Purchasing your first home represents one of the most significant financial decisions you'll make in your lifetime. For many Seattle-area residents, navigating the complexities of a first time mortgage can feel overwhelming, particularly in competitive markets like Bellevue, Redmond, and Kirkland where home prices continue to challenge buyer budgets. Understanding your options, preparing financially, and working with experienced professionals transforms this challenge into an achievable milestone. Whether you're a tech professional with stock compensation or a traditional W-2 employee, the right mortgage strategy positions you for long-term success.

Understanding First Time Mortgage Options in Seattle

The Seattle housing market presents unique challenges that demand strategic mortgage selection. Your first time mortgage choice impacts monthly payments, total interest costs, and even your ability to compete in multiple-offer situations.

Conventional Loans for First-Time Buyers

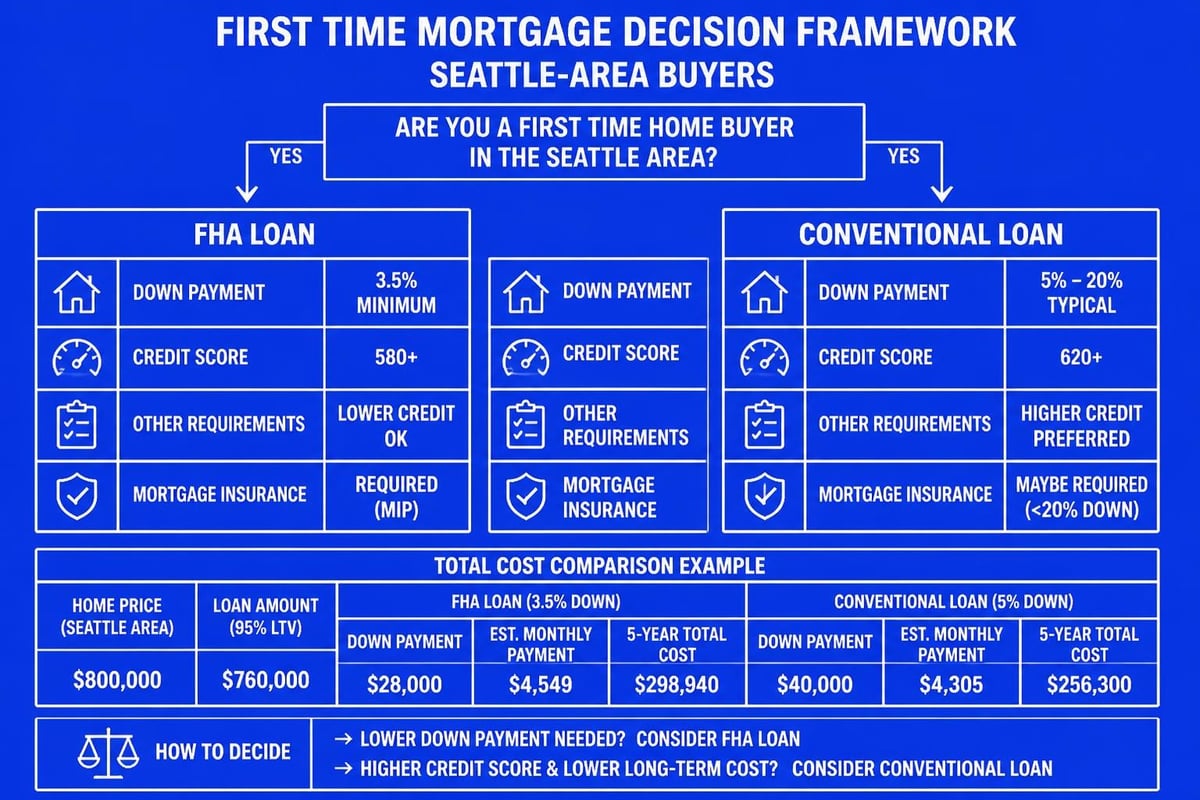

Conventional mortgages remain the most popular choice for buyers with solid credit and stable income. These loans require as little as 3% down for qualified first-time buyers, making homeownership accessible without draining savings accounts.

Key advantages include:

- Lower overall costs compared to government-backed loans when you have strong credit

- Removal of mortgage insurance once you reach 20% equity

- Flexible property type options including condos common in Seattle's urban neighborhoods

- Competitive interest rates for borrowers with 700+ credit scores

For Shoreline and Lynnwood buyers seeking more affordable entry points, conventional loan options provide the flexibility to start with minimal down payment while building equity quickly in appreciating markets.

