Veterans and active-duty service members in Seattle, Bellevue, Redmond, and throughout the Puget Sound region have earned exceptional homeownership benefits through their military service. A va loan refinance represents one of the most powerful financial tools available to leverage your VA benefit, whether you're looking to reduce your monthly payment, access home equity, or eliminate private mortgage insurance. Understanding the specific refinance programs available, their eligibility requirements, and how they apply to the competitive Seattle housing market can save you thousands of dollars over the life of your loan. With home values continuing to appreciate across neighborhoods from Shoreline to Kirkland, refinancing your existing VA loan or converting a conventional mortgage into a VA-backed loan may unlock substantial financial advantages.

Understanding VA Loan Refinance Options

The Department of Veterans Affairs offers two distinct refinance pathways designed to serve different financial objectives. Each program carries unique benefits, eligibility requirements, and cost structures that align with specific homeowner goals.

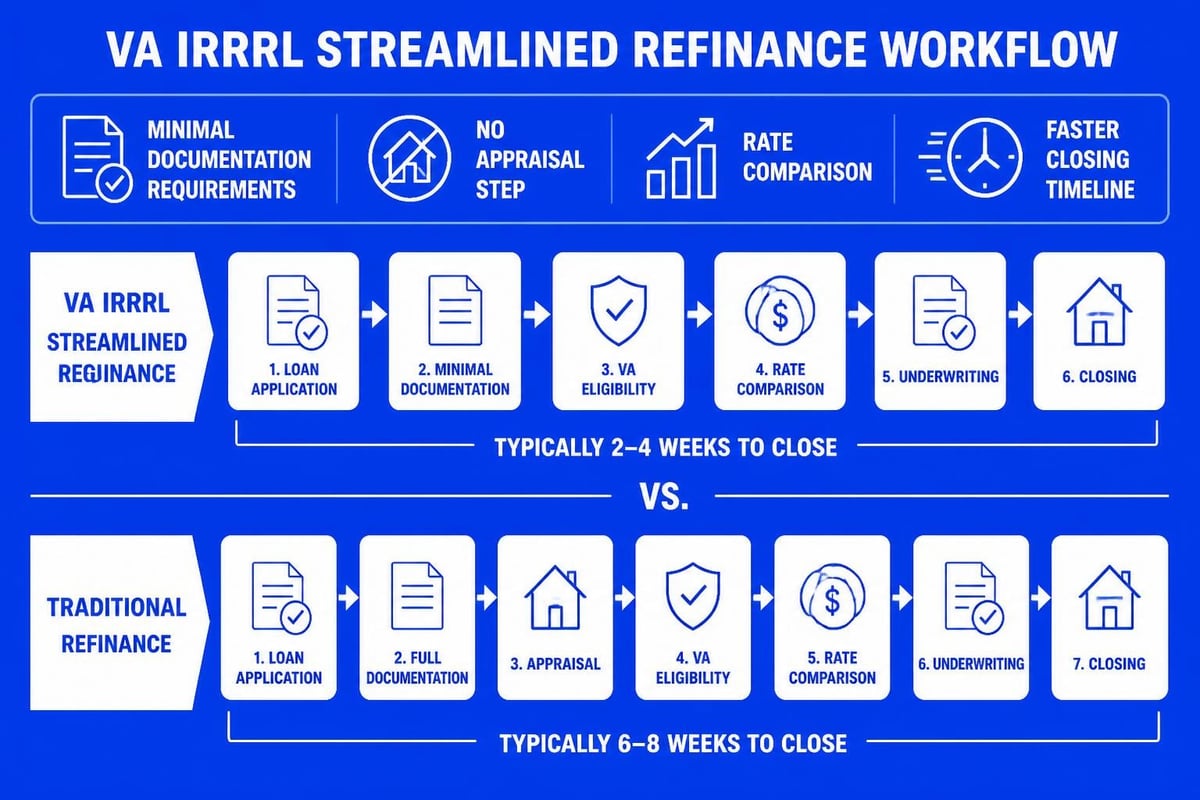

Interest Rate Reduction Refinance Loan (IRRRL)

The IRRRL program, commonly called a VA streamline refinance, delivers the fastest and most straightforward path to lowering your interest rate. This program requires minimal documentation and no appraisal in most cases, making it ideal for Seattle-area homeowners who want to capitalize on favorable rate environments without extensive paperwork.

