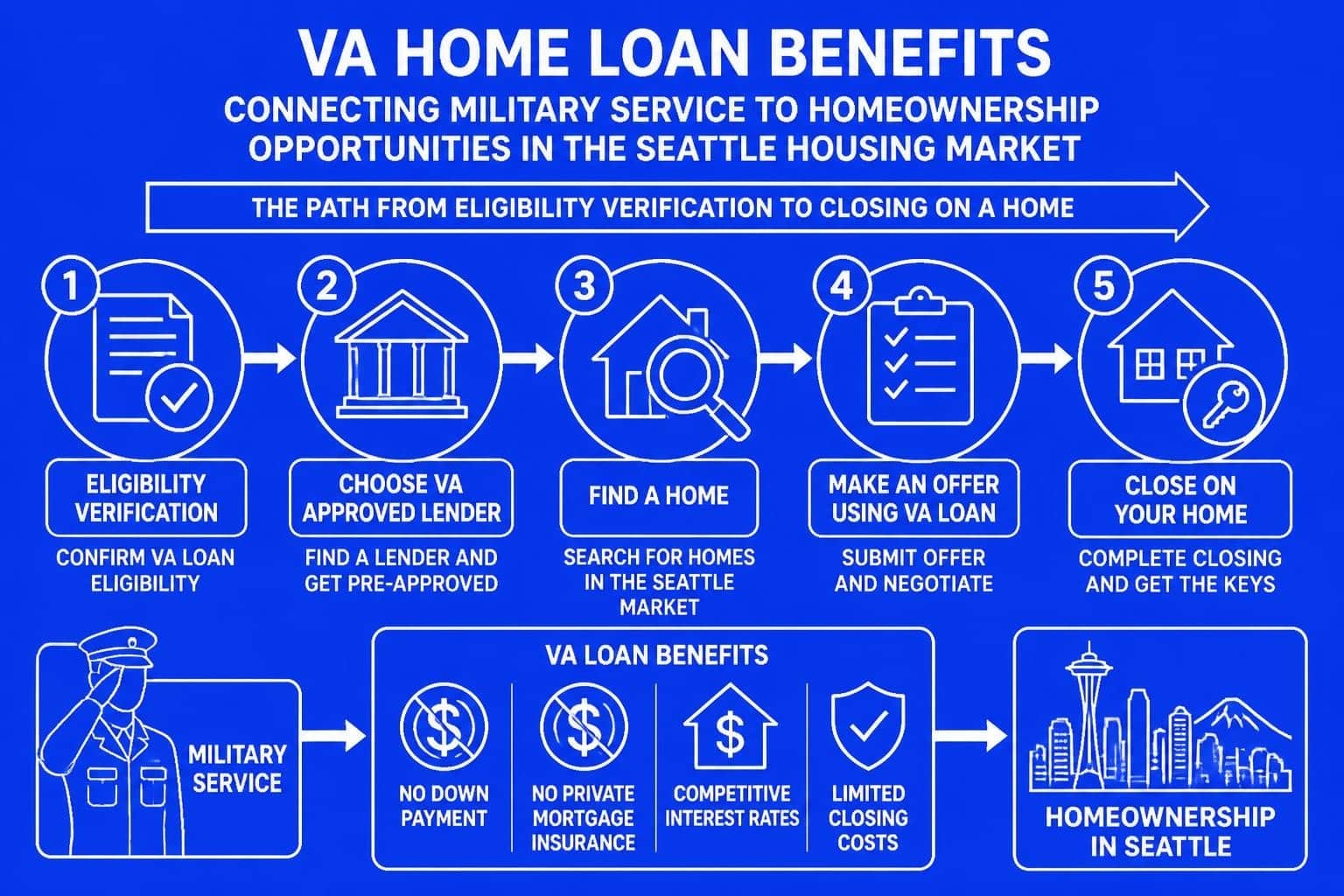

Military service members and veterans in the Seattle area have access to one of the most powerful homebuying tools available: VA loans for homes. These government-backed mortgages offer exceptional benefits that can make homeownership more accessible and affordable across Seattle, Bellevue, Redmond, Kirkland, and surrounding communities. Understanding how these loans work and maximizing their advantages requires knowledge of eligibility requirements, loan types, and strategic planning, especially in competitive Pacific Northwest markets where home prices continue to climb.

Understanding VA Loans for Homes and Their Core Benefits

VA loans for homes represent a unique mortgage program guaranteed by the U.S. Department of Veterans Affairs, designed to reward military service with tangible homeownership advantages. Unlike conventional financing, these loans eliminate many barriers that typically challenge homebuyers.

The most significant advantage is zero down payment required on most purchases. In Seattle's housing market, where median home prices exceeded $800,000 in 2026, this benefit translates to substantial savings. Veterans can purchase properties without accumulating tens of thousands of dollars for a traditional down payment, preserving cash for other investments or expenses.

