Understanding mortgage how does it work is essential for anyone preparing to purchase a home in Seattle, Bellevue, or surrounding areas. A mortgage represents a secured loan specifically designed for real estate purchases, where the property itself serves as collateral until you repay the borrowed funds. For tech professionals at Amazon, Microsoft, and Google navigating competitive housing markets in Redmond and Kirkland, grasping the fundamentals of mortgage mechanics can mean the difference between a confident purchase and costly mistakes. This comprehensive guide breaks down every component of the mortgage process, from initial application through final closing, with insights tailored to the Greater Seattle real estate landscape.

Understanding the Basic Mortgage Structure

When exploring mortgage how does it work, you must first recognize that a mortgage consists of two primary legal instruments: the promissory note and the security instrument (deed of trust in Washington State). The promissory note establishes your obligation to repay the borrowed amount, while the deed of trust gives the lender a legal claim against your property if you fail to meet repayment terms.

Principal and Interest Components

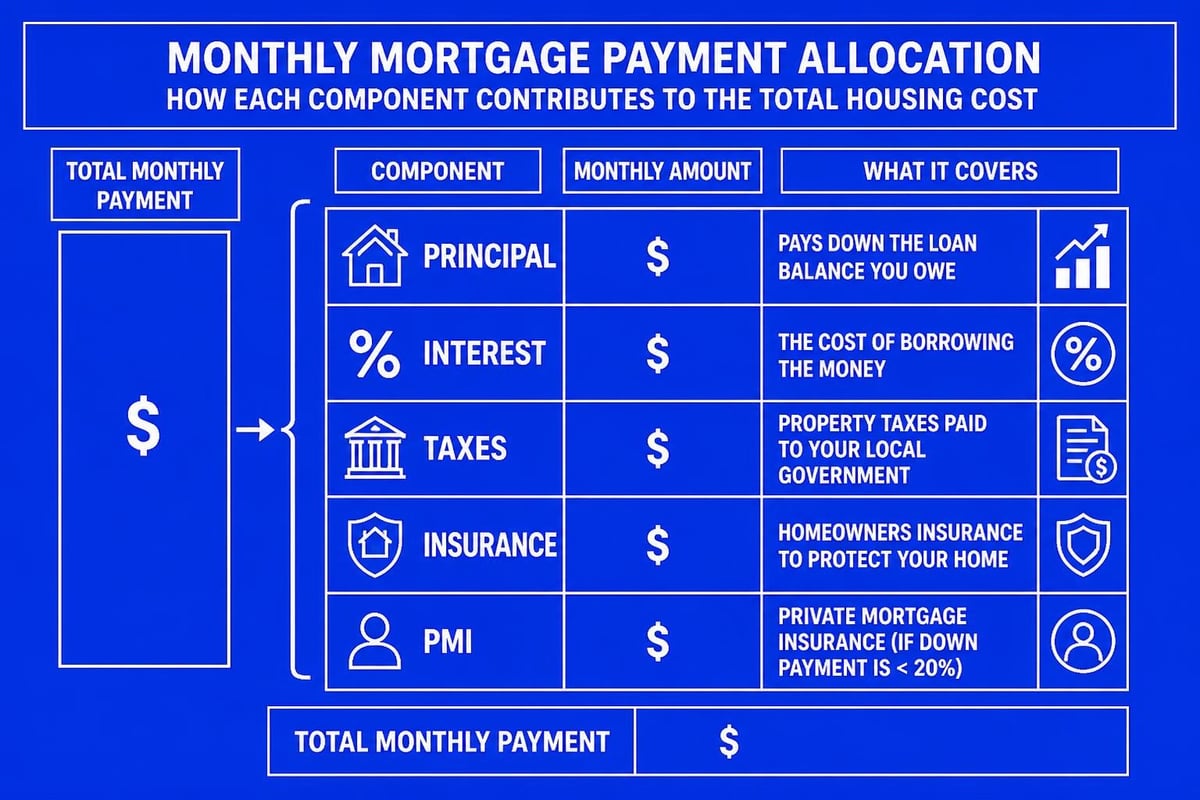

Your monthly mortgage payment divides into several distinct parts. Principal represents the portion that reduces your actual loan balance, while interest compensates the lender for extending credit and assuming risk. According to Britannica’s detailed mortgage explanation, these two components form the foundation of every mortgage payment structure.

