Becoming a homeowner in Seattle represents one of the most significant financial decisions you'll make. For first home buyers navigating the Greater Seattle area in 2026, understanding mortgage options, down payment requirements, and available assistance programs can mean the difference between getting outbid repeatedly or securing your ideal property. The Seattle housing market presents unique challenges-from competitive bidding in Bellevue to rising prices in Mill Creek-but with proper preparation and strategic guidance, homeownership remains achievable. This comprehensive guide breaks down everything first-time buyers need to know about financing, qualifying, and closing on their first property in the Pacific Northwest.

Understanding Your Financial Position

Before exploring homes in Seattle or Shoreline, first home buyers must establish a clear picture of their financial health. This foundation determines which loan programs you qualify for and how much home you can afford.

Credit Score Requirements and Impact

Your credit score serves as the cornerstone of mortgage qualification. Most conventional loans require a minimum score of 620, though various first-time homebuyer loans and programs offer flexibility for different credit profiles.

Credit score ranges and typical loan options:

| Credit Score | Available Loan Types | Typical Down Payment |

|---|---|---|

| 580-619 | FHA, some conventional | 3.5%-10% |

| 620-679 | Conventional, FHA, VA | 3%-5% |

| 680-739 | All loan types, better rates | 3%-20% |

| 740+ | Best rates, jumbo options | 3%-20% |

For tech professionals at Amazon or Microsoft in Seattle, even minor credit improvements can translate into thousands saved over the loan term. Focus on paying down revolving debt, avoiding new credit inquiries during your home search, and correcting any errors on your credit report before applying.

