For experienced investors or repeat buyers, efficiency and pricing take priority. Match the mortgage professional's strengths to your specific needs rather than defaulting to brand recognition alone.

The mortgage banker versus broker decision ultimately depends on your unique circumstances. Straightforward purchases with conventional financing may benefit from a mortgage banker's streamlined approach. Complex scenarios involving multiple income sources, unique properties, or specialized loan programs often require the flexibility that experienced brokers provide through multiple lending relationships.

Regulatory Oversight and Consumer Protections

Whether working with a mortgage banker or broker, federal and state regulations provide substantial consumer protections throughout the lending process. Understanding these safeguards helps you recognize your rights and identify potential violations.

The Consumer Financial Protection Bureau (CFPB) oversees mortgage lending practices, establishing disclosure requirements, prohibiting certain fees, and enforcing fair lending laws. Both mortgage bankers and brokers must comply with identical federal regulations, though some state-level requirements vary.

Key regulatory protections include:

- Loan Estimate disclosure within three business days of application

- Closing Disclosure provided at least three days before closing

- TILA-RESPA Integrated Disclosure (TRID) requirements

- Prohibition of kickbacks and unearned fees under RESPA

- Equal Credit Opportunity Act protections against discrimination

- Right to shop for settlement services

Mortgage bankers and brokers face the same disclosure obligations and consumer protection requirements. The regulatory framework doesn't favor one model over another-both must provide transparent pricing, clear disclosures, and fair treatment regardless of borrower characteristics.

State-Level Licensing in Washington

Washington State requires all mortgage professionals to hold active NMLS licenses and complete continuing education requirements. These standards apply equally to mortgage bankers and brokers, ensuring baseline competency across the industry.

You can verify any mortgage professional's licensing status, employment history, and complaint record through the NMLS Consumer Access portal. This transparency allows Seattle homebuyers to research credentials before committing to a lending relationship. For those exploring conventional financing options or specialized programs, verifying your loan officer's experience with specific product types adds another layer of confidence.

Making Your Decision in Seattle's Competitive Market

Seattle's housing market demands strategic financing decisions aligned with your specific goals and timeline. The mortgage banker question represents just one component of your broader lending strategy, but it's an important one that affects rate, service quality, and execution certainty.

For buyers with straightforward financial profiles seeking conventional loans under conforming limits, a reputable mortgage banker may provide the streamlined experience you need. The direct relationship, internal processing, and brand recognition can facilitate smooth transactions, especially when you already maintain banking relationships with the institution.

However, Seattle's high property values push many transactions into jumbo territory, where specialized underwriting expertise becomes critical. Tech professionals with substantial equity compensation, self-employed buyers with complex tax returns, or investors managing multiple properties often benefit from the flexibility and market access that experienced brokers provide through wholesale lending relationships.

Final considerations for your decision:

- Transaction complexity: Simple versus complex income, property, or credit scenarios

- Rate sensitivity: How much difference in pricing matters to your financial goals

- Timeline requirements: Standard closing versus accelerated timeframes

- Relationship value: Existing banking relationships or preference for new partnerships

- Service expectations: Hands-off efficiency versus consultative guidance

The right answer varies by individual circumstances. What matters most is choosing a mortgage professional-whether banker or broker-who demonstrates expertise with your specific scenario, communicates transparently, and executes reliably in Seattle's competitive environment. Reviews, referrals, and direct consultations reveal far more about likely service quality than job title alone.

Choosing between a mortgage banker and other lending professionals requires understanding the structural differences, advantages, and limitations of each approach. For Seattle-area homebuyers navigating complex compensation structures, competitive markets, or specialized loan scenarios, working with an experienced professional who understands local market dynamics makes all the difference. Keith Akada brings over 25 years of mortgage expertise to Seattle, Bellevue, Redmond, and Kirkland through Mortgage Reel, specializing in qualifying stock compensation, executing jumbo loans, and providing the transparent guidance that has earned 750+ five-star reviews. Whether you're a first-time buyer or seasoned investor, connect with a lending partner who prioritizes education, strategy, and reliable execution in every transaction.