Securing a mortgage for first home represents one of the most significant financial decisions you'll make in your lifetime. For buyers in Seattle, Bellevue, Redmond, and Kirkland, navigating the competitive real estate market requires not just adequate preparation but strategic planning and expert guidance. The Pacific Northwest housing market presents unique challenges-from high median home prices to intense bidding scenarios-making it essential to understand your financing options, qualification requirements, and the full spectrum of loan programs available to first-time buyers in 2026.

Understanding Mortgage Options for First-Time Buyers

When pursuing a mortgage for first home, you'll encounter several loan programs designed specifically to help new buyers overcome common barriers like limited down payment funds or strict credit requirements. Each option carries distinct advantages depending on your financial situation, employment status, and long-term homeownership goals.

Conventional Loans with Low Down Payments

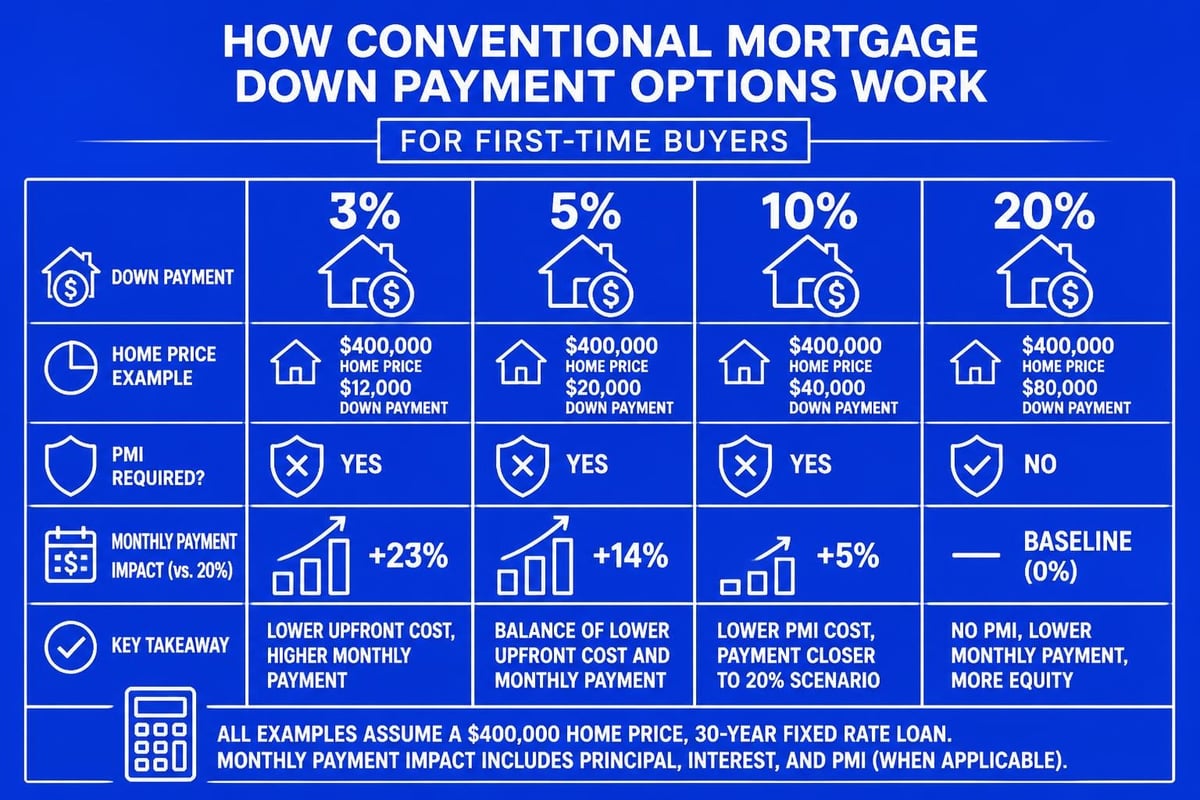

Conventional mortgages offer flexibility that many first-time buyers overlook. While the traditional 20% down payment remains ideal for avoiding private mortgage insurance (PMI), conventional loans actually allow down payments as low as 3% for qualified first-time buyers. This makes homeownership accessible even in expensive markets like Seattle and Shoreline.

For tech professionals working at Amazon, Microsoft, or Google, conventional loans provide excellent options for qualifying stock-based compensation. When working with experienced mortgage brokers in Seattle, RSUs and vested stock can be factored into your income calculation, significantly increasing your purchasing power in competitive neighborhoods from Lynnwood to Lake Forest Park.

Key benefits of conventional loans include:

- Lower overall borrowing costs compared to government-backed programs

- No upfront mortgage insurance premiums

- Ability to remove PMI once you reach 20% equity

- Flexible property type eligibility including condos and investment properties

- Competitive interest rates for borrowers with strong credit profiles

FHA Loans for Lower Credit Scores

Federal Housing Administration (FHA) loans serve as a popular choice for buyers who may not qualify for conventional financing. These government-backed mortgages accept credit scores as low as 580 with just 3.5% down, making them accessible for buyers in Mill Creek and Everett who are building their credit history.

