Seattle's housing market presents unique challenges for homebuyers, particularly in neighborhoods like Capitol Hill, Bellevue, and Redmond where median home prices routinely exceed conforming loan limits. When purchasing properties valued above these thresholds, a jumbo home mortgage becomes necessary. Understanding how these specialized loans work, what lenders expect, and how tech professionals can leverage their compensation packages is critical for successful financing in 2026's competitive environment.

What Defines a Jumbo Home Mortgage

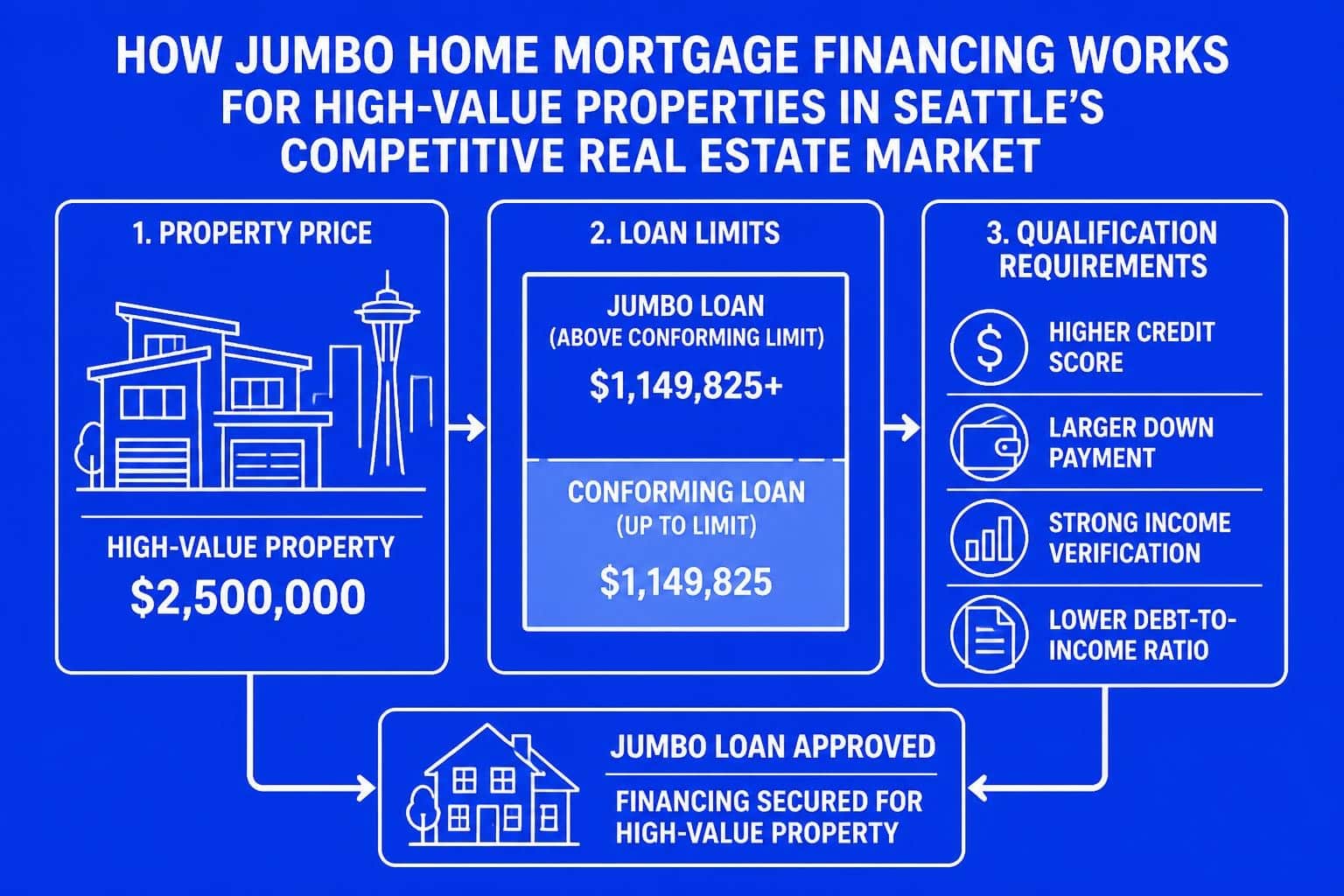

A jumbo home mortgage is a loan that exceeds the conforming loan limits set annually by the Federal Housing Finance Agency. In 2026, the baseline conforming limit stands at $806,500 for most counties nationwide, though certain high-cost areas may have higher thresholds. King County and Snohomish County fall into this category, with limits adjusted to reflect local market realities.

