Purchasing your first home in Seattle represents one of the most significant financial milestones you'll achieve. Understanding the mortgage for first time buyers can feel overwhelming, especially in competitive markets like Seattle, Bellevue, and surrounding communities. With the right guidance and a clear strategy, you can navigate the financing process with confidence and secure the keys to your first property. This comprehensive guide breaks down everything you need to know about obtaining a mortgage as a first-time buyer in the Greater Seattle area.

Understanding First-Time Buyer Mortgage Options

The mortgage landscape offers several paths for first-time buyers, each designed to address different financial situations and goals. Choosing the right loan type directly impacts your monthly payment, upfront costs, and long-term financial flexibility.

Conventional Loans for First-Time Buyers

Conventional loans remain the most popular choice for buyers with solid credit and stable income. These mortgages aren't backed by government agencies, which means lenders set their own guidelines within parameters established by Fannie Mae and Freddie Mac.

For first-time buyers in Seattle and Shoreline, conventional financing offers several advantages:

- Down payments as low as 3% for qualified borrowers

- Competitive interest rates with strong credit scores (typically 620 or higher)

- Ability to cancel private mortgage insurance (PMI) once you reach 20% equity

- Flexible property types including single-family homes, condos, and townhouses

The trade-off comes with stricter credit requirements and the need for PMI when you put down less than 20%. However, for tech professionals working at Amazon, Microsoft, or Google with strong compensation packages including RSUs and stock options, conventional financing often provides the most efficient path to homeownership.

FHA Loans: Lower Down Payment Solution

FHA loans backed by the Federal Housing Administration offer a mortgage for first time buyers with more accessible qualification standards. These government-insured mortgages require as little as 3.5% down with credit scores as low as 580, making them attractive for buyers still building credit history.

Key considerations include:

- Lower credit score requirements compared to conventional

- Higher debt-to-income ratio allowances (up to 50% in some cases)

