Navigating the Seattle real estate market requires more than just finding the right home-it demands smart mortgage strategies that align with your financial goals and maximize your purchasing power. Whether you're a first-time buyer in Shoreline, a tech professional upgrading in Bellevue, or an investor expanding your portfolio in Kirkland, understanding the full spectrum of financing options can save you tens of thousands of dollars over the life of your loan. The right approach combines market awareness, financial preparation, and strategic timing to secure terms that support both immediate affordability and long-term wealth building.

Understanding Your Mortgage Foundation in Greater Seattle

Before exploring advanced mortgage strategies, establishing a strong financial foundation proves essential for Seattle-area homebuyers. The Pacific Northwest housing market presents unique challenges, with median home prices in Seattle, Redmond, and Bellevue often exceeding national averages by significant margins.

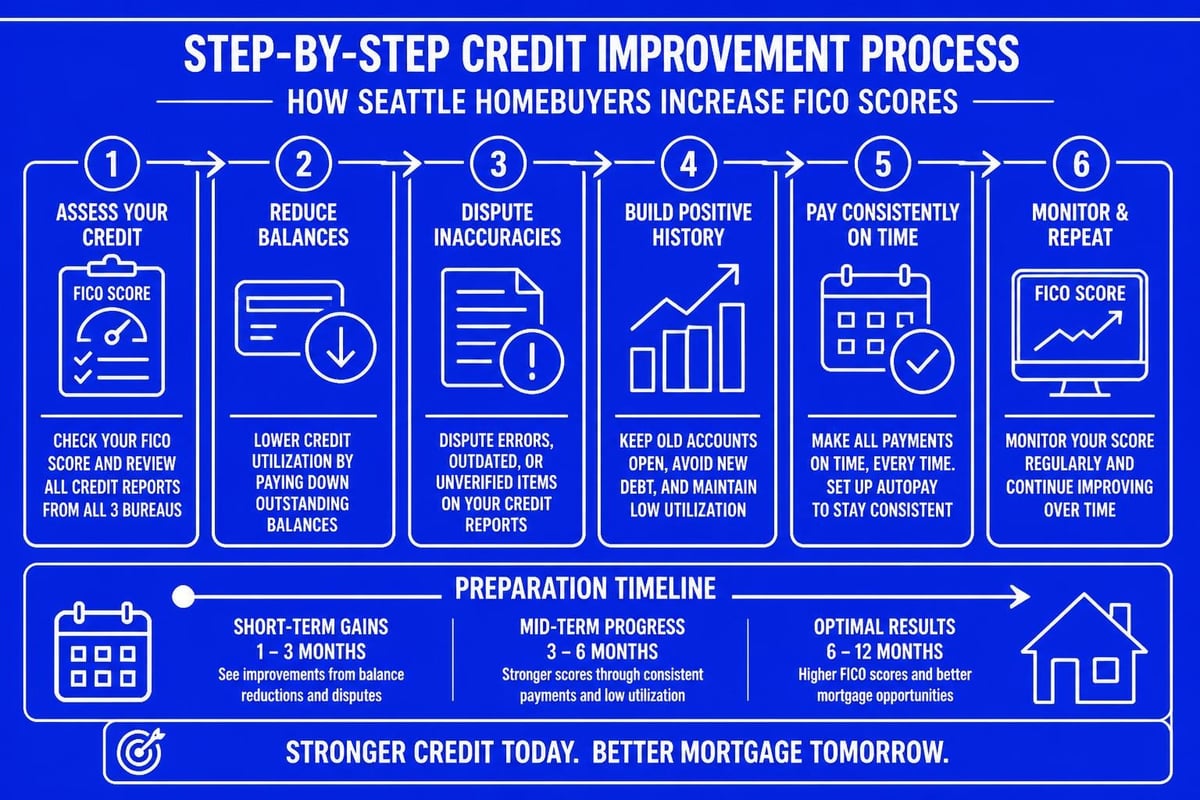

Credit Score Optimization for Better Rates

Your credit score directly impacts the interest rate lenders offer. Every 20-point increase in your FICO score can reduce your rate by approximately 0.125% to 0.25%, translating to substantial savings on a $800,000 home typical in Seattle neighborhoods.

