Refinancing your home loan has become a strategic decision for homeowners across Seattle, Bellevue, and Redmond as loan refinance rates continue to evolve in 2026. Whether you're aiming to lower your monthly payment, access home equity, or adjust your loan term, understanding current rate trends and qualification requirements helps you make confident financial decisions. The difference between securing a competitive rate and missing an opportunity often comes down to timing, preparation, and working with an experienced professional who understands the local market dynamics affecting tech professionals and homeowners throughout the Greater Seattle area.

Understanding Loan Refinance Rates in 2026

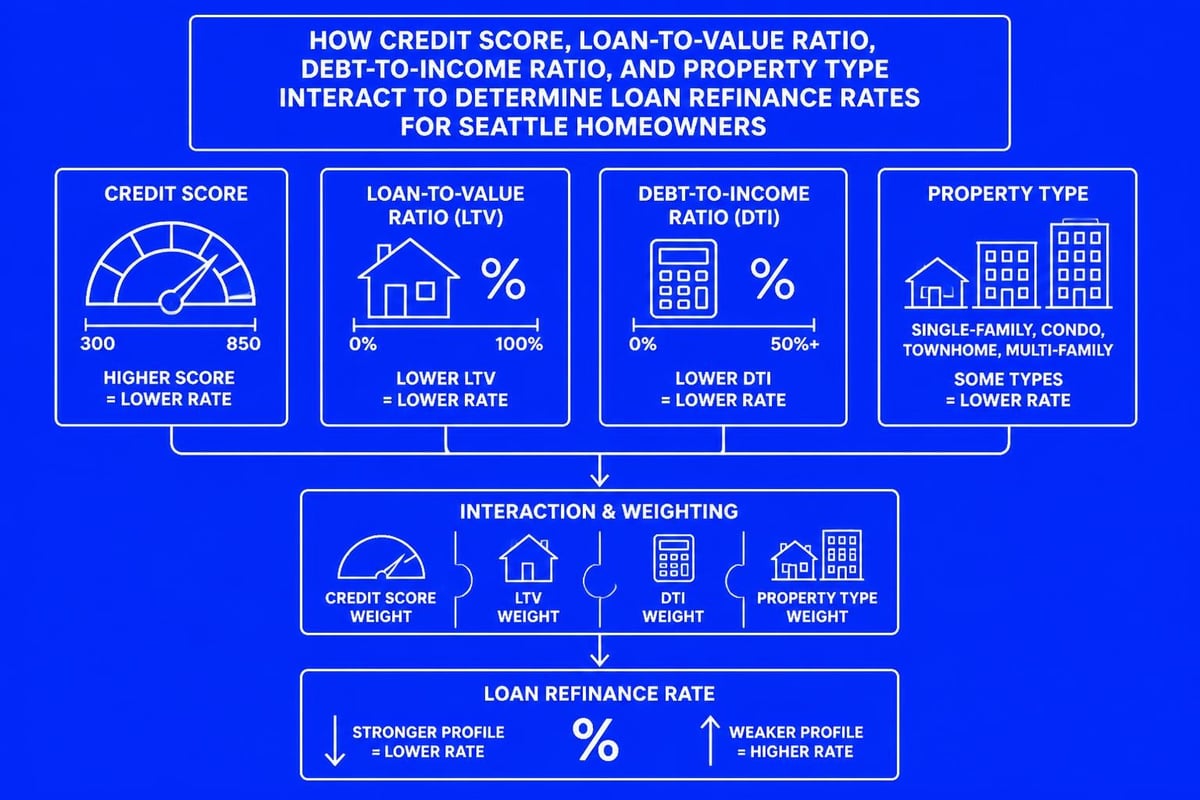

Loan refinance rates represent the interest percentage a lender charges when you replace your existing mortgage with a new one. These rates fluctuate based on Federal Reserve policies, bond market movements, and individual borrower qualifications including credit score, loan-to-value ratio, and debt-to-income ratio.

In July 2026, current refinance rates vary significantly by loan type and borrower profile. Conventional refinance rates typically run lower for borrowers with excellent credit and substantial equity, while FHA and VA refinance programs offer alternatives with different qualification standards.