The relationship between principal and interest shifts throughout your loan term through a process called amortization. During early years, interest claims a larger percentage of each payment. As your loan matures, increasingly larger portions apply toward principal reduction.

Additional Payment Elements

Beyond principal and interest, most mortgage payments include:

- Property taxes collected monthly and held in escrow

- Homeowners insurance premiums distributed throughout the year

- Private mortgage insurance (PMI) when down payments fall below 20%

- HOA fees for properties in managed communities (sometimes)

These combined elements create what lenders call PITI (Principal, Interest, Taxes, Insurance). For Seattle-area homes valued above conforming loan limits, jumbo home mortgage products may require additional documentation and reserves, particularly when incorporating stock compensation into qualifying income.

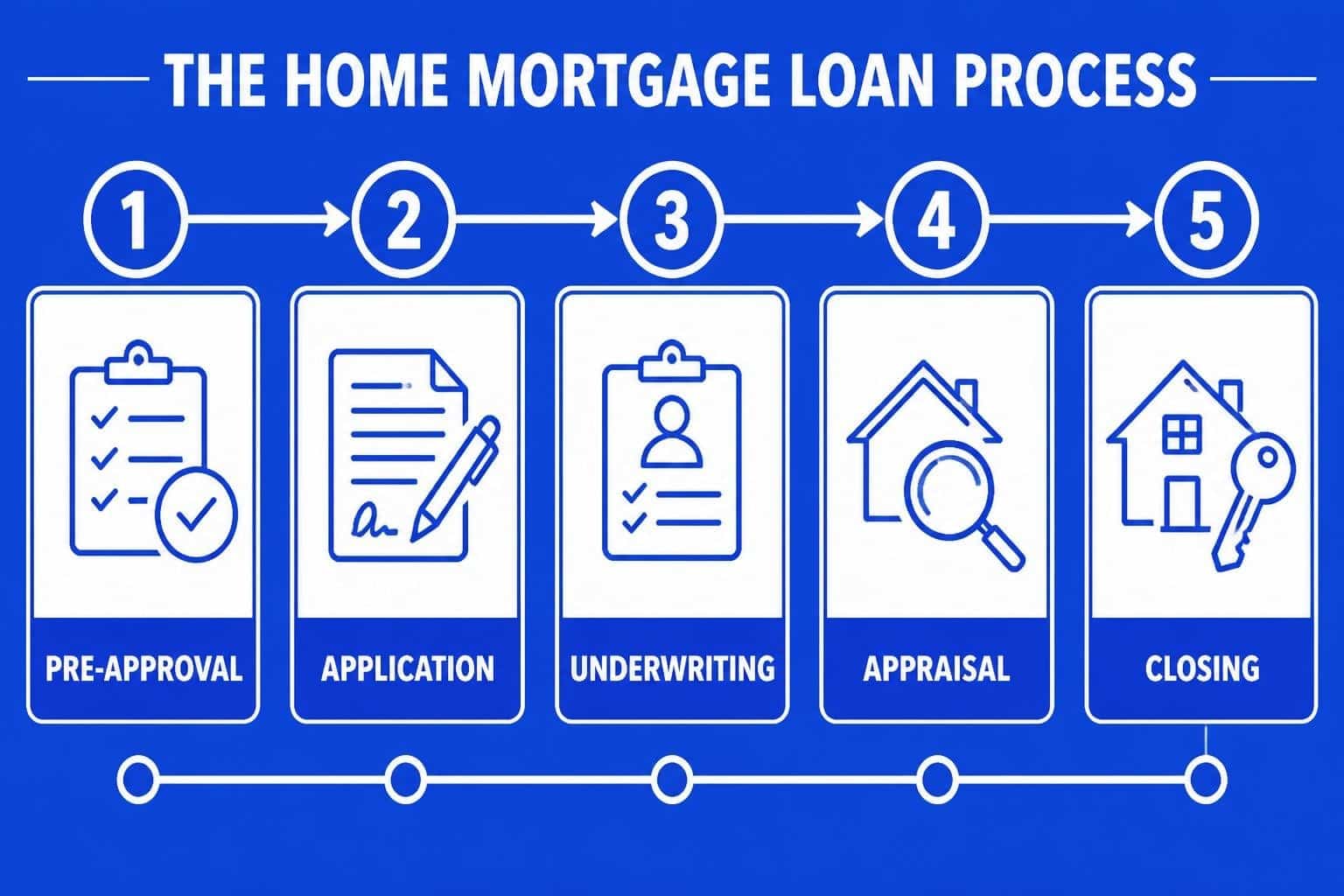

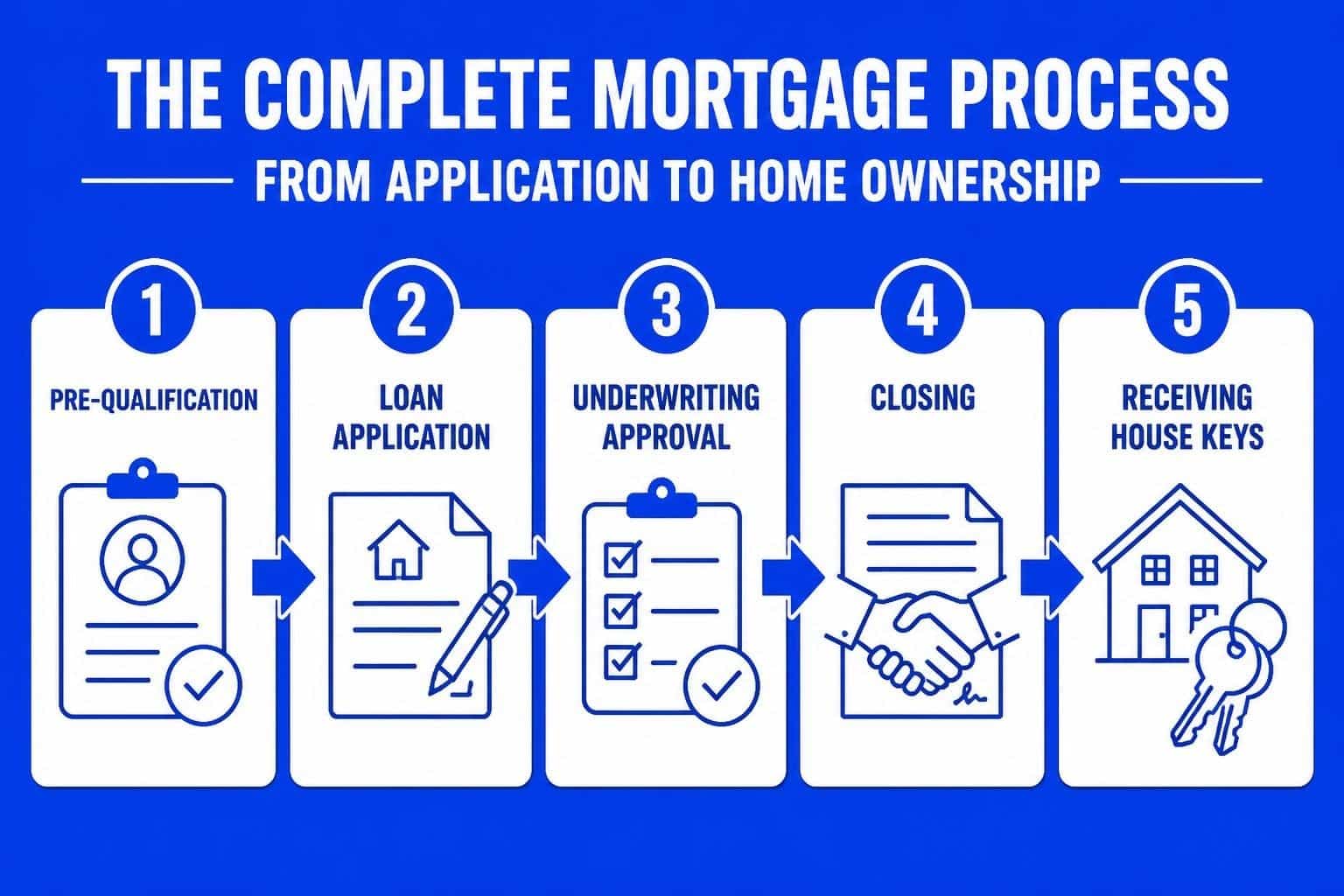

The Mortgage Application Journey

Understanding mortgage how does it work requires walking through the actual loan process from start to finish. The journey typically unfolds across six distinct phases, each with specific requirements and timelines.

Pre-Qualification and Pre-Approval

Pre-qualification offers a preliminary estimate based on self-reported financial information. This informal assessment helps you understand potential borrowing capacity without deep verification.