Key features include:

- No home appraisal required in standard scenarios

- Limited income verification compared to traditional refinancing

- Ability to refinance up to 100% of your home's value

- No out-of-pocket costs if you choose to finance closing expenses

- VA funding fee of 0.5% (can be waived for disabled veterans)

The IRRRL exclusively serves borrowers with existing VA loans who want to reduce their interest rate or convert from an adjustable-rate mortgage to a fixed-rate product. This streamlined approach means you can typically close faster than conventional refinance transactions, often within 30 days.

VA Cash-Out Refinance

When you need to access the equity you've built in your Seattle-area home, the VA cash-out refinance program provides a strategic solution. This option allows you to refinance your existing mortgage (VA or conventional) and receive the difference in cash, which many homeowners use for home improvements, debt consolidation, or educational expenses.

The cash-out refinance requires more documentation than the IRRRL, including:

- Full income verification with pay stubs and tax returns

- Complete credit report review

- Professional home appraisal

- Debt-to-income ratio calculation

- Certificate of Eligibility confirmation

| Feature | IRRRL | Cash-Out Refinance |

|---|---|---|

| Appraisal Required | Usually no | Yes |

| Income Verification | Limited | Full documentation |

| Maximum Loan Amount | Current loan balance plus costs | Up to 100% of home value |

| VA Funding Fee | 0.5% | 2.3% (first use) or 3.6% (subsequent) |

| Eligible Loan Types | VA loans only | VA and conventional loans |

| Cash at Closing | No | Yes |

Tech professionals working at Amazon, Microsoft, or Google in the Seattle area often use cash-out refinancing to consolidate high-interest debt, fund home renovations that increase property value, or invest in additional real estate opportunities. The ability to leverage significant equity gains from Seattle's appreciating housing market makes this an attractive option for strategic financial planning.

Eligibility Requirements for VA Loan Refinance

Meeting the basic eligibility criteria ensures you can access va loan refinance benefits without unnecessary delays or complications. The Department of Veterans Affairs maintains specific standards that apply across all refinance programs.

Service Requirements and Certificate of Eligibility

Your military service determines your fundamental eligibility for VA loan benefits. Active-duty service members, veterans, National Guard members, reservists, and certain surviving spouses qualify under various service length requirements. You'll need to obtain or verify your Certificate of Eligibility (COE), which the VA issues electronically in most cases within minutes.

Minimum service requirements generally include:

- 90 consecutive days of active service during wartime

- 181 days of active service during peacetime

- Six years of service in the National Guard or Reserves

- Spouse of a service member who died in service or from a service-connected disability

Occupancy and Waiting Period Standards

For IRRRL refinancing, you must currently have a VA loan and have previously occupied the property as your primary residence. The VA doesn't require you to live in the home at the time of refinancing, which benefits service members who received orders to relocate from Seattle to another duty station but want to maintain their investment property.

Cash-out refinances carry stricter occupancy requirements. You must certify that you intend to occupy the property as your primary residence, and you cannot complete a cash-out refinance sooner than 210 days after closing your original loan. This waiting period prevents speculative refinancing and protects the program's integrity.

Credit and Income Considerations

While the VA doesn't impose minimum credit score requirements, most lenders establish overlays between 580 and 620 for IRRRL transactions and 620 to 640 for cash-out refinances. Your debt-to-income ratio should generally remain below 41%, though compensating factors like significant residual income or substantial assets can support approval with higher ratios.

For Seattle mortgage financing, understanding how lenders evaluate restricted stock units, performance bonuses, and stock compensation becomes essential for tech industry professionals. Proper documentation of these income sources maximizes your qualifying power and may support larger loan amounts.

