When you search for "find me a mortgage lender," you're taking one of the most important steps in your home financing journey. The mortgage professional you choose will directly impact your interest rate, closing costs, loan approval speed, and overall buying experience. For homebuyers in Seattle, Bellevue, Redmond, and Kirkland, where competitive markets and complex compensation structures are common, selecting the right lender becomes even more critical. This comprehensive guide walks you through exactly how to identify, evaluate, and ultimately choose a mortgage lender who can deliver the results you need in 2026's dynamic housing market.

Understanding the Types of Mortgage Lenders Available

Before you can effectively find me a mortgage lender who meets your specific needs, you must understand the fundamental differences between lender types. Each category operates with distinct business models that affect pricing, service quality, and product availability.

Direct Lenders vs. Mortgage Brokers

Direct lenders fund loans using their own capital and typically offer their proprietary loan products. Banks like Wells Fargo or Chase fall into this category, as do online-only lenders. While direct lenders may streamline certain processes through vertical integration, they can only present options from their own product menu.

Mortgage brokers, by contrast, work with multiple wholesale lenders and can compare dozens of loan programs simultaneously. When working with a great mortgage broker, you gain access to competitive wholesale pricing that often beats retail rates. This becomes particularly valuable for Seattle-area tech professionals with stock compensation, where specialized underwriting expertise makes the difference between approval and denial.

Key differences include:

- Product variety: Brokers access 20-50+ lenders; direct lenders offer only their programs

- Pricing flexibility: Wholesale broker channels frequently offer lower rates and fees

- Specialization: Brokers can match complex scenarios to specialized lenders

- Service model: Brokers provide personalized guidance; some direct lenders use automated systems

Credit Unions, Banks, and Online Lenders

Credit unions often provide competitive rates to members but may have slower processing times and limited product offerings. Traditional banks offer convenience for existing customers but typically charge higher fees than broker or online channels. Online lenders promise speed and technology-driven experiences, though they may lack local market expertise crucial in cities like Shoreline or Lynnwood.

