Securing home loan approval represents one of the most significant financial milestones for Seattle-area homebuyers, whether you're purchasing your first condominium in Shoreline or upgrading to a larger home in Bellevue. The approval process evaluates multiple facets of your financial profile to determine your eligibility and loan terms. Understanding what lenders examine during this critical phase empowers you to prepare thoroughly and increase your chances of success in the competitive Pacific Northwest housing market.

Understanding the Home Loan Approval Framework

The mortgage approval process follows a structured evaluation that mortgage lenders use to assess your financial readiness. Lenders analyze your credit history, income stability, debt obligations, and assets to determine whether you can reliably repay the loan over its term.

This comprehensive review protects both the lender and the borrower. For lenders, it minimizes risk by confirming your ability to manage the financial commitment. For borrowers, it ensures you receive a loan amount aligned with your true purchasing power, preventing overextension that could jeopardize your financial stability.

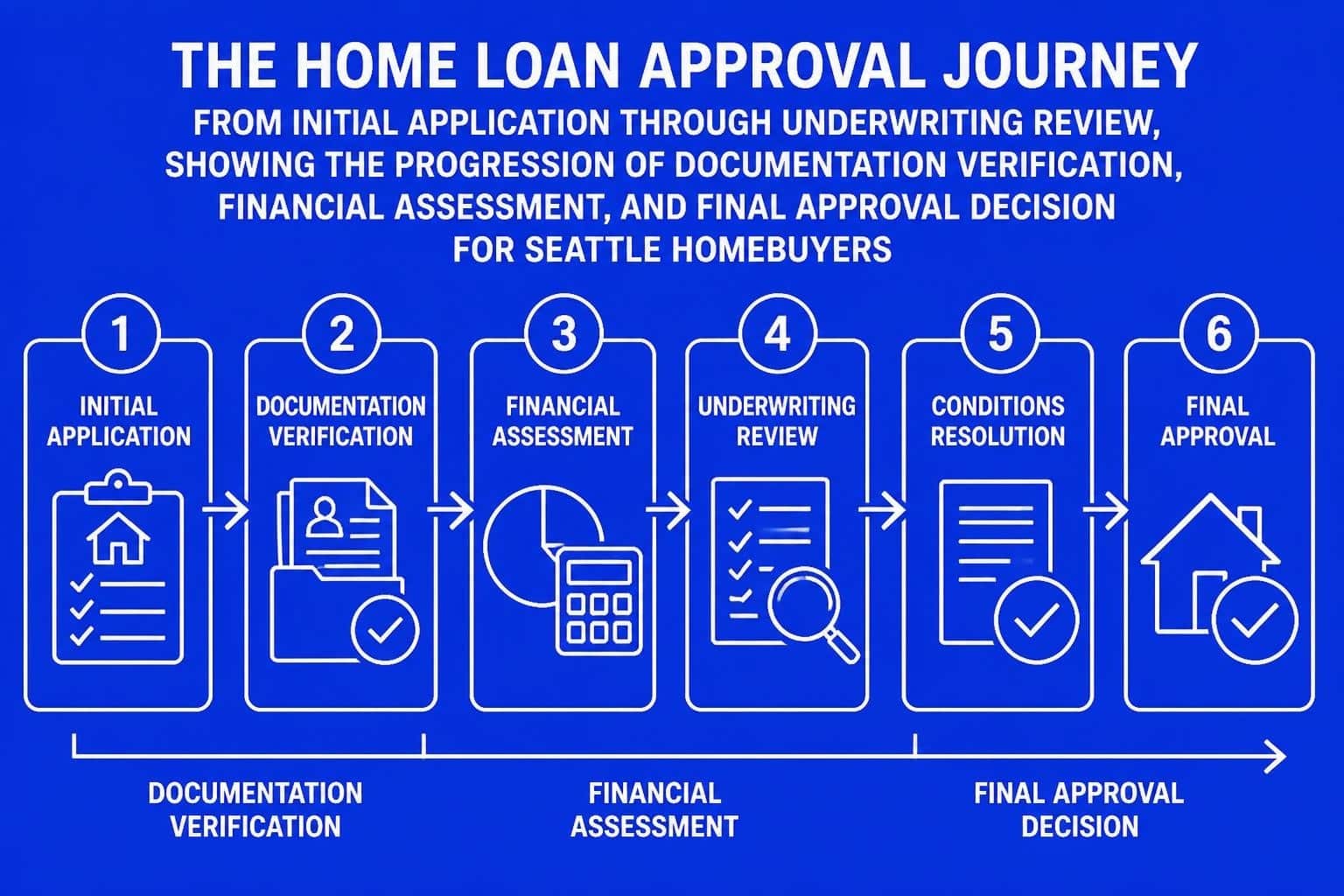

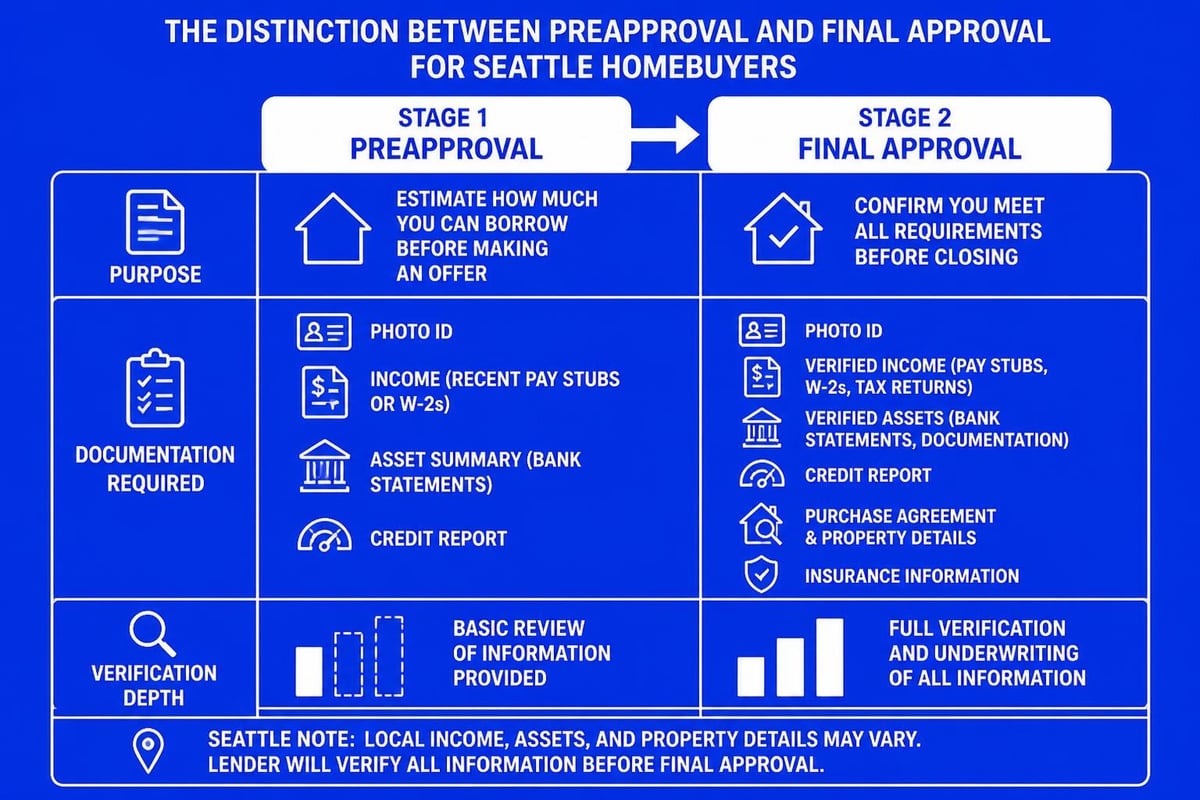

The Two-Stage Approval Process

Most borrowers encounter two distinct approval stages: preapproval and final approval.

Preapproval occurs early in your home search and provides a conditional commitment based on preliminary documentation. This initial review examines your credit score, income verification, and basic financial information. A strong preapproval demonstrates to sellers in competitive markets like Redmond and Kirkland that you're a serious buyer with verified financing capacity.

Final approval happens after you've made an offer and the property enters contract. This stage involves comprehensive underwriting, property appraisal, and verification of all financial details. The underwriter confirms that both you and the property meet all lending guidelines before issuing a clear-to-close status.

