Securing a home lending loan in Seattle's competitive market requires strategic planning, thorough documentation, and expert guidance. Whether you're a first-time buyer in Lake Forest Park or a tech professional upgrading to a larger home in Bellevue, understanding the fundamentals of residential mortgage financing empowers you to make confident decisions. The landscape of home lending has evolved significantly, with advanced underwriting techniques now accommodating diverse income types including restricted stock units (RSUs), bonuses, and equity compensation common among Seattle-area employers like Amazon, Microsoft, and Google.

Understanding Home Lending Loan Fundamentals

A home lending loan represents a secured financial agreement where a lender provides capital to purchase or refinance residential property, with the property itself serving as collateral. The borrower repays the principal amount plus interest over a predetermined term, typically 15 or 30 years. This foundational structure supports homeownership across all price ranges, from starter condos in Mill Creek to multimillion-dollar estates in Medina.

The regulatory framework governing mortgage lending ensures transparency and consumer protection throughout the transaction. These regulations mandate clear disclosure of loan terms, fees, and repayment obligations before closing.

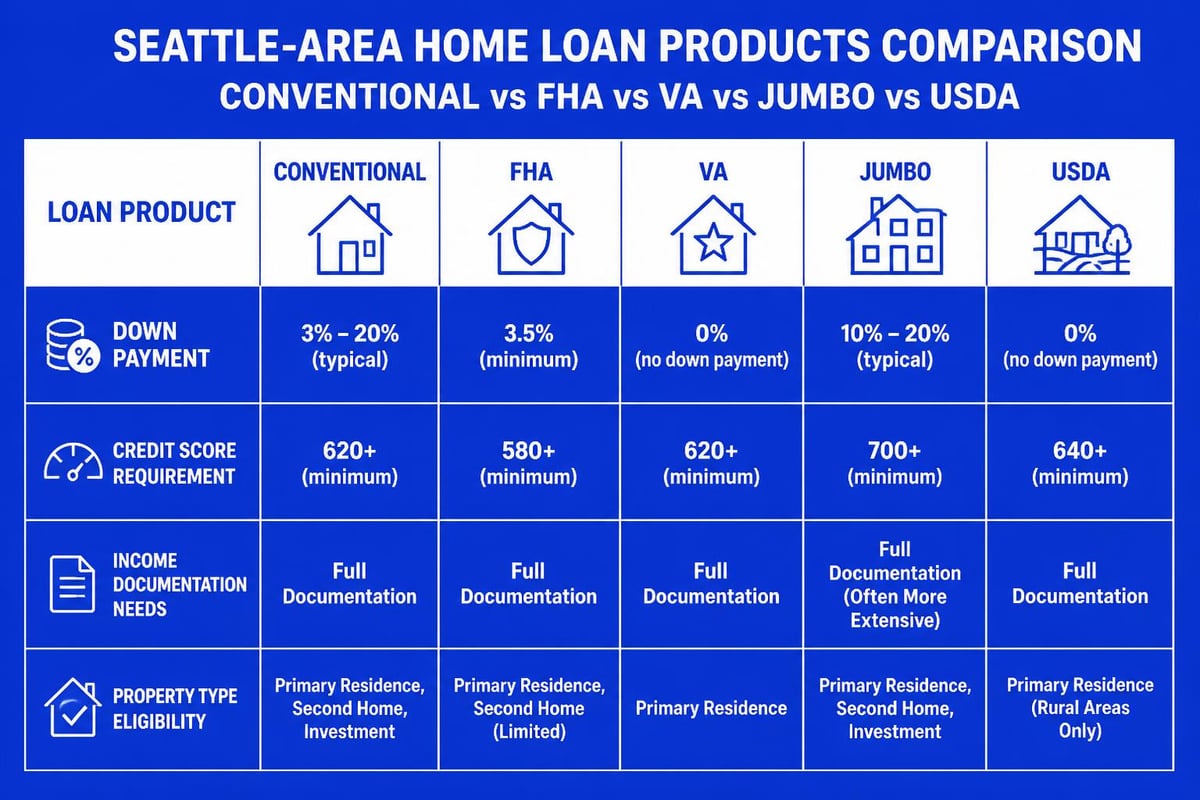

Types of Home Lending Loan Products

Different borrowers require different financing solutions. Here are the primary categories:

- Conventional loans: Not insured by government agencies, offering competitive rates for borrowers with strong credit profiles

- FHA loans: Government-backed options with lower down payment requirements, ideal for first-time buyers

- VA loans: Zero down payment programs for eligible veterans and active military members

- Jumbo loans: For purchase amounts exceeding conforming loan limits, common in high-cost Seattle markets

- USDA loans: Rural development financing available in qualifying areas outside metro Seattle

Each product type carries distinct qualification criteria, down payment requirements, and interest rate structures. Understanding which home lending loan aligns with your financial profile determines your purchasing power and long-term payment obligations.

Qualification Requirements for Home Lending Loans

Lenders evaluate multiple financial factors when determining eligibility and loan terms. Your qualification strength directly impacts interest rates, required down payments, and approval likelihood in competitive offer situations.

Credit Score Considerations

Credit scores significantly influence your home lending loan terms. Most conventional products require minimum scores of 620, though stronger profiles (740+) unlock preferential pricing. FHA loan programs accept scores as low as 580 with adequate compensating factors.

Tech professionals in Seattle often maintain excellent credit due to stable employment and financial discipline. However, recent credit inquiries from equity compensation programs or temporary utilization spikes can temporarily impact scores. Working with an experienced mortgage broker helps time applications strategically to maximize score impact.

Debt-to-Income Ratio Standards

Your debt-to-income (DTI) ratio compares monthly debt obligations to gross monthly income. Conventional loans typically cap total DTI at 43-50%, though compensating factors like substantial reserves or high credit scores may allow flexibility.

Income included in DTI calculations:

- Base salary or hourly wages

- Documented commission income (typically two-year average)

- Bonus income with consistent payment history

- RSU and stock compensation (with proper documentation)

- Rental income from investment properties

- Self-employment earnings (after business expenses)

For Seattle tech employees, properly documenting variable compensation maximizes qualification capacity. Understanding how RSU income affects mortgage qualification proves essential for professionals at major employers.

Employment and Income Verification

Stable employment history demonstrates repayment capacity. Most programs require two years of consistent income in the same field, though exceptions exist for recent graduates with strong job offers or professionals transitioning within related industries.

| Income Type | Documentation Required | Typical Lookback Period |

|---|---|---|

| W-2 Salary | Pay stubs, W-2s, employment verification | 30 days current + 2 years history |

| Self-Employment | Tax returns, profit/loss statements, CPA letter | 2 years (sometimes 1 year) |

| RSU/Stock Comp | Vesting schedules, award letters, recent deposit history | 2 years with continuity evidence |

| Bonus Income | W-2s showing consistent payments, employer letter | 2 years average |

The OCC’s guidance on mortgage processes outlines standard verification procedures lenders follow to ensure income stability.