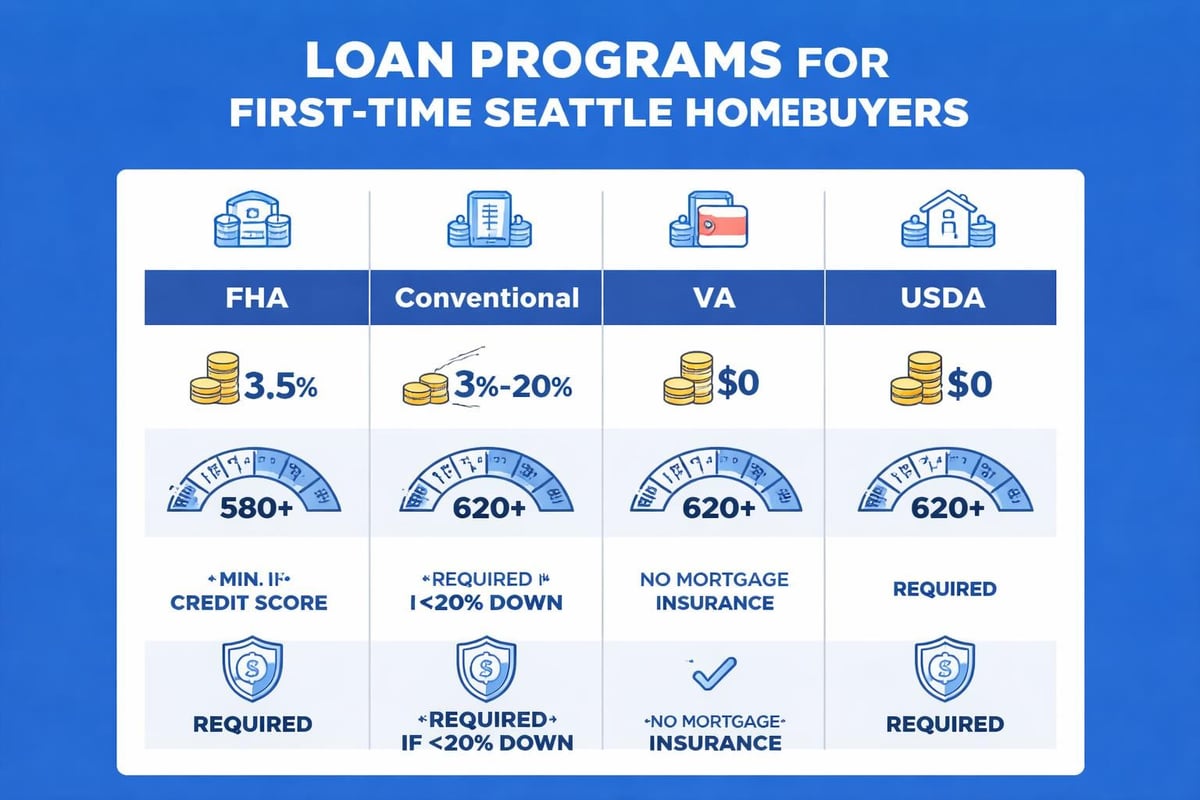

- Mandatory mortgage insurance for the life of the loan (if you put down less than 10%)

- Property must meet FHA appraisal standards

In neighborhoods throughout Lynnwood and Lake Forest Park, FHA financing helps buyers enter the market despite higher home prices. The ongoing mortgage insurance premium represents the primary drawback, typically adding $150-$300 monthly depending on your loan amount.

VA and USDA Loan Programs

VA loans serve military members, veterans, and eligible spouses with exceptional benefits including zero down payment, no mortgage insurance, and competitive rates. If you qualify for VA benefits, this program typically offers the best overall value.

USDA loans support buyers purchasing in eligible rural and suburban areas. While Seattle proper doesn't qualify, portions of Mill Creek and Everett may be eligible depending on population density and location. These loans also offer zero down payment options for income-qualified buyers.

Down Payment Strategies and Programs

The down payment requirement often represents the biggest hurdle for first-time buyers. Understanding your options and local assistance programs can significantly accelerate your path to homeownership.

How Much Do You Really Need?

Contrary to popular belief, you don't need 20% down to buy your first home. Here's the reality across different loan types:

| Loan Type | Minimum Down Payment | PMI Requirement |

|---|---|---|

| Conventional | 3% | Yes (under 20%) |

| FHA | 3.5% | Yes (life of loan) |

| VA | 0% | No |

| USDA | 0% | Yes (annual fee) |

For a $600,000 home in Bellevue (near the median price), a 3% conventional down payment equals $18,000, while 5% requires $30,000. These figures are substantially more accessible than the $120,000 needed for 20% down.

Washington State Down Payment Assistance

Washington State offers several programs specifically designed to help first-time buyers overcome the down payment barrier. The Washington State Housing Finance Commission provides down payment assistance loans that can cover 3-5% of the purchase price.

Additional resources include:

- Seattle Office of Housing programs for income-qualified buyers

- Employer assistance programs common among major Seattle tech companies

- First-time buyer grants through local housing authorities

- IRA withdrawals (up to $10,000 penalty-free for first homes)

Working with an experienced Seattle mortgage broker helps you identify and layer these programs effectively, sometimes combining multiple sources to minimize your upfront cash requirement.

Credit and Income Qualification Guidelines

Understanding how lenders evaluate your financial profile allows you to strengthen your application before submitting it. The mortgage for first time buyers approval process examines three primary areas: credit, income, and assets.

Credit Score Requirements by Loan Type

Your credit score directly influences both loan approval and the interest rate you'll receive. Higher scores unlock better terms and lower monthly payments.

Minimum credit score requirements:

- Conventional: 620 (though 680+ gets better pricing)

- FHA: 580 for 3.5% down, 500 for 10% down

- VA: No official minimum (most lenders want 620+)

- USDA: 640 typical minimum

In Seattle's competitive market, aiming for a 700+ credit score positions you advantageously. For buyers in Redmond and Kirkland working in tech, strong income often pairs with solid credit, but recent credit inquiries or student loans may impact scores temporarily.