Financial Benefits of VA Loan Refinance

Strategic refinancing delivers measurable financial advantages that compound over time, particularly in high-cost housing markets like Seattle, Bellevue, and Redmond where home values and loan amounts exceed national averages.

Interest Rate Reduction Impact

Reducing your interest rate by even 0.5% on a $600,000 mortgage (common for Seattle-area homes) generates approximately $180 in monthly savings and over $64,000 in interest savings across a 30-year term. When rates drop 1% or more below your current mortgage rate, the benefits accelerate dramatically.

Many veterans don't realize they could be losing thousands on their home loan by maintaining higher interest rates when refinancing options exist. Regular rate monitoring and consultation with experienced mortgage professionals helps you identify optimal refinancing windows.

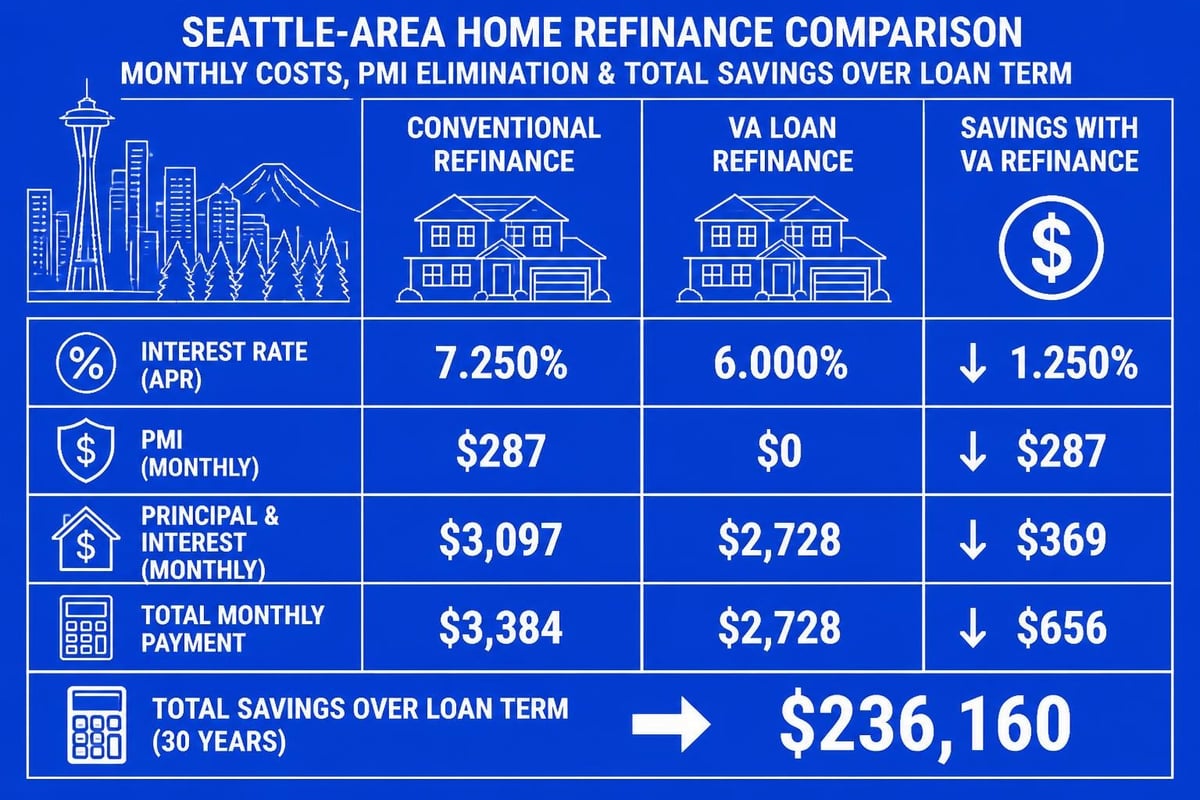

Eliminating Private Mortgage Insurance

Converting a conventional loan to a VA loan through cash-out refinancing eliminates private mortgage insurance requirements, regardless of your equity position. For borrowers paying $200 to $400 monthly in PMI on loans with less than 20% equity, this benefit alone justifies refinancing consideration.

