Purchasing your first home represents one of the most significant financial decisions you'll ever make, and understanding your financing options is essential to success. First time mortgage loans come with unique benefits, specialized programs, and strategic considerations that can make homeownership more accessible than many Seattle-area buyers realize. Whether you're a tech professional at Amazon or Microsoft looking to settle in Bellevue, or a young family searching for your perfect home in Lake Forest Park, knowing how to navigate the mortgage landscape will position you for confident decision-making in 2026's competitive market.

Understanding First Time Mortgage Loans

First time mortgage loans encompass various financing products specifically designed to help new buyers overcome common barriers to homeownership. The Consumer Financial Protection Bureau defines these loan options to include conventional, FHA, VA, and USDA programs, each with distinct advantages depending on your financial situation and homeownership goals.

What qualifies you as a first-time buyer extends beyond the obvious definition. Most programs consider you a first-time homebuyer if you haven't owned a primary residence in the past three years, meaning even previous homeowners may qualify for these specialized programs. This broader definition opens opportunities for buyers in Seattle, Shoreline, and surrounding communities who may have sold a home years ago or co-owned property without being on the mortgage.

Key Benefits for New Homebuyers

First time mortgage loans typically offer advantages that make the path to homeownership more manageable:

- Lower down payment requirements, often as low as 3% for conventional loans and 3.5% for FHA loans

- More flexible credit score requirements compared to standard mortgage products

- Access to down payment assistance programs available through Washington State and local municipalities

- Potential seller concessions to help cover closing costs

- Educational resources and counseling often required or recommended as part of the loan process

The National Association of Realtors reports that these specialized programs have helped millions of Americans achieve homeownership, particularly in high-cost markets like the Greater Seattle area where home prices continue to challenge new buyers.

