Navigating mortgage loan offers can feel overwhelming, especially in competitive markets like Seattle, Bellevue, and Redmond where timing and terms make all the difference. Whether you're a first-time buyer in Shoreline or a tech professional leveraging stock compensation for a jumbo home loan, understanding how to evaluate and compare offers is essential to securing the best financing for your situation. With interest rates fluctuating and lender requirements varying widely in 2026, knowing what to look for in mortgage loan offers can save you thousands of dollars over the life of your loan and position you competitively in fast-moving neighborhoods across the Greater Seattle area.

Understanding the Components of Mortgage Loan Offers

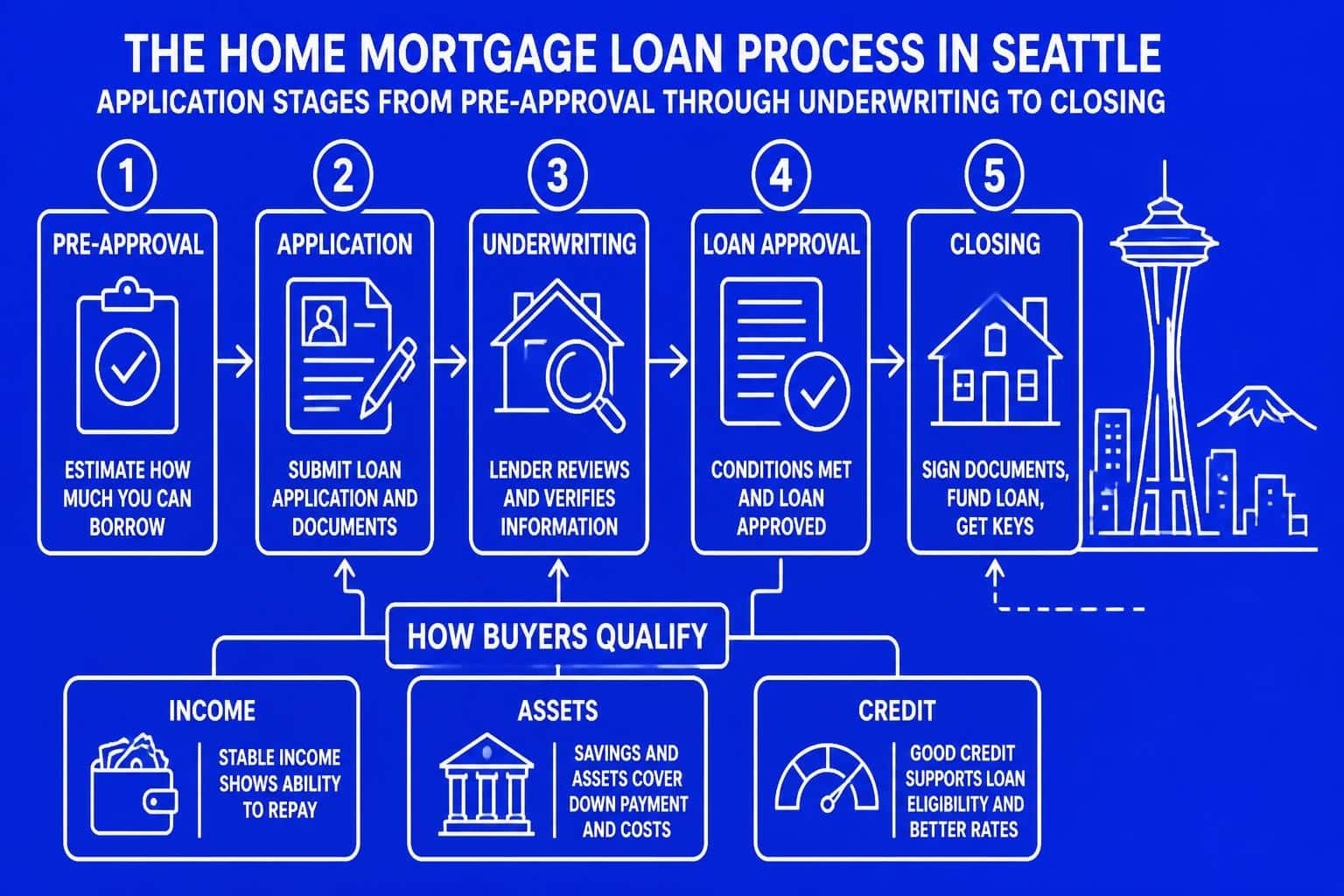

When you receive mortgage loan offers from multiple lenders, each document contains critical information that affects your monthly payment, upfront costs, and long-term financial commitment. The standardized Loan Estimate form, required within three business days of application, provides a structured way to compare loan offers across lenders.

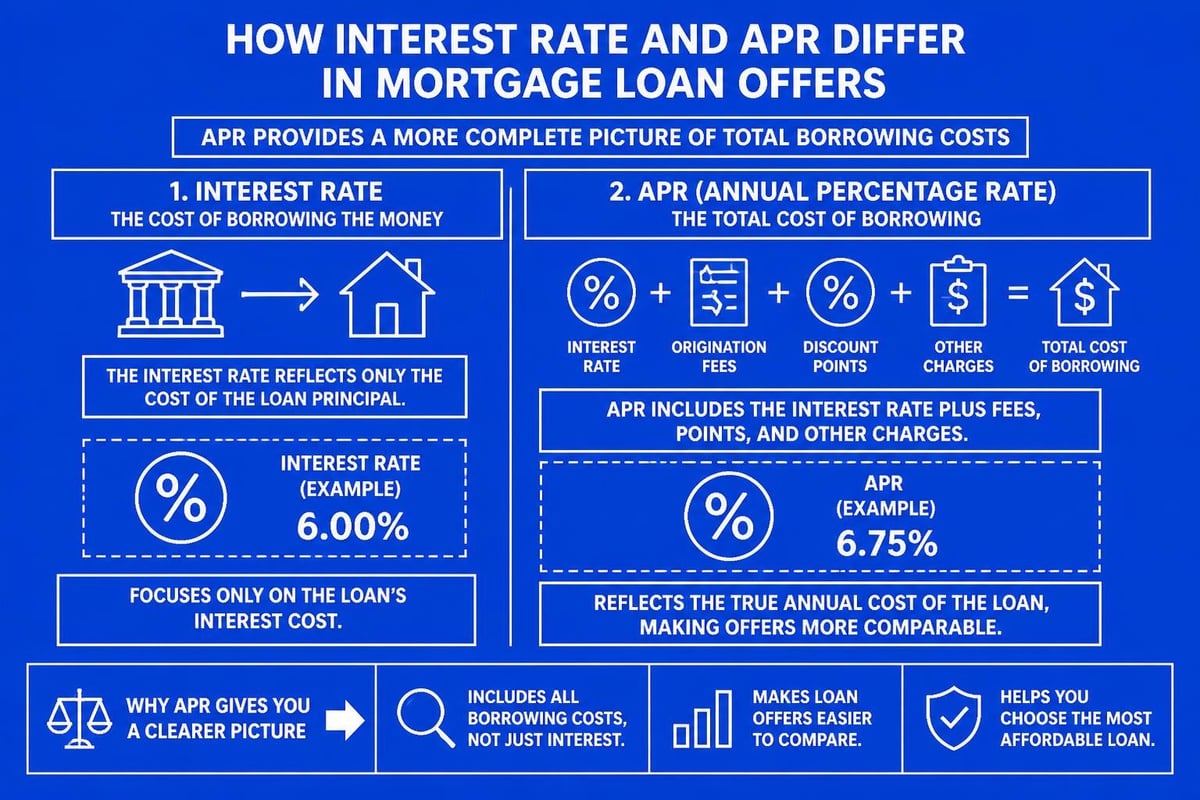

Interest Rate vs. Annual Percentage Rate

The interest rate represents the cost of borrowing the principal amount, while the Annual Percentage Rate (APR) includes the interest rate plus other costs like origination fees, discount points, and mortgage insurance. A lower interest rate doesn't always mean a better deal.