PMI elimination advantages:

- Immediate monthly payment reduction

- No equity threshold requirement with VA loans

- Permanent removal (not temporary until reaching 20% equity)

- Increased cash flow for savings or investments

Debt Consolidation Through Cash-Out

Accessing home equity to consolidate high-interest credit card debt, auto loans, or student loans transfers expensive revolving debt into a lower-rate, tax-deductible mortgage payment. A homeowner with $40,000 in credit card debt at 18% APR pays approximately $600 monthly in interest alone, while that same amount financed into a VA loan at 6.5% costs roughly $216 monthly in interest.

This strategy works particularly well for Seattle-area homeowners who've built substantial equity through market appreciation over the past several years. Properties purchased in neighborhoods like Lake Forest Park, Mill Creek, or Lynnwood five years ago may have appreciated 30% to 50%, creating significant refinancing opportunities.

The VA Loan Refinance Process

Navigating the refinance process efficiently requires understanding each step, preparing required documentation in advance, and working with lenders experienced in VA loan processing.

Documentation Preparation

IRRRL transactions require minimal paperwork compared to traditional refinancing. You'll typically need:

- Certificate of Eligibility verification

- Current mortgage statement

- Proof of on-time mortgage payments (12 months)

- Valid identification

- Basic income verification (often limited to recent pay stubs)

Cash-out refinances demand more comprehensive documentation similar to purchase transactions, including two years of tax returns, 30 days of pay stubs, two months of bank statements, and complete asset documentation. For jumbo home mortgages common in Seattle's luxury market, additional reserves and documentation may be required.

Timeline Expectations

The streamlined IRRRL process typically closes within 30 to 45 days, though experienced lenders can achieve faster timelines when all documentation arrives promptly. Cash-out refinances generally require 45 to 60 days due to appraisal scheduling, underwriting complexity, and additional verification requirements.

Typical milestone timeline:

- Days 1-3: Application submission and initial disclosure review

- Days 4-10: Documentation collection and processing

- Days 11-20: Underwriting review and conditional approval

- Days 21-30: Appraisal completion (cash-out only) and final approval

- Days 31-35: Clear to close and closing preparation

- Day 36+: Closing and funding

Cost Considerations and Funding Fees

Understanding closing costs helps you make informed decisions about refinancing timing and options. IRRRL transactions typically cost between $2,000 and $4,000, depending on your lender's fees and state-specific charges. These costs can be financed into your loan amount, eliminating out-of-pocket expenses at closing.

| Cost Component | IRRRL | Cash-Out Refinance |

|---|---|---|

| VA Funding Fee | 0.5% of loan amount | 2.3% to 3.6% of loan amount |

| Appraisal | $0 (typically waived) | $600-$800 |

| Title Insurance | $500-$1,000 | $1,500-$2,500 |

| Origination Fees | Varies by lender | Varies by lender |

| Recording Fees | $200-$300 | $200-$300 |

Veterans with service-connected disabilities receive automatic funding fee waivers, potentially saving thousands on refinance transactions. Surviving spouses also qualify for this exemption, making VA refinancing particularly attractive for these eligible borrowers.

Common Refinancing Scenarios for Seattle Veterans

Real-world examples illustrate how different homeowners leverage va loan refinance programs to achieve specific financial objectives in the competitive Puget Sound housing market.

