Veterans, active-duty service members, and eligible surviving spouses have access to one of the most powerful financing tools in real estate: the VA home loan. Unlike conventional mortgages, these loans require no down payment, no private mortgage insurance, and offer competitive interest rates. However, not all va home loan lenders operate the same way. Understanding how to identify qualified lenders, compare their offerings, and navigate the approval process can save you thousands of dollars and eliminate unnecessary stress. This guide provides comprehensive insights into selecting the right VA lender in Seattle, Bellevue, Redmond, and surrounding areas, with practical strategies for maximizing your benefits in 2026.

What Makes VA Home Loan Lenders Different

VA home loan lenders are financial institutions approved by the Department of Veterans Affairs to originate loans backed by the VA guarantee. This guarantee reduces lender risk, allowing them to offer more favorable terms than traditional mortgages.

The VA doesn't actually issue loans. Instead, approved lenders work directly with borrowers while the VA provides a partial guarantee on each loan. This arrangement creates a unique lending environment where lender experience with VA guidelines becomes critical.

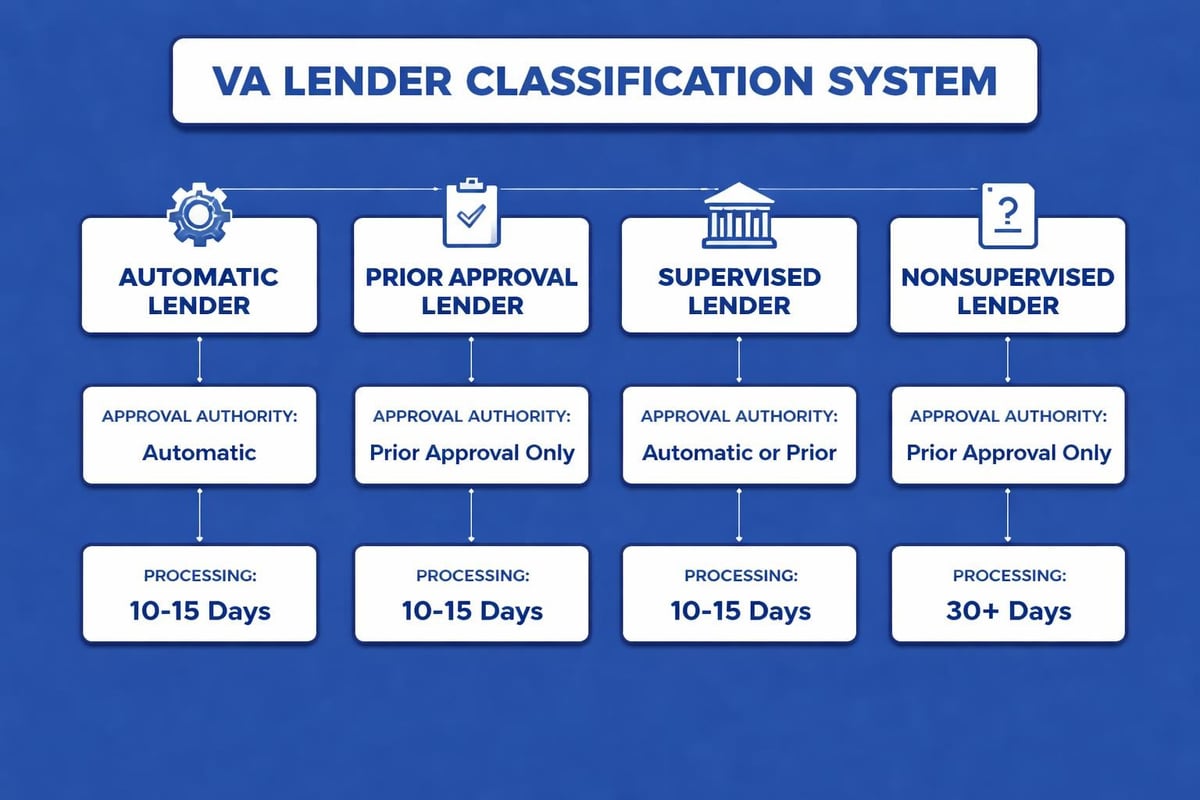

Lender Approval Classifications

Not all institutions have the same level of authority when processing VA loans. The VA recognizes several classifications:

- Automatic lenders: Full authority to close loans without prior VA approval

- Prior approval lenders: Must submit loans for VA review before closing

- Supervised lenders: Operate under government agency supervision

- Nonsupervised lenders: Private institutions approved by the VA

Automatic lenders typically process loans faster because they have demonstrated expertise and established underwriting standards that meet VA requirements. When time matters in competitive markets like Seattle and Kirkland, working with an automatic lender can mean the difference between securing your dream home and losing it to another buyer.

