Are you ready to unlock your home’s potential and stay ahead in the refinance and mortgage landscape of 2026? This comprehensive guide equips you with proven strategies to refinance and mortgage smarter, helping you save money and achieve your financial goals. Explore the latest options, understand evolving loan products, and follow a step-by-step refinancing roadmap. With rates changing and new digital tools available, 2026 offers both opportunities and challenges for homeowners and buyers. Use this resource to make confident, informed decisions and maximize your savings in today’s dynamic market.

Understanding the 2026 Mortgage and Refinance Landscape

The refinance and mortgage landscape in 2026 is rapidly evolving, shaped by shifting economic conditions and new opportunities for homeowners and buyers. Staying informed about these changes is essential for making smart decisions about your home financing strategy.

Refinance and Mortgage Guide: Essential Steps for 2026 Page Separator Site title

Key Takeaways

- The Refinance and Mortgage Guide: Smart Strategies for 2026 helps homeowners navigate the evolving mortgage landscape.

- Key trends include stable interest rates, tighter lending standards, and a rise in non-traditional loan products.

- Homeowners can leverage rising property values for refinancing, while first-time buyers face stricter requirements.

- A step-by-step guide outlines the refinancing process, emphasizing the importance of evaluating goals and comparing lenders.

- Timely refinancing, reducing closing costs, and understanding loan options are crucial for maximizing savings.

Estimated reading time: 15 minutes

Our Refinance and Mortgage Guide: Smart Strategies for 2026 helps you navigate changing rates and maximize savings. Discover more!

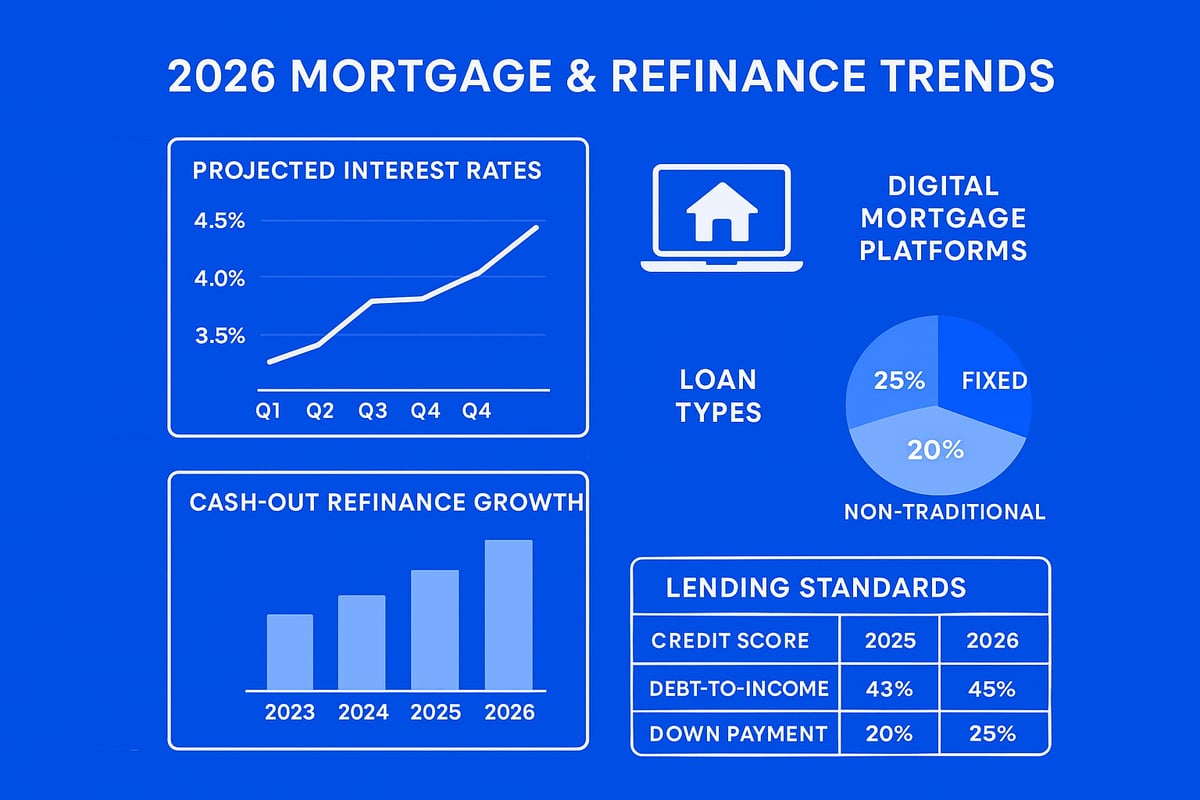

Key Trends Shaping the 2026 Market

Interest rates are at the forefront of the refinance and mortgage conversation for 2026. Experts predict that rates will remain relatively steady, with slight increases possible as the economy continues to recover. Inflation and ongoing Federal Reserve policy decisions play a significant role in determining these rates. For a deeper dive, see the 2026 Mortgage Rates Forecast According to Experts.