Key Advantages That Set VA Loans Apart

- No private mortgage insurance (PMI) regardless of down payment amount

- Competitive interest rates typically lower than conventional mortgages

- Flexible credit requirements with guidelines that accommodate various credit profiles

- Limited closing costs with specific fees prohibited by VA regulations

- No prepayment penalties allowing accelerated payoff strategies

The VA home loan program has helped millions of service members achieve homeownership since 1944. For tech professionals working at Amazon, Microsoft, or Google who also served in the military, combining VA loan benefits with stock compensation strategies can significantly amplify buying power in premium Seattle neighborhoods.

Eligibility Requirements for VA Loans in Seattle

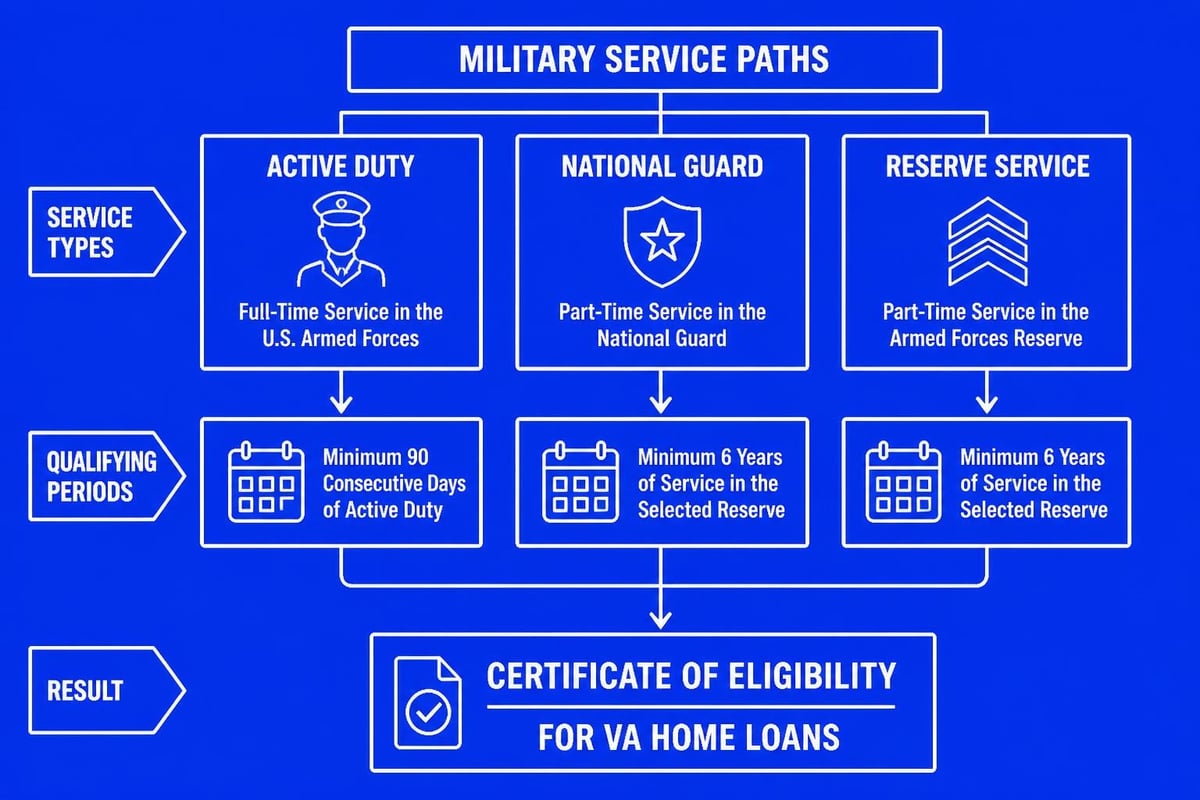

Determining your eligibility for va loans for homes starts with understanding service requirements established by the Department of Veterans Affairs. The VA eligibility criteria consider duty status, length of service, and discharge characterization.

Active Duty Service Members qualify after serving 90 consecutive days during wartime or 181 days during peacetime. National Guard and Reserve members typically need six years of service, though exceptions exist for earlier activation periods.

Veterans who served in conflicts including World War II, Korea, Vietnam, the Gulf War, and post-9/11 operations generally meet service requirements more quickly. Surviving spouses of service members who died in the line of duty or from service-connected disabilities may also qualify.

Obtaining Your Certificate of Eligibility

| Method | Processing Time | Best For |

|---|---|---|

| Online through eBenefits | Immediate to 24 hours | Veterans with DD-214 in system |

| Through approved lender | 1-3 business days | Buyers working with mortgage broker |

| Mail application (26-1880) | 2-4 weeks | Complex situations requiring documentation |

Working with an experienced Seattle mortgage broker streamlines this process considerably. Many lenders can verify eligibility and obtain certificates directly through the VA's WebLGY system, eliminating delays that could jeopardize time-sensitive purchase contracts in competitive neighborhoods like Bellevue or Redmond.

Types of VA Loans Available to Seattle Veterans

The VA guarantees several distinct loan types designed to meet different homeownership needs. Understanding which product aligns with your goals ensures optimal financial outcomes.