Qualifying Complex Income Streams

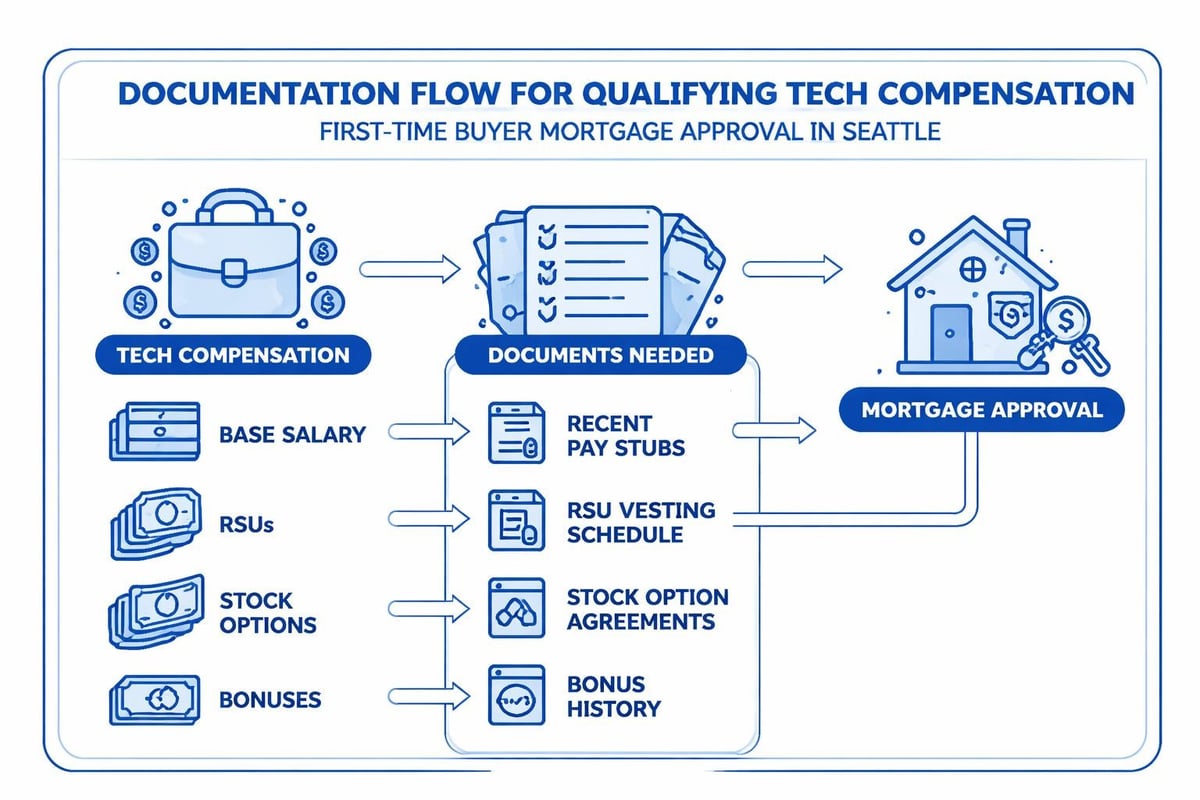

Tech professionals face unique qualification scenarios with equity compensation, bonuses, and stock options. Underwriters can include these income sources, but documentation requirements are specific:

- Base salary: Requires two recent paystubs and W-2s

- RSUs and stock grants: Typically need 2-year history of vesting

- Annual bonuses: Averaged over 2 years if consistently received

- Stock options: Evaluated based on vesting schedule and exercise history

For self-employed buyers or those with commission income, tax returns for the past two years provide the foundation for income calculation. A knowledgeable loan officer specializing in complex compensation structures ensures you maximize your qualifying income.

Debt-to-Income Ratio Explained

Your debt-to-income (DTI) ratio compares monthly debt obligations to gross monthly income. Lenders use this metric to assess your ability to manage the new mortgage payment alongside existing debts.

Front-end DTI (housing ratio): Your proposed housing payment (PITI: principal, interest, taxes, insurance) divided by gross monthly income. Most programs allow up to 28-31% for conventional loans.

Back-end DTI (total ratio): All monthly debt payments including the new mortgage, divided by gross income. Conventional loans typically max out at 45-50%, while FHA allows up to 50-56% with compensating factors.

