Breaking into Seattle's competitive housing market as a first-time buyer can feel overwhelming, especially when navigating loan options. A first time buyer conventional loan offers flexibility, competitive rates, and the potential for lower overall costs compared to government-backed alternatives. Understanding how these loans work and whether you qualify is the first step toward homeownership in Seattle, Bellevue, Redmond, Kirkland, and surrounding communities. With the right preparation and guidance, conventional financing can be an excellent path to securing your first home in 2026.

Understanding Conventional Loans for First-Time Homebuyers

A conventional loan is any mortgage not guaranteed or insured by a government agency like the FHA, VA, or USDA. These loans are backed by private lenders and typically follow guidelines set by Fannie Mae and Freddie Mac. For first-time buyers, conventional loans offer distinct advantages, including lower lifetime costs when you have solid credit and the ability to cancel private mortgage insurance once you reach 20% equity.

Many first-time buyers assume they need 20% down for a conventional loan, but that's no longer true. Programs like Conventional 97 and HomeReady allow qualified buyers to purchase with as little as 3% down, making homeownership accessible earlier. These options are particularly valuable in high-cost areas like Seattle, where home prices continue to challenge entry-level buyers.

Minimum Down Payment Requirements

The down payment threshold for a first time buyer conventional loan has dropped significantly in recent years. Here's what you need to know:

- Conventional 97: Requires just 3% down for qualified first-time buyers

- HomeReady and Home Possible: Fannie Mae and Freddie Mac programs offering 3% down with income limits

- Standard Conventional: 5% down for buyers who don't meet first-time buyer criteria

- Investment Properties: Minimum 15% down for conventional financing on rental properties

For a $600,000 home in Shoreline, a 3% down payment equals $18,000, significantly less than the $120,000 needed for a traditional 20% down scenario. This accessibility opens doors for buyers who have strong income and credit but haven't accumulated massive savings yet.

Credit Score and Income Requirements

Credit standards for conventional loans are more stringent than FHA loans but still achievable for well-prepared buyers. Understanding these requirements helps you position yourself for approval and competitive rates.

Credit Score Thresholds

| Down Payment | Minimum Credit Score | Typical Rate Impact |

|---|---|---|

| 3% | 620 | Higher rates apply |

| 5% | 620 | Moderate rates |

| 10% | 620 | Better pricing |

| 20% | 620 | Best rates available |

Most Seattle-area lenders prefer seeing credit scores of 680 or higher for optimal pricing on a first time buyer conventional loan. Scores between 620 and 679 qualify but may carry rate adjustments that increase your monthly payment. Tech professionals in Redmond and Bellevue often have strong credit profiles from responsible credit card use and student loan management, positioning them well for conventional financing.

Income Documentation Standards

Conventional loans require thorough income verification. For most W-2 employees, lenders need:

- Two years of tax returns

- Recent pay stubs covering 30 days

- Two years of W-2 forms

- Employment verification directly from your employer

For tech workers with stock compensation, the process becomes more nuanced. RSUs, stock options, and performance bonuses can significantly boost your qualifying income, but lenders must document a two-year history and verify vesting schedules. Working with a mortgage broker experienced with Seattle tech industry compensation ensures these income sources get properly counted toward your buying power.

Self-employed buyers in Lynnwood or Mill Creek face additional documentation requirements, including two years of complete tax returns with all schedules and a current profit-and-loss statement. The underwriting process examines net income after business expenses, which can reduce qualifying power compared to W-2 employees earning the same gross amount.