Key credit improvement actions include:

- Paying down credit card balances below 30% utilization

- Avoiding new credit inquiries 6-12 months before applying

- Correcting errors on credit reports from all three bureaus

- Maintaining on-time payment history across all accounts

- Keeping older credit accounts open to preserve history length

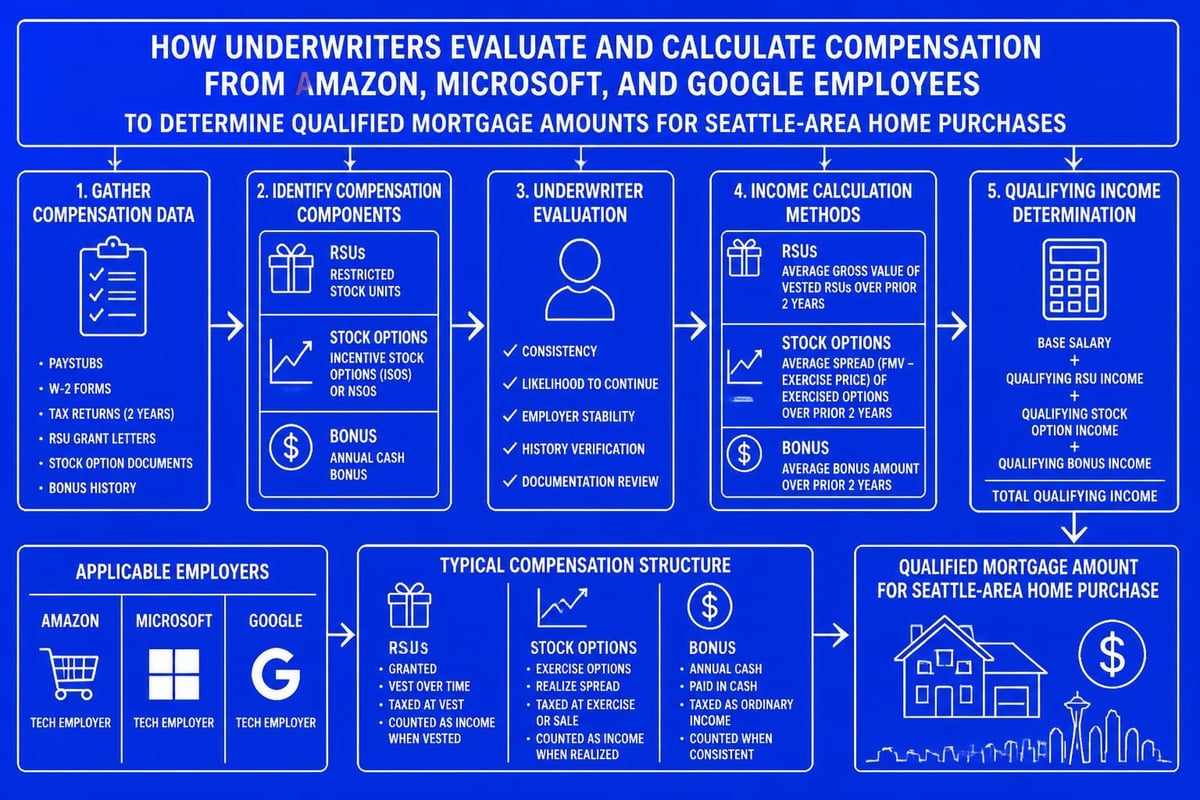

Tech professionals at Amazon, Microsoft, and Google often overlook how RSU vesting schedules impact debt-to-income ratios. Strategic timing of stock sales relative to mortgage applications requires coordination with both your financial advisor and loan officer to present the strongest application.

