Deciding whether to pay off mortgage loan debt early represents one of the most significant financial crossroads for Seattle-area homeowners. With median home values exceeding $800,000 in neighborhoods throughout Seattle, Bellevue, and Redmond, the decision carries substantial weight. Tech professionals with substantial equity compensation, established homeowners nearing retirement, and strategic real estate investors all face this question differently. Understanding the mathematical realities, tax implications, and opportunity costs helps you make an informed choice aligned with your broader financial strategy.

Understanding the Financial Mathematics Behind Early Payoff

The decision to pay off mortgage loan balances ahead of schedule starts with understanding the numbers. Your mortgage amortization schedule reveals how much interest you'll pay over the full term versus how much you could save by accelerating payments.

Key factors influencing your savings potential:

- Current interest rate on your mortgage

- Remaining loan term and principal balance

- Your marginal tax bracket and deduction eligibility

- Alternative investment returns you could reasonably expect

- Your personal risk tolerance and financial security needs

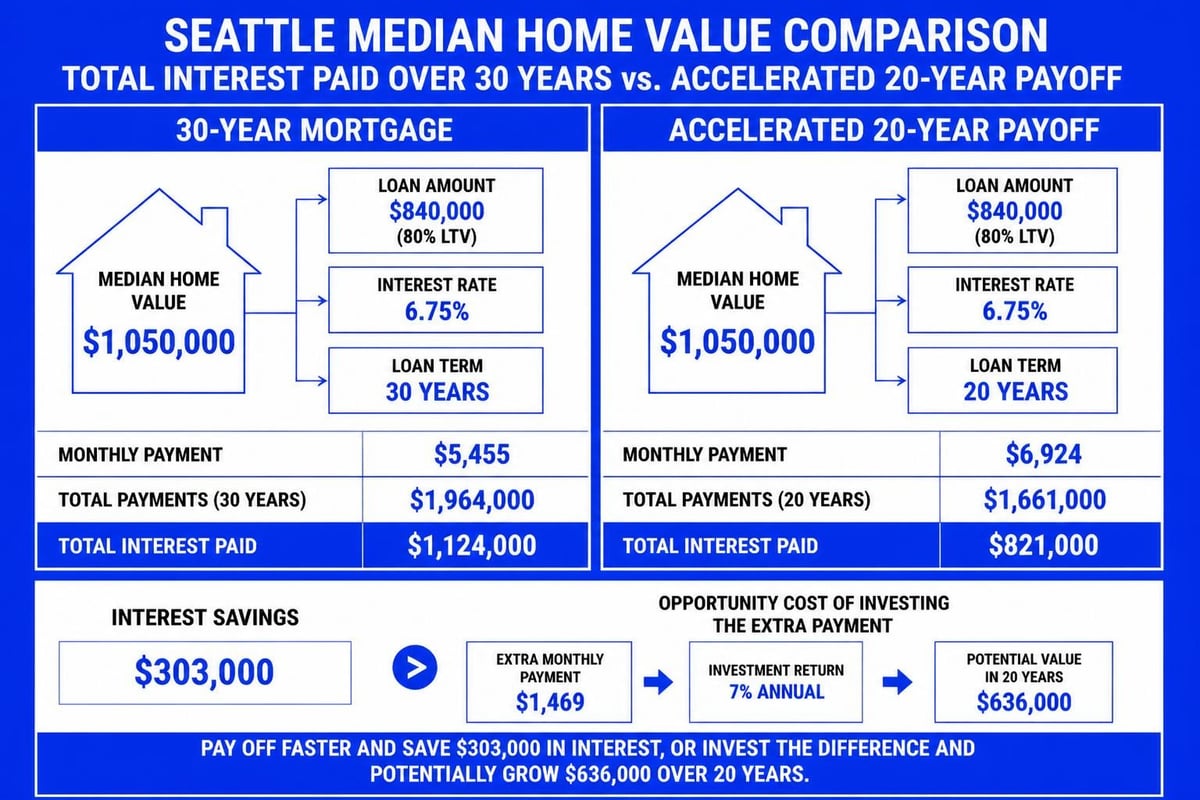

For a $600,000 mortgage at 6.5% interest over 30 years, you'll pay approximately $758,000 in interest alone. Making one extra payment annually could save you over $120,000 in interest and shorten your loan term by nearly six years. However, these savings must be weighed against what those same dollars could accomplish in retirement accounts, taxable investments, or business opportunities.