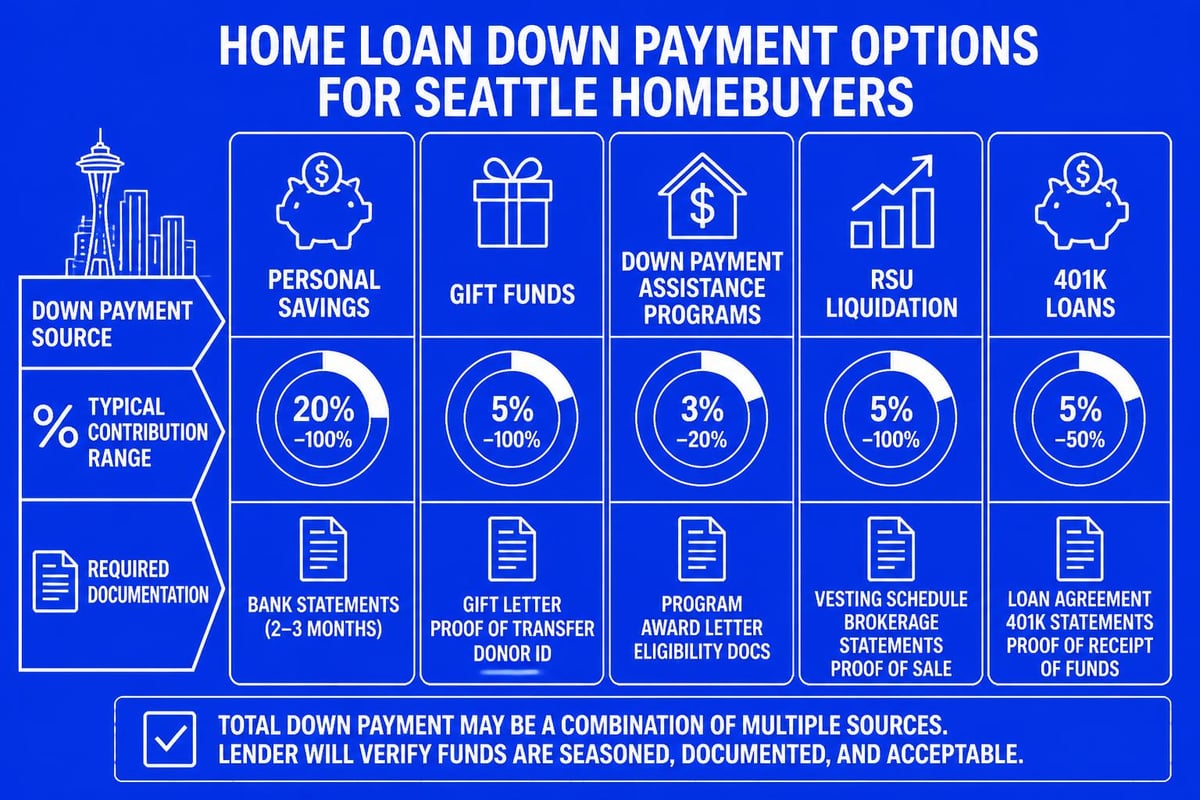

Down Payment Strategies for Seattle Markets

Down payment requirements vary by loan type and property cost. Strategic planning around this crucial component affects both immediate cash needs and long-term loan costs.

Minimum Down Payment by Product

Different home lending loan products require varying down payments:

- Conventional: 3% for first-time buyers, 5% for repeat buyers (standard programs)

- FHA: 3.5% with credit scores 580+

- VA: 0% for eligible veterans

- Jumbo: 10-20% depending on loan amount and compensating factors

For jumbo home loans in Washington State, larger down payments often secure better interest rates and avoid mortgage insurance. Tech professionals frequently leverage RSU vesting events or annual bonuses to reach 20% thresholds, eliminating private mortgage insurance (PMI) costs entirely.

Gift Funds and Down Payment Assistance

Many Seattle buyers utilize gift funds from family members to supplement savings. Conventional and government-backed programs allow gifted down payments with proper documentation including gift letters and transfer verification.

First-time buyer programs in Lake Forest Park and surrounding communities offer additional down payment assistance through state and local initiatives. These programs combine with traditional home lending loan products to reduce upfront cash requirements significantly.

Interest Rates and Loan Costs

The interest rate on your home lending loan represents the largest long-term cost component. Small rate differences create substantial payment variations over 30-year terms.

Rate Determinants

Multiple factors influence the rate lenders offer:

- Credit score strength

- Loan-to-value ratio (down payment size)

- Property type (single-family, condo, investment)

- Occupancy status (primary residence, second home, rental)

- Loan amount (conforming vs. jumbo)

- Market conditions and Federal Reserve policy

In 2026, understanding mortgage broker vs. bank differences helps Seattle borrowers access competitive pricing. Brokers often present multiple investor options, potentially securing better rates than single-lender institutions.

