Navigating the path to homeownership in Seattle's competitive real estate market requires understanding how lenders evaluate your financial profile. Loan approval is not a mystery-it's a structured process where specific criteria determine whether you qualify for financing and under what terms. For buyers in Seattle, Bellevue, Redmond, and surrounding areas, knowing what underwriters assess can transform your approach from reactive to strategic. Whether you're a first-time buyer in Lake Forest Park or a tech professional leveraging stock compensation for a jumbo home loan, understanding the approval framework gives you a competitive advantage.

What Lenders Actually Evaluate During Loan Approval

Mortgage lenders examine your application through a comprehensive lens that extends far beyond your credit score. The approval process involves multiple checkpoints designed to assess your ability and willingness to repay the debt over time.

The Five Pillars of Financial Assessment

Lenders base their decisions on five fundamental criteria that paint a complete picture of your financial health:

- Credit history and score: Demonstrates your track record with previous debts and payment consistency

- Income stability and documentation: Proves reliable earnings to support monthly mortgage obligations

- Debt-to-income ratio (DTI): Measures existing debt against gross monthly income

- Down payment and reserves: Shows financial commitment and ability to weather unexpected expenses

- Collateral value: Ensures the property adequately secures the loan amount

Understanding key factors mortgage lenders consider when approving loans helps you prepare documentation and address potential weaknesses before submitting your application.

How Tech Compensation Affects Approval in Seattle

For professionals at Amazon, Microsoft, Google, and other Seattle-area employers, RSU income and stock compensation require specialized underwriting approaches. Traditional loan approval processes often struggle with variable income sources, but experienced lenders understand how to document and qualify:

- Restricted Stock Units (RSUs): Typically averaged over 24 months with vesting schedules considered

- Performance bonuses: Require two-year history for full consideration

- Stock options: Evaluated based on exercise potential and vesting timelines

- Equity compensation: May be discounted or require longer documentation periods

The ability to maximize these income sources directly impacts your purchasing power in high-value markets like Bellevue and Redmond where home prices frequently exceed conforming loan limits.