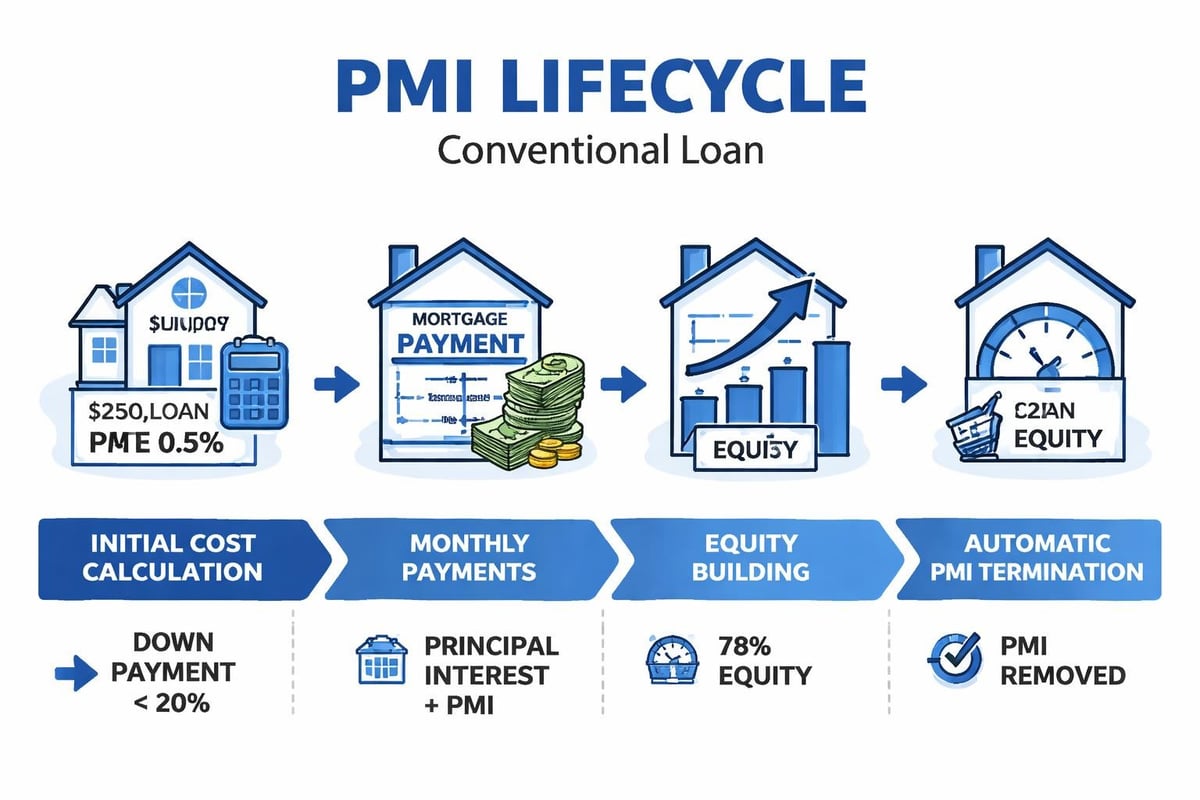

Private Mortgage Insurance (PMI) Considerations

When you put down less than 20% on a conventional loan, private mortgage insurance protects the lender if you default. Understanding PMI costs and removal options is crucial when comparing conventional loans to other first-time homebuyer options.

How PMI Works

PMI typically costs between 0.3% and 1.5% of the original loan amount annually, divided into monthly payments. On a $550,000 loan in Kirkland with 5% down, PMI might add $200 to $350 to your monthly payment, depending on your credit score and loan-to-value ratio.

The significant advantage of conventional PMI over FHA mortgage insurance is cancellation flexibility. Once your loan balance drops to 80% of the original purchase price through payments or appreciation, you can request PMI removal. In Seattle's historically appreciating market, this can happen faster than expected. Some buyers reach 20% equity within three to five years, eliminating hundreds of dollars in monthly insurance costs.

FHA loans, by contrast, require mortgage insurance for the loan's lifetime on purchases with less than 10% down, or for 11 years with 10% or more down. This fundamental difference makes conventional financing more cost-effective long-term for buyers who can meet the credit requirements.

Debt-to-Income Ratio Standards

Your debt-to-income ratio (DTI) measures monthly debt obligations against gross monthly income. Conventional loans typically require DTI ratios below 43%, though some programs allow up to 50% with compensating factors like high credit scores or significant reserves.

