Choosing the right home lending company can determine whether your Seattle homebuying experience feels smooth and strategic or complicated and stressful. With mortgage originations experiencing notable shifts in recent years, understanding how these companies operate, what sets them apart, and how to evaluate your options has never been more important. Whether you're a first-time buyer in Shoreline, a tech professional with stock compensation in Bellevue, or an investor exploring opportunities in Lynnwood, working with an experienced home lending company provides access to expertise, product variety, and personalized guidance that can maximize your buying power and minimize uncertainty.

What a Home Lending Company Actually Does

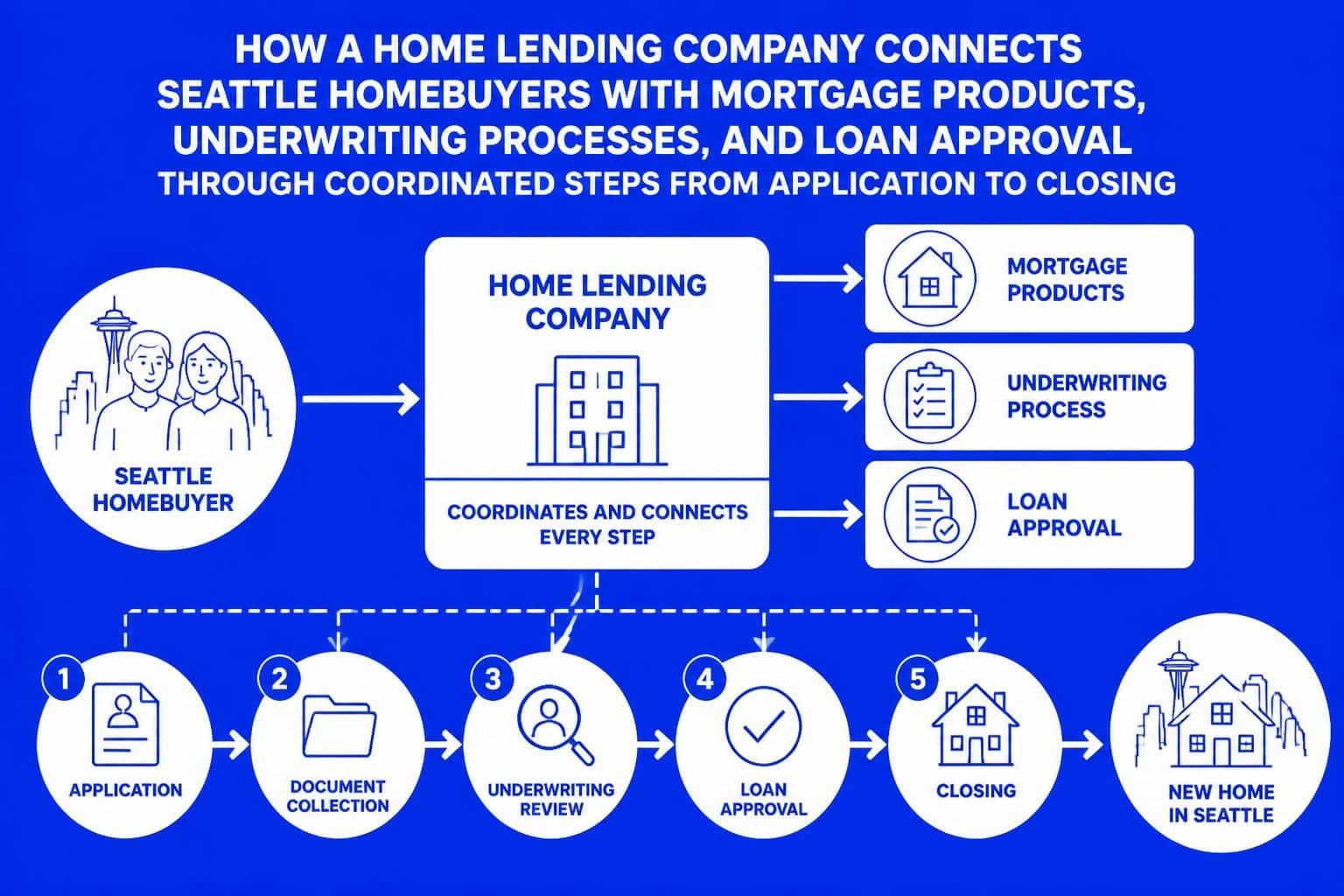

A home lending company specializes in originating, processing, and funding mortgage loans for residential property purchases and refinances. These organizations serve as the intermediary between borrowers and the capital markets, evaluating creditworthiness, verifying income and assets, and ensuring compliance with federal lending regulations.

