Seattle's competitive real estate market presents unique challenges for homebuyers, particularly those seeking properties in prestigious neighborhoods like Madison Park, Laurelhurst, or the waterfront areas of Bellevue and Kirkland. When your dream home exceeds conventional loan limits, a jumbo mortgage loan becomes essential. Understanding how these specialized financing products work can mean the difference between securing your ideal property or missing out in a fast-moving market. For tech professionals at Amazon, Microsoft, and Google with significant stock compensation, jumbo loans often provide the pathway to luxury homes that match their lifestyle and investment goals.

What Defines a Jumbo Mortgage Loan

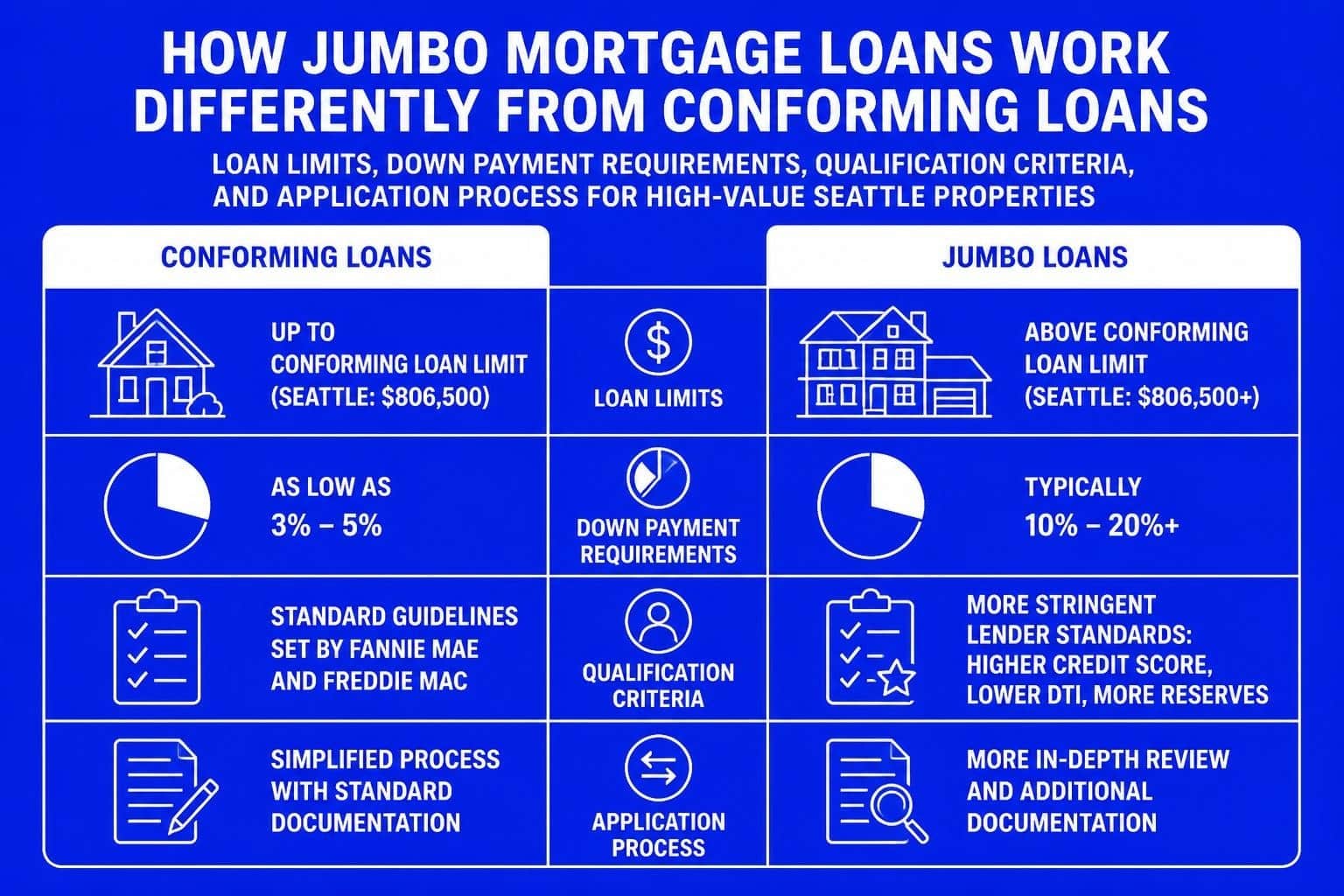

A jumbo mortgage loan is any home loan that exceeds the conforming loan limits established by the Federal Housing Finance Agency (FHFA). In 2026, the conforming loan limit for most counties stands at $766,550 for single-family homes. However, high-cost areas like King County have elevated limits that can reach $1,149,825.

Key characteristics that separate jumbo loans from conventional mortgages include:

- Higher loan amounts exceeding FHFA conforming limits

- More stringent qualification requirements

- Potentially different interest rate structures

- Larger down payment expectations

- Enhanced documentation standards

The distinction matters because jumbo loans cannot be purchased by Fannie Mae or Freddie Mac, the government-sponsored enterprises that provide liquidity to the mortgage market. This means lenders assume greater risk, which translates to more rigorous underwriting standards.

Understanding Loan Limits Across Seattle Metro Areas

Seattle and surrounding communities have varying conforming loan limits based on median home prices. While downtown Seattle properties frequently require jumbo financing, buyers in Shoreline, Lynnwood, or Lake Forest Park may find homes within conforming limits depending on the specific neighborhood and property type.

| Location | Typical Price Range | Jumbo Loan Frequency |

|---|---|---|

| Seattle (Central) | $800K – $2.5M+ | Very High |

| Bellevue | $900K – $3M+ | Very High |

| Kirkland | $750K – $2M+ | High |

| Redmond | $700K – $1.8M | Moderate to High |

| Shoreline | $600K – $1.2M | Moderate |

| Mill Creek | $550K – $1M | Lower to Moderate |

Qualification Requirements for Jumbo Financing

Securing a jumbo mortgage loan demands financial strength beyond conventional loan standards. Lenders scrutinize every aspect of your financial profile because they're extending larger amounts without the safety net of government-sponsored enterprise backing.