Points and Rate Buydowns

Borrowers can pay discount points at closing to reduce interest rates permanently. Each point costs 1% of the loan amount and typically reduces rates by 0.125-0.25%. This strategy benefits buyers planning long-term homeownership in Shoreline, Lynnwood, or other Seattle-area communities.

Alternatively, seller-paid or lender credits can offset closing costs without additional cash outlay, though typically at slightly higher interest rates. Strategic negotiation around these trade-offs optimizes total financing costs.

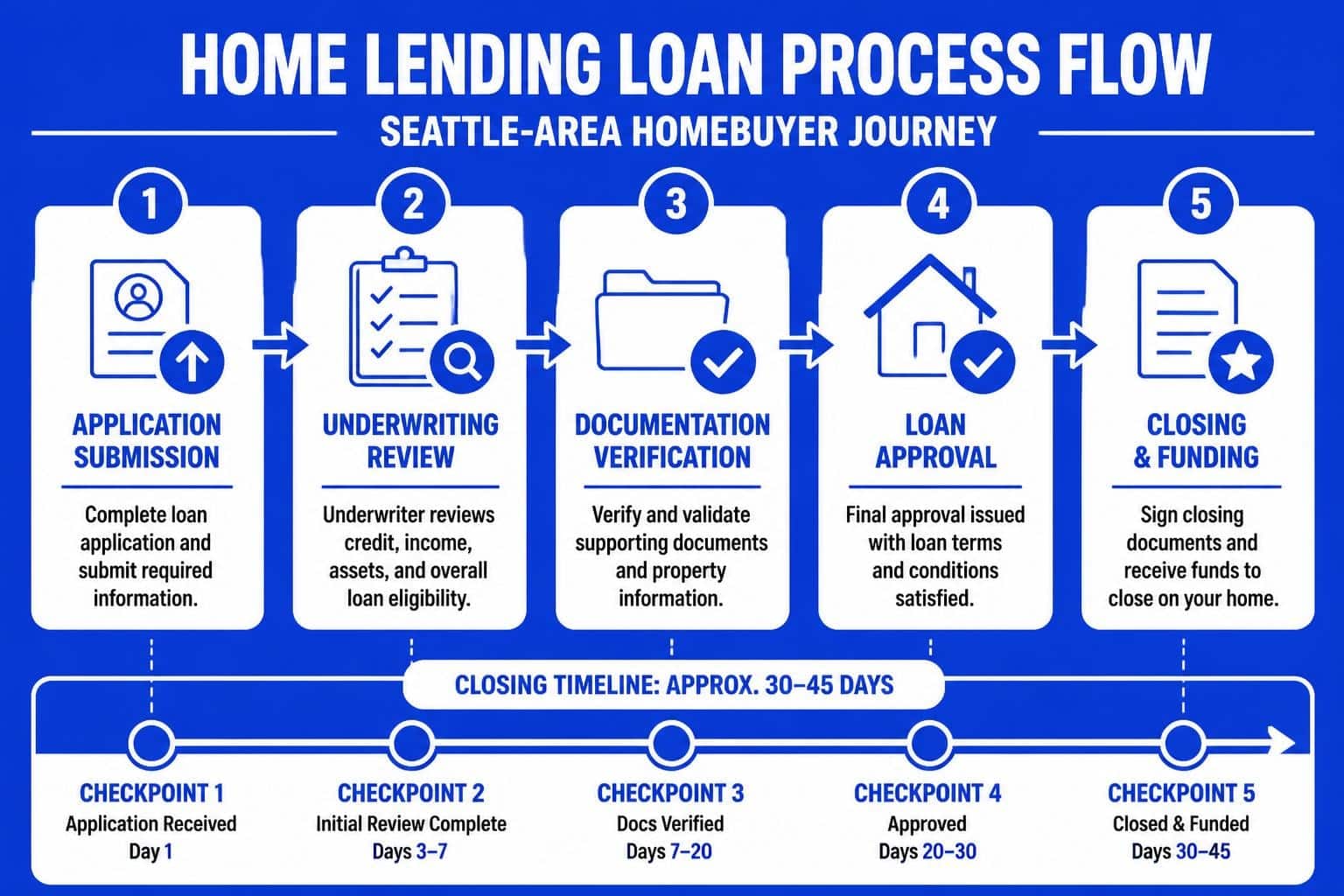

The Home Lending Loan Application Process

Understanding timeline expectations and documentation requirements streamlines the journey from application to closing. Advanced preparation accelerates approval and strengthens competitive positioning in multiple-offer scenarios.

