Veterans and active-duty military personnel in the Seattle area have access to one of the most powerful home financing tools available: the VA loan. Understanding which mortgage lenders for VA loans offer the best combination of competitive rates, efficient processing, and expert guidance can make the difference between a smooth transaction and a frustrating experience. With Seattle's competitive housing market spanning from Shoreline to Everett, working with the right lender who understands both VA guidelines and local market dynamics is essential for maximizing your hard-earned benefits.

What Makes VA Loan Lenders Different from Traditional Mortgage Lenders

Not all mortgage lenders for VA loans operate with the same level of expertise or commitment to military borrowers. VA-approved lenders must meet specific requirements set by the Department of Veterans Affairs and demonstrate experience with the unique guidelines governing these loans.

VA Approval and Lender Requirements

The VA maintains a list of approved lenders who have undergone specific training and demonstrated competency in originating VA-backed mortgages. These lenders understand the nuances of Certificate of Eligibility (COE) verification, funding fee calculations, and occupancy requirements that distinguish VA loans from conventional financing.

Key distinctions of VA-approved lenders include:

- Direct access to VA automated underwriting systems

- Training on residual income calculations specific to VA guidelines

- Experience with VA appraisal requirements and MPRs (Minimum Property Requirements)

- Knowledge of VA funding fee exemptions for disabled veterans

- Familiarity with VA loan limits and how they apply in high-cost areas like Seattle

In markets like Bellevue and Redmond, where median home prices regularly exceed $800,000, understanding how VA loan limits work becomes critical for structuring competitive offers.

Experience with Military Compensation Structures

Top mortgage lenders for VA loans recognize that military pay structures differ significantly from civilian employment. Base pay, housing allowances (BAH), hazardous duty pay, and other military compensation components require specific documentation and qualifying approaches.

For Seattle-area military personnel stationed at Joint Base Lewis-McChord or Naval Station Everett, lenders with deep VA experience understand how to properly document and qualify various income sources. This expertise proves particularly valuable when competing in markets like Lake Forest Park, where strong offers require maximized purchasing power.

Types of Mortgage Lenders Offering VA Loans

The landscape of mortgage lenders for VA loans includes several distinct categories, each with advantages and potential limitations for Seattle-area borrowers.

National Banks and Credit Unions

Large national institutions often originate significant volumes of VA loans. According to recent VA lender statistics, major banks consistently rank among the top originators by loan volume.

| Lender Type | Typical Advantages | Potential Considerations |

|---|---|---|

| National Banks | Established reputation, multiple branch locations | May have higher overlay requirements beyond VA minimums |

| Credit Unions | Member-focused service, competitive rates | Sometimes limited to specific service areas or membership criteria |

| Mortgage Banks | Specialized loan products, faster processing | May vary in VA experience levels |

| Mortgage Brokers | Access to multiple lenders, personalized guidance | Important to verify VA expertise and lender relationships |

Regional and Local Specialists

Seattle-area borrowers often benefit from working with regional lenders who understand Pacific Northwest market conditions. When properties in Lynnwood or Mill Creek require quick closings to compete with cash offers, local expertise in navigating King and Snohomish County recording processes becomes invaluable.

A mortgage broker in Seattle with strong relationships to multiple VA-approved lenders can often provide more flexibility in structuring loans and addressing unique property or borrower situations.

Key Factors When Choosing VA Loan Lenders

Selecting among mortgage lenders for VA loans requires evaluating multiple dimensions beyond advertised interest rates.

Rate Competitiveness and Fee Structures

While VA loans limit certain fees lenders can charge to veterans, significant variations still exist in overall cost structures. Smart borrowers in Seattle compare:

- Base interest rates across multiple lenders on the same day

- Lender credits that can offset closing costs

- Origination charges and processing fees

- Discount points and their impact on long-term savings

- Third-party fees the lender controls or negotiates

The VA prohibits lenders from charging veterans for certain services, but understanding which fees are negotiable creates opportunities for savings. When purchasing in competitive neighborhoods throughout Shoreline or Everett, reducing upfront costs through lender credits can preserve cash for earnest money or post-closing reserves.

Processing Speed and Closing Timeline

Seattle's housing market frequently demands quick closings. The best mortgage lenders for VA loans maintain efficient processes that can compete with conventional financing timelines.