Key Factors Influencing Your Rate

Multiple elements determine the loan refinance rates you'll receive from lenders:

- Credit Score: Scores above 740 typically qualify for the best rates, while scores between 680-739 receive moderate pricing adjustments

- Loan-to-Value Ratio: Keeping your LTV below 80% eliminates private mortgage insurance and often secures better rates

- Loan Amount: Jumbo loan refinancing requires larger loan amounts and may carry different rate structures than conforming loans

- Property Type: Single-family homes generally receive better rates than condos, investment properties, or multi-unit buildings

- Employment Documentation: W-2 income qualifies easily, while stock compensation and RSUs require specialized underwriting

Debt-to-income ratio plays a critical role in rate eligibility. Lenders calculate your total monthly obligations divided by gross income, with most programs preferring ratios below 43% for conventional refinancing and up to 50% for government-backed options.

When Refinancing Makes Financial Sense

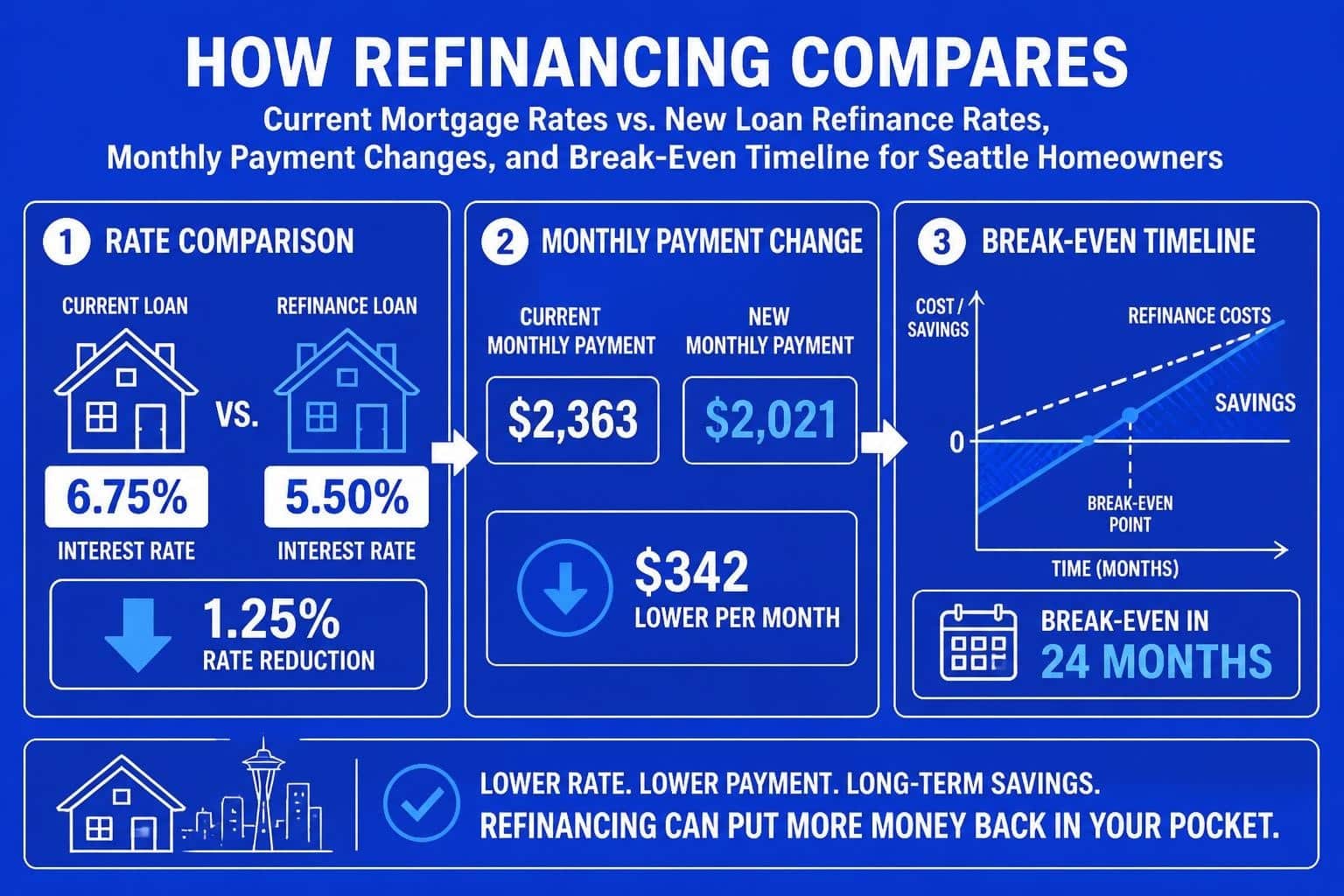

The decision to refinance extends beyond simply finding lower loan refinance rates. You must evaluate closing costs, break-even timelines, and long-term financial goals to determine if refinancing delivers genuine value.

