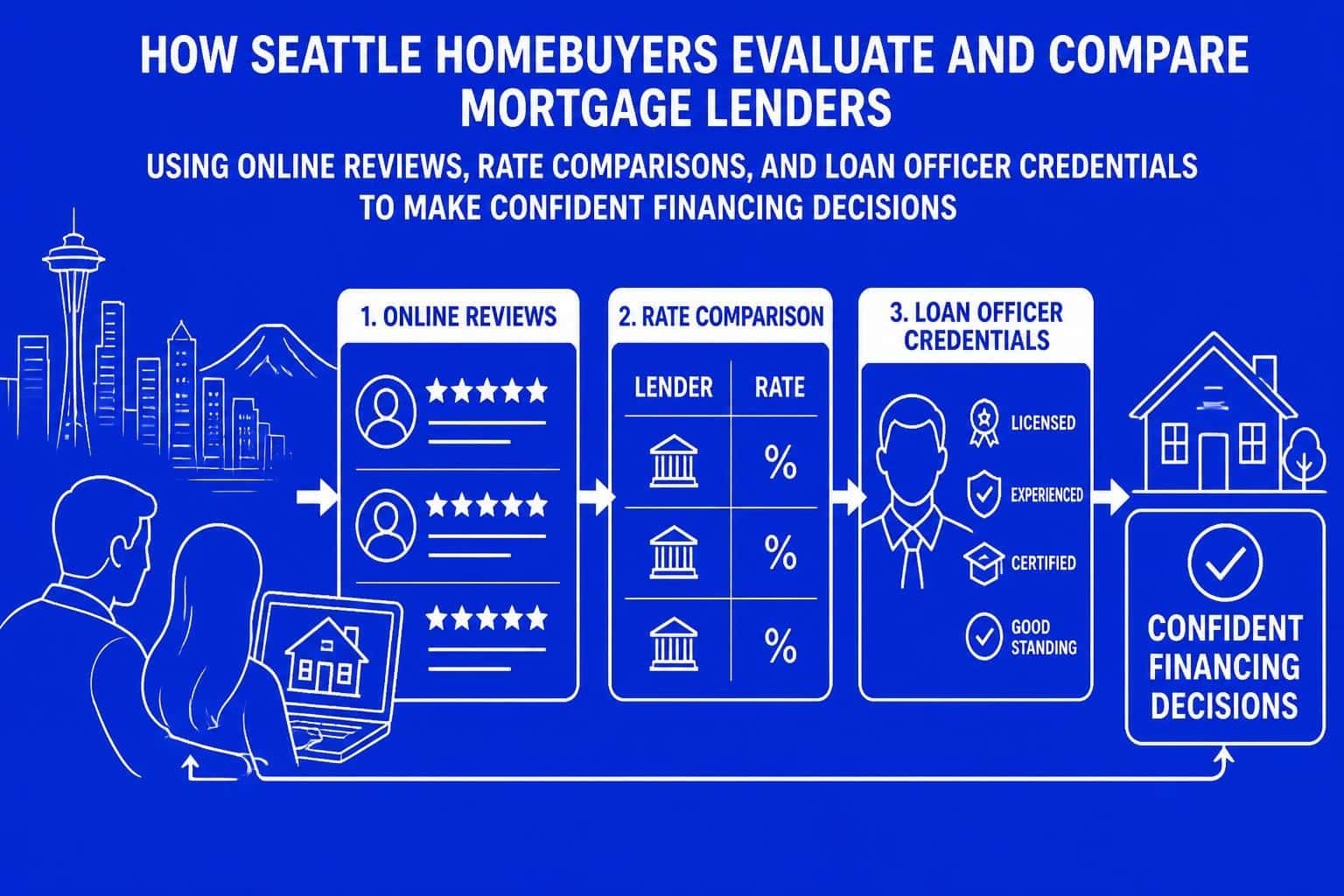

Selecting the right mortgage lender represents one of the most consequential financial decisions Seattle homebuyers make. With hundreds of loan officers competing for business across King County and beyond, understanding how to properly conduct a review for mortgage lender options separates successful transactions from costly mistakes. Whether you're purchasing a tech-corridor condo in Bellevue or a single-family home in Lake Forest Park, the lender you choose directly impacts your interest rate, closing timeline, and overall homebuying experience. This comprehensive guide walks you through the critical factors for evaluating mortgage professionals, interpreting customer feedback, and making informed comparisons that align with your financial goals.