Current Loan Limits Across Greater Seattle

The distinction between conforming and jumbo financing impacts everything from interest rates to underwriting standards. Properties in Seattle, Shoreline, Lake Forest Park, and surrounding areas frequently require jumbo financing due to elevated market values.

| County | 2026 Conforming Limit | When Jumbo Financing Applies |

|---|---|---|

| King County | $1,209,750 | Above $1,209,750 |

| Snohomish County | $1,209,750 | Above $1,209,750 |

| Pierce County | $1,209,750 | Above $1,209,750 |

These limits apply to single-family homes. Multi-unit properties have different thresholds, with duplexes, triplexes, and fourplexes each carrying higher conforming limits. Any mortgage amount exceeding these boundaries requires specialized jumbo financing.

Qualification Requirements for Jumbo Financing

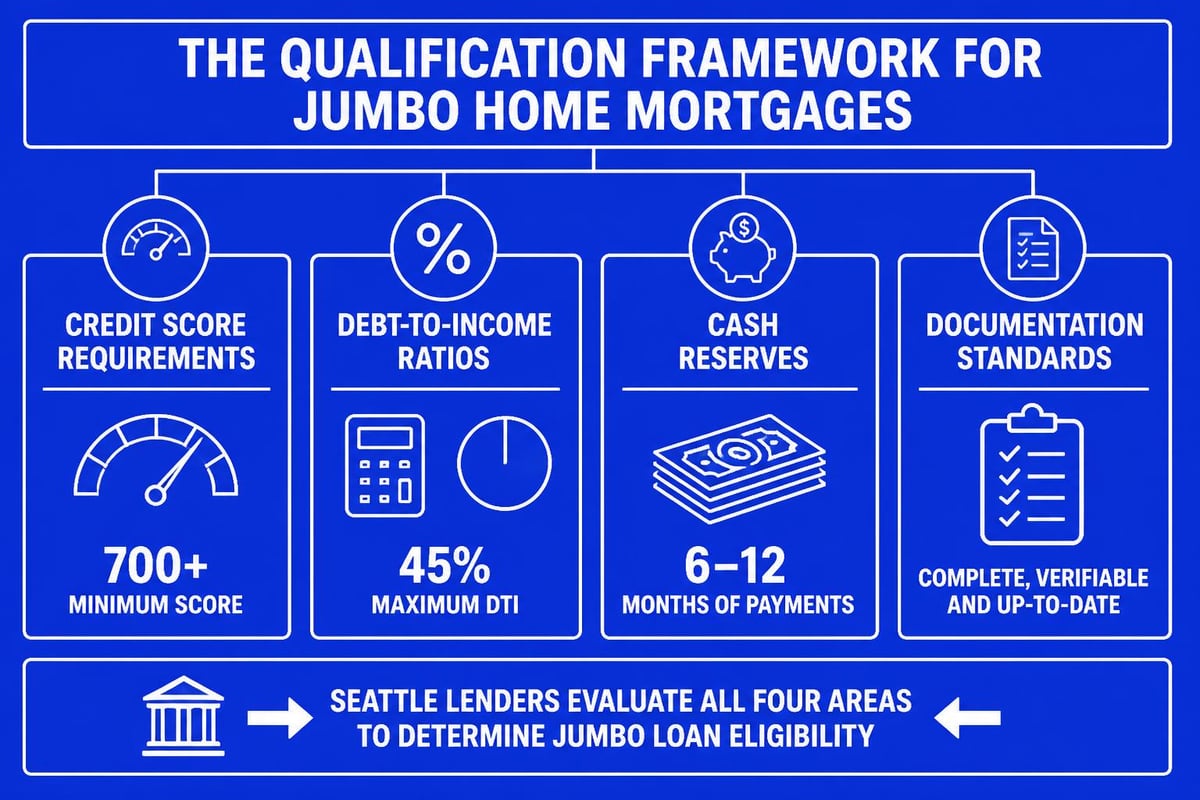

Jumbo home mortgage underwriting follows stricter guidelines than conventional loans. Lenders assume greater risk without government-sponsored enterprise backing, resulting in more comprehensive evaluation criteria.

Credit Profile Expectations

Most lenders require minimum credit scores between 700 and 720 for jumbo financing. However, competitive rates typically demand scores above 740. For tech professionals at Amazon, Microsoft, or Google, maintaining excellent credit through strategic debt management and timely payments creates substantial rate advantages.