Key Benefits VA Lenders Provide

Understanding what va home loan lenders can offer helps you recognize value during your search. These benefits extend beyond basic financing and include several protections designed specifically for military families.

| Benefit | Description | Impact |

|---|---|---|

| No Down Payment | Purchase up to $766,550 with $0 down in Seattle (2026 limit) | Preserves cash for moving costs and reserves |

| No PMI | Private mortgage insurance not required at any LTV | Saves $100-300+ monthly compared to conventional loans |

| Competitive Rates | Typically 0.25%-0.5% lower than conventional | Reduces lifetime interest by $30,000-$50,000 on average |

| Lenient Credit | Minimum scores often 580-620 vs. 640+ conventional | Expands accessibility for service members |

| Limited Closing Costs | VA restricts fees lenders can charge | Prevents predatory practices |

The most significant advantage for Seattle-area buyers is the no down payment requirement. With median home prices exceeding $800,000 in many neighborhoods, this benefit allows veterans to compete without needing $160,000 in cash reserves.

Funding Fee Considerations

Most VA loans include a funding fee, a one-time charge that helps sustain the program. The fee varies based on down payment, loan type, and whether you're a first-time or subsequent VA borrower:

- First-time use, zero down: 2.15% of loan amount

- Subsequent use, zero down: 3.3% of loan amount

- With 5% down: 1.5% first use, 1.5% subsequent

- With 10% down: 1.25% first use, 1.25% subsequent

Veterans receiving disability compensation are exempt from this fee entirely. The funding fee can be rolled into your loan amount, though this increases your overall borrowing cost.

How to Identify Qualified VA Home Loan Lenders

Selecting the right lender requires evaluating multiple factors beyond advertised interest rates. In Seattle's fast-paced housing market, lender competence directly impacts your success.

Verification Steps

Start by confirming the lender's VA approval status. The Department of Veterans Affairs maintains a registry of all approved institutions, including their classification level and approval date.

Next, assess their VA loan volume. Lenders processing hundreds of VA loans annually develop systems and expertise that benefit borrowers. The VA publishes lender statistics showing origination volumes by institution, providing transparency into each lender's experience level.

Experience indicators to evaluate:

- Years participating in VA lending program

- Monthly VA loan closings

- Average processing timeline

- Percentage of loans approved on first submission

- Staff with VA-specific training

For Seattle buyers, particularly those working at Amazon, Microsoft, or other tech employers, finding a lender who understands how to qualify RSU income and stock compensation within VA guidelines is essential. This specialized knowledge can increase your purchasing power by $100,000 or more.

Questions to Ask Potential Lenders

When interviewing va home loan lenders, focus on specific, actionable responses rather than marketing promises:

"What percentage of your monthly closings are VA loans?" This reveals whether VA lending is a core competency or occasional service.

"Can you close in under 21 days?" Speed matters when competing against cash offers in Bellevue and Redmond.

"How do you handle appraisal issues?" VA appraisals include property condition requirements. Experienced lenders know how to navigate repairs and recertifications.

"What closing costs will I actually pay?" VA regulations limit fees, but lenders can charge differently within those parameters.

Understanding VA Loan Types and Lender Offerings

The VA backs several distinct loan programs, each serving different financial needs. Not all lenders offer every program, making it important to match your situation with lender capabilities.

Purchase Loans

Standard VA purchase loans allow you to buy a primary residence with no down payment. These work for single-family homes, condos (if VA-approved), townhouses, and manufactured homes meeting specific standards.

In Seattle and Shoreline, where condo inventory represents a significant market segment, verify your lender has experience with VA condo certification. Units in non-approved buildings require individual approval, adding time to your transaction.

