Navigating the Seattle housing market requires more than just financial preparation-it demands expert guidance from professionals who understand local market dynamics, lending guidelines, and the unique challenges facing today's buyers. Whether you're purchasing your first home in Lake Forest Park, refinancing in Shoreline, or investing in property across Lynnwood, working with experienced mortgage professionals can make the difference between a smooth transaction and a stressful experience. These licensed experts bring market knowledge, product expertise, and strategic thinking to every transaction, helping clients maximize their buying power while avoiding costly mistakes.

What Mortgage Professionals Do for Seattle Homebuyers

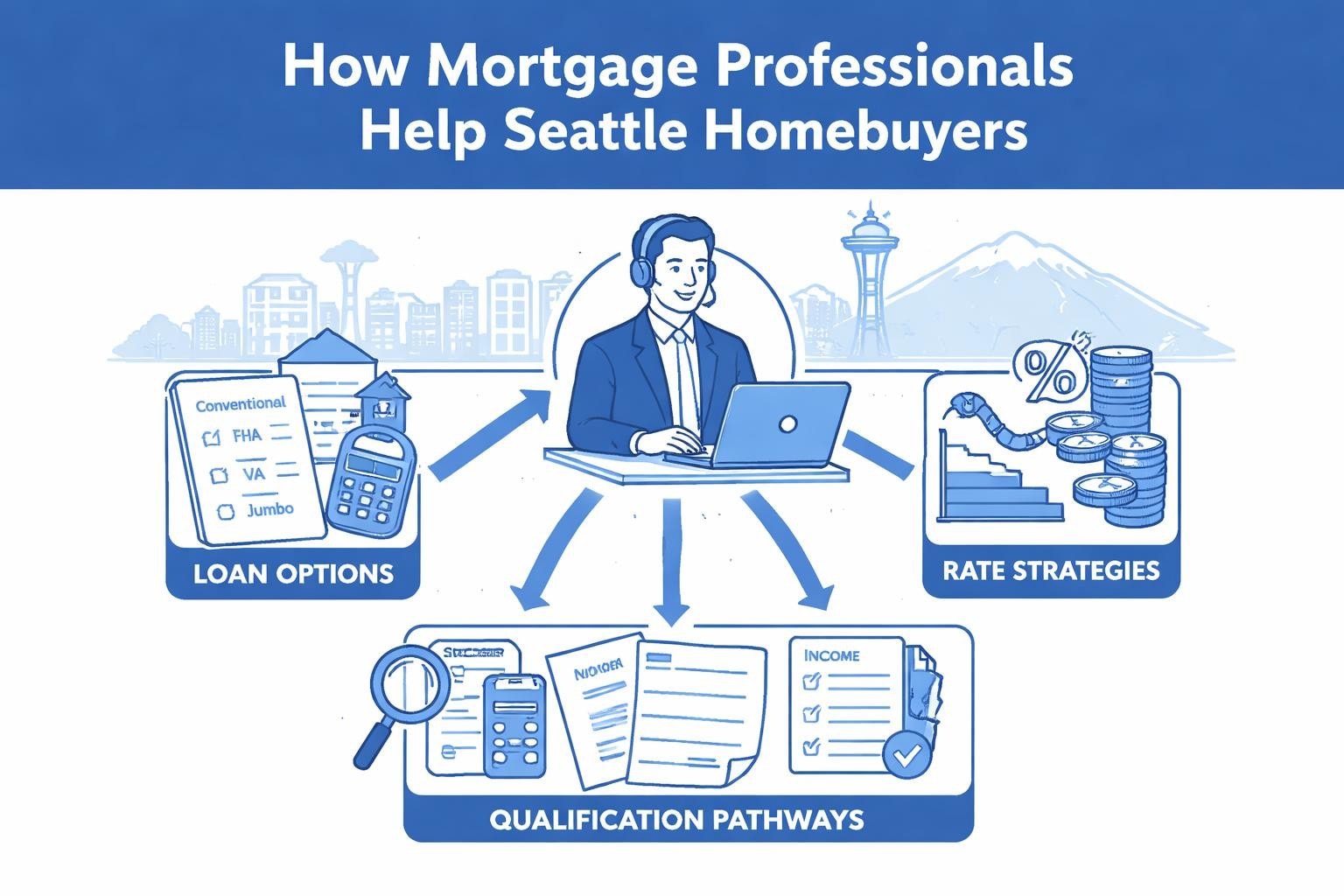

Mortgage professionals serve as the bridge between borrowers and lenders, navigating complex lending guidelines to secure optimal financing solutions. Their role extends far beyond simply processing applications-they analyze financial profiles, recommend appropriate loan products, and advocate for clients throughout the underwriting process.