Understanding What Makes a Review for Mortgage Lender Valuable

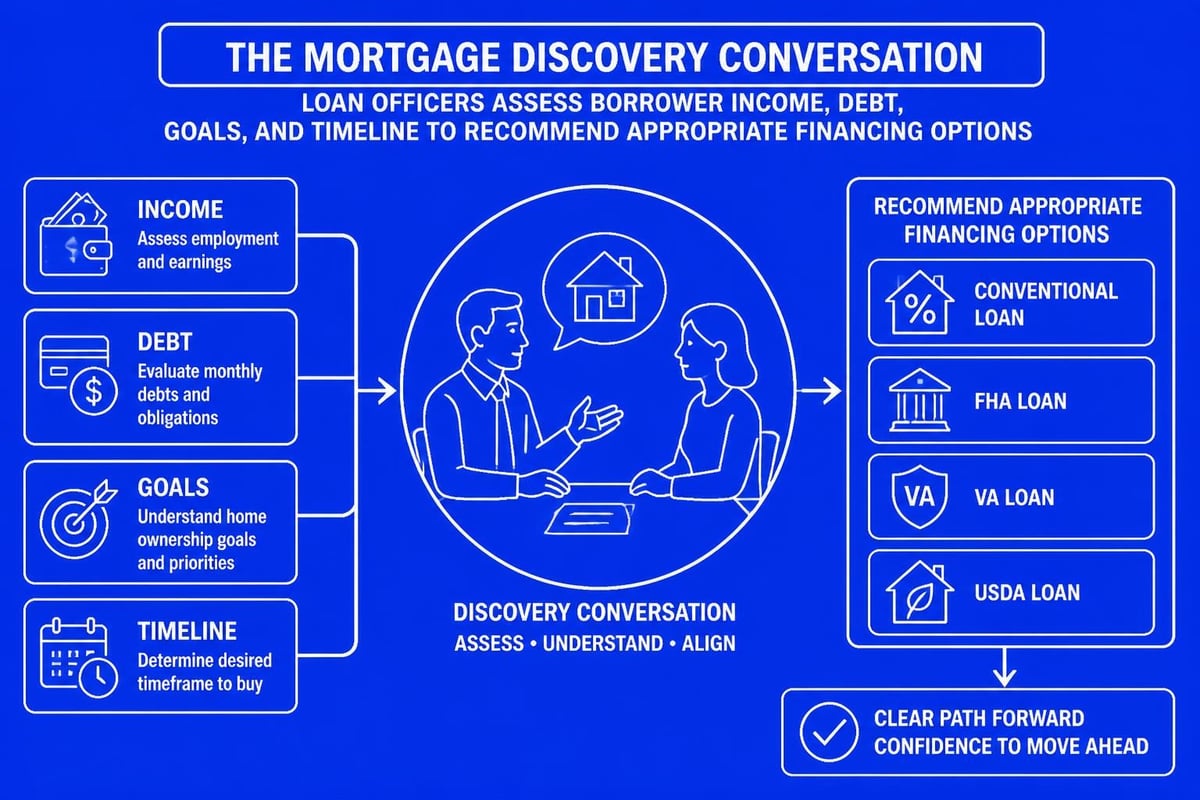

Not all online reviews carry equal weight when evaluating mortgage professionals. A meaningful review for mortgage lender services should provide specific insights into the loan officer's communication style, responsiveness, problem-solving ability, and execution during critical transaction phases.

Identifying Credible Review Platforms

Seattle homebuyers should prioritize reviews from verified platforms where borrowers must complete actual transactions before posting feedback. Google Business reviews, Zillow lender profiles, and Redfin agent recommendations typically require authentication, making them more reliable than anonymous forums.

Key platforms for mortgage lender reviews include:

- Google Business Profile (verified customer reviews)

- Zillow professional profiles with transaction history

- Redfin partner lender ratings

- Yelp business reviews with purchase verification

- WalletHub financial service evaluations

- Experience.com mortgage-specific feedback

Volume matters alongside quality. A Seattle mortgage broker with 750+ verified five-star reviews demonstrates consistent performance across hundreds of transactions, while someone with only 10-15 reviews may not provide sufficient data points for confident decision-making.