Lending standards are tightening, with many lenders raising minimum credit score requirements. This is partly a response to increased economic uncertainty and efforts to manage risk. At the same time, digital mortgage platforms are becoming more widespread. These platforms streamline the application process, offering faster approvals and greater transparency for borrowers.

The market is also seeing a rise in non-traditional loan products. Options like Debt Service Coverage Ratio (DSCR) loans and bank statement loans are gaining popularity, particularly among self-employed individuals and those with complex income streams. This expansion in loan products offers more flexibility for borrowers who may not fit traditional lending profiles.

Demand for refinancing remains high, driven by the growth in home equity over the past few years. In fact, between 2025 and 2026, cash-out refinance applications increased by 10 percent, reflecting homeowners’ desire to tap into their property’s value for various financial goals.

Here is a snapshot of key trends:

| Trend | 2026 Outlook |

|---|---|

| Projected Interest Rates | Slightly higher, but stable |

| Federal Reserve Impact | Careful monitoring continues |

| Lending Standards | Tighter, higher credit scores |

| Digital Mortgage Platforms | Faster, more accessible |

| Non-Traditional Loan Products | Growing share of market |

| Cash-Out Refinance Applications | Up 10% year-over-year |

These factors collectively shape the refinance and mortgage environment, influencing everything from application speed to loan eligibility.

How These Trends Affect Homeowners and Buyers

For homeowners, rising property values mean increased eligibility for refinancing, especially for those looking to access home equity or secure better loan terms. Many are now able to qualify for a refinance and mortgage that was previously out of reach.

First-time buyers, however, face stricter debt-to-income and down payment requirements. This means careful financial planning is more important than ever for those entering the market. The refinance and mortgage process now often requires higher credit scores and more thorough documentation.

Self-employed individuals and tech professionals benefit from the growing selection of loan products, such as DSCR and bank statement loans. These options cater to complex income situations and provide more pathways to approval.

Comparison tools and online calculators have become essential resources in the refinance and mortgage process. With so many options available, borrowers can analyze rates, terms, and fees to find the best fit for their needs. Notably, applications for adjustable-rate mortgages (ARMs) have risen 15 percent year-over-year, signaling increased interest in flexible loan structures.

In summary, 2026 presents both challenges and opportunities for those navigating the refinance and mortgage market. By understanding these trends and leveraging available tools, borrowers can position themselves for success.

Mortgage Types and Refinance Options Explained

Navigating refinance and mortgage decisions in 2026 means understanding the full landscape of available loan products. The right choice depends on your goals, eligibility, and risk tolerance. Let’s break down the most popular mortgage types and refinancing options for today’s market.

Fixed-Rate Mortgages

A fixed-rate mortgage is the gold standard for stability in the refinance and mortgage world. With this option, your interest rate stays the same for the entire loan term. That means predictable payments and easier budgeting, no matter how the market shifts.

Common terms are 30, 20, 15, or even 10 years. In 2026, example rates for a 30-year fixed can be as low as 5.875% APR, while 15-year fixed loans may reach 5.25% APR. This structure is ideal for buyers seeking long-term security or those wanting to refinance and mortgage their home with certainty.

Pros include consistent monthly payments, higher maximum loan amounts, and the ability to consider cash-out options. The primary downside is that initial rates are typically higher than adjustable options. For buyers with strong credit and a stable income, conventional fixed-rate loans—sometimes with as little as 5% down—are especially attractive. Learn more about conventional loans with 5% down to see if this path fits your financial plan.

Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages (ARMs) offer another popular path in the refinance and mortgage process. ARMs start with a fixed rate for a set period—usually 3, 5, or 7 years—then adjust at scheduled intervals based on market conditions.

For example, a 3-year ARM could start at just 5.0% APR, while a 5-year ARM may offer 5.375% APR. These loans are best for those planning to sell or refinance before the initial period ends, or for buyers anticipating lower rates in the future.

The main risk with ARMs is that payments can increase after the fixed period, making budgeting less predictable. However, for short-term homeowners or investors, ARMs can be a strategic choice in the refinance and mortgage landscape.

Cash-Out vs. Rate-and-Term Refinance

When considering refinance and mortgage options, it’s essential to know the difference between cash-out and rate-and-term refinancing.