Critical Factors Affecting Home Loan Approval

Several key factors influence mortgage approval decisions, each carrying different weight in the underwriting evaluation. Understanding these elements allows you to address potential weaknesses before they impact your application.

Credit Score Requirements

Your credit score serves as a primary indicator of financial responsibility and repayment likelihood. Different loan programs establish minimum score requirements:

- Conventional loans: Typically require 620 or higher

- FHA loans: May accept scores as low as 580 with 3.5% down

- VA loans: No official minimum, though most lenders prefer 620+

- Jumbo loans: Usually require 700+ for competitive rates

Beyond meeting minimums, higher scores unlock better interest rates and more favorable terms. For tech professionals in Seattle pursuing jumbo home loans for properties exceeding conventional limits, strong credit becomes even more critical.

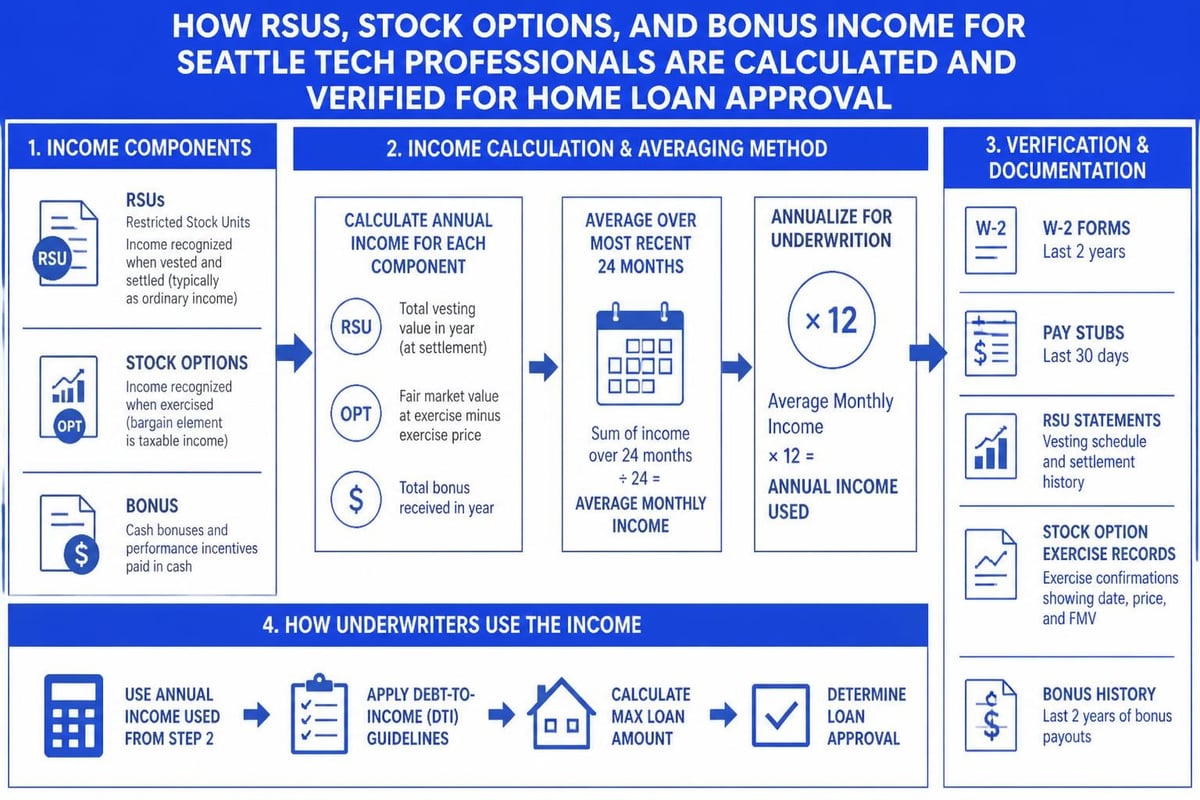

Income Verification and Stability

Lenders need confidence that your income will continue throughout the loan term. They evaluate both the amount and consistency of your earnings.

Traditional W-2 employees provide recent pay stubs, W-2 forms, and verification of employment. Underwriters calculate your qualifying income using your base salary and may include bonuses or commissions if you have a two-year history.