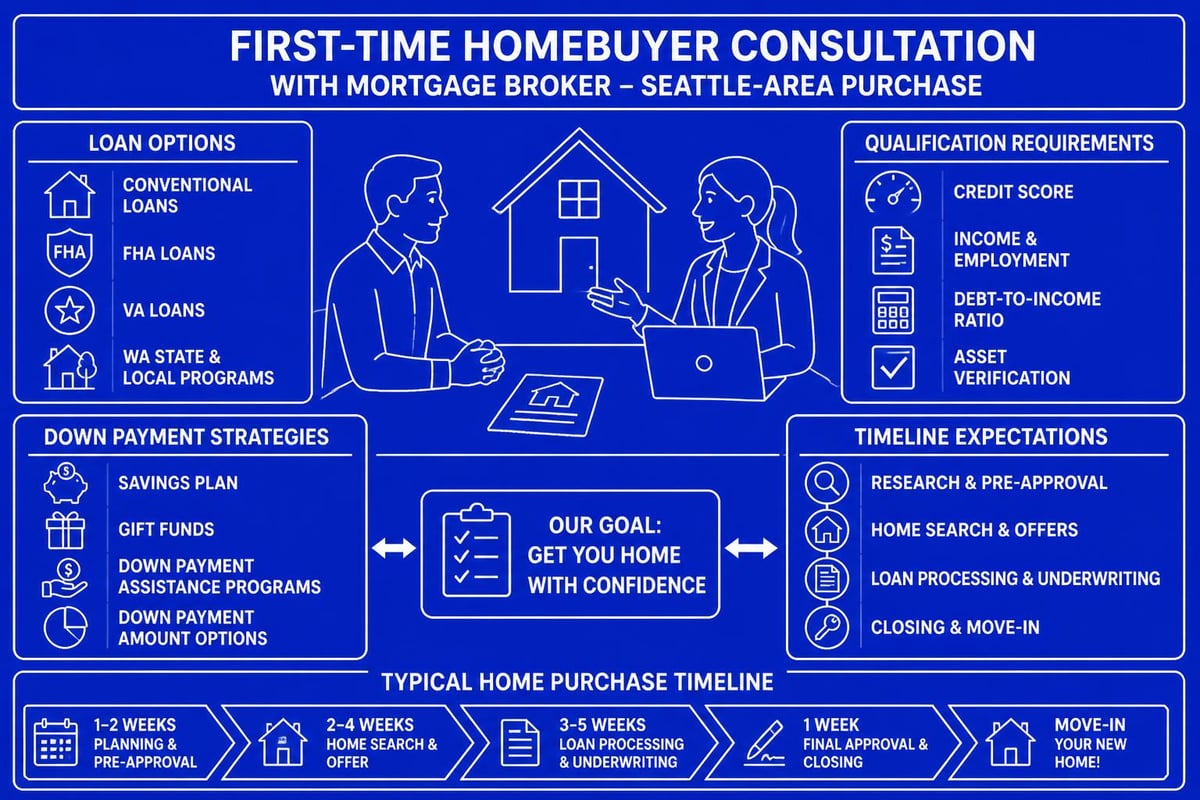

Popular Loan Programs for First-Time Buyers

Selecting the right mortgage product requires understanding how each program aligns with your financial profile, long-term goals, and the specific property you're purchasing.

Conventional Loans with Low Down Payments

Conventional conforming loans backed by Fannie Mae and Freddie Mac now offer down payment options as low as 3% for qualified first-time buyers. These loans have become increasingly attractive in Seattle and Kirkland for buyers with solid credit profiles who want to avoid mortgage insurance more quickly than FHA alternatives.

The primary advantages include:

- Competitive interest rates for borrowers with credit scores above 680

- The ability to cancel private mortgage insurance (PMI) once you reach 20% equity

- Higher loan limits that accommodate Seattle's elevated home prices

- Flexibility in property types, including condos in downtown Seattle or single-family homes in Mill Creek

Working with experienced conventional loan lenders ensures you understand the full scope of options available through these programs.

FHA Loans for Accessible Entry

Federal Housing Administration loans remain one of the most popular choices for first time mortgage loans across Washington State. With just 3.5% down and credit score requirements as low as 580, FHA loans provide accessibility that conventional products sometimes cannot match.

| Feature | FHA Loan | Conventional 3% Down |

|---|---|---|

| Minimum Down Payment | 3.5% | 3% |

| Minimum Credit Score | 580 (with 3.5% down) | 620 |

| Mortgage Insurance | Upfront + Annual (life of loan) | Monthly PMI (cancelable) |

| Debt-to-Income Ratio | Up to 50% (with compensating factors) | Typically 43-45% |

| Gift Funds | 100% of down payment allowed | 100% of down payment allowed |

Understanding FHA home loans helps buyers in Lynnwood and Everett determine whether this program fits their specific situation, especially when balancing slightly higher long-term costs against immediate accessibility.

VA Loans for Military Members

Veterans, active-duty service members, and eligible surviving spouses have access to one of the most powerful first-time buyer tools: VA loans. These government-backed mortgages require zero down payment, offer competitive interest rates, and eliminate monthly mortgage insurance entirely.

The benefits extend significantly in expensive markets like Seattle, where the $0 down payment requirement can mean the difference between renting and owning. For those who've served, exploring VA loan options should be the first step in your homebuying journey.

USDA Loans in Eligible Areas

While much of Seattle proper doesn't qualify, certain areas in Snohomish County and beyond may be eligible for USDA Rural Development loans. These zero-down-payment mortgages serve low-to-moderate income buyers in qualifying rural and suburban areas, making them worth investigating for buyers looking slightly outside the urban core.