Down Payment Strategy Selection

The down payment percentage you choose influences multiple aspects of your mortgage terms, monthly obligations, and overall costs. While 20% down remains the traditional benchmark, several strategic alternatives exist for qualified borrowers in Lake Forest Park, Mill Creek, and Everett.

| Down Payment | PMI Requirement | Rate Impact | Best For |

|---|---|---|---|

| 3-5% | Required | Higher rates | First-time buyers, cash preservation |

| 10-15% | Required | Moderate rates | Balanced approach, growing equity |

| 20%+ | None | Best rates | PMI avoidance, lowest monthly cost |

| 25%+ | None | Optimal rates | Jumbo loans, investment properties |

Homebuyers can explore options to avoid PMI through piggyback loans, lender-paid mortgage insurance, or single-premium PMI paid upfront. Each approach carries distinct trade-offs that require analysis based on your specific financial situation and timeline.

Leveraging Loan Type Selection for Maximum Advantage

Mortgage strategies extend far beyond simply accepting the first conventional loan offer. Understanding the full range of loan products available in Washington State enables strategic matching between your financial profile and optimal financing structure.

Conventional Versus Government-Backed Programs

Conventional loans offer flexibility for borrowers with strong credit and substantial down payments, while FHA, VA, and USDA loans provide alternative pathways with different qualification criteria and cost structures.

Conventional loan advantages:

- No upfront mortgage insurance premium

- PMI removal at 80% loan-to-value ratio

- Higher loan limits for jumbo properties

- Flexible property type eligibility

- Streamlined processing for well-qualified borrowers

Government program benefits:

- Lower down payment requirements (3.5% FHA, 0% VA/USDA)