Pre-Approval vs. Pre-Qualification

Pre-qualification provides an estimate based on stated information without verification. Pre-approval involves credit checks, income documentation review, and conditional commitment from underwriting. In Seattle's competitive markets, serious sellers and listing agents require full pre-approval before considering offers.

Pre-approval documentation checklist:

- Most recent pay stubs (30 days)

- W-2 forms (2 years)

- Tax returns (2 years, if self-employed or documenting variable income)

- Bank statements (2 months, all pages)

- Retirement account statements (if using for reserves)

- RSU vesting schedules and award letters

- Current mortgage statement (if refinancing)

Gathering these documents before starting the home search accelerates timelines significantly. How long it takes to get a mortgage in Seattle depends partly on documentation readiness.

Underwriting and Conditional Approval

Once under contract, your complete file proceeds to underwriting for comprehensive review. Underwriters verify all documentation, run automated underwriting systems, and assess risk factors. They issue conditional approval with outstanding requirements like updated pay stubs, explanation letters for credit inquiries, or additional reserves documentation.

Fast response to conditions prevents closing delays. Experienced loan officers anticipate likely conditions and prepare documentation proactively, minimizing back-and-forth cycles.

Appraisal and Title Work

The lender orders an independent appraisal to confirm property value supports the loan amount. Simultaneously, title companies research ownership history and identify any liens or encumbrances requiring resolution before closing.

Appraisal challenges occasionally arise in rapidly appreciating neighborhoods throughout Everett, Mill Creek, and Seattle proper. Having comparable sales data and renovation documentation ready helps appraisers justify valuations in competitive situations.

Special Considerations for Seattle Tech Professionals

Seattle's concentration of technology employers creates unique mortgage scenarios. Properly documenting compensation structures maximizes qualification potential and purchasing power.

Qualifying RSU and Stock Compensation

Restricted stock units require specific treatment in mortgage underwriting. Lenders typically average two years of RSU income after subtracting taxes. Providing comprehensive documentation including:

- Vesting schedules showing future grants

- Tax withholding statements proving net proceeds

- Deposit history demonstrating actual receipt

- Employer letters confirming ongoing program participation

This documentation transforms RSUs from uncertain variable income into reliable qualifying income for your home lending loan. Many Seattle buyers discover they qualify for significantly more than anticipated when properly documenting equity compensation.

Jumbo Loan Expertise

Seattle's median home prices frequently exceed conforming loan limits, requiring jumbo financing. Understanding what qualifies as a jumbo loan helps buyers prepare for stricter requirements including larger reserves, lower DTI thresholds, and comprehensive income documentation.

However, competitive jumbo programs now offer 10% down payment options for well-qualified borrowers with strong compensating factors. Tech professionals with substantial RSU holdings and excellent credit profiles often access these programs despite lower down payments.

Refinancing Your Existing Home Lending Loan

Market conditions and personal circumstances change over time. Refinancing replaces your existing home lending loan with new terms, potentially reducing payments, shortening loan duration, or accessing equity for other financial goals.

Rate-and-Term Refinancing

This straightforward refinance replaces your current loan with better terms without extracting equity. Benefits include:

- Lower interest rates reducing monthly payments

- Shorter loan terms building equity faster

- Eliminating mortgage insurance when reaching 20% equity

- Converting adjustable rates to fixed rates for payment stability

With federal regulations governing refinancing, borrowers receive clear disclosure of costs and benefits before proceeding.

