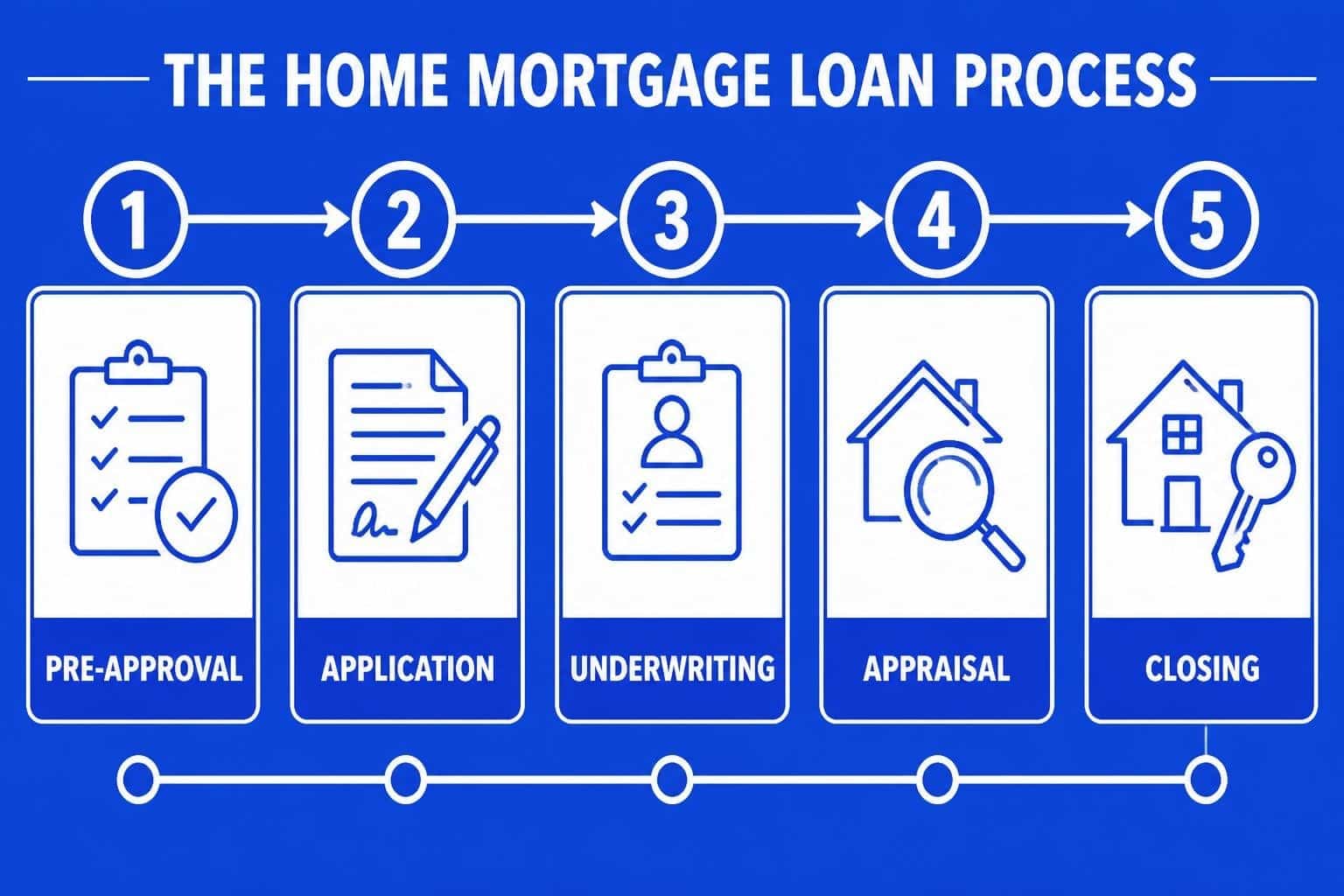

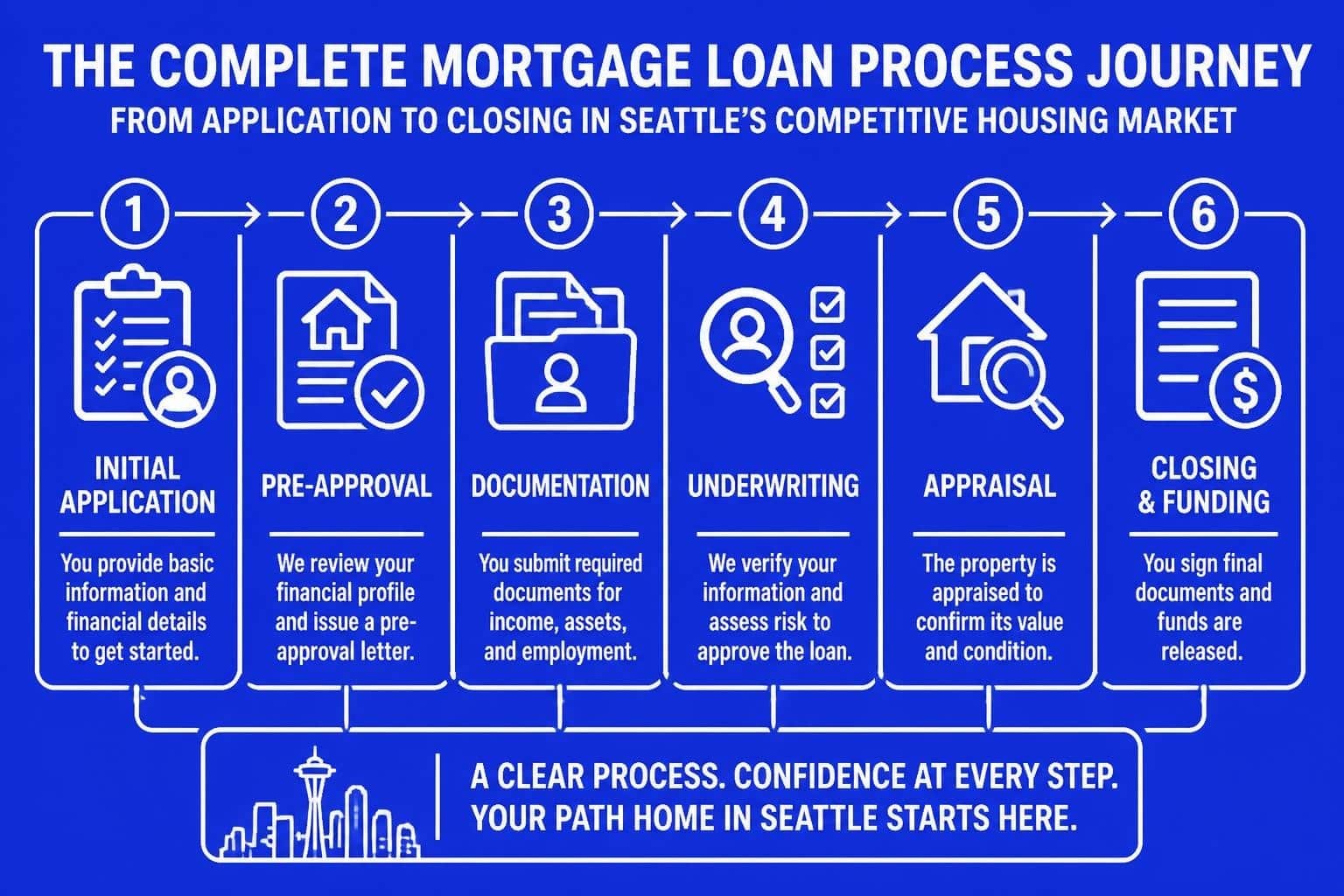

Understanding the mortgage loan process can mean the difference between a smooth transaction and a stressful experience, especially in competitive markets like Seattle, Bellevue, and Redmond. Whether you're a first-time buyer in Lake Forest Park or a tech professional relocating to Kirkland, knowing what to expect at each stage helps you make informed decisions and avoid costly surprises. The mortgage loan process involves multiple steps, from initial pre-approval through final closing, and each phase requires specific documentation, timelines, and decisions that impact your home purchase success.