However, FHA loans require both upfront and ongoing mortgage insurance premiums regardless of your down payment amount. The upfront premium of 1.75% can be rolled into your loan amount, while annual premiums typically range from 0.55% to 1.05% of the loan balance. For a comprehensive understanding of various first-time mortgage loan options, consulting with a knowledgeable broker helps you weigh these costs against the program's accessibility.

| Loan Feature | FHA | Conventional 3% Down |

|---|---|---|

| Minimum Credit Score | 580 | 620 |

| Down Payment | 3.5% | 3% |

| Upfront Insurance | 1.75% | None |

| Monthly Insurance | 0.55%-1.05% | 0.3%-1.5% (removable) |

| Loan Limits (Seattle 2026) | $498,257 | $766,550 |

VA Loans for Military Service Members

Veterans and active-duty service members benefit from exceptional mortgage terms through the VA loan program. VA loans require zero down payment and charge no monthly mortgage insurance, resulting in substantial savings over the loan's lifetime. For eligible buyers in Seattle and surrounding communities, this represents one of the strongest financing tools available.

The VA funding fee, typically 2.3% for first-time use with zero down, can be financed into the loan. Veterans with service-connected disabilities may qualify for fee exemptions. Understanding how different loan programs work helps military buyers maximize these benefits while navigating competitive markets in Bellevue and Redmond.

USDA Loans for Suburban and Rural Areas

While Seattle proper doesn't qualify for USDA financing, eligible areas exist in the broader Pacific Northwest region. These zero-down-payment loans serve moderate-income buyers in designated rural and suburban zones. If you're considering properties beyond the immediate Seattle metro area, USDA loans may provide an affordable path to homeownership with competitive rates and minimal upfront costs.