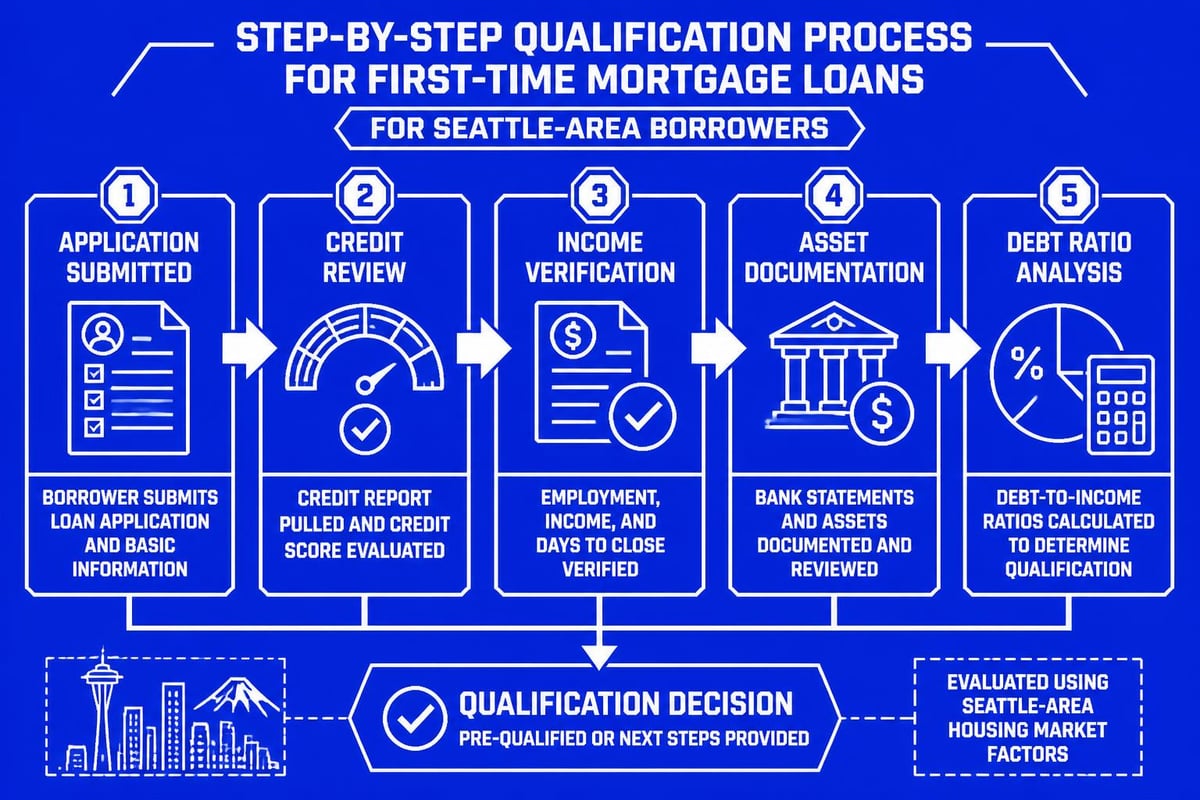

Qualifying for Your First Mortgage

The qualification process for first time mortgage loans involves several critical components that lenders evaluate to determine your borrowing capacity and risk profile.

Credit Score Requirements

Your credit score serves as a foundational element in mortgage qualification. While minimum scores vary by program, understanding where you stand helps set realistic expectations:

- FHA loans: 580 minimum for 3.5% down; 500-579 requires 10% down

- Conventional loans: 620 minimum, though 680+ receives better pricing

- VA loans: No official minimum, though most lenders prefer 580+

- USDA loans: 640 minimum for automated underwriting

Seattle buyers wondering about credit score requirements should know that these are guidelines, not absolutes. Compensating factors like substantial savings, stable employment, or low debt can sometimes offset lower scores.

Income Documentation and Debt Ratios

Lenders evaluate your ability to repay through detailed income verification and debt-to-income (DTI) ratio calculations. For tech professionals in Seattle's booming employment market, this process often involves qualifying stock compensation, RSUs, bonuses, and equity packages that traditional lenders might overlook.

Standard documentation includes:

- Two years of W-2 forms and recent pay stubs

- Two years of tax returns for self-employed buyers

- Bank statements showing reserves and down payment funds

- Documentation of any additional income sources (rental properties, bonuses, commissions)

Front-end DTI (housing expenses divided by gross income) and back-end DTI (all debts divided by gross income) typically shouldn't exceed 43-50%, depending on the loan program and compensating factors.

Down Payment Sources and Strategies

Accumulating your down payment represents one of the most challenging aspects of buying your first home in Seattle's expensive market. Fortunately, multiple strategies and sources can help:

- Personal savings from dedicated homebuying accounts

- Gift funds from family members (properly documented and sourced)

- Down payment assistance programs through Washington State Housing Finance Commission

- Employer assistance programs (increasingly common among Seattle tech companies)

- Retirement account withdrawals (first-time buyers can withdraw up to $10,000 from IRAs penalty-free)

Understanding down payment options specific to Washington State helps buyers in Shoreline and Lake Forest Park create realistic savings timelines and explore all available resources.

Strategic Considerations for Seattle Buyers

The unique characteristics of Seattle's housing market require first-time buyers to approach their mortgage strategy with local knowledge and competitive awareness.