VA Purchase Loans

The most common option, VA purchase loans finance primary residence acquisitions. These loans can fund single-family homes, condominiums in VA-approved projects, manufactured homes, and properties requiring minor renovations.

In Seattle's expensive housing market, purchase loans work particularly well for first-time buyers who haven't accumulated significant savings. Veterans can compete effectively against cash offers by leveraging zero down payment capabilities combined with strong pre-approval letters from reputable lenders.

Cash-Out Refinance Options

Veterans with existing mortgages-whether VA or conventional-can access home equity through cash-out refinancing. This strategy works exceptionally well in Seattle, where property values have appreciated substantially over recent years.

Homeowners in Kirkland or Mill Creek who purchased homes five years ago might have accumulated $200,000 or more in equity. Cash-out refinancing allows accessing this equity at favorable VA rates while maintaining the no-PMI advantage, useful for debt consolidation, home improvements, or investment opportunities.

Interest Rate Reduction Refinance Loans (IRRRL)

Also called VA streamline refinances, IRRRLs help veterans reduce monthly payments by securing lower interest rates. These refinances require minimal documentation and no appraisal in most cases, making them ideal when rates drop or credit profiles improve.

The IRRRL process typically includes:

- Rate comparison against current mortgage

- Break-even analysis for closing costs

- Streamlined documentation submission

- Faster closing timeline than traditional refinances

For homeowners across Seattle and Shoreline, monitoring rate trends and refinancing strategically can save thousands annually. Understanding mortgage financing options helps veterans make informed timing decisions.

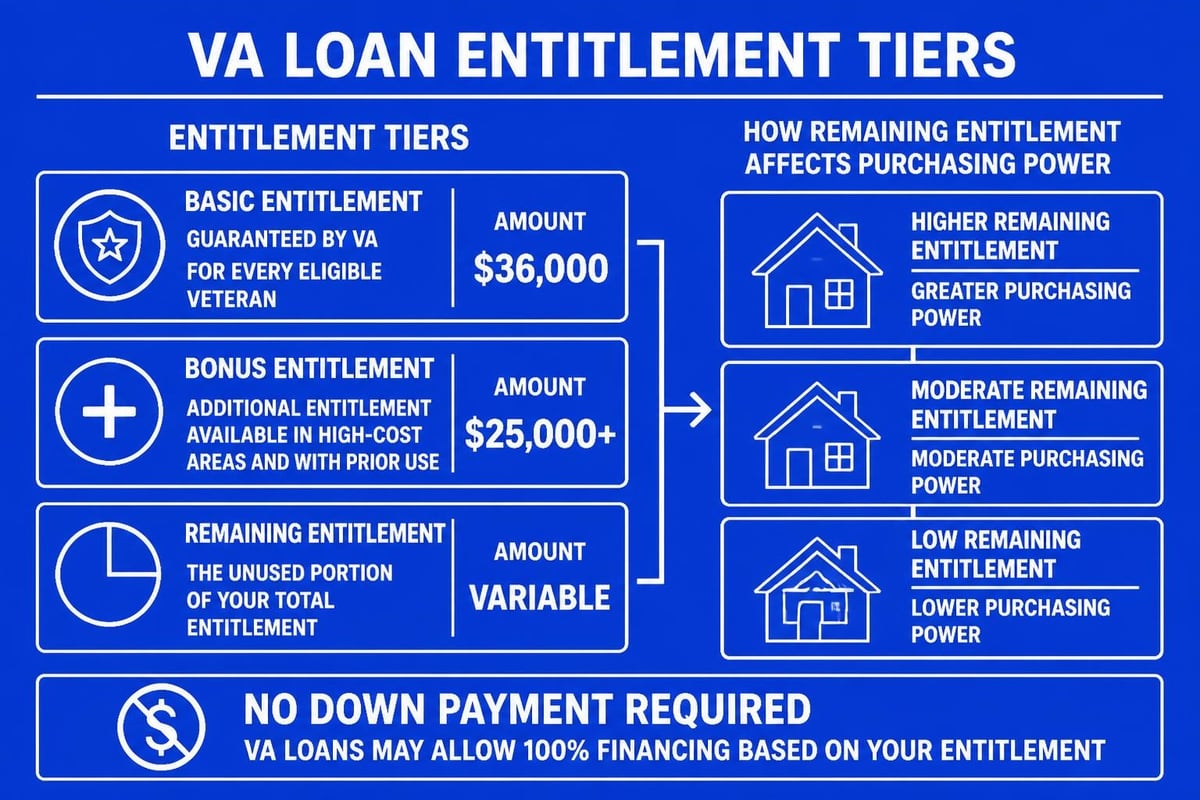

VA Loan Limits and Entitlement in 2026

Following the Blue Water Navy Vietnam Veterans Act of 2019, the VA technically eliminated loan limits for veterans with full entitlement. However, understanding VA loan limits and entitlement structure remains important for financial planning.

