Finding the right mortgage financing can make or break your homebuying experience, particularly in competitive markets like Seattle, Bellevue, Redmond, and Kirkland. While national banks and online lenders advertise competitive rates, local mortgage loans offer distinct advantages that can streamline your purchase and provide the personalized guidance needed to navigate complex financing scenarios. Understanding the difference between working with a community-based professional versus a distant call center becomes especially important when you're competing for limited inventory or dealing with unique income situations like stock compensation.

Why Local Mortgage Loans Matter in Seattle's Housing Market

The Greater Seattle area presents unique challenges for homebuyers. With median home prices consistently above national averages and significant competition from tech professionals, securing financing that aligns with regional market realities makes a measurable difference.

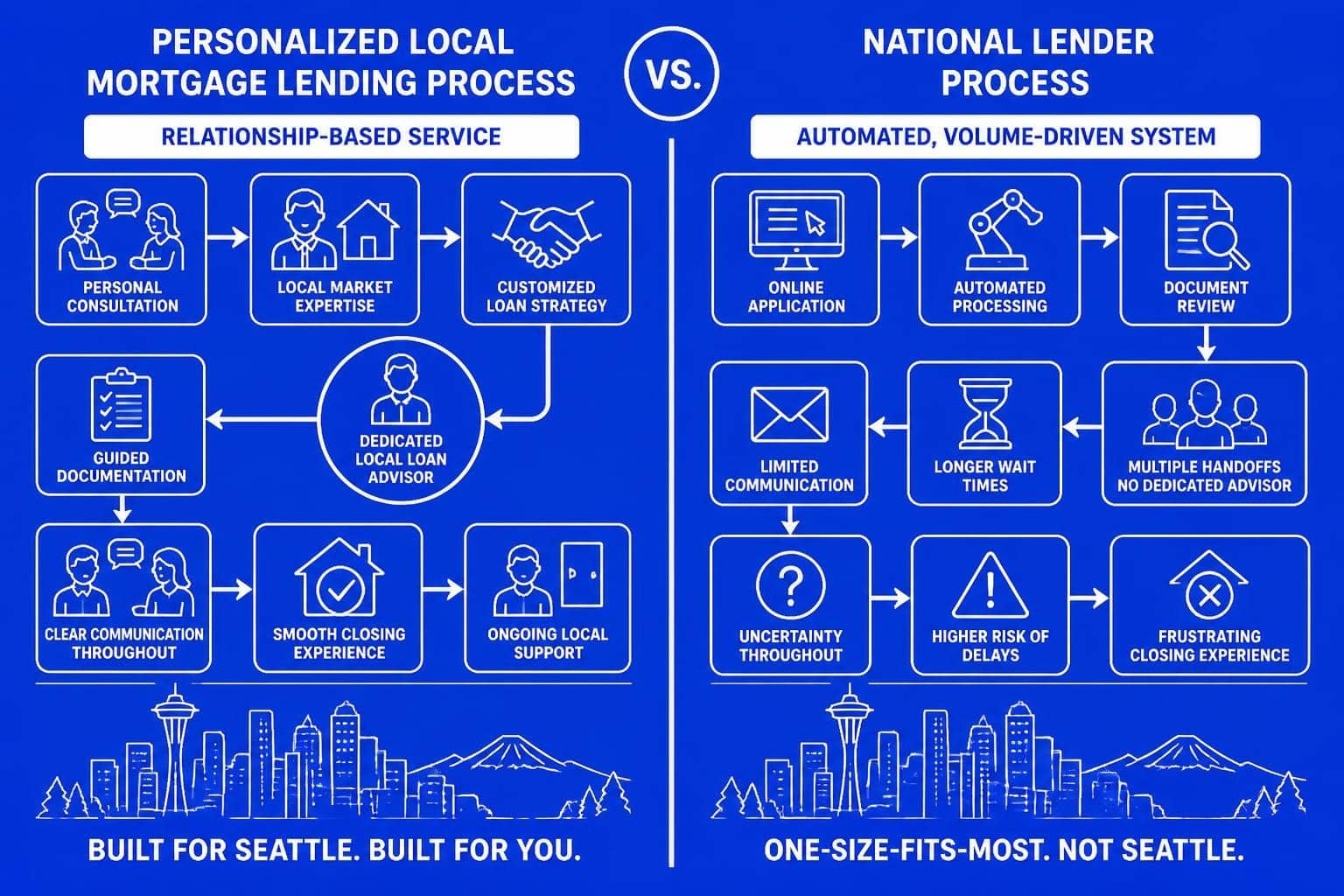

Local mortgage loans through community-based professionals offer several strategic advantages over national alternatives. Market knowledge stands at the forefront-understanding that a property in Shoreline may require different underwriting considerations than one in Mill Creek, or that local appraisers follow specific valuation patterns in neighborhoods like Lynnwood and Lake Forest Park.

Speed and Responsiveness

In competitive offer situations, response time determines success. Local professionals can:

- Answer calls and emails outside traditional business hours

- Provide same-day pre-approval letters with specific property addresses

- Coordinate directly with listing agents and title companies in your area

- Adjust documentation requests based on local underwriting patterns

National lenders typically route applications through centralized processing centers in different time zones, creating delays when quick decisions matter most. When you're submitting an offer on a Lake Forest Park home on Saturday afternoon, having a Seattle mortgage broker who understands local market timing can be the difference between acceptance and rejection.

Understanding Your Local Financing Options

Local mortgage loans encompass the same product types as national lenders but with personalized application to your specific situation. The Consumer Financial Protection Bureau outlines standard loan options including conventional, FHA, VA, and USDA loans-all available through local professionals with added strategic guidance.

Conventional Financing