For example, a lender might offer 6.25% with zero points but charge higher closing costs, while another offers 6.00% with one point paid upfront. Seattle-area buyers, particularly those purchasing in high-cost areas like Kirkland or Bellevue, should calculate which scenario saves more money based on how long they plan to keep the loan.

Loan Terms and Structure

Mortgage loan offers vary significantly in structure, and selecting the right term aligns with your financial goals and timeline:

- 30-year fixed mortgages provide stable payments and lower monthly obligations, ideal for buyers planning long-term homeownership in neighborhoods like Lake Forest Park or Mill Creek

- 15-year fixed mortgages build equity faster with higher monthly payments but substantially lower total interest costs

- Adjustable-rate mortgages (ARMs) start with lower initial rates, potentially beneficial for tech professionals who anticipate job relocations or income increases

- Jumbo loans for properties exceeding conforming loan limits require specialized underwriting, particularly important in Seattle's competitive housing market

The type of mortgage loan you choose should reflect both your current financial capacity and future plans, especially in dynamic markets where career progression and household changes are common.

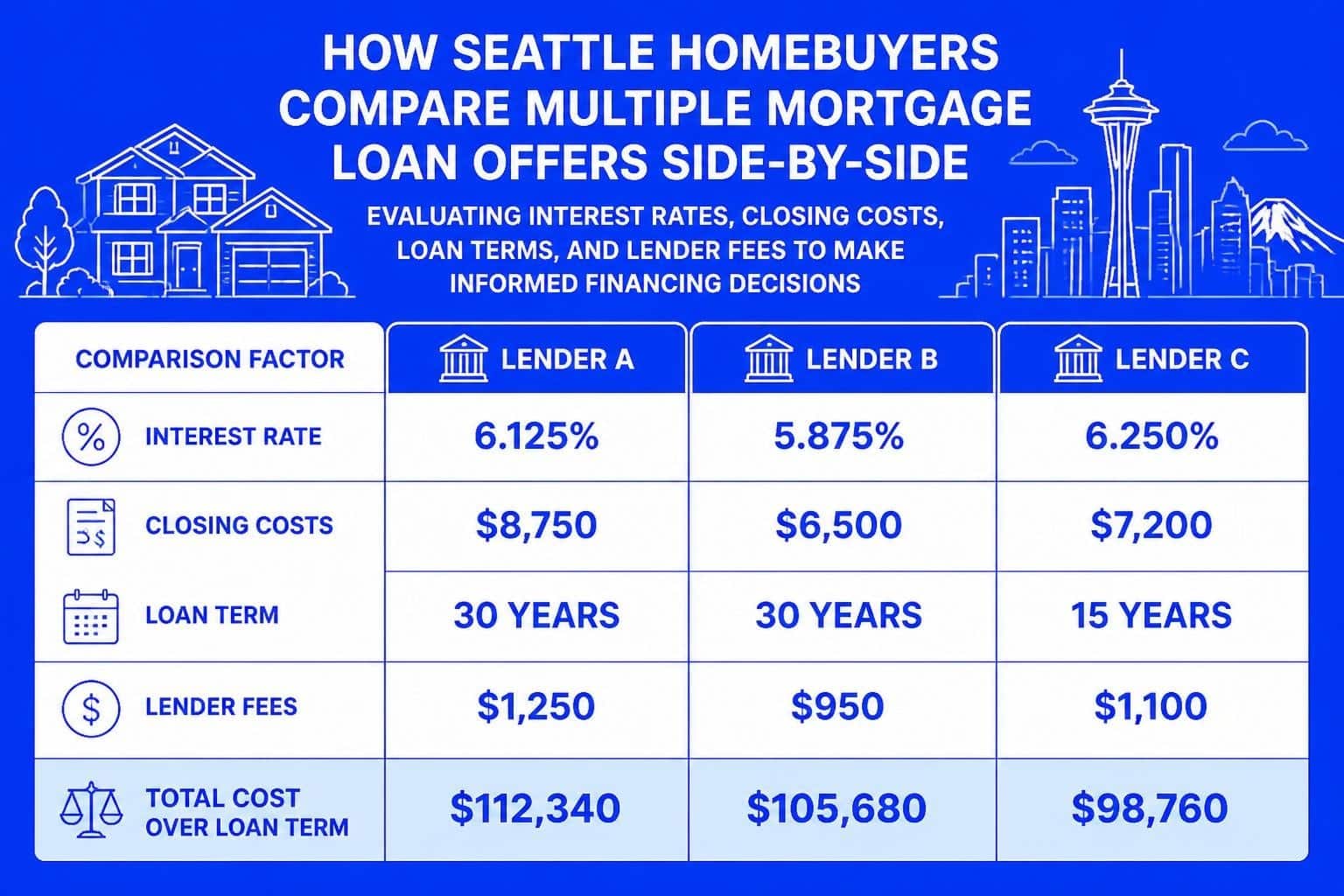

How to Request and Compare Multiple Mortgage Loan Offers

Smart borrowers request mortgage loan offers from at least three to five lenders to ensure they're getting competitive terms. This approach is particularly valuable in the Seattle metro area, where lending capacity and program availability can vary substantially between institutions.

The Application Timeline

When you formally apply for a mortgage, lenders pull your credit and provide a Loan Estimate within three business days. Submitting multiple applications within a 14-45 day window typically counts as a single credit inquiry, minimizing impact on your credit score.

