Navigating Seattle's competitive real estate market requires more than just finding the right property. Between rising home prices across neighborhoods like Bellevue, Redmond, and Kirkland, and the complexity of qualifying income types ranging from W-2 wages to RSUs and stock compensation, the home financing process demands specialized knowledge. Mortgage advisors serve as strategic partners who translate complicated lending guidelines into actionable plans, helping buyers and homeowners make confident decisions about purchase loans, refinancing, and investment property financing.

The Strategic Value of Working with Mortgage Advisors

Professional guidance in mortgage lending delivers measurable advantages that extend far beyond simply submitting loan applications. Experienced advisors analyze your complete financial profile, identify optimal loan programs, and structure financing to maximize purchasing power while minimizing long-term costs.

Understanding Your Complete Financial Picture

Mortgage advisors examine income documentation, employment history, credit profiles, and asset positions to determine what you genuinely qualify for rather than relying on generic online calculators. For tech professionals working at Amazon, Microsoft, or Google in the Seattle area, this expertise proves particularly valuable when qualifying non-traditional income sources.

Key income types advisors help structure:

- Base salary from W-2 employment

- Restricted stock units (RSUs) and vesting schedules

- Stock options and equity compensation

- Annual bonuses and variable pay

- Rental income from investment properties

- Self-employment income requiring detailed documentation

According to research on financial advisory integration, the combination of traditional expertise and modern tools creates superior outcomes compared to purely digital approaches. This hybrid model allows mortgage advisors to leverage technology while applying human judgment to complex financial situations.

Navigating Loan Program Selection

The mortgage industry offers dozens of distinct loan programs, each with specific qualification requirements, down payment thresholds, and pricing structures. Understanding which program aligns with your goals requires detailed knowledge of current guidelines and market conditions.