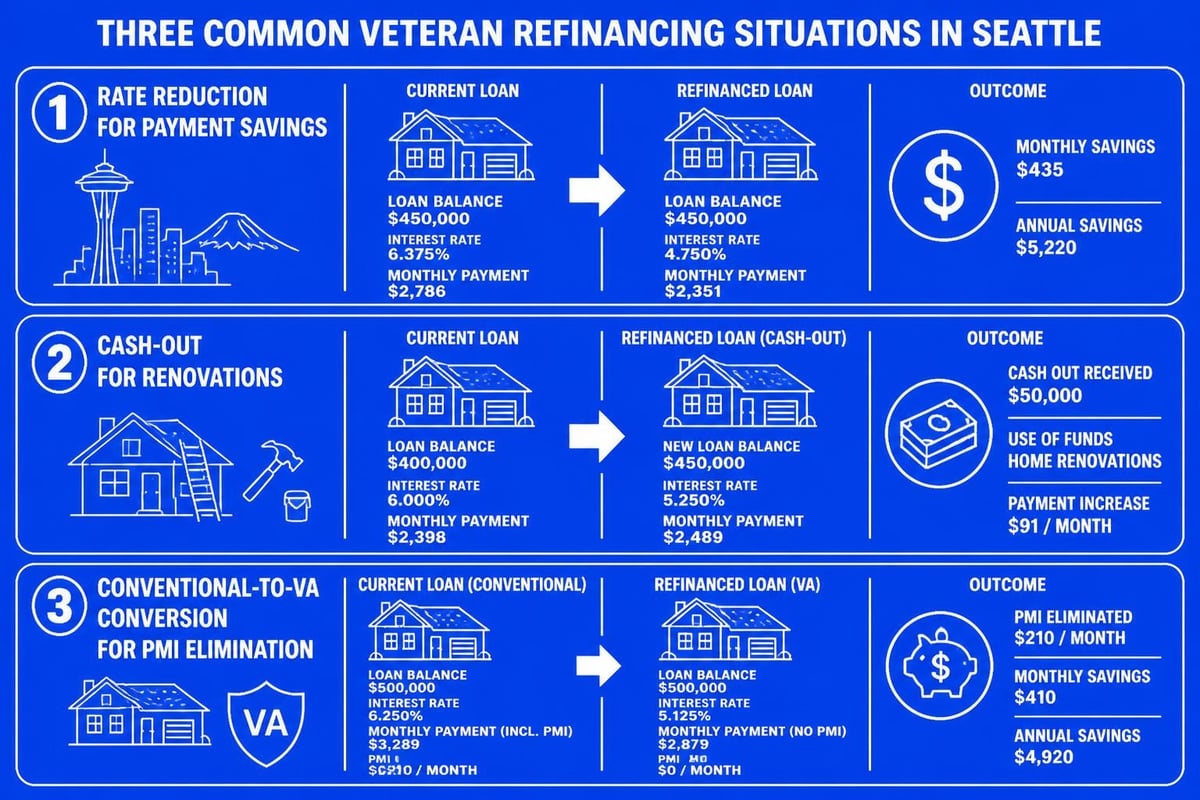

Rate and Term Refinance for Payment Reduction

A Navy veteran who purchased a home in Everett in 2021 at a 6.75% interest rate now sees available rates at 5.5%. Their current $500,000 loan balance generates a $3,245 monthly principal and interest payment. Refinancing through an IRRRL to 5.5% reduces the payment to $2,839, creating $406 in monthly savings with minimal documentation and no appraisal requirement.

Over the remaining loan term, this veteran saves approximately $146,000 in interest while maintaining the same loan balance. The $2,500 refinancing cost pays for itself in just six months of reduced payments.

Cash-Out for Home Improvement

An Air Force veteran purchased a home in Shoreline for $450,000 five years ago with a conventional loan. The property now appraises at $650,000, creating $200,000 in equity (assuming the original $360,000 loan balance is now $340,000). By completing a VA cash-out refinance at 100% loan-to-value, they access $650,000 minus the existing balance, receiving approximately $310,000 before closing costs.

They use $80,000 for a complete kitchen and bathroom renovation that further increases home value, consolidate $30,000 in credit card debt, and maintain $200,000 as reserves. The refinance also eliminates their $285 monthly PMI payment, partially offsetting the increased loan amount impact.