Cash-Out Refinancing

Cash-out refinancing accesses home equity while refinancing. Seattle homeowners frequently use proceeds for:

- Home renovations increasing property value

- Debt consolidation at lower interest rates

- Investment property down payments

- Education expenses or business investments

Understanding the trade-offs between accessing equity and maintaining lower loan balances requires careful analysis of long-term financial goals.

Mortgage Recast Alternative

For borrowers with lump-sum cash available but satisfied with current rates, mortgage recasting offers an alternative. This process applies a large principal payment and re-amortizes remaining balance over the original term, reducing monthly payments without refinancing costs or rate changes.

Fair Lending and Consumer Protections

Robust regulatory frameworks protect consumers throughout the home lending loan process. Understanding these protections ensures fair treatment and transparent dealings.

Equal Credit Opportunity Act

The FDIC’s fair lending resources outline protections preventing discrimination based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance. Lenders must evaluate applications based solely on creditworthiness and repayment capacity.

Truth in Lending Act Disclosures

TILA requires lenders provide clear, standardized disclosures including:

| Disclosure Document | Timing | Purpose |

|---|---|---|

| Loan Estimate | Within 3 business days of application | Itemizes estimated costs, rates, and terms |

| Closing Disclosure | At least 3 business days before closing | Final confirmed costs and loan terms |

| Annual Percentage Rate (APR) | Throughout process | True cost of credit including fees |

These protections ensure borrowers understand total costs and can comparison shop effectively across lenders.

Working with Mortgage Professionals in Seattle

Navigating home lending loan options, documentation requirements, and market conditions benefits significantly from expert guidance. The choice between direct lenders and mortgage brokers impacts product access and personalized service.

Benefits of Local Mortgage Expertise

Local mortgage professionals understand regional market dynamics, property value trends, and community-specific programs unavailable through national platforms. For buyers exploring home loans in Lake Forest Park or other Seattle neighborhoods, this localized knowledge proves invaluable.

Additionally, established relationships with local appraisers, title companies, and real estate professionals expedite transactions and resolve challenges quickly. In competitive markets where timing determines success, these connections matter significantly.

Advanced Underwriting Capabilities

Working with lenders offering sophisticated underwriting platforms enables faster closings without sacrificing thoroughness. Some mortgage companies now close conventional and government-backed loans in as few as 9 business days when documentation is complete and property factors align favorably.

This speed advantage helps Seattle buyers compete effectively in multiple-offer situations, demonstrating seriousness and execution capability to sellers and listing agents.

Preparing for Current Market Conditions

Seattle's housing market in 2026 continues evolving with interest rate fluctuations, inventory constraints, and shifting buyer demographics. Strategic preparation positions you for success regardless of immediate market conditions.

Building Strong Financial Profiles

Months before home shopping, focus on:

- Maintaining low credit utilization (under 30% of limits)

- Avoiding new credit inquiries or major purchases

- Documenting income sources comprehensively

- Accumulating reserves beyond down payment and closing costs

- Addressing credit report inaccuracies proactively

These preparations maximize approval odds and secure optimal home lending loan terms when you identify the right property.

Market Timing Considerations

While "timing the market" perfectly proves impossible, understanding seasonal patterns helps. Seattle typically sees increased inventory in spring and summer with corresponding competition. Fall and winter often present less competition though reduced selection.

Interest rate movements respond to broader economic factors including Federal Reserve policy, inflation trends, and employment data. Monitoring these indicators helps identify favorable financing windows, though purchasing decisions should prioritize personal readiness over market timing speculation.

Securing the right home lending loan requires understanding product options, qualification requirements, and strategic documentation approaches tailored to your financial profile. Whether you're purchasing your first home in Shoreline, upgrading to accommodate a growing family in Lynnwood, or investing in Seattle real estate, expert guidance ensures confident decisions and optimal loan terms. Keith Akada at Mortgage Reel brings 25+ years of experience helping Seattle-area buyers navigate complex mortgage scenarios, particularly for tech professionals with RSU and equity compensation. With 750+ five-star reviews and the ability to close loans in as few as 9 business days, Mortgage Reel combines personalized service with advanced underwriting capabilities to turn homeownership goals into reality.