Finding competitive mortgage loan deals in Seattle's dynamic housing market requires more than simply accepting the first offer you receive. With home prices remaining elevated across neighborhoods from Shoreline to Everett, securing favorable loan terms can save you tens of thousands of dollars over the life of your mortgage. Whether you're purchasing your first home in Lake Forest Park or refinancing an investment property in Lynnwood, understanding how to identify, compare, and negotiate the best mortgage loan deals gives you a significant financial advantage in 2026's competitive landscape.

Understanding What Makes Mortgage Loan Deals Competitive

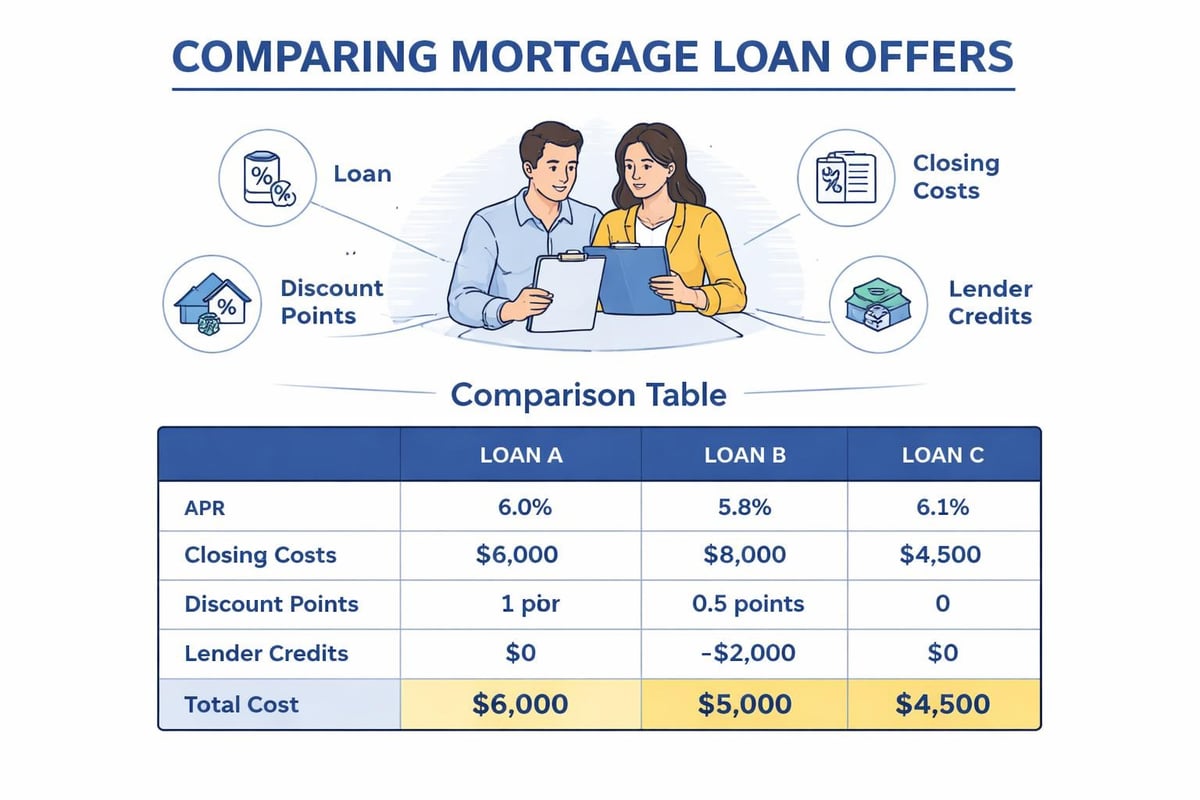

The most attractive mortgage loan deals balance multiple factors beyond just the advertised interest rate. Effective Annual Percentage Rate (APR), which includes both the interest rate and lender fees, provides a more accurate picture of your total borrowing cost. Many borrowers in Seattle focus exclusively on rate quotes without examining closing costs, discount points, or prepayment penalties that can significantly impact long-term affordability.