Veterans with full entitlement can purchase homes at any price without down payment, provided they qualify based on income and debt-to-income ratios. In King County, where conforming loan limits reach $1,089,300 in 2026, this represents substantial buying power.

Entitlement Scenarios for Seattle Buyers

| Situation | Available Entitlement | Down Payment Required |

|---|---|---|

| First-time VA buyer, no prior loans | Full entitlement | $0 on any qualified purchase |

| Previous VA loan paid off, property sold | Restored full entitlement | $0 on new purchase |

| Active VA loan on different property | Partial remaining entitlement | Depends on remaining amount |

| Purchase above 4x remaining entitlement | Limited entitlement | 25% of amount exceeding limit |

Veterans considering properties in Lynnwood or Lake Forest Park should calculate remaining entitlement carefully when maintaining existing VA loans. Strategic planning might involve refinancing previous VA mortgages to conventional products, restoring full entitlement for new purchases.

The VA Funding Fee and Cost Considerations

While va loans for homes eliminate many traditional costs, borrowers pay a VA funding fee that helps sustain the program for future veterans. This one-time fee varies based on service type, down payment amount, and whether it's a first or subsequent use.

2026 VA Funding Fee Structure:

- First-time use, zero down: 2.15% of loan amount

- Subsequent use, zero down: 3.30% of loan amount

- First-time use, 5% down: 1.50% of loan amount

- First-time use, 10%+ down: 1.25% of loan amount

Veterans receiving VA disability compensation and surviving spouses are exempt from funding fees entirely. For a $750,000 home purchase in Seattle with zero down, a first-time borrower would pay $16,125 in funding fees, typically financed into the loan rather than paid at closing.

Prohibited and Allowed Closing Costs

VA regulations protect borrowers by prohibiting certain fees while allowing others. Understanding these distinctions prevents unexpected expenses and ensures compliance.

Prohibited fees include: attorney fees charged to veterans, real estate commissions, and loan origination fees exceeding 1% of the loan amount.

Allowable costs include: appraisal fees, credit reports, title insurance, recording fees, and origination charges within regulatory limits.

Sellers can pay all allowable closing costs through negotiated concessions, particularly valuable in buyer-favorable market conditions. Experienced mortgage brokers structure offers strategically to maximize seller contributions while remaining competitive.