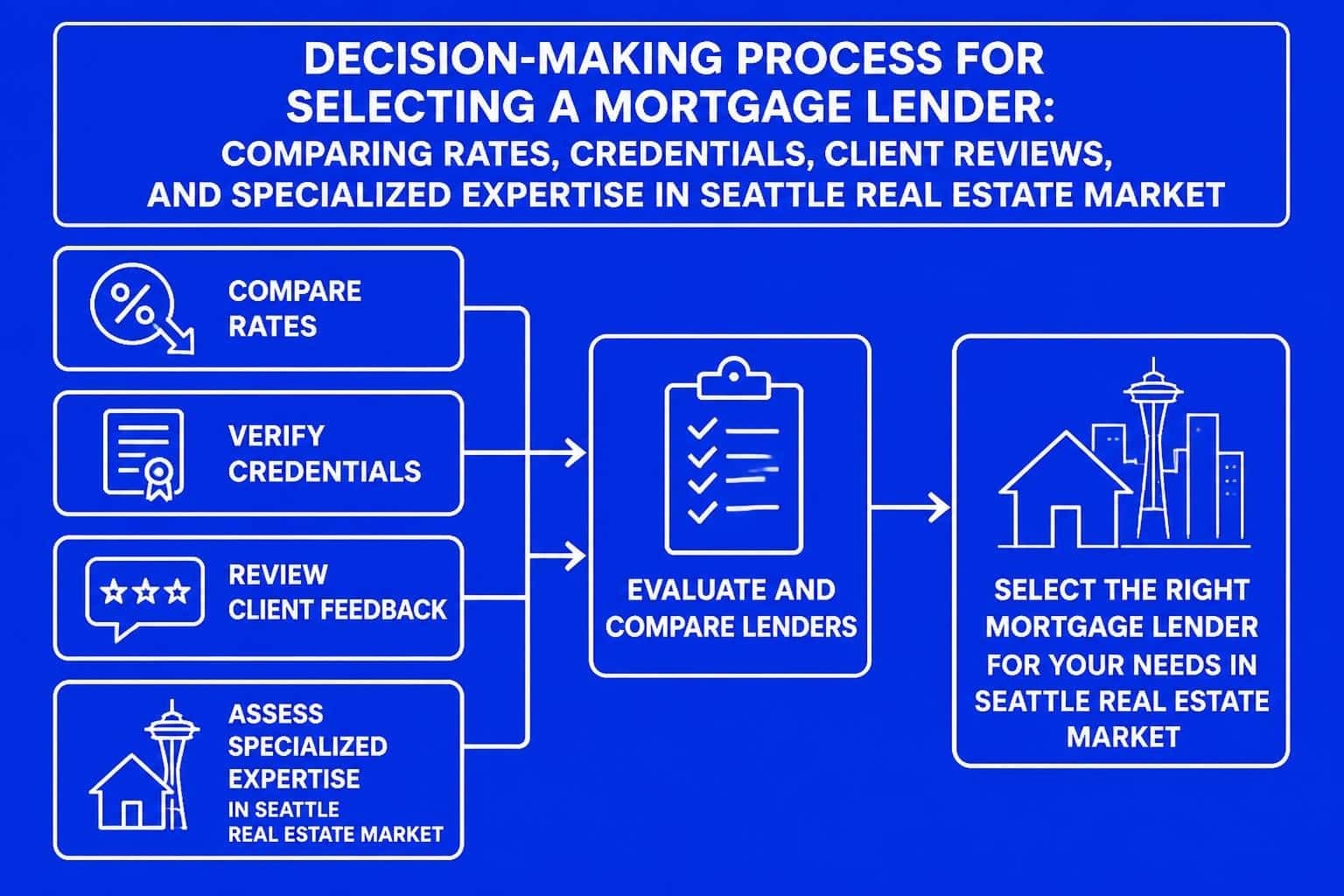

Essential Criteria When You Search to Find Me a Mortgage Lender

The Consumer Financial Protection Bureau emphasizes comparing multiple lenders to secure the best mortgage terms. This comparison process should evaluate several critical dimensions beyond just the interest rate.

Licensing, Experience, and Reputation

Every mortgage professional must hold appropriate state licensing. In Washington State, verify your lender's credentials through the Nationwide Multistate Licensing System (NMLS). Experience matters significantly, particularly when navigating competitive Seattle markets where properties receive multiple offers and fast closings determine success.

Client reviews provide transparent insight into a lender's actual performance. Look for consistent patterns across multiple platforms rather than isolated testimonials. A mortgage professional with 750+ five-star reviews demonstrates sustained excellence in execution, communication, and problem-solving.

| Evaluation Factor | What to Check | Red Flags |

|---|---|---|

| Licensing | Active NMLS license, state authorization | Expired credentials, complaints |

| Experience | Years in business, transaction volume | Less than 2 years, vague answers |

| Reviews | Google, Zillow, multiple platforms | Few reviews, recent negative patterns |

| Response Time | Initial contact to substantive reply | More than 24 hours, automated only |