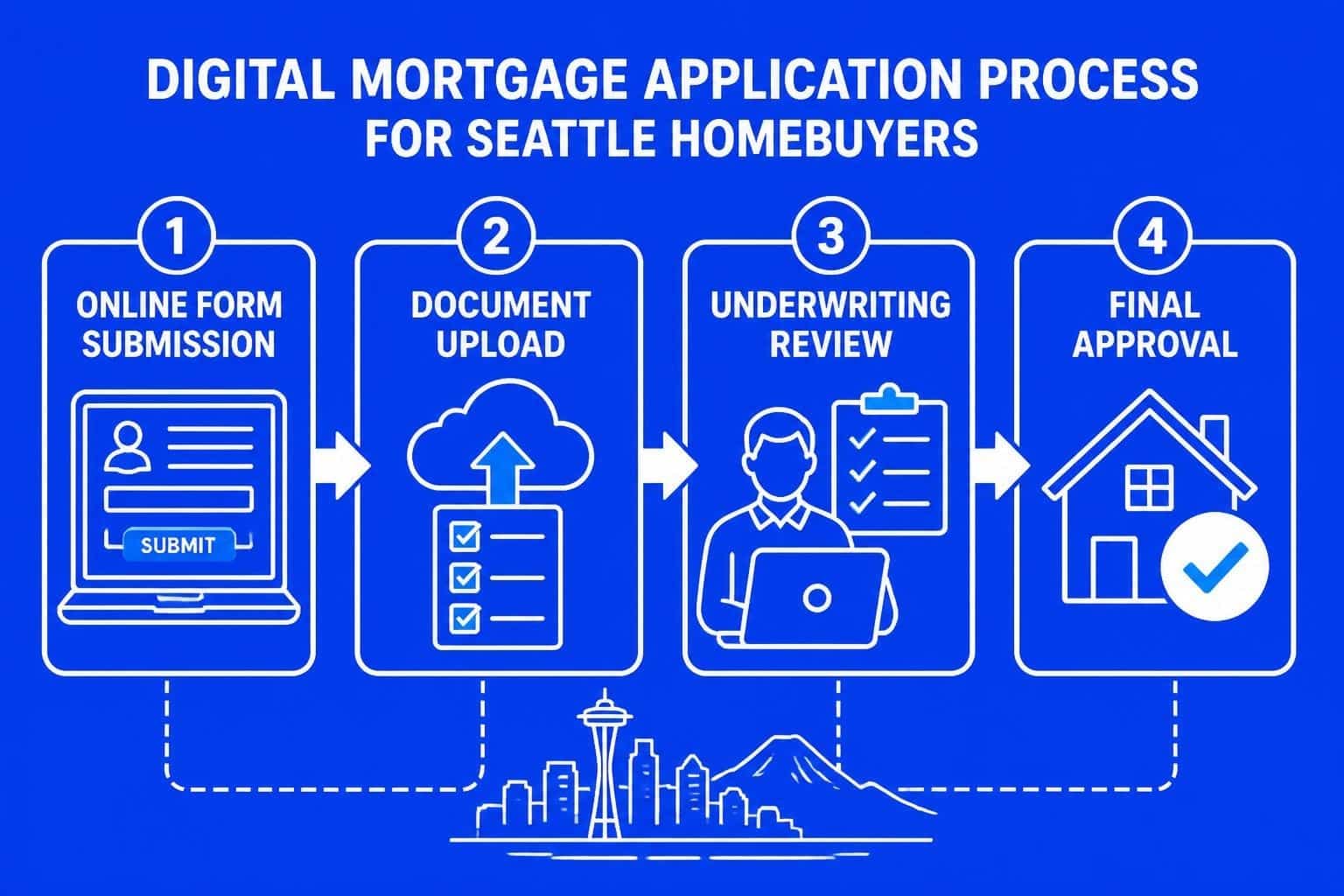

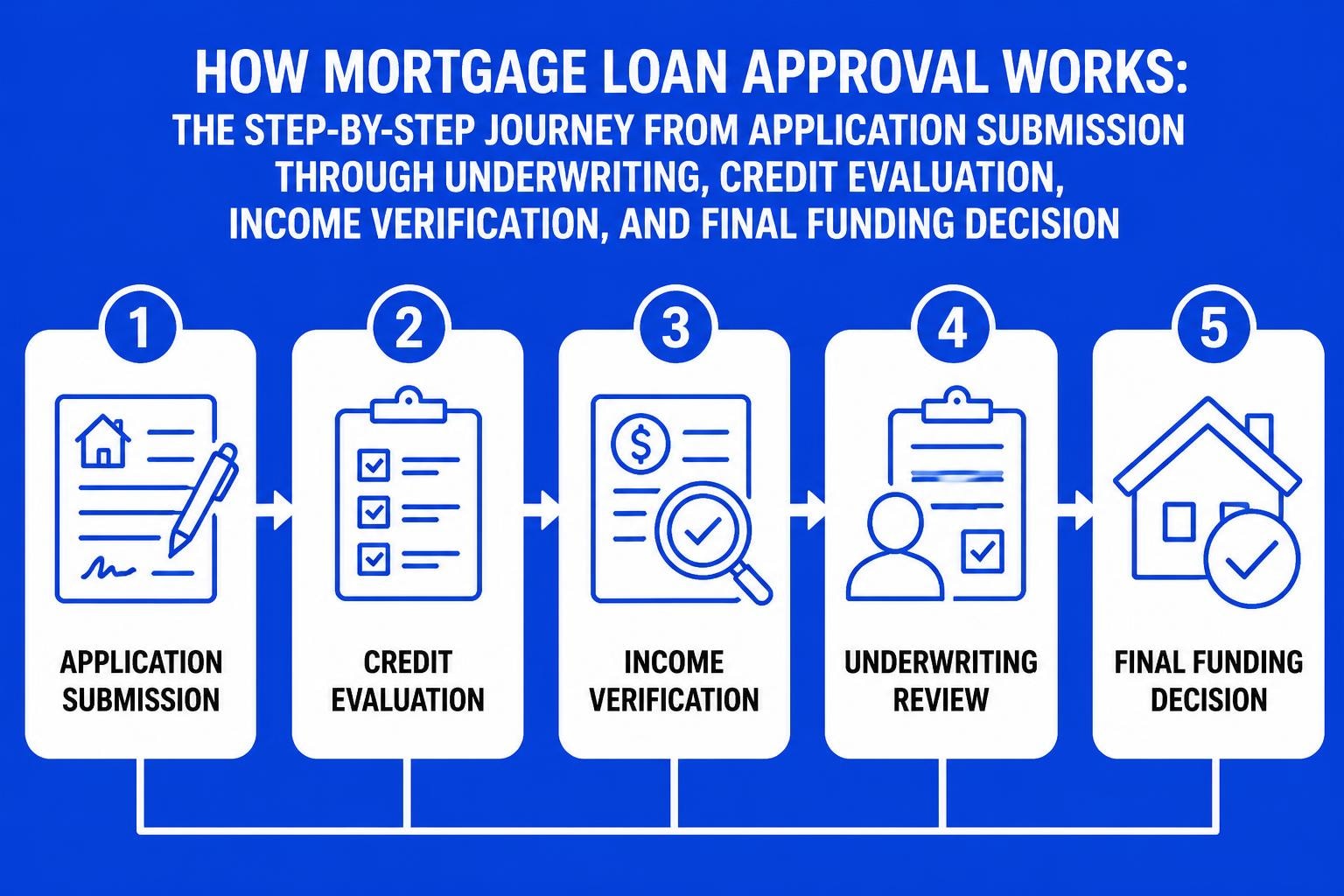

The Step-by-Step Journey Through Loan Approval

The mortgage approval timeline follows a predictable sequence, though duration varies based on complexity and documentation completeness. Understanding each phase helps you prepare appropriately and avoid delays.

