Seattle's competitive real estate market has driven many homebuyers beyond conventional loan limits, making the jumbo mortgage an essential financing tool for properties across Seattle, Bellevue, Redmond, and Kirkland. In 2026, understanding how these larger loans work is crucial for anyone shopping in the region's higher-priced neighborhoods. Whether you're a tech professional leveraging stock compensation or an established homeowner upgrading to a waterfront property, jumbo loans offer the purchasing power needed to compete in one of America's most dynamic housing markets.

What Defines a Jumbo Mortgage in Seattle

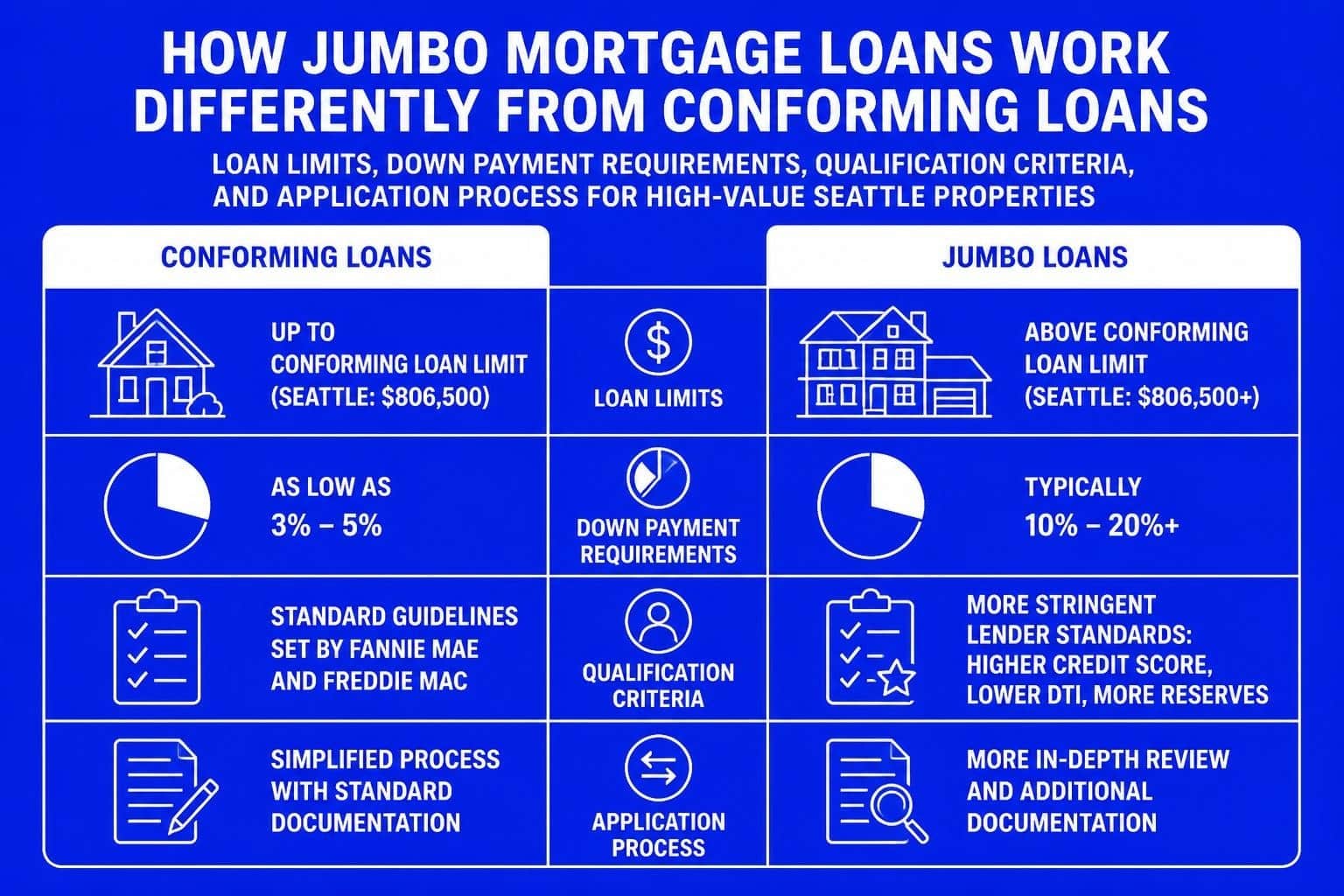

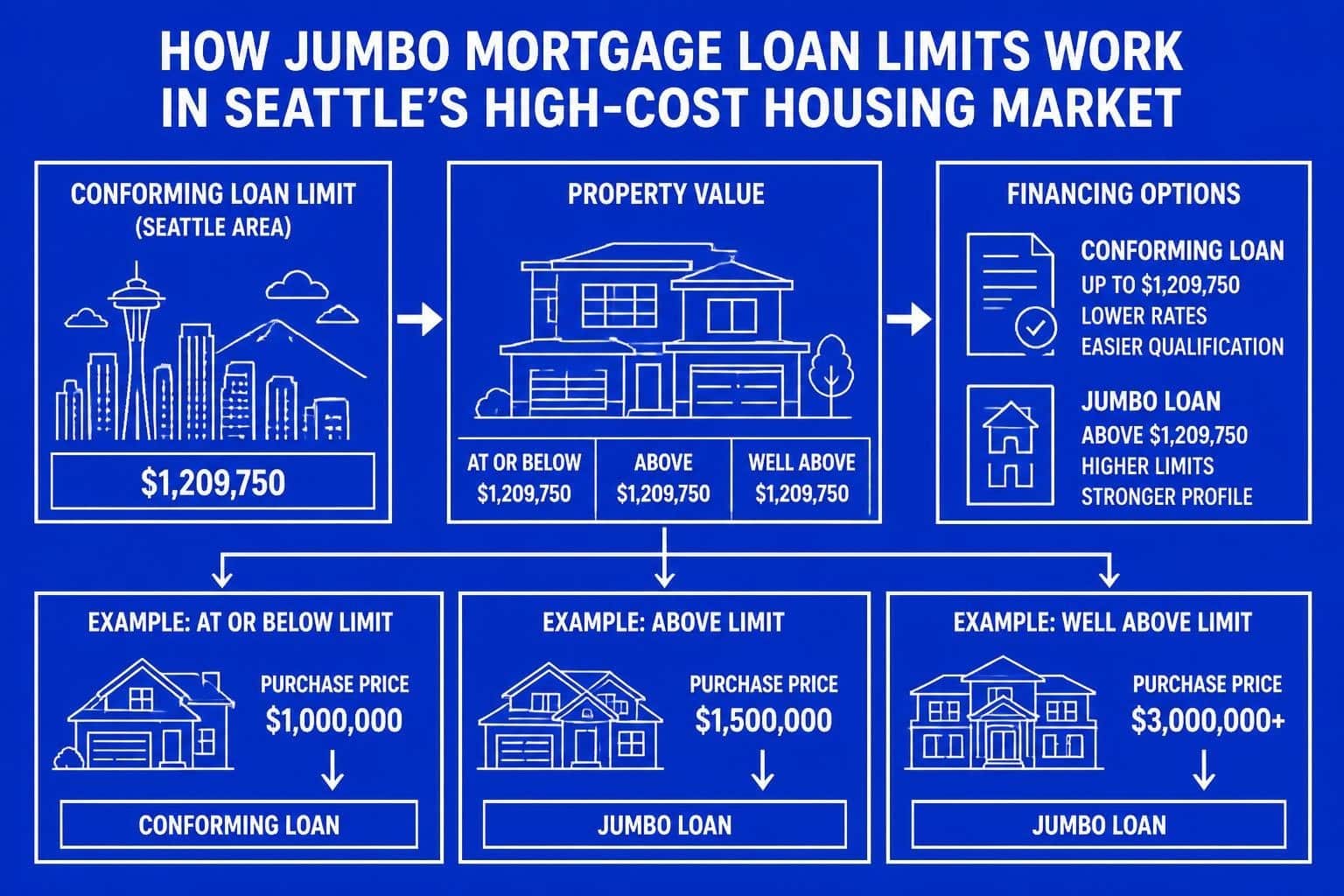

A jumbo mortgage is any home loan that exceeds the conforming loan limits established by the Federal Housing Finance Agency (FHFA). For 2026, the conforming loan limit in most Seattle-area counties sits at $806,500 for single-family homes, though this amount adjusts annually based on housing price trends.