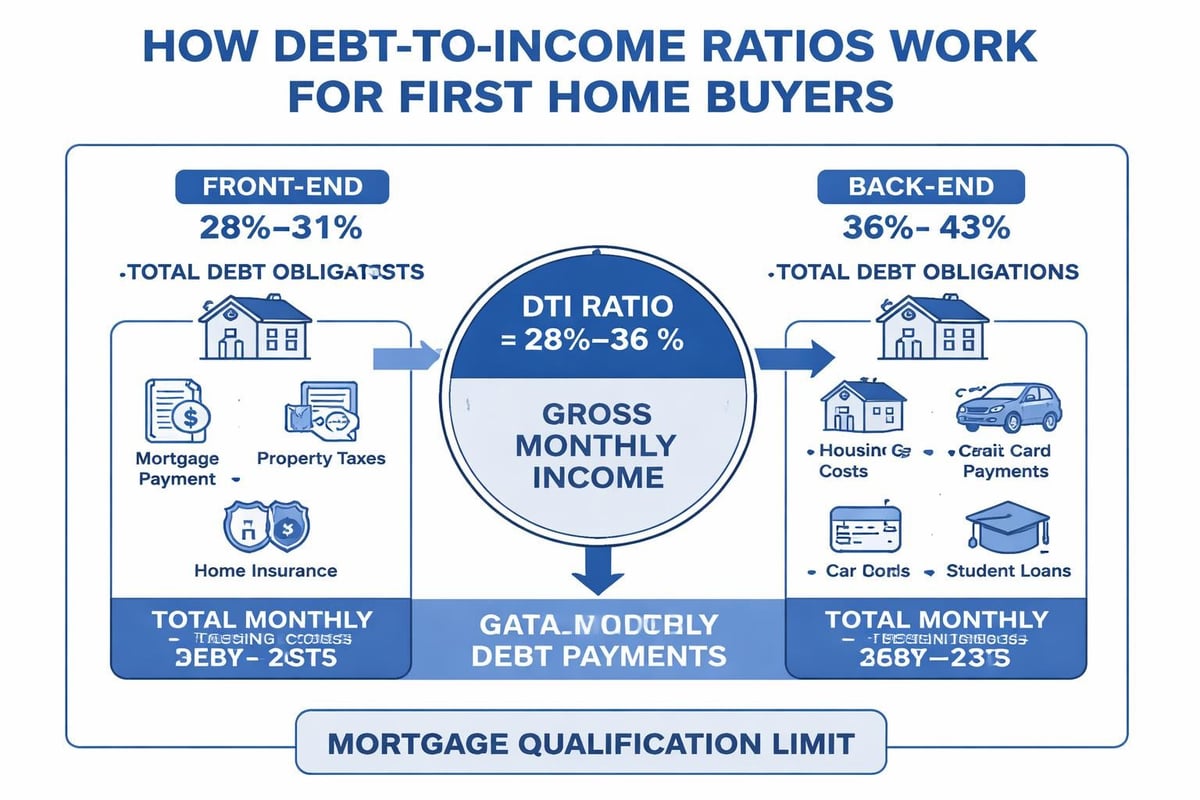

Debt-to-Income Ratio Explained

Lenders evaluate your debt-to-income (DTI) ratio to assess repayment capacity. This calculation divides your monthly debt obligations by your gross monthly income.

Front-end DTI covers only housing costs (principal, interest, taxes, insurance, HOA fees). Most programs allow 28-31% for this ratio.

Back-end DTI includes all debts: housing, car loans, student loans, credit cards, and other recurring obligations. Conventional loans typically cap this at 43-50%, though some programs allow higher ratios with compensating factors.

For a Lynnwood buyer earning $8,000 monthly with $400 in car payments and $300 in student loans, the maximum back-end DTI at 43% allows $3,440 total monthly debt. Subtracting existing debts leaves $2,740 for housing costs.

Down Payment Options and Strategies

The down payment represents the largest upfront cost for first home buyers. Contrary to popular belief, 20% down is not always required in 2026.

Low Down Payment Loan Programs

Multiple loan types accommodate limited cash reserves:

- Conventional 97 (3% down): Available to qualified first home buyers with credit scores of 620+

- FHA loans (3.5% down): More flexible credit requirements, ideal for scores between 580-679

- VA loans (0% down): Exclusive to eligible veterans and active military, no down payment required

- USDA loans (0% down): Available for properties in eligible rural areas outside core Seattle

A Seattle first-time buyer purchasing a $650,000 home with 3% down needs $19,500 plus closing costs, significantly less than the $130,000 required for 20% down.

Private Mortgage Insurance (PMI)

When putting down less than 20%, conventional loans require PMI, which protects the lender if you default. This typically costs 0.3% to 1.5% of the loan amount annually.

On a $630,500 loan (97% of $650,000), PMI might run $150-$300 monthly. However, PMI automatically cancels once you reach 22% equity through payments or appreciation. In Seattle's historically appreciating market, many buyers achieve this milestone within 3-5 years.

FHA loans require mortgage insurance premiums (MIP) for the loan's life if you put down less than 10%, making refinancing to conventional an important future strategy.

Down Payment Assistance Programs

Washington State and local jurisdictions offer several assistance programs. The Washington State Housing Finance Commission provides down payment assistance up to $100,000 in some programs, though income limits apply.

King County's Home Advantage program offers deferred-payment second loans covering a portion of down payment and closing costs. These programs particularly benefit buyers in Lake Forest Park or Everett, where median prices remain slightly below Seattle proper.

Research first-time home buyer programs by state to identify options specific to your income level and target neighborhood. Many programs define "first-time buyer" as anyone who hasn't owned a home in the past three years, expanding eligibility beyond truly first-time purchasers.

Mortgage Loan Types for First Home Buyers

Selecting the right mortgage product impacts your monthly payment, qualification requirements, and long-term costs.

Conventional Loans

Conventional loans, not backed by government agencies, dominate the Seattle market. They offer competitive rates for borrowers with strong credit and stable income.

Conventional loans with 5% down provide a middle ground between minimum down payment options and the 20% threshold. This approach reduces PMI costs while keeping cash reserves available for furniture, repairs, or emergencies.