- Minimum score: 700-720 for approval

- Preferred score: 740+ for best pricing

- Credit history: Two years of established credit

- Recent inquiries: Minimal new credit applications within six months

Income Documentation Standards

Jumbo underwriting requires exhaustive income verification. Standard employment income follows traditional documentation, but stock compensation demands specialized treatment. For Seattle-area tech professionals, understanding how lenders qualify restricted stock units, performance stock units, and bonus income proves essential.

Lenders typically average variable compensation over two years, though some allow one-year calculations for established employees. Keith Akada specializes in maximizing RSU and stock compensation qualification for tech professionals, often identifying additional buying power overlooked by conventional underwriting approaches.

Required documentation includes:

- Two years of tax returns with all schedules

- Two years of W-2 statements

- Year-to-date pay stubs covering recent 30 days

- Vesting schedules for stock compensation

- Employment verification directly from employer

- Detailed asset statements showing reserves

Debt-to-Income Ratio Calculations

Jumbo lenders typically cap debt-to-income ratios at 43%, though some programs allow up to 45% with compensating factors. This metric divides total monthly debt obligations by gross monthly income, creating a percentage that indicates repayment capacity.

For a borrower earning $20,000 monthly with $6,000 in existing debts and a proposed $4,000 mortgage payment, the DTI calculates to 50%, which exceeds most jumbo guidelines. Strategic debt reduction or income documentation optimization becomes necessary.

Down Payment Considerations and Options

Traditional jumbo financing required 20% down payments as standard practice. Today's market offers more flexibility, though larger down payments still provide rate advantages and reduced monthly obligations.

Standard Down Payment Structures

| Down Payment | Mortgage Insurance | Rate Impact | Reserve Requirements |

|---|---|---|---|

| 10% | Usually required | Higher rates | 12-18 months |

| 15% | Sometimes waived | Moderate rates | 9-12 months |

| 20% | Not required | Best rates | 6-12 months |

| 25%+ | Not required | Optimal pricing | 6 months |

The jumbo loan qualifier process evaluates down payment alongside other factors to determine overall risk profile. Borrowers should understand that deciding between 10 percent or 20 percent down on a jumbo loan involves trade-offs between liquidity preservation and long-term cost.

Cash Reserve Requirements

Beyond down payment funds, lenders require substantial cash reserves. These liquid assets demonstrate continued repayment capacity during income disruptions. Requirements typically range from six to twelve months of PITI (principal, interest, taxes, insurance), though larger loan amounts may demand eighteen months or more.

Acceptable reserve sources include checking accounts, savings accounts, investment portfolios, retirement accounts (with discounts applied), and vested stock compensation. Recent asset transfers require thorough documentation and sourcing to prevent undisclosed debt.