Calculating Your DTI

Front-end ratio includes only housing costs: principal, interest, property taxes, insurance, and HOA fees. Back-end ratio adds all monthly debt payments, including student loans, car payments, credit cards, and personal loans.

For a first time buyer conventional loan with a 3% down payment, lenders scrutinize DTI more carefully. A buyer in Lake Forest Park earning $120,000 annually ($10,000 monthly) with $2,500 in housing costs and $1,200 in other debt payments would have a 37% DTI, comfortably within conventional guidelines.

Seattle tech professionals often carry student loan debt from advanced degrees, but their strong incomes typically offset this concern. The key is maintaining reasonable credit card balances and avoiding major purchases during the mortgage application process.

Comparing Conventional and FHA Loans

First-time buyers frequently debate between conventional and FHA financing. Each serves different financial profiles, and understanding the differences helps you make informed decisions.

Key Differences

| Feature | Conventional | FHA |

|---|---|---|

| Minimum Down Payment | 3% | 3.5% |

| Minimum Credit Score | 620 | 580 |

| Upfront Mortgage Insurance | None | 1.75% of loan amount |

| Monthly Mortgage Insurance | Cancellable | Lifetime (with exceptions) |

| Loan Limits (Seattle 2026) | $806,500 | $498,257 |

| Seller Concessions | Up to 3-9% | Up to 6% |

Conventional loans offer significant advantages in Seattle's price environment. The higher conforming loan limits mean buyers can purchase homes up to $806,500 without entering jumbo loan territory, which carries stricter requirements and higher rates. FHA limits of $498,257 exclude most single-family homes in Seattle proper, though options exist in Everett and other outlying areas.

The upfront FHA mortgage insurance premium adds substantial costs. On a $450,000 loan, the 1.75% premium equals $7,875, typically financed into the loan amount. This increases both your loan balance and monthly payment. Conventional loans avoid this upfront charge entirely.

Gift Funds and Down Payment Assistance

A first time buyer conventional loan allows generous use of gift funds from family members, making homeownership achievable for buyers with strong income but limited savings. Understanding these rules helps you leverage available resources.

Gift Fund Guidelines

Conventional loans permit 100% of your down payment and closing costs to come from gifts when you put down less than 20%. The gift must be truly a gift, not a loan requiring repayment. Required documentation includes:

- Gift letter stating the amount, relationship, and no repayment expectation

- Paper trail showing funds transferred from donor to recipient

- Bank statements proving the donor has sufficient funds

For buyers in Bellevue receiving help from parents or grandparents, this flexibility enables entering the market sooner. The donor can transfer funds directly to the title company or to your account, though lenders need to see both the withdrawal and deposit clearly documented.

Down Payment Assistance Programs

Several programs support first-time buyers pursuing conventional financing:

- Seattle Office of Housing: Offers down payment assistance loans for income-qualified buyers

- Washington State Housing Finance Commission: Provides affordable loan programs with down payment help

- Employer Assistance: Many Seattle tech companies offer homebuying grants or low-interest loans

These programs often combine with conventional financing, though some restrict loan types or require specific lenders. Researching available assistance early in your homebuying journey maximizes your options and purchasing power.

Property Types and Conventional Loan Flexibility

Conventional financing accommodates diverse property types, giving first-time buyers more choices than FHA or VA loans. This flexibility matters in Seattle's varied housing stock.

Eligible Property Types

- Single-family homes

- Condominiums (must be on Fannie Mae or Freddie Mac approved list)

- Townhouses

- Multi-family properties (up to four units)

- Manufactured homes on permanent foundations

Purchasing a duplex or triplex as your first home represents a strategic wealth-building approach. Conventional loans allow you to finance up to a four-unit property with owner occupancy, using rental income from additional units to qualify. For example, a buyer in Mill Creek purchasing a duplex and living in one unit can count 75% of the rental income toward qualifying income, significantly boosting buying power.