Navigating Competitive Markets

Seattle, Bellevue, and Redmond consistently rank among the nation's most competitive housing markets. First time mortgage loans must be structured to enable quick closings and strong offers that sellers will accept.

Key competitive advantages include:

- Pre-approval letters that demonstrate verified income and assets

- Financing terms that allow closing in 9-15 business days when needed

- Conventional or VA loans that sellers often prefer over FHA or USDA

- Substantial earnest money deposits showing commitment

- Waiving financing contingencies only when truly appropriate and safe

Working with a Seattle mortgage broker who understands local market dynamics helps position your offer competitively without taking unnecessary risks.

Understanding Total Housing Costs

Your mortgage payment represents just one component of total housing costs. First-time buyers must budget for the complete picture to avoid financial strain:

| Cost Component | Typical Monthly Amount (Seattle Area) |

|---|---|

| Principal & Interest | Varies by loan amount and rate |

| Property Taxes | $300-$800+ (depending on assessed value) |

| Homeowners Insurance | $100-$250 |

| HOA Fees (if applicable) | $200-$600+ |

| Mortgage Insurance | $50-$300 (if less than 20% down) |

| Utilities | $150-$300 |

| Maintenance Reserve | $100-$200 |

This comprehensive view ensures you're financially prepared for the reality of homeownership in neighborhoods from Capitol Hill to Mill Creek.

Timing Your Purchase

Interest rate environments, seasonal market fluctuations, and personal financial milestones all influence optimal purchase timing. In 2026, buyers should consider:

- Current rate trends and whether locking sooner or waiting makes strategic sense

- Seasonal inventory patterns (Seattle typically sees more listings in spring and summer)

- Personal financial readiness including job stability, savings levels, and credit health

- Life circumstances such as lease expirations, growing families, or job relocations

Research from the Federal Housing Finance Agency shows that first-time buyers who take adequate time to prepare financially and educationally tend to experience better long-term outcomes than those who rush the process.

Working with the Right Lending Partner

Selecting your mortgage lender ranks among your most important decisions as a first-time buyer. The difference between a transactional lender and a true advisory partner can mean thousands of dollars and significantly less stress throughout the process.

What to Look for in a Mortgage Broker

First time mortgage loans require expertise, patience, and commitment to education. When evaluating potential lenders in the Seattle area, prioritize these characteristics:

- Extensive experience with first-time buyers and the programs that serve them best

- Clear communication that demystifies complex mortgage concepts

- Transparent pricing with detailed explanations of rates, fees, and closing costs

- Local market knowledge specific to Seattle, Kirkland, Bellevue, and surrounding communities

- Proven track record demonstrated through client reviews and successful closings

Finding good mortgage brokers involves researching credentials, reading reviews, and interviewing multiple candidates to find the right fit.

Questions to Ask Before Committing

Before selecting your lender, gather critical information through targeted questions:

- What first-time buyer programs do you recommend for my specific situation?

- How do you handle income verification for stock compensation and bonuses?

- What is your average timeline from application to closing?

- Can you provide references from recent first-time buyers in Seattle?

- What happens if my financial situation changes during the process?

- How do you communicate throughout the transaction?

- What fees should I expect, and how do they compare to competitors?

These conversations reveal not just technical competence but also whether the lender prioritizes your success and education.

Common Mistakes to Avoid

First-time buyers often encounter predictable pitfalls that can delay closing, increase costs, or even derail transactions entirely. Awareness and proactive planning help you avoid these common errors.

Financial Missteps

- Making large purchases before closing (cars, furniture, appliances) that change your debt ratios

- Changing jobs during the loan process without consulting your lender first

- Opening new credit accounts that lower your credit score or increase monthly obligations

- Making large deposits without proper documentation of their source

- Depleting all savings for down payment without maintaining adequate reserves

Process and Documentation Errors

First time mortgage loans require substantial documentation, and missing or incomplete paperwork causes the majority of closing delays. Stay organized by:

- Responding promptly to all lender requests for documentation

- Keeping digital and physical copies of all submitted documents

- Maintaining consistent communication with your loan officer

- Reading all disclosures carefully before signing

- Asking questions immediately when something is unclear

Property Selection Issues

Not all properties qualify for all loan programs. Common issues include:

- Properties requiring substantial repairs that don't meet FHA or USDA property standards

- Condos not approved by FHA, VA, or Fannie Mae

- Properties in flood zones requiring additional insurance and down payment

- Homes with non-standard features like septic systems in areas with available sewer

- Properties in homeowners associations with financial or legal problems

Understanding these limitations before making offers prevents disappointment and wasted time.