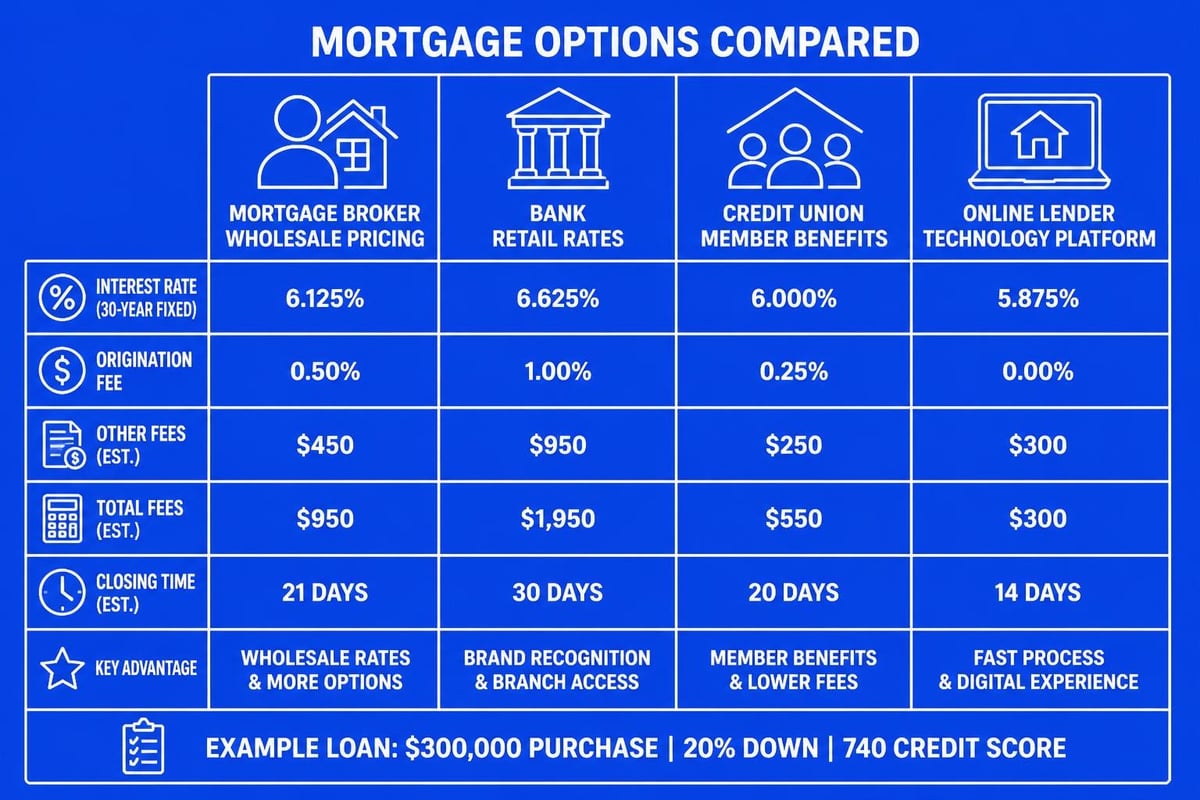

Rate, Fee Transparency, and Total Cost Analysis

When you find me a mortgage lender, don't make decisions based solely on advertised rates. The Annual Percentage Rate (APR) provides a more complete picture by incorporating both interest rate and certain fees. However, even APR doesn't capture every cost.

Request a detailed Loan Estimate within three business days of application. This standardized form allows true apples-to-apples comparison across lenders. Pay particular attention to:

- Origination charges and discount points

- Third-party fees that may be marked up

- Lender credits that can offset closing costs

- Prepayment penalties or rate adjustment clauses

For those exploring mortgage financing options, understanding the interplay between rate, points, and credits becomes essential. A slightly higher rate with lender credits might cost less over your ownership period than a lower rate requiring significant upfront points.

Specialized Expertise for Your Situation

Generic mortgage advice fails when your financial profile involves complexity. Seattle-area buyers frequently encounter scenarios requiring specialized knowledge:

Tech employee compensation: RSUs, stock options, and bonus income require lenders who understand how to properly document and qualify non-traditional income. Many lenders decline or undervalue this compensation, unnecessarily limiting buying power.

Jumbo loans: Properties above conforming loan limits ($806,500 in King County for 2026) require jumbo home mortgage expertise. Underwriting standards, documentation requirements, and pricing vary significantly across jumbo lenders.

Investment properties: Different qualification standards apply for non-owner-occupied purchases. Experienced lenders know which programs allow the most favorable terms for investors in Lake Forest Park or Mill Creek.

Self-employment income: Business owners and 1099 contractors need lenders familiar with alternative documentation methods and income calculation strategies that maximize qualification.