Credit Score Expectations

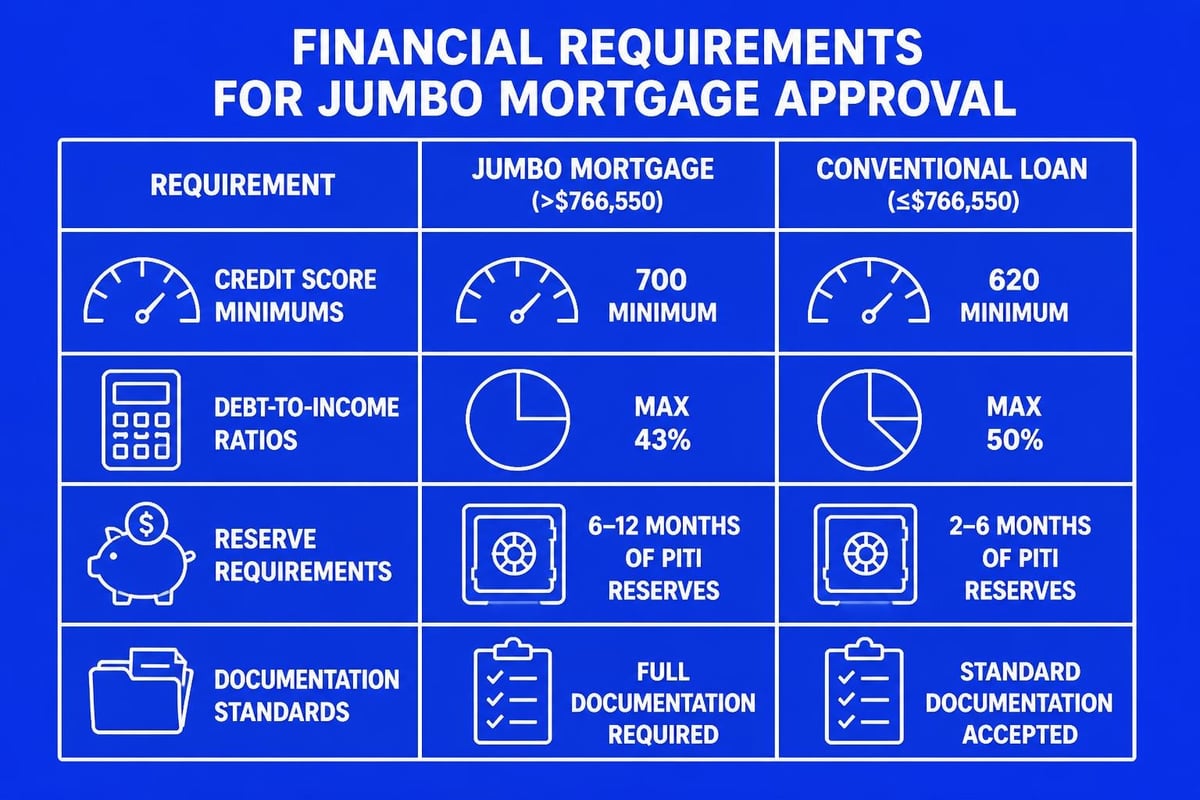

Most lenders require minimum credit scores between 700 and 720 for jumbo loans, though some programs may accept scores as low as 680 with compensating factors. Premium rates typically go to borrowers with scores above 740. Your credit history should demonstrate consistent, responsible financial management over several years.

Payment history carries significant weight. Even one late payment within the past 12 months can impact your rate or approval chances. Collections, charge-offs, or recent bankruptcies create substantial obstacles.

Down Payment Standards

While conventional loans may require as little as 3% down, jumbo loans typically demand 10% to 20% minimum. Properties above $2 million often require 20% to 30% down.

Down payment tiers and their implications:

- 10-15% down: Possible but may require perfect credit, substantial reserves, and lower debt ratios

- 20% down: Standard expectation for most jumbo programs, optimal rate pricing

- 25-30% down: Required for loan amounts exceeding $2-3 million or unique property types

- 40%+ down: May unlock portfolio loan options with flexible terms

For a $1.5 million home in Redmond, a 20% down payment means bringing $300,000 to closing. Tech professionals can often leverage RSU vesting schedules or stock sales to meet these requirements, though timing and tax implications require careful planning.

Debt-to-Income Ratio Limits

Jumbo mortgage lenders typically cap debt-to-income (DTI) ratios at 43% to 45%, though some allow up to 50% with exceptional credit and substantial reserves. This ratio compares your monthly debt obligations to your gross monthly income.

Calculate your DTI by adding all monthly debt payments (proposed mortgage, car loans, student loans, minimum credit card payments, other obligations) and dividing by your gross monthly income. A software engineer earning $300,000 annually ($25,000 monthly) with $8,000 in total monthly debts would have a 32% DTI-well within acceptable parameters.