Cash-Out Refinance

Cash-out refinancing lets you replace your current mortgage (VA or conventional) with a new VA loan for more than you owe, taking the difference in cash. This strategy works well for:

- Consolidating high-interest debt

- Funding home improvements

- Covering education expenses

- Building emergency reserves

Lenders can approve cash-out refinances up to 100% of your home's appraised value. With Seattle home values appreciating significantly since 2020, many veterans have substantial equity available to access.

IRRRL (Interest Rate Reduction Refinance Loan)

The VA streamline refinance, called an IRRRL, allows you to refinance your existing VA loan to a lower rate with minimal documentation. No appraisal, no income verification, and reduced paperwork make this the fastest VA loan to process.

IRRRL requirements:

- Currently have a VA loan

- Be current on payments (no 30-day lates in past 12 months)

- New loan must reduce your interest rate or payment

- Must recoup closing costs within 36 months

Some lenders offer "zero-cost" IRRRLs where they cover your closing costs in exchange for a slightly higher rate. Run the numbers carefully, as this tradeoff doesn't always benefit long-term homeowners.

Comparing Rates and Fees Across Lenders

Interest rates grab attention, but total borrowing cost depends on the complete fee structure. Understanding how to compare lenders accurately prevents costly mistakes.

Rate Components

Your final interest rate consists of:

- Base rate: The current market rate for VA loans

- Lender margin: Profit added by your lender

- Points: Optional upfront fees to reduce your rate

- Rate adjustments: Based on credit score, loan amount, and occupancy

Two lenders quoting 6.25% might have drastically different fee structures. One charges zero points with $2,000 in fees; another charges 1 point ($7,500 on a $750,000 loan) with $800 in fees.

Allowable vs. Non-Allowable Fees

VA regulations protect borrowers by limiting what lenders can charge. The Consumer Financial Protection Bureau details these protections in resources designed for service members.

You CAN be charged for:

- Origination fee (typically 1% of loan amount)

- Appraisal

- Credit report

- Title insurance and related services

- Recording fees

- Prepaid items (taxes, insurance, interest)

- Funding fee

You CANNOT be charged for:

- Attorney fees (except actual title work)

- Loan processing fees

- Document preparation fees

- Application fees

- Underwriting fees

If a lender's estimate includes prohibited fees, find another lender. This signals either incompetence or intentional deception.

Securing the Best Rate

Timing your rate lock strategically maximizes savings. Rates fluctuate daily based on economic indicators, Federal Reserve policy, and investor appetite for mortgage-backed securities.

Work with lenders who explain rate trends rather than pressuring immediate locks. In Lake Forest Park and Mill Creek, where homes may need minor repairs to satisfy VA appraisal requirements, locking too early can result in expiring locks and extension fees.

Rate lock strategies:

- 30-day lock: Best for condos and turnkey homes with quick closings

- 45-day lock: Standard for most transactions

- 60-day lock: New construction or complex transactions

- Float-down option: Allows one rate reduction if market improves (usually costs 0.125%-0.25% upfront)

Working with experienced Seattle mortgage brokers gives you access to multiple lenders simultaneously, creating competitive pressure that often results in better final terms than approaching a single bank directly.