Tech professionals with stock compensation face unique considerations. RSUs, stock options, and equity grants can significantly boost purchasing power when properly documented. Lenders typically require evidence of vesting schedules and two years of consistent stock income to include these earnings in qualification calculations.

Self-employed borrowers must provide additional documentation, including two years of tax returns, profit and loss statements, and business bank statements. Underwriters analyze your net income after business deductions, which may differ substantially from your gross revenue.

| Employment Type | Primary Documentation | Income Calculation Method |

|---|---|---|

| W-2 Employee | Pay stubs, W-2s, VOE | Base + 2-year average of variable pay |

| Stock Compensation | Vesting schedule, tax records | 2-year average of vested stock value |

| Self-Employed | Tax returns, P&L statements | Net income after deductions |

| Commission-Based | 1099s, commission statements | 2-year average with declining income scrutinized |

Debt-to-Income Ratio Thresholds

Your debt-to-income ratio (DTI) compares your monthly debt obligations to your gross monthly income. This metric reveals how much of your income already goes toward existing debts, helping lenders assess your capacity for additional housing payments.

Front-end DTI divides your proposed housing payment (including principal, interest, taxes, insurance, and HOA fees) by your gross monthly income. Most lenders prefer this ratio below 28%.

Back-end DTI includes all monthly debt obligations: housing payment, car loans, student loans, credit card minimum payments, and other recurring debts. Conventional loans typically allow up to 43% DTI, though some programs permit higher ratios with compensating factors.

Reducing your DTI before applying strengthens your home loan approval prospects. Strategies include paying down credit cards, eliminating car loans, or postponing major purchases until after closing.