Income Documentation and Verification

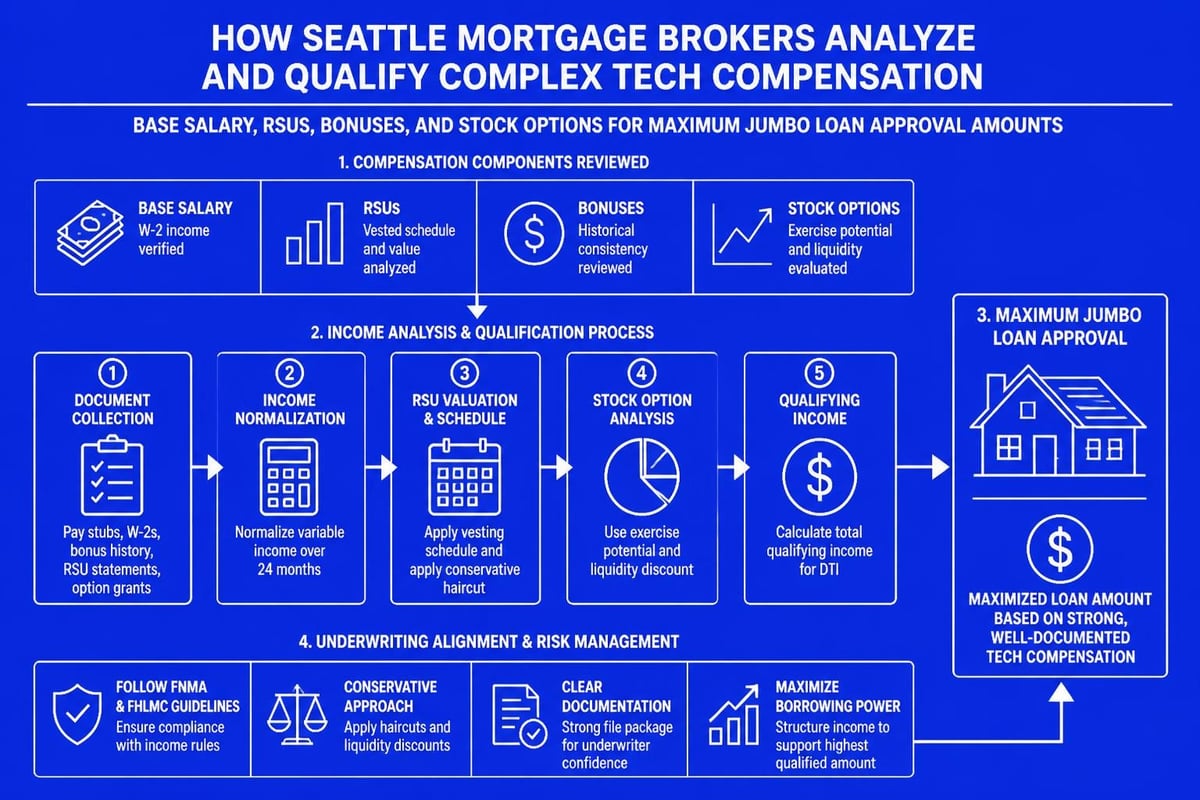

Jumbo underwriting demands comprehensive income documentation, particularly important for Seattle tech workers with complex compensation structures. Base salary alone rarely tells the complete story.

Qualifying Stock Compensation and Bonuses

Restricted stock units (RSUs), stock options, and performance bonuses form substantial portions of total compensation at companies like Amazon and Microsoft. Experienced mortgage brokers understand how to structure these income sources for maximum qualification power.

RSU qualification typically requires:

- Two-year vesting history demonstrating consistency

- Current vesting schedule showing future grants

- Documentation of stock value and sale proceeds

- Tax returns reflecting stock income

Bonuses need a two-year history of receipt to be considered stable income. However, accelerating bonuses or one-time equity events may not count toward qualifying income despite their significant value.

Reserve Requirements

Beyond down payment funds, jumbo lenders require substantial cash reserves-typically 6 to 12 months of mortgage payments (principal, interest, taxes, insurance, and HOA fees) held in liquid accounts after closing.

For a $1.2 million loan in Bellevue with a $9,000 monthly payment, you might need $54,000 to $108,000 in reserves post-closing. Retirement accounts, investment portfolios, and savings all count, though lenders may discount certain asset types.

| Reserve Source | Typical Discount |

|---|---|

| Checking/Savings | 0% (full value) |

| Stocks/Bonds | 0-30% |

| 401(k)/IRA | 30-40% |

| Crypto/Alternative Assets | Case-by-case |

Interest Rates and Pricing Factors

Jumbo mortgage loan rates fluctuate based on market conditions and individual borrower profiles. In 2026, rates remain competitive, sometimes matching or even beating conforming loan rates due to the high-quality borrower pool.

What Influences Your Rate

Multiple factors determine your final interest rate. Loan-to-value ratio significantly impacts pricing-borrowers with 20% equity receive better rates than those with 10% down. Credit scores create pricing tiers, with each 20-point increment potentially affecting your rate by 0.125% to 0.25%.