Pre-Approval: Starting the Mortgage Loan Process Strong

The mortgage loan process officially begins with pre-approval, a critical step that establishes your borrowing capacity and demonstrates credibility to sellers. Unlike pre-qualification, which offers a rough estimate based on self-reported information, pre-approval involves a thorough review of your financial profile, including income verification, credit analysis, and debt assessment.

Documentation Requirements for Pre-Approval

Gathering the right documentation upfront accelerates the mortgage loan process significantly. Most lenders require:

- Recent pay stubs covering the past 30 days

- W-2 forms from the previous two years

- Federal tax returns for the past two years, including all schedules

- Bank statements from all accounts for the last two months

- Employment verification with contact information for HR departments

- Documentation of additional income sources such as bonuses, commissions, or rental income

For tech professionals working at Amazon, Microsoft, or Google in the Seattle area, stock compensation requires specialized documentation. RSUs, stock options, and equity grants can be included in qualifying income when properly documented through vesting schedules and historical award letters. This specialized approach to qualifying stock compensation often increases buying power substantially.

Credit Review and Score Impact

Lenders evaluate credit reports from all three major bureaus during the mortgage loan process. Your credit score influences both loan approval and interest rate pricing. Most conventional loans require minimum scores of 620, though better rates typically start at 740 or higher.

Credit inquiries during mortgage shopping have minimal impact when completed within a 45-day window. This shopping period allows you to compare loan offers from multiple lenders without damaging your score.

Property Search and Purchase Agreement

With pre-approval secured, the mortgage loan process advances to property selection and offer submission. In competitive Seattle-area markets like Bellevue and Redmond, strong pre-approval letters help buyers stand out, particularly when multiple offers compete for the same property.

Your pre-approval amount guides your search parameters, though purchasing below your maximum approval often provides financial flexibility. Many experienced buyers in Shoreline and Lynnwood target homes at 80-85% of their approval amount to maintain comfortable monthly payments and reserves.

Making Competitive Offers in Seattle Markets

The purchase agreement triggers the next phase of the mortgage loan process. Once accepted, you typically have 3-5 days to complete your loan application and deposit earnest money. Seattle's fast-paced market demands quick action-delays can jeopardize your contract or result in penalties.

Your loan officer should review the purchase agreement for financing contingencies, closing timeline requirements, and any seller concessions that impact loan structuring. These details directly affect underwriting decisions and closing coordination.

Formal Loan Application and Initial Disclosures

The formal application initiates the official mortgage loan process through your chosen lender. The Uniform Residential Loan Application (Form 1003) captures comprehensive information about your finances, employment history, assets, debts, and property details.

Within three business days of application, federal law requires lenders to provide key disclosures:

| Disclosure Document | Purpose | Timing Requirement |

|---|---|---|

| Loan Estimate | Standardized summary of loan terms, projected payments, and closing costs | Within 3 business days of application |

| Initial Escrow Disclosure | Breakdown of escrow account requirements for taxes and insurance | Provided with Loan Estimate |

| Home Loan Toolkit | Educational booklet explaining the mortgage loan process | Delivered with application disclosures |

| Special Information Booklet | RESPA guide to settlement costs and borrower rights | Included in initial disclosure package |

The Loan Estimate standardizes cost comparisons across lenders, making it easier to evaluate different mortgage offers. Key sections include loan terms, projected payments, costs at closing, and comparison tables showing total interest and principal over the loan life.

Understanding different types of mortgage loans helps you evaluate whether your application reflects the optimal program for your situation. Conventional loans, FHA financing, VA loans, and jumbo products each serve different borrower profiles and property types.

Processing: Document Collection and Verification

Once your application is submitted, the mortgage loan process enters the processing phase. Your loan processor coordinates document collection, verifies information accuracy, and prepares your file for underwriting review.

