FHA house loans represent one of the most accessible pathways to homeownership for buyers across Seattle, Bellevue, Redmond, and Kirkland. Backed by the Federal Housing Administration and designed specifically for buyers who may not qualify for conventional financing, these government-insured mortgages offer lower down payment requirements and more flexible credit standards. Whether you're a first-time buyer navigating Seattle's competitive housing market or a tech professional at Amazon or Microsoft looking to maximize your purchasing power, understanding how fha house loans function can unlock opportunities that might otherwise seem out of reach.

What Are FHA House Loans and How Do They Work

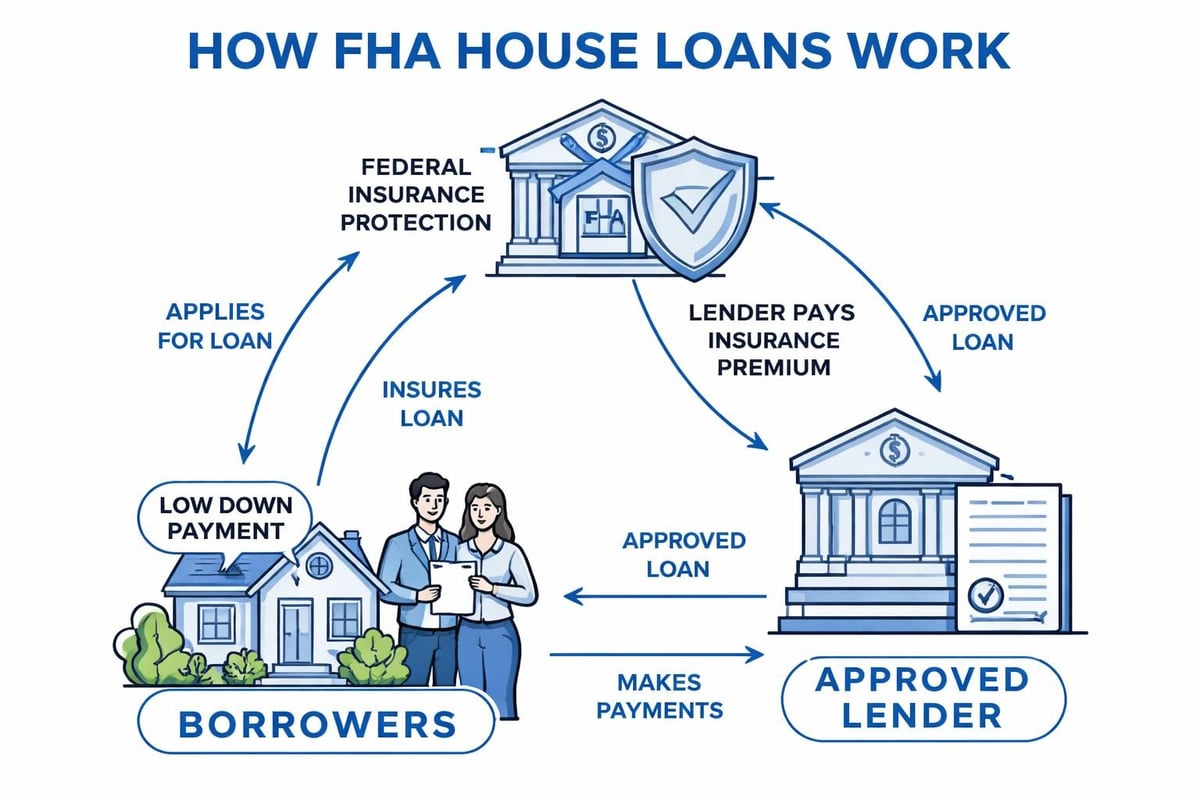

FHA house loans are mortgage products insured by the Federal Housing Administration, a government agency within the Department of Housing and Urban Development. Unlike conventional loans offered directly by banks, FHA loans are originated by approved lenders but protected against default through federal insurance. This insurance protection allows lenders to offer more favorable terms to borrowers who might not meet traditional lending criteria.

The FHA doesn't actually lend money. Instead, it guarantees loans made by approved lenders, reducing their risk and enabling them to extend credit to buyers with smaller down payments or less-than-perfect credit histories. This structure has made homeownership possible for millions of Americans since the program's inception in 1934.