Processing efficiency indicators include:

- Average days from application to clear-to-close

- Underwriter availability and responsiveness

- Technology platforms for document upload and status tracking

- Appraisal ordering and management systems

- Direct VA underwriting authority versus outsourced underwriting

Experienced VA lenders understand that delayed closings can result in lost opportunities, particularly when sellers receive multiple offers. Lenders capable of closing in 15-21 days provide competitive advantages in markets like Bellevue and Redmond.

Understanding VA Loan Benefits Through the Right Lender

The most knowledgeable mortgage lenders for va loans ensure borrowers fully utilize available benefits rather than leaving value on the table.

Zero Down Payment Advantages

VA loans offer qualified borrowers the ability to purchase without down payment up to VA loan limits. In 2026, VA loan limits in King County reflect the high-cost area designation, allowing veterans to borrow substantial amounts with zero down.

Experienced lenders help Seattle-area veterans understand:

- How loan limits apply to their specific situation

- When jumbo VA loans require down payments above limits

- Strategies for combining VA loans with seller concessions

- Documentation requirements for gift funds if used for closing costs

For first-time homebuyers in Seattle, the zero-down benefit eliminates years of saving that conventional loans might require, accelerating the path to homeownership.

Funding Fee Waivers and Reductions

The VA funding fee varies based on down payment amount, loan type, and whether the borrower has used VA benefits previously. Top mortgage lenders for VA loans ensure eligible veterans receive proper exemptions.

Veterans with service-connected disabilities qualify for complete funding fee waivers, creating substantial savings. On a $750,000 purchase in Lake Forest Park, the funding fee waiver could save over $20,000 compared to non-exempt borrowers.

Competitive Interest Rates

VA loans consistently offer lower interest rates compared to conventional financing with similar down payments. Understanding VA loan types helps borrowers select the right product for their situation.

The VA guarantee reduces lender risk, allowing mortgage lenders for VA loans to offer preferential pricing. This rate advantage compounds over the life of a 30-year mortgage, creating tens of thousands in interest savings for Seattle-area veterans.

Common Challenges and How Expert Lenders Address Them

Even with significant benefits, VA loans present specific challenges that experienced lenders navigate effectively.

Property Condition Requirements

VA appraisals include Minimum Property Requirements (MPRs) that can complicate transactions involving older homes or properties needing repairs. Seattle's housing stock includes many homes built before modern building codes, potentially triggering MPR issues.

Skilled mortgage lenders for VA loans help by:

- Pre-screening properties for potential MPR concerns

- Educating buyers on required repairs versus optional improvements

- Coordinating with sellers on addressing issues before closing

- Structuring transactions to accommodate repair escrows when allowed

- Providing alternative solutions when properties cannot meet VA standards

In neighborhoods like Mill Creek with newer construction, MPR issues rarely arise, but buyers considering Everett's historic districts benefit from lender expertise in navigating these requirements.

Seller Perceptions and Competitive Offers

Some Seattle-area sellers or listing agents harbor misconceptions about VA loans, viewing them as slower or more complicated than conventional financing. Top lenders combat these perceptions through:

- Pre-approval letters clearly stating quick closing capabilities

- Lender contact information for agent verification calls

- Track record documentation showing on-time closing rates

- Education materials addressing common VA loan myths

- Proactive communication throughout the transaction

When working with a trusted Seattle mortgage broker, veterans gain an advocate who educates all transaction parties about VA loan efficiency and reliability.

VA Loan Qualification Standards and Lender Overlays

Understanding how different mortgage lenders for VA loans apply qualification standards helps veterans position themselves optimally.

Credit Score Requirements

The VA itself does not establish minimum credit score requirements, but individual lenders implement their own standards. Most VA lenders require minimum scores between 580 and 620, though some offer programs for lower scores with compensating factors.

| Credit Score Range | Typical Lender Response | Rate Impact |

|---|---|---|

| 740+ | Best rates, minimal documentation | None |

| 680-739 | Standard approval, competitive rates | Minor |

| 620-679 | May require additional documentation | Moderate |

| 580-619 | Limited lender options, higher rates | Significant |

| Below 580 | Specialty lenders, manual underwriting | Substantial |

Seattle-area borrowers with lower credit scores benefit from lenders who manually underwrite loans rather than relying solely on automated systems.