Core Functions and Services

Home lending companies provide multiple essential services throughout the mortgage lifecycle:

- Loan origination: Taking applications, collecting documentation, and initiating the underwriting process

- Product selection: Offering various loan programs including conventional, FHA, VA, USDA, and jumbo mortgages

- Rate pricing: Determining interest rates based on market conditions, borrower qualifications, and loan characteristics

- Underwriting coordination: Working with internal or third-party underwriters to assess risk and approve loans

- Closing facilitation: Managing title work, insurance requirements, and final funding logistics

The distinction between different lending entities matters significantly. Independent mortgage banks, which originated 84.1% of single-family loans in 2025, often provide more personalized service and faster decision-making compared to larger institutional lenders.

Regulatory Framework and Consumer Protection

Every reputable home lending company operates under strict oversight from federal and state regulators. The Consumer Financial Protection Bureau (CFPB) enforces Truth in Lending Act (TILA) requirements, ensuring borrowers receive accurate loan estimates and closing disclosures. State licensing boards verify that loan officers maintain continuing education and adhere to ethical standards.

For Seattle-area borrowers, working with a licensed home lending company means your transaction follows standardized procedures designed to protect your interests. This includes mandatory three-day review periods before closing, clear disclosure of all fees, and the right to shop for services like title insurance and home inspections.

Types of Home Lending Companies Serving Seattle

The mortgage industry comprises several distinct business models, each offering different advantages depending on your situation and priorities.

| Lender Type | Primary Advantage | Typical Timeline | Best For |

|---|---|---|---|

| Independent Mortgage Bank | Personalized service, flexible underwriting | 9-21 business days | Complex income, jumbo loans |

| Credit Union | Member benefits, competitive rates | 21-30 business days | Standard W-2 income, existing members |

| Retail Bank | Relationship discounts, convenience | 30-45 business days | Simple transactions, current customers |

| Online Lender | Digital convenience, low fees | 15-25 business days | Tech-savvy borrowers, straightforward scenarios |

Independent Mortgage Banks and Brokerages

Independent mortgage companies like Mortgage Reel partner with multiple wholesale lenders while maintaining direct relationships with borrowers. This model provides access to diverse loan products while preserving the personal touch that competitive Seattle markets demand.

For tech professionals at Amazon, Microsoft, and Google with RSU income, this flexibility proves invaluable. A specialized home lending company can structure documentation to maximize qualifying income from stock compensation, bonuses, and restricted stock units-capabilities that generic retail banks often lack.

Credit Unions and Community Banks

Home equity lending has grown particularly strong at credit unions, with originations rising over 7% recently. These member-owned institutions often provide competitive rates for borrowers with stable W-2 income and strong existing banking relationships.

In areas like Lake Forest Park and Mill Creek, where many homebuyers work in established professions with predictable income patterns, credit unions can offer straightforward conventional loans with relationship-based pricing advantages.

Evaluating a Home Lending Company: Key Criteria

Selecting your lender requires assessment across multiple dimensions that directly impact your experience and financial outcome.

Licensing, Reviews, and Track Record

Verify that any home lending company you consider holds appropriate state licensing through the Nationwide Multistate Licensing System (NMLS). Review ratings across multiple platforms including Google, Zillow, Redfin, and Yelp to identify consistent patterns in customer feedback.

Look specifically for commentary about:

- Communication responsiveness during evenings and weekends

- Timeline reliability in competitive offer situations

- Problem-solving capability when documentation or qualification challenges arise

- Post-closing support for questions about escrow accounts or payment processing

Understanding good mortgage brokers involves evaluating both technical competence and interpersonal skills that make complex transactions feel manageable.