FHA Loans: Lower Down Payment Requirements

Federal Housing Administration loans serve buyers who need lower down payment thresholds or have credit scores in the 580-650 range. With just 3.5% down, FHA financing opens doors that conventional loans might keep closed.

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Down Payment | 3.5% | 3% (first-time buyers) |

| Credit Score Requirement | 580+ | 620+ (typically) |

| Mortgage Insurance | Required for loan life (if <10% down) | Removable at 20% equity |

| Loan Limits (Seattle 2026) | $498,257 | $766,550 |

However, FHA loans carry mortgage insurance premiums for the life of the loan when you put down less than 10%, increasing long-term costs. This trade-off deserves careful consideration alongside your financial timeline.

VA and USDA Loan Alternatives

Veterans and active military members in the Seattle area benefit from VA loans offering zero down payment and no mortgage insurance. These loans represent exceptional value for qualified borrowers, particularly given King County's high home prices.

USDA loans serve buyers in eligible rural areas surrounding Seattle, including portions of Everett and outer Snohomish County. While these programs offer 100% financing, property location restrictions limit applicability in core Seattle markets.

Calculating What You Can Afford

Financial preparation separates successful first-time buyers from those who struggle through the process. Understanding the true costs of homeownership extends beyond your monthly mortgage payment.

The 28/36 Rule and Debt-to-Income Ratios

Lenders evaluate your ability to repay using debt-to-income ratios (DTI). Most conventional loans require:

- Front-end ratio of 28% or less (housing expenses divided by gross monthly income)

- Back-end ratio of 36% or less (all monthly debt payments divided by gross income)

- Compensating factors that may allow higher ratios with strong credit or reserves

For a Seattle tech professional earning $150,000 annually with $800 monthly student loan payments, this calculates to maximum housing costs around $3,500 monthly and total debt obligations not exceeding $4,500.

Beyond the Down Payment: Hidden Costs

First-time buyers often underestimate the capital required beyond the down payment itself. Plan for these essential expenses:

- Closing costs ranging from 2-5% of purchase price ($12,000-$30,000 on a $600,000 Lake Forest Park home)

- Property tax reserves (approximately $6,000 annually for median Seattle properties)

- Homeowners insurance ($1,200-$2,000 yearly depending on coverage)

- HOA fees common in Seattle condos ($300-$800 monthly)

- Inspection and appraisal fees ($800-$1,500 combined)

Many first-time mortgage loan programs offer down payment assistance or closing cost credits to offset these requirements, particularly for buyers in Mill Creek and other growing communities.

Building Your Financial Foundation

Strong mortgage applications begin long before you start house hunting. Strategic preparation positions you for better rates and stronger negotiating power.

Credit Score Optimization Strategies

Your credit score directly influences your interest rate, which compounds into tens of thousands of dollars over a 30-year mortgage. A 680 score versus 760 might cost you an additional $50,000 in interest on a $500,000 loan.

Improve your credit profile by:

- Paying all bills on time for at least 12 months before applying

- Reducing credit card balances below 30% of limits

- Avoiding new credit inquiries six months before mortgage application

- Correcting errors on credit reports from all three bureaus

- Maintaining older credit accounts to preserve credit history length

For comprehensive guidance, Bankrate’s first-time homebuyer tips offer additional strategies for credit improvement and financial preparation.