Phase One: Pre-Qualification and Pre-Approval

Pre-qualification provides an informal estimate based on self-reported information, while pre-approval involves actual verification of financial data. The loan approval process begins with comprehensive documentation review.

Pre-approval requirements typically include:

- Two years of tax returns (W-2s and 1099s)

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Credit report authorization

- Employment verification consent

Seattle-area buyers competing in multiple-offer scenarios find that thorough pre-approval documentation separates serious contenders from hopeful shoppers. Properties in neighborhoods like Capitol Hill and Montlake often receive multiple offers within days, making pre-approval status essential.

Phase Two: Formal Application and Processing

Once you've identified a property and entered contract, the formal application initiates. Loan processors collect detailed documentation while ensuring accuracy and completeness.

| Processing Activity | Timeline | Borrower Action Required |

|---|---|---|

| Application submission | Day 1 | Complete 1003 form, sign disclosures |

| Document collection | Days 2-5 | Provide requested financial records |

| Credit verification | Days 3-7 | Explain credit inquiries if needed |

| Employment verification | Days 5-10 | Respond to HR inquiries promptly |

| Asset verification | Days 3-8 | Explain large deposits, source of funds |

Processing efficiency directly impacts closing timelines. With advanced systems and experienced teams, some lenders can process applications significantly faster than industry averages.

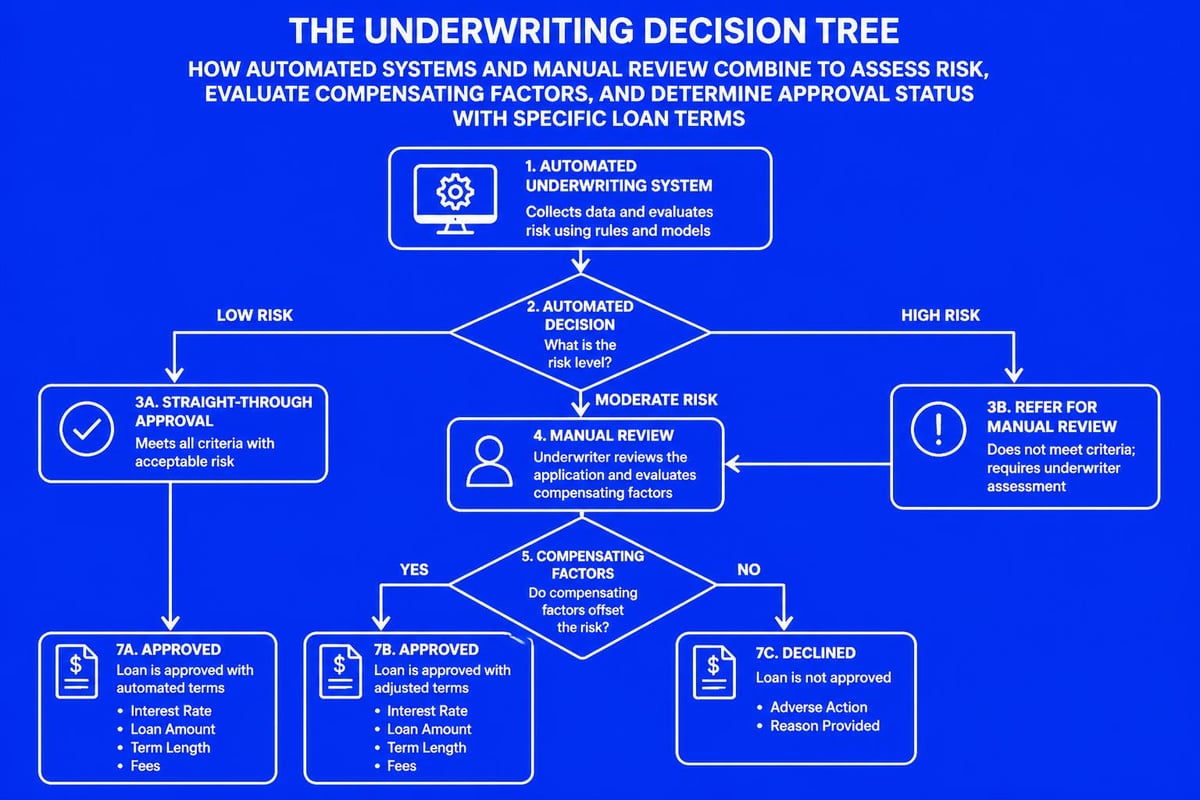

Phase Three: Underwriting Review

Underwriting represents the critical evaluation phase where trained professionals assess risk and ensure guideline compliance. This stage determines whether you receive loan approval, conditional approval, or denial.