Core Responsibilities and Services

The daily work of mortgage professionals encompasses several critical functions. They conduct initial financial consultations to assess borrower readiness, calculate debt-to-income ratios, and evaluate credit profiles. For Seattle-area tech workers, this often includes specialized analysis of stock compensation, RSUs, and bonus income that traditional lenders might overlook.

Key services include:

- Pre-approval preparation and documentation review before house hunting begins

- Loan product comparison across conventional, FHA, VA, jumbo, and specialized programs

- Rate negotiation and pricing strategy based on market conditions

- Credit optimization guidance to improve approval odds and secure better terms

- Closing coordination with escrow, title companies, and real estate agents

These professionals maintain relationships with multiple lending partners, giving them access to diverse product offerings and competitive pricing structures. According to research on consumer behavior in the mortgage process, borrowers who work with mortgage professionals report higher satisfaction and better understanding of their loan terms compared to those who navigate the process independently.

Licensing and Professional Standards

Every legitimate mortgage professional must hold state licensing through the Nationwide Mortgage Licensing System (NMLS). In Washington State, this requires completing pre-licensing education, passing a comprehensive exam, undergoing background checks, and maintaining continuing education credits annually.

Professional organizations like the National Association of Mortgage Brokers set ethical standards and provide ongoing training to ensure mortgage professionals stay current with regulatory changes and industry best practices. These standards protect consumers while elevating the professionalism of the entire industry.

Choosing the Right Mortgage Professional in Seattle

The Seattle market presents unique challenges that require specialized expertise. From competitive bidding situations in Bellevue to investment property purchases in Everett, finding the right professional partner significantly impacts your success.

Experience in Local Markets

Seattle's housing market operates differently than national averages, with faster appreciation, higher price points, and intense competition. Mortgage professionals with deep local experience understand these dynamics and adjust their strategies accordingly.

Consider these differentiating factors:

| Factor | Why It Matters | Questions to Ask |

|---|---|---|

| Local Market Tenure | Understanding of Seattle-specific programs and trends | How long have you worked in the Seattle area? |

| Tech Income Expertise | Critical for Amazon, Microsoft, Google employees | How do you qualify RSU and stock compensation? |

| Jumbo Loan Volume | Essential given Seattle's median home prices | What percentage of your business involves jumbo loans? |

| Review Quality | Reflects client satisfaction and reliability | Can you share recent client testimonials? |

A mortgage professional serving Redmond should understand how stock vesting schedules impact qualifying income and know which lenders offer the most favorable treatment of equity compensation. This specialized knowledge directly affects how much house you can afford.

Communication Style and Availability

Responsive communication separates exceptional mortgage professionals from mediocre ones. In competitive Seattle markets, buyers often face same-day or next-day offer deadlines. Your mortgage professional should respond quickly to questions, provide clear explanations of complex terms, and proactively communicate throughout the process.

Look for professionals who:

- Offer multiple communication channels (phone, email, text, video)

- Provide detailed written summaries after important conversations

- Set realistic expectations about timelines and potential challenges

- Maintain availability during evenings and weekends when needed

The Mortgage Professional America publication regularly highlights the importance of communication quality as the top factor in client satisfaction surveys, even ranking above interest rate savings in many cases.

How Mortgage Professionals Structure Your Loan Strategy

Strategic loan structuring goes beyond finding the lowest rate. Experienced mortgage professionals analyze your complete financial picture, timeline, and goals to recommend optimal financing approaches.

Analyzing Income Sources for Seattle Tech Workers

Seattle's concentration of technology companies creates unique qualifying challenges and opportunities. Mortgage professionals who specialize in this space know how to maximize income calculations for various compensation types.