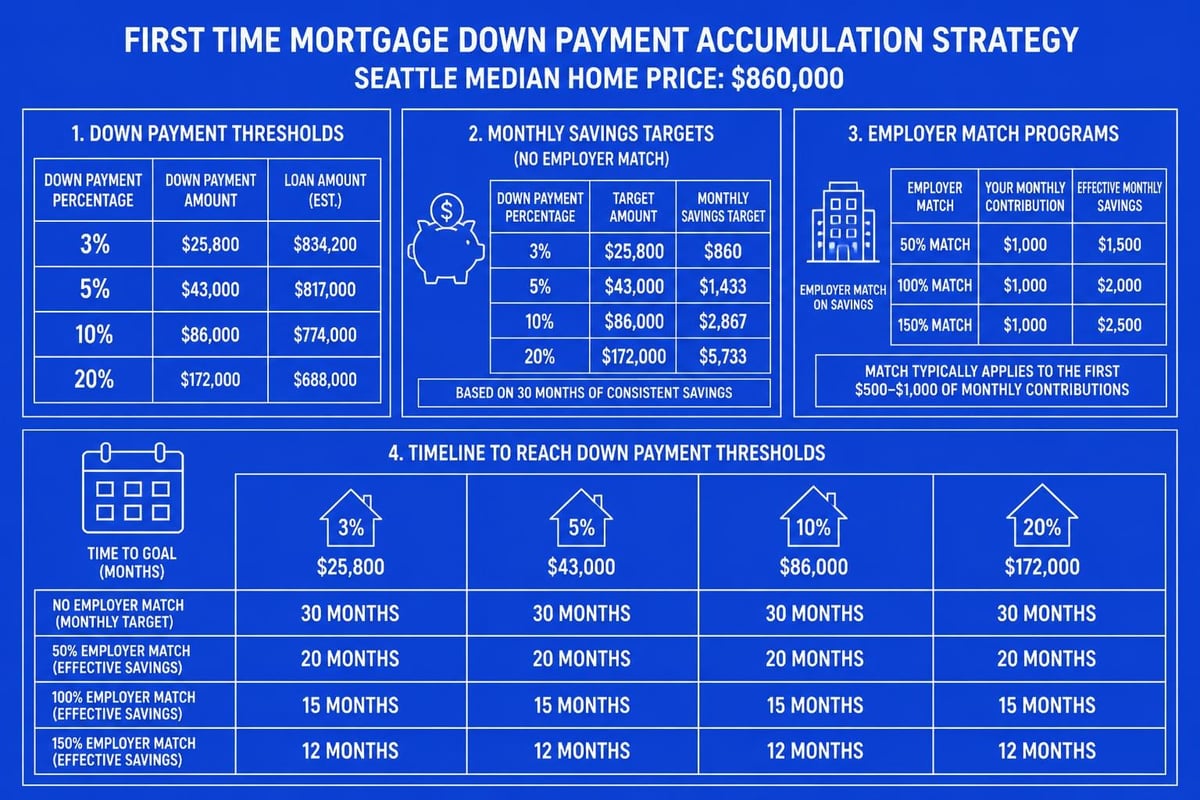

Saving for Your Down Payment

Down payment size affects both your monthly payment and overall loan costs. While low down payment programs exist, larger down payments reduce monthly obligations and eliminate mortgage insurance faster.

Consider these savings strategies:

- Automatic transfers to dedicated savings accounts prevent spending drift

- First-time buyer programs through Washington State Housing Finance Commission

- Gift funds from family members (properly documented for lender requirements)

- Retirement account loans (with careful consideration of long-term impacts)