Key Features That Define FHA Financing

FHA house loans come with several distinguishing characteristics that set them apart from conventional mortgage products:

- Minimum down payment of just 3.5% for borrowers with credit scores of 580 or higher

- Credit scores as low as 500 may qualify with 10% down

- Debt-to-income ratios up to 50% in many cases with compensating factors

- Gift funds allowed for down payment and closing costs from family members

- Assumable loans that can be transferred to future buyers

The program's flexibility extends to property types as well. FHA house loans can finance single-family homes, condominiums in FHA-approved buildings, multi-unit properties up to four units, and even certain manufactured homes. For buyers in Seattle neighborhoods like Shoreline or Lynnwood, this versatility opens doors to various housing options.

Down Payment Requirements and Funding Options

One of the most attractive aspects of fha house loans is the minimal upfront cash requirement. At just 3.5% down for qualified borrowers, the barrier to entry is significantly lower than conventional loans, which typically require 5% to 20% down depending on the borrower's financial profile.

For a $600,000 home in Redmond, the difference is substantial. An FHA loan would require $21,000 down, while a conventional loan at 10% would demand $60,000. This $39,000 difference can be the deciding factor for many Seattle-area buyers, particularly those with strong incomes but limited savings.

Where Your Down Payment Can Come From

FHA guidelines are remarkably flexible regarding down payment sources:

| Source Type | FHA Allowed | Conditions |

|---|---|---|

| Personal savings | Yes | Most common source |

| Gift funds | Yes | Must be from family member with gift letter |

| Employer assistance | Yes | Must be documented properly |

| Grant programs | Yes | Must meet program requirements |

| Retirement accounts | Yes | Subject to withdrawal rules and taxes |

| Sale of assets | Yes | Must document transaction |

Many Seattle-area buyers combine multiple sources to reach their 3.5% threshold. A tech professional might use RSU proceeds alongside a family gift, while a first-time buyer in Mill Creek might leverage a state or local down payment assistance program combined with personal savings.

The flexibility extends beyond just the down payment. Closing costs can also be covered through seller concessions up to 6% of the purchase price, another advantage in negotiations. Understanding mortgage down payment options specific to Washington State can help you maximize these opportunities.

Credit Score and Qualification Standards

FHA house loans have earned their reputation for credit flexibility, but understanding the specific thresholds and requirements helps set realistic expectations. The program uses a tiered approach based on your credit score and compensating factors.

Credit Score Tiers and Requirements

580 or Higher: This is the sweet spot for FHA financing. Borrowers with scores of 580 or above qualify for the minimum 3.5% down payment and generally receive the most favorable treatment during underwriting. Even with scores in the 580-620 range, which conventional lenders often decline, FHA approval remains achievable.

500-579: Borrowers in this range can still qualify for fha house loans, but the down payment requirement increases to 10%. Lenders also scrutinize these applications more carefully, looking for strong compensating factors such as stable employment, low debt-to-income ratios, or significant cash reserves.

Below 500: FHA guidelines technically don't permit scores below 500, though some lenders may have overlays that set higher minimums. At this level, credit repair becomes the priority before pursuing financing.

Beyond the score itself, underwriters examine your credit history for patterns. A 620 score with consistent on-time payments over two years holds more weight than a 640 with recent delinquencies. Recent bankruptcies require a two-year waiting period, while foreclosures need three years of separation with re-established credit.