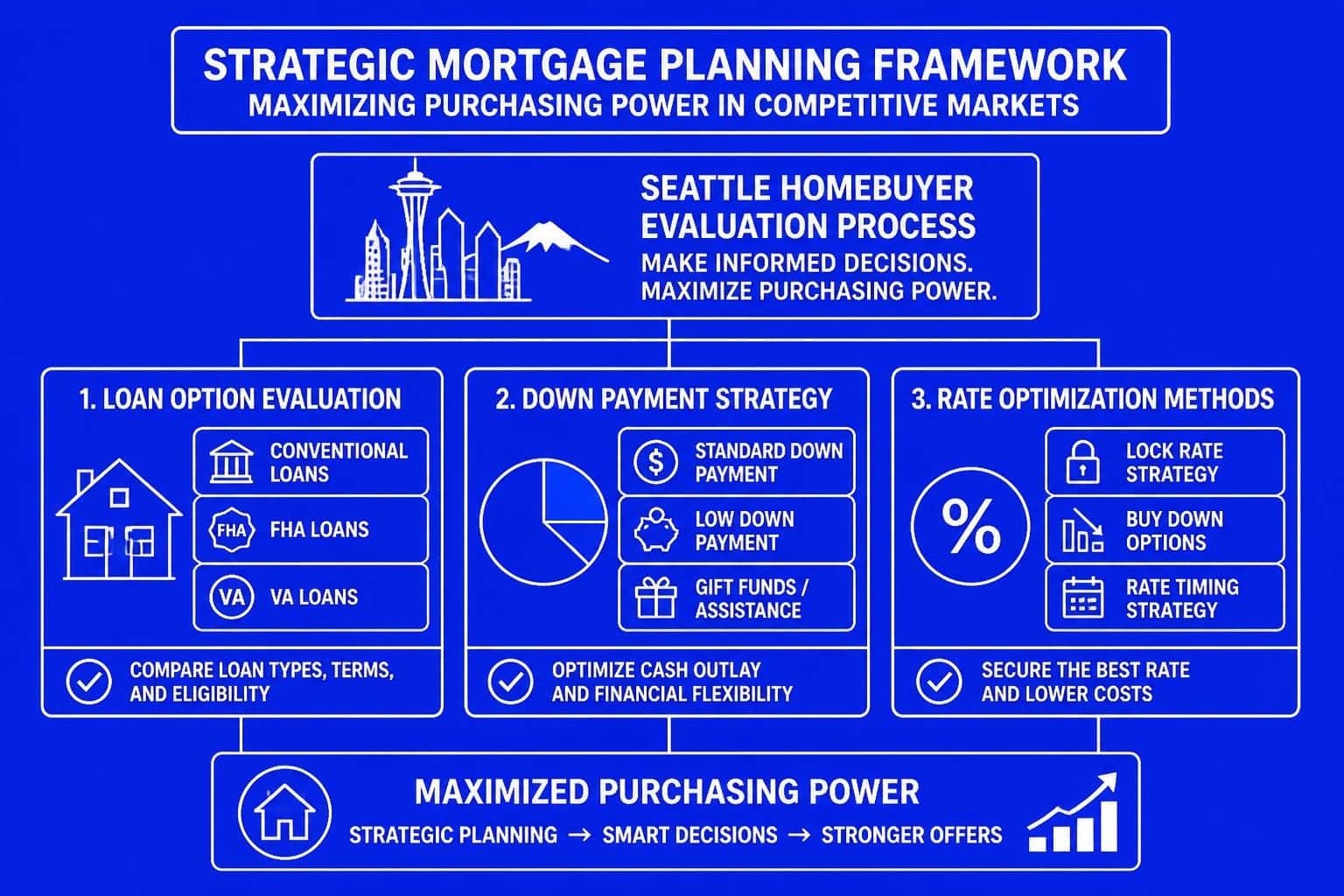

Using VA Loans in Seattle's Competitive Market

Seattle's housing market presents unique challenges where strategic execution separates successful buyers from disappointed ones. VA loans for homes compete effectively when buyers and their representatives understand market dynamics.

Overcoming Common Misconceptions

Many sellers and listing agents mistakenly believe VA loans cause delays or appraisal complications. Educated buyers address these concerns proactively through strong pre-approval documentation and clear communication about VA loan advantages.

Working with experienced Seattle mortgage brokers who close loans efficiently demonstrates credibility. Lenders capable of nine-business-day closings through advanced underwriting processes compete directly with conventional financing timelines.

Strategies for winning offers include:

- Obtaining comprehensive pre-approval with full documentation review

- Including escalation clauses with reasonable caps

- Demonstrating financial strength beyond minimum requirements

- Partnering with real estate agents experienced in VA transactions

- Waiving non-essential contingencies when appropriate and safe

Veterans employed at Microsoft or Amazon often combine VA benefits with strong income profiles from base salary plus RSUs, creating compelling financial pictures that reassure sellers in Redmond or Bellevue markets.

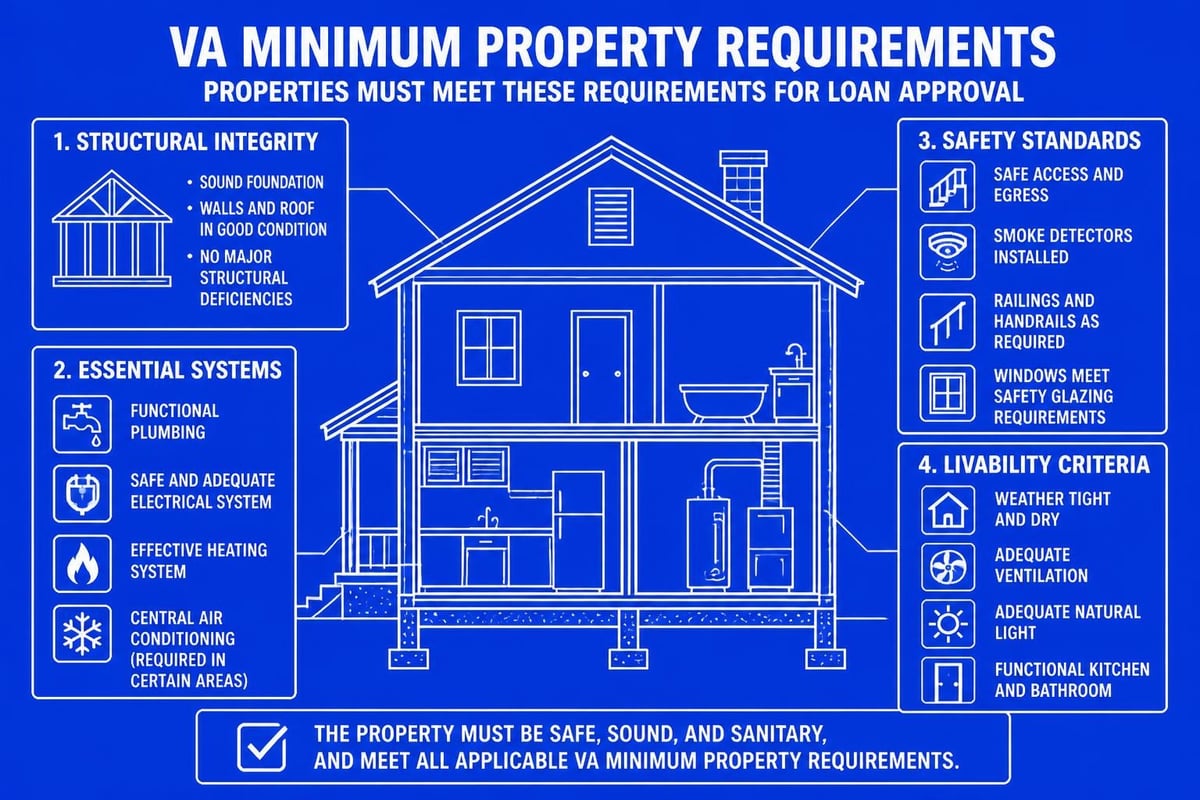

VA Loan Property Requirements and Appraisals

Properties financed through va loans for homes must meet minimum property requirements (MPRs) ensuring safety, soundness, and sanitation. VA appraisers evaluate these standards during the appraisal process, occasionally identifying issues requiring correction before closing.