Underwriters specifically examine:

- Debt-to-income calculations including the proposed housing payment

- Credit event timelines (bankruptcies, foreclosures, late payments)

- Income continuity and probability of sustained earnings

- Asset sufficiency for down payment and reserves

- Property condition and appraisal compliance

Conditional approval means you've substantially met requirements but need to provide additional documentation or explanations. Common conditions include updated pay stubs, explanation letters for credit inquiries, or verification of large deposits. Understanding what lenders look for when approving home loans helps you anticipate requests and respond quickly.

Debt-to-Income Ratio: The Critical Metric

Your DTI ratio represents perhaps the most influential factor in loan approval decisions. This percentage measures your total monthly debt obligations against gross monthly income, revealing how much housing payment you can sustain.

Front-End vs. Back-End Ratios

Lenders calculate two distinct ratios:

Front-end ratio includes only housing expenses:

- Principal and interest payment

- Property taxes

- Homeowners insurance

- HOA dues (if applicable)

- Mortgage insurance (when required)

Back-end ratio encompasses all monthly debt:

- All front-end housing costs

- Credit card minimum payments

- Auto loans and leases

- Student loan obligations

- Personal loans and installment debt

- Child support or alimony payments

Most conventional home loans allow back-end ratios up to 43-50% depending on compensating factors, while FHA financing may permit higher ratios with strong credit profiles.

Strategies to Improve Your DTI Before Applying

Seattle homebuyers facing challenging DTI calculations can take specific actions to strengthen their position:

- Pay down revolving debt: Reducing credit card balances creates immediate ratio improvement

- Consolidate high-interest debt: Lowering monthly obligations without increasing total debt

- Postpone major purchases: Avoiding new auto loans or financing during the approval process

- Increase income documentation: Ensuring all qualifying income sources are properly captured

- Consider co-borrowers: Adding qualified individuals to expand household income

For professionals in Shoreline or Lynnwood purchasing their first home, understanding how down payment strategies interact with DTI requirements helps structure optimal loan scenarios.