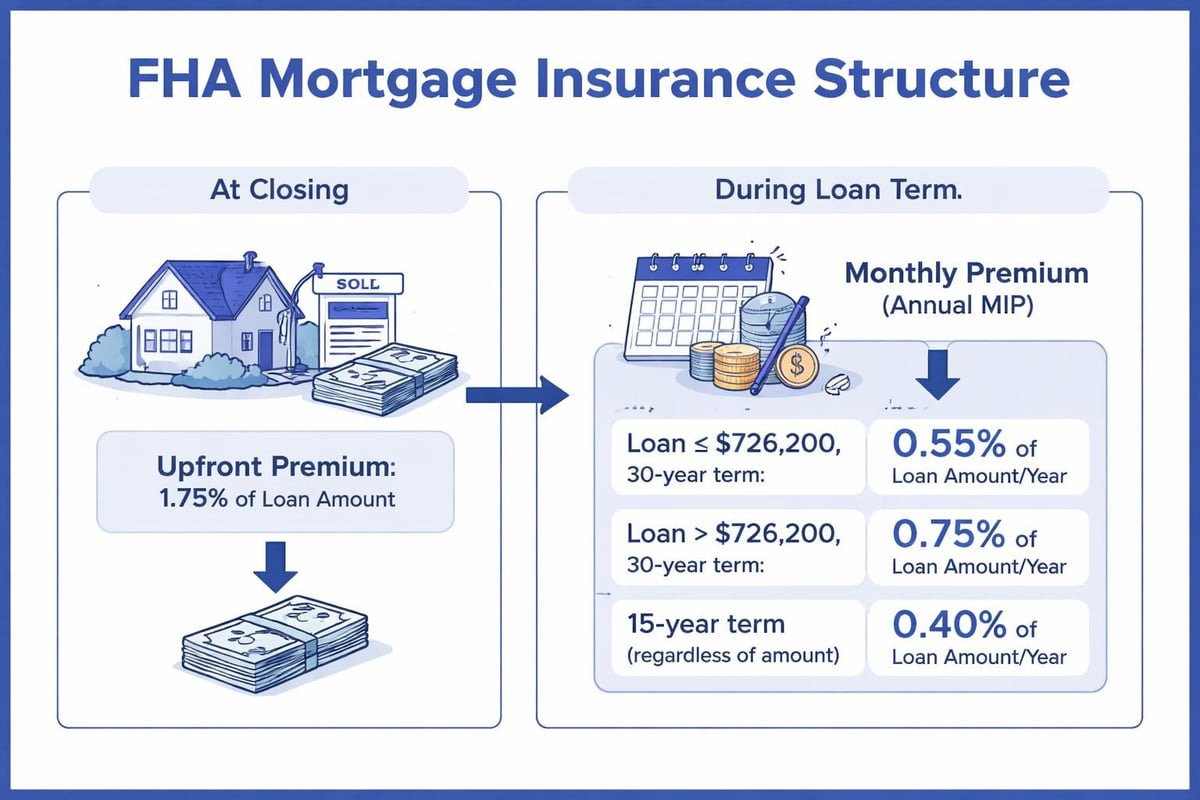

Mortgage Insurance: Understanding the Costs

Every FHA house loan includes mortgage insurance, which protects the lender if you default. This insurance comes in two components, and understanding both is essential for accurate budgeting and long-term planning.

Upfront Mortgage Insurance Premium (UFMIP)

The UFMIP equals 1.75% of your base loan amount and is typically rolled into your mortgage rather than paid at closing. On a $500,000 loan, that's $8,750 added to your principal balance. While this increases your total loan amount slightly, it preserves your cash for other expenses.

Annual Mortgage Insurance Premium (MIP)

The annual MIP is paid monthly as part of your regular mortgage payment. Rates vary based on your loan amount, term, and loan-to-value ratio:

| Loan Amount | Base Loan Term | LTV ? 95% | LTV > 95% |

|---|---|---|---|

| ? $726,200 | 30 years | 0.55% | 0.55% |

| > $726,200 | 30 years | 0.75% | 0.75% |

| ? $726,200 | 15 years | 0.15% | 0.40% |

| > $726,200 | 15 years | 0.40% | 0.65% |

For most borrowers putting 3.5% down on a 30-year loan, the MIP is 0.55% annually. On a $500,000 loan, that translates to $229 per month added to your payment.

The critical consideration: MIP for loans with less than 10% down lasts for the entire loan term. It doesn't automatically cancel when you reach 20% equity like conventional PMI. This permanent nature makes refinancing to a conventional loan a strategic move once you've built sufficient equity and improved your credit profile. Working with experienced Seattle mortgage brokers can help you plan this transition effectively.

Debt-to-Income Ratios and Income Qualification

FHA house loans use two debt-to-income ratios to assess your ability to repay: the front-end ratio (housing costs only) and the back-end ratio (all monthly debts). Understanding these calculations helps you know exactly where you stand before applying.

Front-End Ratio (Housing Ratio)

This ratio compares your total monthly housing payment to your gross monthly income. Your housing payment includes principal, interest, property taxes, homeowners insurance, HOA fees, and mortgage insurance. FHA typically allows up to 31% on the front end, though higher ratios may be approved with compensating factors.

Example: If you earn $10,000 monthly gross income, your total housing payment should ideally stay below $3,100.

Back-End Ratio (Total Debt Ratio)

This broader calculation includes your housing payment plus all other monthly debt obligations: car loans, student loans, credit cards, personal loans, and any other recurring payments. The FHA guideline is generally 43%, though ratios up to 50% or higher can be approved with strong compensating factors.

Example: With the same $10,000 monthly income, your total debt payments (including housing) should stay below $4,300 at the standard guideline, or up to $5,000 with approval.