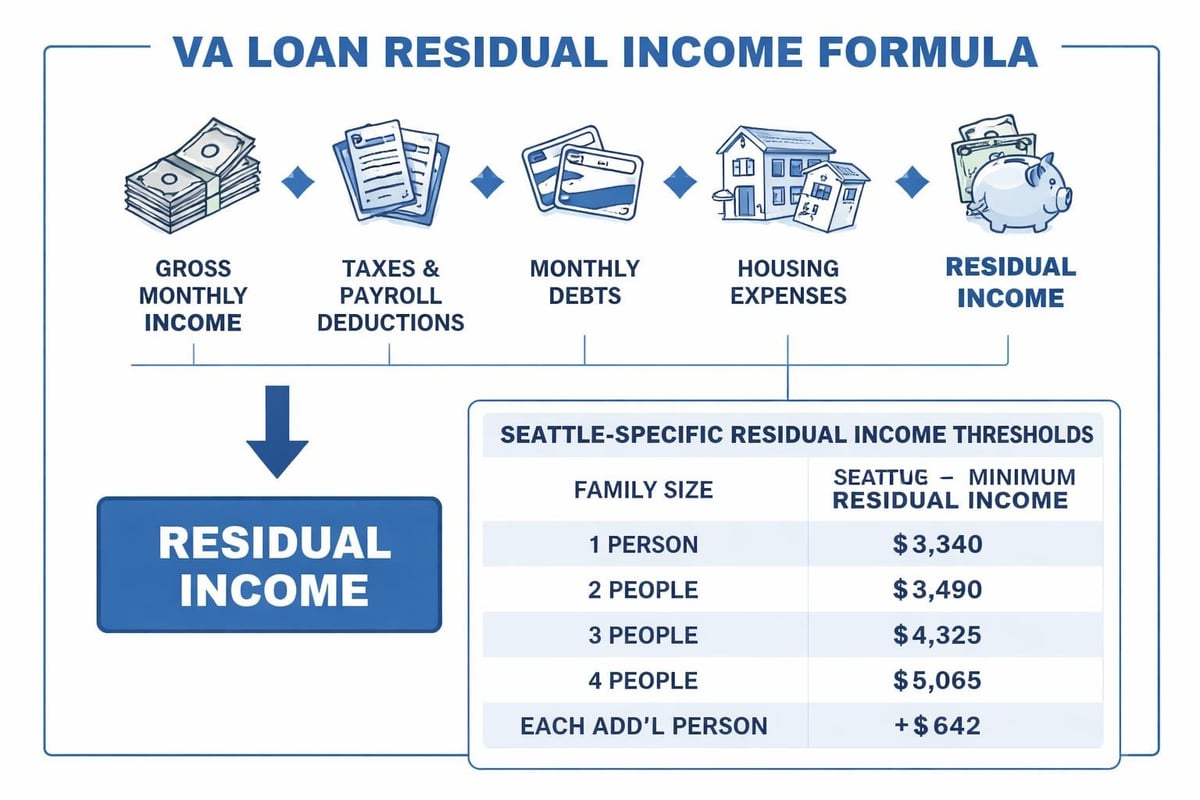

Debt-to-Income Ratios and Residual Income

VA loans use two distinct measures to assess affordability: debt-to-income (DTI) ratios and residual income requirements. The residual income calculation distinguishes VA loans from conventional products and reflects true affordability rather than just payment ratios.

Experienced mortgage lenders for VA loans understand that residual income requirements vary by family size and geographic region. Seattle falls into the West region with higher residual income thresholds reflecting local living costs.

For technology professionals in Bellevue and Redmond, lenders familiar with qualifying RSUs and stock compensation structure income documentation to maximize residual income calculations while managing DTI ratios effectively.

Specialized VA Loan Programs and Lender Capabilities

Beyond standard purchase loans, comprehensive mortgage lenders for VA loans offer specialized programs addressing specific veteran needs.

