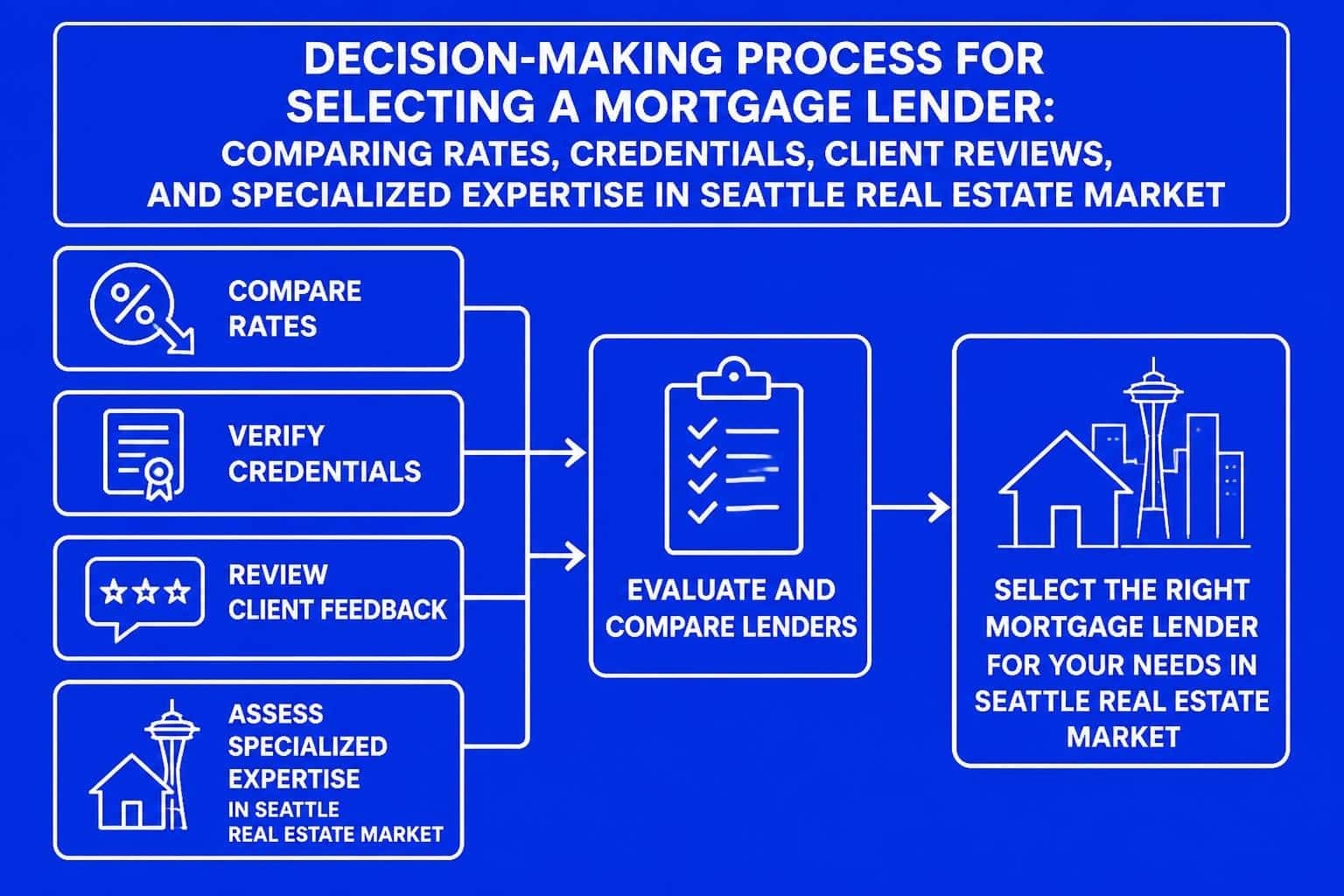

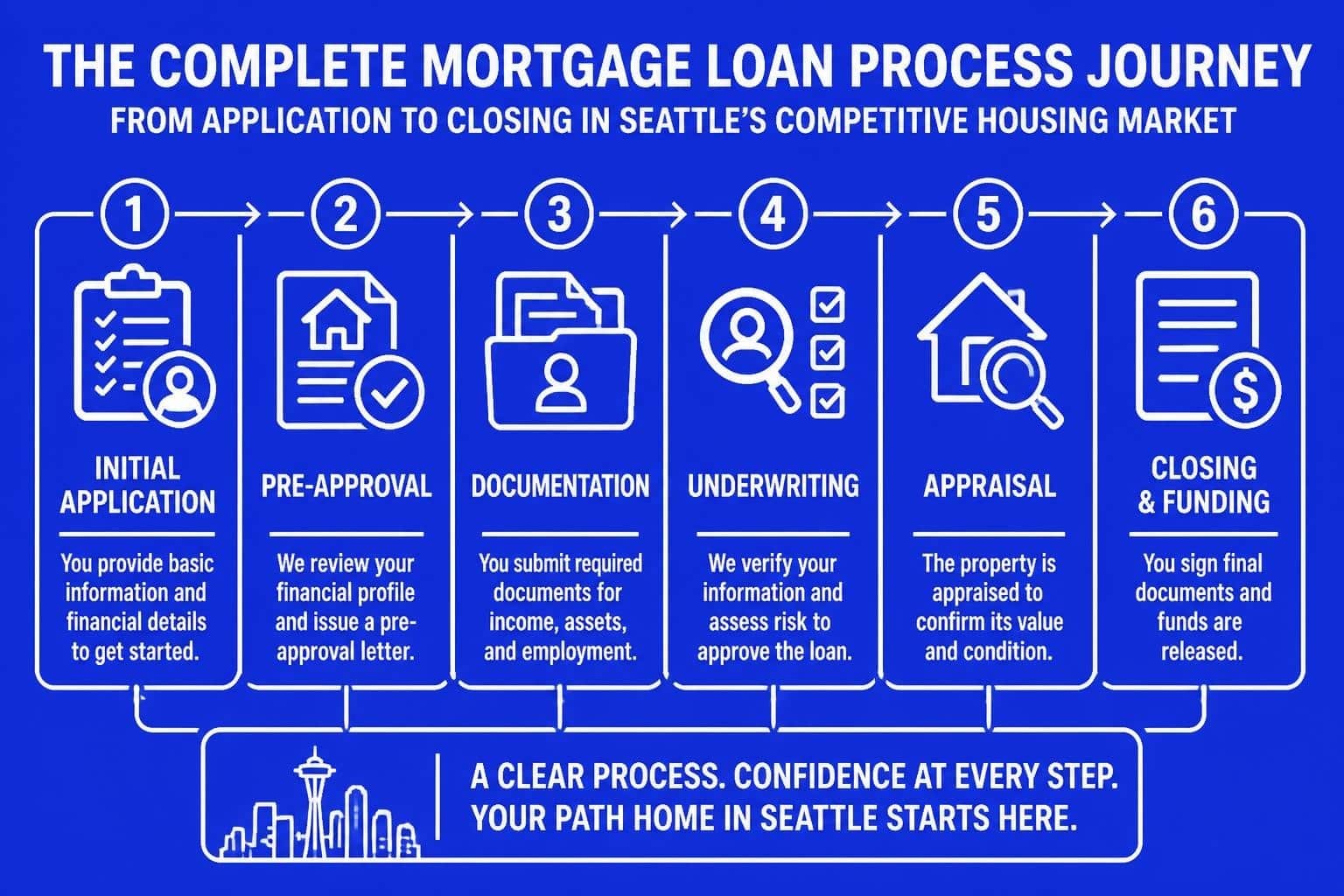

Understanding the home mortgage loan process can feel overwhelming, especially in competitive markets like Seattle, Bellevue, and Redmond where tech professionals and first-time buyers navigate complex financing scenarios. Whether you're purchasing your first home in Lake Forest Park or refinancing a jumbo loan in Kirkland, knowing what to expect at each stage helps you move confidently through one of the biggest financial decisions you'll make. This comprehensive guide breaks down the entire process, from initial pre-approval to closing day, with insights specifically tailored for Seattle-area homebuyers.