| Loan Program | Minimum Down Payment | Best For | Key Advantage |

|---|---|---|---|

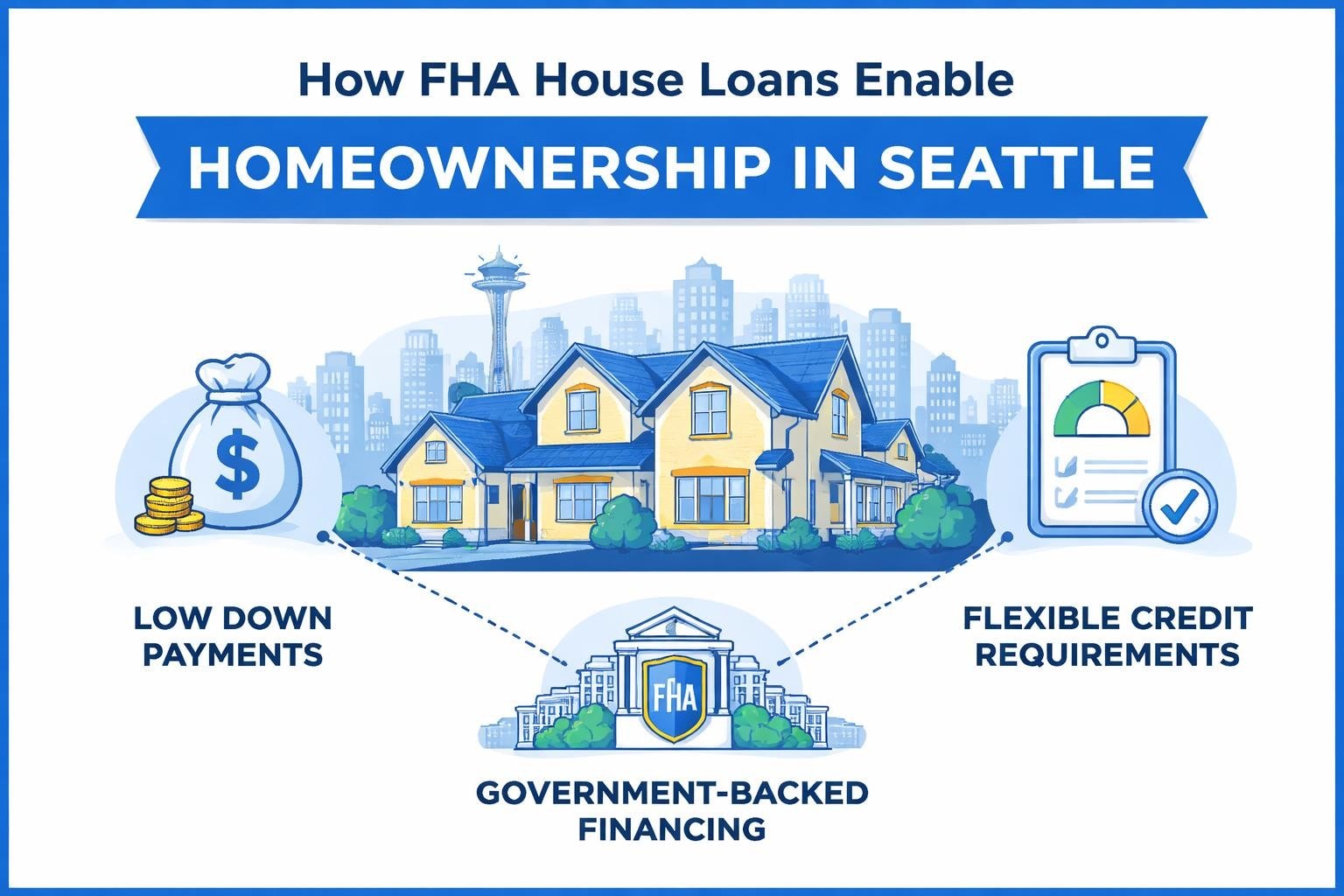

| Conventional | 3% – 5% | Strong credit, stable income | Flexible property types |

| FHA | 3.5% | Lower credit scores, limited savings | Lenient qualification |

| VA | 0% | Military service members | No PMI required |

| Jumbo | 10% – 20% | High-value Seattle properties | Exceeds conforming limits |

Mortgage advisors evaluate your specific situation against these options, often identifying programs you might not have considered. A first-time buyer in Shoreline might benefit from a conventional loan with minimal down payment, while an investor purchasing rental property in Lynnwood requires different structuring entirely.

How Mortgage Advisors Add Value Throughout the Process

The relationship with skilled mortgage advisors extends from initial consultation through closing and beyond, providing continuity that fragmented online services cannot match.

Pre-Approval Strategy and Timing

Obtaining pre-approval before house hunting represents standard practice, but the quality and structure of that pre-approval varies dramatically. Experienced advisors time pre-approvals strategically, ensuring documentation remains current while positioning you competitively in multiple-offer scenarios common across Lake Forest Park and Mill Creek.

Strategic pre-approval elements:

- Complete underwriting review before house hunting

- Documentation of all income sources with verification

- Credit optimization recommendations implemented early

- Clear maximum purchase price with payment breakdown

- Lender commitment letter that sellers and agents trust

Studies show that person-to-person advice remains the top mortgage influencer, particularly in competitive markets where buyers need confidence and credibility. Your pre-approval letter serves as a critical negotiating tool, and having it backed by a respected local advisor strengthens your position significantly.

Rate Negotiation and Lock Strategy

Interest rates fluctuate daily, and determining the optimal time to lock your rate requires market knowledge and risk assessment. Mortgage advisors monitor rate trends, explain lock options, and help you decide between locking immediately versus floating with protective strategies.

For refinancing scenarios, advisors calculate true break-even points by factoring closing costs against monthly savings. This analysis prevents costly mistakes where borrowers refinance without achieving meaningful financial benefit.