VA Cash-Out Refinance Options

Veterans with existing mortgages can access home equity through VA cash-out refinances, often at lower rates than home equity loans or lines of credit. Top VA lenders structure these refinances to:

- Convert conventional or FHA loans to VA financing

- Consolidate higher-interest debt

- Fund home improvements or investments

- Provide cash reserves for financial flexibility

Seattle-area homeowners who purchased before recent refinancing trends often hold substantial equity, creating opportunities for strategic refinancing.

Interest Rate Reduction Refinance Loans (IRRRLs)

The VA streamlined refinance program, called IRRRL or "VA to VA refinance," offers existing VA borrowers a fast path to lower rates with minimal documentation. The best mortgage lenders for VA loans process IRRRLs efficiently, often closing in under two weeks.

IRRRLs require no appraisal, limited income verification, and reduced documentation compared to traditional refinances. When rates drop, veterans throughout Lynnwood and Shoreline can quickly capture savings without extensive underwriting.

VA Construction and Renovation Loans

Some specialized lenders offer VA construction loans or renovation products, allowing veterans to purchase and improve properties with single-loan financing. These programs prove particularly valuable in Seattle's competitive market, where move-in-ready homes command premium pricing.

Questions to Ask Potential VA Lenders

Veterans comparing mortgage lenders for VA loans should conduct thorough interviews focusing on experience, capabilities, and service approach.

Essential questions include:

- How many VA loans do you close monthly in the Seattle area?

- What is your average timeline from application to closing?

- Do you offer in-house underwriting or outsource to third parties?

- What credit score and DTI ranges do you work within?

- How do you handle properties with potential MPR issues?

- Can you provide references from recent VA borrowers?

- What technology platforms do you use for application and tracking?

- How do you communicate with borrowers and real estate agents?

- What distinguishes your VA loan service from competitors?

- Do you offer rate locks and what are the terms?

Responses to these questions reveal lender expertise, commitment to VA borrowers, and operational capabilities that impact transaction success.

The Role of Loan Servicers After Closing

While choosing mortgage lenders for VA loans focuses primarily on the origination process, understanding servicing matters for long-term satisfaction. The VA explains loan servicing responsibilities, which include payment processing, escrow management, and customer service.

Some lenders service their own loans while others sell servicing rights to third parties. Veterans should understand servicer identity, payment procedures, and contact methods before closing. Quality servicers provide:

- Clear monthly statements and online account access

- Responsive customer service for questions or issues

- Accurate escrow accounting for taxes and insurance

- Proper handling of disability exemptions and credits

- Assistance if financial hardship occurs

Finding the Best VA Lenders in Seattle's Market

Seattle-area veterans benefit from numerous VA-approved lenders, but identifying the optimal match requires research and comparison. Resources for finding the best VA lender emphasize evaluating multiple dimensions beyond advertised rates.

Leveraging Online Reviews and Referrals

Military community recommendations provide valuable insights into lender performance. Veterans should seek referrals from:

- Fellow service members who recently purchased in Seattle

- Military housing offices at local installations

- Veteran service organizations with local chapters

- Real estate agents experienced in VA transactions

- Online review platforms specific to mortgage services

Lenders with consistent positive feedback across multiple platforms demonstrate reliable service delivery. When evaluating mortgage lenders for VA loans, patterns in reviews regarding communication, timeline adherence, and problem-solving reveal important performance indicators.

Comparing Multiple Lender Quotes

The Consumer Financial Protection Bureau recommends obtaining Loan Estimates from at least three lenders to ensure competitive pricing. Veterans should request quotes on the same day for accurate comparison, as rates fluctuate daily.

Comparing Loan Estimates requires examining:

- Interest rate and annual percentage rate (APR)

- Lender credits or charges in Section A

- Services you cannot shop for in Section B

- Title and government fees in Sections C, E, and F

- Prepaids and initial escrow deposits in Sections F and G

- Total closing costs and cash to close figures

For purchases in Everett or Shoreline, even small rate differences compound significantly over 30-year terms, making thorough comparison worthwhile.

VA Loan Limits and High-Cost Area Considerations

Seattle's designation as a high-cost housing market directly impacts VA loan limits and borrowing capacity. In 2026, veterans with full entitlement can borrow above standard VA limits without down payments, subject to lender approval and income qualification.