Condominium financing requires the complex to meet specific standards regarding owner-occupancy ratios, financial reserves, and legal compliance. Many Seattle condos qualify, but verification before making an offer prevents costly surprises. Working with an experienced broker ensures proper pre-qualification for your target property type.

Closing Costs and Reserves

Beyond the down payment, first-time buyers must budget for closing costs and potentially cash reserves. Understanding these requirements prevents last-minute funding scrambles.

Typical Closing Costs

Closing costs on a first time buyer conventional loan typically range from 2% to 5% of the purchase price. On a $500,000 home in Redmond, expect $10,000 to $25,000 in closing expenses, including:

- Loan origination fees

- Appraisal and inspection costs

- Title insurance and escrow fees

- Property taxes and insurance prepayments

- Recording fees and transfer taxes

Conventional loans permit seller concessions up to 3% of the purchase price with less than 10% down, 6% with 10% to 25% down, and 9% with more than 25% down. In competitive markets, sellers rarely agree to maximum concessions, but negotiating 1% to 2% helps offset costs. First-time buyers in Shoreline might negotiate for the seller to cover specific costs rather than a percentage, targeting expensive items like title insurance.

Reserve Requirements

Lenders often require cash reserves beyond down payment and closing costs. Reserves equal months of housing payments (principal, interest, taxes, insurance) held in liquid accounts after closing. A first time buyer conventional loan with 5% down typically requires two to six months of reserves, depending on credit strength and employment stability.

For a home with $3,500 monthly housing costs, six months of reserves equal $21,000. This requirement ensures you can weather financial disruptions without defaulting. Assets qualifying as reserves include checking and savings accounts, money market accounts, and portions of retirement accounts, though lenders typically count only 60% to 70% of retirement funds.

Rate Locks and Timing Strategies

Interest rate movements significantly impact your monthly payment and overall loan cost. Understanding rate locks and timing helps you secure favorable terms on your first time buyer conventional loan.

How Rate Locks Work

A rate lock guarantees your interest rate for a specific period, typically 30 to 60 days. Once locked, your rate won't increase even if market rates rise, though you won't benefit if rates drop unless you negotiate a float-down provision.

Most buyers lock rates when they have a signed purchase agreement and know their closing timeline. In Seattle's competitive market, faster closing timelines often strengthen offers. Lenders like Fairway can close conventional loans in as few as nine business days with proper preparation, requiring shorter rate locks and reducing lock extension risks.

Rate locks don't require fees for standard 30 to 45-day periods, but extended locks or float-down options may carry charges. If your closing delays beyond the lock period, extension fees typically range from 0.125% to 0.25% of the loan amount per week.

Monitoring Market Conditions

Interest rates fluctuate based on economic indicators, Federal Reserve policy, and bond market movements. While timing the absolute bottom is impossible, understanding trends helps you make informed decisions.

First-time buyers sometimes delay purchases hoping for rate drops, but this strategy carries risks. In appreciating markets like Kirkland and Bellevue, home prices may increase faster than potential rate savings. A 0.25% rate reduction saves approximately $75 monthly on a $500,000 loan, but a 3% price increase costs $15,000 in additional purchase price.

The best time to buy is when you're financially ready and find a home meeting your needs. Rates can be refinanced later if they drop significantly, but you can't recapture lost appreciation or the years of equity building and stable housing that homeownership provides.

Preparing for Conventional Loan Approval

Success with a first time buyer conventional loan starts months before house hunting. Strategic preparation improves your approval odds and strengthens your negotiating position.

Six Months Before Applying

- Review credit reports from all three bureaus and dispute errors

- Pay down credit card balances below 30% of limits

- Avoid new credit applications that generate hard inquiries

- Maintain stable employment and avoid job changes if possible

- Document income sources including bonuses, RSUs, and commissions

- Save consistently for down payment and closing costs

Tech professionals in Seattle should begin organizing stock compensation documentation early. Vesting schedules, grant letters, and historical patterns of RSU income all factor into qualifying calculations. The more complete your documentation, the faster and smoother your approval process.