Analyzing Review Patterns and Red Flags

When conducting a thorough review for mortgage lender candidates, look beyond star ratings to identify patterns in customer experiences. Multiple borrowers mentioning identical strengths or weaknesses provides valuable signal about a loan officer's operational style.

Pay attention to how lenders respond to negative reviews. Professional mortgage brokers address concerns directly, take accountability for legitimate issues, and demonstrate commitment to resolution. Defensive responses or silence suggest potential service problems.

| Review Element | Positive Indicator | Warning Sign |

|---|---|---|

| Response time | "Answered texts within minutes" | "Took days to return calls" |

| Communication clarity | "Explained complex terms simply" | "Confusing jargon throughout" |

| Problem-solving | "Overcame appraisal gap creatively" | "Disappeared when issues arose" |

| Closing timeline | "Closed in 10 days as promised" | "Delayed closing twice" |

| Transparency | "No surprise fees at closing" | "Hidden costs appeared last minute" |

Critical Factors When Comparing Mortgage Lender Options

Beyond customer reviews, Seattle homebuyers need objective criteria for evaluating lender capabilities. The most highly reviewed loan officers combine competitive pricing with specialized expertise relevant to local market conditions.

Rate and Fee Structure Transparency

Understanding how to compare mortgage lenders requires examining the full cost picture, not just advertised interest rates. Request Loan Estimates from at least three lenders and compare origination fees, discount points, third-party costs, and annual percentage rates.

For Seattle-area tech professionals earning stock compensation, lenders experienced with qualifying RSUs and bonus income often secure better terms than retail banks unfamiliar with equity-heavy compensation structures. This specialized knowledge directly impacts approval amounts for jumbo home loans common in Bellevue and Redmond markets.

When reviewing rate quotes, compare:

- Base interest rate without points

- APR including all lender fees

- Origination charges and processing fees

- Lender credits or rate buydown options

- Lock period duration and extension policies

Specialized Program Knowledge

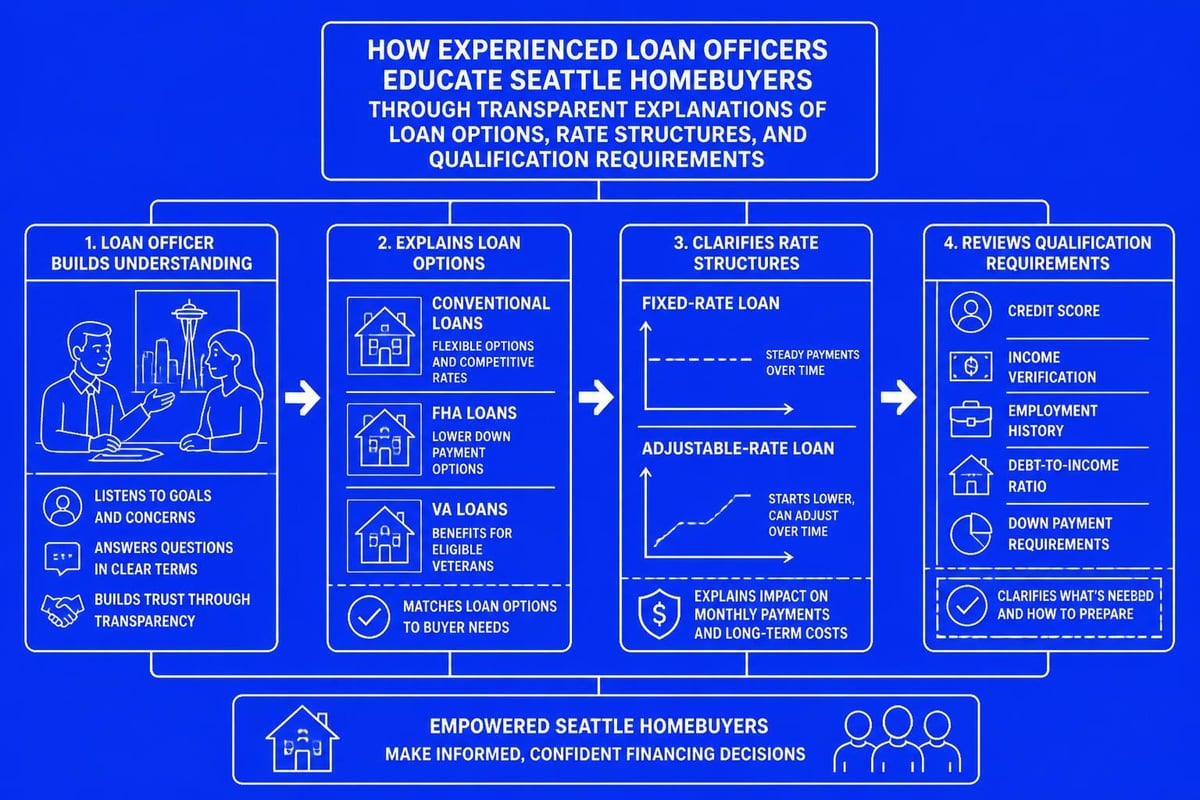

A comprehensive review for mortgage lender expertise should evaluate program variety and underwriting flexibility. The Pacific Northwest housing market demands lenders who navigate FHA, VA, conventional, and jumbo products with equal proficiency.

Loan officers serving Shoreline, Lynnwood, and Mill Creek buyers encounter diverse scenarios requiring creative solutions. First-time buyers need patient education about FHA home loan options, while seasoned investors require sophisticated analysis of cash-out refinance strategies.

Tech employees relocating from California or New York particularly benefit from lenders who understand high-balance conforming limits, jumbo underwriting nuances, and how to maximize qualifying income from complex compensation packages. These capabilities rarely surface in generic online reviews but prove critical during pre-approval and underwriting phases.

The Review Process: Step-by-Step Evaluation Method

Systematic lender comparison prevents common homebuyer mistakes and builds confidence in your financing partner selection. Follow this structured approach when conducting your review for mortgage lender candidates.

Initial Screening and Discovery Calls

Begin by finding a lender through trusted referrals from real estate agents active in your target neighborhoods. Capitol Hill, Lake Forest Park, and Everett markets each have lending specialists who understand hyperlocal pricing dynamics and competitive offer strategies.

During discovery conversations, evaluate how loan officers approach your unique situation. Do they ask probing questions about employment stability, debt obligations, and homeownership goals? Or do they immediately push toward a specific product without understanding your circumstances?

Essential questions for initial lender consultations:

- How do you approach qualifying stock compensation and bonuses?

- What's your average timeline from application to closing?

- Which underwriting challenges most commonly arise in Seattle markets?

- How do you communicate status updates throughout the process?

- What technology platforms do you use for document collection and processing?

Requesting and Comparing Loan Estimates

Federal law requires lenders to provide standardized Loan Estimates within three business days of receiving your application. These documents enable apples-to-apples comparison of costs and terms across multiple lenders.

Understanding the mortgage application process helps borrowers recognize whether loan officers provide accurate initial disclosures or lowball estimates to win business before revealing true costs later.

| Loan Estimate Section | What to Compare | Why It Matters |

|---|---|---|

| Page 1: Loan Terms | Interest rate, monthly payment, prepayment penalties | Core economic terms of your financing |

| Page 2: Projected Payments | Property taxes, insurance, HOA estimates | Accuracy of local market knowledge |

| Page 2: Costs at Closing | Cash needed at closing | Liquidity requirements and planning |

| Page 3: Calculating Cash to Close | Down payment, credits, earnest money | Transaction fund coordination |

| Page 3: Summaries of Transactions | Seller credits, closing cost breakdowns | Negotiation implications |

For competitive Seattle housing markets, lenders who close transactions quickly provide measurable advantage. The ability to close in 9-12 business days rather than the typical 30-45 days makes offers more attractive to sellers and reduces risk of rate lock expiration.

Reading Between the Lines: What Reviews Really Reveal

Experienced homebuyers develop pattern recognition skills when conducting a review for mortgage lender professionals. Certain phrases and themes in customer feedback correlate strongly with actual service quality.

Communication Style and Responsiveness

Reviews mentioning "answered my text at 9 PM" or "called me back within the hour" indicate loan officers who prioritize accessibility during what's often a stressful process. For buyers competing in fast-moving markets like Bellevue or Redmond, this responsiveness directly impacts offer success rates.