Common MPR issues in older Seattle neighborhoods include inadequate heating systems, failing roofs, peeling lead paint, or evidence of wood-destroying insects. Unlike conventional appraisals that merely establish value, VA appraisals protect borrowers by flagging health and safety concerns.

Addressing Appraisal Challenges

When appraisals identify deficiencies, buyers have several options. Sellers can complete repairs before closing, escrow funds for post-closing correction, or reduce purchase prices to offset repair costs.

In competitive markets, requesting seller repairs risks losing properties to competing offers. Savvy buyers evaluate which issues genuinely threaten safety versus cosmetic concerns outside MPR scope, negotiating strategically based on priorities.

Properties in newer developments around Mill Creek or Everett typically encounter fewer MPR issues compared to historic homes in older Seattle neighborhoods. Understanding property age and condition helps set realistic expectations during the search process.

Maximizing Benefits for Seattle Tech Veterans

Veterans working in Seattle's technology sector possess unique advantages when pursuing homeownership through VA loans. Combining military service benefits with high-income tech employment creates exceptional buying power.

Tech professionals at companies like Google or Amazon often receive substantial compensation through restricted stock units (RSUs), performance bonuses, and sign-on packages. Qualified mortgage brokers can structure these income sources to maximize loan approval amounts, particularly relevant for jumbo home loans in premium neighborhoods.

Stock Compensation and VA Loans

Unlike some loan programs that discount or exclude stock compensation, knowledgeable lenders understand how to document and verify RSU income appropriately. Veterans with two-year histories of vesting stock can use these amounts toward qualifying income, substantially increasing purchasing power.

Documentation requirements typically include:

- Most recent pay stubs showing RSU vesting

- Two years of W-2s reflecting historical stock income

- Written verification of future vesting schedules

- Evidence of stable continued employment

For a veteran earning $180,000 in base salary plus $120,000 annually in vesting RSUs, proper income qualification could support purchase prices $200,000 higher than base salary alone would allow. This difference proves critical in Seattle's high-cost housing market.