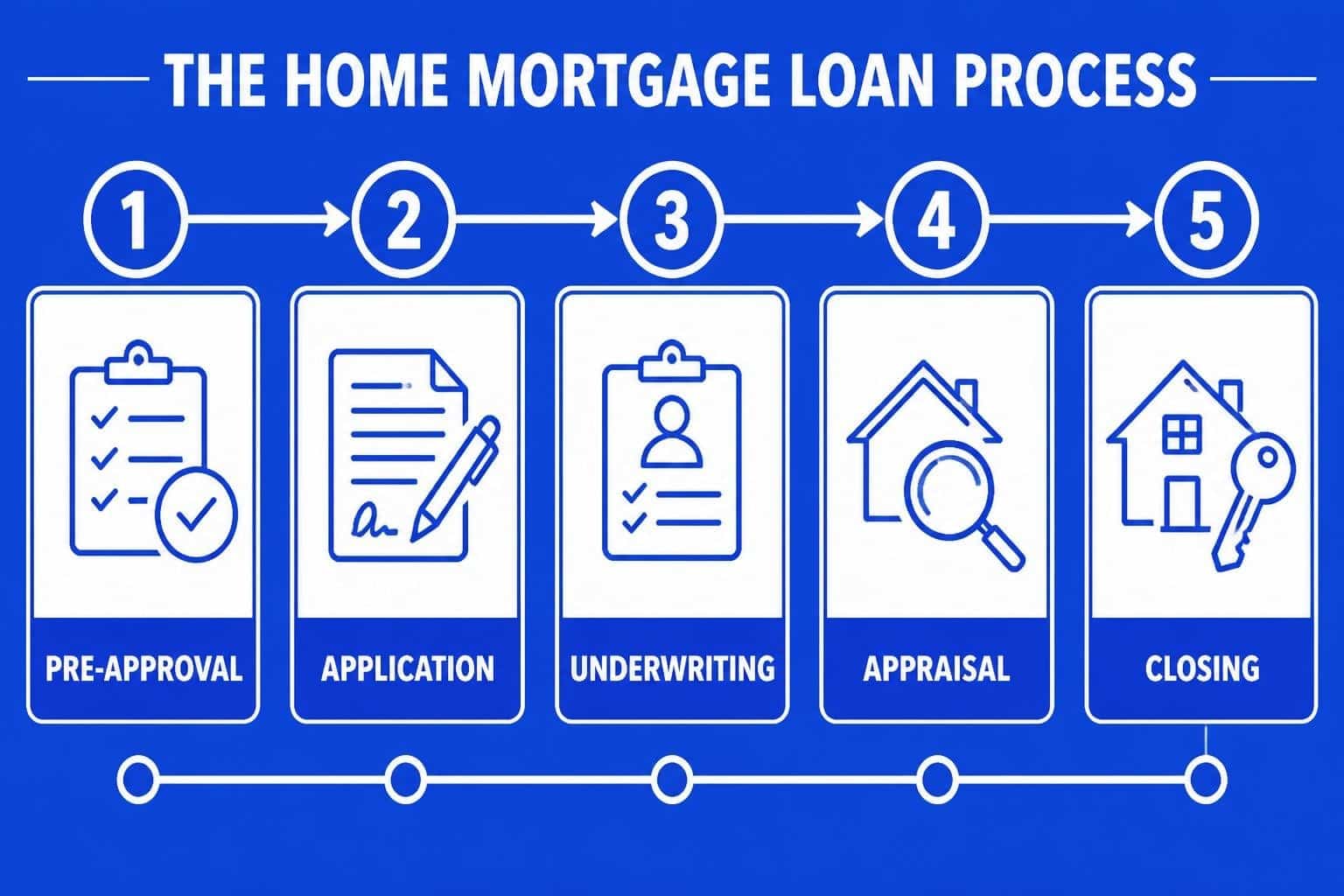

Pre-Approval: Your First Step in the Home Mortgage Loan Process

Pre-approval establishes your buying power before you start house hunting. This crucial first step in the mortgage loan process involves submitting financial documentation to a lender who evaluates your creditworthiness, income stability, and debt-to-income ratio.

For tech professionals working at Amazon, Microsoft, or Google, pre-approval requires specialized attention to stock compensation. Restricted Stock Units (RSUs), bonuses, and equity grants can significantly increase your purchasing power when properly documented and qualified. A skilled Seattle mortgage broker knows how to structure these income sources to maximize your loan amount, particularly for jumbo home loans common in Seattle's higher-priced neighborhoods.