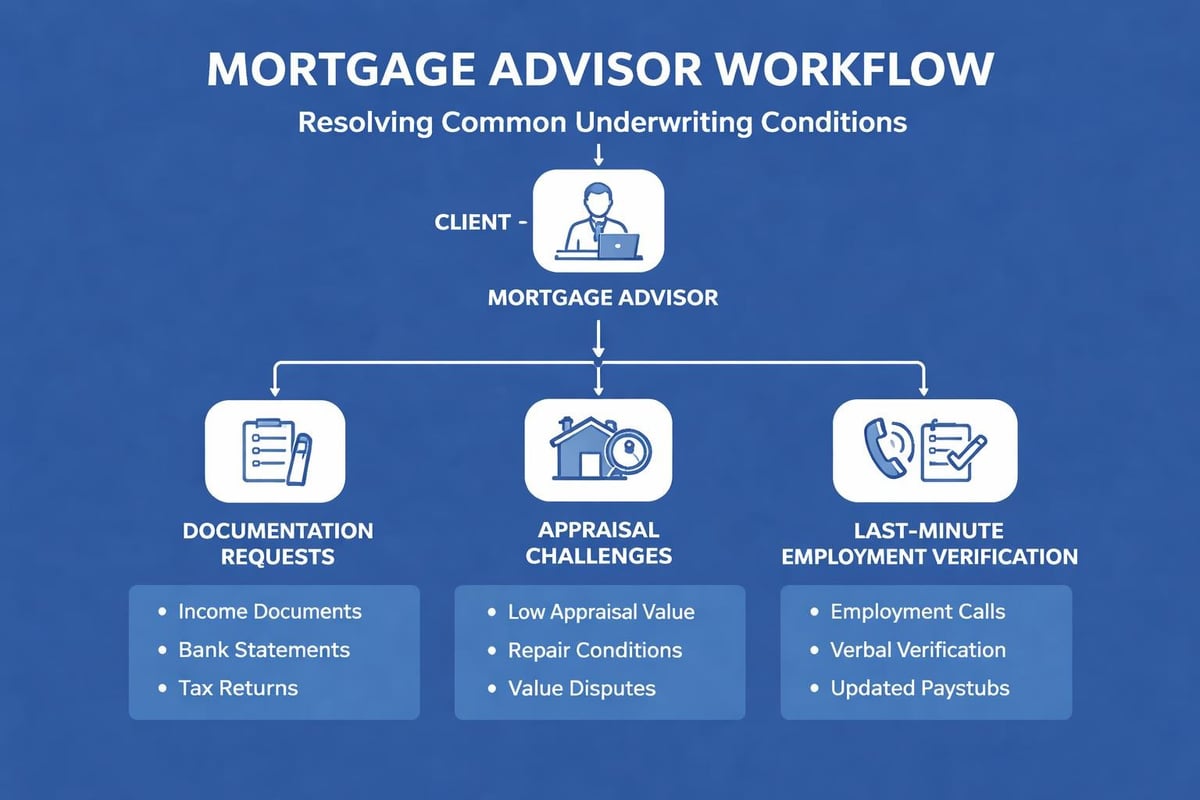

Problem-Solving During Underwriting

Even well-prepared loan applications encounter underwriting conditions requiring additional documentation or explanation. Perhaps an automated valuation comes in below purchase price, or the underwriter questions a recent bank deposit. These situations demand quick, knowledgeable responses that keep transactions on track.

Experienced mortgage advisors have addressed thousands of underwriting scenarios and know exactly how to structure responses that satisfy requirements without delaying closing. This expertise proves especially valuable when working with tight timelines or complex financial situations.

Specialized Expertise for Seattle's Unique Market

Seattle's housing market presents distinct challenges that require local knowledge and specialized experience. From understanding neighborhood price dynamics across Everett to structuring jumbo loans for high-value properties, mortgage advisors with regional expertise deliver superior outcomes.