Property type matters. Single-family primary residences get the best rates, while condos, investment properties, and multi-unit buildings face rate adjustments. Location within the Seattle metro also plays a role, though differences are typically modest.

Fixed vs. Adjustable Rate Options

Fixed-rate jumbo loans provide payment stability for 15, 20, or 30 years. They're ideal when you plan to stay long-term or want predictable budgeting. The 30-year fixed remains most popular despite slightly higher rates than shorter terms.

Adjustable-rate mortgages (ARMs) offer lower initial rates, typically fixed for 5, 7, or 10 years before adjusting annually. A 7/1 ARM might save you 0.5% to 0.75% compared to a 30-year fixed, translating to substantial monthly savings on a $1.5 million loan. This strategy works well for buyers who anticipate moving, refinancing, or significantly increasing income within the fixed period.

Property Types and Restrictions

Not all properties qualify equally for jumbo financing. Single-family homes receive the most favorable terms and widest program availability. Condominiums face additional scrutiny-the building must meet specific criteria regarding owner-occupancy ratios, budget reserves, and insurance coverage.

Unique Property Considerations

Luxury properties in Seattle and Kirkland sometimes include unique features that complicate financing: waterfront access, significant acreage, guest houses, or commercial elements. These characteristics may require portfolio loans or specialized jumbo programs.

Properties exceeding certain thresholds (typically $2.5 to $3 million) enter ultra-jumbo territory with even stricter requirements. Multi-million dollar estates in Medina or Clyde Hill demand substantial down payments, impeccable credit, and significant reserves.

Investment properties and second homes qualify for jumbo financing but face higher rates and larger down payment requirements-typically 25% to 30% minimum.