- Employer assistance programs increasingly common at Seattle tech companies

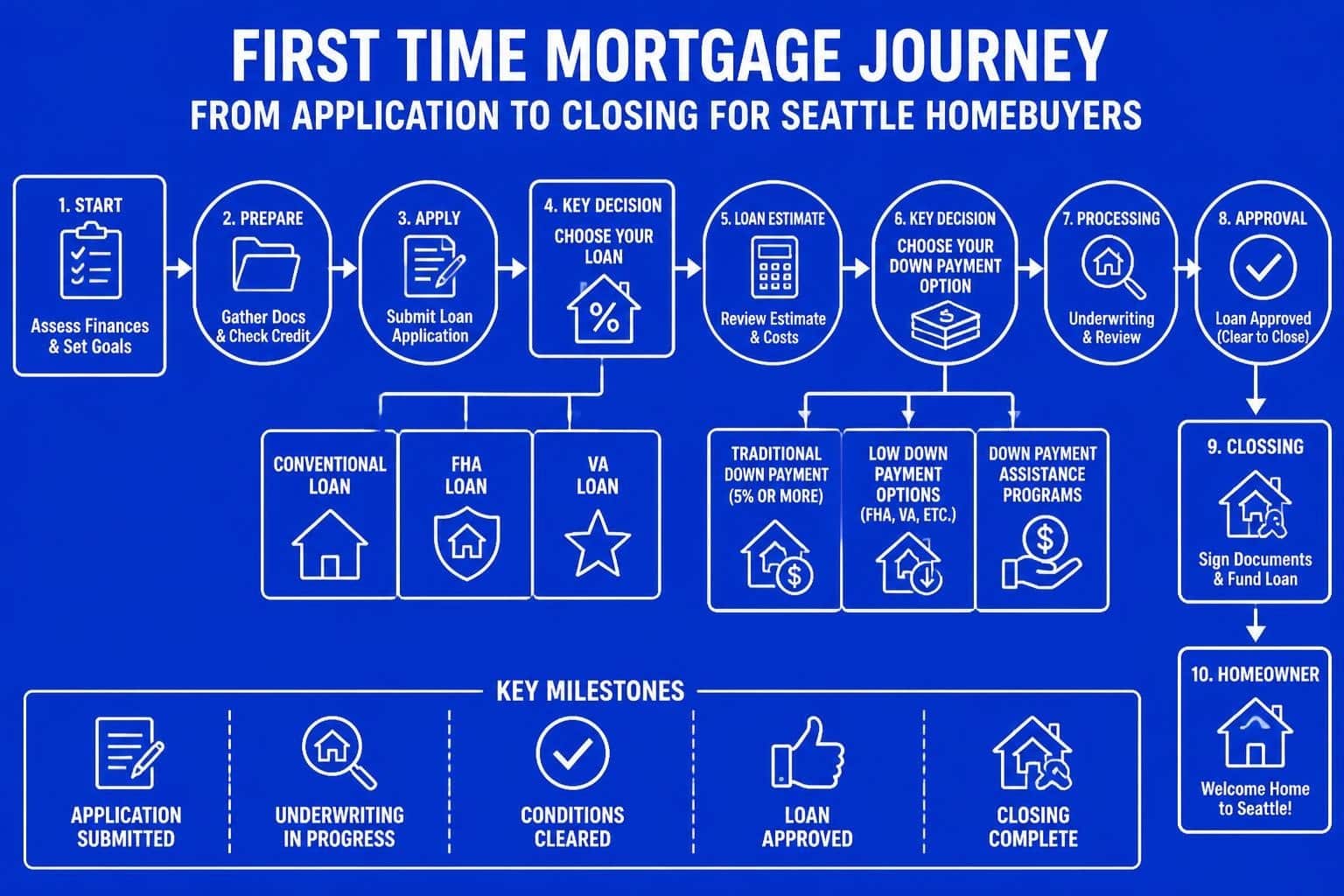

Navigating the Pre-Approval Process

Pre-approval distinguishes serious buyers from window shoppers in competitive Seattle neighborhoods. This credential proves your financing ability before you make offers.

Documentation Requirements

Expect to provide comprehensive financial documentation including:

| Document Type | Specific Requirements |

|---|---|

| Income Verification | 2 years W-2s, recent pay stubs, tax returns |

| Asset Verification | 2-3 months bank statements, investment accounts |

| Employment Confirmation | Direct lender contact with HR department |

| Credit Authorization | Consent for credit report and score review |

| Identification | Government-issued photo ID, Social Security card |

For tech professionals with stock compensation, qualifying RSUs and bonus income requires additional documentation showing vesting schedules and historical award patterns.

Pre-Approval vs Pre-Qualification

These terms are not interchangeable. Pre-qualification provides rough estimates based on self-reported information. Pre-approval involves complete underwriting review of verified documents, offering concrete borrowing limits and demonstrating credibility to sellers.

In Bellevue's competitive market where homes receive multiple offers, pre-approval letters from trusted Seattle mortgage brokers carry significant weight with listing agents and sellers.

Strategic Considerations for Seattle Tech Professionals

Amazon, Microsoft, and Google employees face unique mortgage qualification challenges and opportunities related to equity compensation.

Qualifying Stock-Based Compensation

Traditional mortgage underwriting emphasizes W-2 income stability. However, restricted stock units (RSUs) and bonuses represent substantial portions of tech worker compensation packages.

Effective strategies include:

- Demonstrating two-year history of stock awards and vesting

- Averaging bonus income over 24 months for qualifying calculations

- Timing mortgage applications around vesting schedules to maximize documented income

- Working with experienced lenders familiar with tech compensation structures

This specialized knowledge separates generic lenders from those truly equipped to serve Seattle's tech workforce. Understanding how to properly document and calculate variable income components maximizes your buying power without unnecessary limitations.

