When you're navigating the mortgage process in Seattle's competitive housing market, understanding how to evaluate mortgage loan reviews becomes essential to your success. With hundreds of lenders competing for your business and review platforms offering conflicting information, knowing what to look for can save you thousands of dollars and prevent costly delays. Whether you're a tech professional at Amazon qualifying RSUs for a jumbo loan or a first-time buyer exploring conventional financing options, the right lender choice starts with knowing how to interpret reviews intelligently.

Why Mortgage Loan Reviews Matter More Than Ever

The mortgage industry has transformed dramatically over the past decade, with borrowers now having access to unprecedented information about lender performance. Mortgage loan reviews provide insights that go far beyond interest rates and closing costs, revealing how lenders perform under pressure, communicate with clients, and handle unexpected challenges.

Seattle's unique market dynamics make reviews especially valuable. In neighborhoods from Capitol Hill to Bellevue, multiple-offer scenarios demand lenders who can close quickly and communicate proactively with listing agents. Reviews often highlight which lenders consistently meet tight deadlines and which create unnecessary friction in competitive situations.

The Real Value Behind Five-Star Ratings

Not all five-star reviews carry equal weight. A mortgage loan review becomes meaningful when it addresses specific performance metrics rather than general satisfaction. Look for feedback that discusses:

- Communication frequency and clarity throughout the loan process

- Accuracy of initial estimates compared to final closing costs

- Problem-solving ability when documentation or appraisal issues arise

- Timeline adherence from application to closing

- Post-closing support for questions about escrow or payments

For Seattle homebuyers, particularly those working with complex income structures like stock compensation, reviews that mention successful closings involving RSUs, bonuses, or self-employment income provide valuable validation of a lender's expertise.