Three Months Before Applying

- Get pre-approved with a detailed review of income, assets, and credit

- Avoid large deposits without clear paper trails showing their source

- Don't make major purchases that increase debt or deplete savings

- Organize financial documents including tax returns, pay stubs, and bank statements

- Research neighborhoods in Seattle, Lake Forest Park, Lynnwood, and Mill Creek

Pre-approval differs from pre-qualification. Pre-approval involves full credit review, income verification, and asset documentation, giving you a reliable maximum loan amount. In competitive markets, sellers prioritize pre-approved buyers who can close quickly and confidently.

Navigating Seattle's Competitive Market

Seattle's housing market presents unique challenges for first-time buyers, from limited inventory to multiple-offer situations. Understanding local dynamics helps you compete effectively with a first time buyer conventional loan.

Competitive Offer Strategies

Strong conventional financing gives you advantages over FHA buyers in multiple-offer situations. Sellers prefer conventional loans because they close more reliably, have fewer appraisal issues, and don't require property condition standards beyond typical lender requirements.

When competing against cash offers or conventional buyers with 20% down, emphasize your financing strength through:

- Pre-approval letters showing full underwriting review

- Larger earnest money deposits demonstrating commitment

- Flexible closing timelines matching seller needs

- Minimal contingencies while maintaining appropriate protections

- Personal letters explaining your connection to the neighborhood

Working with experienced Seattle mortgage brokers who can verify your approval strength and communicate directly with listing agents provides additional credibility. When sellers receive five offers, the one backed by responsive, proven financing often wins even without the highest price.

Appraisal Considerations

Conventional loans require appraisals confirming the property's value supports the loan amount. In appreciating markets, appraisals occasionally come in below purchase price, creating complications.

If the appraisal gaps by $10,000 on your $550,000 purchase in Everett, you have several options:

- Negotiate with the seller to reduce the price

- Bring additional cash to cover the gap

- Request a reconsideration of value with supporting comparable sales

- Walk away if you have an appraisal contingency

Conventional appraisal gaps offer more flexibility than FHA scenarios because conventional appraisals aren't transferable between buyers. If you cancel, the seller starts fresh with the next buyer. FHA appraisals stay with the property for six months, potentially limiting the seller's options and making them more willing to negotiate.

Jumbo Loans and High-Cost Area Considerations

Seattle's 2026 conforming loan limit of $806,500 accommodates most single-family home purchases, but properties exceeding this threshold require jumbo financing. Understanding this transition helps first-time buyers evaluate their options across price ranges.

Jumbo Loan Requirements

Jumbo conventional loans typically require:

- Minimum 10% down payment (often 15% to 20% for best rates)

- Higher credit scores (usually 700+)

- Lower debt-to-income ratios (typically 43% maximum)

- Larger cash reserves (often six to twelve months)

- Full income documentation without exceptions

For tech professionals in Bellevue or Redmond considering homes in the $900,000 to $1.2 million range, jumbo financing remains achievable with proper preparation. The key is demonstrating financial stability through substantial income, excellent credit, and significant assets beyond the down payment.

Stock compensation becomes particularly valuable in jumbo scenarios. A software engineer with $200,000 base salary plus $100,000 in annual RSUs has stronger qualifying power than someone earning $250,000 in W-2 income alone, assuming proper documentation of the equity compensation history and vesting schedule.

A first time buyer conventional loan offers Seattle-area homebuyers a flexible, cost-effective path to homeownership with competitive rates, cancellable mortgage insurance, and down payments as low as 3%. Whether you're a tech professional in Redmond looking to leverage stock compensation or a first-time buyer in Shoreline seeking guidance through the approval process, expert support makes all the difference. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle buyers navigate conventional financing, from initial pre-approval through closing in as few as nine business days. If you're ready to explore your options and develop a personalized homebuying strategy, connect with Mortgage Reel today to get started.