Product Variety and Qualification Flexibility

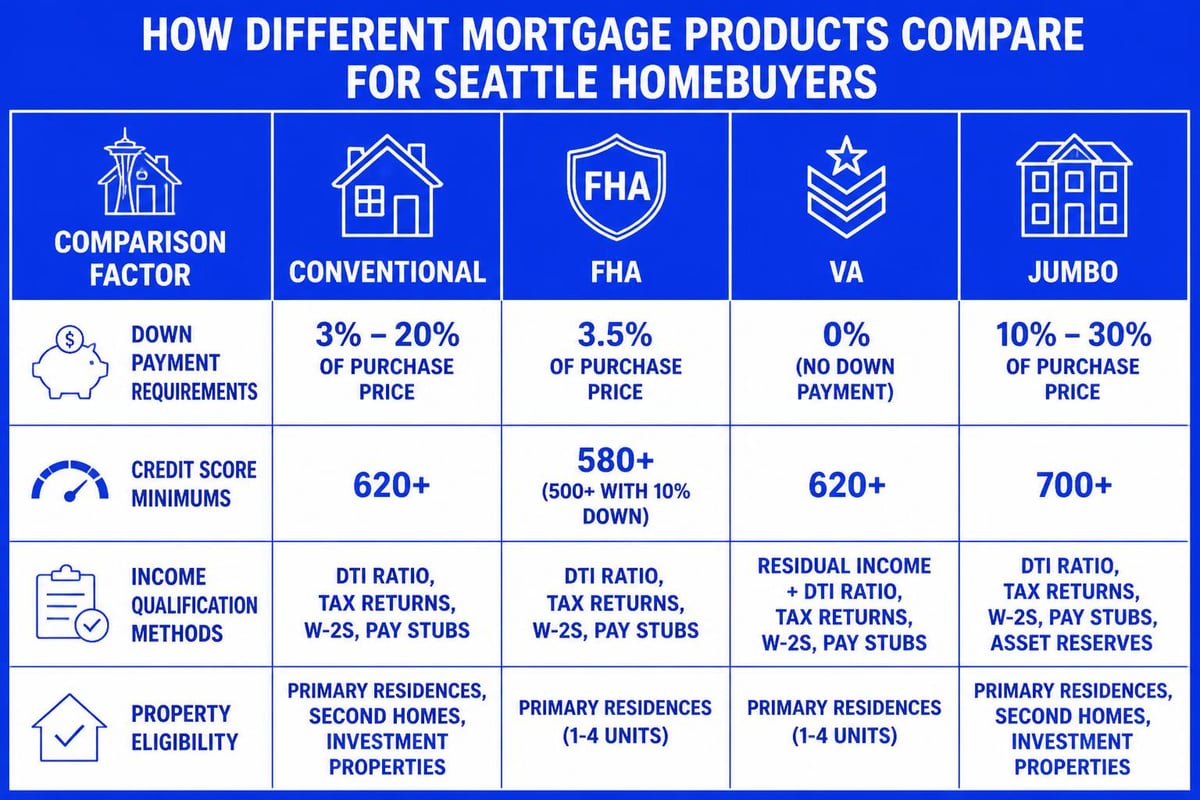

The best home lending company for your situation depends heavily on your income structure, down payment capacity, and property type. First-time homebuyers represented a record share of purchase lending in early 2025, highlighting the importance of low-down-payment options.

Essential product offerings include:

- Conventional loans with as little as 3% down for qualified first-time buyers

- FHA financing allowing credit scores as low as 580 with proper documentation

- VA loans providing zero-down options for eligible military service members and veterans