Base salary provides straightforward qualifying income, but the real complexity emerges with variable compensation:

- Restricted Stock Units (RSUs) can typically be included at 100% of vested value with proper documentation

- Stock options require careful analysis of vesting schedules and tax implications

- Annual bonuses generally need two-year history but can be averaged for qualifying

- Sign-on bonuses may be excluded or partially included depending on structure

A mortgage professional experienced with tech income can often qualify buyers for significantly higher loan amounts than generalists by properly documenting and presenting these income sources to underwriters. This expertise proves especially valuable when pursuing conventional loans for investment property where income requirements increase.

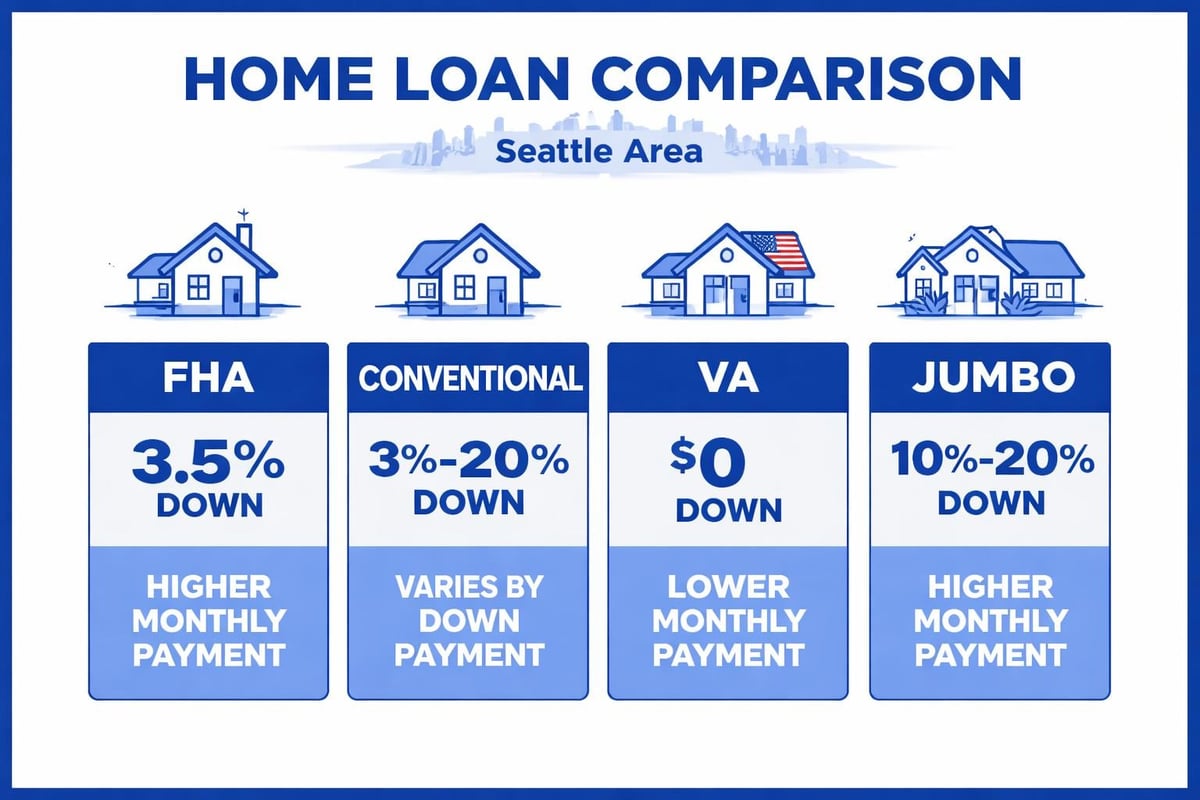

Down Payment Strategy and Program Selection

Down payment requirements vary dramatically across loan programs, and mortgage professionals help clients balance preservation of liquid assets against monthly payment optimization.

Consider these common scenarios in the Seattle market:

- First-time buyers in Mill Creek might benefit from FHA loans with 3.5% down despite slightly higher monthly costs

- Tech professionals in Seattle with substantial RSU income often prefer conventional loans to avoid private mortgage insurance restrictions

- Military veterans in Lynnwood should explore VA loans offering zero-down financing with competitive rates

- Investment buyers typically face 20-25% down payment requirements on rental properties

Understanding the nuances of mortgage 20% down payment requirements helps borrowers plan appropriately. According to Fannie Mae guidelines, conventional loans with 20% down eliminate private mortgage insurance entirely, reducing monthly payments significantly on Seattle's higher-priced homes.