- More flexible credit score minimums

- Assumable loan features on VA and FHA products

- Seller concession allowances up to 6%

- Support for borrowers with limited credit history

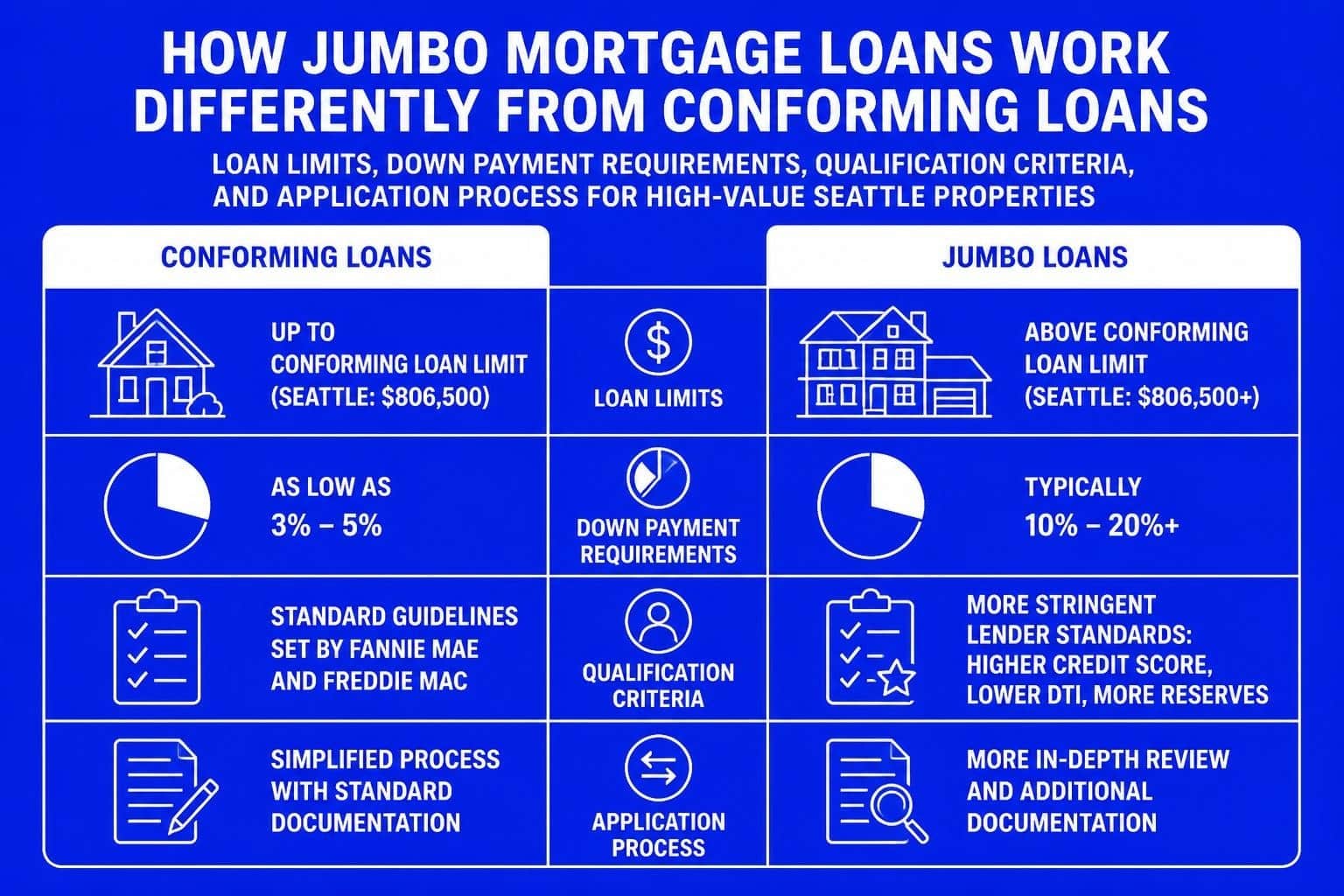

Seattle-area borrowers frequently benefit from conventional jumbo loans when purchasing homes above conforming loan limits, particularly in neighborhoods like Bellevue's downtown core or waterfront properties in Kirkland. These loans require meticulous documentation but offer competitive rates for qualified applicants with substantial compensating factors.

Fixed-Rate Versus Adjustable-Rate Mortgages

Interest rate structure represents one of the most consequential decisions in your mortgage strategy. The choice between fixed and adjustable rates depends on your timeline, risk tolerance, and market outlook.

Fixed-rate mortgages provide payment stability and protection against rising rates-critical benefits during uncertain economic periods. Borrowers planning to remain in their Shoreline or Lynnwood homes for seven or more years typically benefit from locking in predictable costs.

Adjustable-rate mortgages (ARMs) offer lower initial rates, often 0.5% to 0.75% below comparable fixed-rate products. For tech professionals expecting relocation, career advancement, or home upgrades within five years, 5/1 or 7/1 ARM products can reduce total interest costs significantly while maintaining rate stability during the ownership period.

Advanced Mortgage Strategies for Seattle Tech Professionals

The concentration of technology employers throughout the Greater Seattle area creates unique opportunities for specialized mortgage strategies that leverage equity compensation and accelerated income growth trajectories.

Qualifying Stock Compensation and RSU Income

Restricted stock units, employee stock purchase plans, and performance bonuses require specific documentation and calculation methods for mortgage qualification purposes. Understanding how underwriters evaluate these income sources enables accurate pre-qualification and prevents application surprises.

RSU qualification requirements typically include:

- Two-year history of stock compensation receipt

- Vesting schedule documentation from employer

- Calculation using average or conservative value projections

- Verification through W-2s and pay stubs

- Assessment of volatility and likelihood of continuation

Borrowers with substantial equity compensation can leverage these income sources to qualify for higher loan amounts than base salary alone would support. This proves particularly valuable when purchasing homes in premium Seattle neighborhoods or upgrading to accommodate growing families.

Jumbo Loan Optimization Tactics

Jumbo loans-those exceeding conforming loan limits of $806,500 in 2026 for most Washington State counties-require enhanced qualification standards but offer financing for Seattle's higher-priced properties without portfolio loan limitations.

Strategic approaches to jumbo loan qualification include maintaining larger cash reserves, reducing debt-to-income ratios below 43%, and demonstrating employment stability with established employers. Borrowers should review multiple lenders when comparing jumbo loan terms since rate variations between institutions can exceed differences in conventional loan pricing.

Portfolio diversification matters significantly in jumbo loan underwriting. Lenders evaluate not just income but overall financial strength, including retirement accounts, investment portfolios, and liquid reserves capable of covering 12-24 months of mortgage payments.