Working with a Seattle mortgage broker like Keith Akada at Mortgage Reel offers a streamlined alternative. Rather than applying separately with multiple lenders, an experienced broker accesses numerous lending partners simultaneously, comparing mortgage loan offers efficiently while managing the documentation process.

| Comparison Factor | Direct Lender | Mortgage Broker |

|---|---|---|

| Number of offers | 1 per application | Multiple from one application |

| Time investment | High (separate apps) | Low (single process) |

| Rate shopping | Manual comparison | Broker compares for you |

| Complex income (RSUs, stock) | Varies by lender expertise | Specialized knowledge |

| Closing speed | Standard timeline | Can be as fast as 9 days |

Reading the Loan Estimate Form

The Loan Estimate breaks down into three pages covering loan terms, projected payments, and closing costs. Pay particular attention to Section A (origination charges), Section B (services you cannot shop for), and Section C (services you can shop for).

For buyers in Everett, Lynnwood, or other submarkets with varying property tax rates, the projected payment section reveals how insurance and taxes affect your monthly obligation beyond principal and interest. This total housing payment determines your debt-to-income ratio and ultimate affordability.

Evaluating Costs in Mortgage Loan Offers

Understanding the cost structure of mortgage loan offers prevents surprises at closing and helps identify the most economical option for your circumstances.

Upfront Costs and Closing Fees

Closing costs typically range from 2% to 5% of the purchase price, though this varies based on loan type, property location, and lender pricing. Common components include:

- Origination fees (lender charges for processing)

- Appraisal fees ($500-$800 in Seattle-area markets)

- Title insurance and escrow fees

- Recording fees and transfer taxes (particularly significant in King County)

- Prepaid items (property taxes, homeowner's insurance, mortgage insurance)

Some mortgage loan offers advertise "no closing costs," but these programs typically incorporate fees into a higher interest rate. Calculate the break-even point to determine if this trade-off makes financial sense for your timeline.