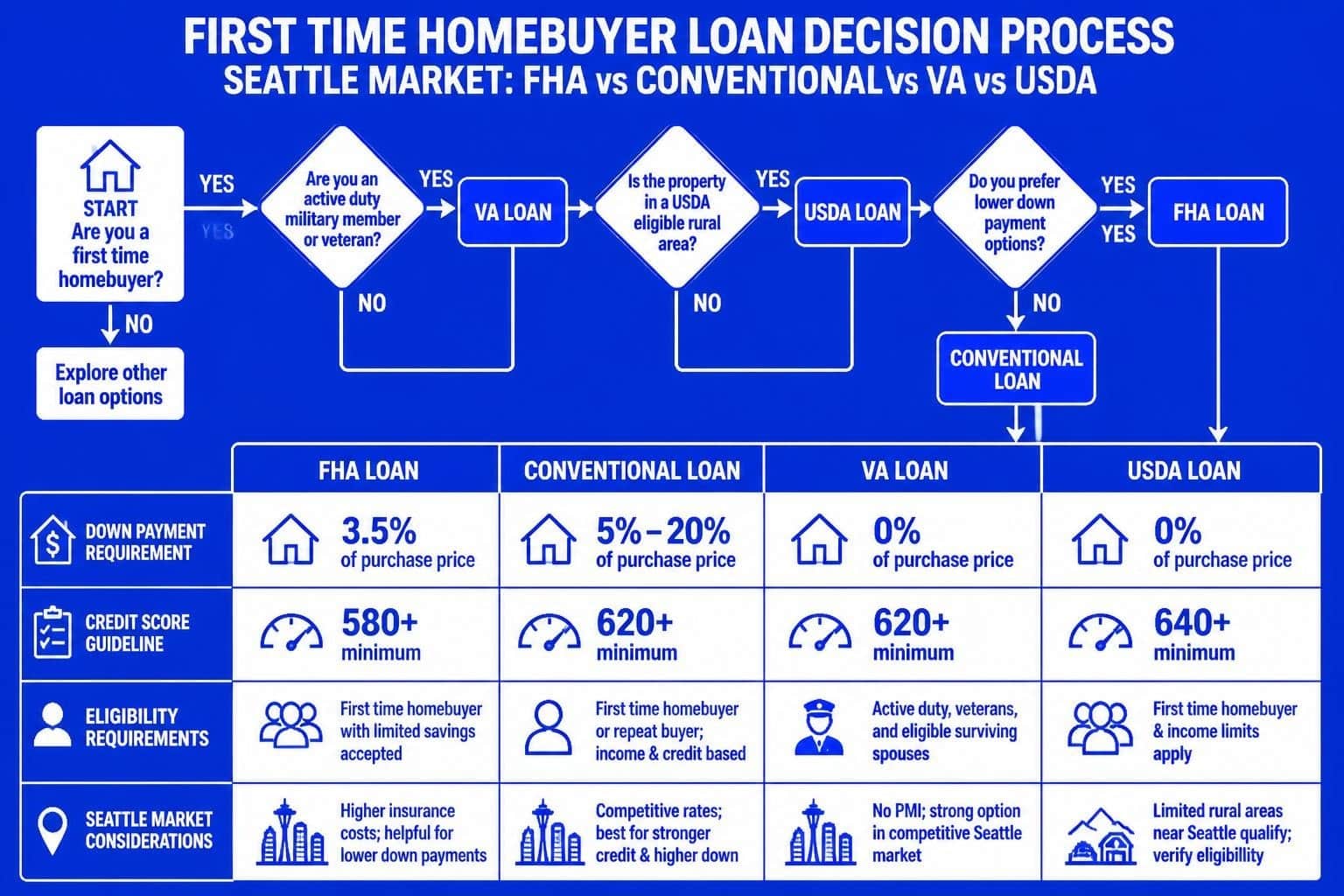

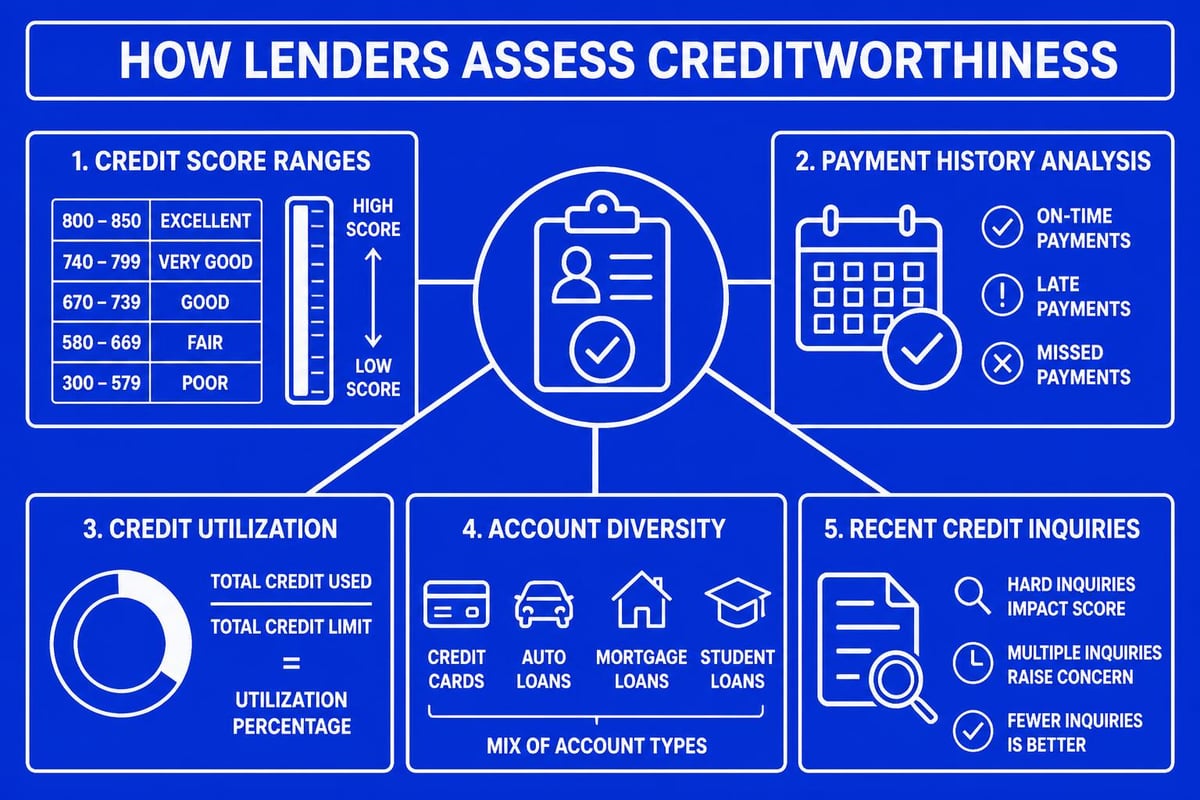

Credit Score Requirements and Nuances

While DTI measures capacity, credit scores indicate willingness to repay based on historical behavior. Different loan programs maintain varying minimum thresholds, but higher scores unlock better terms and expanded options.

Program-Specific Score Requirements

| Loan Type | Minimum Score | Ideal Score | Notes |

|---|---|---|---|

| Conventional | 620 | 740+ | Best rates require 760+ |

| FHA | 580 | 640+ | 500-579 requires 10% down |

| VA | No minimum | 620+ | Lender overlays typically require 580-620 |

| Jumbo | 680-700 | 740+ | Higher scores essential for competitive rates |

| USDA | 640 | 680+ | Automated underwriting preference at 640+ |

Seattle's high home values mean many buyers need jumbo financing, where credit standards tighten significantly. Scores below 720 may face rate adjustments or require larger down payments.