Interest Rate Environment and Refinancing Considerations

The current mortgage rate environment significantly influences the pay off mortgage loan decision. Homeowners who locked in rates below 4% between 2020 and 2021 face a fundamentally different calculation than those with rates above 6.5% in 2025 and 2026.

Low-rate borrowers often benefit more from investing extra payments rather than accelerating payoff. When your mortgage costs 3.25% but diversified index funds historically return 8-10% annually, the mathematical advantage tilts toward investing. Conversely, homeowners with rates above 6% see more compelling interest savings from early payoff.

Seattle tech professionals frequently reassess this decision when receiving substantial RSU vestings or annual bonuses. Rather than making an all-or-nothing choice, many implement a balanced approach-directing some windfalls toward mortgage principal while investing others in tax-advantaged retirement accounts.

Tax Implications of Paying Off Your Mortgage

The tax considerations when paying off a mortgage early deserve careful analysis, particularly for high-income Seattle homeowners. The mortgage interest deduction historically provided significant tax benefits, though recent tax law changes have reduced its impact for many borrowers.

| Tax Consideration | Before Payoff | After Payoff |

|---|---|---|

| Mortgage Interest Deduction | Available (up to $750k loan) | Eliminated |

| Standard vs. Itemized | May itemize if total deductions high | More likely to use standard deduction |

| Effective Interest Cost | Reduced by tax savings | N/A |

| Cash Flow | Monthly payment continues | Payment eliminated |

For 2026, the standard deduction stands at $14,600 for single filers and $29,200 for married couples filing jointly. Many Seattle homeowners find their mortgage interest, property taxes (capped at $10,000 SALT deduction), and charitable contributions no longer exceed these thresholds, especially as loan balances decline and interest payments decrease.

Calculating Your True After-Tax Interest Cost

Understanding your effective interest rate after tax benefits provides clarity. If you're paying 6.5% interest and receive a tax benefit in the 32% federal bracket, your effective cost drops to approximately 4.42%. However, how paying off your mortgage affects your taxes extends beyond just the interest deduction.

Once you pay off mortgage loan debt completely, you'll likely shift to the standard deduction unless you have substantial other itemized deductions. This doesn't represent additional tax liability-it simply means you no longer receive the offsetting benefit of mortgage interest against your taxable income.