Rate Optimization and Timing Strategies

Securing favorable interest rates requires both preparation and strategic timing. Small rate differences compound dramatically over 30-year loan terms, making optimization efforts worthwhile for all borrowers.

Point Purchase Analysis

Mortgage points-upfront payments reducing your interest rate-offer a direct trade-off between immediate cash outlay and long-term savings. Each point typically costs 1% of the loan amount and reduces rates by approximately 0.25%.

The break-even calculation determines whether point purchases make financial sense based on your anticipated ownership timeline and alternative investment opportunities for that capital.

| Loan Amount | Points Cost | Rate Reduction | Monthly Savings | Break-Even Period |

|---|---|---|---|---|

| $600,000 | $6,000 | 0.25% | $95 | 63 months |

| $600,000 | $12,000 | 0.50% | $190 | 63 months |

| $800,000 | $8,000 | 0.25% | $125 | 64 months |

| $800,000 | $16,000 | 0.50% | $250 | 64 months |

Borrowers planning to remain in Mill Creek, Everett, or Lake Forest Park homes beyond the break-even period benefit from point purchases, while those expecting shorter ownership timelines should preserve cash for other purposes.

Rate Lock Timing Decisions

Interest rate volatility creates opportunities and risks during the mortgage process. Rate locks protect approved borrowers from increases but prevent capturing decreases during the lock period. Strategic lock timing balances protection against opportunity cost.

Implementing effective rate shopping strategies involves obtaining quotes from multiple lenders simultaneously, comparing annual percentage rates rather than just interest rates, and understanding fee structures that impact total borrowing costs.

Float-down provisions offer middle-ground solutions, allowing one-time rate adjustments if rates decrease significantly during your lock period. These options typically carry slightly higher initial rates or additional fees but provide insurance against meaningful market movements.