Calculating Your Break-Even Point

Refinancing involves upfront costs typically ranging from 2% to 5% of your loan amount. These expenses include:

| Cost Category | Typical Range | Purpose |

|---|---|---|

| Appraisal Fee | $500-$800 | Property valuation |

| Title Insurance | $1,000-$2,500 | Title search and insurance |

| Origination Fee | 0%-1% of loan | Lender processing |

| Escrow/Attorney | $500-$1,200 | Closing coordination |

| Recording Fees | $100-$300 | County filing |

To calculate break-even, divide total closing costs by monthly payment savings. If refinancing costs $6,000 and saves $250 monthly, you'll break even in 24 months. Plan to stay in your Seattle, Shoreline, or Lynnwood home beyond this timeline for refinancing to make economic sense.

Rate Improvement Thresholds

Traditional guidance suggested refinancing when rates drop 1% below your current rate. Modern scenarios demand more nuanced analysis:

For rate-and-term refinancing, even a 0.50% reduction can justify the transaction if you're early in your loan term and plan extended homeownership. The Consumer Financial Protection Bureau explains mortgage refinancing considerations including how to evaluate whether your specific situation warrants moving forward.

For cash-out refinancing, comparing your new blended rate against accessing equity through a home equity line of credit provides critical context. If current loan refinance rates run significantly lower than HELOC rates, cash-out refinancing might deliver better long-term value.

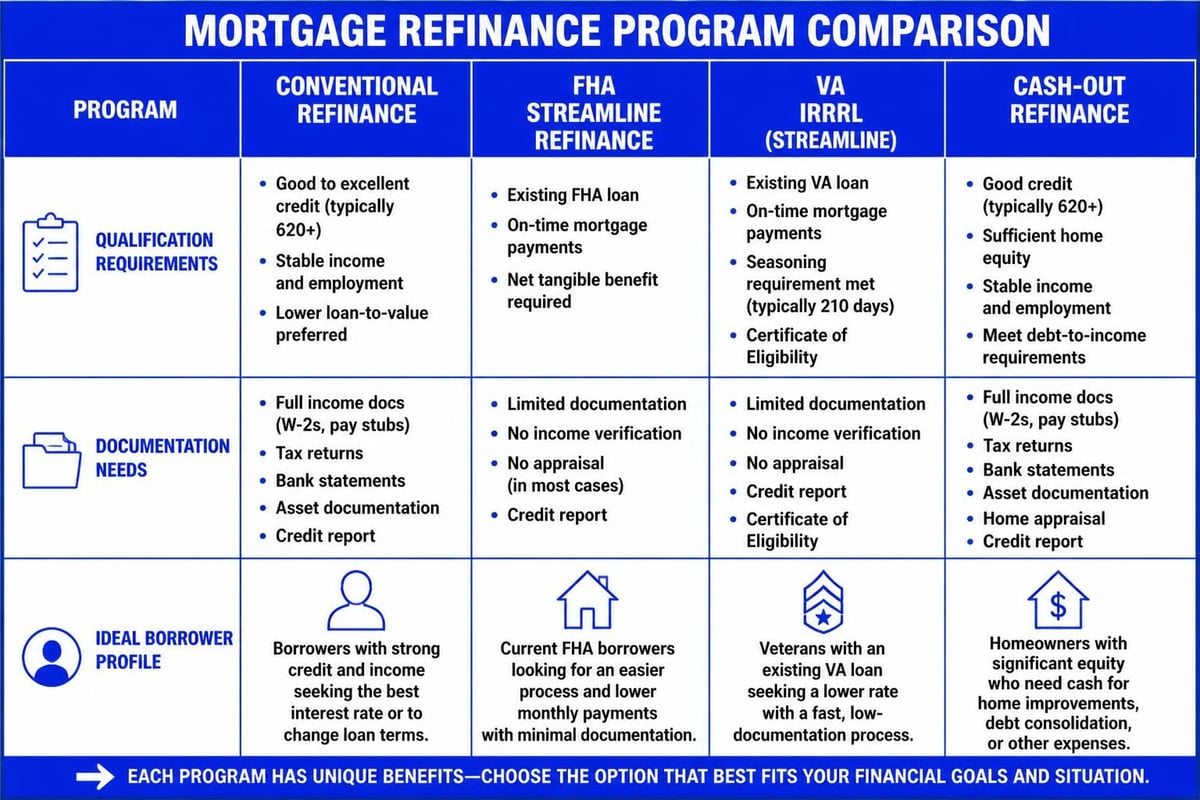

Refinance Rate Types and Program Options

Different refinance programs serve distinct homeowner objectives and qualification profiles. Understanding each option helps you match your financial strategy with the right product.