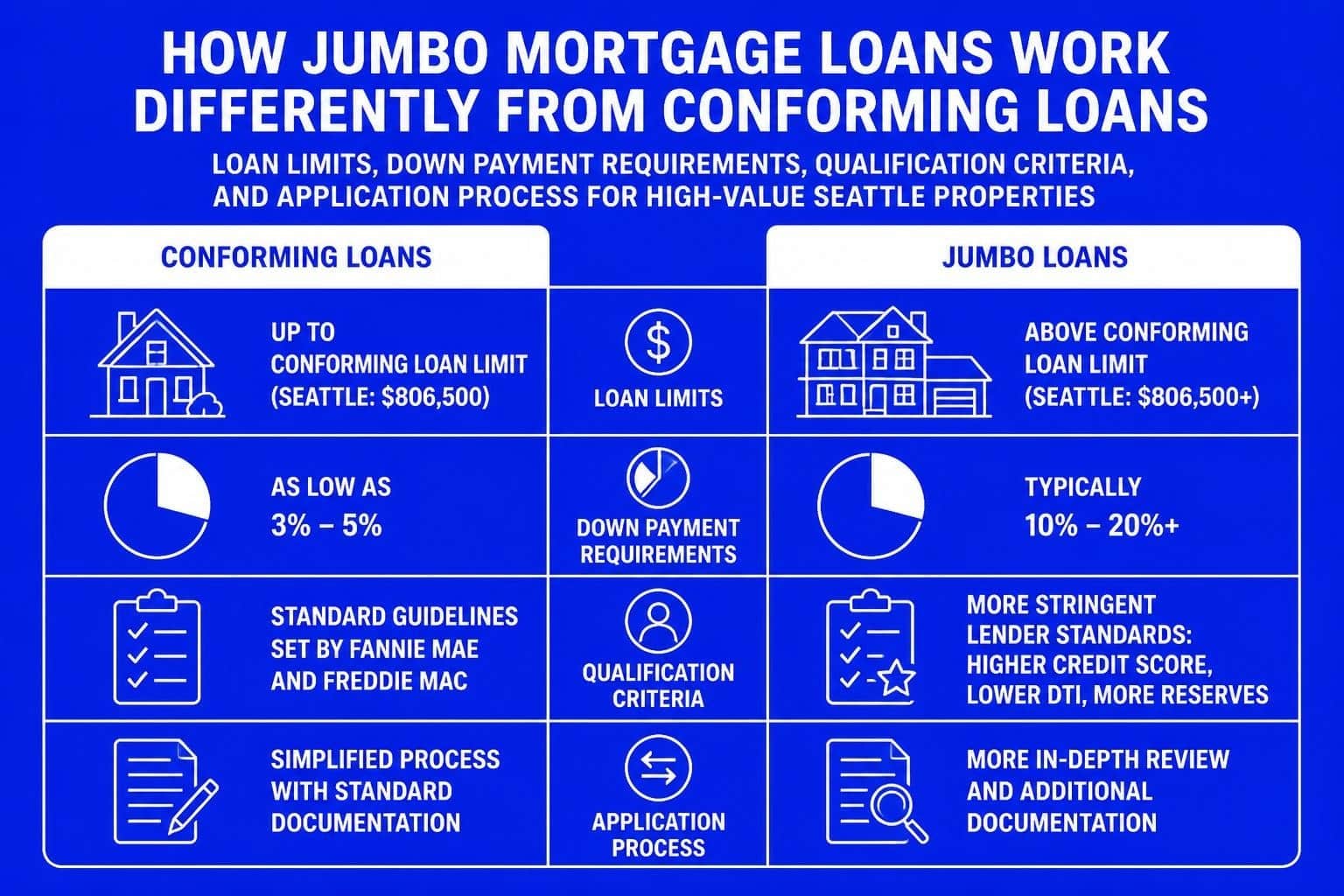

Comparing VA Loans to Other Mortgage Options

Understanding how va loans for homes compare against conventional, FHA, and USDA financing helps veterans make informed decisions aligned with their specific circumstances.

| Feature | VA Loan | Conventional | FHA | USDA |

|---|---|---|---|---|

| Minimum down payment | 0% | 3-5% | 3.5% | 0% |

| Mortgage insurance | None | Required <20% down | Required (MIP) | Required (guarantee fee) |

| Credit score flexibility | Moderate to high | Moderate | High | Moderate |

| Property restrictions | MPR requirements | Standard appraisal | MPR requirements | Rural areas only |

| Occupancy requirement | Primary residence | Varies by program | Primary residence | Primary residence |

For Seattle-area veterans, VA loans typically offer superior terms compared to alternatives. The combination of zero down payment and no PMI creates monthly payment savings that conventional financing cannot match at similar down payment levels.

However, veterans purchasing investment properties or vacation homes need conventional financing since VA loans require owner occupancy. Similarly, properties failing MPR standards might qualify for conventional loans with appropriate disclosures, offering alternative paths forward.

Strategic Refinancing with VA Loans

Veterans who purchased homes with conventional or FHA financing before understanding VA benefits should explore refinancing options. Converting existing mortgages to VA loans eliminates PMI, potentially reduces interest rates, and may allow cash-out access simultaneously.

The VA cash-out refinance program permits refinancing up to 100% of current property value, significantly higher than conventional cash-out maximums of 80%. For Kirkland homeowners who have accumulated substantial equity, this difference represents meaningful additional access to funds.

Calculating Refinance Benefits

Before refinancing, veterans should evaluate break-even timelines and total cost impacts. While eliminating $250 monthly in PMI offers clear savings, funding fees and closing costs require time to recoup through monthly savings.

Key refinance considerations include:

- Current interest rate versus available VA rates

- Remaining loan term and desired new term length

- Total closing costs including funding fee

- Monthly savings from rate reduction and PMI elimination

- Break-even period before positive cash flow impact

Veterans planning to remain in their Seattle homes for five or more years typically benefit from refinancing, while those anticipating shorter occupancy periods might skip refinancing costs.

Working with VA-Experienced Mortgage Professionals

The complexity of va loans for homes demands expertise that not all lenders possess equally. Veterans benefit significantly from partnering with mortgage professionals who specialize in VA lending and understand program nuances thoroughly.

Experienced VA lenders navigate eligibility questions, structure income documentation for complex employment situations, address property requirement concerns proactively, and communicate effectively with sellers and listing agents to facilitate smooth transactions.

In Seattle's fast-paced market, lender responsiveness and efficiency directly impact success rates. Veterans should seek mortgage brokers with strong local reputations, proven track records of timely closings, and specific experience serving military borrowers.

Questions to Ask Potential Lenders

When evaluating mortgage professionals for VA loans, veterans should inquire about:

- Volume of VA loans closed annually and percentage of total business

- Average timeline from application to closing

- Process for obtaining Certificates of Eligibility quickly

- Experience with complex income documentation (RSUs, bonuses, etc.)

- Approach to competitive offer situations and seller concerns

- References from recent veteran clients in similar situations

Lenders who close hundreds of VA loans annually bring institutional knowledge and process efficiency that occasional VA lenders cannot match. This expertise proves invaluable when navigating unique situations or tight timeframes.

VA Loans for Specific Seattle Neighborhoods

Different Seattle-area neighborhoods present distinct opportunities and considerations for VA homebuyers. Understanding local market dynamics, typical property types, and price ranges helps veterans target searches effectively.