Compensating Factors That Matter

When your ratios exceed standard guidelines, underwriters look for strengths that offset the higher debt load:

- Cash reserves exceeding three months of housing payments

- Minimal increase from current rent to proposed mortgage payment

- Strong credit history with high scores

- Established employment in stable industry

- Residual income exceeding standard requirements

- Significant down payment beyond the minimum

For tech professionals in Seattle working at companies like Microsoft or Google, documentation of restricted stock units and bonuses can strengthen your application significantly. These income sources, when properly verified, can increase your qualifying income and improve your ratios.

Property Requirements and Appraisal Standards

Not every property qualifies for fha house loans. The Federal Housing Administration maintains specific standards ensuring that financed properties meet minimum safety, security, and structural integrity requirements. These standards protect both borrowers and the FHA insurance fund from properties with serious defects.

What FHA Appraisers Evaluate

FHA appraisals go beyond determining market value. Appraisers assess:

- Structural integrity: Foundation, roof, walls, and load-bearing components must be sound

- Safety hazards: Properties must be free from health and safety risks

- Accessibility: All areas must be accessible for inspection

- Utilities: Heating, plumbing, and electrical systems must function properly

- Property condition: No peeling paint in homes built before 1978 (lead paint concerns)

In Seattle's older housing stock, particularly in neighborhoods like Ballard or Capitol Hill, these requirements sometimes trigger repair requirements. A home built in 1950 with original plumbing might need updates before FHA approval, while a newer construction property in Kirkland typically sails through.

Common Issues That Delay or Prevent FHA Approval

Several property conditions frequently cause problems:

- Damaged or deteriorating roof requiring replacement

- Cracked or damaged foundations compromising structural integrity

- Non-functioning HVAC systems

- Visible water damage or active leaks

- Peeling or chipping paint on pre-1978 homes

- Missing railings on stairs or decks

- Unsafe electrical wiring or panels

Sellers can complete repairs before closing, buyers can negotiate repair credits, or in some cases, FHA 203(k) rehabilitation loans can finance both purchase and repairs in one transaction. Understanding these options before making offers on fixer-uppers helps avoid unexpected complications.