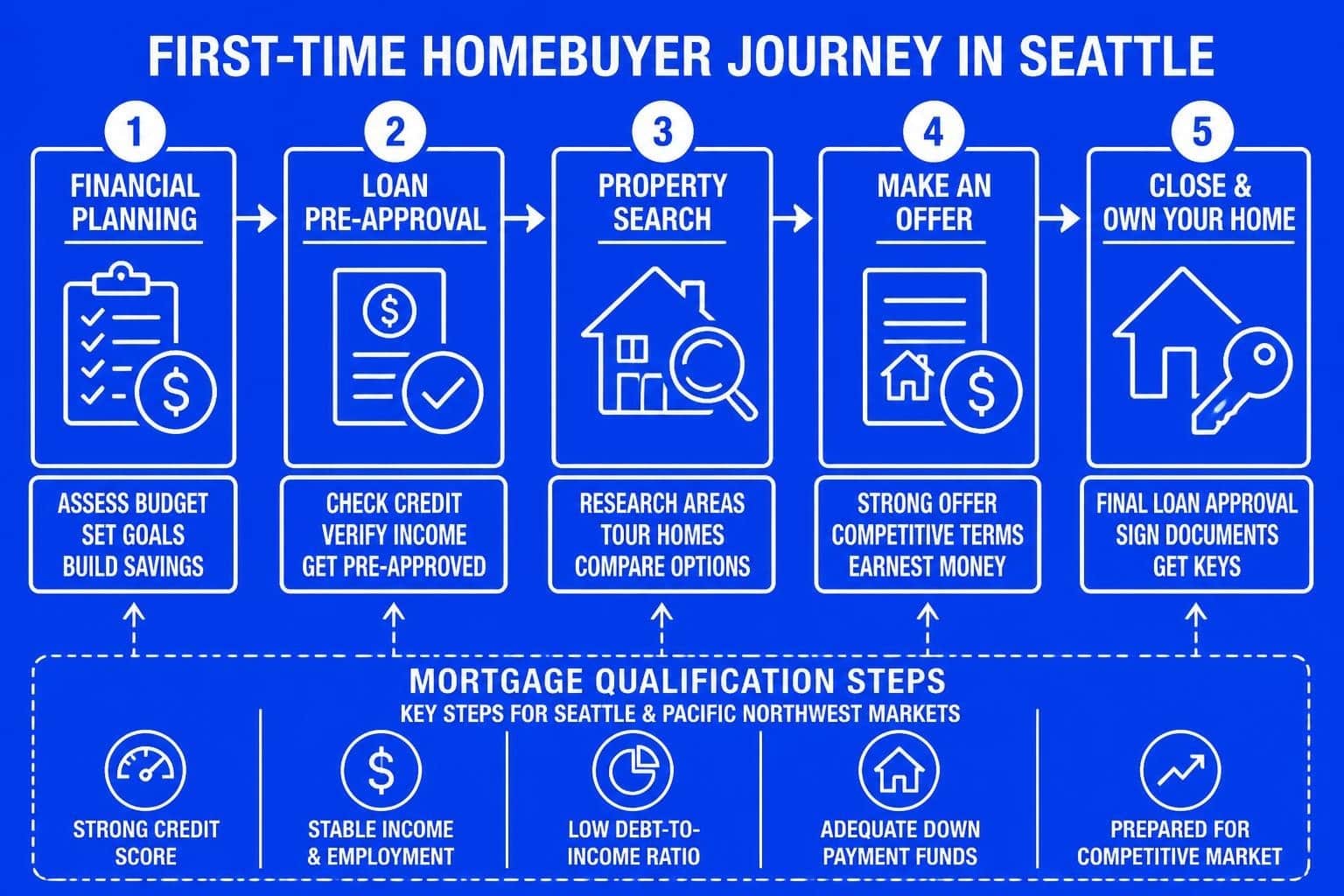

Qualifying for Your First Mortgage

Lenders evaluate three primary factors when approving a mortgage for first home: credit history, debt-to-income ratio, and available down payment funds. Understanding these criteria allows you to strengthen your application before beginning your home search.

Credit Score Requirements

Your credit score significantly influences not just approval odds but also the interest rate you'll receive. Most conventional loans require a minimum score of 620, though higher scores unlock better pricing. FHA loans accept scores as low as 580, while VA and USDA programs may approve borrowers in the 580-620 range depending on compensating factors.

Actions to improve your credit score:

- Pay all bills on time for at least 12 months before applying

- Reduce credit card balances below 30% of available limits

- Avoid opening new credit accounts during your home search

- Dispute any errors on your credit reports from all three bureaus

- Maintain existing credit accounts to preserve credit history length

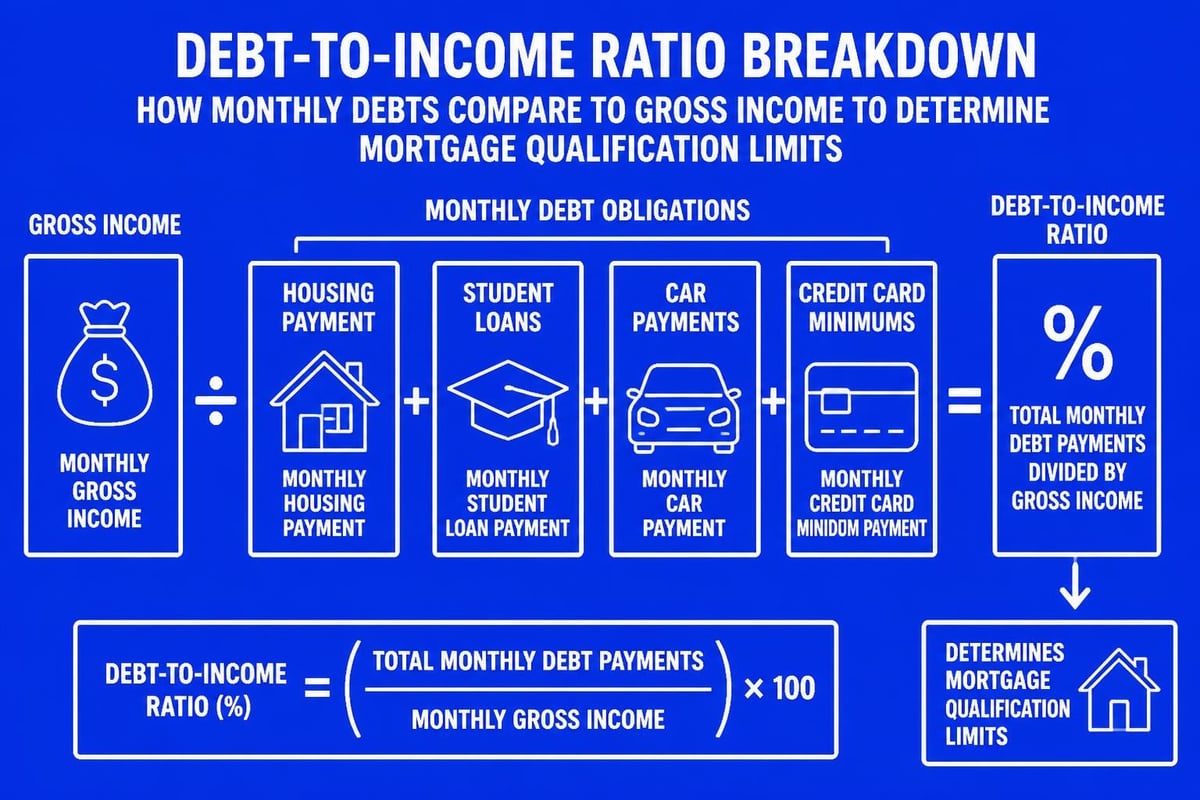

Debt-to-Income Ratio Standards

Lenders calculate your debt-to-income (DTI) ratio by dividing your total monthly debt payments by your gross monthly income. Most programs accept DTI ratios up to 43-45%, though conventional loans may approve ratios up to 50% with strong credit and reserves.