Conversely, comments about "had to chase them down constantly" or "never got straight answers" suggest organizational problems that compound stress during time-sensitive transactions.

Problem-Solving Under Pressure

The true test of mortgage lender quality emerges when unexpected challenges arise. Reviews describing how loan officers navigated appraisal shortfalls, income documentation issues, or title problems reveal crisis management capabilities.

Look for specific problem-resolution examples:

- Successfully restructured loan when appraisal came in low

- Found alternative documentation route for self-employed income verification

- Coordinated with sellers to adjust purchase terms around financing constraints

- Secured rate exceptions through underwriter relationships

- Expedited processing when buyer faced sudden timeline compression

Lenders serving the Greater Seattle area encounter unique challenges around competitive bidding, escalation clauses, and appraisal gaps. Reviews describing successful navigation of these local market dynamics provide valuable signal about real-world performance.

Educational Approach and Transparency

First-time homebuyers particularly benefit from loan officers who emphasize education over transaction volume. Reviews praising "took time to explain every option" or "never felt pressured" indicate client-centered service philosophies.

For complex scenarios involving conventional home loans versus jumbo financing, transparent lenders walk clients through tradeoffs rather than steering toward products that maximize their compensation.

Evaluating Lender Credentials and Market Position

Beyond customer reviews, professional credentials and market position indicate lender reliability and capability. Seattle's mortgage landscape includes everyone from solo brokers to national bank divisions, each with distinct advantages.

Licensing and Regulatory Compliance

All Washington State mortgage loan originators must maintain active NMLS (Nationwide Multistate Licensing System) licenses. Verify license status, check for regulatory actions, and confirm continuing education compliance through the NMLS Consumer Access database.

Lenders affiliated with established firms like Fairway Independent Mortgage Corporation benefit from institutional underwriting relationships, compliance infrastructure, and operational support that solo practitioners may lack. This backing often translates to faster processing, more flexible guidelines, and stronger problem-resolution capabilities.

Industry Recognition and Awards

While not definitive proof of quality, industry recognition from organizations like Scotsman Guide, Mortgage Executive Magazine, or local business journals suggests peer-validated expertise. Similarly, lenders who maintain top producer status year-over-year demonstrate consistent performance.

For Seattle homebuyers evaluating a review for mortgage lender options, combine these credentials with customer feedback to build a complete picture. A loan officer with both 750+ five-star reviews AND recognition as a top regional producer offers more certainty than someone with impressive credentials but limited customer validation.

Technology and Process Efficiency Indicators

Modern mortgage origination increasingly depends on technology platforms that streamline documentation, communication, and processing. Reviews mentioning digital tools often correlate with smoother overall experiences.

Digital Application and Document Management

Lenders offering mobile-responsive applications, electronic signature capabilities, and secure document upload portals reduce friction throughout the mortgage process. Tech-savvy Seattle buyers appreciate these efficiencies, particularly when coordinating purchases while managing demanding careers at Amazon, Microsoft, or Google.

Technology features that improve borrower experience:

- Mobile app for real-time status updates

- Automated task lists with clear next steps

- Text message communication options

- Instant document upload with automatic verification

- Electronic closing capabilities where permitted

Reviews describing "everything happened through the app" or "uploaded docs from my phone" indicate lenders investing in modern origination platforms rather than relying on outdated fax-and-email processes.

Processing Speed and Closing Timelines

When conducting a review for mortgage lender efficiency, closing timeline statistics provide objective performance data. While traditional mortgage closings average 30-45 days, high-performing lenders consistently close conventional purchases in 15-21 days and often achieve 9-12 day timelines when necessary.

For competitive Seattle markets where sellers receive multiple offers, faster closing capability provides measurable advantage. Reviews specifically mentioning "closed in 10 days" or "beat the promised timeline" indicate operational excellence beyond standard industry performance.

Specialized Expertise for Seattle Market Segments

Different buyer profiles require distinct lender capabilities. A comprehensive review for mortgage lender options should consider specialization alignment with your specific situation.

Tech Compensation and Jumbo Loan Expertise

Seattle's concentration of technology employers creates unique lending requirements. Many Microsoft, Amazon, and Google employees earn significant portions of total compensation through RSUs, stock options, and performance bonuses that require specialized underwriting approaches.