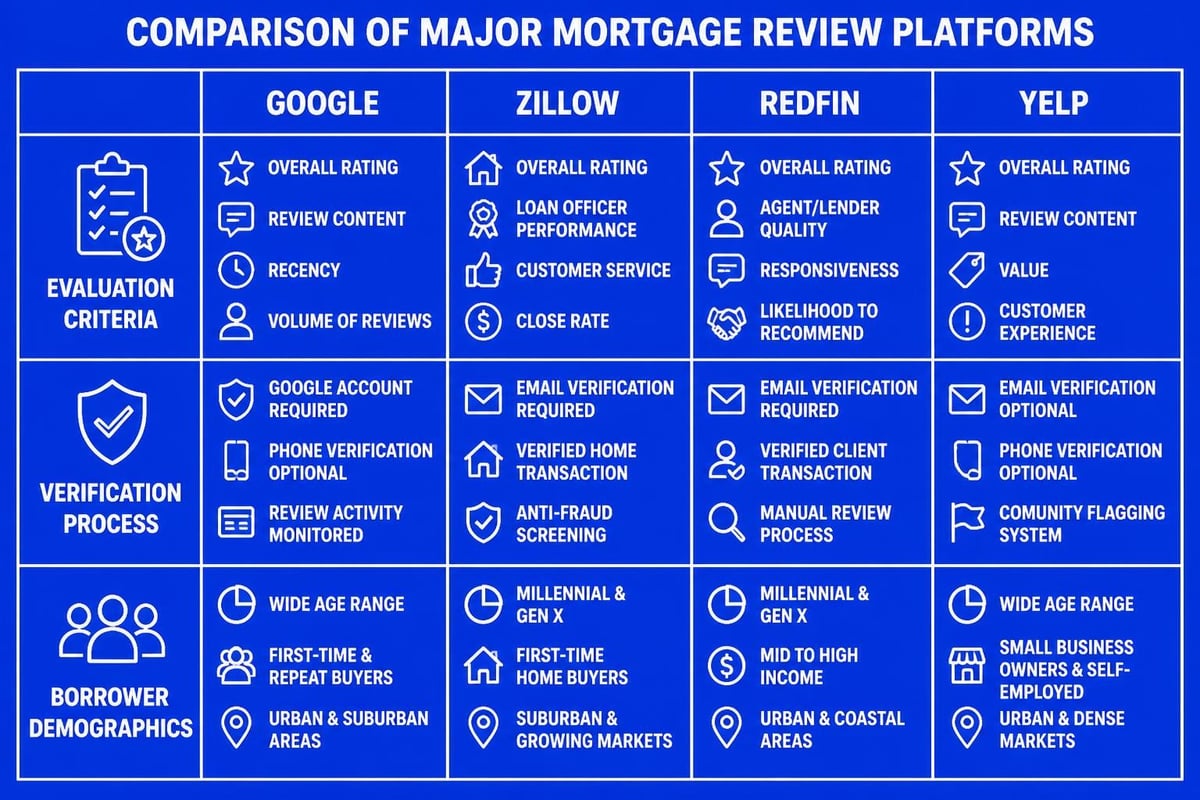

Where to Find Reliable Mortgage Loan Reviews

Multiple platforms host mortgage loan reviews, each with distinct strengths and limitations. NerdWallet provides comprehensive reviews of various mortgage lenders, evaluating factors such as interest rates, fees, and customer service to aid consumer decisions. Similarly, The Motley Fool offers detailed assessments of mortgage lender offerings and services.

| Platform | Verification Method | Best For | Potential Limitations |

|---|---|---|---|

| Google Reviews | Email verification | Overall reputation, local presence | Limited mortgage-specific detail |

| Zillow | Transaction-based | Home purchase scenarios | Skewed toward buyer agents' experiences |

| Redfin | Partner network | Agent-lender coordination | Smaller review volume |

| Yelp | Account-based | Detailed narratives | Self-selection bias |

| WalletHub | Multi-source aggregation | Comparative analysis | Complex navigation |

When evaluating great mortgage brokers in the Seattle area, cross-reference reviews across multiple platforms. A loan officer with 750+ verified five-star reviews across Google, Zillow, Redfin, Yelp, and WalletHub demonstrates consistent excellence rather than platform-specific manipulation.

How to Read Mortgage Loan Reviews Strategically

Reading reviews effectively requires looking beyond star ratings to understand the context and substance of borrower experiences. Professional mortgage loan reviews from established platforms like Bankrate outline specific methodology for evaluating lenders, providing frameworks you can apply to individual reviews.

Identifying Authentic Borrower Experiences

Genuine mortgage loan reviews typically include specific details that generic or fabricated reviews lack. Watch for mentions of:

- Actual loan officers or team members by name

- Specific challenges encountered (appraisal gaps, employment verification, condo approval)

- Timeline specifics (application date, closing date, unexpected delays)

- Comparison points to other lenders the borrower considered

- Outcome details beyond just "great experience"

In Seattle's market, where tech employees frequently deal with jumbo home loans, reviews that discuss successful qualification of complex income sources carry particular weight. A review stating "They qualified my Amazon RSUs and closed in 12 days" provides more actionable information than "Great service, highly recommend."

Red Flags in Mortgage Loan Reviews

Certain patterns in mortgage loan reviews should prompt additional investigation rather than automatic disqualification. Every lender encounters challenging situations, but consistent themes reveal systemic issues:

- Rate-switching complaints where advertised rates differ significantly from final offers

- Closing delays attributed to internal processing rather than external factors

- Communication breakdowns where borrowers couldn't reach their loan officer

- Surprise fees not disclosed in initial loan estimates

- Post-closing errors in escrow accounts or payment processing

One or two negative reviews among hundreds may reflect individual circumstances rather than lender performance. However, recurring themes across multiple reviews, especially recent ones, warrant serious consideration.

What Seattle-Area Borrowers Should Prioritize

Seattle's housing market presents unique challenges that make certain lender capabilities more critical than in other regions. When evaluating mortgage loan reviews, local borrowers should weight specific competencies differently than national averages suggest.

Speed and Certainty in Competitive Markets

In neighborhoods throughout Seattle, Bellevue, Redmond, and Kirkland, multiple-offer situations remain common despite market fluctuations. Reviews highlighting fast closes become especially relevant. The ability to close in as few as 9 business days creates significant competitive advantages when sellers compare similar offers.

Look for mortgage loan reviews that specifically mention:

- Pre-approval strength and seller agent confidence

- Waived contingency support and risk management

- Clear communication with listing agents

- Consistent timeline delivery in competitive scenarios

- Successful navigation of condominium approval processes

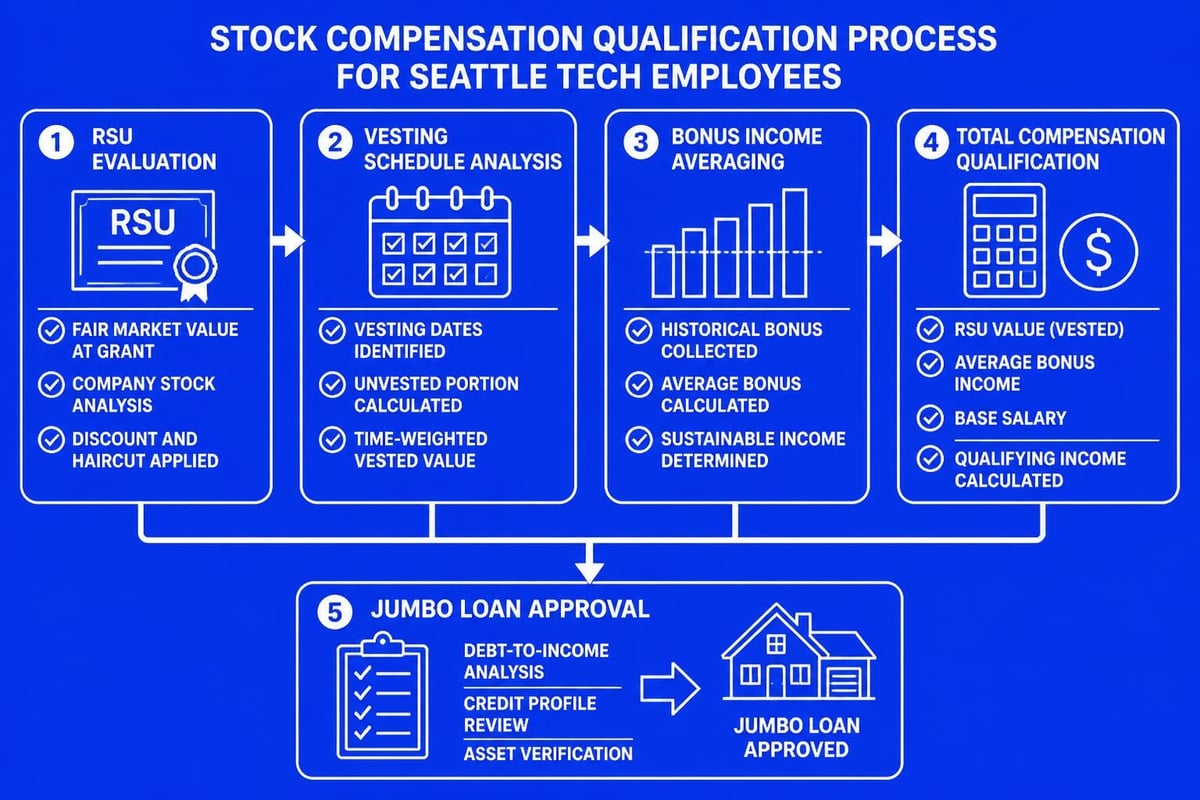

Tech Income Qualification Expertise

For professionals at Amazon, Microsoft, Google, and other Seattle-area tech employers, stock compensation creates unique qualification challenges. Mortgage loan reviews from borrowers with similar income structures provide invaluable insights into lender expertise.

Key qualification scenarios to look for in reviews:

- RSU vesting schedule evaluation and income calculation

- Stock option treatment in debt-to-income ratios

- Bonus income documentation and averaging methods

- Dual-income households with multiple compensation types

- International income for H-1B visa holders

Reviews mentioning successful jumbo home mortgage approvals with complex compensation demonstrate specialized underwriting capability that generic lenders often lack.

Beyond Star Ratings: Understanding Review Context

The numerical rating tells only part of the story in mortgage loan reviews. Context determines whether a particular review applies to your situation and whether the lender's strengths align with your priorities.

Matching Review Context to Your Scenario

A five-star review from a cash-out refinance customer provides limited insight if you're pursuing a first-time mortgage loan. Similarly, conventional loan reviews may not reflect a lender's VA or FHA expertise. Prioritize reviews that mirror your:

- Transaction type (purchase vs. refinance)

- Property category (single-family, condo, multi-unit)

- Loan program (conventional, FHA, VA, jumbo)

- Financial profile (W-2, self-employed, complex income)

- Timeline constraints (quick close, coordinated sale)

Seattle-area borrowers considering properties in specific neighborhoods should particularly value reviews mentioning those locations. Local expertise in areas like Capitol Hill, Shoreline, or Lake Forest Park often translates to smoother transactions through familiarity with local appraisal markets and title companies.