Cash-out refinancing lets you tap into your home’s equity for debt consolidation, renovations, or major expenses. Rate-and-term refinancing, by contrast, focuses on reducing your interest rate or shortening your loan term without taking out extra cash.

Both choices can impact monthly payments and long-term interest. For instance, homeowners who opted for a strategic refinance and mortgage in 2025 saved an average of $250 per month. Data from recent years also shows a 10% increase in cash-out refinance applications, reflecting the growing appeal of leveraging home equity for financial flexibility.

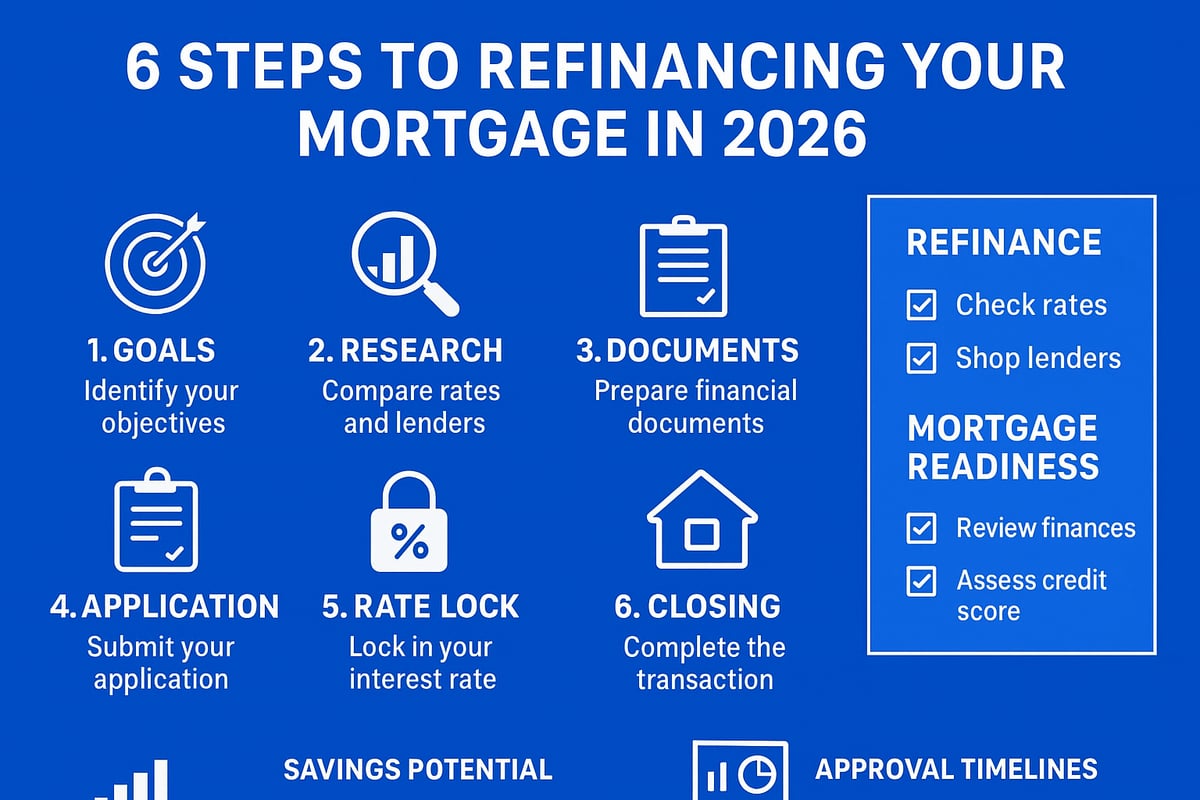

Step-by-Step Guide to Refinancing Your Mortgage in 2026

Navigating the refinance and mortgage process in 2026 requires a clear plan and attention to detail. With changing market dynamics and evolving digital tools, understanding each step can help you secure the best terms and maximize savings. This guide breaks down the entire journey, so you can approach your refinance and mortgage decisions with confidence.

Step 1: Evaluate Your Financial Goals and Eligibility

Start your refinance and mortgage journey by clarifying your objectives. Are you aiming to lower your interest rate, tap into home equity, shorten your loan term, or remove private mortgage insurance? Define your goals, as they will shape your approach and product selection.

Next, review your financial profile. Check your credit score, current mortgage terms, and how much equity you have in your home. Lenders will examine your debt-to-income ratio and property value, so having a clear picture helps set realistic expectations.

Use online calculators to estimate potential savings and determine if now is the right time to refinance and mortgage your property. These tools can show you how your new payment, interest costs, and loan term may change. By starting with a strong foundation, you’ll make smarter, more informed choices.