The Mortgage Professional Advantage in Competitive Markets

Seattle's competitive real estate environment requires speed, precision, and strategic positioning. Mortgage professionals provide critical advantages that help buyers win in multiple-offer situations.

Pre-Approval vs. Pre-Qualification

Many buyers misunderstand the distinction between pre-qualification and pre-approval. Mortgage professionals provide genuine pre-approvals involving full credit review, income verification, and preliminary underwriting. This stronger position gives sellers confidence in your ability to close.

Pre-qualification involves:

- Basic financial discussion without documentation review

- Estimated approval based on stated information

- Limited value in competitive offer situations

- Quick turnaround but minimal verification

Pre-approval requires:

- Complete credit report analysis

- Verification of income through pay stubs, tax returns, and employment

- Asset documentation showing down payment and reserves

- Preliminary underwriting approval subject only to property appraisal

In neighborhoods from Shoreline to Everett, sellers receiving multiple offers consistently favor buyers with solid pre-approvals from reputable mortgage professionals over those with simple pre-qualification letters.

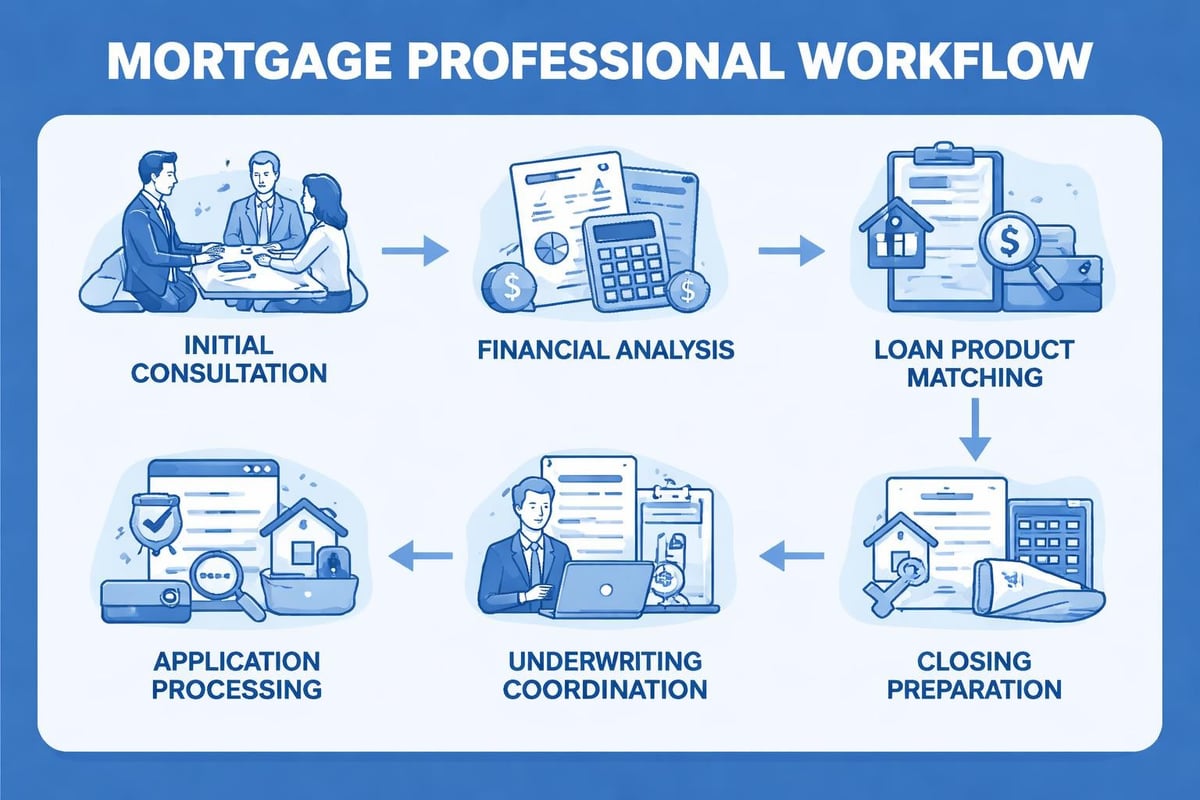

Relationship-Based Processing Speed

Established mortgage professionals maintain strong relationships with underwriters, processors, and closing teams. These relationships translate into faster turnaround times and smoother problem resolution when issues arise.