Conventional loans remain the most common financing vehicle for Seattle-area homebuyers, particularly those with stable employment and solid credit profiles. These loans offer:

- Down payment flexibility from 3% to 20% or more

- Competitive interest rates for well-qualified borrowers

- No upfront mortgage insurance premium

- Higher loan limits suitable for Bellevue and Redmond markets

For tech professionals earning stock compensation, local mortgage loans can incorporate RSUs, ESPP income, and bonuses into qualifying calculations more effectively than automated systems. This specialized income treatment often makes the difference between qualifying for a $800,000 home versus a $1.2 million property.

| Loan Feature | Local Advantage | National Lender Approach |

|---|---|---|

| Income Calculation | Customized analysis of stock compensation, bonuses, overtime | Rigid formula-based calculations |

| Document Review | Line-by-line guidance on what's needed | Generic checklists |

| Underwriting Communication | Direct conversations with decision makers | Multi-layer approval hierarchy |

| Closing Timeline | 9-21 business days typical | 30-45 days standard |

Jumbo Loan Expertise

Seattle's housing market frequently requires jumbo home loans for properties exceeding conforming loan limits. In 2026, King County conforming limits sit at $806,500 for single-family homes, making jumbo financing essential for much of the Eastside market.

Local mortgage loans for jumbo scenarios provide:

- Relationship-based underwriting that considers the complete financial picture

- Competitive rates through established investor relationships

- Experience with high-value Seattle neighborhoods

- Clear communication about reserve requirements and documentation standards

Tech professionals at Amazon, Microsoft, and Google particularly benefit from local expertise in qualifying stock-based compensation for jumbo financing. Understanding vesting schedules, grant types, and continuity calculations requires specialized knowledge that generic underwriting systems don't accommodate well.

The Local Advantage: Service and Accountability

Beyond product knowledge, local mortgage loans deliver relationship-based service that creates accountability throughout the process. When your loan officer lives and works in the Seattle area, their professional reputation depends on consistent execution and community trust.

Transparent Communication

Working with a highly reviewed loan officer means accessing clear explanations of every step, proactive updates on status changes, and honest assessments of timeline expectations. This transparency becomes particularly valuable for first-time buyers navigating unfamiliar terminology and requirements.