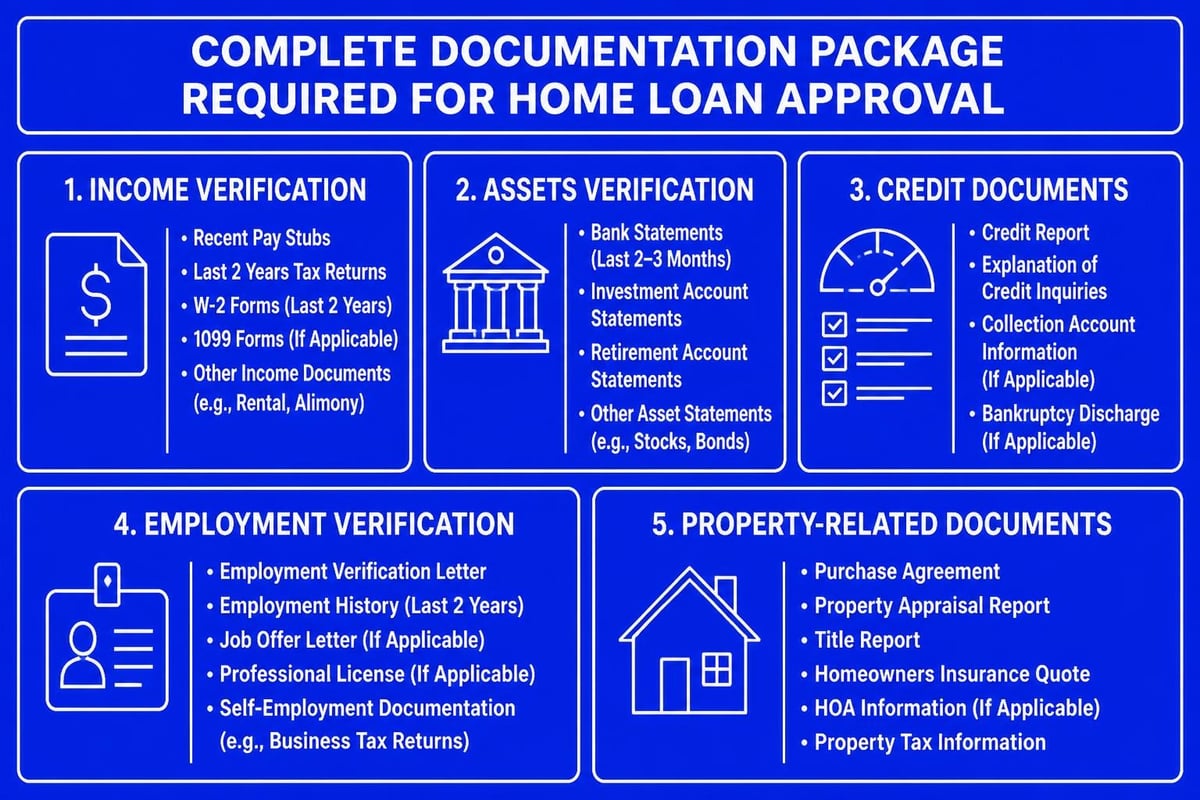

Documentation Requirements for Approval

Thorough documentation forms the foundation of successful home loan approval. Incomplete or inconsistent paperwork creates delays and may lead to denial.

Essential Financial Documents

Prepare these core documents before starting your application:

- Income verification: Recent pay stubs (typically 30 days), two years of W-2s, and tax returns

- Asset statements: Two months of bank statements for all accounts used for down payment and reserves

- Credit authorization: Permission for lender to pull credit reports

- Identification: Government-issued ID and Social Security card

- Employment verification: Contact information for HR department or supervisor

Property-Specific Documentation

Once you have a property under contract, additional documents enter the equation:

- Purchase agreement: Fully executed contract with all addendums

- Earnest money receipt: Proof of deposit made to escrow

- HOA documentation: Budgets, bylaws, and insurance certificates for condominiums

- Appraisal: Independent property valuation ordered by lender

The Underwriting Process Explained

Underwriting represents the most intensive phase of home loan approval, where a trained professional reviews every aspect of your application against lending guidelines. Understanding this process reduces anxiety and helps you respond effectively to requests.

Initial Document Review

The underwriter begins by examining all submitted documentation for completeness and consistency. They verify that income matches across pay stubs, W-2s, and tax returns. Bank statements must show sufficient funds for down payment and closing costs, plus required reserves.

Any discrepancies trigger immediate questions. Large deposits require explanation through paper trail documentation proving the source. Gaps in employment history need written explanations. Missing pages from bank statements must be provided.

Automated Underwriting Systems

Most conventional loans pass through automated underwriting systems that analyze your complete financial profile against program guidelines. These systems generate findings that guide the underwriter's manual review:

- Approved/Eligible: Application meets all automated criteria, requiring only verification

- Refer with caution: Additional review needed but approval likely with proper documentation

- Refer: Significant concerns requiring thorough manual underwriting

- Ineligible: Does not meet program guidelines

Even "approved" findings require manual verification of all supporting documents. The automated decision provides a roadmap, but human review ensures accuracy and catches issues the system might miss.

Property Evaluation Standards

The property itself must meet specific standards for home loan approval. Lenders order an appraisal to confirm the property's value supports the loan amount and verify it meets minimum condition requirements.

Appraisal concerns that can delay or derail approval include:

- Appraised value below purchase price, creating a gap in financing

- Safety hazards like peeling paint, damaged roofing, or electrical issues

- Missing essential systems such as heating or functioning plumbing

- Structural problems requiring significant repairs

- Adverse external conditions affecting value or marketability

For properties in Lake Forest Park or Mill Creek, appraisers compare your home to recent sales of similar properties in the area. Limited comparable sales in unique markets can sometimes create valuation challenges.

Common Approval Challenges and Solutions

Even well-qualified borrowers encounter obstacles during the approval process. Recognizing potential issues early and addressing them proactively improves outcomes.

Credit Report Issues

Problem: Errors on credit reports or unexpected negative items can lower scores and jeopardize approval.

Solution: Pull your credit reports from all three bureaus at least 60 days before applying. Dispute inaccuracies through the bureaus and maintain documentation of the dispute. For legitimate negative items, write a letter of explanation describing the circumstances and how you've remedied the situation.

Employment Changes During Processing

Problem: Changing jobs, transitioning to self-employment, or gaps in employment raise red flags during underwriting.

Solution: Maintain employment stability from application through closing whenever possible. If a job change is unavoidable, ensure it's within the same field and ideally represents a promotion or raise. Notify your mortgage broker immediately so they can manage underwriting concerns proactively.

Asset Verification Complications

Problem: Funds for down payment and closing costs must be sourced and seasoned, meaning you can document where money came from and how long you've held it.