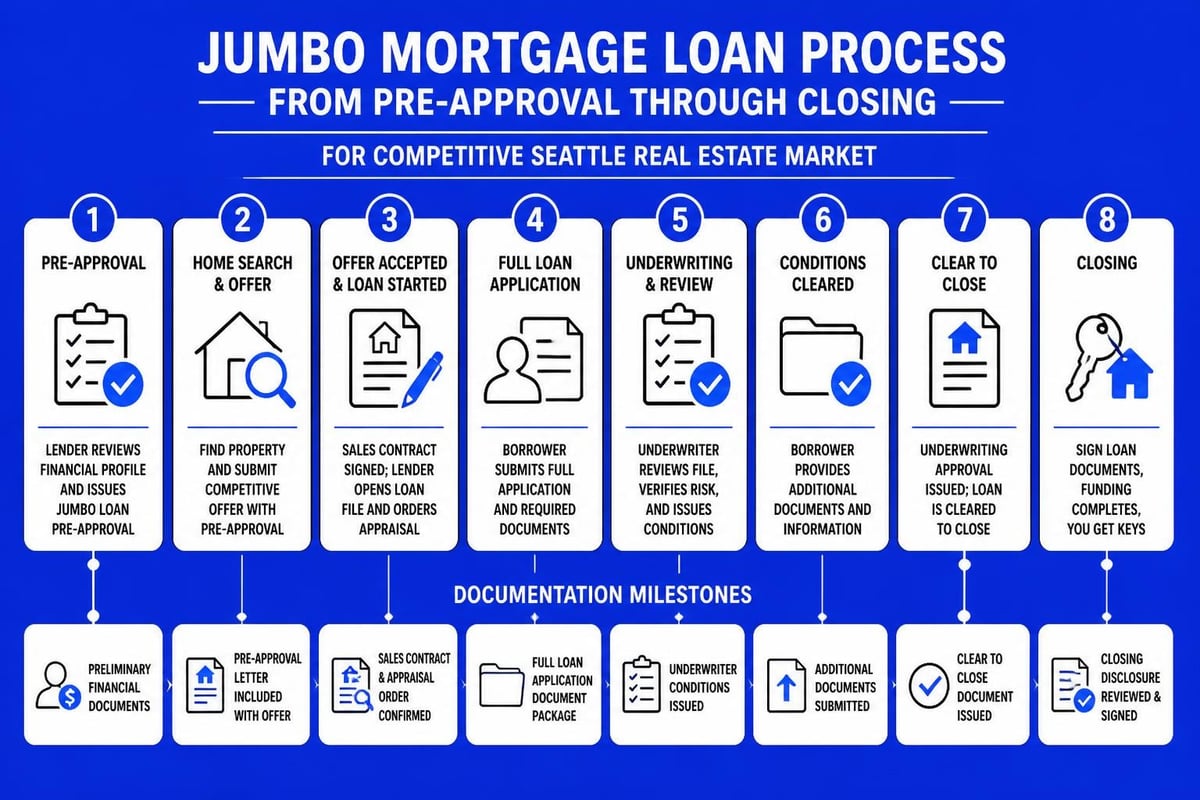

The Application and Approval Process

Securing a jumbo mortgage loan involves more extensive documentation than conventional financing. Expect to provide two years of tax returns, W-2s, recent pay stubs, bank statements covering all accounts, retirement account statements, and documentation for any non-employment income.

Timeline Expectations

While conventional loans often close in 21 to 30 days, jumbo loans may require 30 to 45 days due to enhanced underwriting. However, experienced brokers working with responsive lenders can expedite this process. Some specialized mortgage brokers can close jumbo loans in as few as 9 to 14 business days when borrowers have exceptional documentation and straightforward financial profiles.

The typical jumbo loan timeline includes:

- Pre-approval (3-7 days): Initial documentation review and credit check

- Property search: Armed with pre-approval, you can shop confidently

- Purchase agreement: Earnest money deposit and inspection contingencies

- Full application (1-2 days): Complete documentation submission

- Processing (7-14 days): Detailed file review, employment verification, asset verification

- Underwriting (5-10 days): Comprehensive risk assessment and conditional approval

- Closing preparation (3-5 days): Final conditions cleared, closing disclosure review

- Funding: Wire transfers and document signing

Seattle's competitive market often requires quick closings. Working with trusted local mortgage brokers who understand the urgency gives you an edge when multiple offers compete.

Strategies for Seattle Tech Professionals

Tech workers possess unique advantages when pursuing jumbo financing. High incomes, stock compensation, and strong career trajectories make you attractive borrowers despite sometimes shorter employment histories.

Maximizing Stock Compensation

Time RSU sales strategically to minimize tax impact while ensuring sufficient liquidity for down payment and reserves. Selling stock quarterly as it vests provides steady cash flow, while lump sales might push you into higher tax brackets.