Strategic Approaches to Accelerated Mortgage Payoff

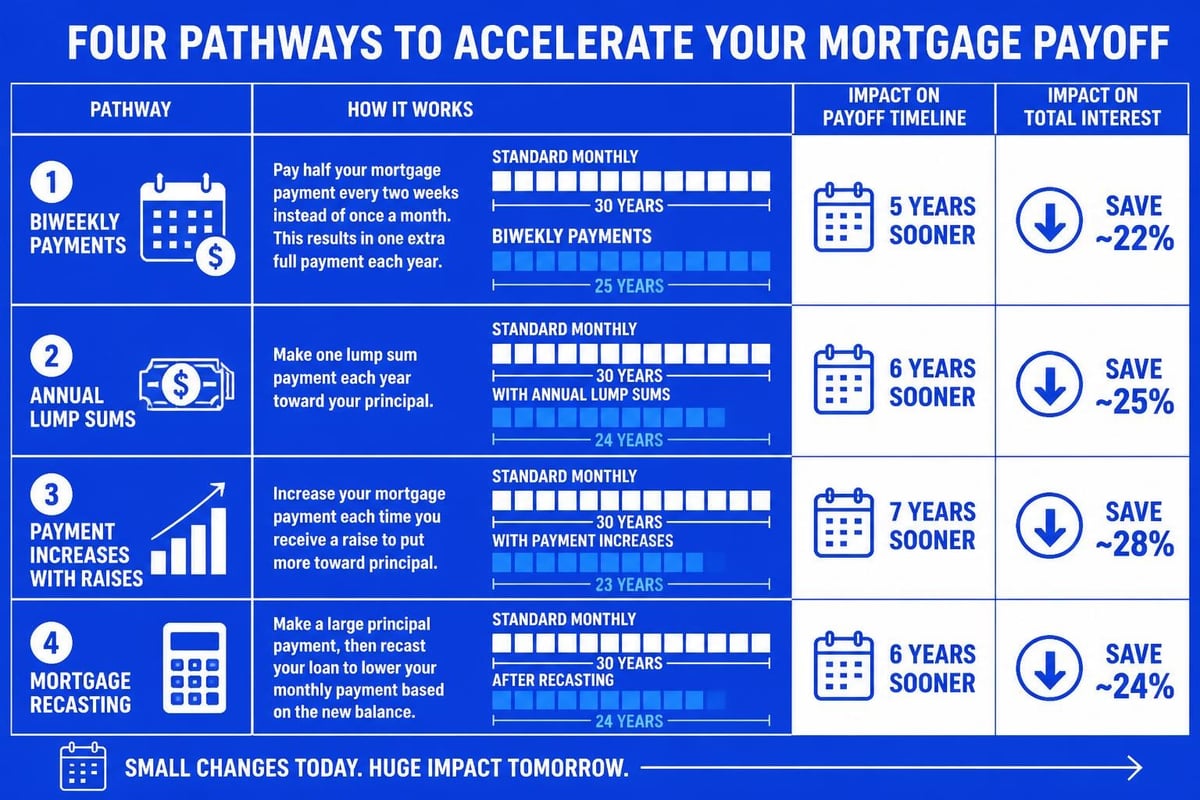

Homeowners pursuing early payoff benefit from implementing structured strategies rather than making sporadic extra payments. Several proven approaches help you systematically reduce principal while maintaining financial flexibility.

Biweekly Payment Programs

Converting from monthly to biweekly payments creates 26 half-payments annually (equivalent to 13 full payments instead of 12). This extra payment goes entirely to principal reduction, potentially cutting years off your loan term without dramatically impacting monthly cash flow.

Implementation considerations:

- Verify your servicer accepts biweekly payments without fees

- Ensure extra payments apply to principal, not advance due dates

- Consider manually making an extra payment annually if biweekly setup proves cumbersome

- Track your amortization schedule to confirm accelerated progress

Recasting Your Mortgage After Lump Sum Payments

For Seattle homeowners receiving substantial bonuses, stock compensation vesting, or inheritance proceeds, mortgage recasting offers an alternative to complete payoff. When you make a large principal payment (typically $10,000 minimum), your lender can recast the loan, recalculating your monthly payment based on the new lower balance while keeping your existing rate and remaining term.

This strategy provides immediate monthly payment relief without refinancing costs or extending your loan term. It works particularly well when mortgage financing costs make refinancing unattractive but you want to reduce monthly obligations.

Balancing Mortgage Payoff Against Other Financial Priorities

The decision to pay off mortgage loan debt early should never occur in isolation from your complete financial picture. Financial advisors consistently emphasize a hierarchy of priorities that typically precedes aggressive mortgage payoff.

Essential Financial Foundations First

Before directing substantial resources toward mortgage principal, ensure you've established:

- Emergency fund: Six to twelve months of expenses in liquid savings

- Retirement contributions: Maximize employer match programs (immediate 100% return)

- High-interest debt elimination: Credit cards, personal loans, or auto loans above 8%

- Adequate insurance coverage: Life, disability, and liability protection

- Health savings account funding: Triple tax advantage for eligible individuals

Seattle tech workers with RSU compensation face unique considerations. Concentrated stock positions create risk that often warrants diversification before accelerating mortgage payoff. When 40-60% of your net worth sits in a single company's stock, NerdWallet’s guidance on paying off mortgages emphasizes ensuring retirement accounts hold properly diversified investments first.

Investment Returns Versus Interest Savings

The mathematical comparison between investing and paying off your mortgage depends on expected returns, time horizon, and risk tolerance. Historically, diversified stock market investments have returned approximately 10% annually over long periods, though with significant volatility.

| Scenario | Mortgage Rate | Expected Investment Return | Mathematical Advantage |

|---|---|---|---|

| Low rate lock | 3.25% | 8% | Investing |

| Moderate rate | 5.5% | 8% | Slight investing edge |

| High current rate | 6.75% | 8% | Closer decision |

| Very high rate | 7.5%+ | 8% | Payoff competitive |

The guaranteed return from paying down mortgage principal equals your interest rate. No investment offers guaranteed returns matching current mortgage rates without substantial risk. This certainty appeals to conservative investors and those approaching retirement who prioritize security over maximum growth.