For Seattle tech professionals with substantial stock compensation, working with a broker experienced in qualifying RSUs and bonus income proves invaluable. Proper documentation and calculation methodology can transform your qualification amount, especially when pursuing properties in Kirkland or other premium Seattle neighborhoods.

Down Payment and Reserve Requirements

While low down payment programs exist, accumulating additional funds strengthens your offer competitiveness and reduces monthly costs. Beyond your down payment, lenders require reserves-typically two months of mortgage payments in savings-to ensure you can handle unexpected expenses.

Down payment sources include:

- Personal savings from checking and savings accounts

- Gift funds from family members with proper documentation

- Down payment assistance programs available through Washington State

- 401(k) loans or withdrawals (though generally not recommended)

- Employer homebuyer assistance programs

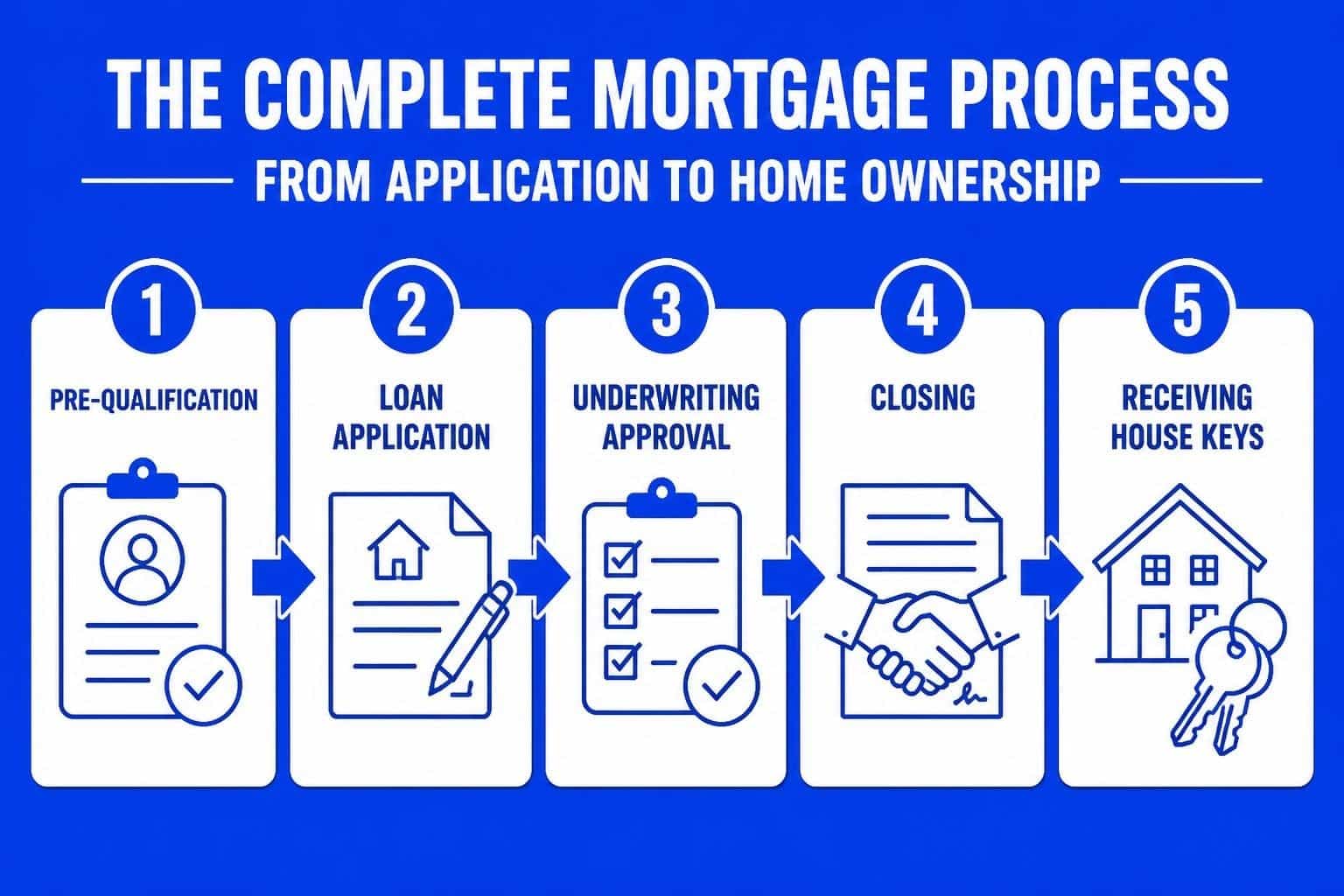

Navigating the Pre-Approval Process

Securing pre-approval before house hunting separates serious buyers from casual browsers, especially critical in competitive Seattle markets where homes often receive multiple offers within days of listing.

Documentation Requirements

Gathering documentation early accelerates the pre-approval process. Standard requirements include two years of W-2 forms, recent pay stubs, two months of bank statements, and signed tax returns. Self-employed buyers need additional documentation including profit and loss statements and business tax returns.