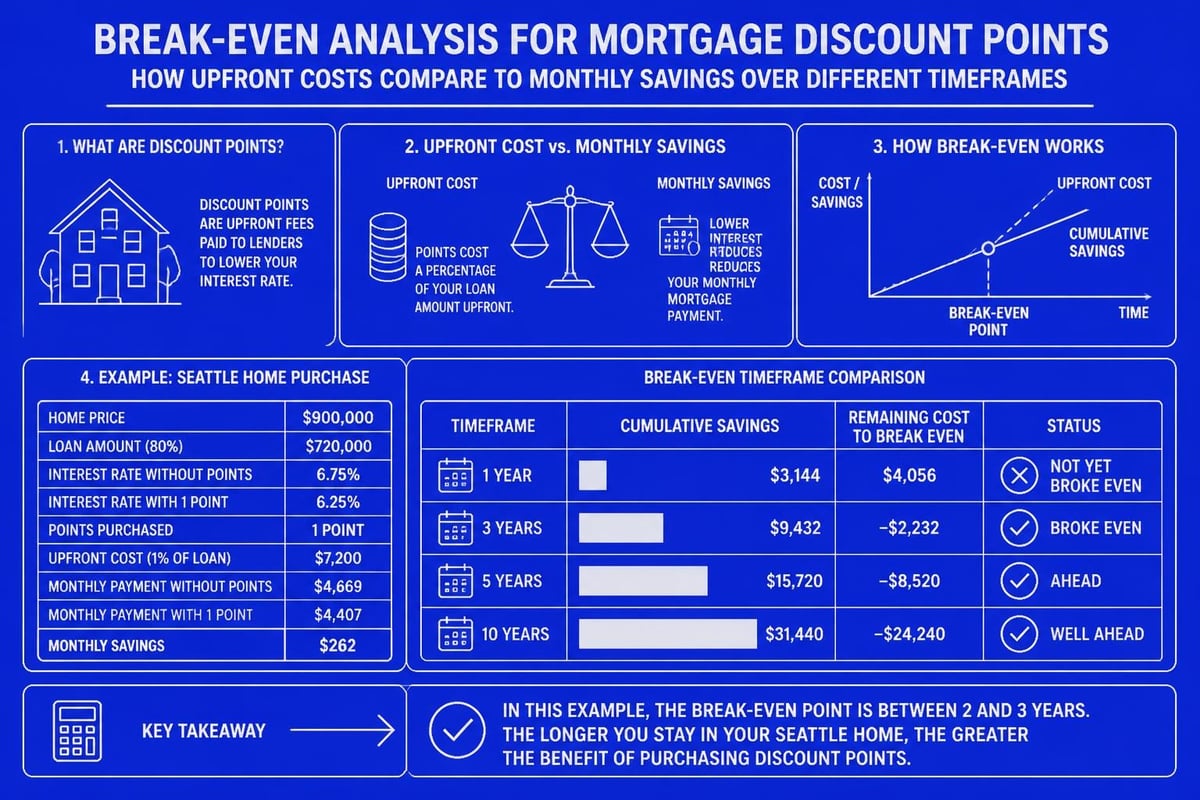

Discount Points and Rate Buydowns

Paying discount points upfront reduces your interest rate, typically by 0.25% per point (1% of the loan amount). For a $750,000 jumbo mortgage common in Seattle's tech-heavy neighborhoods, one point costs $7,500.

Is buying points worthwhile? Divide the upfront cost by your monthly savings to find the break-even period. If you plan to stay in the home beyond that timeframe, points can generate substantial savings. Tech professionals with stock compensation often leverage RSU income specifically for this purpose, reducing their rate and monthly obligation.

Qualifying Complex Income for Better Mortgage Loan Offers

Seattle-area buyers working at Amazon, Microsoft, Google, and other tech employers often receive significant compensation through equity and bonuses. How lenders qualify this income dramatically affects the mortgage loan offers you receive.

Stock-Based Compensation

Restricted Stock Units (RSUs), stock options, and equity grants can boost your purchasing power when properly documented and underwritten. Experienced lenders calculate qualifying income using:

- Two-year average for RSU vesting history

- Current vesting schedule with documented continuity

- Tax-adjusted amounts reflecting actual net income

- Employer verification through offer letters and vesting statements

Not all lenders handle complex compensation equally. Working with specialists who regularly serve tech professionals ensures your full income potential is captured in mortgage loan offers, often increasing your budget by tens of thousands of dollars.

Bonus and Commission Income

Annual bonuses, signing bonuses, and performance incentives require two years of history for most conventional loans, though exceptions exist for well-documented employment transitions. FHA home loans and conventional financing treat this income differently, affecting your qualification and the mortgage loan offers you receive.

For buyers relocating to Seattle or recently promoted into higher compensation tiers, providing detailed employment verification and demonstrating income continuity strengthens your application across multiple lender scenarios.