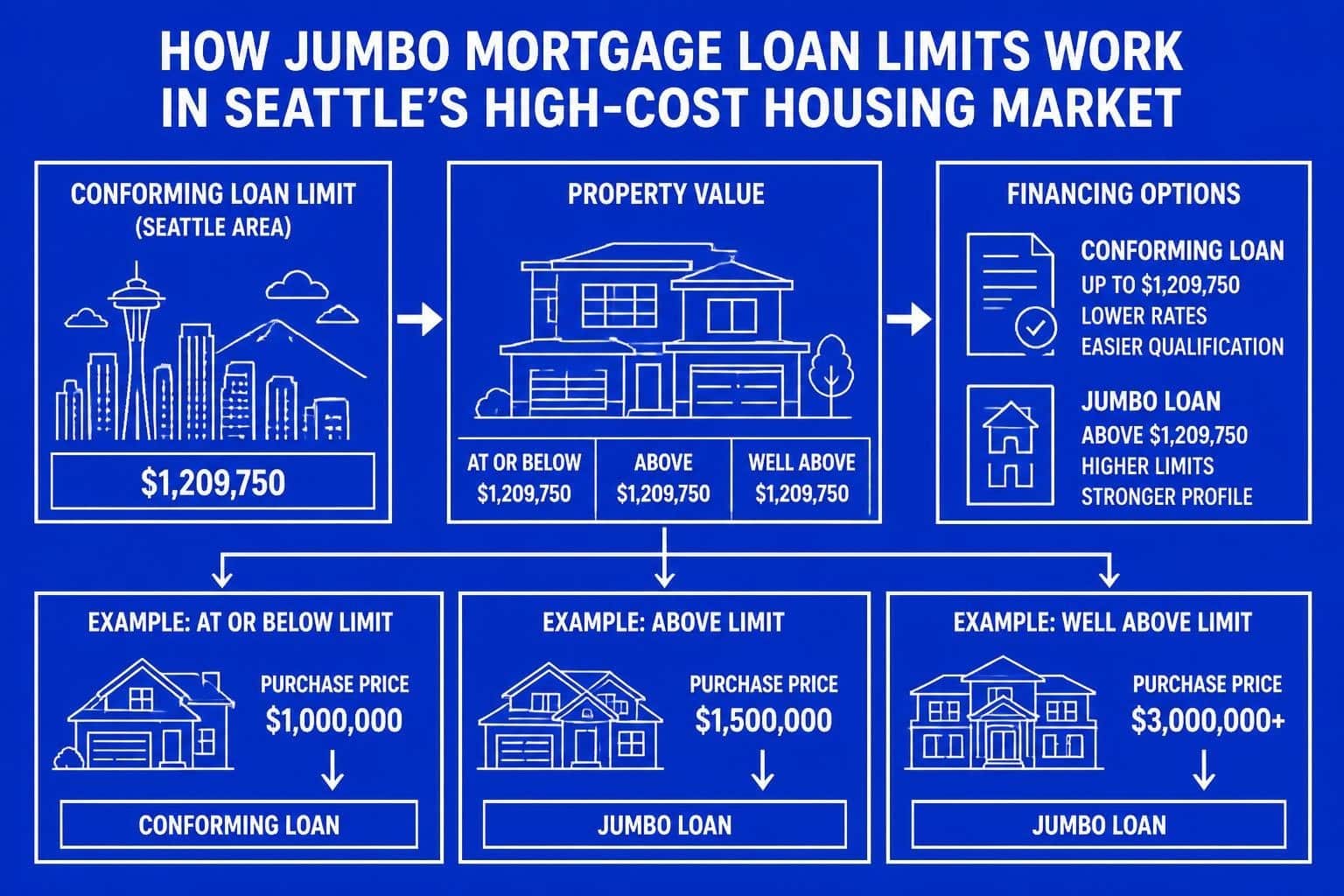

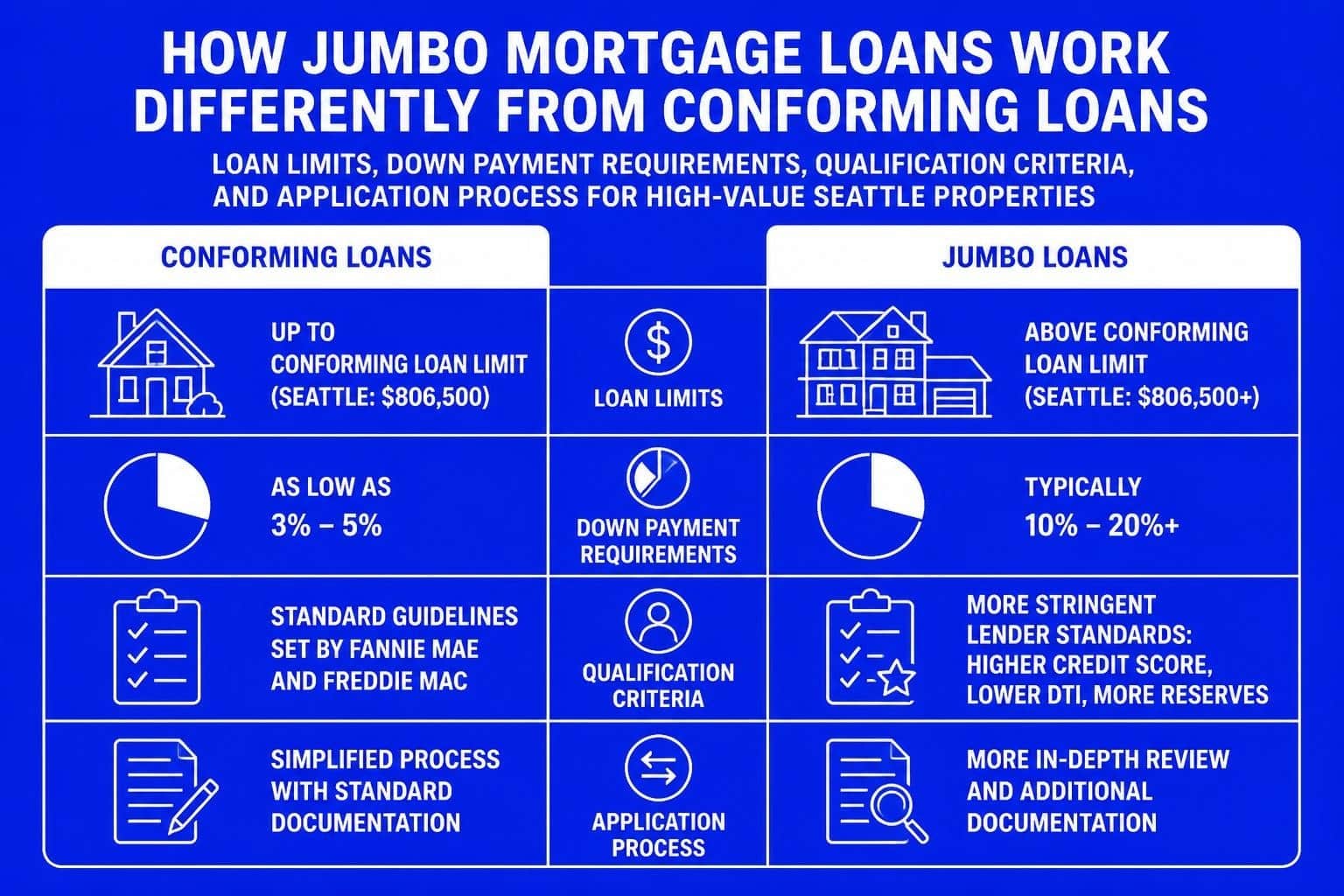

Jumbo Loan Considerations

Seattle's median home price pushes many first-time buyers into jumbo loan territory. These mortgages exceed conventional loan limits ($766,550 in King County for 2026) and carry slightly different requirements.

Jumbo mortgage typically requires:

- Higher credit scores (usually 700+ minimum)

- Larger down payments (10-20% depending on purchase price)

- Lower debt-to-income ratios (typically 43% maximum)

- Significant cash reserves (6-12 months of payments)

Despite stricter requirements, jumbo home loan programs offer competitive rates for well-qualified borrowers purchasing in Redmond, Kirkland, or premium Seattle neighborhoods.

Timeline Management and Closing Preparation

Understanding the mortgage timeline prevents last-minute scrambling and positions you for smooth closings.