For Amazon, Microsoft, and Google employees, stock compensation documentation becomes essential. This includes vesting schedules, recent pay stubs showing RSU income, and brokerage statements confirming stock values. Experienced Seattle mortgage brokers understand how to present this income to underwriters for maximum qualification impact.

Pre-Approval vs. Pre-Qualification

Many buyers confuse pre-qualification with pre-approval, but these represent vastly different levels of commitment. Pre-qualification involves a brief conversation about your finances without verification, resulting in a rough estimate of borrowing capacity. Pre-approval requires full documentation review, credit check, and preliminary underwriting, producing a conditional commitment letter that carries substantial weight with sellers.

In Seattle's competitive market, pre-approval letters from reputable lenders like Fairway often determine whose offer gets accepted when multiple bids arrive at similar prices. Sellers and their agents recognize that pre-approved buyers close more reliably than pre-qualified ones.

Strategic Considerations for Seattle Buyers

The Greater Seattle housing market demands strategic approaches beyond basic qualification. Understanding local market dynamics, timing considerations, and negotiation leverage helps first-time buyers compete effectively.

Understanding Market Conditions

Seattle's real estate market fluctuates seasonally and responds to broader economic factors including employment trends, interest rates, and housing inventory levels. Spring and summer traditionally bring heightened competition, while winter months may offer less competition and more negotiating room in neighborhoods from Shoreline to Everett.

Monitoring current Seattle mortgage rates helps you time your purchase strategically. Even small rate differences impact your monthly payment and total interest costs significantly over a 30-year term.

Choosing Between Neighborhoods

First-time buyers often face trade-offs between location, home size, and budget. While Bellevue and Redmond offer proximity to major tech employers, areas like Lynnwood, Lake Forest Park, and Mill Creek provide more affordable entry points with excellent schools and amenities.

Consider these factors when evaluating neighborhoods:

- Commute time to your workplace and traffic patterns

- School district quality if you have or plan children

- Property tax rates which vary significantly by jurisdiction

- HOA fees for condos and townhomes

- Future appreciation potential based on development plans

Jumbo Loan Considerations

Seattle's high home prices frequently push buyers into jumbo loan territory, defined in 2026 as mortgages exceeding $766,550 in King County. Jumbo loans require stronger financial profiles but offer competitive rates for qualified borrowers, particularly those with substantial stock-based compensation.

| Requirement | Conventional | Jumbo |

|---|---|---|

| Typical Down Payment | 3%-20% | 10%-20% |

| Credit Score Minimum | 620 | 700 |

| DTI Limit | 50% | 43% |

| Reserve Requirements | 2 months | 6-12 months |

| Rate Comparison | Baseline | Often competitive |

Maximizing Your Buying Power

Beyond basic qualification, strategic approaches can increase your purchasing capacity and improve your offer strength in competitive situations.