Example DTI Calculation

Monthly gross income: $10,000

Proposed mortgage payment: $3,000

Car payment: $400

Student loans: $300

Credit cards: $100

Front-end DTI: $3,000 ÷ $10,000 = 30%

Back-end DTI: $3,800 ÷ $10,000 = 38%

This scenario qualifies comfortably for most conventional programs. If your ratios exceed guidelines, strategies include paying down debt, increasing down payment, or securing a co-borrower.

The First-Time Buyer Mortgage Process

Understanding the timeline and steps involved helps you prepare documentation and set realistic expectations. Comparing mortgage lenders early in the process ensures you select the right partner for your situation.

Step-by-Step Application Timeline

- Pre-approval consultation (1-2 days): Review finances, pull credit, analyze income

- Documentation submission (3-5 days): Provide paystubs, bank statements, tax returns, identification

- Underwriting review (5-7 days): Lender verifies all documentation and confirms approval

- Home search and offer: Pre-approval strengthens your position with sellers

- Purchase agreement: Execute contract with agreed-upon terms and timeline

- Full application submission (1 day): Submit complete loan application with property details

- Appraisal and title work (7-10 days): Property valuation and title search completed

- Final underwriting (3-5 days): Conditions cleared, final approval issued

- Clear to close (2-3 days): Final walkthrough, sign closing documents

- Funding and recording (1 day): Loan funds, deed records, you receive keys

The complete process typically spans 30-45 days, though experienced lenders with streamlined processes can close in as few as 9-15 business days when needed. In Seattle's competitive market where multiple offers are common, closing speed can differentiate your offer from others.

Common First-Time Buyer Mistakes to Avoid

Learning from others' experiences helps you sidestep pitfalls that can delay or derail your home purchase. These mistakes appear frequently across the Greater Seattle area.

Financial Missteps

Changing jobs during the process: Lenders verify employment right before closing. Switching employers, especially to a different industry or compensation structure, can trigger re-underwriting or denial.

Making large purchases: Financing furniture, cars, or taking on new credit cards alters your DTI ratio and may disqualify you from the approved loan amount.

Depleting savings: You need reserves for closing costs, moving expenses, and post-purchase repairs. Withdrawing retirement funds or borrowing from family should be strategic decisions made with full knowledge of implications.

Documentation Errors

Incomplete or delayed documentation extends timelines unnecessarily. Have these items organized before starting:

- Two years of W-2s and tax returns (all schedules)

- Two months of bank statements for all accounts

- Recent paystubs covering 30 days

- Gift letters if receiving down payment assistance from family

- Explanations for any credit issues or employment gaps

Market Strategy Issues

In competitive markets like Shoreline and Everett, strategic errors can cost you the home:

Waiving inspection contingencies without professional guidance: While common in hot markets, this carries significant risk for first-time buyers unfamiliar with property condition assessment.

Offering above appraised value without cash reserves: If the home appraises below your offer price, you'll need cash to cover the difference or renegotiate terms.

Skipping pre-approval: Sellers favor pre-approved buyers over pre-qualified ones. The distinction matters, especially when competing against multiple offers.

Seattle-Specific Market Considerations

The Greater Seattle housing market presents unique challenges and opportunities for first-time buyers. Understanding local dynamics helps you time your purchase and structure competitive offers.

Neighborhood Price Variations

Home prices vary significantly across Seattle metro submarkets:

| Area | Median Home Price | Typical Entry Point |

|---|---|---|

| Seattle (central neighborhoods) | $825,000+ | $650,000 |

| Bellevue | $1,100,000+ | $750,000 |

| Redmond | $950,000+ | $700,000 |

| Shoreline | $775,000+ | $600,000 |

| Lynnwood | $650,000+ | $500,000 |

| Everett | $575,000+ | $450,000 |

These figures reflect 2026 market conditions and demonstrate why expanding your search to areas like Lake Forest Park, Mill Creek, and Everett often provides better value and more accessible entry points for first-time buyers.