Conventional to VA Conversion

A Marine Corps veteran initially used a conventional loan to purchase a home in Redmond because they hadn't obtained their Certificate of Eligibility. With 15% down payment, they pay $340 monthly in PMI on their $700,000 loan. Converting to a VA cash-out refinance eliminates PMI immediately, saving $4,080 annually, and provides access to better loan terms including potentially lower interest rates.

Maximizing Your VA Loan Refinance Benefits

Strategic planning and expert guidance help you extract maximum value from your VA refinancing opportunity while avoiding common pitfalls that erode potential benefits.

Timing Your Refinance Decision

Monitor interest rate trends and your current loan's interest rate to identify optimal refinancing windows. Generally, refinancing makes financial sense when you can reduce your rate by at least 0.5% to 0.75% for IRRRL transactions, accounting for closing costs and break-even timelines. For cash-out refinances, evaluate the opportunity cost of accessing equity versus maintaining it as unrealized appreciation.

Break-even calculation factors:

- Total closing costs divided by monthly payment savings

- Expected homeownership duration after refinancing

- Opportunity cost of cash received (cash-out scenarios)

- Long-term interest cost comparison

- Impact on overall financial plan and goals

Working with experienced Seattle mortgage brokers who understand local market dynamics and VA loan nuances ensures you receive accurate break-even calculations and strategic recommendations tailored to your situation.

Understanding Lender Overlays

While the VA establishes baseline program requirements, individual lenders impose additional guidelines called overlays. These might include minimum credit scores, maximum debt-to-income ratios, or seasoning requirements beyond VA minimums. Shopping multiple lenders helps you identify the most favorable overlay environment for your specific circumstances.

Lenders experienced with tech industry compensation understand how to properly document and verify restricted stock units, employee stock purchase plans, and performance bonuses common among Seattle-area technology professionals. This expertise becomes critical when maximizing your qualifying income for larger loan amounts.

Evaluating No-Closing-Cost Options

Some lenders offer no-closing-cost refinancing by incorporating fees into a slightly higher interest rate. This approach makes sense when you plan to refinance again within a few years or when preserving cash for other purposes outweighs long-term interest costs. Calculate the rate differential's impact over your expected holding period to determine if this option aligns with your financial strategy.

VA Refinance Compared to Other Options

Understanding how va loan refinance programs compare to alternative refinancing approaches helps you select the optimal solution for your specific situation.

VA IRRRL Versus Conventional Streamline Programs

FHA and conventional loan programs offer their own streamlined refinancing options, but none match the simplicity and cost-effectiveness of the VA IRRRL. FHA streamline refinances require upfront mortgage insurance premiums and ongoing monthly mortgage insurance regardless of equity position. Conventional streamline programs typically require appraisals and more extensive documentation than IRRRLs, though they avoid funding fees.

For eligible veterans, the IRRRL consistently delivers superior value through minimal documentation, no appraisal requirements, and lower overall costs, particularly for borrowers with service-connected disabilities who receive funding fee waivers.

VA Cash-Out Versus Home Equity Loans

Accessing home equity through a VA cash-out refinance replaces your first mortgage with a new, larger loan at current market rates. Home equity loans and home equity lines of credit (HELOCs) create second liens behind your existing mortgage, typically at higher interest rates but without disturbing your current first mortgage terms.

| Factor | VA Cash-Out Refinance | Home Equity Loan/HELOC |

|---|---|---|

| Interest Rate | First mortgage rates | Higher than first mortgage |

| Loan Structure | Replaces existing loan | Second lien position |

| Closing Costs | Full refinance costs | Lower than refinance |

| PMI Impact | Eliminates PMI | No impact on PMI |

| Tax Deductibility | Interest may be deductible | Interest may be deductible |

When current mortgage rates equal or exceed your existing rate, maintaining that rate through a home equity product may prove more cost-effective than refinancing. Conversely, when rates have dropped or you're paying PMI, the VA cash-out refinance typically delivers better overall value.