Communication standards should include:

- Initial consultation within 24 hours of contact

- Pre-approval documentation clearly outlined with specific requests

- Regular status updates at key milestones

- Problem-solving communication when issues arise

- Post-closing follow-up for refinancing and future purchases

Local professionals build their business on referrals and reviews, creating natural incentives for exceptional service. You can verify this reputation through multiple platforms and often speak directly with past clients in your area.

Market-Specific Guidance

Seattle's neighborhoods each present distinct characteristics that affect financing strategy. A local professional understands:

- Shoreline: Mix of single-family homes and condominiums with varying HOA structures

- Lynnwood: Growing development with new construction financing considerations

- Lake Forest Park: Established neighborhoods with potential appraisal challenges

- Mill Creek: Master-planned community with specific documentation for amenities

- Everett: More affordable entry point with diverse property types

This neighborhood knowledge informs realistic expectations about appraisals, required inspections, and potential financing obstacles before you submit an offer.

Qualifying for Local Mortgage Loans

Understanding qualification requirements helps you prepare effectively and set realistic expectations. Local mortgage loans follow the same fundamental guidelines as national lenders but apply them with contextual understanding of Seattle's employment landscape and income patterns.

Income Documentation Standards

For traditional W-2 employees, qualification typically requires:

- Two years of employment history (or relevant education/training)

- Most recent pay stubs covering 30 days

- W-2 forms from the previous two years

- Tax returns if claiming additional income sources

Self-employed borrowers need more comprehensive documentation, including business tax returns, profit and loss statements, and evidence of business continuity. Local professionals excel at presenting self-employment income in the most favorable light while maintaining compliance with underwriting standards.

Credit Profile Considerations

Credit scores significantly impact both approval odds and interest rates. General thresholds include:

| Loan Type | Minimum Score | Competitive Score | Optimal Score |

|---|---|---|---|

| Conventional | 620 | 680 | 740+ |

| FHA | 580 (3.5% down) | 620 | 660+ |

| VA | No minimum | 620 | 660+ |

| Jumbo | 680 | 720 | 760+ |

Local mortgage brokers can review credit reports line-by-line, identify opportunities for rapid rescoring, and recommend strategic approaches to address credit issues. This personalized analysis often reveals qualification possibilities that automated systems miss.

Down Payment and Reserve Requirements

Down payment requirements vary by loan type and property characteristics. Beyond the initial down payment, lenders assess reserves-the months of mortgage payments you can cover with liquid assets after closing.

Conventional loans typically require:

- 3% down minimum for primary residences

- 2-6 months reserves depending on loan amount and credit profile

- Higher requirements for investment properties or second homes

First-time homebuyers often benefit from down payment assistance programs available through Washington State Housing Finance Commission and local jurisdictions. A local professional stays current on available programs and eligibility requirements.