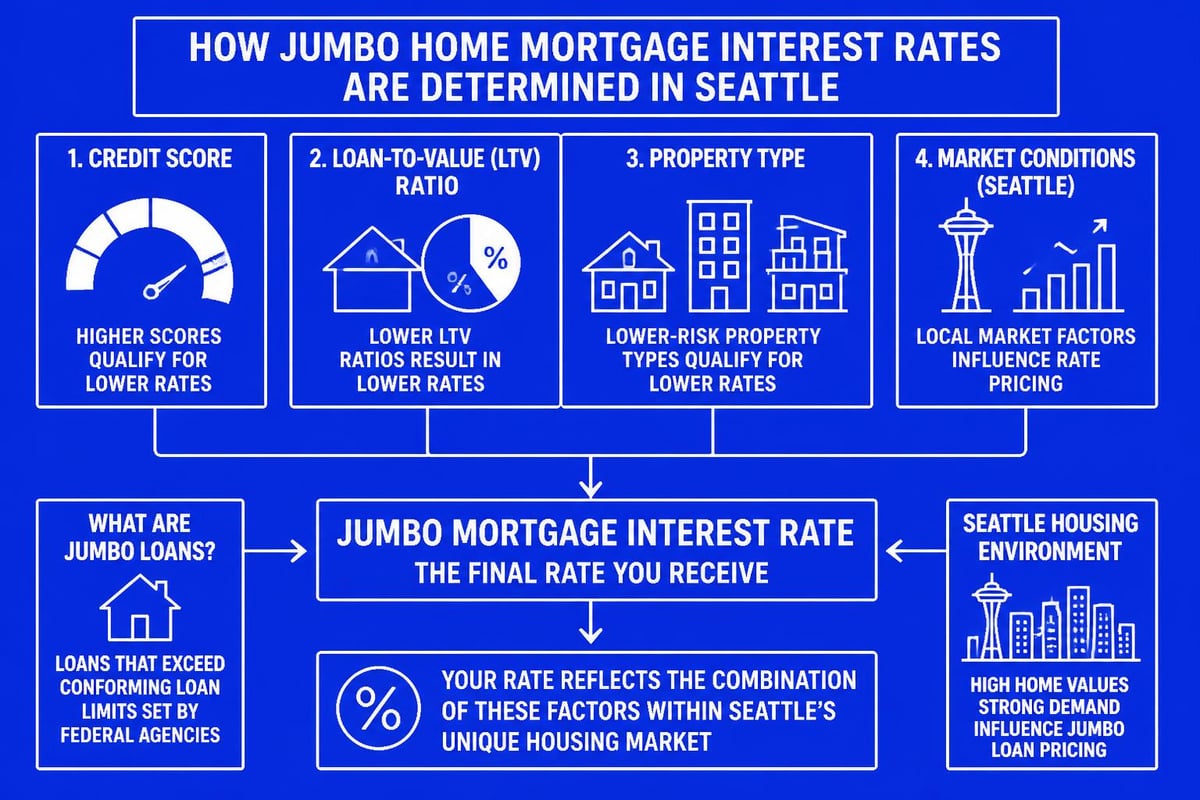

Interest Rates and Pricing Factors

Jumbo home mortgage rates fluctuate based on broader economic conditions plus individual borrower profiles. In 2026's market environment, rates remain sensitive to Federal Reserve policy, inflation data, and global economic trends.

What Influences Your Rate

Several variables determine the final interest rate offered on jumbo financing. Understanding these factors allows borrowers to optimize their profiles before application.

Primary rate determinants include:

- Credit score and overall credit profile

- Loan-to-value ratio and down payment percentage

- Property type and intended use (primary residence versus investment)

- Geographic location and property condition

- Loan amount relative to conforming limits

- Debt-to-income ratio and overall financial strength

- Cash reserves and liquid assets

- Relationship with lender and competitive positioning

Properties in desirable Seattle neighborhoods like Montlake, Portage Bay, or Capitol Hill may receive favorable treatment due to strong resale markets and property appreciation trends. Conversely, unique properties or those in emerging markets might face slight rate adjustments reflecting perceived risk.

Rate Comparison Strategies

Jumbo mortgage rates vary significantly across lenders, making comprehensive comparison essential. Working with an experienced mortgage broker in Seattle provides access to multiple wholesale lenders simultaneously, often revealing pricing advantages unavailable through retail channels.

Keith Akada's network through Fairway includes specialized jumbo lenders offering competitive programs designed specifically for high-earning professionals in technology sectors. This access frequently translates to rate improvements of 0.125% to 0.375% compared to direct bank applications.

Property Type and Location Considerations

Not all properties qualify equally for jumbo financing. Lenders maintain specific requirements regarding property characteristics, condition, and marketability.

Eligible Property Categories

Single-family residences receive the most favorable treatment in jumbo underwriting. Condominiums require additional review of homeowners association finances, reserve funding, and project approval status. Multi-unit properties up to four units remain eligible but face heightened scrutiny regarding rental income projections and property management experience.

Property approval factors:

- Single-family homes: Broadest approval and best rates

- Condominiums: Require project approval and warrantable status

- Townhomes: Similar treatment to single-family properties

- Multi-unit (2-4 units): Require rental income analysis

- New construction: May require completion before closing

- Rural properties: Subject to size and marketability limitations

Geographic Market Dynamics

Seattle's diverse neighborhoods present varying risk profiles to jumbo lenders. Established areas with consistent appreciation and strong sales activity provide confidence in collateral value. Emerging neighborhoods or those with limited comparable sales may require additional appraisal support or face conservative valuation approaches.

Properties in Shoreline, Lynnwood, Mill Creek, and Everett often provide more accessible entry points for jumbo financing compared to central Seattle locations, while still offering proximity to major employment centers and quality school districts. The Shoreline School District and Lake Forest Park area exemplifies this balance, attracting families seeking value without sacrificing lifestyle quality.

Specialized Programs for Tech Professionals

Seattle's concentration of technology employers creates unique opportunities for specialized jumbo financing. Understanding how lenders view stock compensation, retention bonuses, and equity packages significantly impacts buying power.

Stock Compensation Qualification

Restricted stock units, performance stock units, and stock options represent substantial income sources for many Seattle professionals. Traditional underwriting averaged this income over two years, potentially understating current earning capacity. Advanced programs recognize one-year averaging for established employees or even current vesting schedules when supported by employment tenure and consistent grant patterns.

Keith Akada's expertise in qualifying RSU income for mortgage purposes has helped hundreds of tech professionals maximize their purchasing capacity. By working with underwriters who understand technology compensation structures, borrowers often discover $100,000 to $200,000 in additional buying power compared to traditional calculation methods.