First-Time Buyer Programs in Washington State

Beyond federal loan programs, Washington State and local municipalities offer additional resources that make first time mortgage loans more accessible and affordable.

State-Level Assistance

The Washington State Housing Finance Commission administers several programs worth investigating:

- Home Advantage program offering down payment assistance

- House Key program for qualifying first-time buyers

- Targeted area programs with enhanced benefits in certain counties

- MCC (Mortgage Credit Certificate) programs providing federal tax credits

These programs often have income limits, purchase price limits, and property location requirements that vary by county. Seattle and Snohomish County buyers should verify current limits and availability.

Local Municipality Programs

Cities throughout the Greater Seattle area periodically offer their own first-time buyer incentives. Lake Forest Park, Shoreline, and other communities sometimes provide:

- Down payment assistance loans (forgivable over time)

- Reduced fees for first-time buyers

- Property tax exemptions or deferrals

- Partnerships with local employers for employee housing benefits

Exploring first-time buyer programs in your target area ensures you leverage all available resources.

Preparing for Your First Mortgage Application

Successful first time mortgage loans begin with thorough preparation months before you start house hunting.

Building Your Financial Foundation

Six to twelve months before applying:

- Review your credit reports and dispute any errors

- Pay down high credit card balances to improve utilization ratios

- Avoid applying for new credit unless absolutely necessary

- Build your savings to cover down payment, closing costs, and reserves

- Document irregular income sources like bonuses or commissions

- Research loan programs and connect with potential lenders

Creating Your Home Buying Budget

Determine what you can comfortably afford by analyzing:

- Maximum monthly payment you can sustain long-term (including all housing costs)

- Down payment amount currently available or achievable within your timeline

- Closing costs typically 2-5% of purchase price beyond down payment

- Emergency reserves recommended 3-6 months of housing expenses

- Future income prospects and stability

This realistic assessment prevents overextending yourself financially and ensures sustainable homeownership.

Educating Yourself on the Process

Government resources like USA.gov provide valuable information on home loans and the mortgage process. Additionally, many lenders offer educational seminars, one-on-one consultations, and online resources specifically designed for first-time buyers.

Understanding mortgage terminology, timeline expectations, and common scenarios reduces stress and enables better decision-making throughout your journey. Buyers who invest time in education typically report higher satisfaction and confidence in their decisions.

Moving Forward with Confidence

First time mortgage loans in Seattle's dynamic market require strategic planning, expert guidance, and realistic expectations. The path from initial research to closing day involves numerous decisions, each building toward successful homeownership.

Your action steps for moving forward include:

- Assessing your current financial readiness honestly

- Researching loan programs that align with your situation

- Connecting with experienced local lenders who specialize in first-time buyers

- Getting pre-approved before beginning your home search

- Working with a knowledgeable real estate agent familiar with first-time buyer needs

- Remaining patient and flexible as you navigate the competitive Seattle market

The investment you make in proper preparation, education, and professional partnerships will pay dividends throughout your homeownership journey. From tech professionals purchasing condos in Bellevue to growing families finding space in Lynnwood or Everett, first time mortgage loans make homeownership achievable with the right strategy and support.

Understanding programs like home loans for first-time buyers positions you to make confident, informed decisions that align with both your immediate needs and long-term financial goals. The Seattle housing market rewards prepared buyers who combine financial readiness with strategic financing and experienced professional guidance.

Navigating first time mortgage loans successfully requires understanding your options, preparing your finances, and partnering with professionals who prioritize your education and success. Whether you're a tech professional leveraging stock compensation or a traditional W-2 employee building toward homeownership in Seattle, Bellevue, Redmond, Kirkland, or surrounding communities, expert guidance makes all the difference. Keith Akada brings over 25 years of mortgage experience and more than 750 five-star reviews to help first-time buyers make confident, informed decisions throughout the loan process. Contact Mortgage Reel today to discuss your first-time homebuyer options and create a personalized strategy for achieving your homeownership goals in 2026.