Conventional loan advantages:

- Lower overall costs compared to FHA for well-qualified buyers

- PMI cancellation option once reaching 20% equity

- Higher loan limits (up to $1,149,825 in King County for 2026)

- More property type flexibility

FHA Loans

Federal Housing Administration loans prioritize accessibility over premium pricing. These government-backed mortgages accept lower credit scores and smaller down payments.

For a Shoreline buyer with a 600 credit score and limited savings, FHA often represents the most realistic path to homeownership. The trade-off comes through higher insurance costs and more stringent property condition requirements.

FHA loans work well for condominiums if the building maintains FHA approval. Before making offers on Seattle condos, verify the complex's FHA certification status.

VA and USDA Loans

Veterans and active military personnel gain significant advantages through VA financing. Zero down payment, no PMI, and competitive interest rates make this program exceptionally valuable for eligible first home buyers.

USDA loans serve suburban and rural areas, though very little of core Seattle qualifies. Parts of Mill Creek or areas north of Everett may qualify, offering 0% down for moderate-income buyers.

Pre-Approval and the Application Process

Securing mortgage pre-approval before house hunting provides crucial advantages in Seattle's competitive environment.

Pre-Qualification vs. Pre-Approval

Pre-qualification offers a rough estimate based on self-reported information. This quick assessment takes minutes but carries minimal weight with sellers.

Pre-approval involves full credit verification, income documentation review, and underwriter evaluation. This comprehensive process typically completes within 1-2 business days and demonstrates serious buyer intent.

In markets like Bellevue or Redmond, sellers often receive multiple offers. Pre-approved buyers present less transaction risk, increasing acceptance likelihood even with slightly lower offer prices.

Documentation Requirements

Gathering paperwork upfront streamlines the pre-approval process. First home buyers should prepare:

- Two years of W-2s and tax returns

- Recent pay stubs (30-60 days)

- Two months of bank statements for all accounts

- Employment verification contact information

- Photo identification

- Rental payment history (if available)

Tech employees at Google or Microsoft with equity compensation require additional documentation. RSUs, stock options, and annual bonuses can significantly boost buying power when properly documented. A first-time home buyer broker experienced with equity compensation maximizes qualification amounts by presenting these income sources effectively.

Navigating Seattle's Competitive Market

Market dynamics in the Greater Seattle area require first home buyers to adopt strategic approaches beyond basic qualification.

Offer Strategy and Escalation Clauses

When competing against multiple buyers, crafting a compelling offer involves more than price alone. Consider these elements:

Escalation clauses automatically increase your bid in preset increments up to a maximum ceiling when competing offers exist. On a $700,000 Lake Forest Park listing, you might offer $700,000 with $5,000 escalations up to $740,000. If the next highest offer reaches $720,000, yours automatically adjusts to $725,000.

Appraisal gap coverage demonstrates willingness to cover the difference if the home appraises below contract price. In appreciating markets, this protection reassures sellers concerned about deal collapse.

Flexible closing timelines accommodate seller needs, whether they require a quick 14-day close or need 60 days to locate their next home. Lenders capable of closing in as few as 9 business days provide significant competitive advantages.

Inspection Contingencies and Risk Management

While waiving inspection contingencies strengthens offers, first home buyers should carefully weigh this risk. Seattle's older housing stock in neighborhoods like Shoreline may harbor hidden issues requiring expensive repairs.

Consider these alternatives:

- Pre-inspection before making offers (costs $400-600 but provides valuable information)

- Shortened inspection periods (3-5 days instead of 10)

- Information-only inspections that allow review but limit withdrawal rights

Never waive financing contingencies, which protect your earnest money if loan approval fails. This safeguard remains essential regardless of pre-approval strength.