Beyond the Number: What Your Report Reveals

Underwriters examine your full credit report, not just the three-digit score. They evaluate:

- Payment history depth: 12-24 months of positive payment patterns carry significant weight

- Credit mix diversity: Revolving and installment accounts demonstrate broader experience

- Utilization percentages: Keeping balances below 30% of limits shows responsible management

- Recent inquiry patterns: Multiple applications suggest financial stress or rate shopping

- Derogatory event proximity: Recent late payments concern underwriters more than older issues

Understanding what credit score you need to buy a home in Seattle helps set realistic expectations and guides improvement efforts when necessary.

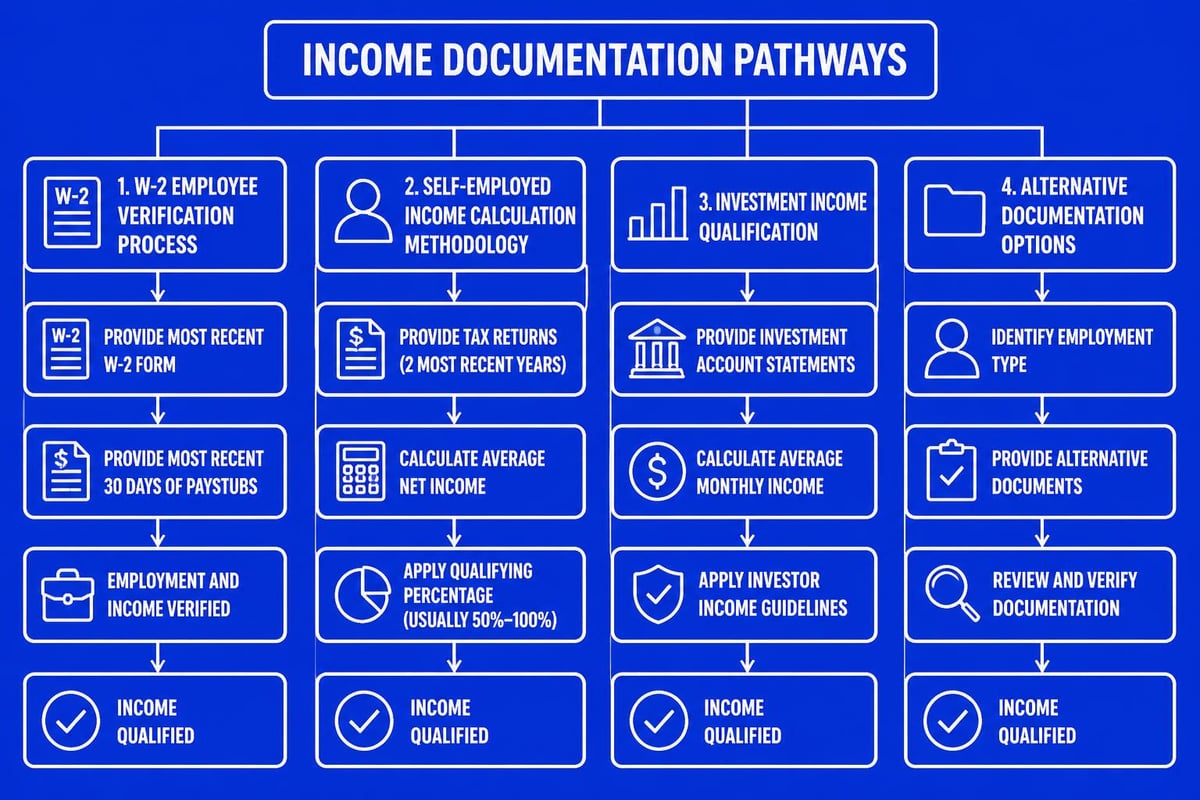

Income Documentation for Different Employment Types

Loan approval hinges on proving stable, reliable income that supports the proposed mortgage payment. Documentation requirements vary significantly based on how you earn.

W-2 Employees: The Straightforward Path

Traditional employees follow relatively simple verification processes:

- Two years of W-2 forms showing consistent employment

- Recent pay stubs covering the most recent 30 days

- Verbal or written employer verification confirming continued employment

- Year-to-date earnings matching projected annual income

Gaps in employment require explanation letters addressing reasons and demonstrating current stability. Seattle tech workers changing employers should understand how job transitions impact approval, particularly during the application process.

Self-Employed Borrowers: Complex but Achievable

Business owners and independent contractors face additional scrutiny during loan approval. Lenders typically require:

- Two years of complete tax returns (1040s with all schedules)

- Business tax returns (1065, 1120, or 1120S) if applicable

- Year-to-date profit and loss statement

- Current business license verification

- CPA letter confirming continued operations

Income calculation methodology:

Self-employed income gets averaged over 24 months after adding back non-cash deductions like depreciation. Declining income trends create challenges, while increasing patterns strengthen applications. Many business owners in Mill Creek and Everett discover their tax-minimization strategies reduce qualifying income, requiring strategic planning before purchase.