Condo and Townhome Considerations

Many first-time buyers in Seattle start with condos or townhomes, which offer lower price points and reduced maintenance responsibilities. However, lender requirements add complexity:

- FHA condo approval: Building must be on FHA-approved list

- Warrantability review: Fannie Mae/Freddie Mac guidelines for conventional financing

- HOA financial health: Reserves, delinquency rates, litigation status

- Owner-occupancy ratio: Typically need 51%+ owner-occupied units

Working with a broker experienced in Seattle's condo market ensures you avoid properties with financing restrictions that could complicate your purchase or future resale.

Interest Rate Impact on Affordability

Interest rates dramatically affect your purchasing power and monthly payment. Understanding this relationship helps you make informed decisions about timing and loan structure.

Rate Comparison Example

For a $600,000 loan amount (30-year fixed):

| Interest Rate | Monthly P&I Payment | Total Interest Paid |

|---|---|---|

| 5.5% | $3,406 | $626,160 |

| 6.0% | $3,597 | $694,920 |

| 6.5% | $3,790 | $764,400 |

| 7.0% | $3,992 | $837,120 |

A 0.5% rate difference equals approximately $191 per month or $68,760 over the loan's life. This underscores the value of strong credit, competitive lender pricing, and strategic rate lock timing.

Rate Lock Strategies

Once approved, you'll need to lock your interest rate. Common lock periods include:

- 30-day lock: Standard for quick closings

- 45-day lock: More common timeframe allowing flexibility

- 60-day lock: Used when delays are anticipated or construction is involved

Locking too early risks missing rate improvements, while waiting too long exposes you to increases. Experienced loan officers monitor market trends and recommend optimal timing based on your specific transaction.

Maximizing Your Buying Power

First-time buyers often leave purchasing power on the table by not fully understanding how lenders calculate qualifying income and acceptable debt levels. Strategic preparation can increase your approved loan amount by tens of thousands of dollars.

Credit Optimization Techniques

Improving your credit score before applying yields significant benefits:

- Pay down revolving balances to below 30% of credit limits (ideally under 10%)

- Avoid closing old credit cards, which reduces your credit history length

- Dispute any errors on credit reports through all three bureaus

- Avoid new credit inquiries in the 6 months before applying

- Become an authorized user on someone else's established account with perfect payment history

A score increase from 680 to 720 can reduce your interest rate by 0.25-0.50%, saving thousands over the loan term while also improving approval odds.

Income Documentation Strategies

For buyers with variable income, bonus compensation, or stock grants, documentation strategy matters:

- Consistent receipt: Two-year history shows reliability to underwriters

- Year-over-year increases: Growing compensation trends favorably

- Clear paper trail: Maintain paystubs and vesting schedules documenting all income sources

- CPA letters: Self-employed buyers benefit from accountant verification letters

Tech professionals in Bellevue and Redmond with substantial equity compensation should explore specialized loan programs designed for complex income structures. These programs recognize that stock-based compensation provides reliable income even when tax returns show lower W-2 wages due to deferred vesting.

Property Type and Financing Considerations

Not all properties qualify equally across loan programs. Understanding restrictions helps you focus your search on homes that align with your financing strategy.

Single-Family Homes

Traditional single-family residences offer the most financing flexibility. All loan types readily approve these properties, assuming they meet basic condition standards. FHA and VA loans require the property to meet minimum property standards (MPS) verified during appraisal.

Condominiums and Townhomes

Condos require additional lender scrutiny focusing on the homeowners association (HOA):

- Financial reserves adequate for building maintenance

- Low delinquency rates among unit owners

- No pending litigation against the association

- Proper insurance coverage (especially in Seattle's earthquake zone)

- Compliance with Fannie Mae/Freddie Mac warrantability requirements

Some Seattle buildings maintain "pre-approved" status with major lenders, streamlining the financing process. Others require full association review adding 7-10 days to closing timelines.

Multi-Family Properties

Purchasing a duplex, triplex, or fourplex allows first-time buyers to offset mortgage payments with rental income. Lenders will typically credit 75% of market rent toward qualifying income after you've established rental history.