Pre-approval involves comprehensive documentation review, including:

- Two years of tax returns and W-2 statements

- Recent pay stubs covering 30-day periods

- Bank statements showing assets and reserves

- Credit report authorization and review

- Employment verification letters

For tech professionals in Shoreline and Lynnwood with RSUs or stock options, pre-approval becomes more nuanced. Underwriters must evaluate vesting schedules, historical stock values, and income continuity. Working with experienced professionals who understand first-time home buyers needs alongside complex compensation structures ensures accurate qualification.

Property Search and Offer Acceptance

Armed with pre-approval, you can confidently search properties within your verified budget. In competitive Seattle neighborhoods, pre-approval letters strengthen offers by demonstrating financial readiness. Sellers and listing agents favor buyers who've completed thorough vetting, particularly for properties in Lake Forest Park and Mill Creek where multiple offers frequently occur.

Once your offer receives acceptance, the formal mortgage process accelerates. Purchase agreements typically allow 30 to 45 days for financing contingencies, though some lenders can close in as few as 9 business days with proper preparation.

Loan Types and Their Mechanics

Different mortgage products operate under varying guidelines and structures. Selecting the appropriate loan type significantly impacts your long-term financial position.

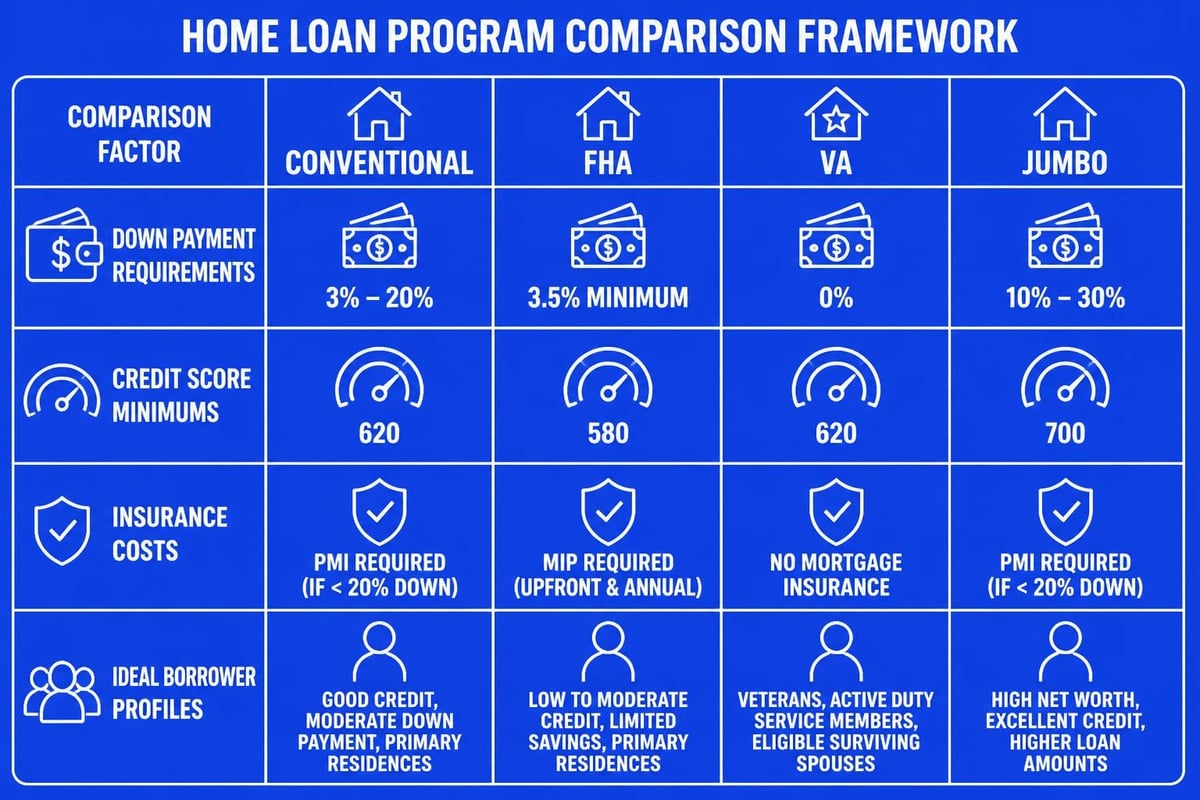

Conventional Loans

Conventional mortgages follow standards established by Fannie Mae and Freddie Mac. These loans typically require:

| Feature | Requirement |

|---|---|

| Minimum Down Payment | 3% for first-time buyers, 5% for repeat buyers |

| Credit Score | 620 minimum, 740+ for best rates |

| Debt-to-Income Ratio | 43% maximum (50% with compensating factors) |

| PMI Requirement | Required below 20% down payment |

Conventional loan lenders offer flexibility in property types and loan amounts up to conforming limits. For 2026, conforming limits in King County allow loan amounts up to $806,500 for single-family homes, though higher-priced areas may qualify for elevated limits.