Conventional Refinance Programs

Conventional refinancing through Fannie Mae and Freddie Mac guidelines dominates the Seattle market for homeowners with strong credit and equity positions. These programs offer:

- Rate-and-term refinance: Replace your existing loan with better terms without extracting equity

- Cash-out refinance: Access up to 80% of your home's value while refinancing

- High-balance loans: Serve the Seattle, Bellevue, and Redmond markets where conforming limits reach $1,209,750 in 2026

- Streamlined documentation: Reduced paperwork for straightforward income scenarios

Tech professionals at Amazon, Microsoft, and Google frequently leverage conventional refinancing to capitalize on stock compensation and RSU income for jumbo refinancing scenarios exceeding conforming limits.

Government-Backed Refinance Options

Government programs provide alternatives with different qualification standards:

FHA Streamline Refinance eliminates appraisal requirements and reduces documentation for existing FHA borrowers. This program works exceptionally well when loan refinance rates drop but your equity position hasn't changed significantly since purchase.

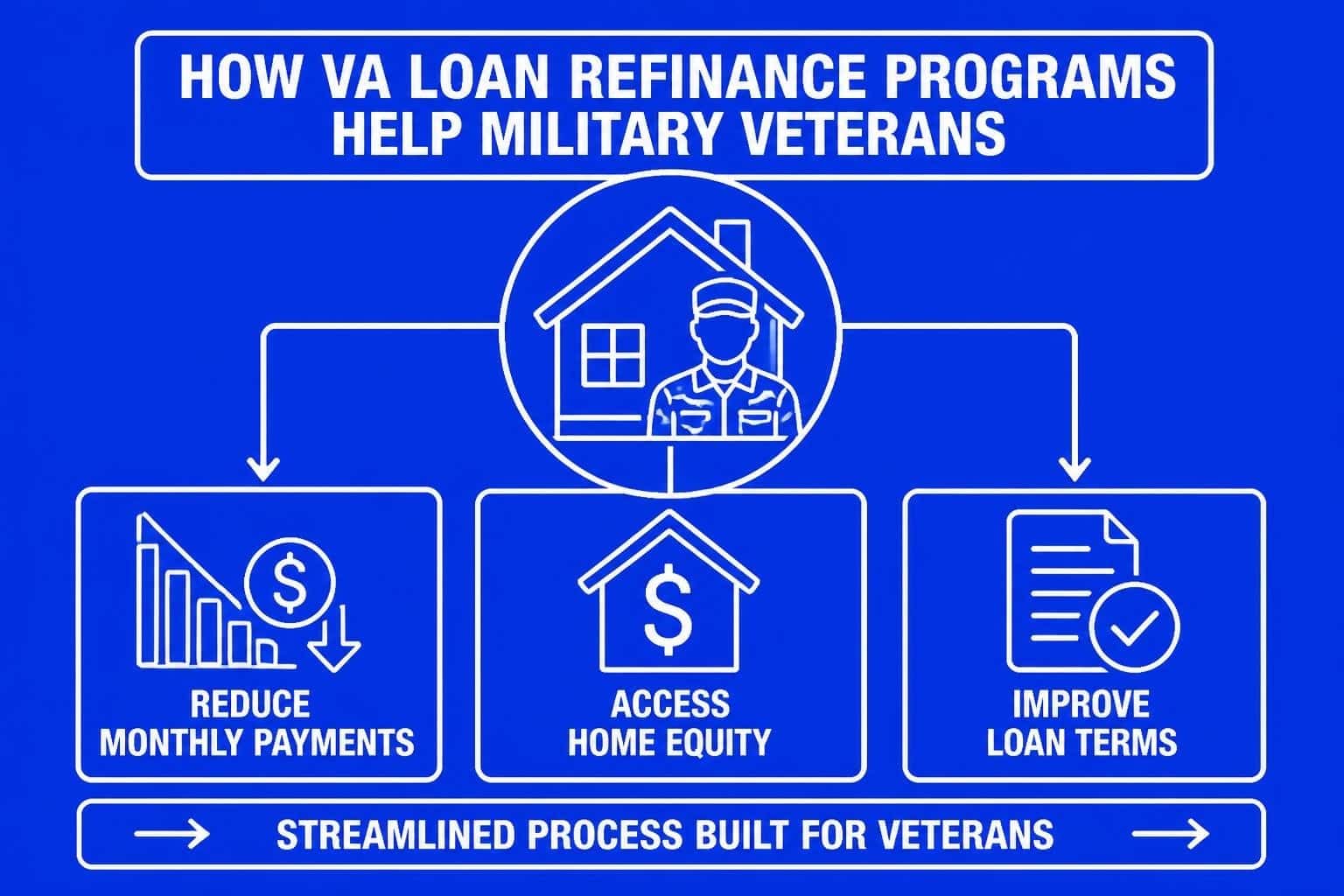

VA Interest Rate Reduction Refinance Loan (IRRRL) offers eligible veterans and service members streamlined refinancing with minimal documentation and no appraisal requirement in most cases. Lake Forest Park and Mill Creek military families often utilize this benefit.

USDA Streamline Assist serves rural and suburban homeowners in qualified areas outside Seattle's urban core, though most King County properties don't meet USDA geographic requirements.

Maximizing Your Refinance Rate in Seattle's Market

Seattle's competitive housing market demands strategic preparation to secure optimal loan refinance rates. Local market conditions, property valuations, and lender competition all influence your final rate.

Timing Your Application

Rate locks typically extend 30 to 60 days, with extensions available for additional fees. Seattle's fast-paced market often requires quick decision-making, but rushing without proper preparation costs money.

Monitor rate trends through national refinance rate reports while consulting local expertise about Pacific Northwest market conditions. Rates fluctuate based on economic data releases, Federal Reserve announcements, and bond market movements.

Consider seasonal patterns: Refinance activity typically increases in spring and summer when home purchase activity peaks. Locking rates during slower periods might provide slight advantages as lenders compete for business volume.