Leveraging Stock Compensation

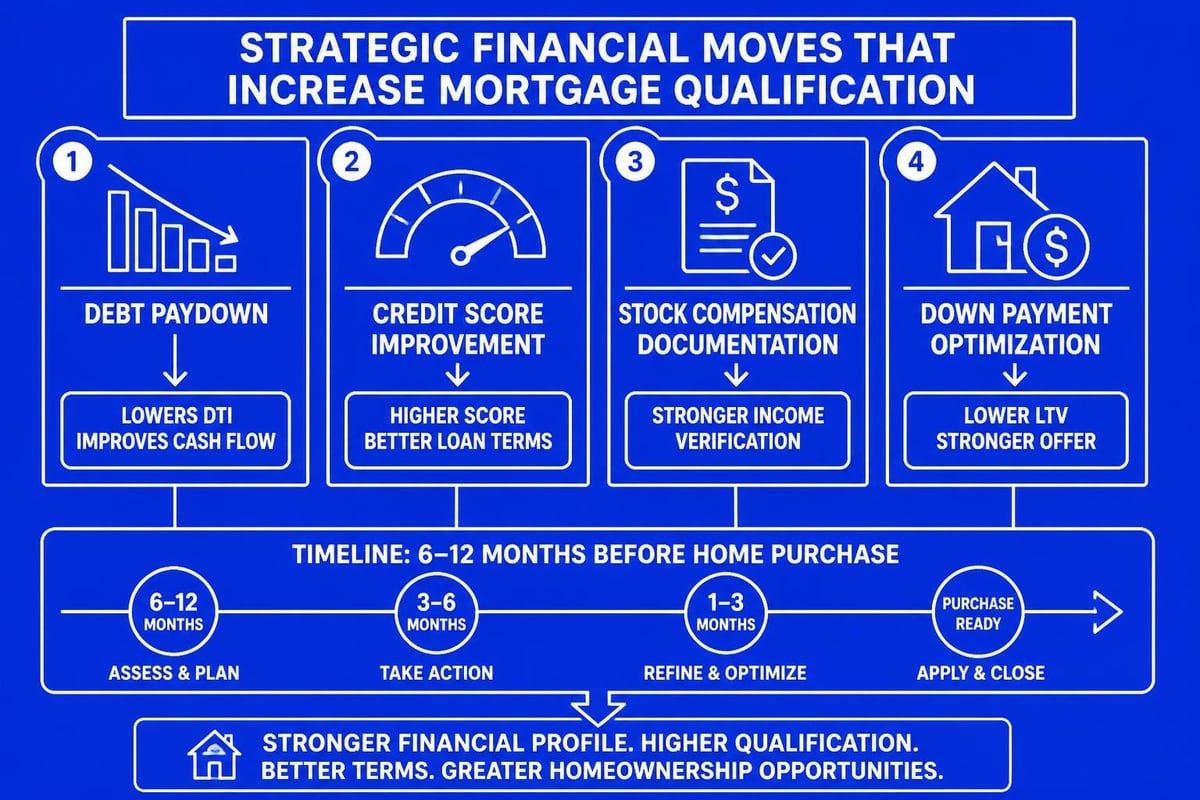

Tech professionals in Seattle possess unique advantages when structuring their mortgage for first home. RSUs, stock options, and annual bonuses can substantially increase qualification amounts when properly documented and calculated. However, lenders vary significantly in their willingness and expertise to qualify these income sources.

Working with a broker who specializes in tech employee financing ensures your complete compensation package gets utilized. This might mean the difference between qualifying for a $600,000 home versus an $800,000 property in desirable neighborhoods.

Reducing Monthly Obligations

Paying down or paying off installment debt before applying increases your qualifying amount more effectively than saving additional down payment funds in many cases. For example, eliminating a $400 monthly car payment could increase your home price qualification by $80,000-$100,000 depending on the interest rate environment.

Strategic debt reduction priorities:

- High monthly payment installment loans (cars, student loans)

- Credit cards with balances above 30% utilization

- Personal loans with fewer than 10 months remaining

- Medical debt appearing on credit reports

Understanding Rate Locks and Timing

Interest rates fluctuate daily based on economic data, Federal Reserve policy, and bond market movements. Once pre-approved, you'll need to decide when to lock your interest rate. Rate locks typically range from 30 to 60 days, with longer locks carrying slightly higher rates as compensation for the lender's extended risk exposure.

Your broker should monitor rate trends and recommend optimal lock timing based on your home search timeline and market conditions. In rapidly rising rate environments, early locks protect you, while stable or falling rate markets may justify waiting until you have an accepted offer.

Common First-Time Buyer Mistakes

Learning from others' missteps helps you avoid costly errors during your home buying journey. These represent the most frequent mistakes first-time buyers make when securing a mortgage for first home in Seattle markets.

Making Large Purchases Before Closing

Financing furniture, cars, or other large purchases between pre-approval and closing can derail your mortgage approval. Lenders verify your financial status immediately before closing, and new debt either disqualifies you entirely or forces you to renegotiate terms. Maintain stable finances throughout the entire process, avoiding new credit cards, loans, or major purchases until after you receive your keys.

Overlooking Total Housing Costs

Your mortgage payment represents just one component of homeownership expenses. Property taxes in King County average 0.92% of assessed value annually but vary by location. Homeowners insurance, HOA fees, utilities, and maintenance costs add substantially to your monthly obligations.

Complete monthly housing budget includes:

- Principal and interest payment

- Property taxes (often escrowed)

- Homeowners insurance (escrowed)

- HOA or condo fees

- Utilities (water, sewer, garbage, electricity, gas)

- Maintenance reserve (typically 1% of home value annually)

Skipping Professional Representation

While not directly mortgage-related, working with an experienced buyer's agent who understands financing contingencies protects your interests during negotiation. Similarly, choosing the right lender impacts your approval odds, interest rate, and closing timeline. As detailed in NerdWallet’s first-time homebuyer guide, the professionals you select significantly influence your overall experience and outcome.

Closing Timeline and Process

Understanding what happens between offer acceptance and closing day helps you prepare for a smooth transaction. The typical closing timeline spans 30-45 days for conventional and FHA loans, though experienced lenders can close qualified buyers in as few as 9 business days when needed.

Key Milestones After Offer Acceptance

Your loan progresses through distinct phases, each with specific requirements and deadlines. Missing deadlines can jeopardize your purchase, particularly in competitive markets where backup offers wait in the wings.

Standard closing timeline:

- Days 1-3: Formal application, initial disclosures, appraisal ordered

- Days 4-7: Title search completed, homeowners insurance selected

- Days 8-15: Appraisal conducted, home inspection performed

- Days 16-25: Underwriting review, potential conditions issued

- Days 26-30: Final conditions cleared, closing disclosure issued

- Days 31-45: Final walkthrough, closing scheduled, funds wired

Understanding Closing Costs

Beyond your down payment, expect to pay 2-5% of the purchase price in closing costs. These include lender fees, title insurance, escrow fees, prepaid property taxes and insurance, and recording fees. Requesting a loan estimate within three days of application provides detailed cost breakdowns.