Government-Backed Programs

FHA loans accommodate buyers with lower credit scores and smaller down payments. The Federal Housing Administration insures these mortgages, allowing lenders to accept 3.5% down payments from borrowers with credit scores as low as 580. However, FHA loans require both upfront and annual mortgage insurance premiums regardless of down payment size.

VA loans serve eligible military service members, veterans, and surviving spouses. These mortgages offer exceptional benefits including zero down payment requirements, no PMI, and competitive interest rates. Veterans purchasing in Everett or other Seattle suburbs should explore VA options as a potentially superior alternative to conventional financing.

USDA loans target rural and suburban properties in designated areas. While Seattle proper doesn't qualify, some outlying communities may offer USDA eligibility for income-qualified buyers.

Jumbo Loan Considerations

Properties exceeding conforming loan limits require jumbo financing. Seattle's housing market frequently necessitates jumbo products, particularly in Bellevue, Kirkland, and premium Seattle neighborhoods. According to NerdWallet’s mortgage fundamentals guide, jumbo loans typically demand:

- Larger down payments (10% to 20% minimum)

- Higher credit scores (700 to 720+)

- Lower debt-to-income ratios (43% or less)

- Significant reserve requirements (6 to 12 months)

For Microsoft and Amazon employees with substantial stock compensation, qualifying for jumbo home loans often requires specialized underwriting that properly evaluates RSU income continuity and future vesting schedules.

Interest Rates and How They're Determined

When examining mortgage how does it work, interest rate mechanics deserve particular attention. Your rate directly influences both monthly payments and total interest paid over the loan term.

Fixed-Rate Mortgages

Fixed-rate mortgages maintain consistent interest rates throughout the entire loan term. Common options include:

- 30-year fixed: Lower monthly payments, higher total interest

- 20-year fixed: Moderate payments, reduced interest costs

- 15-year fixed: Higher monthly payments, substantial interest savings

The stability of fixed rates provides predictability valuable for long-term financial planning. Redfin’s mortgage interest guide demonstrates how even modest rate differences compound significantly over time.

Adjustable-Rate Mortgages (ARMs)

ARMs feature interest rates that adjust periodically based on market index movements. Common structures include 5/1, 7/1, and 10/1 ARMs, where the first number indicates years of fixed rates before adjustments begin.

Benefits of ARMs:

- Lower initial interest rates compared to fixed mortgages

- Reduced payments during the initial fixed period

- Potential rate decreases if market rates fall

Risks to consider:

- Payment increases when rates adjust upward

- Budgeting uncertainty after the fixed period expires

- Potential negative impact if you hold the property long-term

For Seattle tech professionals anticipating stock liquidity events or career advancement, ARMs sometimes align with planned timelines for refinancing or property upgrading.

The Down Payment Equation

Down payments represent your initial equity stake in the property. Understanding how down payment size affects overall mortgage mechanics helps optimize your financing strategy.

Minimum Requirements by Loan Type

Different programs establish varying down payment thresholds:

| Loan Type | Minimum Down Payment | PMI Requirement |

|---|---|---|

| Conventional | 3% to 5% | Yes, below 20% |

| FHA | 3.5% | Always required |

| VA | 0% | Never required |

| Jumbo | 10% to 20% | Varies by lender |

Larger down payments reduce loan amounts, monthly payments, and total interest costs. However, maintaining adequate reserves for emergencies, repairs, and opportunity costs requires balancing down payment size against liquidity needs.

Down Payment Assistance Programs

Washington State offers several assistance programs for qualified buyers in Seattle and surrounding areas. These programs provide grants, forgivable loans, or deferred-payment second mortgages to supplement buyer contributions.

First-time home buyers in Washington may qualify for down payment assistance through Washington State Housing Finance Commission programs, which often feature income limits and property price restrictions. Mill Creek and Lynnwood properties frequently fall within eligible price ranges.