Consider the wash sale rule if you plan to rebuy stock after selling for down payment funds. Coordinate with your tax advisor to optimize timing.

Building Your Profile Before Applying

Start preparing 6 to 12 months before your intended purchase. Pay down high-interest debt to improve DTI ratios. Avoid opening new credit accounts or making large purchases that could affect your credit score or debt levels.

Accumulate reserves in easily accessible accounts. While retirement accounts count, liquid savings provide more flexibility and face no discount.

Common Challenges and Solutions

Even well-qualified borrowers encounter obstacles during the jumbo loan process. Understanding potential issues helps you prepare effective solutions.

Employment Gaps or Job Changes

Switching jobs during the mortgage process creates complications, though not necessarily deal-breakers. If you're moving to a higher position in the same industry with increased compensation, underwriters often approve the change. Provide your offer letter, explain the career progression, and demonstrate continuous industry employment.

Employment gaps exceeding one month require written explanations. Planned gaps between positions (sabbaticals, relocation periods) are acceptable with documentation and sufficient reserves.

Complex Income Structures

Self-employed borrowers, commission-based professionals, and business owners face heightened scrutiny. Lenders average two years of tax returns, focusing on net income after business expenses. This often understates your true earning capacity since business deductions reduce taxable income.

Consider alternatives like bank statement programs or asset-based qualification if traditional income documentation doesn't reflect your financial strength. These programs use 12 to 24 months of business bank deposits to calculate income, potentially qualifying you for larger loan amounts.