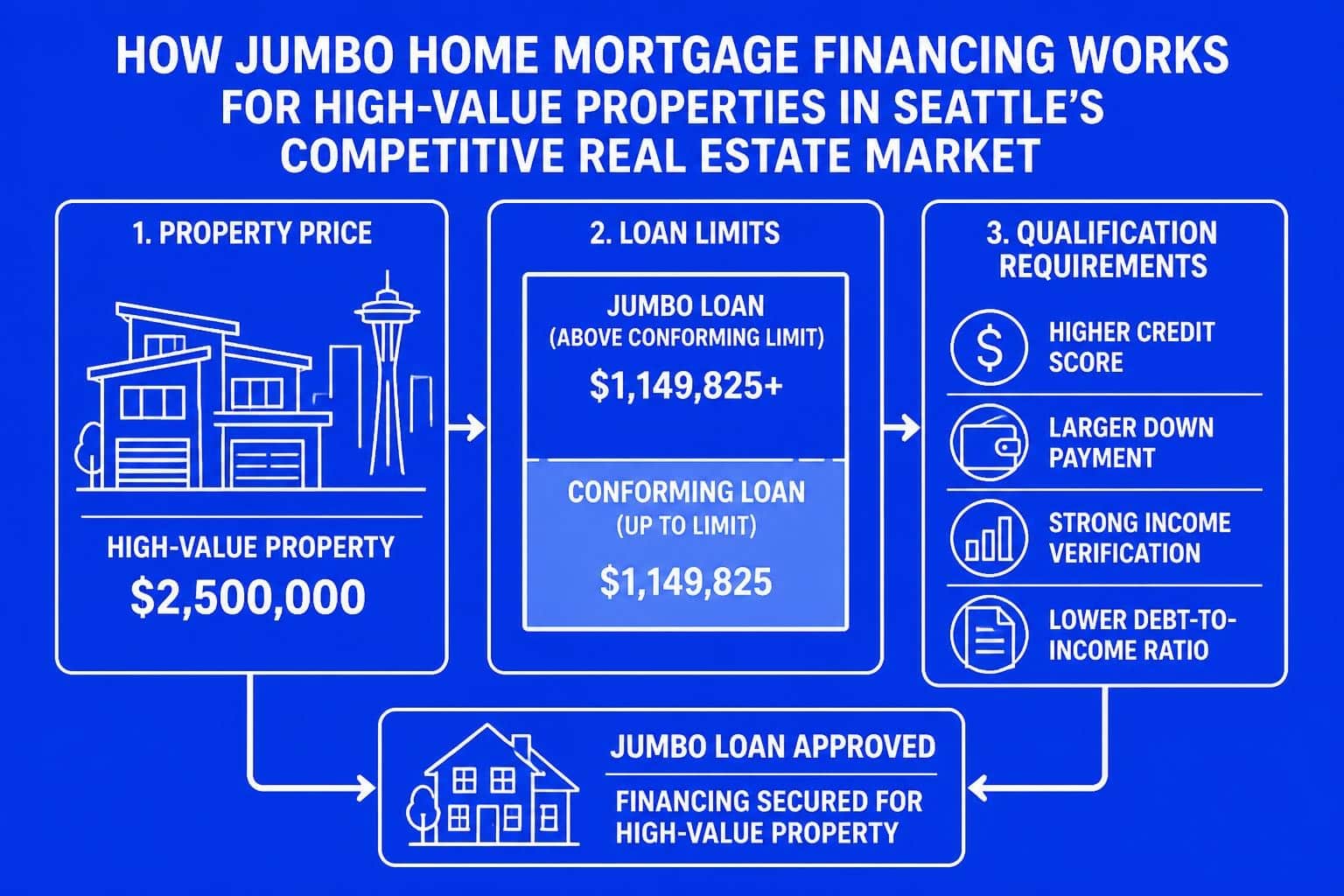

- Jumbo mortgages for properties exceeding conforming loan limits in King and Snohomish counties

- Investment property financing for buyers building rental portfolios in Everett or Shoreline

A home lending company that specializes in jumbo home loans can structure transactions that conventional-only lenders cannot accommodate, particularly important given Seattle's median home prices.

Speed and Execution in Competitive Markets

Federal Reserve policies significantly influence mortgage rates, creating windows of opportunity when rates dip temporarily. A home lending company with streamlined processes can close loans in as few as 9 business days when necessary, providing competitive advantage in multiple-offer scenarios.

Seattle's housing market demands execution speed without sacrificing accuracy. Experienced lenders pre-underwrite files before properties go under contract, identify potential issues early, and maintain clear communication with all transaction parties.

How Home Lending Companies Qualify Seattle Borrowers

Understanding qualification mechanics helps you prepare documentation, improve your profile, and set realistic expectations about loan amounts and terms.

Income Verification Methods

Standard W-2 employees provide recent pay stubs, W-2 forms, and employment verification. The home lending company calculates qualifying income using year-to-date earnings adjusted for payroll deductions and tax obligations.

Self-employed borrowers face more complex documentation requirements:

- Two years of personal tax returns with all schedules

- Two years of business tax returns (for partnerships, S-corps, or sole proprietorships)

- Year-to-date profit and loss statement

- Business license and CPA letter (sometimes required)

For tech professionals with equity compensation, a knowledgeable home lending company can qualify RSUs, ESPP proceeds, and performance bonuses using specific methodologies that maximize borrowing capacity without violating underwriting guidelines.

Credit and Asset Requirements

Minimum credit scores vary by loan program, but conventional financing typically requires 620 or higher for competitive rates. FHA loans accept scores as low as 580 with 3.5% down, while VA loans often approve borrowers at 580-600 depending on compensating factors.