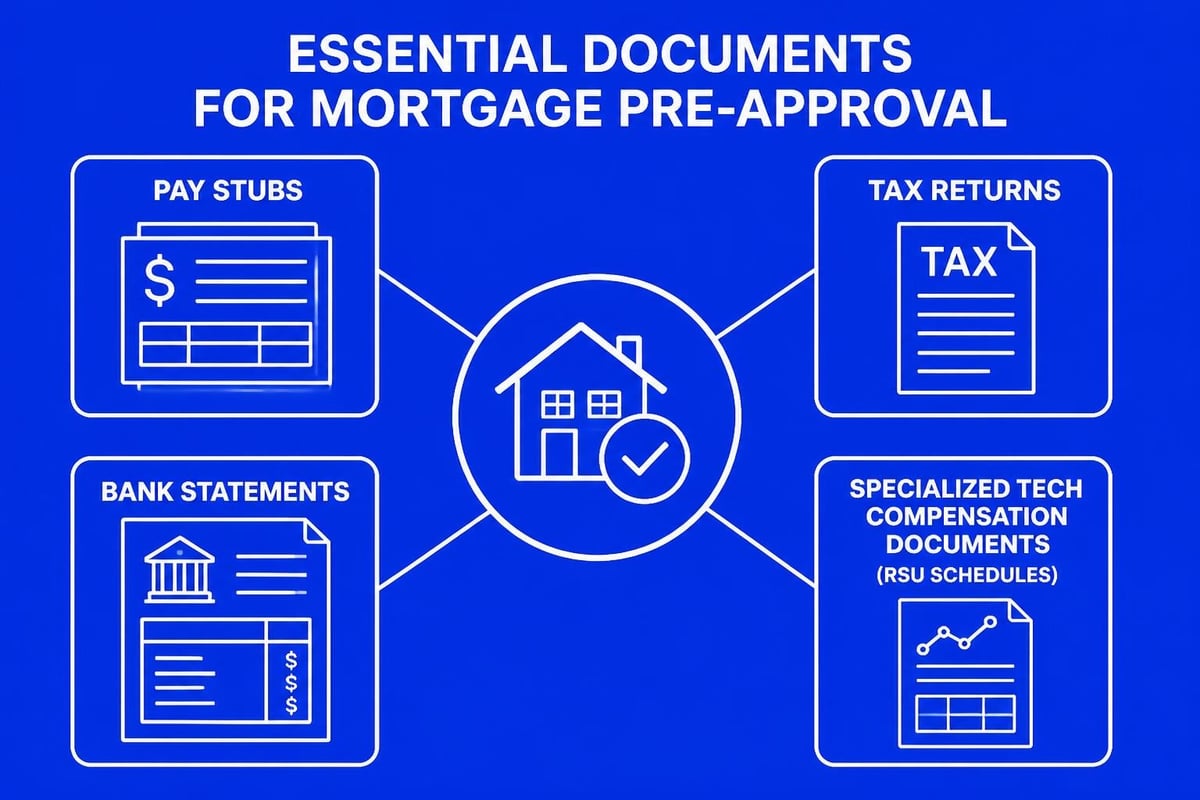

Required Documentation for Pre-Approval

Gathering the right documents upfront accelerates the home mortgage loan process considerably:

- Pay stubs covering the most recent 30 days

- W-2 forms from the past two years

- Tax returns (complete with all schedules) for two years

- Bank statements showing two months of account activity

- Investment account statements for additional assets

- RSU vesting schedules and stock compensation details (for tech employees)

Self-employed buyers or real estate investors in Shoreline or Lynnwood face additional requirements, including profit and loss statements, business tax returns, and balance sheets. The documentation threshold remains higher, but experienced professionals understand how to present self-employment income favorably.

Finding Your Home and Making an Offer

Once pre-approved, you can confidently shop for homes within your budget range. In Seattle's competitive market, having a solid pre-approval letter from a reputable lender makes your offer significantly stronger. Sellers and their agents recognize the difference between a generic online pre-qualification and a thorough pre-approval backed by verified documentation.

Working with a local lender who understands neighborhoods from Mill Creek to Everett provides strategic advantages. They know typical appraisal values, common inspection issues, and realistic closing timelines for different property types. This local expertise becomes invaluable when structuring offers with appropriate contingencies and earnest money deposits.

Loan Application: Formalizing Your Intent

After your offer is accepted, the formal loan application begins. This stage of the home mortgage loan process involves completing a comprehensive Uniform Residential Loan Application (Form 1003) that captures detailed information about the property, your financial situation, and the loan terms you're seeking.

The mortgage application process triggers several important disclosures and timelines. Within three business days, you'll receive:

| Disclosure Document | Purpose | Action Required |

|---|---|---|

| Loan Estimate | Outlines loan terms, projected payments, and closing costs | Review carefully and compare with pre-approval discussion |

| Home Loan Toolkit | Educational guide about the mortgage process | Read to understand your rights and responsibilities |

| Servicing Disclosure | Explains if your loan might be sold or serviced by another company | Awareness only, no action needed |

Understanding these documents helps you identify any discrepancies between what you expected and what's being offered. For first-time mortgage loans, this educational component proves particularly valuable.