Key Components of Favorable Loan Offers

When evaluating mortgage loan deals, examine these critical elements:

- Interest rate and APR spread: A small gap indicates lower fees

- Origination charges and processing fees: Should typically range from 0.5% to 1% of loan amount

- Discount points offered: Each point costs 1% of loan amount and typically reduces rate by 0.25%

- Rate lock duration: 30-60 day locks protect against market fluctuations during underwriting

- Closing cost structure: Compare itemized fees across multiple Loan Estimates

Lender credits represent another important consideration. Some mortgage loan deals offer credits that offset closing costs in exchange for a slightly higher interest rate, which can benefit buyers who need to preserve cash for reserves or home improvements in Mill Creek or other Seattle-area communities.

The Consumer Financial Protection Bureau’s comparison tool helps borrowers understand how to review Loan Estimates from multiple lenders systematically, ensuring you're making apples-to-apples comparisons across different mortgage loan deals.

Where Seattle Borrowers Find the Best Mortgage Loan Deals

Geographic location significantly influences available loan programs and pricing. Seattle borrowers access mortgage loan deals through several distinct channels, each offering unique advantages depending on your financial profile and timeline.

Direct Lenders vs. Mortgage Brokers

| Channel Type | Advantages | Best For |

|---|---|---|

| Banks | Relationship discounts, bundled services | Existing customers with strong banking relationships |

| Credit Unions | Lower fees, member benefits | Borrowers eligible for membership with solid credit |

| Mortgage Brokers | Access to multiple lenders, wholesale pricing | Buyers seeking competitive rates and personalized guidance |

| Online Lenders | Streamlined application, competitive rates | Tech-savvy borrowers comfortable with digital processes |