Solution: Consolidate funds into one or two accounts at least two months before applying. Large deposits require complete paper trails. Gift funds need gift letters from donors and documentation showing the transfer. Avoid moving money between accounts unnecessarily during the approval process.

Debt-to-Income Challenges

Problem: Your DTI exceeds program limits even though you feel comfortable with the payment.

Solution: Consider these strategies:

- Pay down revolving debts to reduce monthly obligations

- Add a co-borrower with qualifying income

- Explore different loan programs with higher DTI thresholds

- Reduce your purchase price to lower the housing payment

- Wait to purchase until income increases or debts decrease

Special Considerations for Seattle-Area Buyers

The Seattle housing market presents unique challenges that impact home loan approval strategies for buyers in Everett, Lynnwood, and surrounding communities.

High Property Values and Jumbo Loans

Seattle's elevated property values frequently push buyers beyond conventional loan limits ($766,550 for single-family homes in 2026 for most counties). Jumbo mortgages carry stricter approval requirements:

| Requirement | Conventional Loan | Jumbo Loan |

|---|---|---|

| Minimum Credit Score | 620 | 700+ |

| Maximum DTI | 43-50% | 43% |

| Down Payment | 3-20% | 10-20%+ |

| Cash Reserves | 2-6 months | 6-12 months |

| Documentation | Standard | Enhanced |

Stock Compensation Qualification

Tech professionals at Amazon, Microsoft, and Google often hold substantial wealth in equity compensation. Properly documenting and qualifying this income dramatically increases purchasing power but requires specialized expertise.

Restricted Stock Units (RSUs) that vest on a predictable schedule can be included in qualifying income using a two-year average of vested shares. Lenders review tax returns showing the income and vesting schedules confirming future grants.

Stock options present more complexity. Only exercised options with documented sale history typically qualify. The volatility of option value makes underwriters conservative in their calculations.

Working with professionals experienced in tech employee mortgages ensures you maximize these income sources during the approval process.

Timeline Expectations for Home Loan Approval

Understanding realistic timelines helps you plan your home search and set appropriate expectations with sellers.

Preapproval Timeline

Initial preapproval typically takes 1-3 business days once you've submitted complete documentation. This assumes no complications with credit, employment, or income verification.

Factors that extend preapproval timelines include:

- Self-employment requiring detailed income analysis

- Complex income structures with multiple sources

- Credit issues requiring explanation or documentation

- Recent job changes needing verification

- Cross-border income or assets

Full Approval and Closing Timeline

From accepted offer to closing typically requires 21-45 days, though experienced lenders can expedite this process. Advanced underwriting capabilities enable closings in as few as 9 business days for well-qualified borrowers with straightforward transactions.

Week 1-2: Appraisal ordered, initial underwriting review, document requests issued

Week 2-3: Appraisal completed, underwriting conditions addressed, title work progresses

Week 3-4: Final underwriting approval, clear-to-close issued, closing scheduled

Week 4+: Closing executed, funding completed, keys delivered

Strategies for Strengthening Your Approval Odds

Proactive preparation significantly improves your home loan approval likelihood and potentially unlocks better terms.

Twelve Months Before Applying

Build a strong financial foundation well in advance:

- Check and improve credit: Review reports, dispute errors, pay down balances

- Increase savings: Build reserves beyond down payment for closing costs and emergencies

- Stabilize employment: Avoid job changes if possible

- Reduce debts: Pay off or pay down loans to improve DTI

- Avoid major purchases: Don't take on new debt for vehicles, furniture, or other large items

Six Months Before Applying

Intensify your preparation as you approach application:

- Document income sources thoroughly

- Organize tax returns, pay stubs, and bank statements

- Research loan programs matching your situation

- Get pre-qualified to understand your purchasing power

- Connect with a trusted mortgage broker who understands your market

During the Approval Process

Maintain financial stability throughout underwriting:

- Respond quickly to all document requests from your lender

- Avoid new credit applications or major purchases

- Maintain employment and income consistency

- Keep assets stable without moving money unnecessarily

- Communicate changes immediately to your loan officer

Alternative Approval Paths

Traditional full documentation approval isn't the only path to homeownership. Alternative programs serve borrowers with non-traditional income or credit profiles.