These properties require:

- Larger down payments (15-25% typical)

- Higher credit scores (usually 680+)

- Greater reserves (6 months PITI common requirement)

- Property management experience or plan

The strategy works exceptionally well in neighborhoods like Lake Forest Park and parts of Seattle where rental demand remains strong and property values have shown consistent appreciation.

Working with Your Mortgage Broker

Selecting the right mortgage professional dramatically impacts your experience and outcome. The mortgage for first time buyers process benefits tremendously from experienced guidance, especially in complex markets like Seattle.

What to Look for in a Broker

Local expertise: Understanding Seattle-area programs, property types, and market dynamics

Communication style: Responsiveness, clarity, and proactive updates throughout the process

Loan product access: Ability to offer multiple loan types and investor options

Technology platform: Streamlined application, document upload, and status tracking

Track record: Reviews, testimonials, and years of experience in the market

First-time buyer specialists bring particular value by anticipating questions, explaining complex concepts clearly, and guiding you through decisions without pressure or confusion.

Questions to Ask Before Committing

Before selecting your mortgage broker, ask:

- What loan programs do you recommend for my situation and why?

- What's your average closing timeline for first-time buyers?

- How do you handle rate locks and pricing adjustments?

- What are all fees associated with your services?

- Can you provide references from recent Seattle-area first-time buyers?

- How do you communicate throughout the process?

Comprehensive answers demonstrate experience and commitment to your success. According to research on first-time buyer challenges, working with trusted advisors significantly improves outcomes and reduces stress throughout the purchase process.

Closing Costs and Final Expenses

Beyond your down payment, closing costs typically add 2-5% of the purchase price to your upfront cash requirement. Understanding these expenses helps you budget accurately and avoid last-minute surprises.

Typical Closing Cost Breakdown

For a $600,000 purchase in Seattle:

- Lender fees: $1,500-$2,500 (origination, processing, underwriting)

- Title and escrow: $2,000-$3,500 (title insurance, escrow fees, recording)

- Appraisal: $500-$750

- Credit report: $75-$100

- Home inspection: $400-$600 (paid separately, not at closing)

- Prepaid items: $3,000-$5,000 (property taxes, homeowners insurance, interest)

- HOA transfer fees: $200-$500 (condos and townhomes)

Total estimated closing costs: $7,675-$12,950

Seller Concessions and Credits

In balanced or buyer-favorable markets, you can often negotiate seller-paid closing costs. Conventional loans allow up to 3% seller concessions with less than 10% down, or up to 6% with 10%+ down. FHA allows up to 6% regardless of down payment amount.

This strategy preserves your cash for reserves, repairs, or future investments while reducing immediate out-of-pocket expenses. Your real estate agent and mortgage broker should coordinate on structuring offers to maximize this benefit.

Post-Closing Financial Planning

Your mortgage responsibilities extend beyond closing day. Smart financial planning ensures long-term success and builds equity efficiently.

Building an Emergency Fund

Homeownership introduces maintenance costs, repairs, and unexpected expenses. Financial advisors recommend 3-6 months of housing expenses in accessible savings. For a $3,500 monthly payment, this equals $10,500-$21,000.

Prioritize building reserves through:

- Automated monthly transfers to savings

- Allocating bonuses and tax refunds to reserves

- Reducing discretionary spending temporarily after purchase

Equity Acceleration Strategies

Once settled in your home, consider strategies to build equity faster:

- Biweekly payments: Paying half your mortgage every two weeks results in 13 full payments annually instead of 12