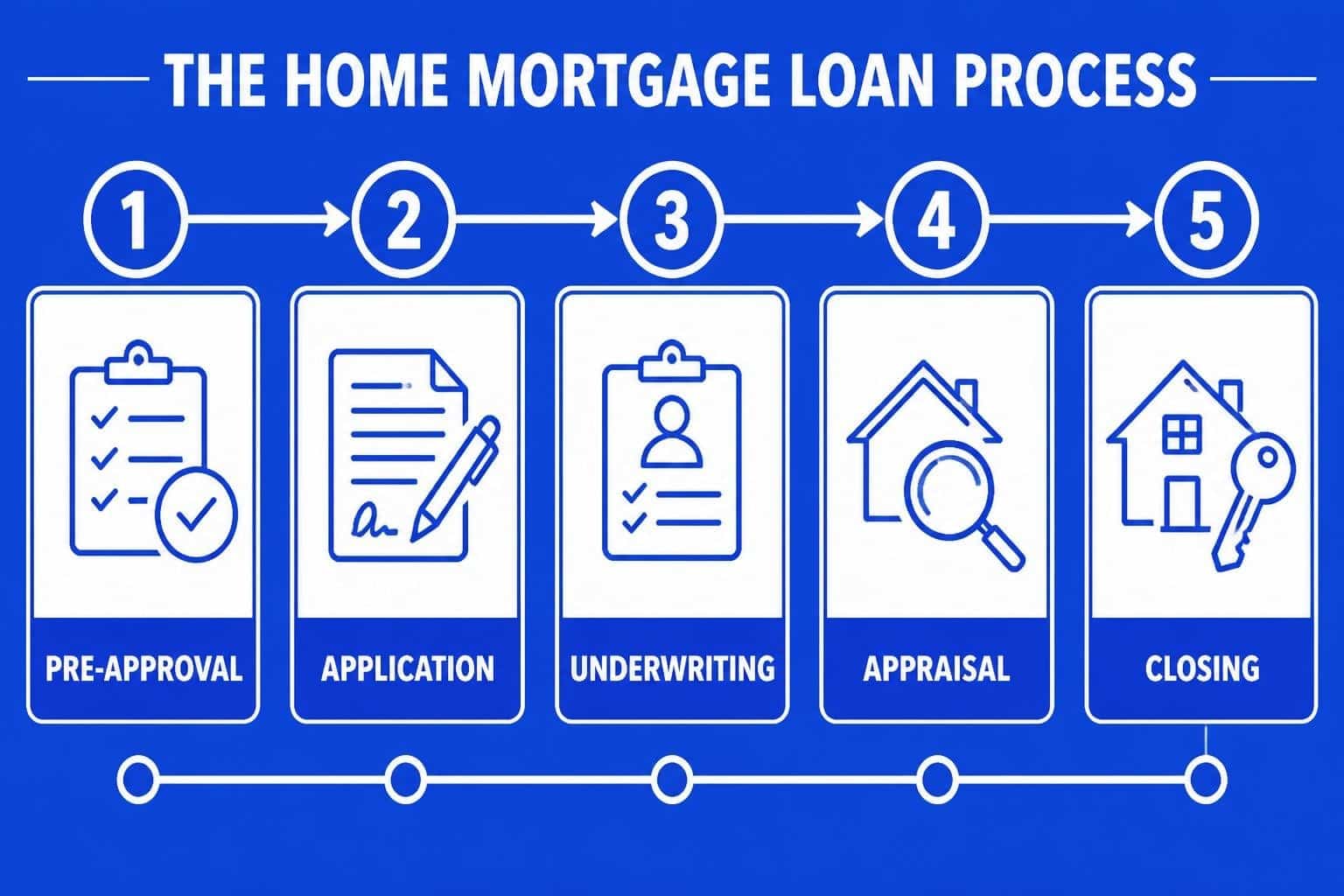

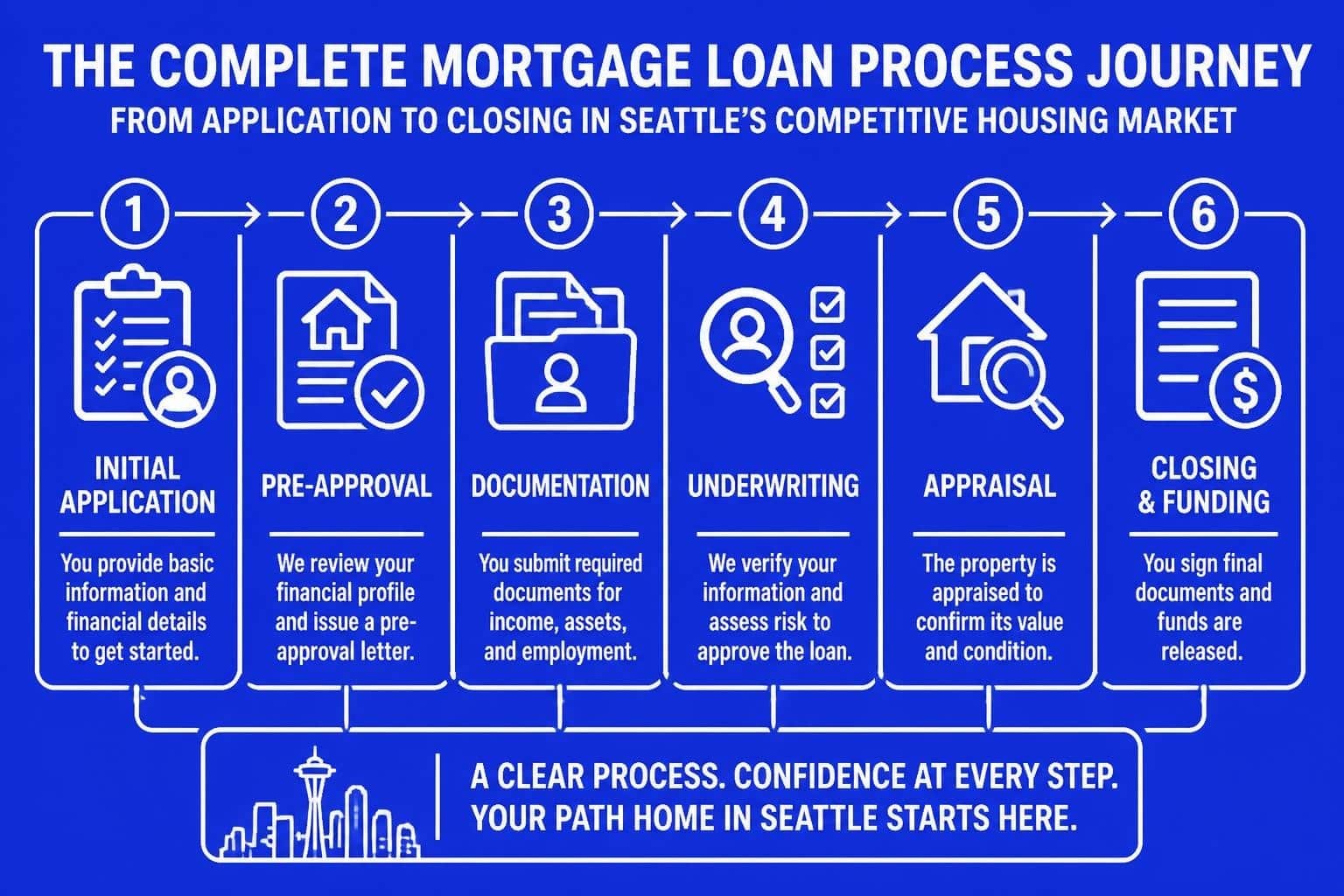

The Strategic Process to Find Me a Mortgage Lender

NerdWallet outlines comprehensive steps for selecting a mortgage lender, emphasizing the importance of understanding both your financial position and available loan options before making contact.

Step 1: Assess Your Financial Position and Goals

Begin by reviewing your credit reports from all three bureaus. Mortgage pricing tiers change at specific credit score thresholds (typically 620, 640, 660, 680, 700, 720, 740, and 760+). Understanding where you fall helps you evaluate whether the quoted rates align with your profile.

Calculate your debt-to-income ratio by dividing total monthly debt payments by gross monthly income. Most conventional loans require ratios below 43-50%, though some programs allow higher ratios with compensating factors.

Define your timeline and priorities. Do you need to close in 9 business days for a competitive Redmond offer? Are you prioritizing the lowest possible monthly payment? Does long-term cost matter more than upfront cash requirements? Clear priorities guide better lender selection.