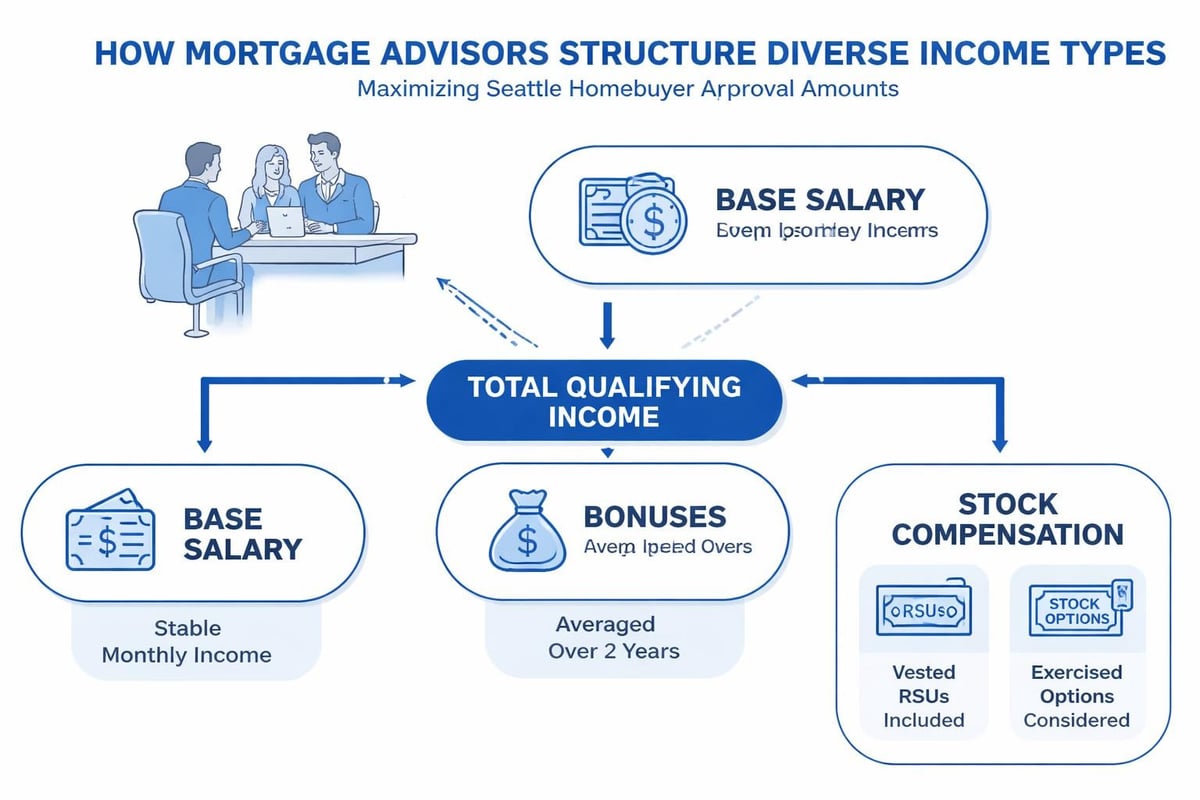

Tech Industry Compensation Qualification

The concentration of major technology employers in the Seattle region means many homebuyers receive significant portions of compensation through equity and bonuses rather than base salary alone. Traditional lending approaches often underutilize this income, reducing buying power unnecessarily.

Skilled mortgage advisors structure income documentation to capture the full value of:

- RSU vesting schedules with historical patterns demonstrating consistency

- Stock option exercises timed strategically for qualification purposes

- Performance bonuses with multi-year track records supporting continuance

- Sign-on bonuses evaluated under appropriate guidelines

This specialized knowledge can increase qualification amounts by $100,000 or more compared to generic underwriting approaches, making the difference between compromise and getting your ideal home.

Jumbo Loan Structuring and Execution

With median home prices in many Seattle neighborhoods exceeding conforming loan limits, jumbo financing becomes necessary for a significant percentage of purchases. These loans carry distinct requirements for reserves, documentation, and property characteristics.

Working with top mortgage brokers in Seattle who specialize in jumbo products ensures access to competitive rates and smooth execution. The variance between a well-structured jumbo loan and a poorly executed one can mean tens of thousands in unnecessary costs or, worse, a failed transaction.