The processing timeline typically follows this sequence:

- Application submission (Day 1): Complete documentation package submitted

- Initial underwriting review (Days 2-3): Credit, income, and asset verification

- Conditional approval (Days 4-5): Approval issued with outstanding conditions

- Condition clearance (Days 6-8): Final documentation submitted and approved

- Clear to close (Day 9): Final approval and closing preparation

Experienced mortgage professionals can often compress this timeline significantly, with some transactions closing in as few as nine business days when all parties work efficiently.

Technology and Innovation in Mortgage Services

Modern mortgage professionals leverage technology to improve accuracy, speed, and client experience. The industry has transformed dramatically over the past decade, with digital tools replacing manual processes throughout the transaction.

Digital Documentation and Verification

Electronic document collection, e-signatures, and automated verification systems have streamlined what was once a paper-intensive process. Mortgage professionals now use secure portals where clients upload documents, track progress, and receive real-time updates.

Advanced verification services connect directly to:

- Payroll systems for instant employment and income confirmation

- Bank accounts through secure read-only access for asset verification

- IRS databases for tax return validation and income documentation

- Credit bureaus for comprehensive tradeline reporting

These integrations reduce processing time while improving accuracy. The Mortgage Industry Standards Maintenance Organization continues developing data standards that enable these seamless exchanges between systems.

Rate Monitoring and Lock Strategy

Interest rates fluctuate daily based on economic indicators, Federal Reserve policy, and market conditions. Skilled mortgage professionals monitor these movements and advise clients on optimal lock timing.

| Rate Lock Period | Typical Cost | Best For |

|---|---|---|

| 15 days | Standard pricing | Refinances, quick closes |

| 30 days | Standard pricing | Most purchase transactions |

| 45 days | 0.125% premium | Extended closing timelines |

| 60 days | 0.250% premium | New construction, complex transactions |

For borrowers researching broker rates on mortgages, understanding lock strategies helps maximize value. Mortgage professionals time locks strategically, avoiding unnecessary extension fees while protecting clients from adverse rate movements.

Specialized Expertise for Different Property Types

Different property types require distinct underwriting approaches and loan products. Mortgage professionals with broad experience can guide clients through these variations effectively.