Understanding entitlement calculations helps veterans maximize benefits. Experienced mortgage lenders for VA loans explain:

- Basic entitlement versus bonus entitlement amounts

- How previous VA loan use affects remaining entitlement

- Restoration of entitlement after selling VA-financed properties

- Calculating available entitlement for second VA loans

For Seattle-area homes exceeding VA limits, some veterans choose jumbo VA loans requiring minimal down payments rather than conventional jumbo financing with steeper requirements.

Working with Real Estate Professionals Who Understand VA Loans

The best mortgage lenders for VA loans partner effectively with real estate agents experienced in veteran transactions. Agent knowledge of VA requirements influences:

- Property selection compatible with MPR standards

- Offer structuring that competes with conventional financing

- Negotiation of seller concessions within VA limits

- Timeline coordination for appraisal and underwriting

- Problem-solving when issues arise during due diligence

Veterans purchasing in competitive Seattle neighborhoods benefit from agent-lender teams with proven collaboration records. This coordination proves especially valuable when multiple-offer situations require quick decisions and strong positioning.

Technology and Digital Tools from Modern VA Lenders

Leading mortgage lenders for VA loans leverage technology to streamline processes and enhance borrower experience. Digital capabilities that improve VA loan transactions include:

- Mobile applications for document upload and status tracking

- Electronic signature platforms reducing paperwork delays

- Automated COE retrieval from VA databases

- Instant pre-qualification calculators with VA-specific parameters

- Real-time rate monitoring and lock capabilities

- Direct messaging systems for lender-borrower communication

Technology adoption accelerates timelines and increases transparency throughout the loan process. For busy military personnel or Seattle-area veterans managing demanding careers, digital tools provide convenience without sacrificing service quality.

Understanding VA Loan Costs Beyond Interest Rates

While VA loans limit certain fees, veterans still pay various costs at closing. Comprehensive mortgage lenders for VA loans provide detailed cost breakdowns and identify savings opportunities.

Typical VA loan costs include:

- VA funding fee (unless exempt due to disability)

- Appraisal fee

- Credit report charges

- Title insurance and settlement services

- Recording fees and transfer taxes

- Prepaid interest and escrow reserves

- Homeowners insurance premiums

The VA prohibits charging veterans for certain services like attorney fees (in non-attorney states) and lender inspection fees. Sellers can contribute up to 4% of the purchase price toward buyer closing costs, creating opportunities for negotiation that reduce out-of-pocket expenses.

Special Considerations for Seattle-Area Military Personnel

Active-duty service members and veterans in the Seattle region face unique considerations when selecting mortgage lenders for VA loans.

Deployment and Remote Closing Capabilities

Military personnel may face deployment or relocation during the home purchase process. The best VA lenders accommodate these situations through:

- Power of attorney acceptance for closings

- Remote online notarization options

- Mail-away closing packages

- Flexible scheduling for final walkthroughs

- Extended rate lock periods

Lenders experienced with military clients anticipate these scenarios and structure processes to accommodate service obligations without derailing transactions.

BAH and Military Allowances in Qualification

Seattle-area military personnel receive Basic Allowance for Housing (BAH) reflecting local cost of living. Knowledgeable mortgage lenders for VA loans properly document and qualify BAH, ensuring veterans receive full credit for this non-taxable income.

Proper BAH qualification significantly impacts purchasing power. For personnel stationed at Joint Base Lewis-McChord qualifying for Seattle-area BAH rates, this allowance provides substantial income that experienced lenders factor appropriately into residual income and DTI calculations.