Verification Steps During Processing

Processors conduct multiple verifications to confirm application accuracy:

- Employment verification through direct employer contact or third-party services

- Income verification by analyzing pay stubs, tax returns, and additional documentation

- Asset verification through bank statements and investment account records

- Debt verification using credit reports and direct creditor inquiries when necessary

- Property verification confirming legal description, ownership chain, and zoning compliance

For self-employed borrowers in Seattle's thriving entrepreneurial community, processing involves additional documentation including profit and loss statements, business tax returns, and CPA-prepared financial statements. The mortgage loan process for business owners typically requires more time due to income calculation complexity.

Underwriting: Risk Assessment and Loan Approval

Underwriting represents the most critical phase of the mortgage loan process. Underwriters evaluate your complete financial profile against specific lending guidelines, assessing risk and determining whether your loan meets investor requirements.

The Three Cs of Mortgage Underwriting

Underwriters evaluate applications through three primary lenses:

Capacity measures your ability to repay the loan based on income stability, employment history, and debt-to-income ratios. Most conventional loans require DTI ratios below 43%, though qualified mortgage standards permit flexibility in certain situations. For jumbo loans common in high-cost Seattle neighborhoods, DTI requirements often tighten to 38% or lower.

Credit assessment extends beyond score evaluation to include payment history patterns, credit utilization, recent inquiries, and derogatory marks. Underwriters look for responsible credit management over time, not perfection. Recent late payments raise more concern than older issues.

Collateral evaluation ensures the property provides adequate security for the loan amount. This phase includes appraisal review, title examination, and property condition assessment. In competitive markets like Bellevue and Redmond, purchase prices sometimes exceed appraised values, requiring additional negotiation or buyer cash investment.

Common Underwriting Conditions

Initial underwriting reviews typically generate conditions-additional documentation or explanation requests. Common conditions include:

- Letters of explanation for credit inquiries, employment gaps, or large deposits

- Updated pay stubs or bank statements if documents age beyond 60-90 days

- Verification of gift funds including source documentation and donor relationship confirmation

- Additional property documentation for condos, co-ops, or unique property types

- Clarification of income sources, particularly for commission or bonus income

Responding to conditions quickly keeps the mortgage loan process on schedule. Delays in condition fulfillment often extend closing timelines and may jeopardize rate locks.

Appraisal: Property Value Determination

Property appraisal occurs during the underwriting phase but warrants specific attention due to its impact on loan approval. Licensed appraisers provide independent assessments of market value, ensuring the property provides adequate collateral for the requested loan amount.

The appraisal process typically takes 7-10 business days from order to delivery, though complex properties or rural locations may require additional time. Appraisers evaluate the property through multiple approaches:

- Sales comparison approach analyzing recent comparable sales in the area

- Cost approach estimating replacement cost minus depreciation

- Income approach for investment properties based on rental income potential

In Seattle's dynamic real estate market, appraisal challenges occasionally arise when purchase prices reflect competitive bidding rather than comparable sales data. Working with an experienced Seattle mortgage broker helps navigate appraisal issues through strategic solutions like reconsideration of value requests, additional comparable data submission, or loan restructuring.

Appraisal Contingency Strategy

Most purchase agreements include appraisal contingencies protecting buyers when appraised values fall below contract prices. Understanding this protection within the broader mortgage loan process empowers you to negotiate effectively with sellers when value shortfalls occur.

Clear to Close: Final Approval Stage

Receiving clear-to-close status represents a major milestone in the mortgage loan process. This designation confirms that underwriting has approved your loan, all conditions have been satisfied, and only final steps remain before funding.

The clear-to-close phase involves several coordinated activities:

Final Documentation and Verification

Lenders conduct final verifications within days of closing to ensure no material changes have occurred since initial approval. This includes employment reverification, credit refresh, and asset confirmation. Any significant changes-job loss, large purchases, new credit accounts-can derail approval even at this late stage.

Critical actions to avoid during the mortgage loan process:

- Opening new credit accounts or applying for additional credit

- Making large purchases on credit or depleting savings

- Changing jobs or employment status without lender consultation

- Transferring funds between accounts without documentation

- Co-signing loans for other individuals

Title Review and Insurance

Title companies conduct comprehensive searches confirming clear ownership and identifying any liens, easements, or encumbrances affecting the property. Title insurance protects both lender and owner against future claims or defects in the title chain.