Asset verification confirms down payment sources and reserves. A home lending company examines:

| Asset Type | Verification Method | Typical Documentation |

|---|---|---|

| Bank accounts | 2 months statements | All pages, all accounts |

| Retirement accounts | Current statement | 401(k), IRA, TSP balances |

| Investment accounts | Recent statement | Stocks, bonds, mutual funds |

| Gift funds | Gift letter + proof of transfer | Donor statement + recipient deposit |

Properties in Lynnwood, Shoreline, and Mill Creek often require reserves (additional months of mortgage payments in savings) for jumbo loans or investment properties.

Market Trends Affecting Home Lending Companies in 2026

The lending landscape continues evolving in response to economic conditions, regulatory changes, and consumer preferences that shape how home lending companies operate.

Interest Rate Environment and Volume Trends

Analysis of U.S. home lending trends for 2025 reveals how rising mortgage rates affected home sales and lender competition. Despite these headwinds, mortgage originations and home equity lending grew in Q2 2025 as borrowers adapted to the new rate reality.

For Seattle buyers, this environment creates opportunities. Reduced competition means more negotiating leverage, while experienced home lending companies can structure creative solutions like temporary rate buydowns or seller concessions that offset higher borrowing costs.

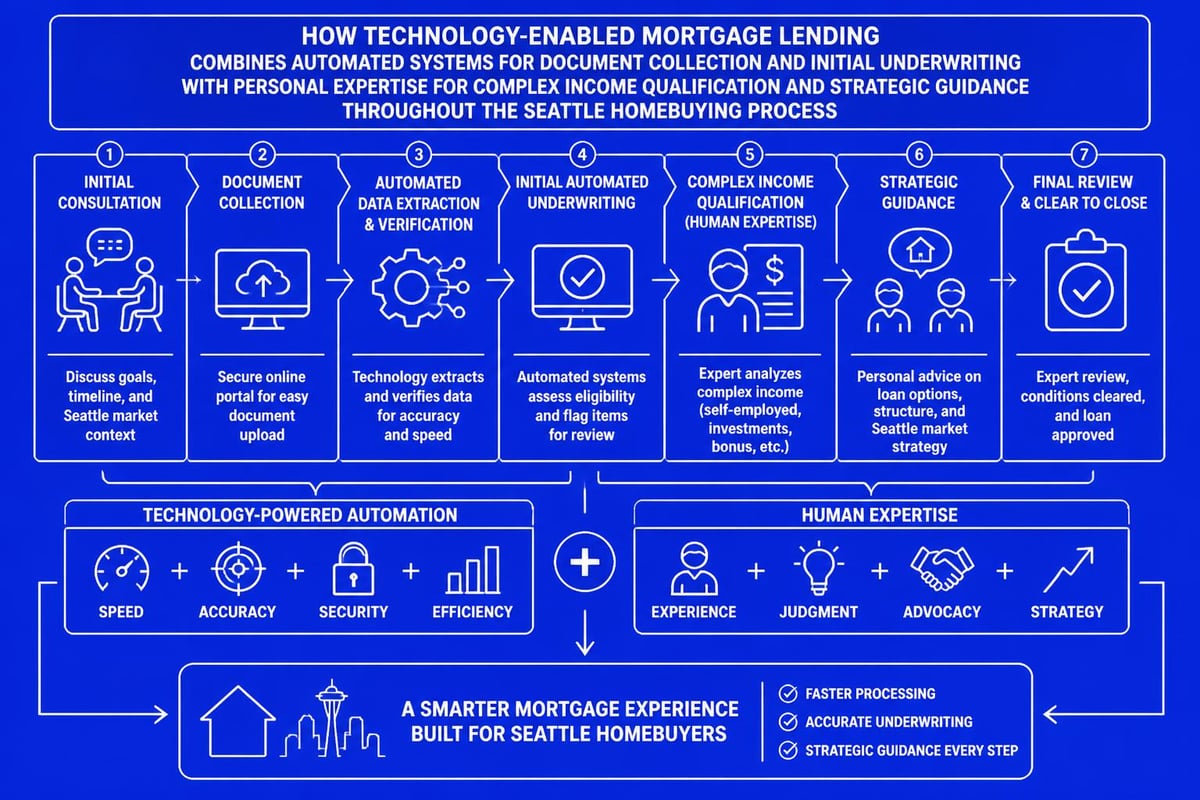

Technology Integration and Digital Processes

Modern home lending companies leverage technology to accelerate processing while maintaining compliance standards. Automated underwriting systems provide preliminary approvals within minutes, digital document collection eliminates mailing delays, and electronic signatures streamline closing procedures.