When your financing needs surpass this threshold, you enter jumbo territory. These loans aren't backed by Fannie Mae or Freddie Mac, which means lenders assume greater risk and typically impose stricter qualification requirements.

Current Market Dynamics

The Seattle metro area consistently ranks among the nation's highest-cost housing markets. Here's what that means for local buyers:

- Median home prices in Bellevue frequently exceed $1.2 million

- Waterfront properties in Kirkland often require $2 million or more

- Even renovated homes in Shoreline and Lynnwood can push past conforming limits

- Downtown Seattle condos routinely demand jumbo financing

This reality makes understanding jumbo mortgage options essential for anyone serious about purchasing in competitive neighborhoods.

Qualification Requirements for Jumbo Loans

Lenders view jumbo mortgages as higher-risk products, which translates directly into more stringent qualification standards. Understanding these requirements before you start house hunting can save considerable time and frustration.

Credit Score Expectations

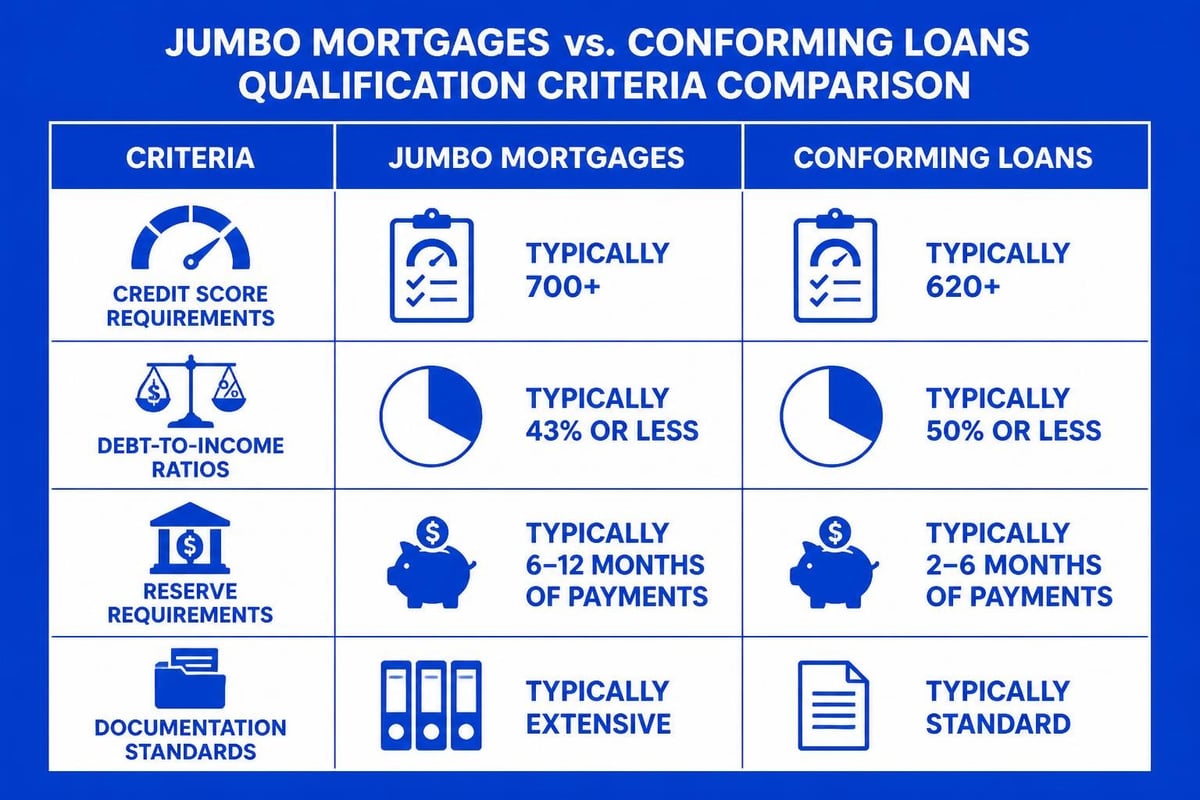

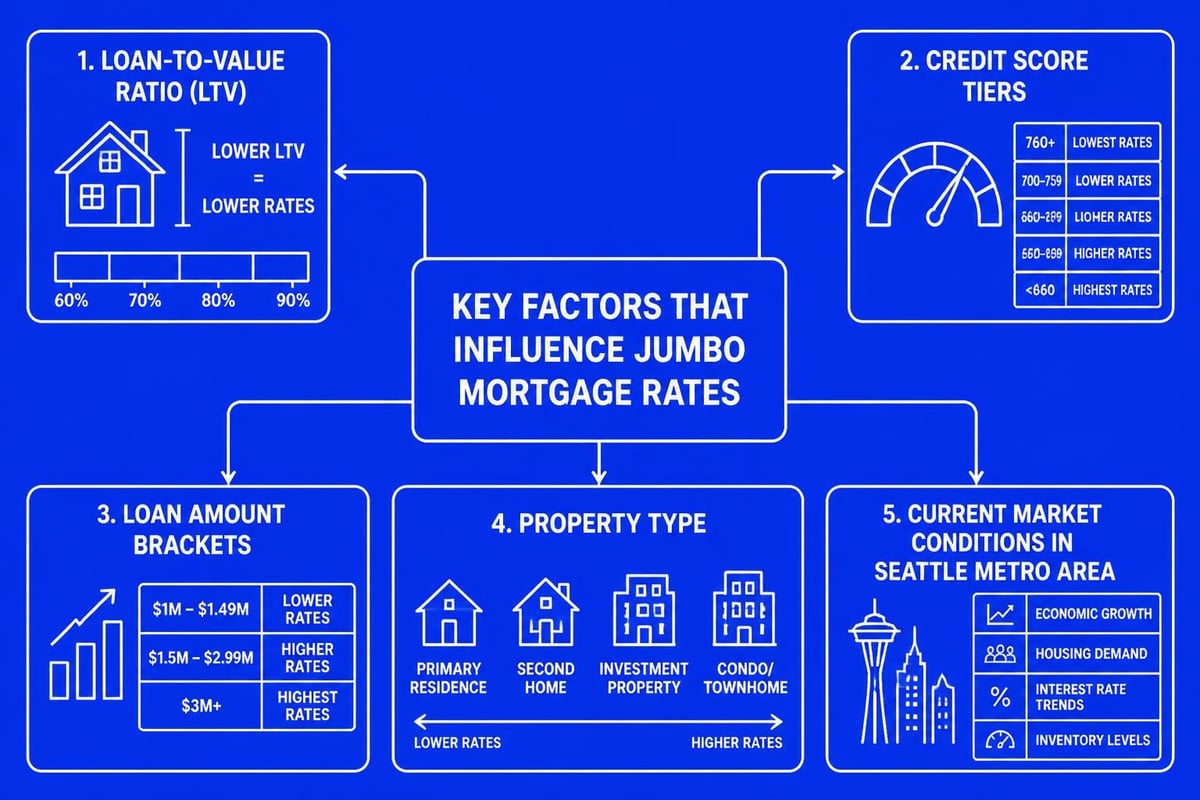

Most lenders require a minimum credit score of 700 for jumbo financing, though competitive rates typically start at 720 or higher. For loan amounts exceeding $2 million, some institutions may require scores of 740 or above.

The logic is straightforward: without government backing, lenders need confidence in your creditworthiness and repayment history. A strong credit profile demonstrates financial responsibility and reduces perceived risk.

Income Documentation and Stability

Expect comprehensive income verification. Traditional W-2 employees should prepare to provide:

- Two years of tax returns with all schedules

- Recent pay stubs covering the past 30 days

- W-2 forms for the previous two years

- Written verification of employment

For Seattle's tech workforce, qualifying RSUs, stock options, and bonus income requires specialized expertise. These compensation forms can dramatically increase your buying power when properly documented and averaged according to underwriting guidelines.

Debt-to-Income Ratio Standards

Jumbo lenders typically cap your total debt-to-income (DTI) ratio at 43%, though some programs allow up to 45% with compensating factors like substantial reserves or higher credit scores.

Your DTI calculation includes:

- Proposed mortgage payment (principal, interest, taxes, insurance)

- HOA fees or condo dues

- Existing installment loans (auto, student, personal)

- Minimum credit card payments

- Other real estate obligations

In markets like Mill Creek and Lake Forest Park, where property taxes can be substantial, accurately projecting your total housing payment is critical for staying within DTI guidelines.