Step 2: Research and Compare Lenders

Comparing lenders is essential for a successful refinance and mortgage experience. Each lender offers unique rates, fees, and approval processes, so shopping around can save you thousands over the life of your loan.

Gather quotes from at least three lenders. Pay attention to the annual percentage rate (APR), which includes both the interest rate and fees. Also, compare closing costs, lender credits, and customer service ratings. Digital mortgage platforms in 2026 often provide instant pre-qualification, making it easier to compare options.

Look for lenders with transparent terms and positive reviews. Consider both local and national providers, as some may offer special programs for tech professionals or self-employed borrowers. Taking time to research ensures you secure the most competitive refinance and mortgage terms available.

Step 3: Gather Documentation

Preparing your paperwork in advance streamlines the refinance and mortgage process. Typical documents include:

- Income verification (pay stubs, W-2s, 1099s)

- Recent tax returns

- Bank and investment account statements

- Proof of homeowners insurance

- Current mortgage statement

- Property tax records

If you are self-employed or have complex income, be ready to provide additional details, such as profit and loss statements or documentation of stock compensation. Digital uploads and e-signatures have made this step faster than ever.

If you are new to mortgage terminology or unfamiliar with required documents, visit the Mortgage glossary and definitions for clear explanations. Being organized reduces delays and helps you move confidently through your refinance and mortgage application.

Step 4: Submit Your Application

Once you have selected a lender and gathered your documents, complete your refinance and mortgage application. You will choose the loan product that best fits your needs, whether you want a lower rate, shorter term, or cash-out option.

After submitting, your application enters underwriting, where the lender reviews your information and orders an appraisal of your property.

Respond promptly to requests for additional details to prevent processing delays. Staying engaged and proactive during this stage helps keep your refinance and mortgage timeline on track.

Step 5: Review Loan Estimate and Lock Your Rate

After applying, you will receive a Loan Estimate outlining your interest rate, closing costs, and projected monthly payment. Review this document carefully to ensure all terms match your expectations and ask questions if anything is unclear.

Consider locking your rate to secure current market terms, especially if rates are rising. Rate locks typically last 30 to 45 days, giving you time to complete the process without worrying about fluctuations.

Negotiate lender credits if possible to offset closing costs. Making informed decisions at this stage helps you maximize the value of your refinance and mortgage transaction.

Step 6: Close on Your New Loan

The final step in the refinance and mortgage process is closing. You will receive a Closing Disclosure at least three days before signing, which details your final terms and costs. Review every line item and confirm that there are no unexpected fees.

Attend your closing appointment to sign the necessary documents. After closing, your new lender will pay off your old loan, and your new payments will begin. Set up your payment method, escrow accounts, and update your insurance as needed.

A successful closing means you have completed the refinance and mortgage journey. Keep all documents for your records and monitor your new loan to ensure everything is set up correctly.

Smart Strategies to Maximize Savings and Success

Unlocking the full potential of your refinance and mortgage decisions in 2026 calls for a thoughtful approach. With shifting market conditions and evolving loan products, the right strategies can help you maximize savings and achieve your financial goals.

Timing Your Refinance for Maximum Benefit

Timing matters when it comes to refinance and mortgage planning. Market rates fluctuate based on economic factors, so keeping an eye on trends can pay off. In 2026, many homeowners are leveraging home equity growth to secure better terms, eliminate PMI, or free up cash for investments.

Use online calculators and rate trackers to monitor the best windows for refinancing. If rates are predicted to dip, waiting could save thousands in interest. For example, some homeowners saved over $30,000 in interest by refinancing at the right moment.

Evaluate your financial goals, and consider whether a rate drop or increased home value makes refinancing advantageous. Strategic timing can lead to significant long-term savings.

Reducing Closing Costs and Fees

Closing costs can quickly add up in any refinance and mortgage transaction. Savvy homeowners compare lender fees, title charges, and appraisal costs before committing. Shopping around is essential, as costs can vary between lenders and even within the same market.

Consider rolling closing costs into your loan if upfront cash is tight, but weigh the long-term impact on your loan balance and interest paid. Some lenders offer no- or low-cost refinance programs, which may be ideal for qualifying borrowers.

For more tips tailored to your local area, explore Seattle refinance resources to understand fee structures and savings opportunities specific to your market.

Choosing the Right Loan Term

Selecting the right loan term is a cornerstone of refinance and mortgage success. Shortening your term, such as moving from a 30-year to a 15-year loan, often means higher monthly payments but substantial savings on total interest.

| Loan Term | Example Rate (APR) | Estimated Savings |

|---|---|---|

| 30-year | 5.875% | Baseline |

| 15-year | 5.25% | Save tens of thousands in interest |

A shorter term also helps you build equity faster. However, ensure your monthly budget can accommodate the increased payment. If flexibility is your priority, a 30-year term may offer lower payments, but at a higher total cost.