In Washington State, buyers typically choose the title company, though sellers sometimes specify providers in purchase agreements. Working with reputable title companies familiar with King County, Snohomish County, and local jurisdiction requirements streamlines the mortgage loan process.

Closing: Finalizing Your Mortgage

The closing appointment concludes the mortgage loan process and transfers property ownership. Washington State conducts closings through escrow companies rather than attorney-supervised table closings common in other regions.

Closing Disclosure Review

Federal law requires lenders to provide the Closing Disclosure at least three business days before closing. This document details final loan terms, closing costs, and cash requirements. Compare this carefully against your initial Loan Estimate to identify any changes or unexpected fees.

The three-day review period allows you to identify issues, ask questions, and address concerns before finalizing the transaction. Material changes to loan terms can reset the three-day clock, potentially delaying closing.

What to Bring to Closing

Successful closings require specific items and preparation:

- Government-issued photo identification (driver's license or passport)

- Cashier's check or wire transfer confirmation for closing costs and down payment

- Proof of homeowners insurance with the lender listed as mortgagee

- Copy of the Closing Disclosure for reference during document review

Review the extensive mortgage loan origination process to understand typical closing costs including origination fees, title insurance, recording fees, prepaid property taxes, and initial escrow deposits.

Closing appointments typically last 60-90 minutes, involving numerous document signatures. Key documents include the promissory note (your legal obligation to repay), deed of trust (security instrument), and various disclosure forms. The escrow officer guides you through each document, though you should understand major terms before arrival.

Post-Closing: After the Mortgage Loan Process

Your responsibilities continue after closing concludes the mortgage loan process. Understanding post-closing obligations ensures smooth homeownership transition.

First Mortgage Payment Timing

Your first mortgage payment typically occurs 30-45 days after closing, not the following month. This timing reflects interest accrual from closing through month-end, plus the standard 30-day payment cycle. Your servicer sends payment coupons or online account access within 15-20 days of closing.

Loan Servicing Transfer

Many lenders sell loans to investors or transfer servicing rights after closing. Federal law requires advance notice of servicing transfers, though these changes don't affect your loan terms, interest rate, or repayment obligations. Update automatic payments when servicers change to avoid payment disruptions.

Important Documents to Retain

Maintain organized records of key mortgage documents:

| Document Type | Retention Period | Purpose |

|---|---|---|

| Closing Disclosure | Permanent | Tax deduction verification, refinance comparison |

| Promissory Note | Until loan payoff | Legal payment obligation documentation |

| Deed of Trust | Until loan payoff | Security instrument and lien documentation |

| Title Insurance Policy | Permanent | Ownership protection and claim resolution |

| Property Appraisal | Until next refinance or sale | Value documentation and PMI removal support |

| Tax Returns (post-purchase) | 7 years | Mortgage interest deduction substantiation |

Special Considerations for Seattle-Area Buyers

The mortgage loan process in Seattle presents unique considerations reflecting the region's competitive market dynamics and demographic profile.

Technology Industry Compensation

Seattle's concentration of technology employers creates specialized lending scenarios. Amazon, Microsoft, Google, and numerous startups compensate employees through complex packages including base salary, RSUs, stock options, bonuses, and benefits. Lenders experienced with tech compensation structures can maximize qualifying income by properly documenting and calculating these components.

Unvested RSUs typically don't qualify for income calculation, though vested grants with two-year history can contribute to qualifying income. Stock options require careful analysis of exercise prices, vesting schedules, and historical values. Bonuses qualify when documented through two years of consistent receipt.

Jumbo Loan Requirements

Seattle's high home prices frequently push buyers into jumbo loan territory. Conforming loan limits for King County reach $1,149,825 in 2026, but many desirable neighborhoods in Bellevue, Redmond, and central Seattle feature median prices exceeding these thresholds.

Jumbo loans through the mortgage loan process require stronger financial profiles including higher credit scores (typically 720+), larger down payments (often 10-20%), and lower debt-to-income ratios. However, experienced lenders structure competitive jumbo programs with favorable rates and flexible terms for qualified borrowers.