Evaluating Response to Negative Reviews

How lenders respond to critical mortgage loan reviews often reveals more about their character than glowing testimonials. Professional responses demonstrate:

- Accountability for mistakes without defensive justifications

- Specific remediation explaining how they addressed the issue

- Process improvements implemented to prevent recurrence

- Empathy for the borrower's frustration and experience

- Contact information offering offline resolution

Birdeye discusses various platforms where mortgage lender reviews appear and their significance in borrower decision-making. A lender who engages constructively with criticism typically maintains that same professionalism when challenges arise during your transaction.

Volume and Recency in Review Evaluation

The quantity and timing of mortgage loan reviews provide important context for assessing reliability and current performance. A loan officer with 750+ verified reviews across multiple platforms over many years demonstrates sustained excellence rather than a temporary promotional campaign.

Why Review Volume Matters

High review volumes create statistical significance that individual testimonials cannot provide. Consider these benchmarks:

| Review Count | Reliability Level | What It Indicates |

|---|---|---|

| Under 20 | Limited data | New to market or low volume |

| 20-100 | Moderate confidence | Established but smaller operation |

| 100-300 | Strong track record | Consistent client satisfaction |

| 300-500 | Exceptional performance | High volume with quality maintenance |

| 500+ | Market leader | Sustained excellence over years |

For borrowers seeking conventional loan lenders in Seattle, loan officers with hundreds of reviews provide more predictable experiences than those with limited feedback, regardless of average rating.

The Recency Factor

Recent mortgage loan reviews reflect current market conditions, staffing, and operational capabilities. The mortgage industry evolved significantly during 2025 and into 2026, with rate volatility, underwriting guideline changes, and technology integration affecting lender performance.

Prioritize reviews from the past 12-18 months when evaluating current lender capabilities. A lender who excelled three years ago may have experienced staff turnover, policy changes, or capacity constraints that alter their current performance profile.

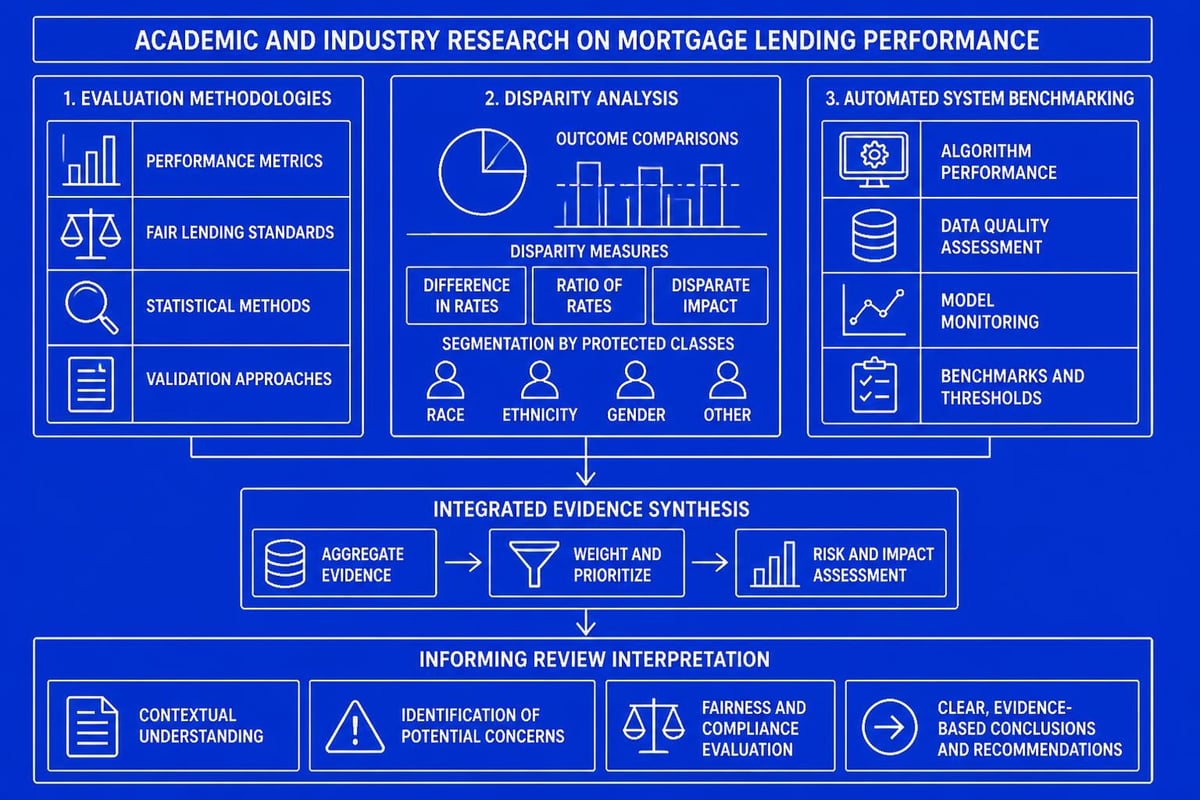

How Industry Research Informs Review Interpretation

Academic and industry research provides frameworks for understanding what mortgage loan reviews reveal about lender performance. Research on mortgage loan origination agents introduces benchmarks for evaluating automated systems in loan processing, highlighting the importance of efficiency metrics borrowers should look for in reviews.