Comparing Lender Reputation and Service Quality

Beyond numbers, the quality of your lending experience matters significantly in competitive markets where timing can determine whether you win a bidding war.

Closing Speed and Reliability

When you're competing for homes in Redmond or downtown Seattle, sellers favor buyers with strong pre-approvals and fast closing capabilities. Some lenders consistently close in 30-45 days, while others with streamlined underwriting can close in as few as 9 business days.

This difference often determines whose offer gets accepted in multiple-bid situations. The mortgage loan offers with the lowest rate become irrelevant if the lender can't perform within the purchase agreement timeline.

Communication and Transparency

Consider these factors when evaluating lenders:

- Responsiveness to questions and document requests

- Clear explanations of complex guidelines

- Proactive updates throughout the process

- Problem-solving ability when issues arise

- Post-closing support for questions about payments or refinancing

Keith Akada's 750+ five-star reviews across multiple platforms reflect consistent execution in these service dimensions, particularly valued by first-time buyers navigating unfamiliar processes.

Negotiating and Optimizing Your Mortgage Loan Offers

Even after receiving initial mortgage loan offers, opportunities exist to improve your terms through strategic negotiation and informed decision-making.

Rate Matching and Lender Credits

If you receive a better rate from one lender, others may match or beat it to earn your business. This works best when comparing similar loan products (conventional to conventional, jumbo to jumbo) with comparable fees and structures.

Lenders can also offer credits toward closing costs in exchange for accepting a slightly higher interest rate. The Consumer Financial Protection Bureau provides guidance on how to effectively compare and negotiate these components.

Timing Your Rate Lock

Interest rates fluctuate daily based on economic data, Federal Reserve policy, and bond market activity. When you receive mortgage loan offers, the rate is typically guaranteed for 30-60 days through a rate lock.

Strategic considerations for Seattle-area buyers include:

- Lock immediately if rates are rising or you're close to closing

- Float longer if rates trend downward and you have time

- Consider lock extensions if closing delays occur (typically 0.125%-0.25% per 15 days)

- Monitor market conditions through reliable sources like Bankrate

Tech professionals with flexibility in closing dates can sometimes time rate locks more advantagiously, though this requires coordination with sellers and real estate agents.

Special Considerations for Seattle-Area Homebuyers

Local market dynamics create unique scenarios when evaluating mortgage loan offers in the Greater Seattle region.