Retirement Timeline Considerations

Homeowners approaching retirement face distinct considerations when deciding whether to pay off mortgage loan obligations. Financial planners discussing mortgage payoff before retirement emphasize both the psychological benefits of debt-free retirement and the practical liquidity concerns.

The Case for Entering Retirement Mortgage-Free

Eliminating your housing payment before retirement substantially reduces your required monthly income. For Seattle-area retirees where property taxes, insurance, and utilities already consume significant cash flow, removing the mortgage payment creates meaningful budget flexibility.

Advantages of debt-free retirement:

- Reduced monthly income requirements from retirement accounts

- Greater flexibility to withstand market downturns without forced withdrawals

- Psychological peace of mind and reduced financial stress

- Protection against potential income disruption or health expenses

- Simplified estate planning and legacy considerations

A Lake Forest Park couple retiring with $4,200 monthly mortgage payments needs an additional $50,400 annually from retirement savings. Eliminating this obligation significantly extends portfolio longevity, particularly during market downturns when sequence-of-returns risk threatens retirement security.

Maintaining Liquidity and Investment Growth

The counterargument emphasizes maintaining liquidity and investment potential through retirement. Once you pay off mortgage loan debt, that equity becomes illiquid-you can't easily access it without selling your home, establishing a HELOC, or pursuing a reverse mortgage.

Retirees who maintain moderate mortgages while keeping larger investment portfolios preserve flexibility for unexpected expenses, long-term care needs, or legacy planning. For affluent Seattle homeowners in Bellevue and Redmond, the interest paid on a mortgage often pales compared to potential investment growth and tax-efficient withdrawal strategies.

Special Considerations for Seattle-Area Homeowners

The Greater Seattle housing market presents unique factors influencing the pay off mortgage loan decision. Understanding these regional dynamics helps you contextualize your personal situation within broader market conditions.

High Home Values and Jumbo Loans

Seattle's elevated home prices mean many homeowners carry jumbo home loans exceeding conventional conforming limits. These larger balances amplify both the total interest paid over the loan term and the potential savings from early payoff.

A $1.2 million jumbo loan at 6.75% interest carries a monthly principal and interest payment of approximately $7,784. Over 30 years, you'll pay roughly $1.6 million in interest alone. Even modest acceleration strategies create substantial absolute dollar savings, though the percentage impact remains consistent regardless of loan size.

Tech Compensation and Irregular Income

Seattle's concentration of technology employers creates unique cash flow patterns. Amazon, Microsoft, and Google employees often receive substantial portions of compensation through RSUs that vest on quarterly or semi-annual schedules. This irregular income makes the pay off mortgage loan decision more nuanced than for salaried professionals with consistent biweekly paychecks.

Strategic approaches for tech professionals include:

- Automated percentage allocation: Direct a fixed percentage of each RSU vesting toward mortgage principal

- Annual bonus deployment: Apply year-end bonuses to principal while maintaining regular income for expenses

- Tax withholding coordination: Align extra payments with vesting events to manage cash flow around tax obligations

- Balanced approach: Split windfalls between mortgage payoff, tax-advantaged retirement contributions, and taxable investment accounts

Working with experienced mortgage professionals who understand tech compensation helps optimize your strategy. First-time buyers entering the market and established homeowners alike benefit from guidance tailored to Seattle's unique employment landscape.

Prepayment Penalties and Loan Terms

Before implementing any accelerated payoff strategy, review your mortgage documents for prepayment penalties. Most conventional mortgages originated in recent years, particularly those from conventional loan lenders and reputable mortgage brokers, do not include prepayment penalties. However, some portfolio loans, specialized jumbo products, or older mortgages may impose fees for early payoff.