Lock Your Interest Rate

Interest rate locks protect you from market fluctuations during the processing period. In 2026's dynamic rate environment, most buyers lock their rate for 30 to 45 days, though longer locks are available for a fee. Seattle-area tech buyers closing on new construction often need extended locks of 60 to 90 days.

Timing your rate lock requires balancing market conditions with your closing timeline. Your mortgage professional monitors rates and advises on optimal timing, particularly when Federal Reserve policy shifts or economic data releases impact mortgage rates significantly.

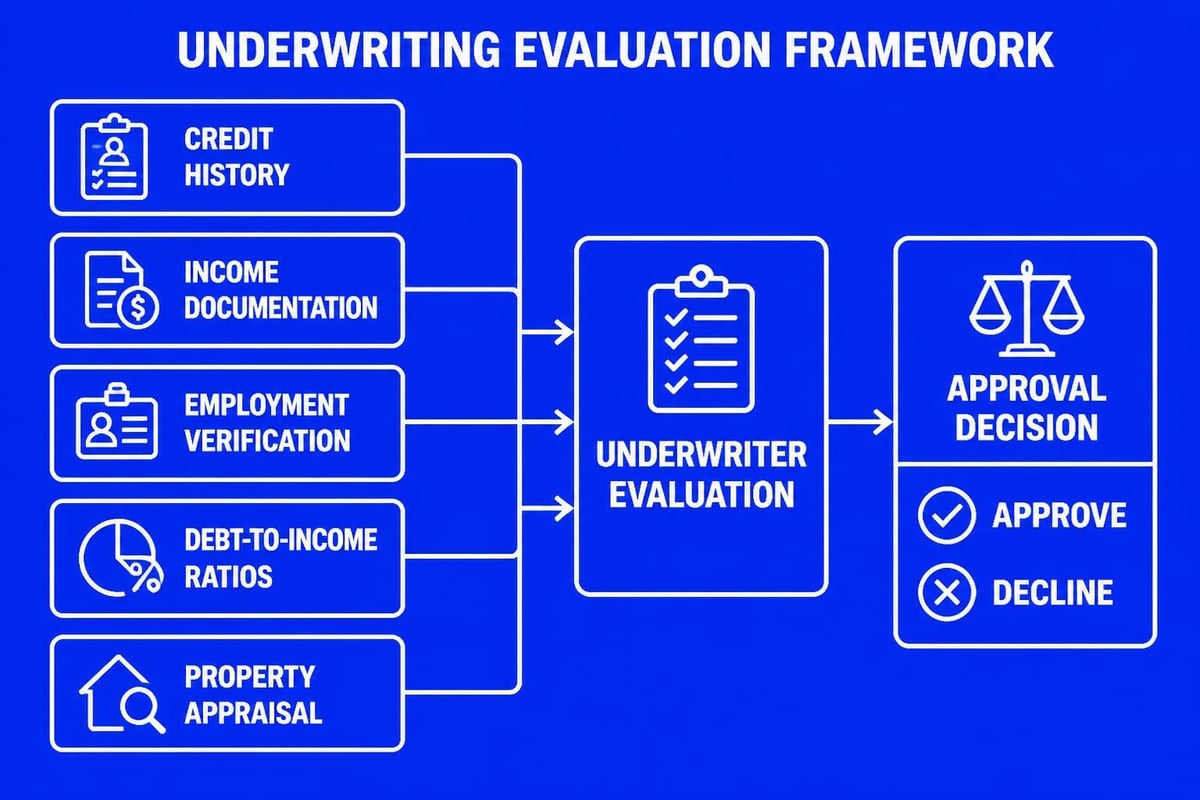

Processing and Underwriting: The Verification Phase

Processing involves collecting, verifying, and organizing all documentation required for underwriting approval. Your loan processor serves as the central coordinator, requesting additional documents, ordering third-party reports, and ensuring completeness before submission to underwriting.

Third-Party Reports and Verifications

The home mortgage loan process requires several independent verifications:

- Credit report pulled from all three bureaus (Experian, Equifax, TransUnion)

- Appraisal conducted by a licensed appraiser to confirm property value

- Title search ensuring clear ownership and no outstanding liens

- Employment verification confirming your job status and income

- Homeowners insurance quote meeting lender requirements

- HOA documentation (if applicable) showing financial health and regulations

For properties in Seattle neighborhoods like Capitol Hill or Montlake, understanding appraisal nuances becomes critical. Unique architectural features, location premiums, and comparable sales data all influence the final valuation.