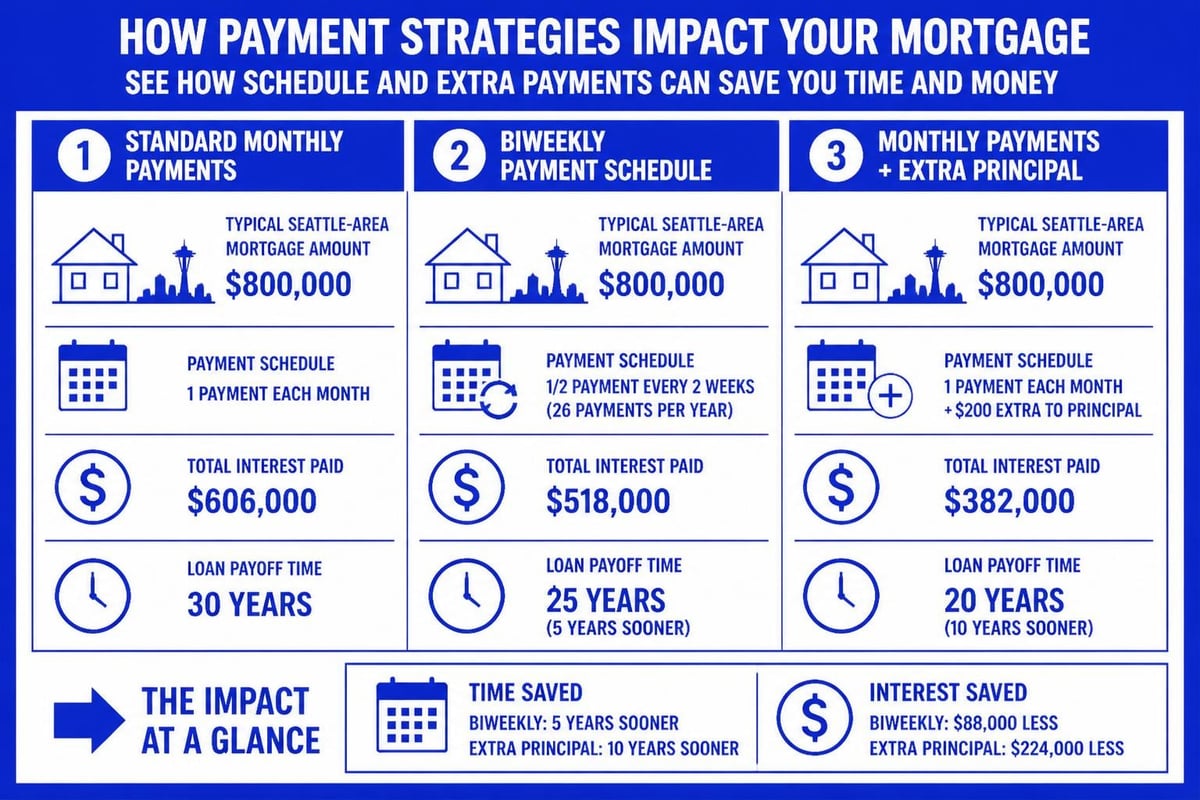

Accelerated Payoff Mortgage Strategies

Building equity faster through strategic payment approaches reduces total interest costs and accelerates the path to mortgage-free homeownership. These mortgage strategies particularly benefit borrowers with stable income growth expectations and minimal higher-return debt obligations.

Extra Principal Payment Methods

Additional principal payments directly reduce your loan balance, decreasing future interest charges and shortening the loan term. Even modest extra payments compound significantly over time.

Effective extra payment approaches include:

- Adding fixed amounts to each monthly payment

- Applying annual bonuses or tax refunds to principal

- Making one extra full payment annually (13 payments per year)

- Rounding up payment amounts to convenient figures

- Allocating salary increases to mortgage acceleration

A borrower with a $700,000 mortgage at 6.5% paying an extra $500 monthly would save approximately $178,000 in interest and repay the loan 9 years earlier. For Seattle tech professionals receiving regular RSU vesting, directing a portion toward mortgage principal creates forced savings while reducing interest obligations.

Biweekly Payment Conversion

Biweekly payment plans split your monthly mortgage payment in half and submit payments every two weeks. This schedule results in 26 half-payments annually-equivalent to 13 full monthly payments-automatically accelerating payoff without requiring large lump-sum contributions.

The strategy works particularly well for borrowers paid on biweekly schedules, aligning mortgage obligations with income receipt and simplifying budgeting. Implementation requires either formal program enrollment through your servicer or manual extra payment submission using your existing monthly billing.

Refinancing as an Ongoing Strategy

Mortgage strategies extend beyond the initial purchase. Ongoing portfolio management includes periodic refinancing evaluation to optimize terms as circumstances change.

Rate-and-Term Refinancing Opportunities

Rate-and-term refinancing replaces your existing mortgage with new terms, potentially lowering your interest rate, changing your loan duration, or both. Borrowers who purchased or last refinanced when rates exceeded current market levels by 0.75% or more should analyze potential benefits.

The refinancing decision requires calculating break-even periods based on closing costs, comparing total interest savings over your expected remaining ownership timeline, and assessing current home values to ensure adequate equity positions. Homeowners in appreciating Seattle neighborhoods often discover improved loan-to-value ratios that qualify them for better pricing tiers.

Cash-Out Refinancing for Investment

Cash-out refinancing converts home equity to liquid capital while restructuring your mortgage. This approach funds home improvements, consolidates higher-rate debt, or provides investment capital for additional real estate acquisitions.

Strategic cash-out usage generates returns exceeding the incremental borrowing cost. Converting 6.5% mortgage debt to eliminate 18% credit card balances produces immediate arbitrage. Similarly, extracting equity from a Seattle primary residence to purchase a rental property in Everett or Lynnwood can accelerate wealth building through leverage.

Tax Planning and Mortgage Interest Deductions

Mortgage strategies intersect significantly with tax planning, particularly for high-earning tech professionals in elevated tax brackets. Understanding deduction limitations and optimization techniques reduces after-tax borrowing costs.

The Tax Cuts and Jobs Act of 2017 limited mortgage interest deductions to loans of $750,000 or less for married couples filing jointly ($375,000 for single filers) on primary and secondary residences combined. Interest on amounts exceeding these limits remains non-deductible, affecting jumbo loan borrowers throughout Seattle's premium neighborhoods.