Understanding Your Loan Agreement

Your closing documents specify whether prepayment penalties apply, their duration, and calculation method. Typical prepayment penalties, when present, apply only during an initial period (often 3-5 years) and may calculate as:

- A percentage of the outstanding balance (commonly 1-2%)

- A specific number of months' interest

- A sliding scale that decreases over time

Contact your loan servicer directly to confirm your prepayment rights. Request written confirmation if your loan allows unlimited additional principal payments without penalty. This documentation proves valuable when making large payments or pursuing complete payoff.

Alternative Strategies Worth Considering

The binary choice between maintaining your current mortgage and aggressively paying it off overlooks middle-ground approaches that optimize financial flexibility while reducing debt burden.

The Hybrid Approach: Split Your Resources

Rather than directing all available funds toward mortgage principal, consider a balanced allocation that advances multiple goals simultaneously. This approach might involve:

- Contributing enough to employer retirement plans to capture full matching (immediate 100% return)

- Funding Roth IRA or backdoor Roth conversions (tax-free growth)

- Allocating 20-30% of remaining surplus toward mortgage principal

- Investing the balance in diversified taxable accounts (maintains liquidity)

- Maintaining robust emergency reserves (prevents forced liquidation during hardship)

This diversified strategy provides the psychological satisfaction of mortgage reduction while preserving access to capital and continuing wealth accumulation through investments.

Leverage for Wealth Building

Some Seattle-area real estate investors and affluent professionals intentionally maintain mortgage debt as part of a wealth-building strategy. By keeping low-rate mortgages while deploying capital into appreciating assets, rental properties, or business ventures, they pursue returns exceeding their borrowing costs.

This leveraged approach carries risks and suits specific financial profiles-typically those with substantial net worth, multiple income sources, and sophisticated investment strategies. It's not appropriate for everyone, but it represents a valid perspective on the pay off mortgage loan question for certain situations.

Making Your Personal Decision

Ultimately, the choice to pay off mortgage loan debt early depends on factors extending beyond pure mathematics. Your personal risk tolerance, life stage, career stability, and financial goals all influence the optimal path forward.

Questions to Guide Your Decision

Honest answers to these questions help clarify your priorities:

- How does carrying mortgage debt affect your stress level and peace of mind?

- What is your timeline to retirement, and how does housing payment impact your retirement budget?

- Do you have adequate emergency reserves independent of your home equity?

- Are you maximizing tax-advantaged retirement contributions and employer matches?

- What alternative uses for these funds (education, business opportunities, investments) merit consideration?

- How secure is your employment and income stream?

- What does your overall debt profile look like beyond your mortgage?