The Underwriter's Role

Underwriters assess risk by evaluating your complete financial profile against lending guidelines. They verify that your income can support the mortgage payment, your credit history demonstrates responsible borrowing, and the property provides adequate collateral for the loan amount. The role of mortgage underwriters is to protect both you and the lender from unsustainable debt.

Underwriters commonly request additional documentation through conditions. These aren't denials-they're requests for clarification or supplemental information. Common conditions include:

- Letters of explanation for credit inquiries or large deposits

- Updated pay stubs if processing extends beyond 30 days

- Proof that gift funds have been deposited and seasoned

- Additional bank statements showing reserve requirements

Tech employees in Bellevue or Redmond often receive conditions related to equity compensation, requesting updated vesting schedules or explanations of stock sale timing. Responding quickly and thoroughly to these requests keeps the home mortgage loan process on schedule.

Appraisal: Establishing Property Value

The appraisal protects both you and your lender by confirming the property's market value supports the purchase price. In Seattle's appreciating market, most well-priced homes appraise at or above contract price. However, appraisal gaps occasionally occur, particularly in multiple-offer situations where emotions drive pricing.

Licensed appraisers use three approaches to value:

- Sales Comparison Approach: Analyzing recent sales of similar properties

- Cost Approach: Calculating replacement cost minus depreciation

- Income Approach: Evaluating rental income potential (for investment properties)

For single-family homes, the sales comparison approach carries the most weight. Appraisers typically use three to six comparable sales within a one-mile radius, making adjustments for differences in size, condition, amenities, and location.

Handling Appraisal Challenges

If an appraisal comes in below purchase price, you have several options:

- Renegotiate the purchase price with the seller

- Increase your down payment to cover the gap

- Challenge the appraisal with additional comparable data

- Request a second appraisal (if lender guidelines permit)

- Walk away using your appraisal contingency

Working with a knowledgeable professional who understands Lake Forest Park or Shoreline property values helps you prepare realistic expectations and develop contingency strategies before issues arise.