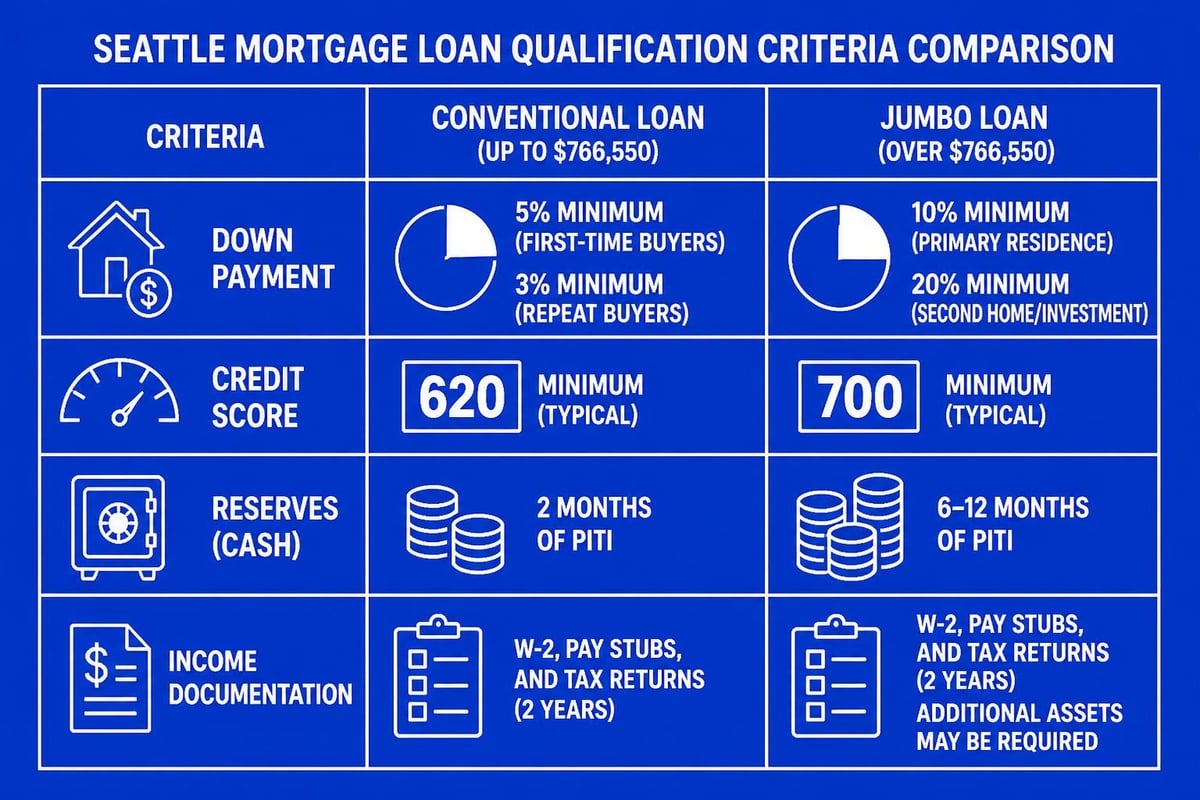

Jumbo Loan Requirements

Properties exceeding $806,500 in 2026 require jumbo financing, common throughout Seattle, Bellevue, Kirkland, and other high-cost neighborhoods. Jumbo mortgage loan offers typically feature:

| Requirement | Conventional | Jumbo |

|---|---|---|

| Minimum down payment | 3%-5% | 10%-20% |

| Credit score | 620+ | 700+ |

| Debt-to-income ratio | Up to 50% | Typically 43% |

| Reserves required | 2-6 months | 6-12 months |

| Documentation | Standard | Enhanced |

Understanding these requirements helps you prepare for jumbo financing before requesting mortgage loan offers, ensuring you receive realistic quotes aligned with underwriting standards.

Condominium Financing Considerations

Seattle's urban neighborhoods feature numerous condominium buildings with varying levels of lender approval. Some buildings qualify for conventional financing with minimal documentation, while others face restrictions based on:

- Owner-occupancy ratios (typically 51% minimum)

- HOA financial health and reserve funding

- Pending litigation against the association

- FHA or VA certification status

When comparing mortgage loan offers for condos in Capitol Hill, Belltown, or South Lake Union, verify that your chosen lender has experience with your specific building and can navigate any approval complexities.

Red Flags to Watch for in Mortgage Loan Offers

Protecting yourself from problematic lending practices ensures you secure legitimate, fair financing for your Seattle-area home purchase.

Unrealistic Rate Advertising

The Federal Trade Commission warns against deceptive mortgage advertisements that promise rates significantly below market averages. If mortgage loan offers seem too good to be true, investigate:

- Hidden fees not disclosed in initial quotes

- Teaser rates that adjust quickly after closing

- Qualification requirements that don't match your profile

- Bait-and-switch tactics where promised rates aren't honored

Legitimate lenders provide transparent Loan Estimates that match their initial quotes, with any changes clearly explained and justified by specific circumstances.

Pressure Tactics and Application Fees

Reputable mortgage professionals never pressure you to make rushed decisions or pay large upfront fees before providing formal mortgage loan offers. Standard practice includes:

- Free initial consultations and rate quotes

- Reasonable time to review Loan Estimates

- Clear explanations of all fees and charges

- No-obligation applications for comparison purposes

Working with established, well-reviewed lenders like those partnered through Mortgage Reel provides consumer protections and professional standards that prevent predatory practices.

Leveraging Professional Guidance for Mortgage Loan Offers

The complexity of mortgage financing in 2026, combined with Seattle's competitive housing market, makes professional guidance increasingly valuable for buyers at all experience levels.

Benefits of Mortgage Broker Relationships

Rather than navigating multiple lender websites and applications independently, mortgage brokers streamline the comparison process while adding expertise in areas like complex income qualification, program selection, and guideline interpretation.