Bank Statement Loans

Self-employed borrowers who write off substantial business expenses may show lower taxable income than actual cash flow. Bank statement loans allow qualification based on deposits rather than tax returns, typically using 12-24 months of business bank statements to calculate income.

These programs usually require larger down payments (10-20%+) and carry slightly higher interest rates, but they enable approval for borrowers who couldn't qualify through conventional documentation.

Non-QM Loans

Non-Qualified Mortgage (Non-QM) programs provide flexibility beyond standard qualified mortgage rules. They may accommodate:

- Higher debt-to-income ratios

- Recent credit events like bankruptcy or foreclosure

- Unique income documentation needs

- Investment property portfolios

- Foreign nationals

Trade-offs typically include higher rates, larger down payments, and more stringent asset requirements.

Working with Professionals Throughout the Process

The complexity of home loan approval makes professional guidance invaluable, particularly in competitive markets where mistakes can cost you your dream home.

The Role of a Mortgage Broker

A knowledgeable mortgage broker serves as your advocate throughout the approval process. They pre-qualify you accurately, match you with appropriate loan programs, manage documentation, troubleshoot underwriting issues, and coordinate with all parties to ensure smooth closing.

For first-time homebuyers, this guidance proves especially valuable. Experienced professionals explain each step, set realistic expectations, and help you avoid common pitfalls that derail approval.

Additional Team Members

Beyond your mortgage broker, assemble a complete team:

- Real estate agent: Guides property search and negotiation

- Real estate attorney: Reviews contracts and protects your interests (in some states)

- Home inspector: Identifies property condition issues before purchase

- Insurance agent: Secures homeowners insurance required for closing

- Tax professional: Advises on tax implications and deductibility

This coordinated team approach streamlines the process and minimizes surprises that could jeopardize your home loan approval.

Maintaining Approval Through Closing

Receiving initial approval doesn't guarantee closing. Lenders verify your financial status immediately before funding, and any changes can derail the transaction.

What Not to Do After Approval

Avoid these actions once you're approved:

- Making large purchases on credit, even for the new home

- Changing jobs or income structure

- Opening new credit accounts or closing existing ones

- Making large deposits without documentation

- Co-signing loans for others

- Missing bill payments that could impact credit

Lenders pull credit again just before closing and re-verify employment. Any negative changes can result in delayed funding or outright denial, even after you've packed your moving boxes.

Final Verification Process

In the 48-72 hours before closing, expect:

- Final credit report pull

- Employment re-verification

- Asset re-verification

- Appraisal review for any changes in property condition

- Title update to ensure no new liens or issues

Respond immediately to any last-minute requests. Delays at this stage postpone closing, potentially breaching your purchase contract and costing you earnest money.

Regional Market Considerations

Understanding local market dynamics helps you navigate home loan approval more strategically in different Seattle-area communities.

Competitive Offer Situations

In hot markets, sellers may receive multiple offers. Your financing strategy impacts competitiveness:

- Strong preapproval letters from reputable lenders carry more weight

- Larger down payments demonstrate financial strength

- Faster closing timelines appeal to motivated sellers

- Waiving financing contingencies (risky but sometimes necessary)

Work with your mortgage professional to structure offers that balance protection with competitive advantage.

Condominium Approval Challenges

Seattle's abundant condominium inventory presents unique approval considerations. Lenders review the entire project, not just your individual unit:

- Project approval: Lender must approve the condominium project itself

- Owner-occupancy ratios: Sufficient percentage must be owner-occupied, not rentals

- Financial health: HOA must maintain adequate reserves

- Litigation: Pending lawsuits can make projects ineligible

- Insurance: Project must carry proper coverage

New condominium projects may lack lender approval, requiring additional time to establish eligibility.

Successfully navigating home loan approval requires thorough preparation, complete documentation, and strategic planning. Understanding what lenders evaluate and addressing potential weaknesses before they become obstacles positions you for a smooth approval process and confident closing. Keith Akada at Mortgage Reel brings over 25 years of experience helping Seattle-area homebuyers secure financing, specializing in complex income scenarios including stock compensation for tech professionals. With advanced underwriting capabilities and the ability to close in as few as 9 business days, Keith provides the expertise and execution you need to achieve your homeownership goals in Seattle, Bellevue, Redmond, and throughout the Puget Sound region.