Employment Stability Considerations

Lenders evaluate employment stability alongside income levels. Technology professionals with established tenure at major employers like Amazon, Microsoft, or Google benefit from perceived stability. Recent job changes require careful documentation of industry experience and career progression to demonstrate continued earning capacity.

Contract workers and consultants face additional scrutiny, typically requiring two years of self-employment history with consistent or increasing income. However, specialized programs recognize that high-earning contractors with strong skill sets and client relationships present acceptable risk profiles when properly documented.

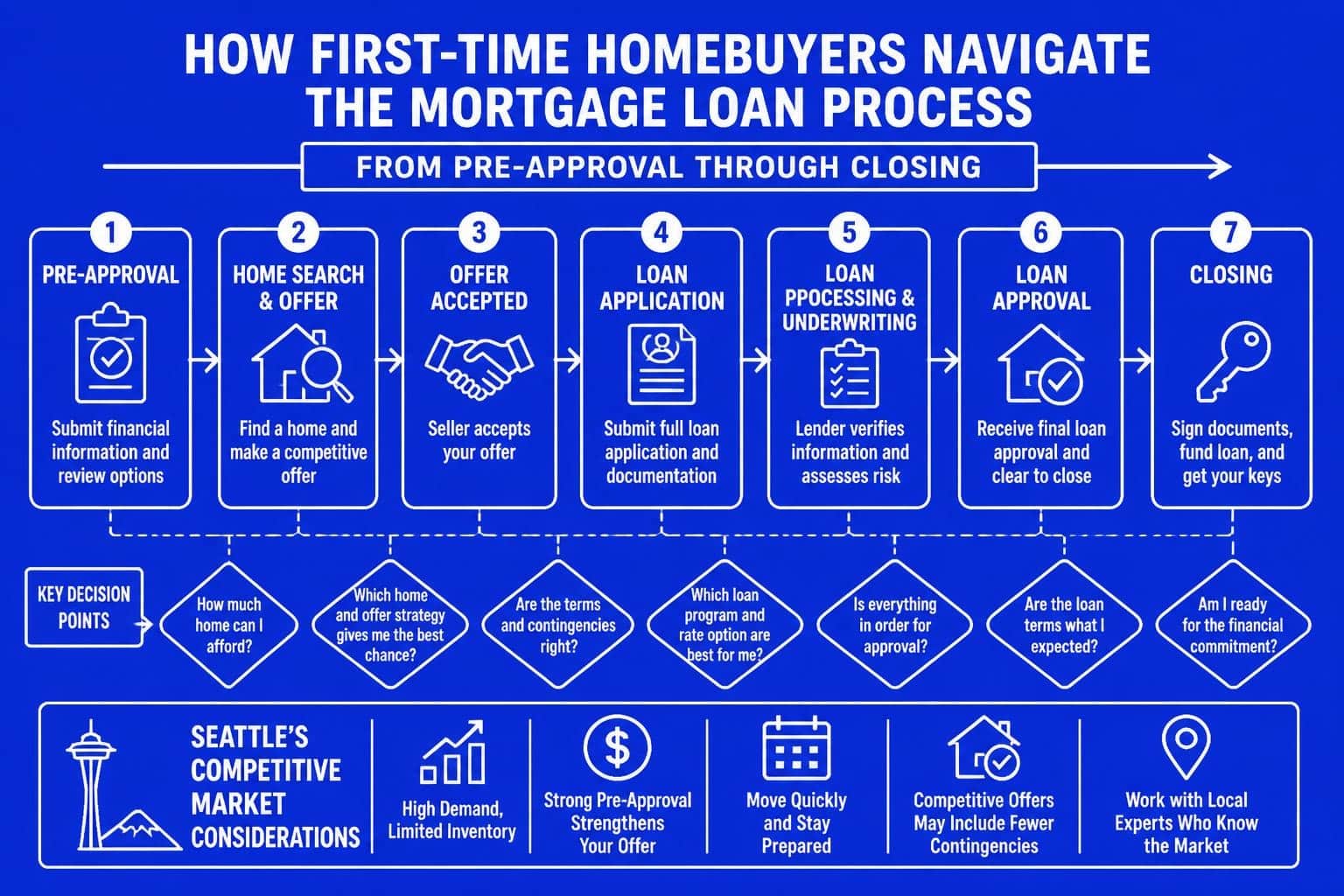

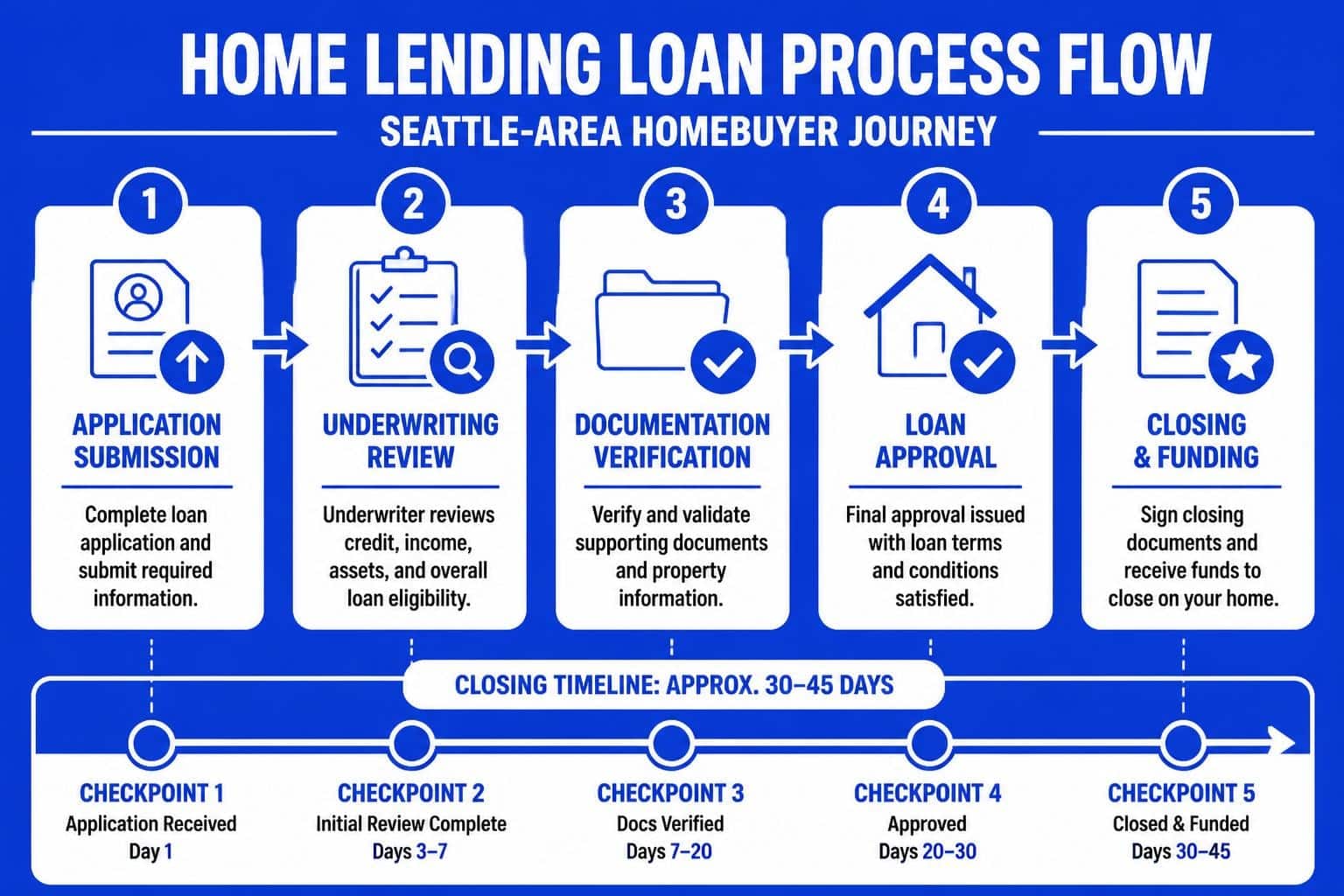

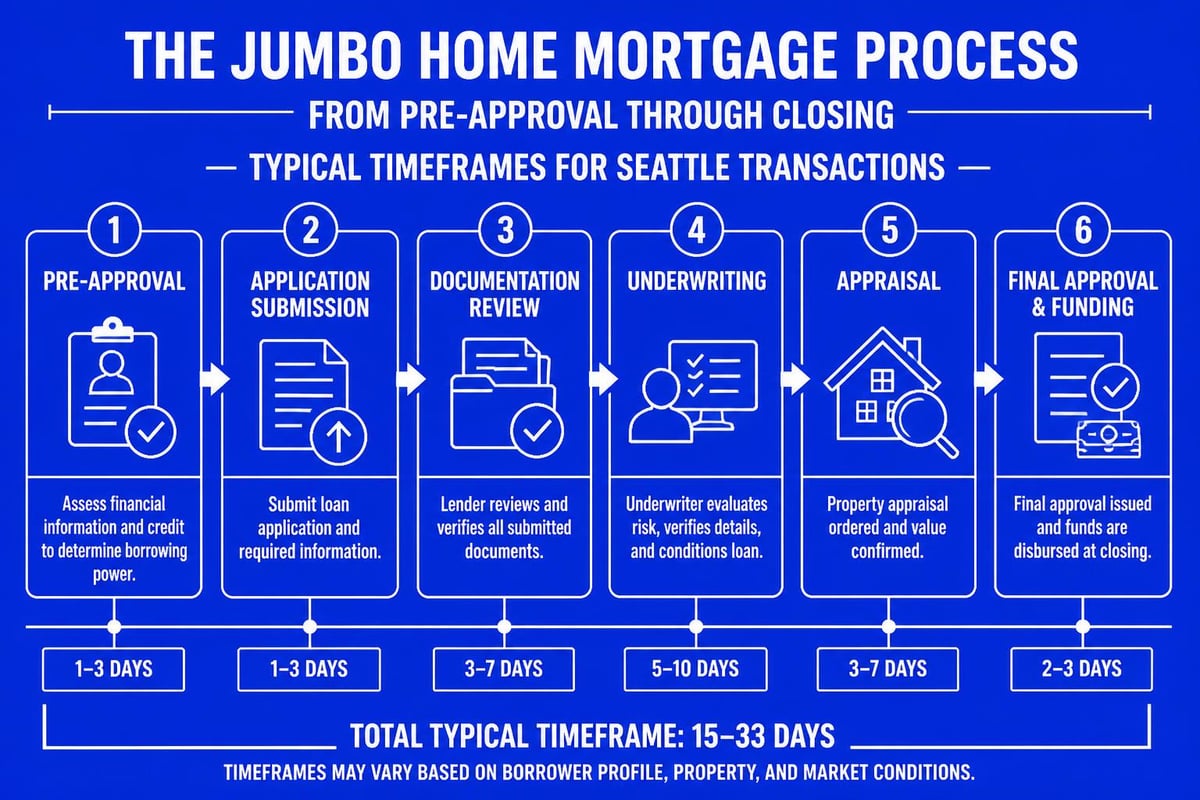

Application Timeline and Process Management

Jumbo home mortgage applications involve more extensive documentation and review than conforming loans. Understanding the timeline helps borrowers plan accordingly in competitive markets where quick closings provide negotiating advantages.

Documentation Preparation Phase

Successful jumbo applications begin with thorough document preparation. Gathering required materials before home selection accelerates subsequent steps and demonstrates seriousness to sellers in multiple-offer situations.