Understanding Total Monthly Costs

Purchase price represents only one component of homeownership expenses. First home buyers must budget for:

| Expense Category | Typical Monthly Cost | Notes |

|---|---|---|

| Principal & Interest | 65-75% of payment | Varies by rate and term |

| Property Taxes | $500-$900 | Based on assessed value |

| Homeowners Insurance | $100-$200 | Required by all lenders |

| HOA Fees | $200-$600 | Condos and some communities |

| PMI | $150-$300 | If down payment under 20% |

| Maintenance Reserve | $200-$400 | 1% of home value annually |

A $650,000 Lynnwood home with 5% down at 6.5% interest creates approximately:

- $3,280 principal and interest

- $680 property taxes

- $150 insurance

- $200 PMI

- $4,310 total monthly housing cost

Add utilities, maintenance, and potential HOA fees to determine true affordability. Many first-time home buyer programs include homeownership education covering these budgeting essentials.

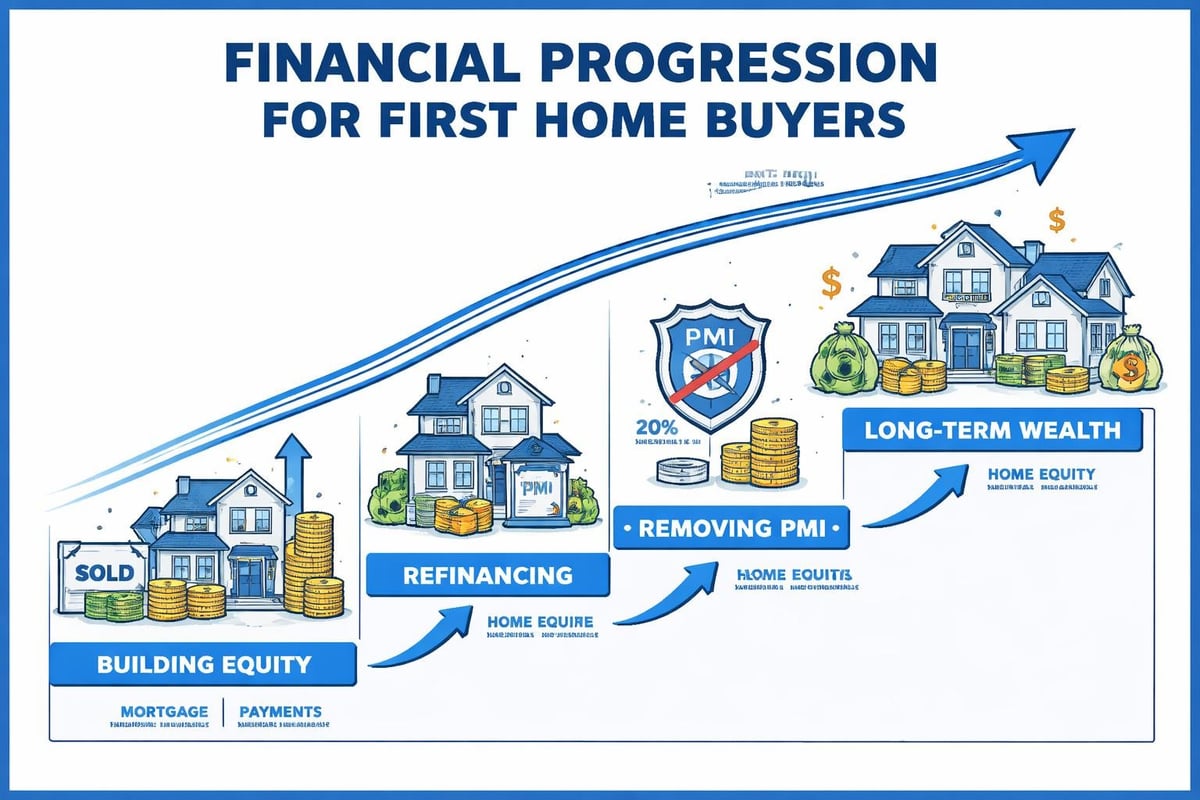

Long-Term Financial Planning

Homeownership extends well beyond closing day. First home buyers should consider multi-year financial strategies.

Refinancing Opportunities

Interest rates fluctuate based on economic conditions. If rates decrease 0.75% or more after your purchase, refinancing may reduce monthly payments or shorten loan terms.