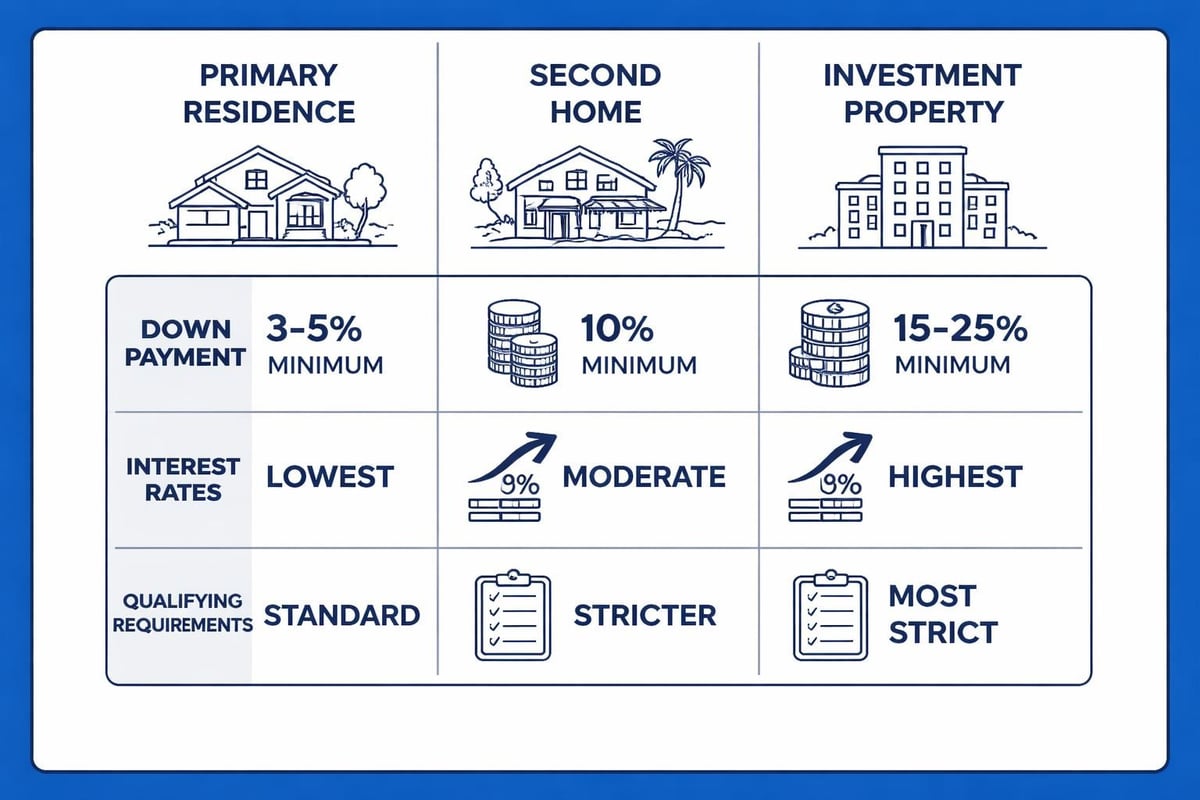

Primary Residence vs. Investment Property

The distinction between primary residence and investment property dramatically affects available loan terms, down payment requirements, and interest rates. Mortgage professionals ensure proper classification while maximizing favorable terms where possible.

Primary residence advantages include:

- Lower down payment options (as low as 3% on conventional loans)

- More favorable interest rates (typically 0.5-1.0% lower than investment properties)

- Access to first-time homebuyer programs and assistance

- Reduced reserve requirements

Investment property considerations involve:

- Minimum 15-20% down payment on most programs

- Higher interest rates reflecting increased lender risk

- Stricter debt-to-income calculations including projected rental income

- Larger cash reserve requirements (6-12 months)

Mortgage professionals help Seattle-area investors structure purchases optimally, sometimes recommending delayed investment property acquisition until building sufficient equity in a primary residence.

Jumbo Loans in Seattle's High-Cost Market

Seattle's median home prices frequently exceed conforming loan limits, requiring jumbo financing for many transactions. Mortgage professionals with jumbo loan expertise provide access to competitive programs that many borrowers assume are unattainable.

Jumbo loan requirements have relaxed considerably in recent years, with many lenders now offering:

- Down payments as low as 10% on qualified borrowers

- Competitive rates often within 0.25% of conforming loans

- Flexible debt-to-income ratios for well-qualified applicants

- Alternative documentation for self-employed borrowers and investors

According to National Mortgage News, the jumbo loan market has expanded significantly as lenders compete for business in high-cost metropolitan areas like Seattle. This competition benefits borrowers working with mortgage professionals who maintain relationships across multiple jumbo lenders.

Regulatory Compliance and Consumer Protection

The mortgage industry operates under extensive federal and state regulations designed to protect consumers. Understanding these protections helps borrowers recognize professional, compliant service.

Federal Disclosure Requirements

The Consumer Financial Protection Bureau mandates specific disclosures at key milestones throughout the mortgage process. Mortgage professionals must provide these documents within strict timelines and ensure borrowers understand their content.

Loan Estimate requirements include:

- Delivery within three business days of application

- Standardized format showing loan terms, projected payments, and closing costs

- Detailed breakdown of lender fees, third-party services, and prepaids

- Comparison information for different scenarios and alternatives

Closing Disclosure standards mandate:

- Delivery at least three business days before closing

- Final loan terms and actual closing costs

- Side-by-side comparison with original Loan Estimate

- Itemized settlement statement with all transaction details

Resources from the U.S. Department of Housing and Urban Development provide consumer education about these disclosures and borrower rights throughout the mortgage process.

Fiduciary Responsibility and Best Interest Standards

While not all mortgage professionals operate under fiduciary duty, ethical practitioners prioritize client interests above commission considerations. This means recommending appropriate loan products even when they generate lower compensation.

Quality mortgage professionals demonstrate this commitment by:

- Presenting multiple loan options with transparent cost comparisons

- Explaining trade-offs between rate and closing costs clearly

- Disclosing all compensation received from lenders or other parties

- Recommending against refinancing when it doesn't benefit the client

- Providing post-closing support and ongoing consultation

Research from Fannie Mae on consumer perceptions shows that borrowers value trustworthiness and transparency more highly than marginal rate differences when selecting mortgage professionals.