Credit Optimization Strategies

Three to six months before refinancing, implement credit improvement tactics:

- Pay down revolving balances below 30% utilization across all credit cards

- Avoid new credit inquiries that temporarily reduce scores

- Dispute inaccurate information on credit reports through official channels

- Maintain on-time payments across all existing obligations

- Reduce debt-to-income ratio by paying down installment loans or increasing income

Even small credit score improvements translate to better loan refinance rates. The difference between a 719 and 740 credit score often means 0.25% to 0.50% rate improvement, saving thousands over a 30-year term.

Equity Building and LTV Improvement

Higher equity positions unlock better rates and eliminate mortgage insurance requirements. For Seattle homeowners who purchased within the past few years, property appreciation has likely improved equity positions substantially.

If your original LTV exceeded 80%, request a new appraisal to capture appreciation. Everett, Shoreline, and Lynnwood neighborhoods have experienced significant value increases, potentially pushing your current LTV below key thresholds that trigger better pricing.

Private mortgage insurance removal occurs automatically at 78% LTV on conventional loans, but you can request cancellation at 80% LTV. This elimination, combined with refinanced loan refinance rates, dramatically reduces monthly payments.

Stock Compensation and Refinancing for Tech Professionals

Seattle's concentration of technology employers creates unique refinancing scenarios involving restricted stock units, stock options, and performance bonuses. Traditional underwriting often struggles with non-W-2 income, but specialized approaches unlock significant refinancing power.

Qualifying RSU and Stock Income

Lenders evaluate stock compensation differently than salary:

| Income Type | Documentation Required | Stability Period | Calculation Method |

|---|---|---|---|

| Base Salary | Recent paystubs, W-2s | Current employment | Gross annual amount |

| RSU Vesting | Vesting schedule, tax returns | 2-year history | Average of 2 years |

| Stock Options | Exercise history, company documents | 2-year history | Conservative projection |

| Bonuses | 2 years W-2 documentation | Consistent receipt | Two-year average |

Working with experienced mortgage brokers who understand technology compensation structures proves essential. Standard automated underwriting systems often misinterpret RSU income, requiring manual underwriting expertise to maximize qualifying power.