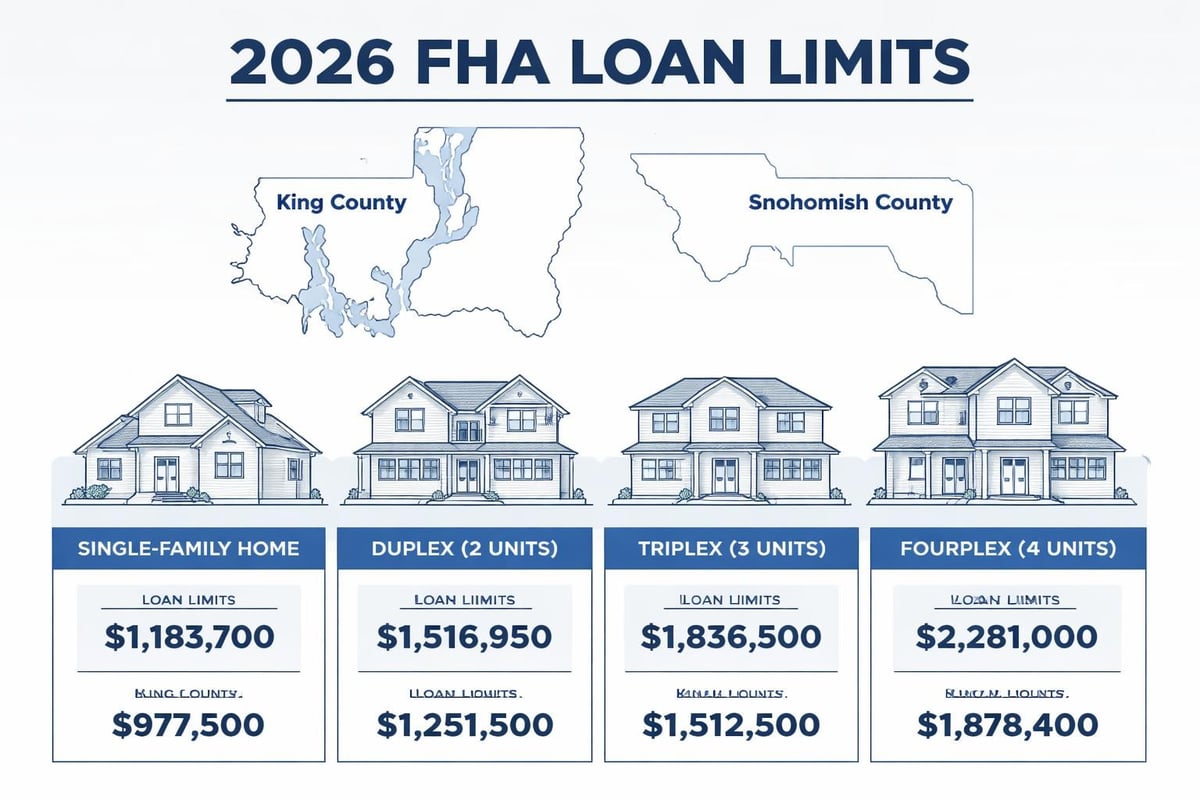

FHA Loan Limits for the Seattle Area

FHA house loans have maximum borrowing limits that vary by county and are adjusted annually. For 2026, King County (which includes Seattle, Bellevue, Redmond, and Kirkland) has higher limits due to the area's elevated housing costs.

The standard FHA loan limit for King County in 2026 is $806,500 for a single-family home, significantly higher than the baseline limit of $498,257 in lower-cost areas. This increase reflects Seattle's expensive housing market and enables FHA financing for more properties in the region.

Loan Limits by Property Type

| Property Type | King County Limit | Snohomish County Limit |

|---|---|---|

| Single-family | $806,500 | $805,500 |

| Two-unit | $1,032,350 | $1,031,050 |

| Three-unit | $1,248,075 | $1,246,375 |

| Four-unit | $1,550,775 | $1,548,550 |

For buyers targeting multi-unit properties as a house-hacking strategy, these higher limits enable FHA financing on duplexes, triplexes, and fourplexes throughout the Seattle metro area. Living in one unit while renting the others can offset your housing costs significantly.

Properties exceeding these limits require alternative financing. For tech professionals with substantial compensation packages, jumbo loan programs may better serve purchases above FHA limits, particularly when factoring in equity compensation and bonus income.

Comparing FHA to Conventional Loans

Choosing between fha house loans and conventional financing requires weighing multiple factors specific to your financial situation and homeownership goals. Neither option is universally superior; the right choice depends on your credit profile, available funds, and long-term plans.

When FHA Makes More Sense

FHA loans typically offer better terms when:

- Your credit score falls below 680

- You have limited funds for down payment (less than 10%)

- Your debt-to-income ratios exceed 45%

- You're purchasing a multi-unit property as a primary residence

- You have recent credit challenges (bankruptcy, foreclosure) within conventional waiting periods

When Conventional Loans Win

Conventional financing often provides advantages when:

- Your credit score exceeds 740

- You can put down 10% or more

- You're purchasing a higher-priced property with strong income

- You want mortgage insurance to cancel automatically at 20% equity

- You're refinancing and already have substantial equity

The Hybrid Approach

Many Seattle buyers start with an FHA loan to enter the market with minimal down payment, then refinance to conventional within three to five years. This strategy leverages FHA's accessibility initially while eventually eliminating the permanent mortgage insurance through a conventional refinance.

Working with knowledgeable Seattle home financing professionals helps you map this progression from the start, ensuring your initial FHA loan positions you for future refinancing success.