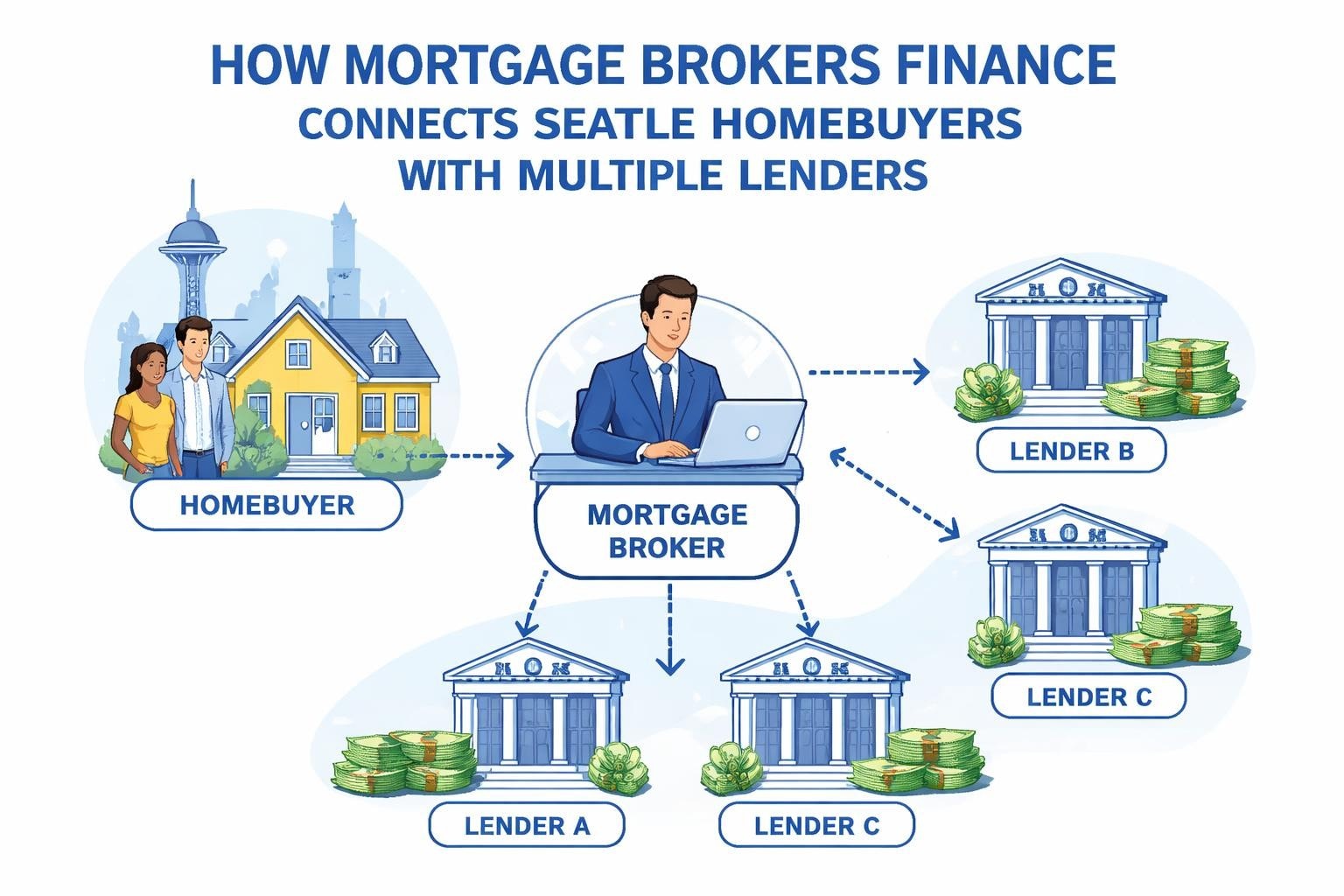

Working with an experienced Seattle mortgage broker provides access to wholesale mortgage loan deals not available to retail consumers. Brokers compare offerings from dozens of lenders simultaneously, which proves especially valuable for buyers with complex income structures such as stock compensation from Amazon, Microsoft, or Google.

Timing Your Search for Optimal Deals

Mortgage rates fluctuate daily based on bond market activity and Federal Reserve policy. The best mortgage loan deals typically emerge when:

- Economic data suggests slowing inflation

- The Federal Reserve signals potential rate cuts

- Seasonal slowdowns reduce purchase competition (typically November through January)

- Lenders launch promotional campaigns to meet quarterly volume targets

Monitor rate trends for 30-45 days before beginning your home search in Shoreline or Everett. This baseline helps you recognize genuinely competitive mortgage loan deals versus average market pricing.

Comparing Mortgage Products to Maximize Savings

Different loan programs offer varying advantages depending on your down payment, credit profile, and long-term homeownership plans. Understanding these distinctions helps you identify which mortgage loan deals provide the best value for your specific situation.

Conventional Loan Options

Conventional mortgages conforming to Fannie Mae and Freddie Mac guidelines represent the most common mortgage loan deals in Seattle. These loans offer:

- Down payments as low as 3% for first-time buyers with qualifying income

- PMI removal once you reach 20% equity through payments or appreciation

- Competitive rates for borrowers with credit scores above 680

- Higher loan limits reflecting Seattle's elevated home prices ($1,149,825 for 2026 in King County)

Borrowers with 5% down often find excellent conventional loan programs that balance monthly payment affordability with competitive interest pricing, particularly in Lynnwood and Lake Forest Park where median prices create opportunities for this loan structure.

Government-Backed Loan Alternatives

FHA, VA, and USDA loans provide specialized mortgage loan deals for qualifying borrowers:

FHA loans require just 3.5% down with credit scores as low as 580, making homeownership accessible despite Seattle's high prices. However, mandatory mortgage insurance remains for the loan's lifetime unless you refinance.

VA loans offer zero-down financing with no monthly mortgage insurance for eligible service members and veterans. These represent some of the most advantageous mortgage loan deals available, with competitive rates and flexible underwriting.

USDA loans provide 100% financing for qualifying properties in eligible rural areas surrounding Seattle, though most King County neighborhoods don't qualify given population density.