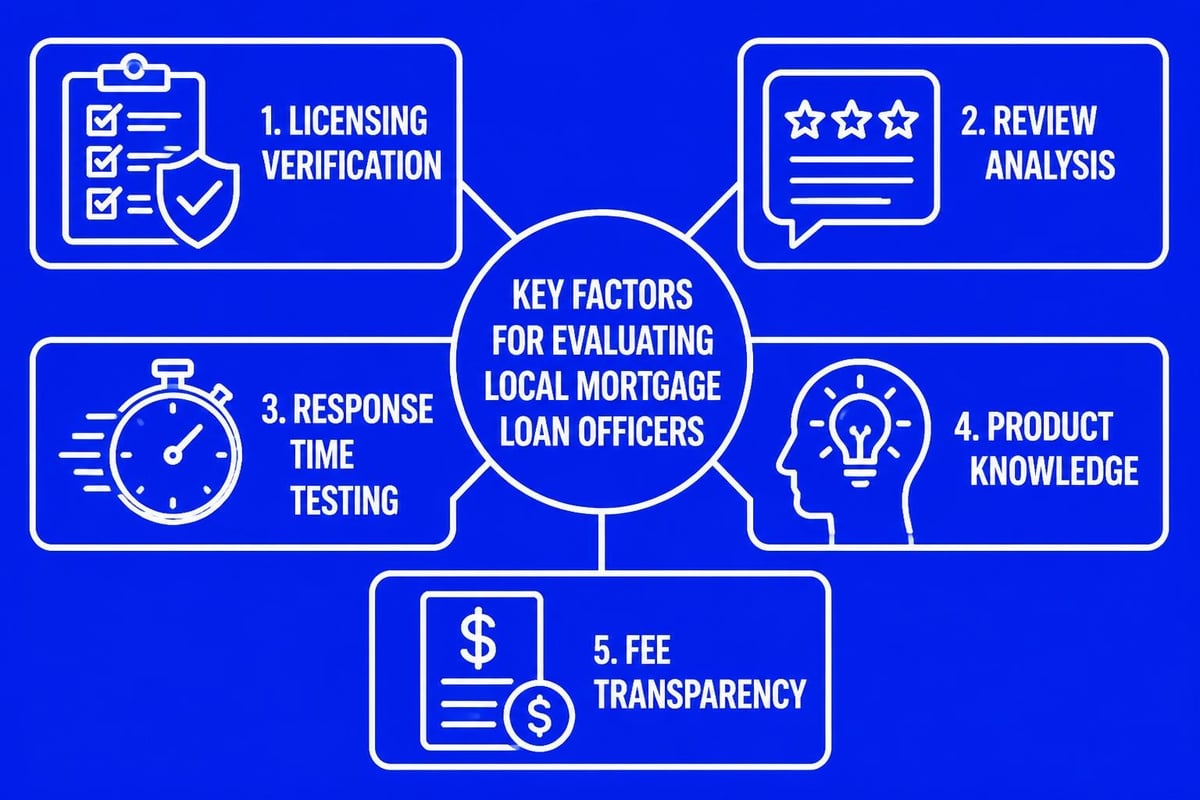

Selecting Your Local Mortgage Professional

The choice between national lenders and local mortgage loans deserves careful consideration. Bankrate’s comparison of national versus local lenders highlights key decision factors including service quality, rate competitiveness, and closing speed.

Verification and Credentials

Before committing to any mortgage professional, verify their licensing and authorization. The Consumer Financial Protection Bureau provides guidance on checking lender credentials through the Nationwide Multistate Licensing System (NMLS).

Washington State requires mortgage loan originators to:

- Maintain active NMLS registration

- Complete continuing education requirements

- Pass background checks and financial responsibility reviews

- Carry errors and omissions insurance

Additionally, review the Washington State Department of Financial Institutions’ guide to home loans for consumer protection information and regulatory oversight details.

Review and Reputation Assessment

Online reviews provide valuable insights into service quality and execution reliability. Look for:

- Consistency across multiple platforms (Google, Zillow, Yelp)

- Specificity in feedback about communication, speed, and problem-solving

- Volume indicating sustained performance over time

- Recent reviews confirming current service standards

A loan officer with 750+ five-star reviews across multiple platforms demonstrates exceptional consistency and client satisfaction. Pay attention to reviews mentioning challenging scenarios-complex income situations, tight timelines, or problem-solving abilities.

Rate and Fee Transparency

Competitive pricing matters, but lowest advertised rates don't always translate to best value. Local mortgage loans should include:

- Clear fee disclosure with itemized costs

- Rate lock policies explaining lock periods and extension fees

- Lender credit options showing rate-cost tradeoffs

- Third-party cost estimates for title, escrow, and recording fees

Request Loan Estimates from multiple sources and compare not just rates but total closing costs, required reserves, and prepayment terms. A trustworthy professional explains these tradeoffs clearly rather than highlighting only favorable comparisons.

Navigating Special Circumstances

Seattle's diverse employment landscape creates unique financing scenarios that benefit from local expertise. Stock compensation, contract work, international income, and non-traditional employment all require specialized approach.