Commission, Bonus, and Variable Income

Sales professionals, consultants, and employees with performance-based compensation need minimum two-year histories for income consideration. Lenders average earnings over 24 months and may discount or exclude income showing decline.

Maximizing variable income qualification:

- Maintain detailed documentation of commission structures and payment schedules

- Provide employment letters confirming continuation of compensation plans

- Show consistent or increasing earnings patterns across multiple years

- Separate guaranteed base salary from variable components for calculation clarity

The factors lenders evaluate for approval extend beyond simple income totals to stability and continuity probability.

Asset Requirements Beyond Down Payment

Loan approval requires demonstrating not just ability to cover the down payment, but sufficient reserves for unexpected expenses or income disruptions.

Reserve Requirements by Loan Type

Reserves represent months of housing payments held in liquid accounts after closing. Requirements vary:

- Primary residence conventional: Typically 2-6 months based on down payment and credit

- Second homes: Usually 6 months minimum

- Investment properties: Often 6-12 months depending on portfolio size

- Jumbo loans: Commonly 6-12 months, increasing with loan amount

- FHA and VA: Generally no reserves required for primary residences

Qualifying asset sources:

- Checking and savings accounts

- Stocks, bonds, and mutual funds (70-90% of value)

- Retirement accounts (60-70% of vested balance)

- Gift funds properly documented

- Proceeds from asset sales with clear paper trails

Seattle homebuyers in high-value markets should understand that jumbo loan requirements typically demand substantial reserves, especially for properties exceeding $1.5 million.

Sourcing and Seasoning Requirements

Large deposits require explanation during loan approval. Underwriters track all deposits exceeding 25-50% of monthly income, requiring documentation of sources.

Acceptable sources include:

- Regular payroll deposits matching employment verification

- Tax refunds with supporting documentation

- Sale of assets with complete transaction records

- Gift funds with proper letters and donor bank statements

- Transfers between your own verified accounts

Seasoning refers to how long funds have been in accounts. While not universally required, 60-day seasoning simplifies verification and reduces documentation requests. Strategic account management before application streamlines the approval process.

The Appraisal's Role in Final Approval

Property value directly impacts loan approval since the home serves as collateral securing the debt. Appraisals provide independent valuation protecting both borrower and lender interests.

What Appraisers Evaluate

Licensed appraisers assess multiple factors when determining market value:

- Comparable sales: Recent transactions of similar properties within one mile

- Property condition: Overall maintenance, functionality, and quality

- Location factors: School districts, proximity to amenities, neighborhood trends

- Unique features: Upgrades, views, lot characteristics affecting value

- Market conditions: Supply-demand dynamics in the specific micromarket

Seattle's diverse neighborhoods create significant valuation variations. Properties in established areas like Montlake or Capitol Hill may appraise differently than similar homes in developing submarkets despite comparable features.

When Appraisals Come In Low

Appraisal shortfalls complicate loan approval since lenders base loan amounts on the lower of purchase price or appraised value. Resolution options include:

- Renegotiate purchase price: Requesting seller reduction to appraised value

- Increase down payment: Bringing additional cash to maintain desired loan amount

- Challenge the appraisal: Providing compelling comparable sales the appraiser missed

- Request second opinion: Ordering new appraisal (if permitted by contract and lender)

- Adjust loan structure: Considering different programs with varying LTV limits

Understanding market dynamics helps buyers and sellers set realistic expectations, reducing appraisal-related delays.

Timeline Expectations and Acceleration Strategies

Standard loan approval timelines range from 30-45 days in most markets, but efficient processes and preparation can significantly compress this window.

Industry Standard vs. Optimized Processing

| Milestone | Standard Timeline | Accelerated Timeline | Key Success Factor |

|---|---|---|---|

| Pre-approval | 3-5 days | 24-48 hours | Complete documentation upfront |

| Processing | 7-14 days | 3-5 days | Responsive borrower communication |

| Underwriting | 5-10 days | 1-3 days | Clean initial submission |

| Conditional approval | 3-5 days | 24-48 hours | Immediate condition responses |

| Clear to close | 48-72 hours | 24 hours | All parties aligned |

Understanding how long it takes to get a mortgage in Seattle helps you plan purchase timelines appropriately, especially in competitive multiple-offer situations.

Borrower Actions That Accelerate Approval

Taking proactive steps dramatically reduces approval timelines:

- Organize documentation before application: Create digital folders with all required documents

- Respond to requests within hours: Treating lender requests as urgent priorities

- Avoid financial changes: Postponing job changes, large purchases, or credit applications

- Maintain communication availability: Ensuring processors can reach you quickly

- Review documents carefully: Catching errors before submission prevents revision cycles

Seattle homebuyers working with experienced mortgage professionals benefit from streamlined systems and proactive guidance that identify potential issues before they cause delays.

Common Approval Challenges and Solutions

Even well-qualified borrowers encounter obstacles during the approval process. Recognizing common issues and knowing resolution strategies prevents surprises and delays.