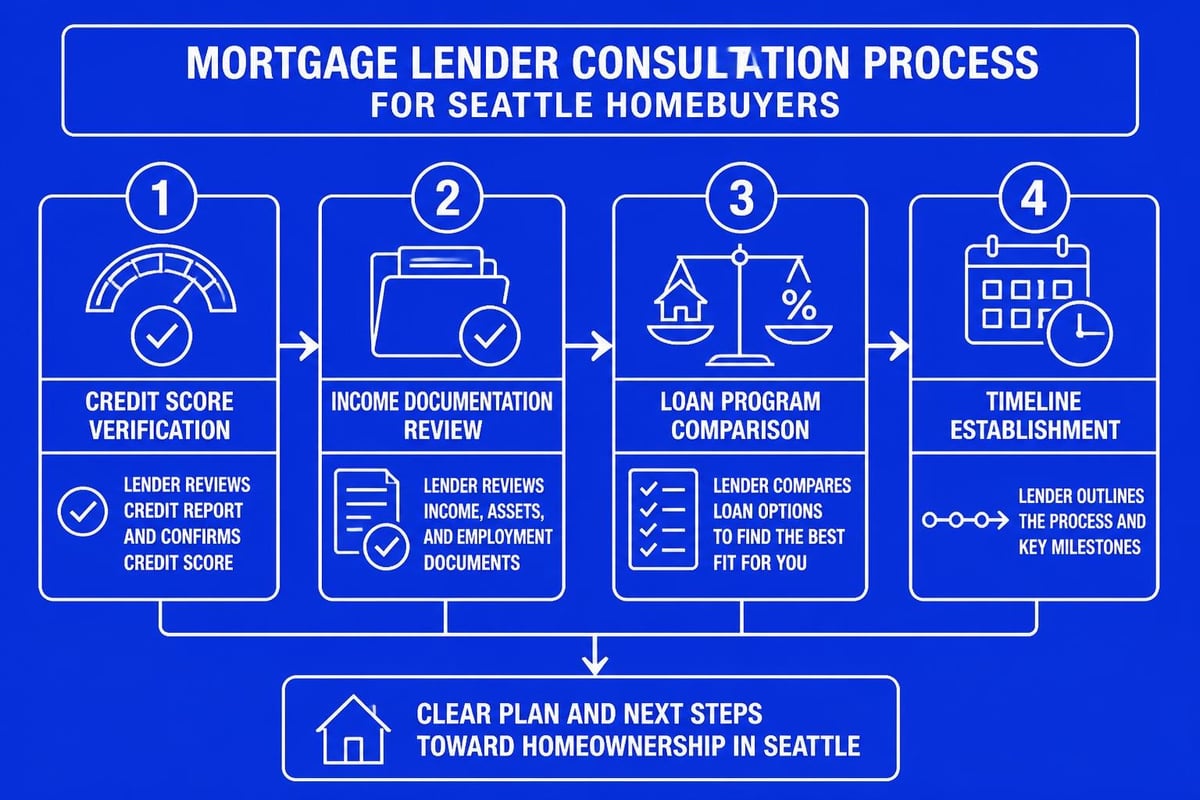

Step 2: Request Consultations and Loan Estimates

Contact at least three to five lenders representing different channel types. During initial conversations, assess how each professional approaches your situation. Do they ask detailed questions about your income, assets, and goals? Or do they immediately push toward an application without understanding your needs?

- Prepare a consistent scenario for each lender

- Request Loan Estimates based on identical assumptions

- Ask specific questions about their process and timeline

- Evaluate responsiveness and communication quality

- Compare total costs, not just interest rates

Quality lenders provide education rather than sales pressure. They explain options clearly, identify potential obstacles proactively, and demonstrate genuine interest in your success.

Step 3: Evaluate Communication and Service Quality

The mortgage process involves dozens of communications over 30-45 days (or as few as 9 business days with efficient lenders). Your lender's communication style during initial contact predicts the entire experience.

Strong mortgage professionals:

- Respond to inquiries within hours, not days

- Provide proactive updates rather than waiting for your calls

- Explain complex concepts in accessible language

- Set realistic expectations about timelines and requirements

- Maintain availability through evenings and weekends during critical periods

For first-time home buyers in Seattle, this educational approach proves particularly valuable. The complexity of Seattle's competitive market, combined with mortgage financing intricacies, creates a steep learning curve that knowledgeable lenders can flatten significantly.

Understanding Loan Programs and Options

When you find me a mortgage lender, ensure they can clearly articulate how different loan programs align with your specific situation. The right program choice impacts both immediate affordability and long-term costs.

Conventional, FHA, VA, and Jumbo Loans

Conventional loans require minimum credit scores around 620 and down payments as low as 3% for first-time buyers. These loans offer the most flexible terms and best pricing for borrowers with strong credit and stable income. Conventional loan lenders in Seattle markets frequently encounter properties exceeding conforming limits, requiring jumbo expertise.

FHA loans accommodate lower credit scores (as low as 580) and higher debt-to-income ratios. However, mandatory mortgage insurance remains for the loan's life unless you refinance. This trade-off benefits buyers prioritizing accessibility over long-term cost efficiency.

VA loans provide exceptional terms for eligible veterans and active-duty service members, including zero down payment requirements and no mortgage insurance. Despite these benefits, not all lenders understand VA appraisal requirements or processing nuances.

Jumbo loans finance properties above conforming limits and require enhanced documentation, larger reserves, and typically higher credit scores. Working with home loan lenders experienced in jumbo programs becomes essential for Bellevue and Kirkland properties frequently exceeding $1 million.

| Loan Type | Min. Credit Score | Down Payment | Mortgage Insurance | Best For |

|---|---|---|---|---|

| Conventional | 620+ | 3-20% | Removable at 20% equity | Strong credit, stable income |

| FHA | 580+ | 3.5% | Required for loan life | Lower credit scores, higher DTI |

| VA | No minimum | 0% | None | Eligible veterans, military |

| Jumbo | 700+ | 10-20% | Varies by lender | High-value properties |

Rate Lock Strategies and Timing

Understanding whether to lock or float your mortgage rate represents a critical decision point. Rate locks guarantee your interest rate for a specified period, typically 30-60 days. This protection proves valuable in rising rate environments or when closing timing is certain.

Floating your rate allows you to capture lower rates if markets improve before closing. However, rates can also increase, potentially costing hundreds monthly. Experienced lenders help you evaluate current market conditions, economic indicators, and your risk tolerance to make informed locking decisions.

Red Flags and Warning Signs to Avoid

Not every mortgage professional operates with integrity or competence. Recognizing warning signs early protects you from costly mistakes and stressful experiences.

Pressure tactics: Legitimate lenders educate and guide; they don't pressure you into rushed decisions or create false urgency around rate locks.