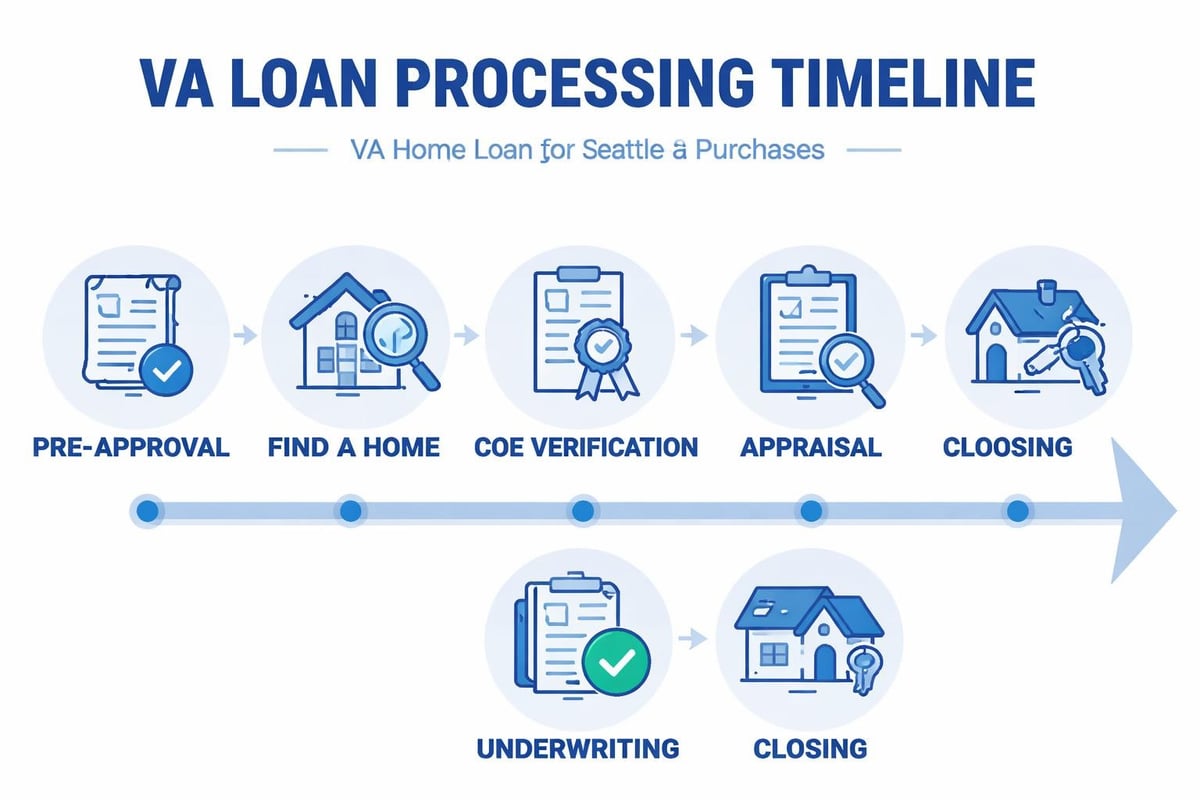

The Importance of Pre-Approval from VA Lenders

Serious homebuyers in Seattle's competitive market require strong pre-approval letters from reputable mortgage lenders for VA loans. Comprehensive pre-approval involves:

- Complete credit report review and analysis

- Income documentation and verification

- Asset statement collection and sourcing

- Debt obligation verification

- COE procurement from the VA

- Preliminary underwriting review

Strong pre-approvals from respected lenders carry weight with sellers and listing agents. When competing against multiple offers in Bellevue or Redmond, a pre-approval demonstrating thorough vetting and quick closing capability strengthens negotiating position.

Understanding home loan approval timelines helps veterans prepare documentation efficiently and position themselves competitively from the first showing.

VA Loan Assumption Opportunities

An often-overlooked benefit of VA financing involves loan assumability. When interest rates rise above existing loan rates, VA loan assumption becomes attractive to buyers, potentially increasing home marketability.

The best mortgage lenders for VA loans educate veterans about:

- Assumption qualification requirements

- Entitlement release procedures

- Liability release importance

- Marketing advantages of assumable loans

- Processing assumption requests

Buyers assuming VA loans must qualify based on current lender standards, but they acquire the existing interest rate rather than current market rates. This feature provides strategic options for both buyers and sellers in changing rate environments.

Selecting the right mortgage lenders for VA loans requires evaluating expertise, service quality, competitive pricing, and local market knowledge. Veterans and active-duty personnel in the Seattle area deserve lenders who maximize their hard-earned benefits while delivering efficient, transparent service throughout the home financing process. Keith Akada and the team at Mortgage Reel bring over 25 years of experience helping Seattle-area veterans navigate VA loan options with confidence, combining deep VA lending expertise with local market knowledge across Seattle, Bellevue, Redmond, and surrounding communities. Whether you're a first-time buyer or experienced homeowner, we're ready to help you leverage your VA benefits effectively. Connect with Mortgage Reel today to explore your VA loan options with a trusted Seattle mortgage professional.