Jumbo mortgage specialists understand how to qualify this variable income, navigate verification requirements, and structure loans that maximize purchasing power while maintaining comfortable debt-to-income ratios. This expertise proves particularly valuable in high-cost areas like Bellevue, where median home prices frequently exceed conforming loan limits.

First-Time Buyer Education and Support

Buyers entering homeownership for the first time benefit from lenders who prioritize education and patience. Reviews mentioning "answered my questions without making me feel stupid" or "walked me through every step" indicate loan officers who invest time in client understanding rather than rushing through transactions.

First-time mortgage loans often involve down payment assistance programs, FHA financing with lower credit requirements, or creative structuring to minimize upfront cash needs. Lenders experienced in these programs serve Shoreline, Lynnwood, and Mill Creek buyers more effectively than those focused exclusively on conventional high-balance loans.

Investment Property and Portfolio Lending

Real estate investors require lenders who understand non-owner-occupied underwriting, debt service coverage ratios, and portfolio lending options. Reviews from investor clients describe capabilities like "qualified me for my fifth rental property" or "structured a blanket loan for my properties" that indicate specialized expertise.

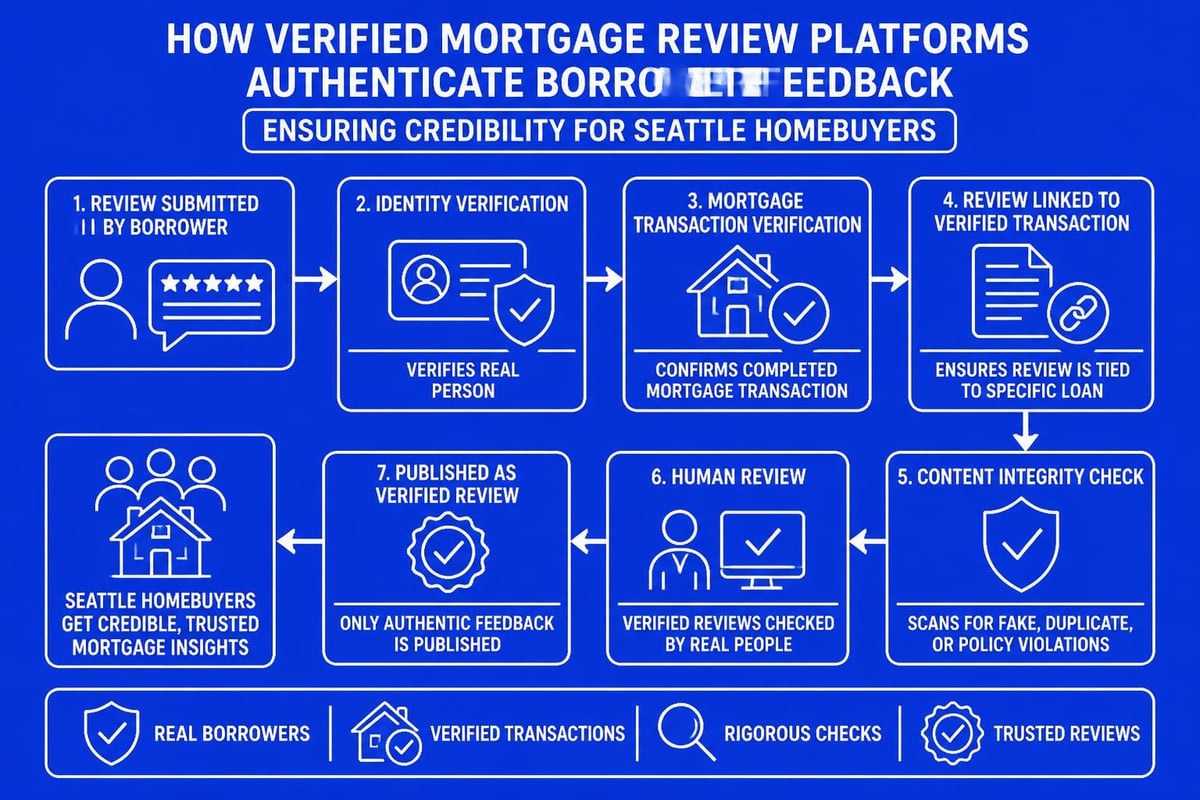

Verifying Reviews and Avoiding Manipulation

As online reviews increasingly influence consumer decisions, some businesses attempt to game the system through fake reviews or selective feedback solicitation. Savvy homebuyers develop skills for identifying authentic feedback.