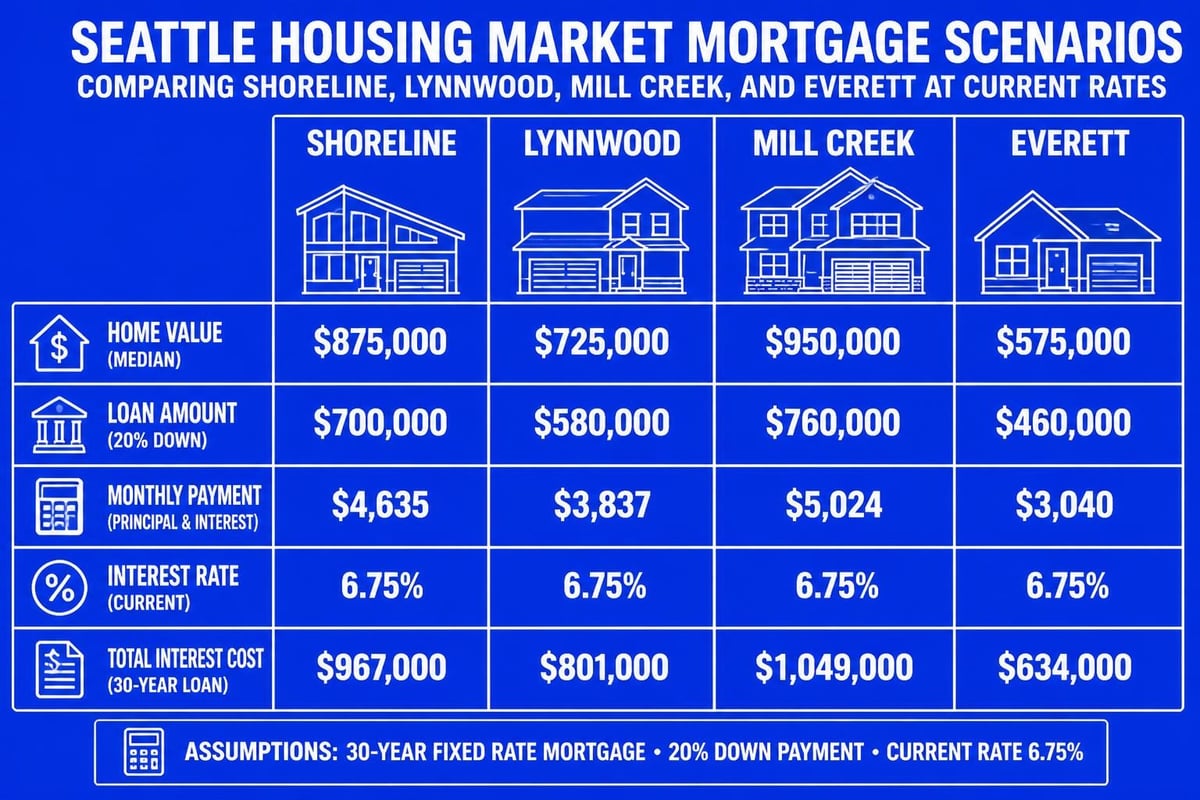

Mill Creek and Lynnwood homeowners with stable employment, maximized retirement contributions, and low risk tolerance often find substantial value in aggressive mortgage payoff. Conversely, Shoreline and Everett professionals earlier in their careers with opportunities for career advancement and investment growth may benefit from maintaining mortgages while building diversified wealth.

Running the Numbers for Your Situation

Create a personalized analysis using mortgage calculators and financial planning tools. Compare scenarios including:

- Status quo: Maintain current payment schedule

- Moderate acceleration: Add $300-500 monthly to principal

- Aggressive payoff: Direct all surplus toward mortgage

- Balanced approach: Split between mortgage and investments

Calculate total interest saved, years eliminated from your loan term, and opportunity costs from foregone investment returns. Factor in your tax situation, expected investment returns, and risk preferences. This data-driven analysis, combined with your personal circumstances and preferences, guides you toward the optimal decision for your household.

Implementation and Ongoing Management

Once you decide to pay off mortgage loan debt ahead of schedule, proper implementation ensures your efforts translate to actual progress. Common mistakes can undermine even well-intentioned strategies.

Setting Up Automatic Principal Payments

Most mortgage servicers offer online portals where you can schedule recurring additional principal payments. When setting up automatic payments:

- Clearly designate payments as "principal only" to prevent application as advance payment

- Schedule payments for dates when you reliably have available funds

- Confirm each payment posts correctly by reviewing monthly statements

- Request annual payoff statements showing accelerated progress

- Maintain documentation of all additional payments for your records

Some servicers process principal payments more efficiently through specific channels (online versus mail). Contact your servicer to identify the optimal submission method ensuring payments post correctly and promptly.

Annual Review and Adjustment

Your financial situation evolves-review your mortgage payoff strategy annually. Reassess when you experience:

- Significant income changes (promotion, job transition, bonus structure modifications)

- Major life events (marriage, children, inheritance, health issues)

- Shifts in interest rate environment or investment returns

- Changes to tax laws affecting mortgage interest deductibility

- Approaching retirement or other major life stage transitions

This periodic review ensures your mortgage strategy remains aligned with your current priorities rather than reflecting outdated assumptions from years past.

Deciding whether to pay off mortgage loan debt early requires balancing guaranteed interest savings against opportunity costs, tax implications, and personal priorities. The optimal choice varies based on your unique financial situation, risk tolerance, and life goals. Whether you're a tech professional in Seattle navigating RSU compensation, a homeowner approaching retirement in Bellevue, or an investor evaluating leverage strategies, Keith Akada and the team at Mortgage Reel provide personalized guidance grounded in 25+ years of experience serving the Greater Seattle area. With transparent education and strategic insight, we help you make confident decisions aligned with your complete financial picture.