Jumbo Refinancing Considerations

Redmond, Bellevue, and Seattle homeowners frequently require jumbo refinancing exceeding conforming loan limits. These scenarios involve:

Stricter qualification standards including higher credit score requirements (typically 700+), lower maximum DTI ratios (often 43% or less), and substantial reserve requirements ranging from six to twelve months.

Competitive rate pricing varies significantly among jumbo lenders. Portfolio lenders sometimes offer superior rates compared to secondary market lenders, making thorough rate shopping essential for securing optimal loan refinance rates.

Documentation intensity increases for jumbo refinancing, particularly regarding asset verification, employment stability, and income consistency. Tech professionals should prepare comprehensive documentation packages including equity compensation agreements and vesting schedules.

Common Refinancing Mistakes to Avoid

Even experienced homeowners make costly errors when pursuing refinanced loan rates. Understanding common pitfalls helps you navigate the process successfully.

Overlooking Total Cost Analysis

Focusing exclusively on interest rate without evaluating total refinancing costs creates incomplete financial pictures. Compare:

- All-in APR reflecting fees and points, not just note rate

- Total interest paid over your expected ownership timeline

- Opportunity costs of cash used for closing versus alternative investments

- Tax implications of deductibility changes under current tax law

Some Mill Creek and Lake Forest Park homeowners benefit more from shorter-term refinancing even at slightly higher rates, paying substantially less total interest despite higher monthly payments.

Extending Loan Terms Unnecessarily

Refinancing a 25-year remaining term into a new 30-year loan reduces monthly payments but extends your debt obligation and increases total interest paid. Consider:

Refinancing into your remaining term or shorter maintains your payoff timeline while capturing lower rates. If you have 23 years remaining, refinancing into a 20-year term at lower loan refinance rates might provide ideal balance between payment savings and accelerated equity building.

Hybrid approaches combining rate reduction with term shortening optimize long-term wealth building for financially stable households.