However, technology cannot replace human expertise when handling complex scenarios. The optimal home lending company combines digital efficiency with personal guidance, particularly valuable for first-time mortgage loans where buyers need education alongside execution.

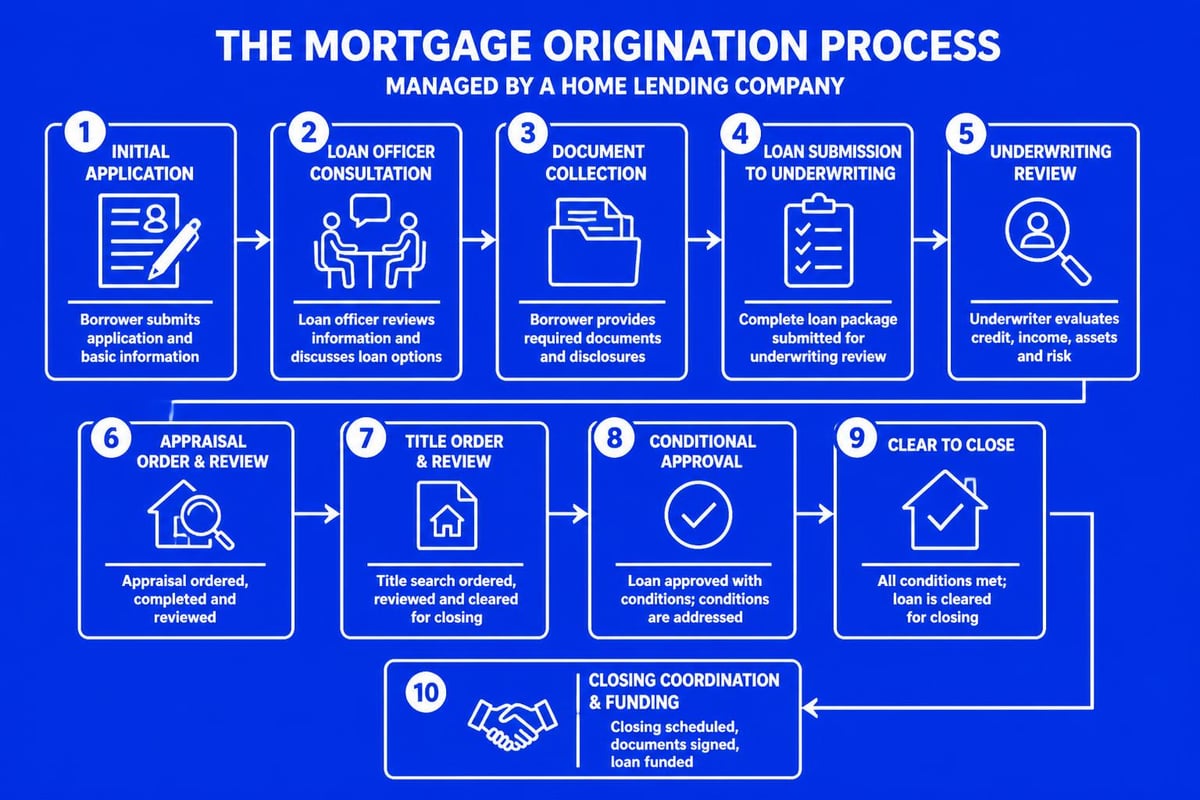

Working with a Home Lending Company: Process Overview

Understanding the typical timeline and milestones helps you prepare adequately and avoid last-minute surprises.