Mortgage Insurance Explained

Understanding mortgage how does it work includes recognizing when and why insurance requirements apply. Mortgage insurance protects lenders against borrower default risk when down payments fall below certain thresholds.

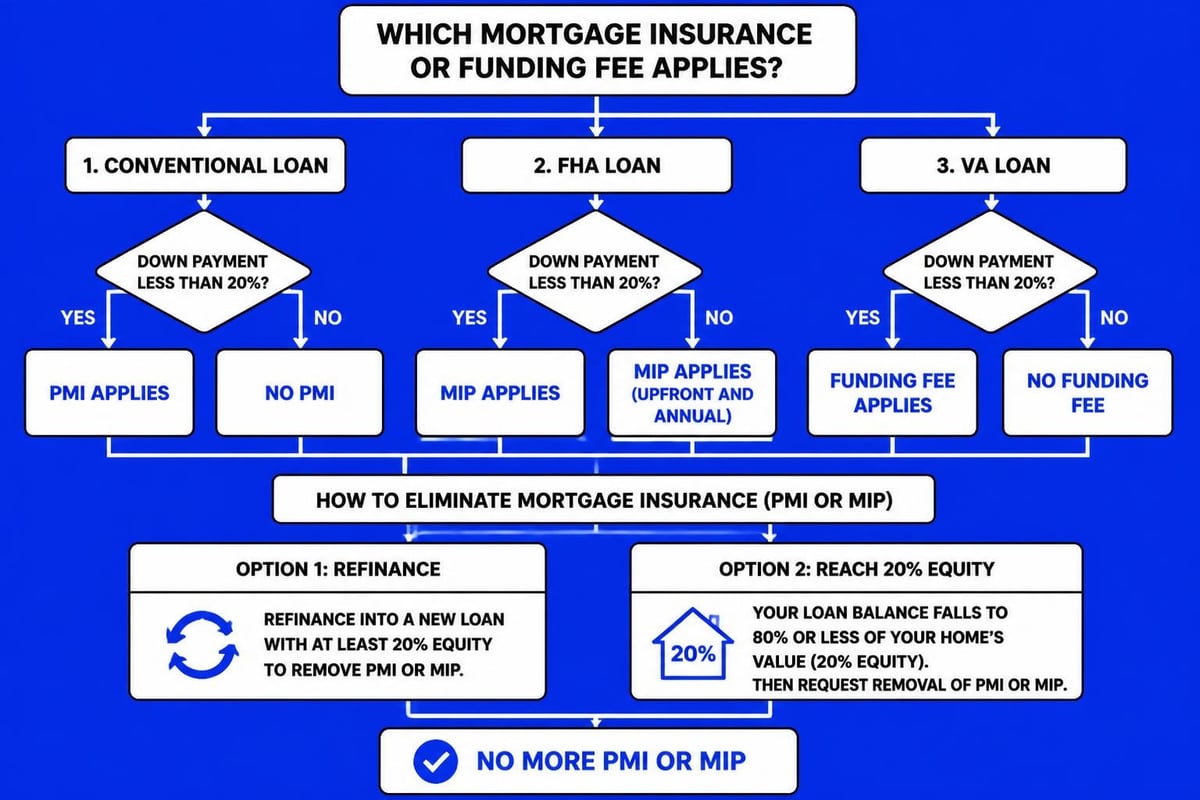

Private Mortgage Insurance (PMI)

Conventional loans with less than 20% down payment require PMI. This insurance typically costs 0.3% to 1.5% of the original loan amount annually, divided into monthly premiums added to your payment.

According to the Consumer Financial Protection Bureau’s mortgage insurance explanation, PMI automatically terminates once your loan balance reaches 78% of the original property value, provided you maintain current payment status. You can also request cancellation upon reaching 80% loan-to-value through payments or appreciation.

FHA Mortgage Insurance

FHA loans require two insurance components:

- Upfront Mortgage Insurance Premium (UFMIP): 1.75% of the loan amount, typically financed into the mortgage

- Annual Mortgage Insurance Premium (MIP): 0.45% to 1.05% annually, depending on loan term and down payment

For FHA loans originated after June 2013 with down payments below 10%, MIP continues for the entire loan term. This permanent insurance represents a significant long-term cost factor when comparing FHA versus conventional financing options.

The Underwriting and Approval Process

Once you've submitted a complete loan application with supporting documentation, underwriting begins. This critical phase determines whether the lender approves your mortgage request.