Complete documentation package includes:

- Federal tax returns (two years, all schedules)

- W-2 statements (two years)

- Pay stubs (most recent 30 days)

- Bank statements (all accounts, two months)

- Investment account statements (two months)

- Stock vesting schedules and grant documentation

- Employment verification authorization

- Explanation letters for any credit inquiries or unusual deposits

- Purchase agreement and property information

- Homeowners insurance quotes

Underwriting and Approval Process

Initial underwriting typically requires five to seven business days for complete file review. Underwriters issue conditional approval outlining specific requirements for final clearance. These conditions might request updated pay stubs, additional asset documentation, or property-specific information like HOA budgets or appraisal clarifications.

Fairway's advanced underwriting capabilities enable closings in as few as nine business days when borrowers provide responsive documentation and properties appraise without complications. This speed provides meaningful advantages in markets where sellers prioritize closing certainty and transaction efficiency.

Common Misconceptions About Jumbo Financing

Several myths persist regarding jumbo home mortgages, often deterring qualified borrowers from exploring available options. Understanding reality versus perception helps buyers make informed decisions.

Myth: Jumbo Loans Always Cost More

While jumbo rates historically exceeded conforming rates, competitive market dynamics have narrowed this gap significantly. Well-qualified borrowers with strong credit profiles and substantial down payments frequently secure jumbo rates within 0.125% to 0.250% of conforming rates, and sometimes achieve parity or better pricing.

Myth: Twenty Percent Down Is Always Required

Modern jumbo programs offer 10% down payment options for qualified borrowers. While lower down payments typically require mortgage insurance and result in higher rates, they preserve capital for other investment opportunities or emergency reserves. Strategic borrowers evaluate the total financial picture rather than defaulting to maximum down payment approaches.

Myth: Self-Employed Borrowers Cannot Qualify

Self-employed professionals with two years of consistent income documentation regularly qualify for jumbo financing. The key lies in proper tax planning that balances legitimate business deductions against demonstrated income for mortgage qualification purposes. Working with mortgage professionals who understand business tax returns proves essential for optimal outcomes.