Additionally, studies examining disparities in mortgage lending offer valuable context for understanding fair lending practices. When evaluating mortgage loan reviews, notice whether diverse borrowers report consistent treatment and whether lenders demonstrate inclusive practices across different communities throughout Seattle, Lynnwood, Mill Creek, Shoreline, Everett, and Lake Forest Park.

Translating Research to Practical Review Evaluation

Professional research emphasizes several factors that correlate with positive borrower outcomes:

- Initial disclosure accuracy predicting final costs within 1-2%

- Communication cadence with regular updates at key milestones

- Documentation efficiency through technology rather than repeated requests

- Problem anticipation identifying potential issues before they cause delays

- Cross-functional coordination between processors, underwriters, and closers

Mortgage loan reviews that touch on these operational elements provide deeper insights than those focusing solely on personality or general satisfaction.

Making Your Final Lender Decision

After researching mortgage loan reviews across multiple platforms, synthesize your findings into an actionable decision framework. Your ideal lender should demonstrate consistent excellence in areas most critical to your specific situation.

Creating Your Lender Scorecard

Develop a simple scoring system based on your priorities:

Must-Have Capabilities (Deal-breakers):

- Expertise with your loan type and income structure

- Track record of on-time closes in competitive markets

- Strong communication throughout the process

- Transparent pricing with no surprise fees

Nice-to-Have Advantages (Tie-breakers):

- Extended availability for questions

- Digital application and document upload

- Relationship with your real estate agent

- Post-closing support and resources

Reviews addressing your must-have capabilities deserve greater weight than those focused on nice-to-have features. A Seattle mortgage broker specializing in your property type and financial profile will typically outperform a generalist, even if the generalist has marginally higher overall ratings.

Questions to Ask During Initial Consultations

Use insights from mortgage loan reviews to formulate intelligent questions during lender interviews:

- "I noticed reviews mentioning [specific issue]. How do you handle that situation?"

- "What percentage of your loans close on the original target date?"

- "How do you communicate with borrowers and agents during the process?"

- "Can you share examples of successfully qualifying [your income type]?"

- "What's your process if unexpected issues arise before closing?"

Loan officers who provide specific, detailed answers rather than generic reassurances demonstrate the competence and transparency that positive mortgage loan reviews consistently highlight.

The Local Advantage in Seattle Markets

While national lenders offer competitive rates, local expertise provides advantages that mortgage loan reviews from Seattle-area borrowers consistently emphasize. Understanding neighborhood-specific dynamics, maintaining relationships with local appraisers and title companies, and knowing which underwriters understand regional property types creates smoother transactions.

Reviews mentioning seamless coordination with Seattle real estate professionals or quick resolution of condo approval complexities highlight the value of choosing a local lender. These operational advantages often outweigh marginal rate differences, particularly in competitive multiple-offer scenarios where certainty and speed determine success.

Regional Market Knowledge in Action

Mortgage loan reviews that describe neighborhood-specific expertise provide particular value. A lender familiar with Shoreline School District properties, Lake Forest Park community requirements, or Capitol Hill condominium associations navigates potential complications before they become deal-threatening issues.

For buyers exploring various Seattle neighborhoods, reviews from borrowers who purchased in similar areas offer the most relevant performance indicators. This local knowledge extends to understanding employer verification processes at major tech companies, qualifying rental income from Seattle investment properties, or navigating land use restrictions in specific communities.

Understanding how to evaluate mortgage loan reviews strategically empowers you to choose a lender who will execute flawlessly when it matters most. With over 25 years of experience and 750+ five-star reviews across all major platforms, Keith Akada and Mortgage Reel bring proven expertise in complex income qualification, jumbo financing, and competitive-market execution to homebuyers throughout Seattle, Bellevue, Redmond, and Kirkland. Whether you're qualifying stock compensation or navigating a quick close, working with a highly-reviewed local expert ensures your mortgage process matches your expectations.