Some buyers negotiate seller-paid closing costs, particularly in slower markets or with properties that have been listed longer. However, in competitive Seattle markets, asking sellers to contribute toward your closing costs may weaken your offer compared to buyers who don't make such requests.

For detailed insights on the complete homebuying process, Bankrate’s comprehensive first-time homebuyer guide walks through every step from financial assessment through closing.

Special Programs and Assistance

Washington State and local jurisdictions offer programs specifically designed to help first-time buyers overcome down payment and closing cost barriers. These programs complement your primary financing and can make homeownership achievable sooner than saving 20% down.

Washington State Housing Finance Commission

The state offers down payment assistance programs providing deferred loans for eligible first-time buyers. Income and purchase price limits apply, but these programs work alongside FHA, VA, USDA, and conventional loans to bridge the down payment gap.

Employer Assistance Programs

Major Seattle employers increasingly offer homebuyer assistance as a retention and recruitment tool. Amazon, Microsoft, and other tech companies may provide grants, forgivable loans, or matched savings programs for employees purchasing homes. These benefits often require specific tenure or position levels, so investigate your eligibility early in your planning process.

First-Time Buyer Tax Benefits

Federal tax law allows first-time buyers to withdraw up to $10,000 from traditional IRAs without the typical early withdrawal penalty when used for a home purchase. While you'll still owe income tax on the withdrawal, avoiding the 10% penalty provides additional funding flexibility. Roth IRA contributions can be withdrawn anytime without taxes or penalties, making them another potential source for down payment funds.

Interest Rate Considerations

Your interest rate dramatically impacts both your monthly payment and the total interest paid over your loan's life. Even quarter-point differences compound significantly over 30 years.

Fixed-Rate vs. Adjustable-Rate Mortgages

Most first-time buyers choose 30-year fixed-rate mortgages for payment stability and predictability. Your rate remains constant regardless of future market conditions, protecting you from payment increases. However, adjustable-rate mortgages (ARMs) offer lower initial rates, potentially saving thousands annually during the fixed period.

ARMs make sense when you plan to move or refinance within the fixed-rate period, typically 5, 7, or 10 years. For buyers certain they'll relocate for career advancement or family reasons, the lower initial rate provides real savings without exposure to rate adjustment risk.

Rate Buydowns and Discount Points

Paying discount points at closing reduces your interest rate for the loan's entire term. Each point costs 1% of your loan amount and typically reduces your rate by 0.25%. This makes financial sense if you plan to keep the mortgage long enough to recoup the upfront cost through lower monthly payments.

Conversely, accepting a slightly higher rate often allows lenders to credit closing costs, reducing your upfront cash requirements. As explained in Capital One’s guide to first-time homebuyer loans, understanding these trade-offs helps you structure financing aligned with your financial goals and cash position.