Strategic Refinancing Opportunities

Existing jumbo borrowers should monitor rate environments for refinancing opportunities. Even modest rate reductions generate substantial monthly savings on large loan balances.

When Refinancing Makes Sense

A general guideline suggests refinancing when rates drop 0.50% or more below current mortgage rates, though this threshold varies based on loan balance, remaining term, and closing cost structures. For a $1,500,000 mortgage, a 0.50% rate reduction saves approximately $625 monthly or $7,500 annually.

Beyond rate reduction, refinancing enables term optimization, cash-out for investment opportunities, or elimination of mortgage insurance when equity positions improve. Understanding mortgage financing strategies helps homeowners maximize long-term value.

Mortgage Recast Alternatives

Borrowers receiving windfalls from stock vesting, bonuses, or inheritance might consider mortgage recast options as alternatives to refinancing. Recasting applies lump-sum principal payments to reduce monthly obligations while maintaining existing interest rates and terms. This strategy avoids refinancing costs while achieving payment relief, particularly valuable when current rates exceed existing mortgage rates.

Working With Specialized Jumbo Lenders

Not all mortgage lenders offer competitive jumbo programs. Many retail banks maintain jumbo products but lack specialized underwriting expertise or competitive pricing. Understanding the difference between mortgage brokers and banks reveals advantages in program access and rate competition.

Benefits of Broker Relationships

Mortgage brokers maintain relationships with multiple wholesale lenders, each offering distinct jumbo programs with varying guidelines and pricing. This access creates competitive dynamics that benefit borrowers through better rates and more flexible underwriting approaches.

Additionally, experienced brokers understand which lenders excel at specific borrower profiles. Tech professionals with substantial stock compensation receive optimal treatment from lenders familiar with these income structures, while self-employed borrowers benefit from specialists in business income analysis.

Local Market Expertise

Choosing a local lender in Seattle provides market knowledge that national institutions cannot replicate. Understanding neighborhood dynamics, appraisal challenges, and competitive offer structures proves invaluable during home searches and negotiations.

Keith Akada's 25-plus years serving Seattle, Bellevue, Redmond, and Kirkland creates institutional knowledge regarding property values, school districts, development trends, and neighborhood trajectories. This expertise helps clients make informed decisions beyond pure financing mechanics.

Advanced Strategies for Maximum Buying Power

Sophisticated borrowers optimize multiple variables simultaneously to maximize jumbo financing capacity while maintaining financial flexibility.

Debt Optimization Timing

Strategic debt reduction before mortgage application improves debt-to-income ratios and potentially increases qualifying capacity. However, maintaining strong cash reserves sometimes outweighs modest DTI improvements. The optimal approach depends on individual circumstances, existing debt interest rates, and overall financial goals.

Paying off automobile loans or student debt immediately before application eliminates these obligations from DTI calculations. Conversely, installment debts with fewer than ten remaining payments may be excluded from calculations without payoff, preserving liquidity.

Asset Positioning Strategies

Lenders require two months of asset statements showing funds for down payment, closing costs, and reserves. Large deposits during this period trigger documentation requirements and potential delays. Strategic borrowers consolidate assets into verification accounts well before application, avoiding last-minute transfers that complicate underwriting.

For those receiving stock compensation, timing vesting events relative to home purchase creates advantages. Vested shares documented through brokerage statements provide immediate reserve credit, while unvested grants may receive partial consideration based on lender guidelines and vesting schedules.

Rate Lock Strategies

Interest rate locks protect borrowers from market fluctuations during the application and closing process. Standard locks extend 30 to 45 days, with longer periods available at incrementally higher costs. In volatile rate environments, extended locks provide peace of mind despite modest expense.

Float-down provisions allow borrowers to capture rate improvements if markets decline after initial lock. These options carry fees but provide valuable protection in uncertain economic conditions. Discussing rate lock strategies with experienced loan officers helps borrowers navigate these decisions based on current market dynamics and personal risk tolerance.

Understanding jumbo home mortgage financing opens doors to Seattle's most desirable properties while ensuring smart financial decisions aligned with long-term goals. Whether you're a tech professional leveraging stock compensation or an established buyer seeking optimal financing terms, working with specialized expertise makes the difference between adequate and exceptional outcomes. Keith Akada and the team at Mortgage Reel bring 25-plus years of experience, 750-plus five-star reviews, and deep Seattle market knowledge to every jumbo financing transaction, with the capability to close in as few as nine business days. Connect with Mortgage Reel to explore your jumbo financing options with a trusted local expert who prioritizes education, transparency, and results.