Clear to Close: Final Approval

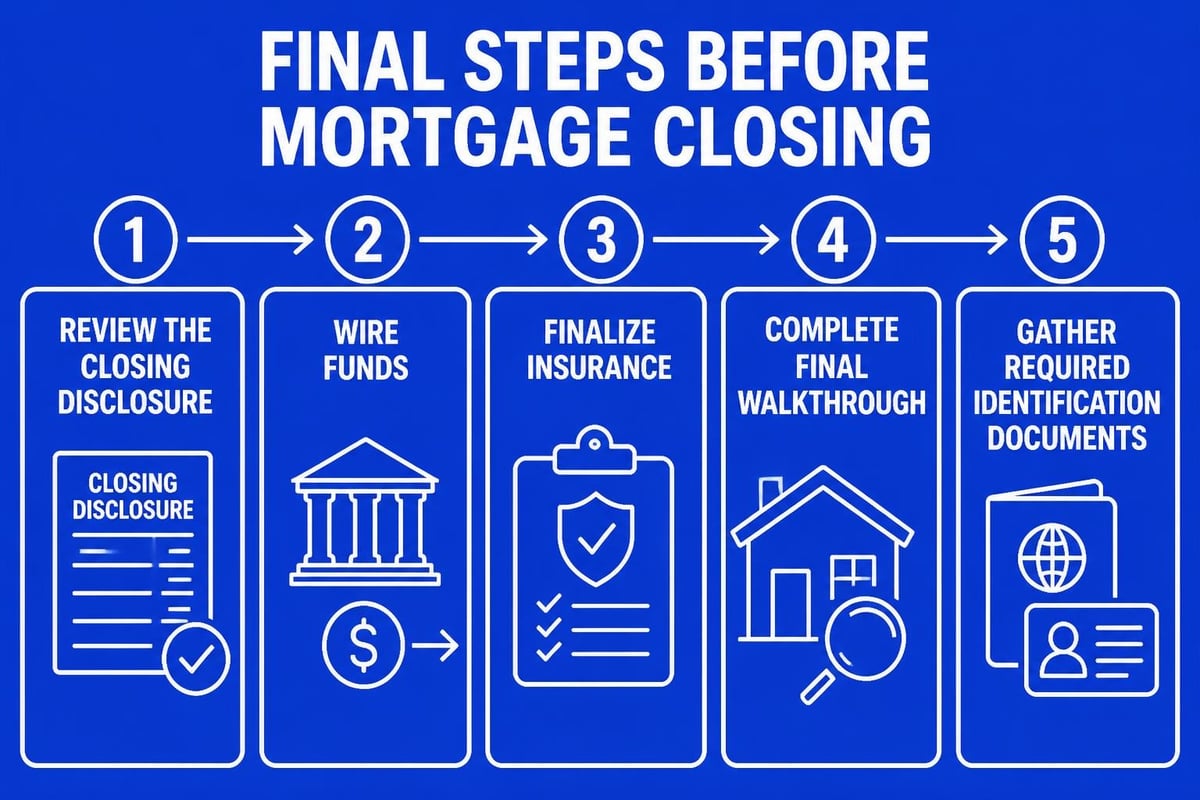

Clear to close status means underwriting has approved your loan and all conditions have been satisfied. At this stage, the home mortgage loan process shifts to closing preparation. Your lender coordinates with the title company, schedules your closing appointment, and prepares final documents.

Approximately three business days before closing, you'll receive the Closing Disclosure, which itemizes your final loan terms, monthly payments, and closing costs. Federal law requires this three-day waiting period, giving you time to review and compare the Closing Disclosure against your initial Loan Estimate.

Pre-Closing Requirements

Several critical tasks must be completed before closing day:

- Final walkthrough of the property (typically 24 hours before closing)

- Wire funds for your down payment and closing costs

- Homeowners insurance policy bound and paid for one year

- Final employment verification (often completed the morning of closing)

- Utility transfer arrangements made

Avoid making major financial changes during this period. Don't open new credit accounts, make large purchases, change jobs, or move money between accounts without discussing with your lender first. These actions can trigger new conditions or potentially derail your approval.

Closing Day: Finalizing Your Home Purchase

Closing (also called settlement) is where you sign final documents, receive keys, and officially become a homeowner. Most closings in the Seattle area occur at title company offices, though some lenders offer mobile notary services for convenience.

Plan for closing to take 60 to 90 minutes. You'll sign numerous documents, including:

| Document Type | Purpose | Key Details |

|---|---|---|

| Promissory Note | Your promise to repay the loan | Loan amount, interest rate, payment terms |

| Deed of Trust | Secures the property as collateral | Gives lender right to foreclose if you default |

| Closing Disclosure | Final cost breakdown | Must match the one received three days prior |

| Initial Escrow Statement | Details escrow account funding | Property taxes and insurance payments |

| Certificate of Occupancy | Confirms property meets code | Required for new construction |

Bring a government-issued photo ID and be prepared to answer questions about the documents you're signing. While the stack of paperwork seems daunting, your title officer or closing attorney explains each document's purpose.

Post-Closing: Your First Year as a Homeowner

The home mortgage loan process doesn't truly end at closing. Your first year involves adjusting to homeownership responsibilities, understanding your mortgage statement, and planning for future financial opportunities.

Making Your First Payment

Your first mortgage payment typically comes due 30 to 45 days after closing. For example, if you close on June 15, 2026, your first payment would be due August 1, 2026. The gap allows time for loan servicing transfer and account setup.

Most borrowers receive a servicing transfer notice within the first few months. Loan servicing rights are frequently sold between companies, which doesn't change your loan terms but does change where you send payments. Monitor these notices carefully and update any automatic payment arrangements.

Building Equity and Refinancing Opportunities

Monitor interest rate trends and your home's value appreciation. Seattle-area properties in neighborhoods like Montlake and Capitol Hill have historically appreciated well, creating refinancing opportunities sooner than you might expect. When rates drop significantly or your equity position improves, refinancing options become worth evaluating.

For tech professionals expecting income increases through promotions, stock vesting, or bonuses, staying in touch with your mortgage broker helps you strategically time refinances or consider purchasing investment properties in Mill Creek or Everett.

Special Considerations for Seattle Tech Professionals

The home mortgage loan process for Amazon, Microsoft, and Google employees involves unique considerations around stock compensation and rapid income growth. Understanding how lenders qualify equity compensation can mean the difference between a conventional conforming loan and a jumbo loan with more flexible terms.

Qualifying Stock-Based Compensation

Underwriters typically use a two-year average of RSU income, requiring vesting schedules and documentation of stock sales. For employees with increasing grants, this averaging can understate current income. Some portfolio lenders offer more aggressive income calculations, using current vesting schedules rather than historical averages.