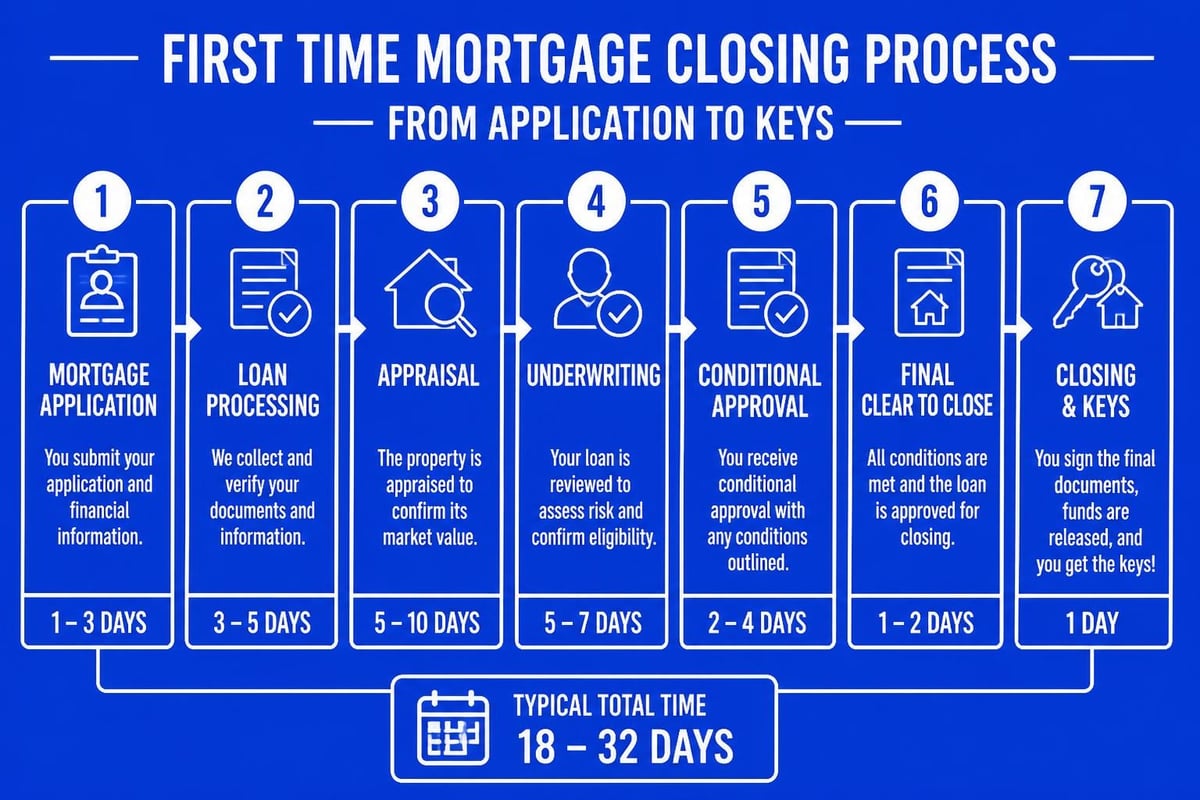

The 30-45 Day Standard Process

Traditional first time mortgage closings follow this general timeline:

- Days 1-3: Application submission and initial document collection

- Days 4-10: Processing, verification, and appraisal ordering

- Days 11-20: Underwriting review and conditional approval

- Days 21-30: Condition clearance and final approval

- Days 31-45: Clear to close, final walkthrough, and closing appointment

Experienced lenders like those at Mortgage Reel can compress this timeline to as few as 9 business days when necessary, providing competitive advantages in fast-moving Seattle markets.

Common Closing Obstacles to Avoid

Even well-prepared buyers encounter preventable delays. Protect your closing date by avoiding these mistakes:

- Large purchases that change debt ratios between approval and closing

- Job changes during the mortgage process (even promotions require re-verification)

- New credit inquiries that trigger lender alerts and additional scrutiny

- Moving money between accounts without clear paper trails

- Missing deadline responses to lender condition requests

Proactive communication with your loan officer prevents most timeline issues before they become problems.

Making Competitive Offers in Seattle Markets

Your first time mortgage strategy influences offer competitiveness beyond just pre-approval status.

Financing Contingency Considerations

Financing contingencies protect buyers if loans fall through but may weaken offers in competitive situations. Strategic approaches include:

- Shorter contingency periods (10-14 days versus standard 21)

- Stronger earnest money deposits demonstrating commitment

- Escalation clauses with financing limits clearly defined

- Seller communication about lender reliability and closing speed

Working with experienced Seattle mortgage brokers who can verify your pre-approval credibility adds weight to your offer package.

Down Payment Strategy and Offer Strength

Higher down payments signal financial strength and reduce seller concerns about appraisal gaps. Even if you qualify for 3% down programs, consider these advantages of larger down payments:

- Appraisal gap coverage becomes easier with more cash available

- Lower monthly payments improve long-term budget flexibility

- Faster equity building in Seattle's appreciating market

- Reduced total interest costs over the loan lifetime

Balance these benefits against maintaining emergency reserves and investment opportunities when determining your optimal down payment amount.

First-Time Buyer Programs and Assistance

Washington State and local jurisdictions offer numerous programs designed specifically for first-time buyers in Seattle, Shoreline, Lynnwood, and surrounding communities.

Washington State Housing Finance Commission

The state's primary homebuyer assistance program provides:

- Down payment assistance loans up to 5% of purchase price

- Below-market interest rates for qualified buyers

- Tax credit opportunities reducing annual tax liability

- Income and purchase price limits varying by county

These programs work alongside conventional and FHA financing, not as replacements. Combining state assistance with your primary first time mortgage maximizes affordability.

Local City and County Programs

King and Snohomish counties maintain additional assistance programs targeting specific buyer demographics or geographic areas. Research current offerings through housing departments, as programs change based on funding availability and policy priorities.

For detailed information on home loans for first-time buyers, consult with local housing counselors and experienced mortgage professionals familiar with current program availability.