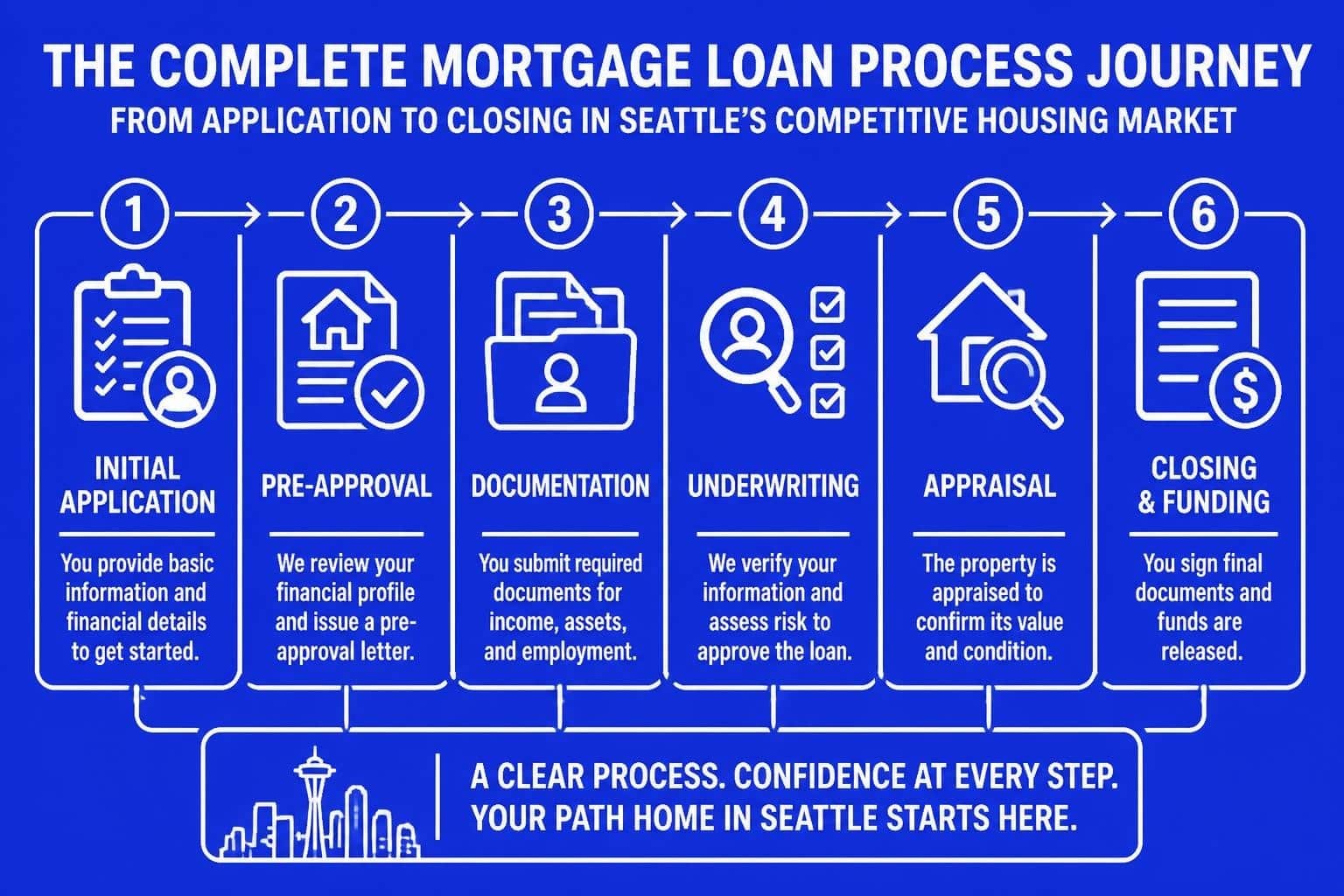

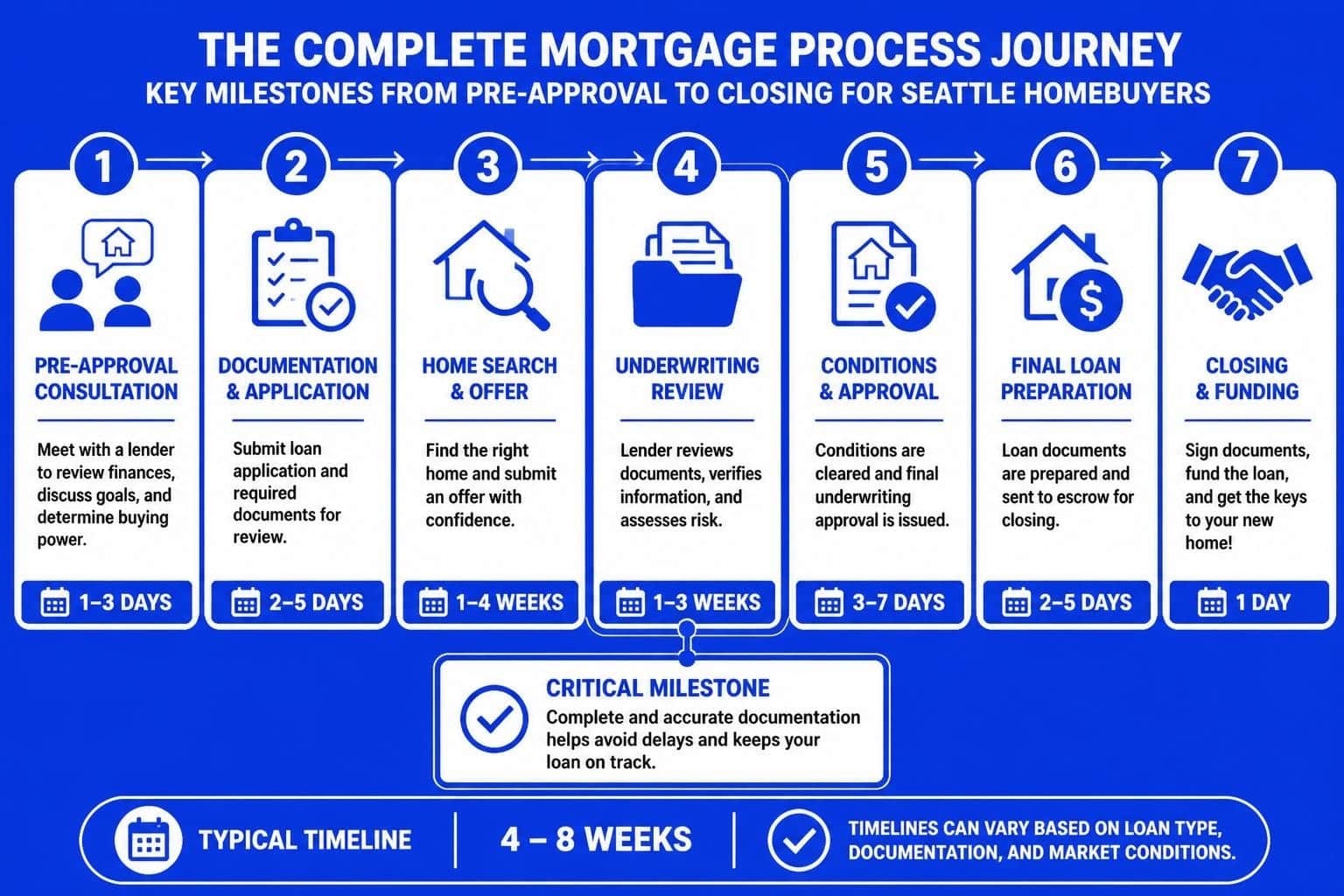

The FHA Application and Approval Process

Navigating the FHA application process efficiently requires preparation and understanding of what lenders need. While the basic process mirrors conventional loans, FHA underwriting has specific documentation requirements and timelines.

Pre-Approval: Your First Critical Step

Before house hunting in Seattle's competitive market, obtaining pre-approval establishes your budget and strengthens your offer. The Consumer Financial Protection Bureau provides guidance on understanding FHA requirements early in your home buying journey.

Pre-approval for fha house loans requires:

- Credit report review from all three bureaus

- Income verification through recent pay stubs and W-2s

- Asset documentation showing funds for down payment and reserves

- Employment verification confirming stability and continuity

- Debt analysis reviewing all current obligations

For tech employees with complex compensation, additional documentation of RSUs, stock options, and annual bonuses may be necessary. A two-year history of receiving these forms of compensation typically allows lenders to include them in qualifying income.

From Application to Closing

The typical FHA timeline spans 30 to 45 days from application to closing, though experienced lenders can accelerate this process:

- Days 1-7: Full application submission and initial underwriting review

- Days 8-21: Property appraisal ordered and completed

- Days 22-35: Final underwriting, condition clearing, and approval

- Days 36-45: Closing preparation and final walkthrough

Seattle's competitive market often demands faster timelines. Working with lenders who have streamlined processes and strong relationships with appraisers, title companies, and underwriters can reduce this timeline significantly. Some lenders can close FHA loans in as few as 20 days when all parties coordinate effectively.