Down Payment and Reserve Requirements

Unlike conforming loans that may accept down payments as low as 3%, jumbo mortgages demand more substantial upfront investment and financial cushion.

Minimum Down Payment Thresholds

| Loan Amount | Typical Minimum Down Payment | Preferred Down Payment |

|---|---|---|

| $806,501 – $1,500,000 | 10% – 15% | 20% |

| $1,500,001 – $2,500,000 | 15% – 20% | 25% |

| $2,500,001+ | 20% – 30% | 30% |

Putting down 20% or more typically secures better rates and eliminates private mortgage insurance (PMI), though some jumbo products don't require PMI regardless of down payment size.

Cash Reserve Requirements

Lenders want assurance you can weather financial disruptions. Reserve requirements typically range from six to twelve months of total housing payments, held in liquid accounts after closing.

For a $1.5 million home with a $7,500 monthly payment, you might need $45,000 to $90,000 in reserves beyond your down payment and closing costs. These funds must be sourced, seasoned, and verified through bank statements.

Interest Rates and Pricing Structure

According to current jumbo mortgage rate data, rates on these loans fluctuate based on multiple variables. Understanding what drives pricing helps you time your application and negotiate effectively.

Rate Influencers

Credit score impact: A 760 score might secure a rate 0.25% to 0.50% lower than a 700 score on the same loan amount. Over 30 years on a $1 million mortgage, that difference represents tens of thousands in interest savings.

Loan-to-value ratios: Lower LTV ratios translate to better rates. A borrower putting 30% down typically receives pricing advantages over someone contributing 15%.

Property type and use: Single-family primary residences receive the best rates. Investment properties, condos, and second homes may carry rate premiums of 0.375% to 0.75%.

Fixed vs. Adjustable Rate Options

Jumbo borrowers can choose between fixed-rate mortgages (FRMs) and adjustable-rate mortgages (ARMs). In 2026's rate environment, understanding these options is particularly important.

- 30-year fixed: Provides payment stability but typically carries higher initial rates

- 15-year fixed: Builds equity faster with lower rates but higher monthly payments

- 7/1 ARM: Fixed for seven years, then adjusts annually based on index performance

- 10/1 ARM: Offers longer initial fixed period before adjustment

For professionals planning shorter ownership periods or anticipating income growth, ARMs can provide meaningful savings during the fixed period while maintaining competitive caps on future adjustments.

Navigating Seattle's High-Cost Housing Markets

Seattle's diverse neighborhoods each present unique opportunities and challenges for jumbo borrowers. Local market knowledge significantly impacts your financing strategy.

Bellevue and Eastside Considerations

Bellevue's luxury condo market and high-end single-family neighborhoods routinely demand jumbo financing. Properties near tech campuses combine premium pricing with strong appreciation potential, making them attractive despite higher entry costs.

When evaluating mortgage financing options for Eastside properties, consider:

- HOA fees that can exceed $1,000 monthly in luxury buildings

- Property tax rates that vary by specific location within King County

- Resale demand driven by proximity to major employers

- Potential rental income if converting to investment property later

Shoreline and Lynnwood Opportunities

These markets offer relative value compared to central Seattle while maintaining excellent school districts and community amenities. Many renovated homes in established neighborhoods now exceed conforming limits, particularly those with significant square footage or waterfront access.

Buyers in Everett and Mill Creek often discover that jumbo financing opens doors to properties offering more space and features than similarly priced conforming-limit homes closer to downtown Seattle.

Special Considerations for Tech Professionals

Seattle's concentration of technology employers creates unique opportunities for jumbo borrowers with non-traditional income streams. Stock compensation, RSUs, and performance bonuses can substantially increase qualifying income when properly documented.

Qualifying Stock-Based Compensation

Underwriting guidelines allow lenders to include various equity compensation forms, though methodology varies by lender and compensation structure:

Restricted Stock Units (RSUs): Typically averaged over the vesting period or previous two years, whichever provides the most conservative projection. Lenders examine vesting schedules and stock price stability.

Stock options: May be calculated based on exercise value minus strike price, often requiring sustained profitability over time.

Annual bonuses: Usually averaged over two years with documentation showing consistency and likelihood of continuation.

Working with experienced professionals who understand how to present compensation for jumbo loans maximizes your qualifying power without triggering documentation issues or delays.