Long-Term Relationship Value Beyond the Transaction

The best mortgage professionals view client relationships as long-term partnerships rather than one-time transactions. This perspective creates ongoing value through market updates, refinancing opportunities, and strategic consultation.

Portfolio Review and Refinancing Strategy

Market conditions change, and mortgage professionals monitor client portfolios for beneficial refinancing opportunities. Interest rate drops, equity accumulation, or credit score improvements can all justify refinancing consideration.

Strategic refinancing serves multiple purposes:

- Rate-and-term refinancing to lower interest rates and reduce monthly payments

- Cash-out refinancing to access equity for renovations, investments, or debt consolidation

- Loan type conversion from adjustable to fixed rates or removal of private mortgage insurance

- Term modification to accelerate payoff or extend amortization for cash flow management

Mortgage professionals calculate break-even points, considering closing costs against monthly savings to ensure refinancing provides genuine financial benefit. They also anticipate future scenarios, advising clients when holding existing loans makes more sense despite current rate environments.

Growth Planning and Investment Strategy

As clients' financial situations evolve, mortgage professionals help structure financing for expanded real estate portfolios. A first-time buyer in Lake Forest Park today might become an investment property owner in Everett within five years.

Strategic planning includes:

- Building credit history and reserves for future investment purchases

- Structuring primary residence loans to preserve equity for down payments

- Timing property acquisitions to optimize tax benefits and cash flow

- Leveraging 1031 exchanges and portfolio lending strategies for multiple properties

- Coordinating with tax advisors and financial planners for integrated wealth building

This comprehensive approach transforms mortgage professionals from transaction facilitators into strategic financial advisors contributing to long-term wealth accumulation.

Common Challenges Mortgage Professionals Solve

Even well-prepared borrowers encounter obstacles during the mortgage process. Experienced mortgage professionals anticipate these challenges and implement solutions proactively.

Credit Issues and Score Optimization

Credit challenges range from minor reporting errors to significant derogatory marks. Mortgage professionals guide borrowers through credit improvement strategies, often working several months before application to optimize scores.

Minor issues requiring quick resolution:

- Disputing inaccurate tradelines or reporting errors

- Paying down credit card balances to improve utilization ratios

- Adding positive payment history through authorized user accounts

- Correcting identity mix-ups with credit bureaus

Major issues requiring strategic planning:

- Rehabilitating past foreclosures or bankruptcies with seasoning periods

- Explaining legitimate credit events with documentation and letters

- Establishing new credit after periods of non-use

- Managing collections strategically (some should be paid, others left alone)

Professional guidance prevents common mistakes like paying old collections that restart statute of limitations or closing accounts that reduce available credit.

Income Documentation Complexities

Self-employed borrowers, commission-based employees, and those with multiple income sources face additional documentation requirements. Mortgage professionals experienced with complex income situations know how to present documentation favorably while maintaining full compliance.

For self-employed borrowers in Seattle's thriving entrepreneurial ecosystem, this expertise proves invaluable. Two years of tax returns rarely tell the complete story, and strategic presentation of profit and loss statements, business bank accounts, and CPA letters can maximize qualifying income.

Appraisal Challenges in Competitive Markets

When appraisals come in below contract price, mortgage professionals coordinate solutions protecting both the transaction and the client's financial interests. Options include renegotiating price, challenging the appraisal with additional comparable sales data, increasing down payment, or restructuring with alternative loan products.

In rapidly appreciating neighborhoods throughout Shoreline and Lynnwood, appraisal gaps occur regularly. Experienced mortgage professionals maintain relationships with appraisal management companies and understand effective processes for reconsideration of value when warranted.

Working with skilled mortgage professionals transforms the home financing experience from overwhelming to manageable, providing expert guidance through every stage of the process. Whether you're purchasing your first home, refinancing an existing property, or building a real estate investment portfolio, the right professional partnership makes all the difference. Keith Akada at Mortgage Reel brings over 25 years of Seattle-area experience, specializing in helping tech professionals and homebuyers throughout Seattle, Bellevue, Redmond, and Kirkland navigate complex financing with clarity and confidence. With 750+ five-star reviews and the ability to close loans in as few as nine business days, Mortgage Reel delivers the expertise, responsiveness, and results you need in today's competitive market.