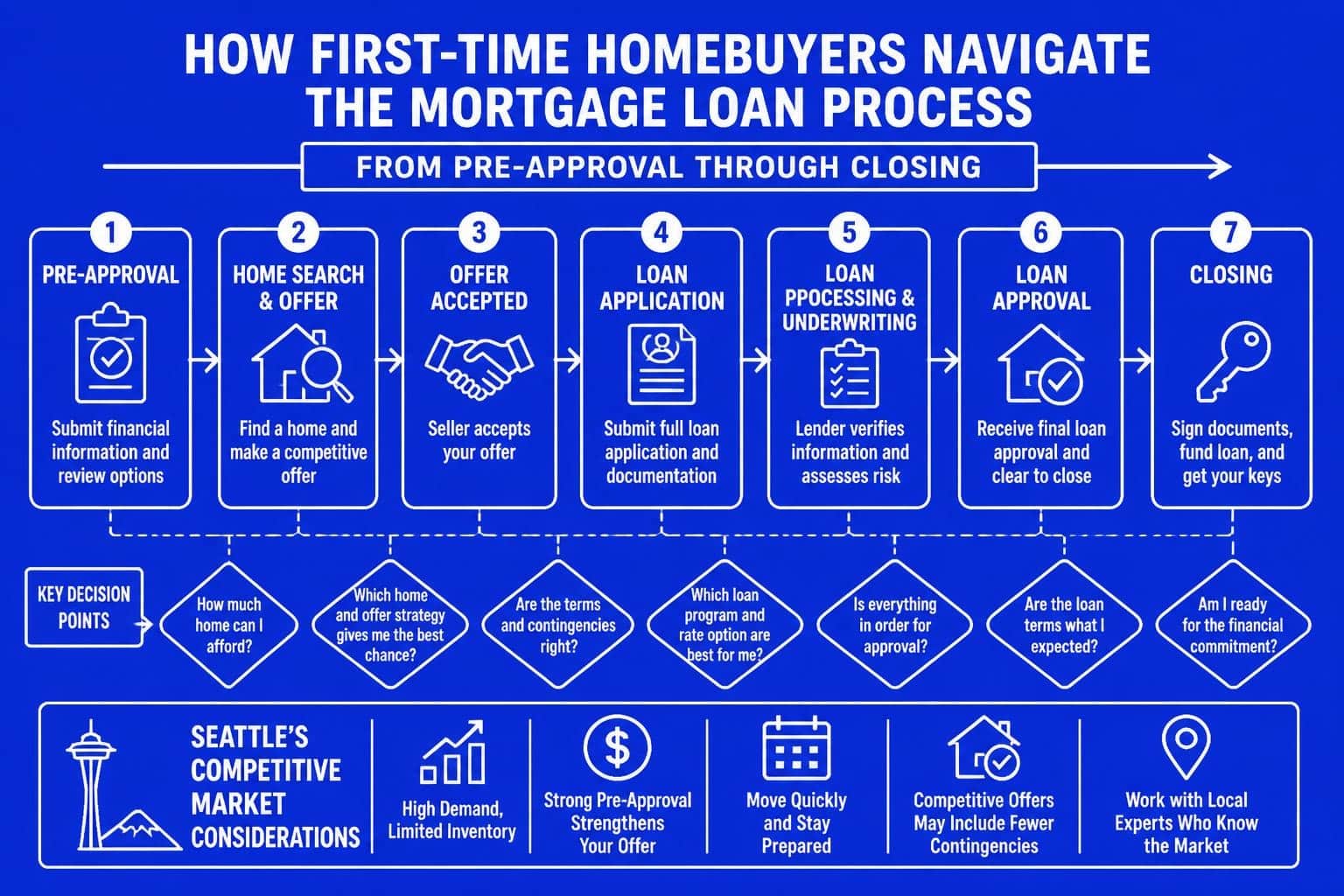

Pre-Approval Through Application

The relationship with your home lending company begins with pre-approval, a critical step in competitive Seattle markets. This process involves:

- Initial consultation to discuss goals, timeline, and preliminary qualifications

- Credit report review identifying scores and any issues requiring attention

- Income and asset documentation collection establishing borrowing capacity

- Pre-approval letter issuance showing sellers you're a serious, qualified buyer

A strong pre-approval from a reputable home lending company often proves decisive when sellers receive multiple offers. Listing agents recognize lenders with reliable track records and favor offers backed by thorough pre-underwriting.

Under Contract Through Closing

Once you have an accepted offer, your home lending company coordinates multiple concurrent activities:

- Formal application submission with complete documentation package

- Property appraisal ordering to verify value supports loan amount

- Title examination ensuring clear ownership and identifying lien issues

- Homeowners insurance coordination meeting lender coverage requirements

- Final underwriting review confirming all conditions are satisfied

Clear communication during this phase separates exceptional home lending companies from average ones. Regular status updates, proactive problem identification, and weekend availability ensure you're never uncertain about your transaction's progress.

Special Considerations for Seattle-Area Buyers

Local market dynamics create unique situations that experienced home lending companies navigate routinely.