Fast-Close Capabilities

In competitive Seattle markets, closing speed matters. Properties in desirable neighborhoods often receive multiple offers, and sellers favor buyers who can close quickly with confidence.

Advanced underwriting processes enable qualified borrowers to close jumbo loans in as few as 9 to 15 business days, providing a significant competitive advantage when bidding against cash offers or slower conventional financing.

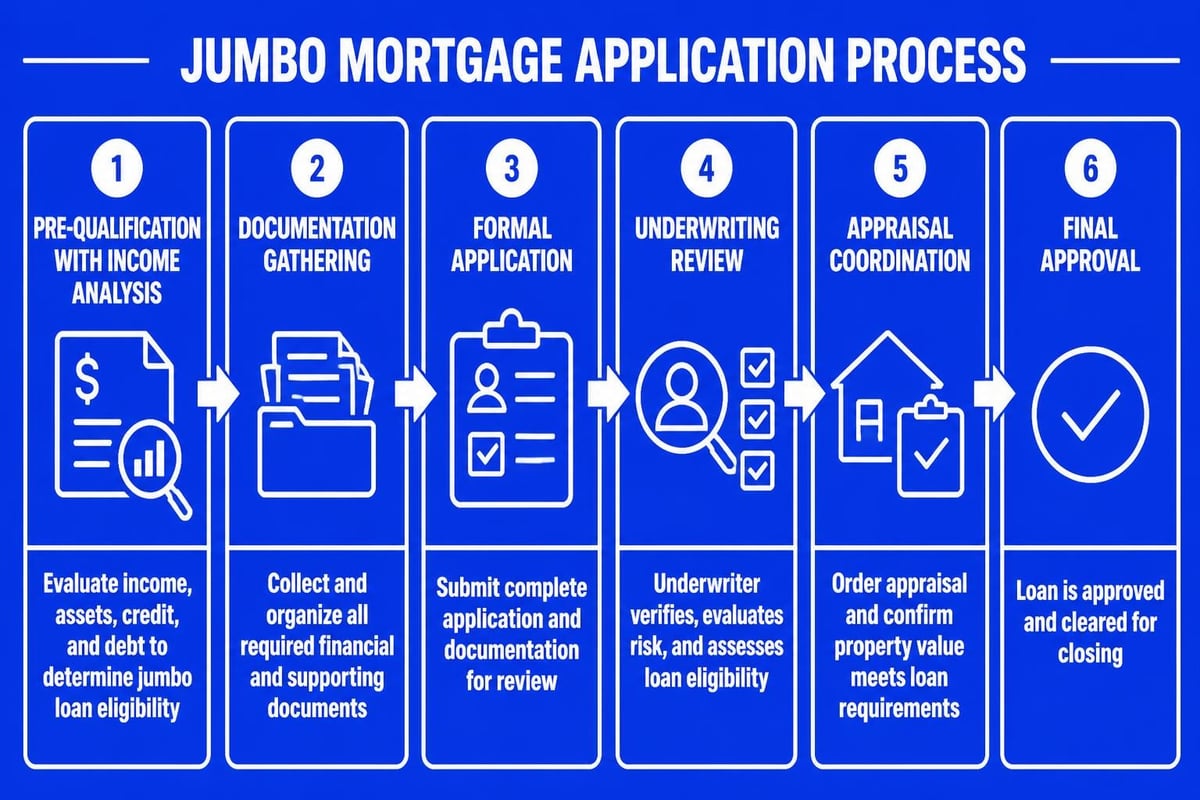

Documentation and Underwriting Process

Jumbo mortgage underwriting involves thorough documentation review. Being prepared accelerates approval and prevents last-minute surprises.

Essential Documentation Checklist

Gather these items before applying:

- Income verification: Two years tax returns with all schedules, recent pay stubs, W-2s, bonus/RSU statements

- Asset documentation: Two to three months bank statements for all accounts, investment account statements, retirement account summaries

- Credit authorization: Signed authorization for credit report pulls

- Property information: Purchase agreement, property address, estimated value

- Additional items: Divorce decrees (if applicable), gift letters for down payment assistance, business ownership documentation if self-employed

Timeline Expectations

| Phase | Duration | Key Activities |

|---|---|---|

| Pre-approval | 3-5 days | Initial application, credit review, preliminary underwriting |

| Processing | 5-10 days | Full documentation review, employment verification, appraisal order |

| Underwriting | 3-7 days | Comprehensive file review, conditions issued |

| Clear to Close | 1-3 days | Final conditions satisfied, funding authorization |

Total timeline varies based on file complexity, but well-documented applications with responsive borrowers typically close within 15 to 25 days.