Negotiating Better Terms on Mortgage Loan Deals

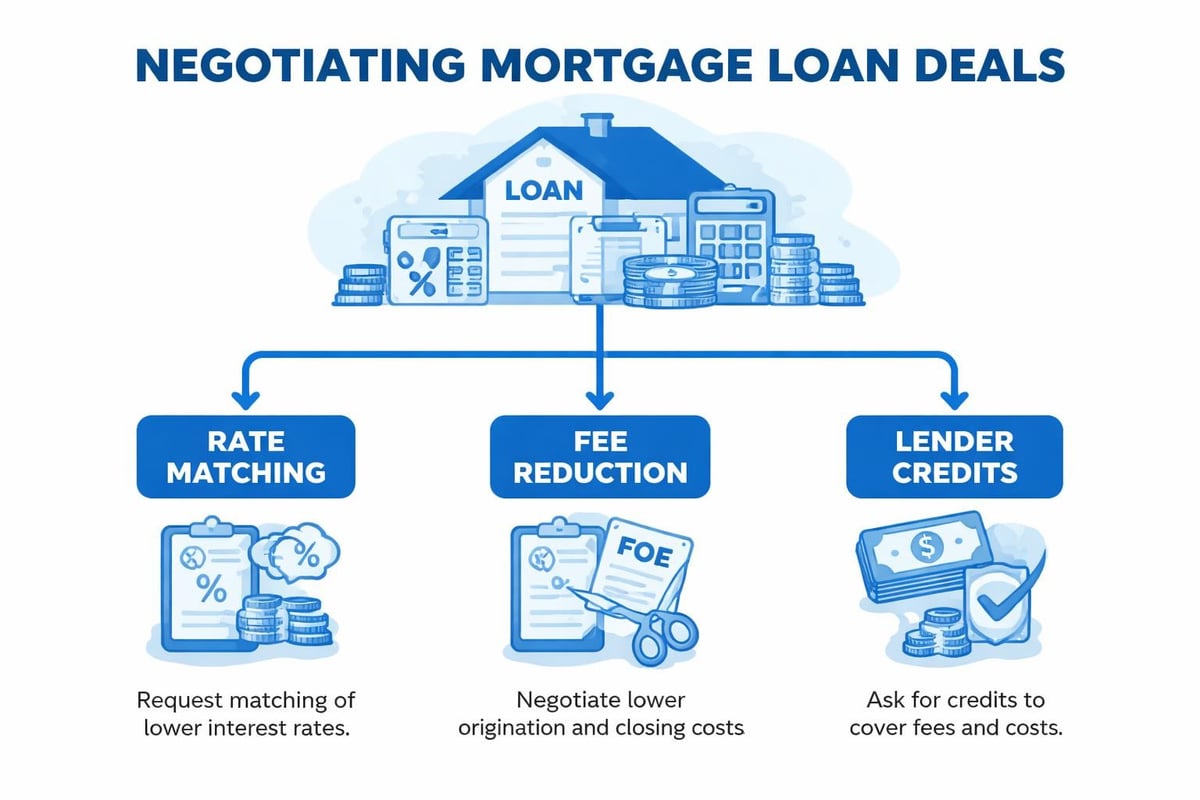

Lenders price mortgage loan deals with built-in flexibility for negotiation. Understanding this reality empowers you to request better terms rather than accepting initial offers.

Rate Matching and Fee Reduction Strategies

Present competing Loan Estimates to lenders and request rate matching. Most lenders would rather reduce their margin slightly than lose a qualified borrower to a competitor. Focus negotiations on:

- Reducing origination charges: Often negotiable by 0.25% to 0.5% of loan amount

- Waiving application or processing fees: Commonly charged but frequently negotiable

- Including rate locks without additional fees: Some lenders charge for extended locks

- Increasing lender credits: Can offset third-party costs for appraisal and title

For tech professionals with substantial equity compensation, demonstrating strong financial capacity often leads to more favorable mortgage loan deals. Lenders view borrowers with diversified income streams and significant reserves as lower-risk, creating negotiating leverage.

Leveraging Your Credit Profile

Your credit score dramatically impacts available mortgage loan deals. Even small score improvements can shift you into better pricing tiers:

- 740+ scores: Access to best available rates across most programs

- 680-739 scores: Competitive pricing with slightly higher rates

- 620-679 scores: Higher rates and potentially increased fees

- Below 620: Limited conventional options, FHA may provide better deals

Before shopping for mortgage loan deals, obtain your credit reports from all three bureaus and dispute any errors. A 20-point score increase can reduce your rate by 0.25% to 0.5%, translating to substantial monthly savings on Seattle's typical home prices.

According to Consumer Reports, considering smaller lenders and thoroughly understanding Loan Estimates helps borrowers identify the most affordable mortgage options.

Evaluating Total Cost vs. Monthly Payment in Loan Deals

Seattle's competitive housing market often pushes buyers to prioritize qualifying for maximum loan amounts over optimizing long-term costs. The best mortgage loan deals balance immediate affordability with total interest paid over the loan term.