Reluctance to provide documentation: Quality professionals provide Loan Estimates promptly and answer fee questions directly. Vague responses about costs signal potential problems.

Unrealistic promises: Claims of guaranteed approval before reviewing your financial profile or promises of rates significantly below market averages often indicate bait-and-switch tactics.

Poor communication: Inconsistent responses, missed deadlines, or difficulty reaching your lender during business hours predict a difficult closing process.

Lack of local market knowledge: Seattle markets operate differently than other regions. Lenders unfamiliar with King County appraisal practices, title processes, or competitive offer strategies add risk to your transaction.

Technology, Speed, and the Modern Lending Experience

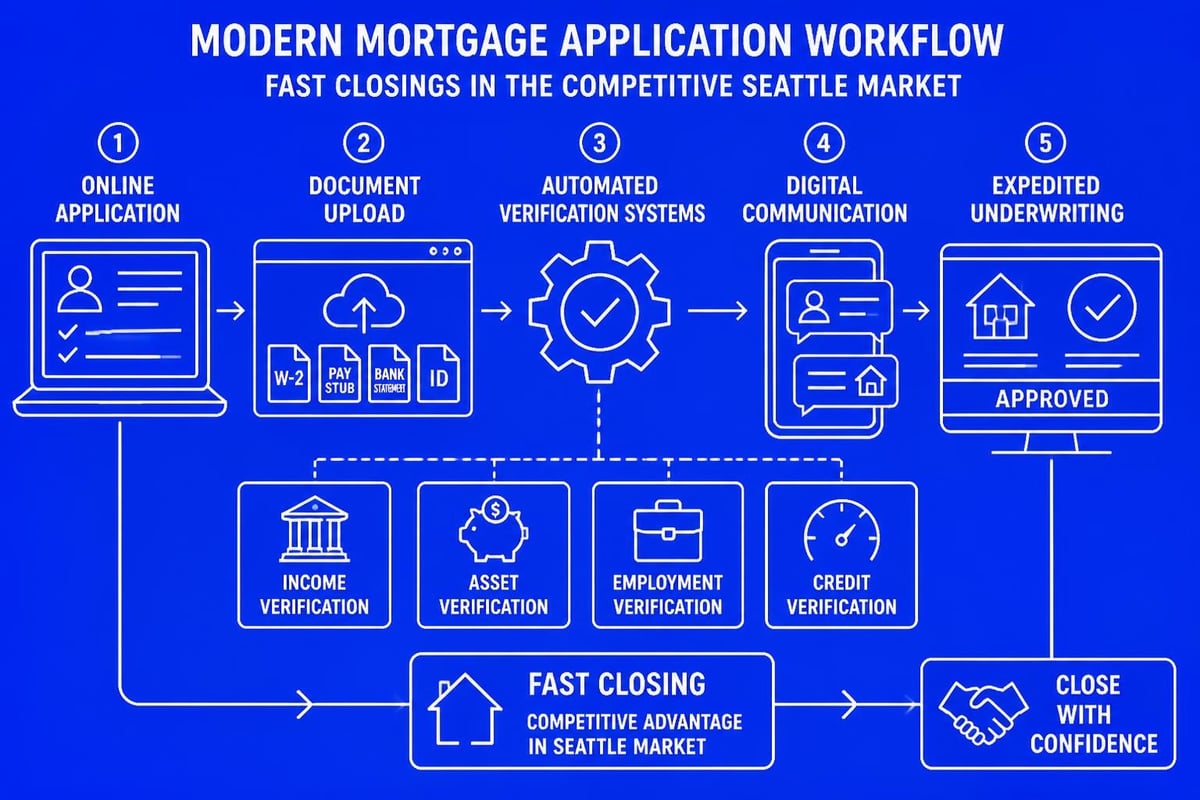

The mortgage industry has evolved significantly through technology adoption, but automation alone doesn't guarantee superior service. When you find me a mortgage lender, evaluate how they balance efficiency with personalization.

Advanced lenders now offer:

- Digital document upload portals that eliminate faxing and mailing

- Automated income and asset verification reducing documentation requirements

- Real-time application status tracking through client portals

- Electronic signature capabilities expediting document execution

- Accelerated underwriting timelines closing loans in 9-12 business days

However, technology should enhance rather than replace human expertise. Complex scenarios involving stock compensation, multiple income sources, or non-traditional documentation still require experienced professional judgment. The ideal combination pairs efficient technology with accessible expertise.

Questions to Ask Prospective Lenders

Prepare specific questions that reveal each lender's capabilities, processes, and fit for your situation. Surface-level conversations hide important differences that emerge under detailed inquiry.