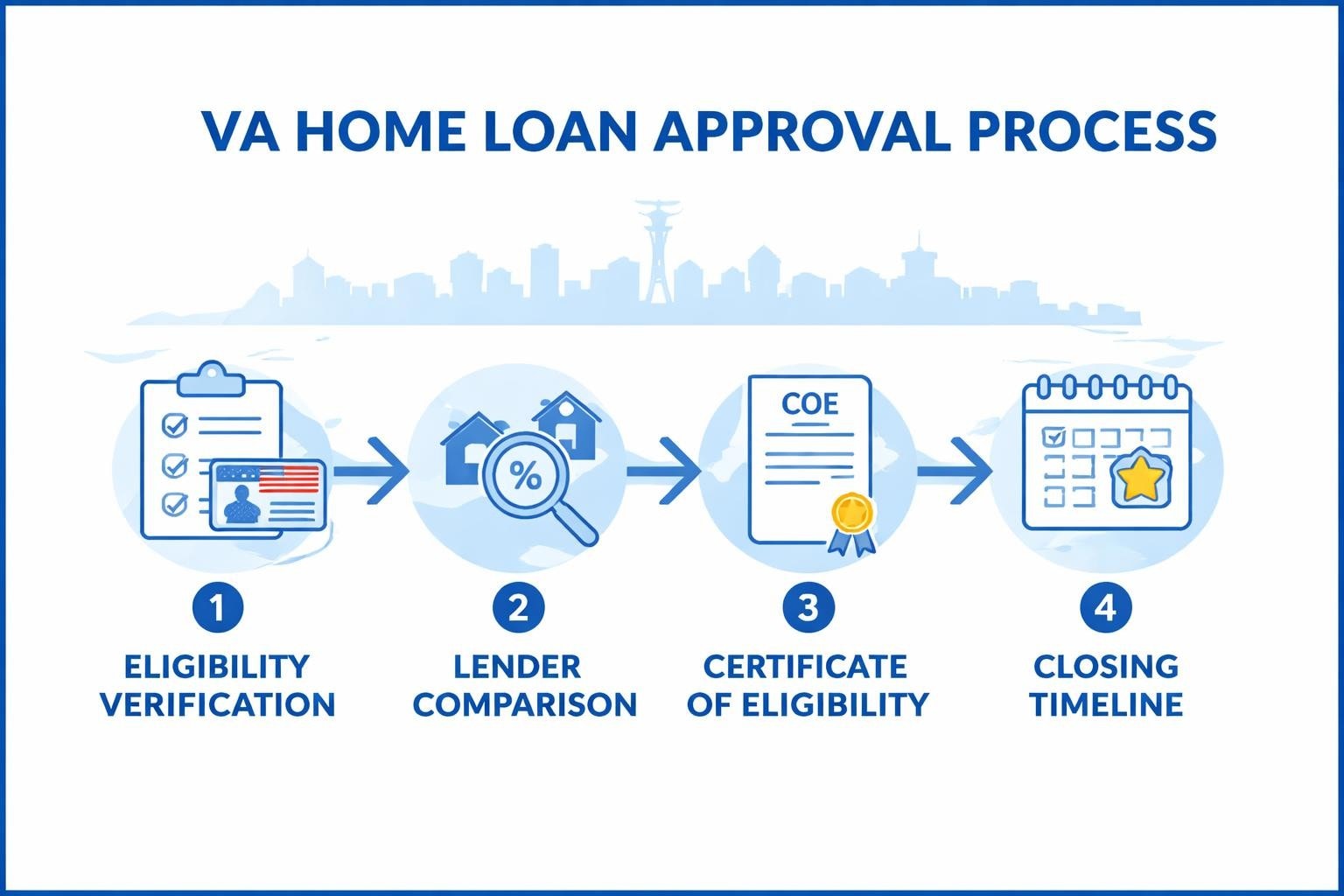

The VA Loan Application Process

Understanding the timeline and requirements helps you prepare documentation and avoid delays. The process follows a structured path from pre-qualification through closing.

Certificate of Eligibility (COE)

Your COE proves VA loan eligibility to lenders. Most va home loan lenders can obtain this electronically within minutes during your application. You can also request it directly from the VA through their online portal, by mail, or through your lender.

Eligibility generally requires:

- 90+ consecutive days of active service during wartime

- 181+ days during peacetime

- 6+ years in National Guard or Reserves

- Spouse of service member who died on duty or from service-connected disability

If you've previously used VA loan benefits, your COE shows remaining entitlement. In high-cost areas like Seattle, veterans often have sufficient entitlement for multiple loans simultaneously.

Documentation Requirements

VA lenders need standard mortgage documentation plus military-specific items:

Financial documents:

- 2 years tax returns with all schedules

- 2 most recent pay stubs

- 2 months bank statements for all accounts

- Retirement account statements if using for reserves

- Explanations for any credit issues

Military documents:

- DD-214 (Certificate of Release or Discharge)

- Current Leave and Earnings Statement (active duty)

- Statement of Service (active duty without DD-214)

For Seattle tech professionals with RSU income, provide your most recent equity statement and vesting schedule. Experienced lenders know how to calculate usable income from unvested shares, significantly increasing your buying power for competitive Seattle properties.