Condominium Financing Complexity

Seattle's urban core features extensive condominium inventory, and condo financing adds complexity to the mortgage loan process. Lenders evaluate both borrower qualifications and project certifications, reviewing HOA budgets, reserve funds, owner-occupancy ratios, and pending litigation.

FHA and VA condo approval lists limit financing options for many buildings, while conventional lending offers broader flexibility through project review processes. Working with lenders familiar with Seattle-area condo projects accelerates approval and prevents purchase agreement complications.

Timeline Expectations Throughout the Process

Understanding realistic timelines helps manage expectations during the mortgage loan process. While accelerated timelines exist for qualified borrowers with experienced lenders, standard timeframes provide reliable planning benchmarks.

Standard Mortgage Loan Process Timeline

Days 1-3: Application submission and initial disclosure delivery

Days 3-7: Processing begins, initial document collection and verification

Days 7-14: Appraisal ordered and completed (property-dependent)

Days 10-21: Underwriting review and initial conditions issued

Days 14-25: Condition fulfillment and final underwriting approval

Days 25-30: Clear to close, final verifications, and closing preparation

Day 30-35: Closing appointment and funding

Accelerated programs compress timelines to 9-15 business days for highly qualified borrowers with complete documentation, stable employment, and straightforward property types. These expedited closings prove valuable in competitive markets where sellers prioritize closing certainty and speed.

Factors That Extend Timelines

Several factors commonly extend the mortgage loan process beyond standard timeframes:

- Complex income documentation for self-employed or commissioned borrowers

- Property appraisal challenges including value shortfalls or condition issues

- Condominium or unique property types requiring additional review

- Credit issues requiring explanations, disputes, or resolution

- Multiple loan programs or structure changes during processing

- High application volume during peak homebuying seasons

Proactive communication with your loan officer throughout the mortgage loan process helps identify potential delays early and implement solutions before they impact closing dates.

Optimizing Your Mortgage Loan Process Experience

Strategic preparation and informed decision-making significantly improve your mortgage loan process experience. Consider these professional insights from 25+ years serving Seattle-area homebuyers.

Start Pre-Approval Early

Begin the mortgage loan process 60-90 days before serious home shopping. This timeline allows credit optimization, documentation gathering, and strategic planning without purchase pressure. Early pre-approval also reveals potential qualification challenges, providing time for corrective action.

Maintain Financial Stability

Consistency throughout the mortgage loan process proves crucial for smooth approval. Maintain stable employment, avoid large purchases, preserve savings balances, and continue existing credit patterns. Underwriters view consistency as reliability, while changes trigger additional scrutiny and documentation requirements.

Choose Experienced Local Expertise

The mortgage loan process complexity demands knowledgeable guidance, particularly in specialized markets like Seattle. Local mortgage expertise provides advantages including market knowledge, local processing efficiency, underwriting familiarity with area property types, and closing coordination with regional title companies.

Respond Promptly to Requests

Timely responses to documentation requests, condition fulfillment, and lender inquiries keep the mortgage loan process moving forward. Most delays result from slow borrower response rather than lender processing inefficiency. Treat condition requests as urgent priorities requiring same-day or next-day attention.

Understand Your Loan Programs

Research available loan programs before application to ensure optimal product selection. Conventional loans, FHA financing, and specialized products each serve different scenarios with varying qualification requirements, down payment needs, and cost structures. Understanding program differences empowers better decisions aligned with your financial situation and homeownership goals.

Navigating the mortgage loan process successfully requires preparation, knowledge, and experienced guidance. From initial pre-approval through closing and beyond, each phase presents specific requirements and decisions that impact your home purchase outcome. Whether you're a first-time buyer in Lake Forest Park, a tech professional relocating to Seattle, or an experienced investor in Bellevue, understanding the complete mortgage loan process empowers confident decisions and smooth transactions. Keith Akada brings 25+ years of mortgage expertise and 750+ five-star reviews to help Seattle-area homebuyers navigate every step with clarity and confidence. Visit Mortgage Reel to start your home financing journey with a trusted local expert who specializes in tech compensation, jumbo loans, and fast closings in competitive markets.