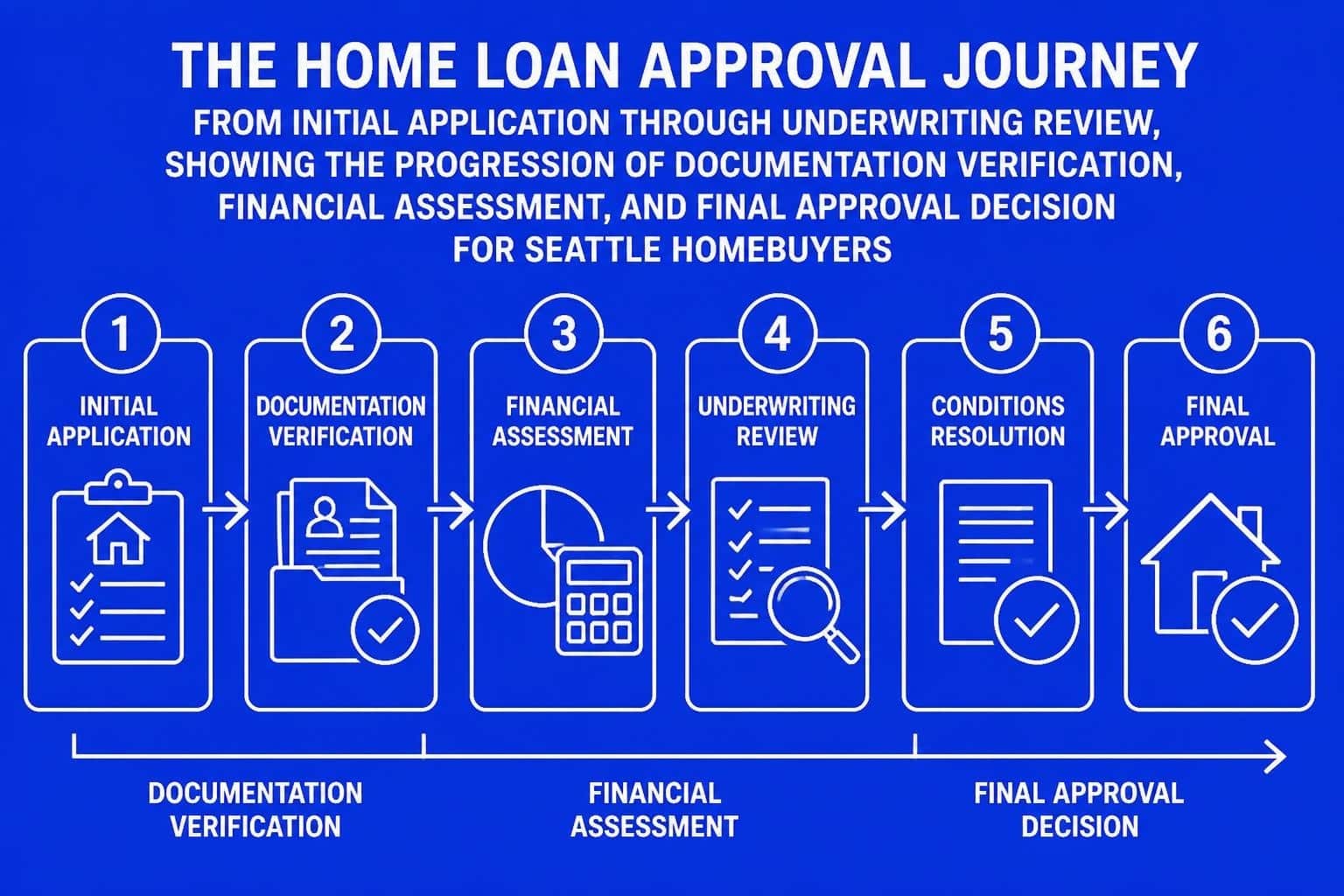

Documentation and Application Process

Streamlined refinancing requires organized documentation and clear communication with your lender. Advanced preparation accelerates approval and closing timelines.

Essential Documentation Checklist

Gather these materials before application submission:

- Income verification: Two recent paystubs, two years W-2s, two years personal tax returns (if self-employed or claiming rental income)

- Asset statements: Two months complete bank statements, investment account statements, retirement account balances

- Property information: Homeowners insurance declarations, property tax statements, HOA documentation

- Identification: Government-issued photo ID, Social Security card or verification

- Current mortgage: Recent mortgage statement showing current balance and payment amount

Tech professionals should additionally provide RSU vesting schedules, stock option agreements, and equity compensation documentation for underwriting review.

Timeline Expectations

Typical refinancing timelines in Seattle range from 30 to 45 days from application to closing, though experienced lenders with streamlined processes can close in as few as 21 days for straightforward scenarios.

Key milestones include:

- Application and initial disclosure (Day 1-3): Submit documentation and receive Loan Estimate

- Processing and underwriting (Day 4-20): Lender reviews documentation and orders appraisal

- Conditional approval (Day 15-25): Underwriter issues approval with outstanding conditions

- Clear to close (Day 25-35): All conditions satisfied, closing scheduled

- Funding and recording (Day 30-45): Transaction funds and records with county

Borrowers can expedite timelines by responding promptly to documentation requests and maintaining organized files throughout the process.

Rate Lock Strategies and Market Timing

Protecting your loan refinance rates through strategic rate locks prevents market volatility from derailing your refinancing benefits. Understanding lock mechanics and costs helps optimize this critical decision.

Lock Period Selection

Standard lock periods range from 15 to 60 days, with longer locks carrying higher costs:

- 15-day locks: Best for extremely simple refinances with all documentation ready

- 30-day locks: Standard timeline for straightforward refinancing

- 45-day locks: Accommodates complex scenarios or slower appraisal timelines

- 60-day locks: Necessary for jumbo loans or complicated underwriting situations

Seattle's active real estate market sometimes creates appraisal scheduling delays. Lock periods should account for realistic timelines rather than optimistic projections.

Float-down options allow borrowers to capture rate decreases if markets improve during your lock period, typically for an upfront fee of 0.125% to 0.25% of loan amount. This insurance makes sense when rates show downward momentum but you need to lock for qualification purposes.

Rate Renegotiation Scenarios

If rates improve significantly between application and closing, discuss renegotiation options with your lender. Some Shoreline and Lynnwood lenders offer one-time float-downs, while others require re-locking at current pricing with extended timelines.

Breaking and re-locking restarts the qualification process but might deliver substantial savings if loan refinance rates drop meaningfully. Weigh extended timelines against financial benefits carefully.

Local Market Considerations for Seattle Homeowners

Pacific Northwest housing dynamics create unique refinancing considerations compared to national markets. Understanding local factors helps Seattle, Bellevue, and Redmond homeowners make informed decisions.