Appraisal and Inspection

VA appraisals serve dual purposes: establishing market value and ensuring minimum property standards. The property must be safe, sound, and sanitary.

Common issues in older Seattle homes include:

- Peeling paint (built pre-1978)

- Missing handrails on stairs

- Damaged roof surfaces

- Inadequate heating systems

- Non-functioning appliances included in sale

Sellers must complete required repairs before closing. Skilled lenders help negotiate these repairs during your purchase agreement, preventing last-minute transaction failures.

Local Market Considerations for Seattle Veterans

Seattle's housing market presents unique challenges and opportunities for VA borrowers. Understanding regional dynamics helps you compete effectively.

Loan Limits and Purchasing Power

As of 2026, veterans with full entitlement can borrow the conforming loan limit ($766,550 in Seattle) with no down payment. Above this amount, you'll need a down payment of 25% of the difference.

Example: $900,000 purchase price

- Amount over limit: $133,450

- Required down payment: $33,363 (25% of excess)

Many Seattle-area properties exceed conforming limits, particularly in neighborhoods like Bellevue, Kirkland, and parts of Redmond. Veterans with disability ratings may qualify for additional benefits that reduce or eliminate funding fees, preserving more cash for larger down payments when needed.

Competing in Multiple Offer Situations

Sellers and listing agents sometimes hesitate accepting VA offers due to misconceptions about:

- Lengthy approval timelines

- Strict appraisal requirements

- Lower likelihood of closing

Counter these perceptions with:

- Pre-approval from a reputable lender: Generic pre-qualifications carry little weight; detailed pre-approvals from established lenders demonstrate serious intent

- Proof of quick closing capability: Lenders who close in 15-21 days match or beat conventional timelines

- Appraisal gap coverage: Offering to cover appraisal shortfalls up to a specific amount shows financial strength

- Personal letter: Sharing your service background often resonates with sellers

In Everett and Lynnwood, where competition remains intense but slightly less frenzied than core Seattle neighborhoods, VA buyers frequently succeed with properly structured offers and experienced representation.

Working with Mortgage Brokers vs. Direct Lenders

Veterans can access VA loans through mortgage brokers or direct lenders. Each approach offers distinct advantages depending on your situation.

Mortgage Broker Benefits

Brokers maintain relationships with multiple lenders, allowing them to:

- Shop your scenario to 10+ lenders simultaneously

- Match your unique situation with specialized lenders

- Negotiate better terms through volume relationships

- Provide backup options if your first-choice lender faces delays

This model particularly benefits:

- Self-employed veterans with complex income documentation

- Borrowers with credit challenges

- Buyers needing exceptionally fast closings

- Those purchasing properties requiring renovation

Understanding your approval timeline helps set realistic expectations when working with either broker or direct lender channels.

Direct Lender Advantages

Banks and credit unions offering VA loans directly provide:

- Potentially lower costs (no broker compensation)

- Single point of contact throughout the process

- Relationship benefits for existing customers

- In-house underwriting and processing

Direct lenders work well for straightforward transactions with strong credit, stable employment, and standard property types.

Making Your Choice

Evaluate based on:

Your financial profile: Complex income or credit situations benefit from broker expertise

Property type: Unique properties (condos needing approval, fixer-uppers, manufactured homes) often require specialized lenders that brokers can access

Timeline pressure: Brokers with multiple lender relationships provide fallback options if one lender experiences delays

Rate sensitivity: Brokers can create competitive bidding among lenders, though direct lenders sometimes offer relationship discounts

Many Seattle veterans discover that working with experienced local mortgage brokers who specialize in VA lending provides the best combination of rate, service, and reliability.

Special Considerations for Seattle Tech Professionals

Veterans working in Seattle's technology sector face unique income qualification challenges and opportunities when using VA benefits.