Understanding the Rate vs. Points Tradeoff

Paying discount points upfront reduces your interest rate permanently. Evaluate whether this strategy makes sense by calculating your break-even timeline:

Break-even months = Total points paid ÷ Monthly payment reduction

If you plan to keep your home and loan for longer than the break-even period, paying points for a lower rate typically represents one of the smartest mortgage loan deals available. For Seattle homeowners planning to stay long-term in neighborhoods like Mill Creek or Shoreline, this strategy often maximizes savings.

Conversely, if you anticipate refinancing within 3-5 years or relocating for career opportunities common among tech professionals, accepting a slightly higher rate without points preserves capital for other investments.

Amortization Strategies That Improve Loan Economics

| Strategy | Monthly Impact | Total Interest Savings | Best For |

|---|---|---|---|

| 15-year term | Higher payment | 50-60% interest reduction | High earners, equity-building focus |

| Biweekly payments | Minimal change | 15-20% interest reduction | Disciplined savers |

| Extra principal | Flexible amounts | Varies by consistency | Variable income professionals |

| Recast after lump sum | Lower payment | Moderate savings | Bonus/RSU recipients |

The Federal Deposit Insurance Corporation provides helpful guidance on evaluating down payment requirements and fee structures when comparing mortgage options.

Special Considerations for Seattle-Area Buyers in 2026

The Greater Seattle housing market presents unique challenges and opportunities that influence which mortgage loan deals provide optimal value.

Qualifying Tech Compensation for Better Loan Amounts

Tech professionals in Seattle, Bellevue, and Redmond often receive substantial portions of compensation through equity grants, bonuses, and stock options. Traditional lenders frequently discount or exclude this income, limiting the mortgage loan deals available to you.

Specialized underwriting for RSUs and stock compensation allows qualifying this income at higher percentages, dramatically improving your purchasing power for homes in competitive neighborhoods. Working with lenders experienced in tech compensation ensures you access mortgage loan deals that fully leverage your financial capacity.

Jumbo Loan Landscape in High-Cost Areas

Seattle's elevated home prices push many purchases above conforming loan limits. Jumbo mortgage loan deals have become increasingly competitive in 2026, with:

- Rate pricing often within 0.125% to 0.25% of conforming loans

- Down payment requirements as low as 10% with strong credit and reserves

- Flexible DTI ratios for well-qualified borrowers

- Streamlined documentation for substantial asset portfolios

For professionals purchasing in Everett or Lynnwood where prices may fall just above conforming limits, comparing both conforming and jumbo mortgage loan deals helps identify the most advantageous program structure.

Accelerated Closing Timelines as Competitive Advantages

In Seattle's competitive market, the ability to close quickly often determines whose offer gets accepted. The best mortgage loan deals increasingly include expedited underwriting capabilities that strengthen your position against competing buyers.

Advanced underwriting technology and streamlined processes enable closings in as few as 9-10 business days for well-documented borrowers. This capability proves especially valuable when:

- Multiple offers compete for desirable properties in Lake Forest Park or Shoreline

- Sellers need quick closings for relocation or timing-sensitive transactions

- Investment property opportunities require rapid execution

- Rate locks approach expiration during extended negotiations

Speed doesn't require sacrificing favorable terms. Many lenders offering quick closings also provide competitive mortgage loan deals on rates and fees, combining both advantages for strategic buyers.

Documentation Requirements for Fast Processing

Accelerated timelines require thorough preparation:

- Complete tax returns for the most recent two years

- Recent pay stubs showing year-to-date income

- Bank statements for all accounts (typically 2-3 months)

- Investment account statements documenting reserves

- Stock compensation documentation for equity grants and vesting schedules

Tech professionals should prepare supplemental documentation explaining equity compensation structures, vesting timelines, and historical grant values to expedite underwriting of complex income profiles.

How Market Conditions Influence Available Deals

Mortgage loan deals fluctuate based on broader economic conditions, housing supply, and lender competition for market share. Understanding these dynamics helps you time your search strategically.