Special FHA Programs and Options

Beyond the standard FHA house loan, several specialized programs serve specific buyer needs and situations. These alternatives expand FHA's reach and provide solutions for unique property types and circumstances.

FHA 203(k) Rehabilitation Loans

The 203(k) program finances both purchase and renovation in a single loan. This option works brilliantly for buyers targeting fixer-uppers in established Seattle neighborhoods where properties need updating but have strong underlying value.

Two versions exist:

- Standard 203(k): For major renovations exceeding $35,000, including structural repairs

- Limited 203(k): For minor improvements up to $35,000, like updated kitchens or bathrooms

These loans require additional documentation, contractor bids, and draw schedules, but they enable buyers to purchase homes that wouldn't qualify for standard FHA financing in their current condition.

FHA Energy Efficient Mortgage (EEM)

The EEM program allows buyers to finance energy-efficient improvements along with their purchase, up to specific limits. This program particularly benefits buyers of older Seattle homes where energy efficiency upgrades provide long-term savings and increased comfort.

Qualifying improvements include:

- High-efficiency HVAC systems

- Solar panels and solar water heaters

- Energy-efficient windows and doors

- Insulation upgrades

- Air sealing and duct improvements

FHA Streamline Refinance

Current FHA borrowers benefit from streamline refinancing, which reduces documentation and speeds processing when refinancing their existing FHA loan. This program requires no appraisal, no income verification, and no credit check in many cases, making it the fastest refinance option available.