Comparing Loan Programs and Lenders

Not all jumbo products offer identical terms. Comparing options ensures you secure optimal financing for your specific situation.

Portfolio vs. Correspondent Lending

Portfolio lenders keep loans on their own books rather than selling to investors. This approach can provide more flexibility on underwriting guidelines but may offer less competitive rates.

Correspondent lenders originate loans meeting investor criteria, then sell them on the secondary market. This model often delivers better rates through competition among multiple investors.

Evaluating Total Cost

Look beyond interest rates when comparing offers. Consider:

- Origination fees and lender charges

- Discount points required to achieve quoted rates

- Third-party closing costs

- Prepayment penalty provisions

- Rate lock periods and extension fees

A loan with a slightly higher rate but significantly lower fees might cost less over your expected ownership period than a lower-rate option with substantial upfront charges.

Risk Mitigation and Long-Term Strategy

Jumbo mortgages represent significant financial commitments requiring careful long-term planning. Strategic approaches minimize risk and maximize benefits.

Building Equity Protection

Larger loan balances mean slower equity accumulation in early years. Strategies to accelerate equity growth include:

- Making extra principal payments when cash flow allows

- Choosing 15-year terms if monthly payment fits comfortably in budget

- Refinancing to shorter terms as income increases

- Applying windfalls (bonuses, stock sales) toward principal reduction

Interest Deduction Considerations

Current tax law limits mortgage interest deductions to interest paid on the first $750,000 of acquisition debt for primary residences. Understanding these implications helps with tax planning and overall cost evaluation.

Consult tax professionals to optimize deduction strategies, especially when financing exceeds deduction limits or juggling multiple properties.

Common Mistakes to Avoid

Even sophisticated borrowers make errors that complicate jumbo applications or cost money. Awareness prevents these pitfalls.

Timing Missteps

Opening new credit accounts, making large purchases, or changing jobs during the application process can derail approvals. Maintain financial stability from application through closing.

Large deposits unrelated to regular income require extensive documentation and sourcing. Avoid moving money between accounts unnecessarily during the loan process.

Overlooking Total Cost of Ownership

Monthly mortgage payments represent just one component of housing costs. Property taxes in King County, homeowner's insurance for high-value properties, maintenance reserves, and HOA fees all impact affordability.

For a $1.5 million property in Kirkland, total monthly housing costs might include:

- Principal and interest: $6,800

- Property taxes: $1,875

- Homeowner's insurance: $350

- HOA fees: $650

- Total: $9,675 monthly

Ensure your budget comfortably accommodates the complete picture, not just the mortgage payment.

Alternative Strategies for High-Cost Properties

Some buyers benefit from creative approaches rather than traditional single-loan jumbo financing.

Piggyback Loan Structures

Combining a conforming first mortgage with a second mortgage or HELOC can sometimes provide advantages:

- First mortgage at $806,500 (conforming limit)

- Second mortgage or HELOC for additional needed funds

- Potential for better blended rate than single jumbo loan

- Increased complexity with two loans and payments

This approach works best when the combined rate and fees produce savings versus a single jumbo mortgage.

Delay and Build Strategy

For buyers with flexibility, purchasing a home within conforming limits initially, then trading up after building additional equity and income, spreads the financial commitment across time while housing appreciation works in your favor.

This strategy particularly benefits younger professionals anticipating significant career and income growth over the next five to ten years.

Understanding jumbo mortgage requirements, processes, and strategies positions Seattle-area homebuyers to confidently pursue properties that match their goals and lifestyle. Whether you're relocating from another tech hub, upgrading from a starter home, or investing in waterfront property, specialized expertise makes the difference between frustrating delays and smooth closings. Keith Akada brings 25+ years of experience helping Seattle, Bellevue, Redmond, and Kirkland clients navigate complex jumbo financing, with particular expertise qualifying stock compensation and equity income for tech professionals. Explore your jumbo loan options and discover how strategic financing can maximize your purchasing power at Mortgage Reel.