Rate Lock Strategies and Timing

Interest rates fluctuate daily, making rate lock timing a critical decision point in your first time mortgage process.

Understanding Rate Lock Periods

Most lenders offer rate locks ranging from 15 to 60 days, with longer locks carrying slightly higher rates. Match your lock period to your expected closing timeline:

| Lock Period | Best For | Rate Premium |

|---|---|---|

| 15 days | Quick closings, cash purchases converting to financing | None (best rate) |

| 30 days | Standard transactions with clear timelines | Standard pricing |

| 45 days | New construction, complex financing | 0.125% – 0.25% |

| 60 days | Extended closings, construction loans | 0.25% – 0.375% |

If rates drop significantly after locking, some lenders offer float-down options allowing one-time rate adjustments. Understand these policies before locking your rate.

Market Timing Considerations

Attempting to time mortgage rates perfectly often backfires. More effective strategies include:

- Focusing on affordability rather than rate perfection

- Maintaining realistic expectations based on current market conditions

- Prioritizing home purchase timing over rate speculation

- Refinancing opportunities when rates drop post-purchase

For current market insights, follow resources like Chase’s homebuyer tips and local Seattle market analysis from experienced professionals.

Post-Closing Mortgage Management

Your first time mortgage journey extends well beyond closing day. Strategic management builds wealth and financial flexibility.

Building Equity Strategically

Home equity accumulates through principal reduction and property appreciation. Accelerate equity building by:

- Making extra principal payments when budgets allow

- Applying windfalls (bonuses, tax refunds) toward principal

- Refinancing from FHA to conventional once reaching 20% equity

- Avoiding home equity borrowing for depreciating purchases

Seattle's historically strong appreciation rates support equity building, though future appreciation should never be assumed or relied upon for financial planning.

When to Consider Refinancing

Refinancing makes sense when rate reductions, term changes, or cash-out needs justify closing costs. Common scenarios include:

- Rate drops of 0.75% or more below your current rate

- FHA-to-conventional refinancing to eliminate mortgage insurance

- Adjustable-to-fixed rate conversions for payment stability

- Term adjustments from 30 to 15 years as income increases

For personalized analysis of mortgage refinance opportunities, consult with your original lender or shop multiple options through experienced brokers.

Common First-Time Buyer Mistakes to Avoid

Learning from others' experiences prevents costly errors in your own first time mortgage journey.

Overextending Your Budget

Maximum qualification differs substantially from comfortable affordability. Lenders approve based on ratios and guidelines, not your specific lifestyle expenses, career stability, or financial goals.

Calculate your comfortable payment by accounting for:

- Retirement contributions and savings goals

- Lifestyle expenses including travel and hobbies

- Future family planning and associated costs

- Emergency fund maintenance and building

- Career uncertainty or potential income changes

Just because you qualify for a $700,000 Everett home doesn't mean that purchase serves your best financial interests.

Neglecting Inspection and Appraisal Contingencies

Waiving contingencies might strengthen offers but exposes you to significant risks. Structural issues, environmental hazards, or appraisal gaps can cost tens of thousands of dollars.

Maintain appropriate protections while remaining competitive by:

- Using pre-inspection strategies before making offers

- Shortening contingency periods rather than eliminating them

- Including specific coverage amounts rather than open-ended protections

- Communicating clearly about your commitment and ability to close

Understanding mortgage fundamentals helps you make informed decisions about which protections matter most for your specific situation.

Choosing Lenders Based Solely on Rate

Interest rates represent just one component of total mortgage value. Consider these equally important factors:

- Closing timeline reliability critical in competitive markets

- Communication quality throughout the process

- Experience with your specific situation (tech compensation, investment properties, etc.)

- Problem-solving ability when issues arise

- Post-closing support for questions and future needs

The cheapest rate becomes expensive when closing delays cost you your dream home or poor service creates unnecessary stress.

Securing your first time mortgage requires strategic planning, financial discipline, and expert guidance tailored to Seattle's unique market dynamics. From understanding loan options and building strong financial foundations to navigating competitive offers and closing successfully, each step contributes to long-term homeownership success. Whether you're a tech professional in Bellevue leveraging stock compensation or a traditional buyer in Lynnwood, the right mortgage strategy transforms homeownership from overwhelming to achievable. Keith Akada and the team at Mortgage Reel bring 25+ years of experience serving Seattle-area buyers with transparent guidance, advanced underwriting capabilities, and closing timelines as fast as 9 business days-discover how personalized mortgage solutions can help you achieve your homeownership goals at Mortgage Reel.