Additionally, once reaching 20% equity, refinancing from FHA to conventional eliminates ongoing mortgage insurance premiums. For a buyer who purchased a Mill Creek home with FHA financing, property appreciation combined with principal paydown might enable this strategy within 3-4 years.

Building Equity Strategically

Equity accumulates through two mechanisms: principal reduction and appreciation.

Principal reduction happens automatically with each payment. Standard 30-year amortization means early payments heavily favor interest, but principal portions steadily increase.

Appreciation depends on market conditions. Seattle-area homes appreciated approximately 8-12% annually from 2020-2023, though future rates remain uncertain. Even modest 3-4% annual appreciation builds substantial equity over time.

Making additional principal payments accelerates equity building. An extra $200 monthly on a $630,000 loan saves over $100,000 in interest and shortens the loan by nearly 7 years.

Tax Advantages of Homeownership

First home buyers gain several tax benefits:

- Mortgage interest deduction on loans up to $750,000

- Property tax deduction (subject to SALT cap)

- No capital gains tax on first $250,000 ($500,000 married) of profit when selling

Consult tax professionals to maximize these advantages within your specific financial situation. Benefits prove particularly valuable for higher-income tech employees in Redmond or Bellevue facing substantial federal tax obligations.

Common Mistakes to Avoid

Learning from others' missteps helps first home buyers navigate the process more smoothly.

Overextending Your Budget

Qualification amount and comfortable payment differ significantly. Lenders approve based on maximum allowable DTI ratios, but life involves more than housing costs.

Account for career changes, family planning, vehicle replacement, healthcare costs, and retirement savings. A payment consuming 40% of gross income leaves little cushion for unexpected expenses or lifestyle preferences.

Neglecting Future Resale Considerations

While purchasing your forever home sounds romantic, statistics show most first home buyers sell within 7-10 years. Consider resale factors even if you plan to stay longer:

- School district quality (impacts values even for buyers without children)

- Proximity to employment centers and transportation

- Neighborhood trajectory and development plans

- Property layout appeal to broad buyer pools

A quirky layout you find charming might limit your buyer pool when selling. Balance personal preferences with mainstream appeal.

Skipping Professional Guidance

Navigating a tough housing market requires experienced guidance. Working with knowledgeable professionals-mortgage brokers, real estate agents, and home inspectors-pays dividends through avoided mistakes and optimized outcomes.

Mortgage brokers access multiple lenders, shopping rates and programs on your behalf. This proves especially valuable for first home buyers with unique situations like equity compensation, self-employment income, or credit challenges.

Special Considerations for Seattle Tech Employees

The concentration of major technology employers creates unique opportunities and challenges for first home buyers in the Seattle area.

Qualifying Equity Compensation

Amazon, Microsoft, and Google employees often receive significant stock-based compensation. Traditional underwriting approaches struggle with these variable income sources, but specialized expertise enables proper qualification.

RSUs (Restricted Stock Units) require two-year vesting history for most programs. Lenders average the vested amount received over 24 months, then apply a percentage (typically 70-90%) for qualifying purposes.

Stock options follow similar patterns but require additional analysis around exercise timing and taxation.

Annual bonuses qualify when demonstrated over two consecutive years with reasonable consistency expectations.

A Redmond-based Microsoft employee earning $150,000 base salary plus $80,000 annual RSUs might qualify using $206,000 income ($150,000 + $56,000 averaged RSU at 70%). This dramatically increases purchasing power compared to base salary alone.

Jumbo Loan Considerations

Seattle's high property values frequently exceed conforming loan limits of $1,149,825. Jumbo loans require:

- Higher credit scores (typically 700+)

- Lower DTI ratios (usually 43% maximum)

- Larger reserves (6-12 months payments in savings)

- More extensive documentation

Despite stricter requirements, jumbo rates in 2026 often approximate conforming rates for well-qualified borrowers. Tech employees with strong incomes and substantial equity compensation frequently navigate jumbo financing successfully.