Signs of Genuine Customer Reviews

Authentic reviews typically include specific transaction details, mention individual team members by name, describe concrete problems and resolutions, and acknowledge both strengths and minor weaknesses. Generic praise like "great service!" without supporting details carries less information value.

Compare review distribution across multiple platforms. Legitimate businesses maintain consistent ratings on Google, Zillow, Redfin, and other sites, while manipulated review profiles often show dramatic quality differences between platforms.

Checking References Beyond Online Reviews

Supplement your online review for mortgage lender research by requesting direct references from recent clients with situations similar to yours. Speaking with a borrower who recently purchased a Bellevue condo using stock compensation provides insights more relevant than reading reviews from first-time buyers financing Everett starter homes.

Real estate agents working your target neighborhoods offer valuable perspective on lender performance, particularly regarding communication quality, closing reliability, and problem-resolution effectiveness during complex transactions.

Making Your Final Lender Selection

After completing thorough research, narrow your options to 2-3 finalists and conduct detailed consultations. These conversations should confirm initial impressions and reveal any red flags that didn't surface during preliminary research.

Questions That Reveal Lender Quality

Move beyond generic mortgage questions to probe specific capabilities relevant to your situation and Seattle market dynamics. Ask about recent transactions similar to yours, challenging scenarios they've navigated, and their approach to time-sensitive competitive situations.

Advanced questions for final lender evaluation:

- How have you helped buyers structure offers that won in multiple-bid situations?

- What's your success rate qualifying stock-heavy compensation packages?

- Describe your most challenging transaction in the past six months and how you resolved it

- Which underwriters do you work with most frequently, and how do those relationships benefit borrowers?

- What happens if my appraisal comes in low on a property with an escalation clause?

The depth and confidence of responses indicate whether you're working with a true market expert or someone who handles generic transactions without developing specialized Seattle market knowledge.

Trust Your Instincts Alongside Data

While comprehensive review for mortgage lender research provides essential information, personal rapport matters during what's often a months-long relationship. If a highly-reviewed loan officer communicates in ways that don't align with your preferences, continue searching for better fit.

The mortgage process involves sharing detailed financial information, making high-stakes decisions under time pressure, and coordinating complex logistics. Choose a lender you trust to guide you through challenges while respecting your autonomy in decision-making.

Regional Considerations for Greater Seattle Borrowers

Market dynamics vary significantly across King and Snohomish counties, requiring lenders with neighborhood-specific knowledge. When evaluating mortgage professionals, confirm they actively serve your target area and understand local pricing trends, inventory patterns, and competitive conditions.

Understanding Local Market Expertise

A lender specializing in Lake Forest Park home loans brings different value than one focused on downtown Seattle condos. Suburban single-family markets involve different appraisal considerations, property tax structures, and buyer demographics than urban high-rise developments.

Reviews from borrowers who purchased in your specific target neighborhoods provide the most relevant performance signal. Look for mentions of the schools, commute patterns, and community characteristics that matter to your decision-making.

Navigating Competitive Offer Strategies

Seattle's competitive housing market often requires strategic financing approaches that strengthen offer appeal. Lenders experienced in local markets help buyers structure competitive offers through tactics like larger earnest money deposits, shortened inspection contingencies, or appraisal gap coverage strategies.

Reading reviews that describe successful competitive outcomes provides insight into a lender's strategic advisory capabilities beyond simple transaction processing. Phrases like "helped us win against five other offers" or "structured our financing to appeal to the sellers" indicate value-added guidance.

Conducting a thorough review for mortgage lender options requires balancing quantitative analysis with qualitative assessment to identify the right financing partner for your Seattle-area home purchase. By systematically evaluating customer feedback, comparing rate structures, verifying credentials, and confirming specialized expertise, you position yourself for a smooth transaction and optimal loan terms. Keith Akada at Mortgage Reel brings 25+ years of Seattle market expertise, 750+ five-star verified reviews, and specialized capabilities qualifying tech compensation for buyers across Bellevue, Redmond, Kirkland, and surrounding communities, delivering transparent guidance and reliable execution throughout your homebuying journey.