Documentation Review

Underwriters examine three primary areas:

Income verification confirms employment stability and sufficient earnings to support mortgage obligations. For traditional W-2 employees, this process remains straightforward. Tech professionals with stock compensation face more complex analysis, as underwriters must determine what percentage of RSU income qualifies for debt-to-income calculations.

Asset verification ensures you possess adequate funds for down payment, closing costs, and reserves. Bank statements must show seasoned funds (typically 60 days of account history) to prevent undisclosed borrowed down payments.

Credit evaluation assesses your borrowing history, payment patterns, and current debt obligations. Underwriters review credit reports for accuracy and may request explanations for derogatory marks, inquiries, or unusual patterns.

Appraisal Requirements

Lenders require professional appraisals to confirm property values support loan amounts. Appraisers evaluate:

- Recent comparable sales in the neighborhood

- Property condition and features

- Market trends affecting value

In Seattle's competitive market, appraisal gaps sometimes occur when purchase prices exceed appraised values. Buyers must either negotiate price reductions, increase down payments to cover gaps, or terminate contracts under appraisal contingencies.

Conditional Approval and Clear to Close

Initial underwriting typically generates conditional approval with specific documentation requests or clarifications needed. Common conditions include:

- Updated pay stubs or bank statements

- Explanation letters for credit inquiries or deposits

- Verification of employment immediately before closing

- Title clearance and homeowners insurance proof

Once you satisfy all conditions, the loan reaches clear to close status. This milestone means underwriting approval is complete and closing can proceed on schedule. For those exploring mortgage financing options in Shoreline or Lake Forest Park, understanding these phases helps set realistic timeline expectations.

Closing: The Final Steps

The closing process represents the culmination of your mortgage journey, where ownership officially transfers and loan funding occurs.

Final Walk-Through

Before closing, conduct a final property inspection to verify:

- Agreed-upon repairs were completed properly

- Property condition remains consistent with purchase agreement

- Seller has removed personal belongings

- Major systems (HVAC, plumbing, electrical) function properly

Closing Disclosure Review

At least three business days before closing, you'll receive the Closing Disclosure, a standardized form detailing:

- Final loan terms and monthly payment amounts

- Closing costs itemized by category

- Cash required to close

- Comparison to initial Loan Estimate

Review this document carefully against your Loan Estimate. According to Fidelity’s comprehensive mortgage overview, significant changes in loan terms may require a new three-day waiting period.

The Closing Table

Closings typically occur at title company offices, where you'll:

- Review and sign loan documents (promissory note, deed of trust)

- Sign closing disclosures and settlement statements

- Provide certified funds for down payment and closing costs

- Receive property keys and official ownership

Washington State closings involve escrow companies that coordinate between all parties, hold funds, and ensure proper document recording. Most closings conclude within one to two hours.

Post-Closing Responsibilities

Understanding mortgage how does it work extends beyond closing day. Homeownership brings ongoing financial and maintenance obligations.

Making Payments

Your first mortgage payment typically comes due on the first day of the month following your first full month of ownership. If you close on June 15th, your first payment arrives August 1st (covering July interest).

Many lenders offer automatic payment options that prevent missed payments and may provide slight interest rate reductions. Setting up autopay through your mortgage servicer ensures consistent on-time payments that protect your credit profile.

Escrow Account Management

Lenders conduct annual escrow analyses to ensure collected amounts adequately cover property taxes and insurance premiums. If either expense increases, your monthly payment adjusts upward. Conversely, decreases generate refunds or payment reductions.

Refinancing Opportunities

Market conditions and personal circumstances may create refinancing opportunities. Consider refinancing when:

- Interest rates drop significantly below your current rate

- Your credit profile improves enough to qualify for better terms

- You've accumulated sufficient equity to eliminate PMI

- You want to switch from ARM to fixed-rate financing

For Seattle homeowners who've benefited from rapid appreciation in Bellevue or Redmond, refinancing options might unlock better terms or allow cash-out refinancing for other financial goals.

Special Considerations for Tech Professionals

Seattle's concentration of major technology employers creates unique mortgage considerations. Understanding how lenders evaluate stock compensation significantly impacts borrowing capacity.

RSU and Stock Option Qualification

Most lenders require two-year histories of stock compensation to include it as qualifying income. Underwriters typically average RSU values over 24 months and may apply haircuts (reductions) to account for volatility. Some advanced underwriting platforms allow:

- Use of current vesting schedules to project future income

- Consideration of unvested RSUs with documented continuity

- Qualification of restricted stock units at current market values

These sophisticated approaches require lenders experienced with tech employee compensation structures, particularly for jumbo mortgage products common in Seattle's higher-priced markets.