Property Valuation Challenges

Seattle's diverse neighborhoods show varying appreciation patterns. Capitol Hill, Fremont, and Ballard properties often appraise above automated valuation models, while some suburban areas lag regional averages.

Appraisal gaps occur when refinance appraisals come in below expected values, potentially disrupting LTV calculations and rate pricing. Request appraisers familiar with your specific neighborhood to ensure accurate comparable selection and valuation methodology.

Condo refinancing in Seattle's downtown and Belltown markets sometimes faces additional scrutiny regarding building financial health, litigation status, and owner-occupancy ratios affecting Fannie Mae and Freddie Mac eligibility.

Tax and Insurance Implications

Washington's lack of state income tax affects tax deduction calculations for mortgage interest. The federal standard deduction at $29,200 for married couples in 2026 means many Seattle homeowners no longer itemize deductions.

Refinancing decisions should account for actual tax benefits rather than assuming full interest deductibility. Consult tax professionals about your specific situation, particularly for jumbo refinancing scenarios where interest amounts might exceed standard deduction thresholds.

Property insurance costs in Lake Forest Park and other areas near water or wooded regions sometimes increase substantially, affecting debt-to-income calculations and payment affordability analysis.

Working With Mortgage Brokers Versus Direct Lenders

Refinancing through mortgage brokers provides access to multiple lender options, while direct lenders offer single-source relationships. Understanding advantages and limitations helps you choose the right approach.

Broker Advantages for Rate Shopping

Mortgage brokers submit your scenario to multiple wholesale lenders simultaneously, comparing loan refinance rates and programs across diverse institutions. This competition often produces better pricing than single-lender shopping.

Specialized expertise proves particularly valuable for complex scenarios including stock compensation income, jumbo refinancing, or unique property types. Brokers navigate underwriting nuances across different lenders to find optimal matches.

Broker compensation through lender-paid arrangements often costs borrowers nothing additional compared to direct lending, while still providing expanded options and personalized service throughout the transaction.

Direct Lender Benefits

Large banks and credit unions offer direct refinancing with potential relationship discounts for existing customers. Chase, Bank of America, and BECU sometimes provide rate reductions for checking account holders or loan package discounts.

Streamlined servicing continues when you refinance with your current servicer, avoiding payment transfer and escrow reconciliation hassles. This convenience matters less than rate savings but provides psychological comfort for some homeowners.

Portfolio lenders keeping loans on their own books sometimes offer flexible underwriting for unusual scenarios that automated systems reject.

Preparing for Appraisal and Property Requirements

Refinance appraisals verify property value supporting your requested loan amount. Understanding appraisal processes and requirements prevents surprises during underwriting.

Appraisal Waiver Eligibility

Automated valuation models sometimes eliminate appraisal requirements for low-risk refinancing scenarios. Fannie Mae and Freddie Mac offer property inspection waivers when:

- Loan-to-value remains low (typically below 70-80%)

- Strong payment history exists on current mortgage

- Recent purchase or refinance provides current valuation data

- Property condition hasn't changed substantially

Receiving an appraisal waiver accelerates closing timelines by 7-14 days and saves $500-$800 in appraisal fees. Not all scenarios qualify, but discussing this possibility with your lender during application proves worthwhile.

Property Condition Standards

Appraisers evaluate both value and condition during refinance inspections. Significant deferred maintenance might trigger repair requirements before closing:

Health and safety issues including faulty electrical systems, plumbing leaks, or structural concerns must be addressed before most lenders fund refinancing. Cosmetic updates rarely affect approval but significant deferred maintenance can delay or prevent refinancing.

Everett and Mill Creek homeowners should address obvious property issues before scheduling appraisals to avoid conditional approval complications.

Understanding loan refinance rates and the strategic timing required to maximize refinancing benefits empowers Seattle homeowners to make confident financial decisions. Whether you're looking to reduce monthly payments, access equity for renovations, or consolidate debt, working with an experienced professional ensures you navigate current market conditions successfully. Keith Akada at Mortgage Reel brings 25+ years of expertise helping Seattle, Bellevue, Redmond, and Kirkland homeowners-including tech professionals with complex compensation structures-secure competitive refinancing that aligns with their long-term financial goals. With 750+ five-star reviews and the ability to close in as few as 9 business days, Keith provides the education, transparency, and execution you need to refinance with confidence.