Review your financial situation, future plans, and risk tolerance before choosing a term. The right choice will keep your refinance and mortgage goals on track.

Leveraging Cash-Out Refinancing Wisely

Cash-out refinancing can be a powerful tool when used strategically. By tapping into your home equity, you can access funds for debt consolidation, renovations, or investments. However, this increases your loan balance and may impact monthly payments.

In 2025, there was a notable 10 percent rise in cash-out refis as homeowners capitalized on rising property values. Learn more about this trend in Cash-Out Refinancing Trends in 2025.

Before proceeding, weigh the benefits against potential risks. Use funds for purposes that improve your financial position, not just for discretionary spending. Responsible use of cash-out refinancing strengthens your refinance and mortgage strategy.

Avoiding Common Refinancing Mistakes

Even experienced homeowners can make errors during the refinance and mortgage process. Common pitfalls include not comparing enough lenders, underestimating closing costs, or misunderstanding loan terms.

- Failing to shop around for rates and products

- Overestimating property value or available equity

- Ignoring prepayment penalties or long-term costs

To avoid these traps, use online tools, read lender reviews, and consult with trusted professionals. Stay informed about your options and never rush through paperwork. A careful, methodical approach leads to better decisions and maximizes your savings from any refinance and mortgage transaction.

Frequently Asked Questions: Refinancing and Mortgage Basics

Whether you are considering a refinance and mortgage update in 2026 or simply want clarity on the process, these frequently asked questions provide actionable answers for homeowners and buyers. Let’s address the most common concerns in today’s evolving market.

Rolling Closing Costs into Your Loan

Many homeowners ask if they can roll closing costs into their new refinance and mortgage. The answer is yes, in most cases. When you refinance, lenders often allow you to add the closing costs to your principal balance. This increases your loan amount but lets you avoid paying large sums up front.

Consider how this impacts your total interest paid over the life of your loan. Use a refinance and mortgage calculator to estimate monthly payments and total costs. Review your loan estimate carefully to see how fees affect your bottom line.

Removing Private Mortgage Insurance (PMI)

Eliminating PMI is a top goal for many pursuing a refinance and mortgage. Typically, you can remove PMI by lowering your loan-to-value (LTV) ratio to 80% or less, either by paying down your balance or through increased property value.

Refinancing can help if your home has appreciated. Lenders will require a new appraisal to confirm your eligibility. Once you meet the requirements, your monthly payment can decrease, boosting your long-term savings.

Options If You’re Struggling with Payments

If you are struggling with refinance and mortgage payments, several alternatives exist. Loan modification, forbearance, or government relief programs may offer temporary or permanent solutions. Contact your lender as soon as you anticipate difficulty to explore these options.

Refinancing to a lower rate or extending your loan term can also provide relief, though it may increase total interest paid. Always review all terms before deciding on the best path for your financial health.

Online Tools and Calculators

Online refinance and mortgage calculators are valuable for estimating payments, comparing loan products, and identifying potential savings. These digital tools simplify decision-making by projecting costs and helping you assess what you can afford.

For further guidance, explore Seattle home loans advice for local insights, tips, and up-to-date information tailored to your region’s market trends.

Application and Approval Timeline in 2026

The refinance and mortgage process in 2026 is faster than ever, thanks to digital applications and streamlined underwriting. Most qualified borrowers can expect approval and closing within two to four weeks. Fast-track options may close in as little as nine business days.

For a deeper understanding of how economic policy may affect your timeline, see this resource on the Federal Reserve’s Impact on Mortgage Rates. Staying informed helps you act when rates are most favorable.

Documentation and Credit Requirements

To qualify for a refinance and mortgage, you will need to provide proof of income, tax returns, credit details, and property information. Minimum credit scores and debt-to-income (DTI) ratios vary by lender and product.

Improve eligibility by paying down debts and checking your credit report for errors before applying. Digital uploads and e-signatures speed up the documentation process, making 2026 approvals more efficient than ever.

Now that you have a clearer picture of the 2026 mortgage landscape and the strategies that can help you make the most of your home’s equity, you might be wondering how these insights apply to your unique situation. Whether you’re a first-time homebuyer, an experienced investor, or considering a refinance to take advantage of new loan products, personalized guidance can make all the difference. If you’d like to talk through your options, discuss your goals, or simply get answers to your questions, Let’s have a conversation.