Urban Seattle Options

Core Seattle neighborhoods like Capitol Hill, Queen Anne, and Ballard offer proximity to employment centers, cultural amenities, and urban lifestyle advantages. However, higher price points, older housing stock, and competitive markets require strategic approaches.

Veterans targeting these areas should prepare for potential MPR issues in older homes, budget for competitive offer situations, and consider condominiums as alternatives to single-family homes. Many Seattle condos fall within VA loan limits while providing urban convenience.

Eastside Communities

Bellevue, Redmond, and Kirkland attract tech professionals with proximity to major employers and excellent school districts. These cities feature newer construction, modern amenities, and strong appreciation potential, though prices typically exceed Seattle averages.

VA buyers in these markets benefit from combining military service benefits with tech sector income, accessing price points that challenge traditional buyers. Properties near Microsoft or Amazon campuses particularly suit veterans employed by these companies.

North Seattle Suburbs

Shoreline, Lake Forest Park, and Lynnwood provide more affordable entry points while maintaining reasonable commute access to Seattle and Eastside employment centers. These communities offer larger properties, family-friendly environments, and somewhat less competitive buying conditions.

Veterans prioritizing space and value over urban proximity often find optimal situations in these northern suburbs. First-time homebuyers particularly benefit from lower competition levels and more negotiation flexibility.

Everett and Mill Creek

Further north, Everett and Mill Creek represent the most affordable options within reasonable commuting distance of Seattle. These areas provide significant purchasing power advantages, newer developments, and growing community infrastructure.

Veterans willing to accept longer commutes can maximize their VA loan benefits in these markets, purchasing substantially more house than equivalent budgets would allow closer to Seattle. Boeing employees stationed at Everett facilities find these locations particularly convenient.

Common VA Loan Mistakes to Avoid

Even with excellent benefits, veterans can encounter challenges when approaching va loans for homes without proper preparation and guidance. Understanding common pitfalls helps avoid complications that delay or derail transactions.

Frequent mistakes include:

- Waiting until house hunting begins to verify eligibility and obtain COE

- Assuming all lenders offer equivalent VA loan expertise and service

- Overlooking funding fee costs in budget calculations

- Not documenting complex income sources properly from the start

- Choosing properties with obvious MPR issues without contingency planning

- Accepting generic pre-approvals rather than comprehensive underwriting reviews

Veterans can avoid these issues by engaging experienced mortgage professionals early, obtaining thorough pre-approval before shopping, and educating themselves about program requirements and market dynamics.

Planning Timeline Considerations

Successful VA home purchases require adequate preparation time. Veterans should begin the process at least 60-90 days before desired closing dates, allowing time for:

- Certificate of Eligibility acquisition

- Credit report review and any necessary improvements

- Income documentation compilation and verification

- Pre-approval underwriting and approval

- Property search and offer negotiation

- Purchase contract execution and processing

Rushing these steps increases stress, limits options, and potentially results in suboptimal outcomes. Strategic timeline planning creates better experiences and results.

Future Outlook for VA Loans in Seattle

The Seattle housing market continues evolving with economic trends, interest rate movements, and demographic shifts all influencing opportunities for VA homebuyers. Understanding these dynamics helps veterans time decisions strategically.

Interest rates in 2026 have stabilized compared to the volatile 2022-2024 period, creating more predictable planning environments. Veterans can model monthly payments confidently and evaluate affordability with reasonable certainty about rate locks and closing costs.

Seattle's continued growth as a technology and aerospace hub ensures sustained housing demand. While this supports property values long-term, it also maintains competitive market conditions requiring strategic approaches to successful purchases.

Legislative and Program Changes

The VA periodically adjusts loan program parameters based on housing market conditions and veteran needs. Recent years have seen improvements including eliminated loan limits for full entitlement users, expanded assumability options, and streamlined refinancing processes.

Veterans should monitor VA announcements and work with lenders who stay current on program updates. Changes to funding fees, entitlement calculations, or property requirement standards can impact purchase strategies and refinancing decisions.

Homeownership through VA loans represents not just housing acquisition but wealth building and financial stability. Seattle-area veterans who leverage these benefits position themselves advantageously in one of the nation's strongest real estate markets, building equity while enjoying the Pacific Northwest lifestyle.

VA loans for homes provide Seattle-area veterans with exceptional opportunities to achieve homeownership through zero down payment requirements, competitive rates, and eliminated mortgage insurance. Understanding eligibility, property requirements, and strategic application of these benefits maximizes success in competitive markets across Seattle, Bellevue, Redmond, and surrounding communities. Keith Akada at Mortgage Reel brings 25+ years of experience helping veterans navigate VA loans with transparency and expertise, combining military service benefits with advanced strategies for tech professionals earning stock compensation. Whether you're a first-time buyer or experienced homeowner, personalized guidance from a trusted Seattle mortgage broker ensures you maximize your VA loan advantages while closing efficiently in today's market.