Selecting the Right Mortgage Advisor for Your Needs

Not all mortgage advisors offer equivalent value or expertise. Understanding how to evaluate and select the professional who best serves your specific situation ensures you receive optimal guidance throughout the lending process.

Credentials and Professional Standards

While licensing represents the baseline requirement for practicing mortgage lending, additional certifications demonstrate commitment to professional development and ethical standards. The National Association of Certified Mortgage Advisors directory provides resources for locating advisors who have completed advanced training.

Credentials to consider:

- State licensing and NMLS registration

- Professional certifications beyond basic requirements

- Specialized training in complex income qualification

- Continuing education in evolving lending guidelines

Beyond formal credentials, track records matter significantly. Choosing a trusted local mortgage broker involves reviewing client feedback, verification of successful closings, and assessment of communication practices.

Reputation and Client Reviews

In 2026, transparency through online reviews provides unprecedented insight into advisor performance. Examining patterns across multiple platforms reveals consistency in service quality, communication responsiveness, and problem-solving ability.

When evaluating mortgage advisors, look for:

- Volume and recency of reviews across Google, Zillow, and other platforms

- Specific details about challenges overcome and processes followed

- Consistency in praise for particular attributes like communication or expertise

- Response patterns to both positive feedback and concerns raised

Understanding how to interpret mortgage lender rating lists helps distinguish meaningful metrics from promotional content. Focus on verified client experiences rather than marketing claims.

Communication Style and Accessibility

The mortgage process spans weeks and involves numerous time-sensitive decisions. Your advisor's communication approach directly impacts your stress level and ability to make informed choices under pressure.

| Communication Aspect | What to Evaluate | Why It Matters |

|---|---|---|

| Response time | Hours, not days | Time-sensitive decisions require quick input |

| Explanation clarity | Technical concepts made understandable | You must comprehend options to choose wisely |

| Proactive updates | Regular status communications | Reduces anxiety and prevents surprises |

| Availability channels | Phone, email, text options | Flexibility matches your preferences |

Even in an increasingly digital world, mortgage advisors remain favored over purely digital solutions specifically because of the human element in communication and reassurance during stressful processes.

Advanced Strategies Mortgage Advisors Employ

Sophisticated mortgage advisors employ strategies that go beyond basic loan origination, optimizing both immediate transaction success and long-term financial positioning.

Portfolio Lending and Alternative Programs

When conventional, FHA, and other standard programs don't fit unique situations, portfolio lending through relationship-based lenders provides flexibility. Mortgage advisors with extensive lender networks access programs unavailable to typical borrowers, including:

- Bank statement loans for self-employed borrowers with complex returns

- Asset-based qualification using investment portfolios

- Debt service coverage ratio (DSCR) loans for investment properties

- Non-QM products for situations outside standard guidelines

These specialized programs often carry higher rates but enable transactions that otherwise couldn't proceed. Knowing when they represent the best option versus waiting to improve standard qualification requires experienced judgment.

Multi-Property and Investment Strategy

For clients building rental property portfolios or purchasing second homes, mortgage advisors structure financing sequences that maximize leverage while maintaining qualification capacity. This involves strategic timing of purchases, understanding how rental income counts toward qualification, and structuring entities appropriately.

First-time home buyer guidance differs substantially from investor strategies, yet the same advisor often serves clients through multiple life stages as financial situations evolve.

Refinancing Optimization Beyond Rate

While rate reduction drives most refinancing decisions, experienced mortgage advisors evaluate additional factors:

- Cash-out refinancing for home improvements or debt consolidation

- Term modification to accelerate payoff or reduce payments

- PMI removal when equity reaches appropriate thresholds

- Product changes from adjustable to fixed rates or vice versa

The Consumer Financial Protection Bureau recommends building a network of advisors including mortgage professionals, real estate agents, and attorneys to make comprehensive housing decisions. This integrated approach ensures all aspects of homeownership receive proper attention.