Bonus Income Documentation

Annual bonuses require similar documentation showing consistency over two years. Underwriters examine whether bonuses represent guaranteed compensation or discretionary awards. Declining bonus trends may reduce usable income, while increasing patterns can strengthen qualification.

Liquidity Event Planning

Employees anticipating IPOs, acquisitions, or major stock events should consult mortgage professionals before major financial changes. Large deposits from stock sales can complicate qualification if not properly documented and seasoned. Planning loan applications around these events optimizes qualification while preserving flexibility.

Common Mortgage Mistakes to Avoid

Even sophisticated buyers sometimes stumble during the mortgage process. Recognizing common pitfalls helps you navigate successfully.

Changing jobs during the process: Employment changes between application and closing can derail approvals. Lenders require stability, and new employment often necessitates waiting periods before income qualifies.

Making large purchases: Financing furniture, vehicles, or other major expenses before closing can push debt-to-income ratios beyond acceptable limits. Delay significant purchases until after closing.

Skipping pre-approval: Searching without pre-approval wastes time on properties beyond your budget and weakens your competitive position when you find the right home.

Ignoring credit during the process: Underwriters pull credit immediately before closing. New accounts, increased balances, or missed payments discovered during this final check can prevent closing.

Underestimating closing costs: Beyond down payments, expect 2% to 5% of the purchase price in closing costs. Microsoft’s mortgage guide emphasizes proper budgeting for these additional expenses.

Market-Specific Insights for Seattle Buyers

Seattle's housing market presents unique dynamics that affect mortgage strategies. Median home prices significantly exceed national averages, with Bellevue and Kirkland commanding premium valuations.

Competitive Offer Environments

Multiple-offer scenarios remain common, particularly for desirable properties in Mill Creek and Lake Forest Park. Strategies to strengthen your position include:

- Obtaining pre-approval from reputable local lenders

- Offering larger earnest money deposits

- Limiting contingencies when financially prudent

- Demonstrating closing flexibility to accommodate seller timelines

Rising Property Values

Consistent appreciation provides equity-building opportunities but requires careful affordability analysis. Calculate whether monthly payments remain sustainable across various economic scenarios, including job changes, interest rate adjustments (for ARMs), or unexpected expenses.

Condominium Considerations

Seattle's urban core features extensive condominium inventory. Condo financing requires additional scrutiny of:

- HOA financial health and reserve funds

- Owner-occupancy ratios within buildings

- Pending litigation affecting the association

- Warrantability through Fannie Mae/Freddie Mac guidelines

Not all condos qualify for conventional financing. Working with knowledgeable professionals familiar with the mortgage lending process in Seattle ensures you target financeable properties.

Building Long-Term Wealth Through Homeownership

Beyond providing shelter, mortgages serve as structured savings vehicles that build equity through forced principal reduction and potential appreciation. For Everett and Shoreline residents, homeownership historically delivers superior long-term returns compared to renting, despite higher upfront costs.

Equity Accumulation Strategies

Accelerate equity building through:

- Making additional principal payments when financially feasible

- Choosing shorter loan terms (15 or 20 years versus 30)

- Leveraging appreciation in strong markets

- Maintaining properties to preserve and enhance value

Tax Advantages

Mortgage interest and property taxes generally qualify as itemized deductions on federal tax returns. For high-income tech professionals in Seattle, these deductions can generate substantial tax savings, though 2026 tax laws cap deductions and may limit benefits compared to standard deductions.

Portfolio Diversification

Real estate provides diversification beyond stock-heavy portfolios common among technology employees. While your primary residence shouldn't be viewed purely as an investment, it does offer inflation protection and tangible asset characteristics that complement liquid investment holdings.

Understanding mortgage how does it work empowers you to navigate one of life's largest financial transactions with confidence and clarity. From selecting the appropriate loan type to closing on your Seattle-area home, each step builds toward successful homeownership. Whether you're a first-time buyer in Lynnwood exploring home loans for first home buyers or a tech professional seeking jumbo financing in Bellevue, working with experienced professionals makes the difference between stress and success. Keith Akada at Mortgage Reel brings 25+ years of expertise helping Seattle homebuyers qualify complex compensation, navigate competitive markets, and close quickly with transparency and strategy you can trust.