RSU and Stock Compensation Qualification

Restricted stock units, employee stock purchase plans, and stock options require specialized underwriting knowledge. The VA allows this income, but lenders apply it differently:

Vested RSUs: Count 100% of value after 2-year history

Unvested RSUs: Some lenders count 0%, others average 50-70% based on vesting schedule

ESPP: Typically counted at 100% with 2-year history

Stock options: Usually excluded unless exercised with established sale pattern

A $150,000 base salary plus $100,000 annual RSU vesting creates vastly different buying power depending on whether your lender counts $0, $50,000, or $100,000 of equity income.

Jumbo VA Loans

Seattle's high housing costs frequently push veterans into jumbo territory. While the VA doesn't technically have loan limits anymore (for those with full entitlement), lenders maintain internal maximums, typically $1.5-2 million for VA loans.

Jumbo VA requirements often include:

- Credit scores of 660-680+

- Debt-to-income ratios under 45%

- 6-12 months reserves

- Larger down payments for amounts exceeding $766,550

Finding lenders experienced with jumbo financing in Seattle ensures you receive accurate qualification guidance rather than discovering limitations late in your search.

Common VA Loan Mistakes to Avoid

Even experienced homebuyers make preventable errors when using VA benefits. Awareness helps you sidestep these pitfalls.

Not Shopping Multiple Lenders

The first lender you contact may not offer the best terms. Rate and fee differences of 0.25% and $2,000 respectively create $15,000+ in lifetime cost variations on a $750,000 loan.

Comparison shopping strategy:

- Contact 3-5 lenders within a 14-day period (counts as single credit inquiry)

- Request Loan Estimates for identical scenarios

- Compare APR, closing costs, and loan terms side-by-side

- Ask about lender-specific overlays beyond VA minimums

Skipping Pre-Approval

Pre-qualification provides rough estimates; pre-approval involves documentation review and underwriter assessment. In competitive Seattle neighborhoods, sellers rarely consider offers without solid pre-approval letters.

Quality pre-approval demonstrates:

- Verified income and assets

- Reviewed credit and liabilities

- Underwriter preliminary approval

- Specific loan amount and program

This documentation separates serious buyers from casual shoppers, particularly important when competing against conventional and cash offers.

Ignoring Property Eligibility

Not all properties qualify for VA financing. Common issues include:

Condos: Building must have VA approval or unit requires individual approval (slower process)

Mixed-use properties: Residential portion must be primarily occupied

Investment properties: VA loans require owner occupancy; no rental properties

Property condition: Must meet Minimum Property Requirements (MPRs)

Review VA eligibility before writing offers. For first-time buyers in Seattle, understanding these limitations prevents disappointment and wasted inspection fees.

Overlooking Residual Income Requirements

Unlike debt-to-income ratios used for conventional loans, VA lenders must also verify residual income: money remaining after paying all debts and housing costs.

Seattle area residual income requirements (family of 4):

- Loans under $79,999: $1,003/month

- Loans $80,000+: $1,117/month

This calculation includes state and federal taxes, Social Security, retirement contributions, and all debt obligations. Veterans with high incomes but also high debts may struggle meeting these thresholds despite strong DTI ratios.

Refinancing Strategies with VA Lenders

Current VA loan holders have unique refinancing opportunities that conventional borrowers don't access. Strategic refinancing maximizes long-term savings.

When IRRRL Makes Sense

The streamlined VA refinance works best when:

- Rates dropped 0.5%+ since your original loan

- You plan to keep the home 3+ years

- You want to eliminate monthly PMI from a conventional loan

- Your current VA loan has an adjustable rate you want to fix

Calculate your break-even point by dividing closing costs by monthly savings. If you recover costs in under 24 months and plan to stay longer, refinancing typically makes financial sense.

Cash-Out Refinance Applications

Access home equity for strategic purposes:

High-interest debt consolidation: Credit cards at 18-24% APR vs. mortgage at 6-7% creates substantial savings

Home improvements: Kitchen and bathroom updates in Seattle homes often return 60-80% of cost at resale

Investment opportunities: Funding down payments on additional properties or business ventures

Education expenses: College costs for children without high-interest student loans

Maintain sufficient equity for financial security. Extracting every dollar leaves no buffer if home values decline or unexpected repairs emerge.

Removing Non-Veteran Co-Borrowers

VA refinancing allows you to remove non-veteran ex-spouses or co-borrowers from your loan. This restores their eligibility for VA benefits while establishing your sole ownership. Work with lenders experienced in these specific scenarios, as documentation requirements exceed standard refinances.