Jumbo Loan Qualification

Properties exceeding $806,500 (the 2026 conforming loan limit for King County) require jumbo financing with stricter requirements. Most home lending companies require:

- Minimum 680-700 credit score depending on down payment

- Lower debt-to-income ratios (typically 43% maximum)

- Larger reserves (6-12 months mortgage payments)

- Additional income documentation for self-employed borrowers

For Seattle tech professionals, understanding how your home lending company qualifies stock compensation becomes essential. Proper documentation of vesting schedules, historical grant patterns, and market volatility considerations can add tens of thousands to your qualifying income.

Condominium and Townhome Financing

Seattle's urban neighborhoods feature significant condominium inventory requiring special attention. A knowledgeable home lending company verifies that condo projects meet Fannie Mae, Freddie Mac, FHA, or VA approval standards before proceeding with your loan.

Key issues include:

- Owner-occupancy ratios meeting minimum thresholds for conventional financing

- Reserve fund adequacy ensuring the HOA maintains proper savings

- Litigation status confirming no major legal actions against the association

- Commercial space percentage staying within allowable limits

Projects in Bellevue, Redmond, and Kirkland sometimes require manual underwriting when they fall outside standard approval parameters, making your home lending company's expertise and lender relationships critical.

Cost Structure and Fee Transparency

Understanding what you pay and why helps you evaluate whether a home lending company provides fair value.

Loan Origination Charges

Lender fees typically include:

- Origination fee (0.5-1.0% of loan amount) covering processing and underwriting

- Discount points (optional) allowing you to buy down your interest rate

- Application fee (sometimes charged) for credit reports and initial processing

- Underwriting fee covering the cost of loan evaluation and approval

Reputable home lending companies provide detailed loan estimates within three business days of application, itemizing every charge so you can compare offers accurately. Learning about mortgage broker cost structures helps you understand industry norms and identify excessive fees.

Third-Party Services

Additional costs come from service providers your home lending company coordinates but doesn't directly control:

| Service | Typical Cost (Seattle) | Purpose |

|---|---|---|

| Appraisal | $500-$800 | Property valuation verification |

| Title insurance | $1,200-$2,500 | Ownership protection |

| Escrow/closing | $400-$800 | Settlement services coordination |

| Home inspection | $400-$600 | Property condition assessment |

| Survey (if required) | $350-$600 | Boundary verification |

Your home lending company should explain which services you can shop for independently and which come with lender requirements that limit your choices.

Questions to Ask Before Choosing Your Lender

Strategic questioning reveals whether a home lending company matches your needs and communication preferences.

Expertise and Specialization

- How many years has your loan officer worked in the Seattle market?

- What percentage of your clients have income structures similar to mine?

- Do you have experience with conventional loan lenders that approve complex compensation packages?

- Can you provide references from recent clients in my target neighborhoods?

Process and Communication

- What's your typical timeline from application to closing?

- How do you handle communication during evenings and weekends?

- Who will I work with if my primary loan officer is unavailable?

- What technology platforms do you use for document sharing and status updates?

Product Knowledge and Options

- What loan programs do you offer beyond conventional and FHA?

- Can you explain how you'd structure financing for a property requiring jumbo home mortgage products?

- Do you work with portfolio lenders for non-conforming scenarios?

- What's your approach to rate locks and timing strategy?

Why Local Expertise Matters in Seattle Markets

National online lenders offer convenience, but local home lending companies provide context that generic services cannot match. Understanding neighborhood price trends in Shoreline versus Everett, knowing which condo projects have financing restrictions, and recognizing how Seattle's tech economy affects income qualification makes a measurable difference in your outcome.

An experienced local home lending company anticipates issues before they become problems. They know which appraisers understand specific neighborhoods, which title companies handle complex situations efficiently, and which underwriters approve loans other lenders decline.

For buyers exploring opportunities throughout King and Snohomish counties, working with a home lending company that serves the entire region means consistent service quality whether you're purchasing in Lake Forest Park or Mill Creek. This geographic breadth combined with deep local knowledge creates competitive advantages that online-only lenders simply cannot replicate.

Selecting the right home lending company fundamentally shapes your Seattle homebuying experience, determining how smoothly your transaction proceeds and how well your financing aligns with your long-term goals. Whether you're pursuing home loans for first-time buyers or navigating complex jumbo financing with stock compensation, experienced guidance makes all the difference. Keith Akada brings 25+ years of Seattle mortgage expertise to every transaction, combining Fairway's advanced underwriting capabilities with personalized service that has earned 750+ five-star reviews. Get started with Mortgage Reel today.