Cost Structures and Compensation Models

Understanding how mortgage advisors are compensated helps set appropriate expectations and evaluate whether recommendations serve your interests or primarily generate fees.

Lender-Paid vs. Borrower-Paid Compensation

Most mortgage originations involve lender-paid compensation, where the lender pays the advisor based on loan amount and sometimes rate selection. This creates inherent potential conflicts of interest, making advisor integrity and transparency critical.

Compensation considerations:

- Lender-paid models standardize costs but may influence product recommendations

- Borrower-paid options provide complete transparency but require upfront fees

- Hybrid approaches combine elements of both structures

- Disclosure requirements mandate clear presentation of all compensation

Ethical mortgage advisors prioritize client outcomes over compensation maximization, recommending programs that genuinely serve borrower interests even when alternatives might generate higher fees.

No-Cost Refinancing and Rate Tradeoffs

Popular "no-cost" refinancing isn't actually free but rather involves accepting slightly higher rates in exchange for lender credits covering closing costs. Advisors should clearly explain this tradeoff and calculate whether it makes mathematical sense given your expected holding period.

For Seattle homeowners considering refinancing options, understanding current mortgage rates provides context for evaluating whether now represents an optimal time to refinance or whether waiting might prove more beneficial.

Technology Integration in Modern Mortgage Advisory

While personal relationships remain central to mortgage advisory services, technology integration enhances efficiency, transparency, and client experience when properly implemented.

Digital Application and Documentation

Modern mortgage processes incorporate secure portals for document upload, application completion, and status tracking. Quality advisors leverage these tools to streamline operations while maintaining personal touchpoints at critical decision moments.

Technology touchpoints that enhance service:

- Automated document collection with clear checklists

- Real-time status updates accessible 24/7

- Digital signing for time-sensitive disclosures

- Secure messaging for quick questions

- Video consultations for remote clients

The goal involves using technology to eliminate friction and busywork while preserving human expertise for strategy, problem-solving, and complex decisions.

Data-Driven Rate Shopping

Sophisticated mortgage advisors monitor rate sheets from multiple lenders continuously, enabling them to identify optimal pricing windows and negotiate effectively on clients' behalf. This data-driven approach delivers better rates than borrowers typically secure shopping independently across retail lenders.

Access to wholesale lending channels unavailable to direct consumers represents a significant advantage of working with established mortgage advisors rather than pursuing direct-to-lender options.

Building Long-Term Relationships with Mortgage Advisors

The most valuable advisor relationships extend beyond single transactions, providing ongoing consultation as financial circumstances and market conditions evolve.

Periodic Portfolio Reviews

Even after closing, market rate movements create potential refinancing opportunities. Advisors who conduct periodic reviews proactively identify situations where refinancing makes sense, calculating break-even timeframes and presenting clear recommendations.

For homeowners across Seattle, Shoreline, and surrounding communities, these ongoing relationships ensure you never miss beneficial opportunities due to lack of awareness or analysis paralysis.

Life Stage Transitions and Housing Evolution

As families grow, careers advance, or retirement approaches, housing needs change. The advisor who helped with your first condo purchase in Bellevue can later structure financing for a family home in Redmond, investment property in Everett, or eventual downsizing plans.

This continuity means your advisor understands your complete financial history, goals, and preferences, enabling increasingly refined recommendations with each interaction. Working with experienced professionals who serve clients through multiple decades creates compounding value that transcends any single transaction.

Understanding mortgage approval timelines helps set realistic expectations whether you're purchasing your first home or your fifth property, and experienced advisors adjust processes based on urgency and complexity.

Choosing qualified mortgage advisors transforms the home financing process from a stressful obstacle into a strategic advantage, particularly in competitive markets like Seattle where expertise and execution speed directly impact success. Whether you're navigating complex tech compensation, structuring jumbo financing, or simply seeking transparent guidance through your first home purchase, working with Keith Akada at Mortgage Reel provides the experienced partnership you need to make confident decisions backed by 25+ years of proven results and 750+ five-star client reviews.