Recent IPO employees or those receiving significant stock refreshers should work with lenders experienced in tech compensation structures. The complexity of qualifying this income means not all lenders handle it equally well, making choosing the right mortgage broker particularly important.

Understanding Different Loan Programs

The home mortgage loan process varies slightly depending on your chosen loan program. Each program has unique guidelines, documentation requirements, and processing timelines.

Conventional Loans

Conventional loans backed by Fannie Mae or Freddie Mac represent the most common financing option. They offer competitive rates, flexible terms, and options for as little as 3% down for first-time buyers. For Seattle-area properties exceeding conforming loan limits ($806,500 in 2026 for most of Washington State), jumbo home loans become necessary.

FHA Loans

FHA home loans serve buyers with lower credit scores or limited down payment funds. With minimum down payments of 3.5% and credit scores as low as 580, FHA loans provide accessible homeownership paths. However, they require both upfront and monthly mortgage insurance premiums that can increase overall costs.

VA Loans

Veterans, active-duty service members, and eligible spouses can access VA loans with zero down payment and no monthly mortgage insurance. These loans offer exceptionally competitive terms but require a Certificate of Eligibility and compliance with VA property standards.

Common Timeline Expectations

Understanding realistic timelines helps you plan appropriately throughout the home mortgage loan process. While some lenders advertise closings in as few as 9 business days, most transactions take 30 to 45 days from application to closing.

Accelerated timelines work best when you:

- Have simple employment and income documentation

- Purchase properties requiring no repairs or contingencies

- Respond immediately to all document requests

- Work with experienced local professionals

- Avoid making financial changes during processing

Extended timelines often result from:

- Self-employment income requiring extensive documentation

- New construction with delayed completion dates

- Complex title issues or HOA approval processes

- Appraisal delays or value challenges

- Multiple debt or income sources requiring verification

Avoiding Common Mistakes

Certain actions derail the home mortgage loan process even after initial approval. Understanding what to avoid protects your transaction:

Don't change jobs without discussing with your lender first. Employment gaps or job changes during processing require extensive re-verification and can delay closing significantly.

Don't make large purchases on credit. Financing furniture, vehicles, or other items increases your debt-to-income ratio and may disqualify you from the approved loan amount.

Don't move money between accounts without creating a clear paper trail. Unexplained deposits trigger money laundering concerns and require extensive documentation.

Don't ignore requests from your lender or processor. Every request serves a specific purpose, and delays in responding directly extend your closing timeline.

Don't assume approval means nothing can change. Final employment and credit verifications occur immediately before closing, and significant changes can result in last-minute denials.

Working with the Right Professionals

The complexity of the home mortgage loan process makes working with experienced professionals essential. Beyond your lender, assemble a team including:

- Real estate agent with deep local market knowledge

- Home inspector to identify property condition issues

- Real estate attorney (in some transactions)

- Insurance agent providing competitive homeowners coverage

- CPA or tax advisor for tax planning strategies

For purchases in Lynnwood, Everett, or other King County and Snohomish County locations, professionals with specific neighborhood expertise provide valuable insights about schools, development plans, and resale potential.

Market-Specific Considerations for 2026

Seattle's real estate market in 2026 reflects broader economic trends including employment growth in the tech sector, inventory constraints in desirable neighborhoods, and evolving lending guidelines. Understanding current conditions helps you navigate the home mortgage loan process more effectively.

Inventory levels remain relatively low in popular areas, creating competitive bidding situations. Strong pre-approval and quick closing capabilities provide significant advantages when multiple offers emerge.

Interest rates fluctuate based on Federal Reserve policy, inflation data, and bond market activity. The Washington State Department of Financial Institutions provides valuable resources about current lending practices and consumer protections.

Appraisal management has become more conservative following previous market cycles, with underwriters scrutinizing comparable sales selections and value conclusions more carefully. This increases the importance of realistic pricing and understanding neighborhood-specific value drivers.

The home mortgage loan process requires patience, organization, and expert guidance to navigate successfully, particularly in competitive Seattle-area markets where timing and strategy make significant differences in outcomes. Whether you're a first-time buyer exploring home loans for first-time buyers or a tech professional leveraging stock compensation for a jumbo purchase, understanding each stage prepares you for confident decision-making. Keith Akada at Mortgage Reel brings 25+ years of experience helping Seattle-area homebuyers through every step of this process, with the knowledge and proven track record to close your loan efficiently while protecting your interests throughout the transaction.