Itemization threshold considerations matter equally. The standard deduction of $30,000 for married couples in 2026 requires substantial deductible expenses-including mortgage interest, property taxes (capped at $10,000), and charitable contributions-before itemization provides tax benefits.

Tax optimization tactics include:

- Timing points and prepaid interest for maximum deduction years

- Bunching charitable contributions and property tax payments

- Maintaining separate tracking for deductible versus non-deductible interest

- Coordinating mortgage decisions with overall tax planning strategies

- Consulting tax professionals about AMT implications on larger loans

Relationship Banking and Portfolio Lending Advantages

Establishing comprehensive banking relationships with mortgage lenders can unlock preferential pricing, streamlined processing, and enhanced flexibility for complex financial profiles common among Seattle-area borrowers.

Portfolio lending programs offer customized underwriting for situations falling outside conventional guidelines-such as recently self-employed borrowers, those with substantial assets but variable income, or purchasers of unique properties in Kirkland or Bellevue requiring specialized appraisal approaches.

Relationship discounts typically reduce rates by 0.125% to 0.25% for borrowers maintaining specified deposit balances, automating payments from institution accounts, or consolidating multiple financial services. While seemingly modest, these reductions compound to five-figure savings on large Seattle-area mortgages over full loan terms.

Private banking services for high-net-worth borrowers provide white-glove processing, dedicated underwriting teams, and expedited closing timelines-critical advantages in competitive markets requiring 9-business-day closings to secure desirable properties against multiple offers.

Market Timing and Economic Cycle Awareness

While timing markets perfectly proves impossible, awareness of economic cycles and rate trends informs strategic decision-making about purchase timing, product selection, and refinancing opportunities.

Federal Reserve policy significantly influences mortgage rates through its federal funds rate adjustments and bond-purchasing programs. Monitoring economic indicators-including inflation trends, employment data, and GDP growth-provides context for rate forecasting and strategic planning.

Seattle's robust technology sector creates local economic dynamics somewhat insulated from national trends but not immune to broader market forces. Understanding both macro and micro factors enables informed decisions about ARM versus fixed-rate selection, point purchases, and lock timing.

Borrowers should recognize that managing existing mortgages during high-rate environments requires different strategies than optimizing during low-rate periods, including accelerated payoff emphasis and portfolio rebalancing rather than refinancing focus.

Documentation and Application Process Optimization

Efficient mortgage processing requires meticulous documentation preparation and proactive communication. Delays frequently stem from incomplete information submission rather than underwriting complexity.

Essential documentation categories include:

- Two years of W-2s and tax returns for all borrowers

- Recent pay stubs covering 30-day periods

- Two months of bank statements for all accounts

- Investment account statements showing balances and activity

- Retirement account documentation when using for reserves

- Explanation letters for credit inquiries, gaps in employment, or large deposits

Seattle tech professionals should prepare additional documentation for stock compensation, including vesting schedules, historical award letters, and employer verification of continuation likelihood. Organizing these materials before application submission accelerates processing and demonstrates financial sophistication to underwriters.

Digital document management systems streamline ongoing communication with loan officers and processors. Responsive borrowers who promptly address conditional approval requirements often close significantly faster than those treating the process passively-particularly important in competitive Seattle neighborhoods where delayed closings risk transaction failure.

Strategic mortgage planning combines market knowledge, financial optimization, and proactive decision-making to minimize costs while maximizing purchasing power throughout your homeownership journey. Whether you're entering the Seattle market for the first time, upgrading to accommodate life changes, or refinancing to improve existing terms, these mortgage strategies provide frameworks for confident decisions aligned with your long-term financial goals. Keith Akada brings 25+ years of experience helping Seattle, Bellevue, Redmond, and Kirkland homebuyers navigate complex financing decisions with transparency and expertise, specializing in tech professional income qualification and jumbo loan optimization. Discover how strategic mortgage planning can maximize your purchasing power and long-term savings with Mortgage Reel.