Stock-Based Compensation

Tech professionals frequently hold significant wealth in RSUs, stock options, and ESPP shares. Local mortgage loans can incorporate this income when properly documented and analyzed. Underwriters typically require:

- Grant agreements showing vesting schedules

- Pay stubs reflecting income deposits

- Tax returns documenting two-year history (if available)

- Vesting continuity evidence of ongoing grants

The calculation methodology varies by grant type. RSUs with regular vesting typically qualify at 100% of expected income. Stock options require more complex analysis of strike prices and vesting likelihood.

Self-Employment and Contract Income

Seattle's gig economy and entrepreneurial culture means many buyers earn income through non-traditional employment. Self-employed borrowers benefit from local professionals who understand:

- Industry-specific expense patterns

- Legitimate business deductions that don't reduce qualifying income

- Partnership and S-corporation income calculations

- Strategies for presenting income trends favorably

Two years of self-employment history typically suffices, though exceptions exist for buyers transitioning from related employment or with significant assets.

Multi-Property Strategies

Real estate investors require different approaches than primary residence buyers. Local mortgage loans for investment properties involve:

- Higher down payment requirements (typically 15-25%)

- Rental income qualification from existing properties

- Portfolio lending for buyers with multiple mortgaged properties

- Strategic timing for purchases and refinances

A local professional with investor experience can sequence purchases to optimize qualification and leverage existing equity effectively.