Working with VA-Experienced Mortgage Professionals

The complexity of VA loan guidelines, combined with Seattle's competitive housing market and unique income documentation requirements for tech professionals, demands working with mortgage professionals who bring specific expertise to these transactions.

Qualifications to Seek in Your Lender

Identify lenders and loan officers with demonstrated VA loan experience, measured by annual transaction volume and specific knowledge of VA guidelines. Ask about their familiarity with IRRRL and cash-out refinance programs, typical processing timelines, and relationships with VA-approved appraisers in your area.

For first-time home buyers transitioning from rental to ownership, or experienced homeowners considering refinancing, understanding the lender's communication style, responsiveness, and ability to explain complex concepts in accessible language contributes significantly to a positive experience.

Local Market Knowledge Benefits

Mortgage professionals serving the Greater Seattle area understand regional property value trends, neighborhood-specific appreciation patterns, and local economic factors affecting home values. This knowledge becomes particularly valuable during the appraisal process for cash-out refinances, where supporting comparable sales data and market trend analysis may influence appraised values.

Lenders familiar with Lynnwood, Mill Creek, Lake Forest Park, and Everett submarkets can provide realistic expectations about equity positions, refinancing opportunities, and timing considerations based on local market cycles. This localized expertise complements broader VA loan knowledge to deliver optimal refinancing outcomes.

Technology and Streamlined Processing

Advanced lenders leverage technology platforms that simplify documentation submission, provide real-time status updates, and accelerate processing timelines. Digital verification of income, assets, and employment reduces paperwork burdens while maintaining compliance with VA and investor requirements. These capabilities become especially valuable for busy professionals managing demanding careers while navigating refinancing transactions.

Avoiding Common VA Refinance Mistakes

Even experienced homeowners make errors during refinancing that increase costs, delay closing, or reduce overall benefits. Awareness of common pitfalls helps you navigate the process more effectively.

Failing to Compare Multiple Lenders

Interest rates and closing costs vary significantly across lenders, even for identical VA loan programs. Obtaining written loan estimates from at least three lenders ensures competitive pricing and prevents leaving thousands of dollars on the table through inadequate comparison shopping. Focus on the annual percentage rate (APR) and total closing costs rather than interest rate alone, as fees significantly impact overall value.

Ignoring the Breakeven Timeline

Refinancing makes financial sense only when you'll recover closing costs through monthly savings before selling or refinancing again. Calculate your breakeven period by dividing total closing costs by monthly payment reduction. If you plan to sell within two years, a $4,000 refinance cost requires at least $167 monthly savings to break even, potentially making the transaction uneconomical.

Overlooking Funding Fee Exemptions

Veterans with service-connected disabilities qualify for complete funding fee waivers, saving 0.5% to 3.6% of the loan amount depending on the program. Surviving spouses also receive this exemption. Failing to document your disability rating with the VA results in unnecessary costs that reduce refinancing benefits. Submit your disability documentation early in the process to ensure proper fee waivers.

Misunderstanding Cash-Out Seasoning Requirements

The VA requires 210 days of ownership before completing a cash-out refinance on your current property. Attempting to refinance sooner results in automatic denial and wasted time. Plan your refinancing timeline accordingly, particularly if you need to access equity for time-sensitive purposes like debt consolidation before interest capitalizes or home improvement projects with seasonal considerations.

VA loan refinancing offers Seattle-area veterans powerful opportunities to reduce costs, access equity, and optimize their housing finances through specialized programs designed exclusively for their benefit. Whether you're pursuing an IRRRL for rate reduction or a cash-out refinance for equity access, understanding program requirements, costs, and strategic timing maximizes your financial outcomes. Keith Akada and the Mortgage Reel team bring 25+ years of specialized experience helping veterans and active-duty service members across Seattle, Bellevue, Redmond, and Kirkland navigate VA refinancing with clarity and confidence, backed by 750+ five-star reviews and expertise in qualifying complex compensation structures common among local tech professionals. Connect with Mortgage Reel today to explore your VA loan refinance options and develop a customized strategy that aligns with your financial goals.