Multiple Property Ownership

Owning multiple properties affects debt ratios and reserve requirements. If you're buying a primary residence while keeping your current home as a rental, you'll need adequate rental income documentation or sufficient reserves to cover both mortgages.

Properties in Lynnwood or Everett purchased as investments years ago now provide rental income that can offset their mortgage obligations. Provide lease agreements and document rental payment history to strengthen your application.

Jumbo Refinancing Opportunities

Homeowners with existing jumbo mortgages can benefit from refinancing when rates drop, home values increase, or financial profiles strengthen. The 2026 market offers opportunities for borrowers who secured higher-rate jumbo loans in previous years.

Rate and Term Refinancing

Replacing your current jumbo loan with a new one at better terms can save thousands monthly and hundreds of thousands over the loan life. Refinancing strategies become attractive when rates fall 0.5% or more below your current rate, though even smaller differences justify refinancing if you plan to stay long-term.

Calculate your break-even point by dividing closing costs by monthly savings. If refinancing costs $15,000 and saves $800 monthly, you break even in 19 months. Any time beyond that represents pure savings.

Cash-Out Refinancing

Seattle's appreciating real estate market has built substantial equity for homeowners. Cash-out refinancing lets you access this equity while maintaining jumbo loan status. Use proceeds for home improvements, investment properties, education expenses, or debt consolidation.

Lenders typically allow cash-out refinancing up to 80% loan-to-value on primary residences. A home in Mill Creek purchased for $800,000 five years ago now worth $1.1 million offers access to significant equity while maintaining favorable jumbo loan terms.

Working With Experienced Jumbo Loan Specialists

The complexity of jumbo financing demands expertise beyond basic mortgage knowledge. Selecting the right mortgage broker significantly impacts your experience, rate, and approval likelihood.

What to Look for in a Jumbo Specialist

Seek brokers with extensive jumbo loan experience, particularly with tech compensation structures common in Seattle. They should offer multiple lender relationships, providing access to various jumbo programs and competitive rate shopping.

Reviews and testimonials from clients with similar profiles validate a broker's capabilities. Look for consistent praise regarding communication, problem-solving, and closing reliability in competitive situations.

The Value of Local Market Knowledge

Brokers deeply familiar with Seattle neighborhoods understand property valuation nuances, HOA requirements, and local lending conditions. This expertise proves invaluable when appraising unique properties or navigating condominium approval processes in competitive buildings.

Local specialists maintain relationships with appraisers, title companies, and real estate attorneys who facilitate smooth closings even under tight timelines.

Alternative Jumbo Loan Programs

Beyond traditional jumbo mortgages, specialized programs serve specific borrower needs. Portfolio loans held by banks rather than sold to investors offer flexibility on debt ratios, credit requirements, or unique property types.

Portfolio and Private Banking Solutions

High-net-worth individuals may access portfolio loan programs through private banking relationships. These loans consider overall wealth, not just income and debt ratios. Substantial investment accounts, business holdings, or trust assets can compensate for higher debt ratios or unconventional income documentation.

Interest-Only Jumbo Loans

Interest-only options let you pay only interest for an initial period (typically 5 to 10 years), reducing required monthly payments. This strategy works for borrowers expecting significant future income increases, those planning to sell before the interest-only period ends, or investors prioritizing cash flow.

After the interest-only period, payments increase substantially as you begin paying both principal and interest. Carefully evaluate whether this structure aligns with your long-term financial plan.

Understanding jumbo mortgage loan requirements and strategies positions you for success in Seattle's luxury real estate market, particularly when navigating complex compensation structures and competitive property bidding. Whether you're purchasing a waterfront home in Kirkland, upgrading to a larger property in Bellevue, or investing in Seattle real estate, having an experienced partner makes all the difference. Keith Akada at Mortgage Reel brings 25+ years of expertise helping tech professionals and homebuyers navigate jumbo financing with specialized knowledge in qualifying RSUs, stock compensation, and bonus income. With 750+ five-star reviews and the ability to close loans in as few as 9 business days, Keith provides the clarity and execution you need in today's competitive market.