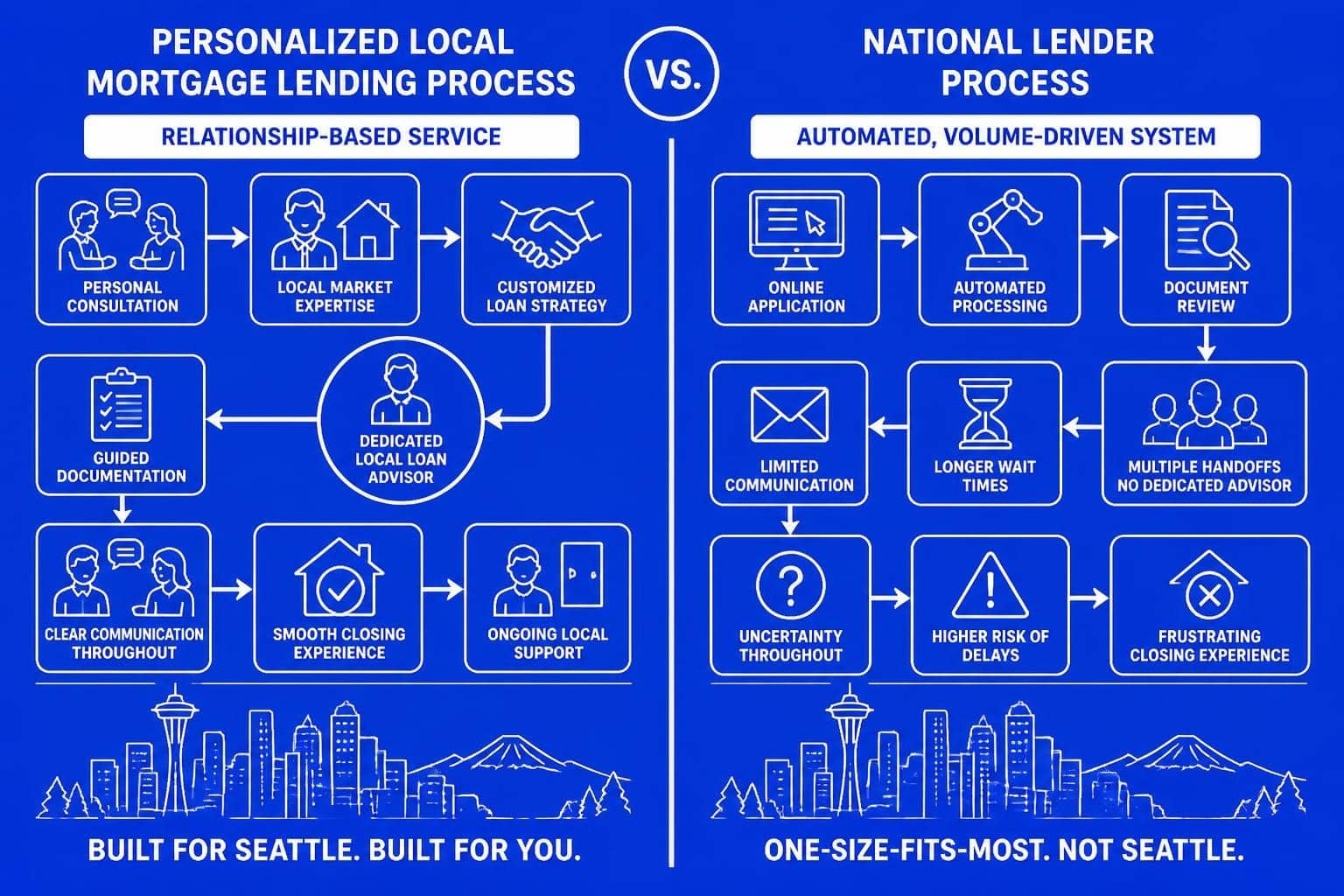

Working with a Mortgage Broker

Choosing between direct lenders and mortgage brokers represents an important early decision. Brokers access multiple lenders and loan products, often securing better rates and terms than borrowers could obtain independently, while direct lenders offer a single institution's products.

Benefits of Broker Representation

Experienced brokers bring market knowledge, negotiating leverage, and problem-solving expertise that proves invaluable for first-time buyers navigating complex situations. They handle communication with underwriters, coordinate with real estate agents and title companies, and troubleshoot issues that arise during processing.

For Seattle buyers, particularly those with stock-based compensation or complex financial situations, working with a great mortgage broker who understands local market conditions and specialized income documentation requirements often determines approval success. Brokers with 25+ years of experience and hundreds of five-star reviews demonstrate the track record and expertise needed for confident decision-making.

Questions to Ask Potential Lenders

Interviewing multiple lenders helps you compare not just rates but also service levels, expertise, and cultural fit. Ask about their experience with your specific situation, average closing timelines, and what sets them apart from competitors.

Essential questions include:

- How many first-time buyers did you help in 2025?

- What percentage of your loans close on time?

- How do you handle stock-based compensation for qualification?

- What loan programs do you recommend for my situation and why?

- Can you provide recent client references?

- What is your typical response time for questions?

For those evaluating builder incentives or new construction purchases, Kiplinger’s analysis of builder mortgage incentives provides important context about potential trade-offs these offers may include.

Long-Term Mortgage Strategy

Your initial mortgage for first home doesn't need to be permanent. Understanding refinancing opportunities, payment strategies, and equity building helps you optimize your financing over time.

When to Consider Refinancing

Refinancing makes sense when you can reduce your interest rate by at least 0.75-1%, eliminate mortgage insurance, shorten your loan term, or access equity for other financial goals. Market conditions fluctuate, and rates may drop substantially from your original mortgage, creating opportunities to save thousands over your remaining loan term.

Monitor rates annually and work with your broker to evaluate refinancing potential. Transaction costs typically range from 2-5% of the loan amount, so you need sufficient savings to justify the expense within a reasonable timeframe.

Accelerated Payoff Strategies

Making extra principal payments reduces your total interest cost and builds equity faster. Even modest additional payments create significant long-term savings. For example, paying an extra $200 monthly on a $500,000 loan at 6.5% saves over $100,000 in interest and shortens the loan by nearly 8 years.

Alternative strategies include making bi-weekly payments instead of monthly, applying windfalls like bonuses or tax refunds to principal, or refinancing to a 15-year mortgage when financially feasible. Each approach accelerates equity building and positions you for future property upgrades or investment opportunities.

Securing a mortgage for first home requires careful planning, strategic decision-making, and expert guidance, particularly in competitive markets like Seattle where home prices and buyer demand remain strong. Understanding your loan options, qualification requirements, and the complete homebuying process empowers you to make confident decisions aligned with your financial goals. Keith Akada at Mortgage Reel brings over 25 years of experience helping first-time buyers throughout Seattle, Bellevue, Redmond, and Kirkland navigate every aspect of home financing, from qualifying complex stock compensation to closing in as few as 9 business days. With 750+ five-star reviews and specialized expertise serving tech professionals, Keith provides the education, transparency, and strategic guidance that transforms first-time buyers into confident homeowners.