About Their Experience and Approach

- How many years have you been originating mortgages in the Seattle area?

- What percentage of your business involves borrowers with stock compensation?

- How many loans do you personally close monthly?

- Which wholesale lenders do you work with for jumbo loans?

- Can you provide references from recent clients with similar profiles?

About Process and Timeline

- What's your average timeline from application to closing?

- What's your fastest recent closing, and what made it possible?

- How do you handle appraisal delays or title issues?

- What documentation will I need to provide initially?

- How frequently will you provide status updates?

About Costs and Programs

- Can you explain the difference between your rate and APR?

- What lender fees do you charge beyond third-party costs?

- How does your pricing compare between different loan programs?

- Do you offer lender credits, and how do they work?

- What happens if rates drop after I lock?

Zillow provides additional insights on choosing a mortgage lender, highlighting the importance of understanding your financial position before beginning lender conversations. This preparation enables more productive discussions and better comparison of lender responses.

The Value Proposition of Local Expertise

National online lenders offer convenience and technology, but they often lack the local market knowledge that proves critical in Seattle's competitive environment. When you find me a mortgage lender with deep Seattle roots, you gain strategic advantages:

Market timing insights: Understanding seasonal patterns in Shoreline, Lynnwood, and surrounding markets helps you time rate locks optimally and structure competitive offers.

Appraisal expertise: Seattle's unique property types, from older character homes to modern construction, require appraisers familiar with neighborhood dynamics and comparable sales. Local lenders maintain relationships with reliable appraisers who understand these nuances.

Title and escrow coordination: Smooth closings depend on efficient coordination between all parties. Established local relationships with title companies and escrow officers prevent delays and resolve issues quickly.

Real estate agent networks: Top agents prefer working with lenders who close reliably and communicate proactively. This reputation makes your offers more competitive in multiple-bid situations common across Bellevue, Redmond, and Kirkland.

Special Considerations for Seattle-Area Tech Professionals

Seattle's concentration of technology employers creates unique mortgage scenarios that require specialized expertise. When Amazon, Microsoft, Google, or other tech companies compensate employees through equity, standard lending guidelines often fail to maximize qualification potential.

Qualifying RSUs and Stock Compensation

Restricted Stock Units (RSUs) can significantly increase buying power when properly documented and underwritten. However, many lenders either decline to consider unvested RSUs or apply overly conservative calculation methods that unnecessarily limit qualification.

Experienced lenders understand how to:

- Document vesting schedules and calculate qualifying income

- Apply appropriate haircuts for volatility while maximizing usable income

- Navigate different underwriting guidelines across lenders

- Structure documentation that satisfies compliance requirements

- Coordinate timing around vesting events for optimal qualification

Bonus Income and Variable Compensation

Sales commissions, performance bonuses, and other variable compensation require two-year histories for most conventional programs. However, strategic lenders know exceptions and workarounds that can incorporate more recent income or higher percentages of variable pay.

For professionals moving to Seattle companies like those in Mill Creek or Everett, understanding the mortgage lending process with relocation scenarios helps you qualify based on new, higher compensation rather than historical earnings from previous positions.

Making Your Final Decision

After completing consultations, comparing Loan Estimates, and evaluating each lender's expertise, synthesize your findings to make a confident decision. The lowest rate doesn't always represent the best choice when other factors matter.

Prioritize these elements:

- Total cost over your expected ownership period

- Closing timeline capability matching your needs

- Communication quality and accessibility

- Specialized expertise relevant to your scenario

- Demonstrated track record with similar borrowers

Trust your instincts about the relationship. You'll communicate frequently with your mortgage professional over the coming weeks. Choose someone who inspires confidence, demonstrates competence, and treats your goals with appropriate seriousness.

Remember that when you find me a mortgage lender, you're not just selecting a financial transaction facilitator. You're choosing a strategic partner who can significantly impact your home purchase success, monthly payment affordability, and long-term financial position. This decision deserves careful consideration informed by thorough research and multiple comparisons.

Finding the right mortgage lender transforms from an overwhelming challenge into a strategic process when you understand evaluation criteria, ask pointed questions, and compare options systematically. For Seattle-area homebuyers navigating competitive markets, complex compensation structures, or jumbo home loans, working with experienced local expertise makes all the difference. Keith Akada brings 25+ years of mortgage experience and 750+ five-star reviews to help clients across Seattle, Bellevue, Redmond, and Kirkland achieve their homeownership goals with confidence, transparency, and reliable execution. Visit Mortgage Reel to experience the difference that specialized knowledge and proven performance deliver.