The streamline requires demonstrating a "net tangible benefit," typically a minimum 0.5% rate reduction. For Seattle homeowners who obtained FHA financing when rates were higher, this program provides an efficient path to lower payments.

Common Mistakes to Avoid with FHA Loans

Even experienced buyers make errors that complicate or derail their FHA house loan approval. Awareness of these common pitfalls helps you navigate the process smoothly.

Financial Missteps Before Closing

Opening new credit accounts: New credit cards, car loans, or other debt during the approval process changes your debt ratios and can void your approval. Avoid all new credit from application through closing.

Making large deposits: Unexplained deposits trigger scrutiny. If you receive gift funds or sell assets, document everything thoroughly. Lenders must verify and source all deposits exceeding 1% of your purchase price.

Changing jobs: Employment changes, even for higher pay, complicate approval. Lenders verify employment immediately before closing, and a job change can delay or cancel your loan. If you must change employers, inform your loan officer immediately.

Depleting reserves: Keep adequate funds in your accounts beyond what you need for closing. Lenders verify that you have reserves remaining after all closing costs are paid.

Property and Contract Issues

Choosing properties that don't meet FHA standards wastes time and money on inspections and appraisals for homes that ultimately won't qualify. Understanding FHA property requirements before making offers prevents this frustration.

Negotiating contracts without FHA contingencies exposes you to risk if the property fails appraisal or doesn't meet FHA standards. Always include FHA appraisal and financing contingencies that allow you to exit if the home doesn't qualify.

Maximizing Your FHA House Loan Success in Seattle

Seattle's housing market presents unique challenges and opportunities for FHA borrowers. Strategic planning and local market knowledge help you compete effectively while staying within FHA guidelines.

Strategies for Multiple Offer Situations

FHA buyers often face perception challenges in competitive markets where sellers worry about appraisal issues or longer closing times. Counter these concerns by:

- Obtaining full underwriting approval before making offers, not just pre-qualification

- Offering strong earnest money deposits showing commitment

- Working with experienced lenders known for on-time closings

- Writing competitive offers that don't rely solely on low down payment advantage

- Including flexible appraisal language addressing potential value gaps

In neighborhoods like Lake Forest Park or Mill Creek where competition may be less intense than central Seattle, FHA buyers often find better reception and more negotiating room.

Building Your Post-Purchase Strategy

Smart FHA borrowers think beyond just getting approved. Plan for:

- Accelerated equity building through extra principal payments

- Credit improvement to position for conventional refinancing

- Market monitoring to identify optimal refinancing windows

- Property maintenance that preserves and increases value

The goal for many should be transitioning from FHA to conventional financing within three to five years, eliminating the permanent mortgage insurance while securing a lower rate based on improved credit and equity position.

Regional Considerations for Seattle FHA Buyers

Different Seattle-area submarkets present varying opportunities and challenges for fha house loans. Understanding these local nuances helps you target the right areas.

King County Core: Seattle, Bellevue, Redmond, Kirkland

These central markets feature higher prices, intense competition, and properties that frequently exceed FHA limits. FHA buyers find the most success targeting:

- Condominiums in FHA-approved buildings

- Smaller single-family homes in established neighborhoods

- Properties needing minor updates that scare conventional buyers

- Multi-unit properties for house-hacking strategies

Competition requires exceptional preparation and aggressive offers, but opportunities exist for determined buyers with solid approval.

Snohomish County: Shoreline, Lynnwood, Everett, Mill Creek

These northern markets offer better FHA opportunities with:

- Lower overall price points fitting comfortably within FHA limits

- Less intense competition allowing for easier negotiations

- Newer construction and well-maintained properties meeting FHA standards

- Growing job markets and improving infrastructure

First-time buyers often find Snohomish County markets more accessible and welcoming to FHA financing, with sellers more accustomed to working with FHA buyers and transactions.

FHA house loans provide accessible financing for qualified buyers throughout the Greater Seattle area, combining low down payments with flexible credit requirements to make homeownership achievable. Whether you're purchasing your first home in Everett, upgrading to a multi-unit property in Shoreline, or navigating Seattle's competitive market with limited savings, understanding FHA guidelines positions you for success. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle-area buyers navigate FHA financing, conventional loans, and complex compensation structures to achieve their homeownership goals. Contact Mortgage Reel today to discuss your specific situation and create a customized financing strategy that works for you.