Reading Market Signals for Optimal Timing

The spread between short-term and long-term Treasury yields provides insight into mortgage rate direction. When the yield curve steepens (longer-term rates rise relative to short-term rates), mortgage pricing typically increases. Conversely, yield curve flattening or inversion often precedes more favorable mortgage loan deals.

Monitor these indicators when considering whether to lock your rate or float:

- 10-year Treasury yield trends: Mortgage rates typically track 1.5% to 2% above this benchmark

- Federal Reserve policy statements: Forward guidance on rate decisions impacts bond markets

- Inflation data releases: CPI and PCE reports drive rate volatility

- Employment reports: Strong job growth can pressure rates higher

For refinance opportunities, evaluate whether current mortgage loan deals provide sufficient savings to justify closing costs, typically requiring at least 0.50% to 0.75% rate improvement.

Seasonal Patterns in Mortgage Pricing

Lender competition for business creates seasonal variations in mortgage loan deals:

Spring and summer bring increased purchase activity but also heightened lender competition, sometimes producing promotional mortgage loan deals despite higher baseline rates.

Fall and winter typically see reduced purchase volume, leading some lenders to offer aggressive pricing to maintain loan production targets, particularly in November and December.

According to Bankrate, lenders actively offer deals and discounts to attract borrowers in competitive markets, making it essential to compare multiple offers.

Red Flags to Avoid in Mortgage Loan Deals

Not all seemingly attractive mortgage loan deals provide genuine value. Recognize warning signs that indicate potentially problematic loan structures or predatory lending practices.

Questionable Loan Features and Terms

Avoid mortgage loan deals containing these elements:

- Prepayment penalties: Especially those extending beyond 3 years or exceeding 2% of loan balance

- Balloon payments: Required lump sum payments after 5-7 years create refinance risk

- Negative amortization: Payments that don't cover interest, increasing loan balance over time

- Excessive fees: Origination charges above 1.5% or numerous "junk fees" padding lender profit

- Teaser rates: Artificially low initial rates that adjust substantially higher

Rate lock specifics require careful review. Some mortgage loan deals advertise attractive rates but include expensive lock extension fees if closing delays occur. Ensure your rate lock period provides adequate buffer beyond your expected closing date.

Verifying Lender Credibility

Research lender reputation through multiple channels before committing to mortgage loan deals:

- Check state licensing through the Nationwide Multistate Licensing System (NMLS)

- Review complaints filed with the Consumer Financial Protection Bureau

- Examine ratings on independent review platforms beyond promotional materials

- Verify lender standing with Better Business Bureau

- Request client references for similar loan scenarios

The Consumer Financial Protection Bureau’s exploration guide outlines various mortgage options and helps borrowers understand different loan types to make informed decisions.

Maximizing Value from Refinance Opportunities

Existing homeowners in Seattle can capture significant savings through strategic refinancing when mortgage loan deals improve relative to current loan terms.

Rate-and-Term Refinance Considerations

Evaluate refinance mortgage loan deals by calculating total savings after accounting for closing costs. Use this framework:

Monthly savings × Months until sale/refinance – Closing costs = Net benefit

For Seattle homeowners planning to stay long-term, even modest rate improvements of 0.50% to 0.75% often justify refinancing. However, if you anticipate selling within 2-3 years, require larger rate improvements to recover closing costs.

Cash-Out Refinancing for Strategic Purposes

Homeowners with substantial equity can access favorable cash-out mortgage loan deals in 2026. Strategic uses include:

- Consolidating high-interest debt at mortgage rates significantly below credit card or personal loan rates

- Funding investment property purchases to expand real estate portfolios

- Home improvements that increase property value and enjoyment

- Education expenses at rates lower than most student loans

Maintain at least 20% equity after cash-out to avoid mortgage insurance and access the most competitive pricing on these mortgage loan deals.

Finding competitive mortgage loan deals requires systematic comparison, strategic timing, and thorough understanding of how different loan features impact both immediate affordability and long-term costs. Whether you're purchasing your first home or refinancing an existing property in Seattle's dynamic market, working with experienced professionals who understand local market conditions and specialized income qualification provides significant advantages. Keith Akada and the team at Mortgage Reel bring 25+ years of expertise helping Seattle-area buyers and homeowners secure optimal financing solutions, from conventional purchases to complex jumbo loans for tech professionals with equity compensation.