- Principal curtailment: Adding extra amounts to principal with each payment

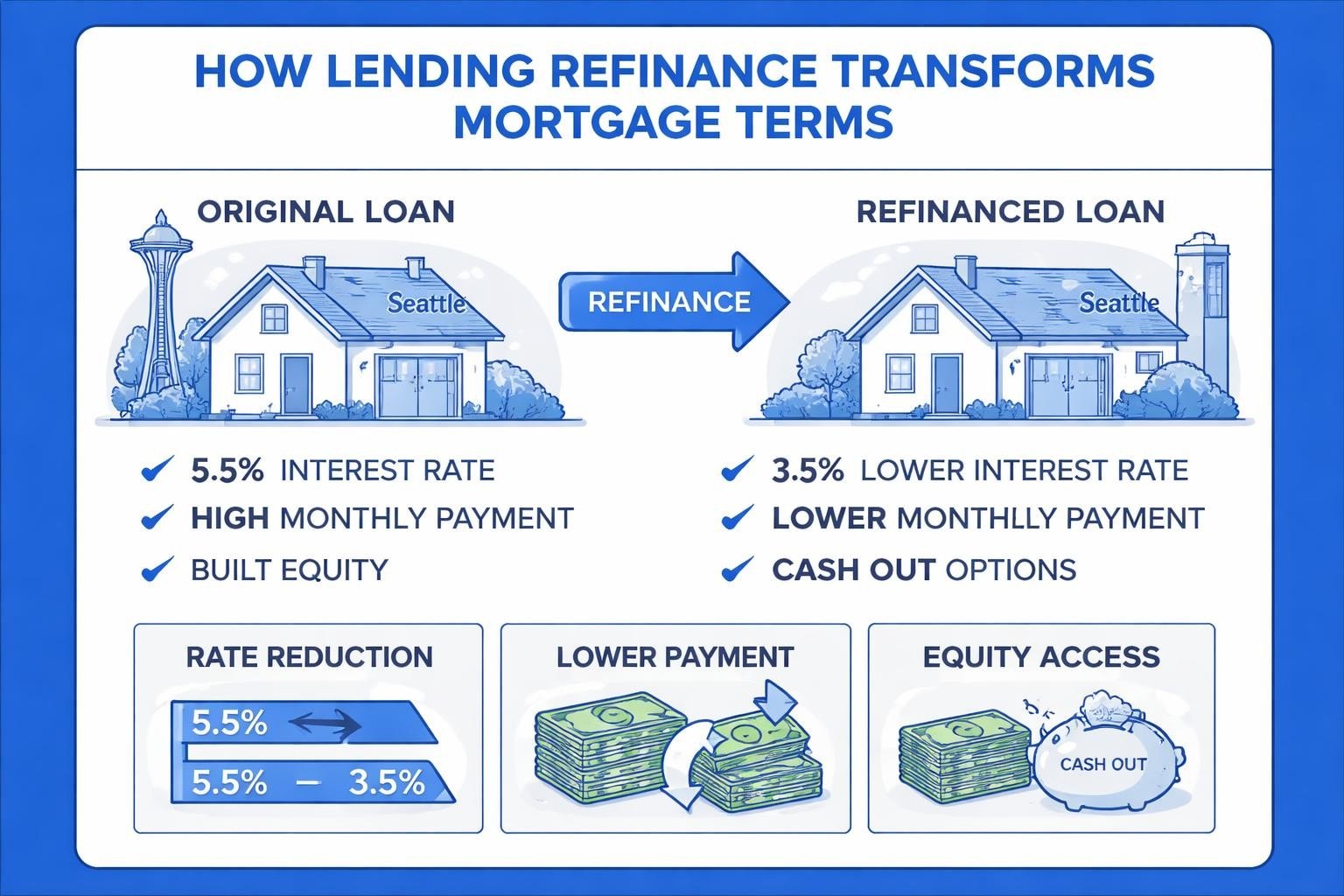

- Refinancing: If rates drop significantly, refinancing to a lower rate or shorter term builds equity faster

Even modest additional payments compound significantly over time. Adding $200 monthly to a $600,000 30-year loan at 6% saves approximately $120,000 in interest and pays off the loan 7 years early.

Navigating the mortgage for first time buyers in Seattle requires understanding loan options, qualification requirements, and local market dynamics. With proper preparation and expert guidance, you can confidently secure financing that aligns with your financial goals and positions you for long-term success. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping first-time buyers throughout Seattle, Bellevue, Redmond, and surrounding communities make informed decisions backed by transparent communication and proven results. Whether you're a tech professional with complex compensation or a traditional W-2 employee, we specialize in maximizing your buying power and closing efficiently in competitive markets. Start your homeownership journey with confidence by connecting with Mortgage Reel today.