Employment Changes During Application

Changing jobs mid-process doesn't automatically derail loan approval, but requires careful management:

Same industry, similar position: Generally acceptable with offer letter showing comparable or higher income, start date before closing, and explanation of circumstances.

Career change or industry shift: Creates complications requiring re-evaluation of income stability and may necessitate postponing purchase until establishing work history.

Self-employment transition: Typically requires waiting period before qualifying based on business income, though some exceptions exist for professionals in licensed fields.

Transparency with your lender immediately upon considering employment changes allows strategic planning rather than crisis management.

Gift Funds and Family Assistance

Many Seattle-area buyers, particularly first-time purchasers in Lake Forest Park or Shoreline, receive down payment assistance from family members. Proper documentation ensures loan approval proceeds smoothly:

- Gift letter requirements: Signed statement confirming funds are gifts, not loans requiring repayment

- Source documentation: Bank statements from donor showing fund availability

- Transfer documentation: Clear paper trail from donor account to borrower account

- Relationship verification: Confirmation that donor is family member (requirements vary by program)

First-time buyer programs often have specific gift fund guidelines that experienced lenders navigate efficiently.

Multiple Property Ownership

Buyers with existing properties face additional scrutiny during loan approval. Underwriters verify:

- DTI calculations including all property payments and obligations

- Rental income documentation with lease agreements and tax return schedules

- Reserve requirements increase with property count

- Exit strategy if selling current residence after purchase

Investment property buyers or those relocating within the Seattle area should understand how existing mortgages impact new loan approval even when planning to sell or rent previous homes.

Special Considerations for Seattle-Area Buyers

Regional market characteristics create unique loan approval considerations for buyers in King and Snohomish counties.

High-Value Market Dynamics

Seattle's median home prices consistently exceed national averages, pushing many buyers into jumbo loan territory. This shift impacts approval through:

- Stricter credit requirements with minimum scores typically 700-720

- Larger down payment expectations, often 10-20% minimum

- Enhanced income documentation and verification protocols

- Substantial reserve requirements reflecting larger payment obligations

Understanding what qualifies as a jumbo loan in Seattle helps buyers prepare appropriately for enhanced underwriting scrutiny.

Condo Approval Complexities

Many Seattle neighborhoods feature significant condo inventory requiring additional approval layers:

Project certification requirements:

- FHA and VA loans require specific condo project approval

- Conventional financing needs warrantability review

- Master insurance policies must meet minimum coverage standards

- HOA financial health assessment including reserve funding

- Owner-occupancy ratio verification confirming investment balance

Properties in urban neighborhoods often face approval delays when condo associations lack current certifications, making working with knowledgeable lenders essential.

Tech Industry Income Optimization

Seattle's concentration of major technology employers creates opportunities for strategic income maximization during loan approval. Specialized underwriting approaches allow:

- RSU income averaging using 24-month vesting schedules

- Bonus income inclusion with two-year documented history

- Stock option valuation for exercisable, vested equity

- Sign-on bonus consideration under specific circumstances

- Relocation package treatment as verified one-time income

These specialized approaches require lenders experienced with Seattle home financing for technology professionals rather than generalist mortgage providers unfamiliar with equity compensation structures.

Choosing the Right Lending Partner

The lender you select significantly impacts your loan approval experience, timeline, and ultimate success.

Mortgage Broker vs. Direct Lender Advantages

Understanding mortgage broker versus bank differences helps you choose the optimal partnership structure:

Mortgage brokers offer:

- Access to multiple investor relationships and program options

- Ability to match specific situations with ideal loan products

- Local market expertise and relationship-based service

- Flexibility in addressing unique income or credit scenarios

Direct lenders provide:

- In-house underwriting for potentially faster decisions

- Direct control over entire approval process

- Proprietary loan programs unavailable through brokers

- Single point of contact throughout transaction

Many Seattle buyers find that experienced local brokers provide the best combination of product access, market knowledge, and personalized service.

Value of Local Market Expertise

Seattle's real estate market presents unique characteristics that local lending professionals navigate more effectively:

- Understanding neighborhood-specific appraisal challenges and comparable sales patterns

- Relationships with local processors, underwriters, and closing agents

- Familiarity with regional employment verification processes for major employers

- Knowledge of condo project approval status across different buildings

- Awareness of competitive offer strategies and timeline expectations

Working with local lenders in Seattle provides advantages that extend beyond rate comparisons to comprehensive guidance through complex transactions.

Successfully navigating loan approval requires understanding what lenders evaluate, preparing comprehensive documentation, and partnering with experienced professionals who prioritize your success. Whether you're purchasing your first home in Lake Forest Park, upgrading in Bellevue, or leveraging stock compensation for a jumbo loan in Seattle, the approval process becomes manageable with proper guidance and strategic preparation. Keith Akada and the Mortgage Reel team bring 25+ years of experience helping Seattle-area buyers and homeowners achieve their financing goals with clarity, efficiency, and proven results across every loan scenario.