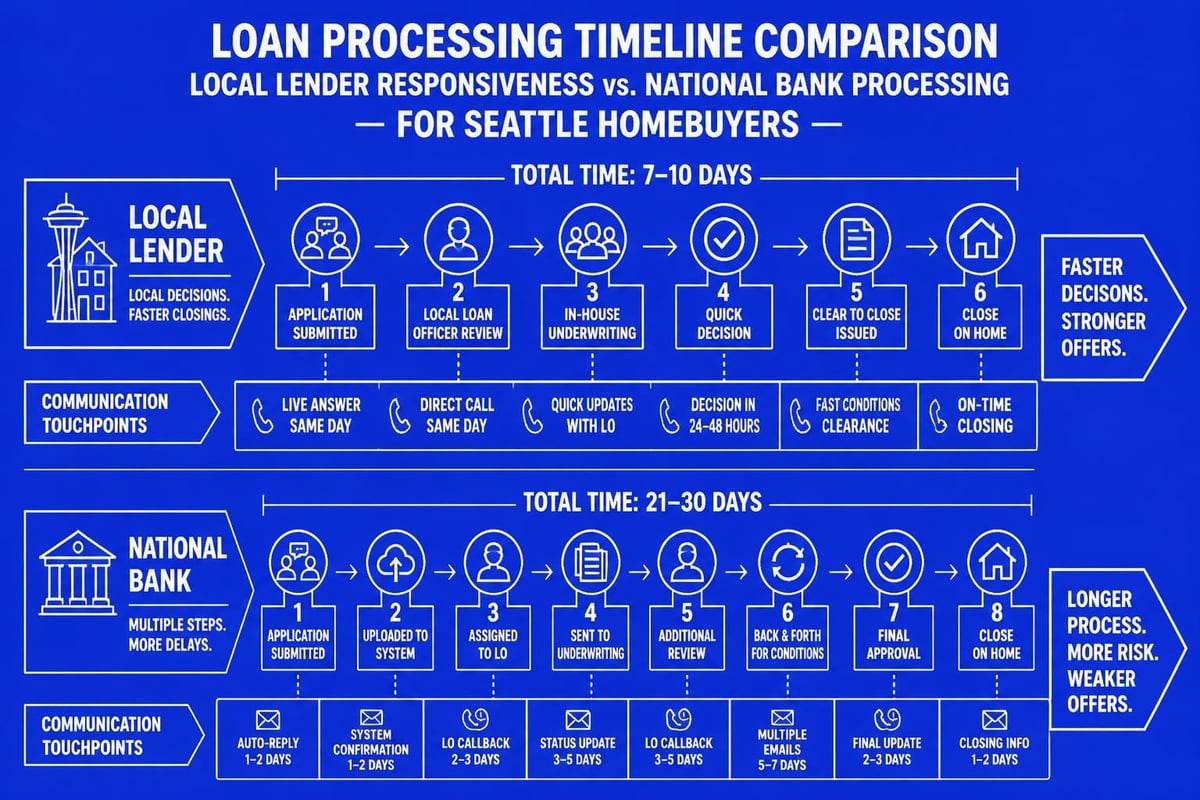

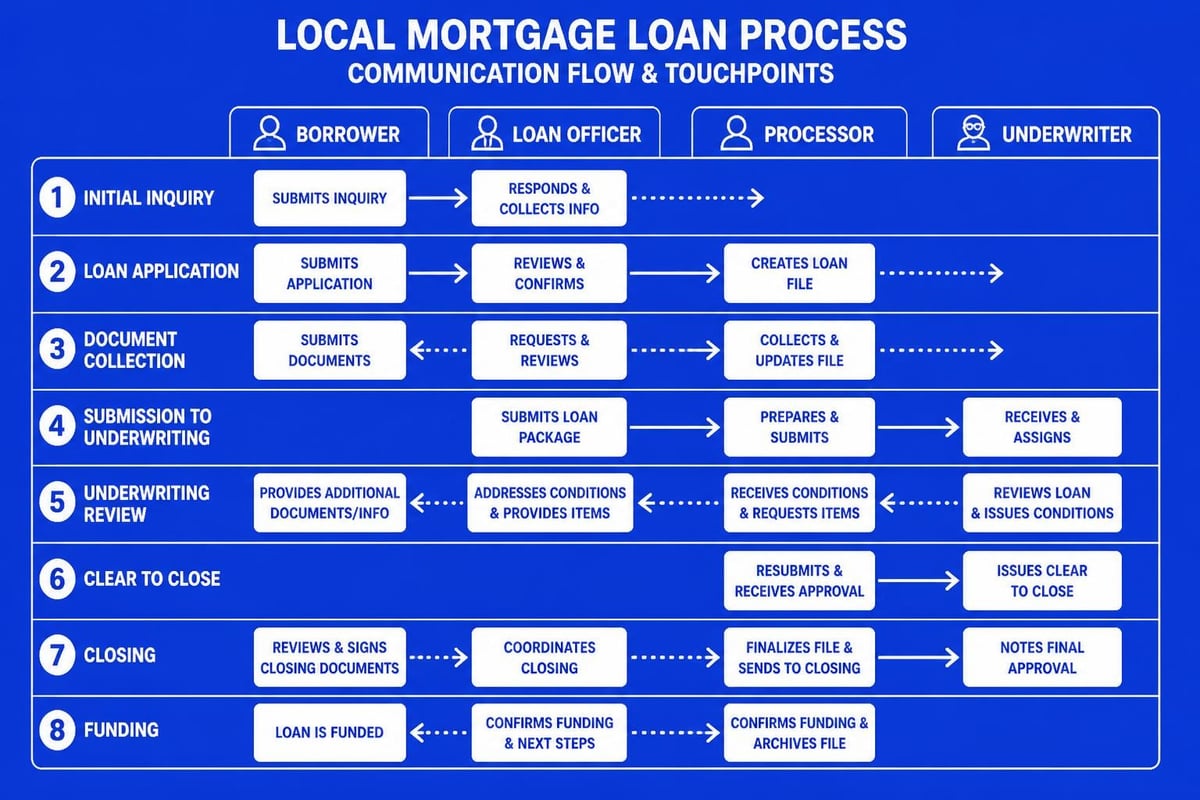

Timeline Expectations for Local Mortgage Loans

Understanding realistic timelines helps you plan effectively and set appropriate expectations with sellers. While Fairway's advanced underwriting enables closings in as few as 9 business days, typical timelines vary based on loan complexity and property characteristics.