Relocation Considerations

Many Seattle tech employees relocate from other states or countries. First home buyers new to the area face additional complexity around establishing local credit, understanding neighborhood dynamics, and timing purchases with job start dates.

Rental history from previous locations helps establish payment reliability. International buyers may need alternative credit documentation and larger down payments depending on visa status and employment authorization.

Timeline and Process Overview

Understanding the typical purchase timeline helps first home buyers plan effectively.

Phase 1: Preparation (2-6 months)

- Review and improve credit scores

- Save for down payment and closing costs

- Research neighborhoods and price ranges

- Interview and select mortgage broker and real estate agent

- Obtain pre-approval

Phase 2: House Hunting (1-4 months)

- Attend open houses and private showings

- Refine criteria based on available inventory

- Monitor new listings in target areas

- Submit offers when finding suitable properties

Phase 3: Under Contract (30-45 days)

Days 1-10:

- Execute purchase agreement

- Submit earnest money

- Complete home inspection

- Finalize loan application

Days 11-25:

- Complete appraisal

- Submit additional documentation to lender

- Review title report and HOA documents

- Resolve any inspection or appraisal issues

Days 26-45:

- Obtain final loan approval

- Conduct final walkthrough

- Schedule closing appointment

- Attend closing and receive keys

In competitive Seattle markets, experienced lenders expedite this timeline significantly. Some transactions close in 14-21 days when all parties prioritize speed and efficiency.

Working with the Right Mortgage Professional

First home buyers benefit enormously from selecting an experienced, responsive mortgage broker who understands local market dynamics.

Questions to Ask Potential Brokers

Evaluate mortgage professionals using these criteria:

Experience and specialization: How many first home buyers have you helped in the past year? What percentage of your business serves the Seattle area?

Communication style: What's your typical response time? How do you keep clients updated throughout the process?

Lender relationships: How many lenders do you work with? Can you access specialty programs for unique situations?

Technology and efficiency: Do you offer digital application and document upload? What's your average timeline from application to closing?

Reviews and reputation: Can you provide references from recent clients? What do online reviews indicate about your service quality?

Value Beyond Rate Shopping

While interest rates matter, they represent only one component of total value. Consider:

- Ability to close quickly in competitive situations

- Expertise with complex income situations

- Responsiveness during evenings and weekends

- Problem-solving skills when challenges arise

- Educational approach that builds your understanding

A broker charging slightly higher fees but securing your dream home through superior execution and guidance delivers far greater value than the lowest rate from an unresponsive lender who costs you the property.

Resources for Continued Learning

First home buyers should leverage multiple information sources throughout their journey.

Educational programs through HUD-approved counselors provide comprehensive guidance on the home-buying process, often required for certain assistance programs.

State-specific resources like the Washington State Housing Finance Commission detail available programs, income limits, and application procedures.

Online calculators help model different scenarios: down payment percentages, interest rate impacts, and total cost comparisons. However, personalized analysis from qualified professionals accounts for nuances calculators miss.

Local market reports from real estate associations provide data on inventory levels, price trends, and days-on-market statistics across Seattle neighborhoods. This information helps time purchases and set realistic expectations.

Consider attending first-time buyer seminars offered by lenders, real estate brokerages, and community organizations. These events answer common questions and connect you with service providers.

The path to homeownership requires substantial research, planning, and execution, but thousands of first home buyers successfully navigate the process each year in Seattle, Bellevue, Lynnwood, and surrounding communities.

Successfully purchasing your first home in the Seattle area requires thorough preparation, strategic planning, and experienced guidance throughout the qualification and closing process. Understanding loan options, assistance programs, and local market dynamics positions you to make confident decisions aligned with your financial goals. Keith Akada brings 25+ years of mortgage experience helping first home buyers navigate complex scenarios, from qualifying equity compensation for tech employees to expediting closings in competitive markets. With 750+ five-star reviews and deep Seattle-area expertise, he provides the education, transparency, and strategic execution needed for successful homeownership. Start your journey today with Mortgage Reel and discover how personalized guidance transforms the home-buying experience.