Keith Akada's 25+ years of experience serving Seattle-area buyers provides specific advantages:

- Access to multiple lending partners from a single application

- Specialized knowledge of tech compensation and jumbo financing

- Established relationships that facilitate smooth underwriting

- Local market expertise across Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett

- Fast closing capability competitive in multiple-offer scenarios

Educational Approach to Mortgage Decisions

The best mortgage professionals prioritize education over sales, ensuring you understand not just which offer to choose but why it's the right fit for your financial situation. This approach builds confidence in your decision and prevents buyer's remorse.

For first-time homebuyers, comprehensive education about mortgage loan offers, including how different programs work and what to expect at each stage, reduces anxiety and empowers informed decision-making throughout the purchase process.

Strategic Timing for Requesting Mortgage Loan Offers

When you request quotes affects both the rates you receive and your negotiating position with sellers.

Pre-Approval vs. Pre-Qualification

Understanding this distinction strengthens your position when submitting offers on Seattle-area properties:

- Pre-qualification provides an estimate based on self-reported information without verification

- Pre-approval involves full application, credit check, income documentation, and conditional underwriting approval

Sellers and their agents recognize the difference. In competitive neighborhoods where multiple offers are common, a thorough pre-approval backed by a reputable lender carries significantly more weight than a basic pre-qualification letter.

Market Timing Considerations

While predicting interest rate movements is challenging, certain patterns and economic indicators influence when mortgage loan offers might be more favorable:

- Economic data releases (employment reports, inflation data) affect bond markets and mortgage rates

- Federal Reserve meetings and policy announcements create rate volatility

- Seasonal patterns with slightly lower rates in winter months historically

- Market disruptions creating temporary opportunities

Following mortgage rate trends specific to the Seattle market helps you identify favorable timing for both rate locks and purchase offers.

How Different Loan Programs Affect Your Offers

The type of financing you pursue fundamentally shapes the mortgage loan offers you receive and their suitability for your situation.

Conventional Loans

Offering flexibility in down payment (as low as 3% for qualified buyers), competitive rates for strong credit profiles, and the ability to cancel mortgage insurance once you reach 20% equity, conventional loans dominate Seattle's housing market for purchases above FHA limits.

Benefits include:

- No upfront mortgage insurance premium

- Lower rates for excellent credit (740+)

- Higher loan limits supporting purchases up to conforming limits

- Streamlined refinancing options for rate improvement

FHA Financing

Federal Housing Administration loans feature lower down payments (3.5%) and more flexible credit requirements, making them accessible for buyers with limited savings or credit challenges. However, mortgage loan offers for FHA include:

- Upfront mortgage insurance premium of 1.75% of the loan amount

- Ongoing monthly mortgage insurance for the life of the loan (if down payment is less than 10%)

- Property condition requirements that may limit eligible homes

Understanding FHA down payment requirements helps you evaluate whether this program provides the best path to homeownership in your target neighborhoods.

VA and Other Special Programs

Veterans, active military, and eligible surviving spouses access VA loans with zero down payment, no mortgage insurance, and competitive rates. These mortgage loan offers often represent the most favorable terms available, though property eligibility and funding fee considerations apply.

Washington State also offers programs through the Washington State Housing Finance Commission for first-time buyers and those purchasing in targeted areas, potentially including down payment assistance that improves your overall financing package.

Comparing mortgage loan offers effectively requires understanding rate structures, cost components, lender reliability, and program differences that affect both immediate affordability and long-term value. For Seattle-area homebuyers navigating high-cost markets while balancing complex income sources and competitive timelines, partnering with an experienced professional streamlines this process significantly. Keith Akada and the team at Mortgage Reel bring specialized expertise in tech compensation, jumbo financing, and rapid closings, backed by 25+ years of experience and 750+ five-star reviews from clients throughout Seattle, Bellevue, Redmond, Kirkland, Shoreline, and surrounding communities. Whether you're purchasing your first home or your fifth investment property, having a trusted advisor who prioritizes education and transparency ensures you secure the best possible financing for your unique situation.