Red Flags When Selecting VA Lenders

Certain warning signs indicate problematic lenders. Recognizing these patterns protects you from poor experiences and potential financial harm.

Pressure Tactics

Legitimate lenders educate and guide; predatory ones pressure and rush. Be wary of:

- "Rate expires today" urgency on initial contact

- Discouraging rate shopping or comparing offers

- Requesting earnest money before you've signed purchase agreements

- Pushing specific properties or real estate agents

- Refusing to provide written Loan Estimates

Professional lenders understand you need time to evaluate options. They earn your business through competence, not pressure.

Unrealistic Promises

If terms sound too good to be true, they probably are:

- Rates significantly below market averages

- "No closing costs" with unclear rate tradeoffs

- Guaranteed approval regardless of credit or income

- Processing timelines well below industry norms

Verify specific claims with written documentation. Marketing promises mean nothing; Loan Estimates create legal obligations.

Poor Communication

Lender responsiveness during pre-approval predicts service quality during closing. Problems include:

- Taking 48+ hours to return calls or emails

- Providing vague answers to specific questions

- Frequently unavailable or passing you to multiple people

- Unclear about next steps or timeline expectations

Quality lenders maintain proactive communication, updating you regularly even when no action is required. This becomes critical when issues emerge requiring quick decisions.

Hidden Fee Structures

Request detailed fee breakdowns early. Some lenders advertise low rates but compensate through:

- Excessive origination charges

- Rate lock extension fees (if you don't close on time)

- Processing fees despite VA prohibitions

- Required use of affiliated service providers at inflated costs

Compare Loan Estimates line by line. Significant variations in Section B (services you cannot shop for) and Section C (services you can shop for) reveal lender pricing strategies.

Maximizing Your VA Loan Benefits in 2026

Strategic use of VA benefits creates significant financial advantages over conventional financing. Implement these approaches to optimize your experience.

Combining VA Loans with Local Programs

Several Seattle-area programs complement VA benefits:

Washington State Housing Finance Commission: Offers down payment assistance that can cover the VA funding fee or closing costs

Local first-time buyer programs: Available in some King County municipalities, providing additional grants

Energy-efficient mortgages: VA allows including energy improvements in your loan amount

Research available programs with lenders familiar with combining benefits. The application complexity increases, but savings often justify the additional effort.

Building Long-Term Wealth

VA loans create wealth-building opportunities through:

Leverage: Control $750,000 in real estate with $0-$15,000 invested

Appreciation: Seattle home values averaged 6-8% annual growth over the past decade

Equity buildup: Principal reduction plus appreciation creates substantial net worth

Tax benefits: Mortgage interest and property tax deductions (consult your tax advisor)

Veterans who purchased Seattle homes in 2016 with VA loans have seen $200,000-$400,000 in equity gains while paying no PMI and minimal down payments.

Preserving Entitlement for Future Use

Understanding entitlement helps with long-term planning:

Full entitlement: Can get loans up to conforming limits ($766,550 in Seattle) with no down payment

Partial entitlement: Previous VA loan not fully paid off; remaining amount available for additional loans

Restored entitlement: Prior VA loan paid in full or assumed by another veteran; full benefits restored

Many veterans don't realize they can have multiple VA loans simultaneously. If you have sufficient remaining entitlement, you can buy a second home (meeting occupancy requirements) while keeping your first VA-financed property.

Selecting the right VA home loan lender significantly impacts your financing costs, closing timeline, and overall homebuying experience. Veterans in the Seattle area benefit from comparing multiple lenders, understanding local market dynamics, and working with professionals who specialize in qualifying complex income streams common among tech sector employees. Whether you're buying your first home in Shoreline, upgrading to a larger property in Bellevue, or refinancing your current mortgage in Redmond, informed lender selection ensures you maximize your hard-earned VA benefits. Keith Akada at Mortgage Reel brings 25+ years of experience helping Seattle-area veterans navigate VA loans with clarity and confidence, specializing in qualifying RSU and stock compensation to maximize buying power while closing loans in as few as 9 business days.