Pre-Approval Phase (1-3 Days)

Initial pre-approval requires basic documentation:

- Recent pay stubs

- Bank statements showing down payment funds

- Authorization for credit report

- Basic employment verification

A responsive local professional provides pre-approval letters within 24-48 hours for straightforward scenarios. Complex income situations may require additional time for analysis and documentation.

Application to Clear-to-Close (15-25 Days)

Once under contract, the timeline includes:

- Complete application (Day 1)

- Processing review (Days 2-5)

- Underwriting submission (Days 6-8)

- Initial underwriting decision (Days 9-12)

- Condition resolution (Days 13-20)

- Final approval (Days 21-25)

Delays typically stem from appraisal scheduling, title issues, or incomplete documentation. Local professionals anticipate common obstacles and request documentation proactively.

Closing Preparation (3-5 Days)

Final steps before closing include:

- Title clearance and final title policy

- Closing disclosure review (required 3 business days before closing)

- Final walkthrough coordination

- Funding preparation and wire instructions

Clear communication during this phase ensures smooth execution and eliminates last-minute surprises.

Managing Costs and Maximizing Value

Local mortgage loans should deliver not just competitive rates but total cost efficiency. Understanding the complete expense picture helps you make informed decisions and avoid unnecessary costs.

Closing Cost Components

Total closing costs typically range from 2% to 5% of the purchase price, including:

- Lender fees: Origination, underwriting, processing

- Third-party costs: Appraisal, credit report, title insurance

- Prepaid items: Interest, property taxes, insurance premiums

- Escrow deposits: Tax and insurance reserves

Some costs are negotiable or can be offset through seller credits or lender credits in exchange for slightly higher rates. A transparent professional presents these tradeoffs clearly.

Rate Lock Strategies

Interest rate locks protect against rate increases during your transaction. Lock strategies depend on:

- Current rate trends and economic indicators

- Time until closing

- Rate volatility and risk tolerance

- Lock extension fees if closing delays occur

For competitive Seattle markets with quick closings, shorter lock periods (15-30 days) often suffice. New construction or complex transactions may benefit from 45-60 day locks despite slightly higher costs.

Long-Term Cost Considerations

Beyond closing, evaluate total ownership costs:

- Monthly payment including principal, interest, taxes, and insurance

- Private mortgage insurance (if applicable)

- HOA fees for condominiums and planned communities

- Maintenance and repair reserves

Mortgage financing strategies should align with your long-term plans for the property and overall financial goals.

Refinancing with Local Mortgage Loans

Rate and term refinancing provides opportunities to reduce payments, adjust loan terms, or access equity as circumstances change. Local professionals offer strategic guidance on when refinancing makes sense.

Refinancing Scenarios

Common refinancing triggers include:

- Rate reduction: Lowering your rate by 0.50% or more

- Term adjustment: Switching from 30-year to 15-year terms

- PMI removal: Eliminating mortgage insurance after reaching 20% equity

- Debt consolidation: Cash-out refinancing to eliminate high-interest debt

Break-even analysis determines whether savings justify closing costs. Generally, if you recoup costs within 2-3 years, refinancing makes financial sense.

Streamlined Refinancing Options

VA and FHA loans offer streamlined refinancing programs with reduced documentation and faster processing. These programs benefit homeowners who've maintained strong payment history but may not qualify under current stricter standards.

Conventional borrowers can access similar efficiency through desktop appraisals and automated valuation models when equity position and payment history support reduced verification.

Securing the right financing transforms your homebuying experience from stressful to strategic, particularly in competitive markets like Seattle, Bellevue, and the greater Eastside area. Local mortgage loans deliver the personalized service, market expertise, and responsive communication that turn complex transactions into smooth closings. Whether you're a first-time buyer navigating the process, a tech professional leveraging stock compensation for a jumbo purchase, or an investor building a rental portfolio, working with Keith Akada at Mortgage Reel provides the education, transparency, and proven execution you need to make confident decisions backed by 25+ years of experience and 750+ five-star reviews across multiple platforms.